Our Drunken Sailors are in No Mood to slow down. Massive waves of migrants also boost retail sales.

By Wolf Richter for WOLF STREET.

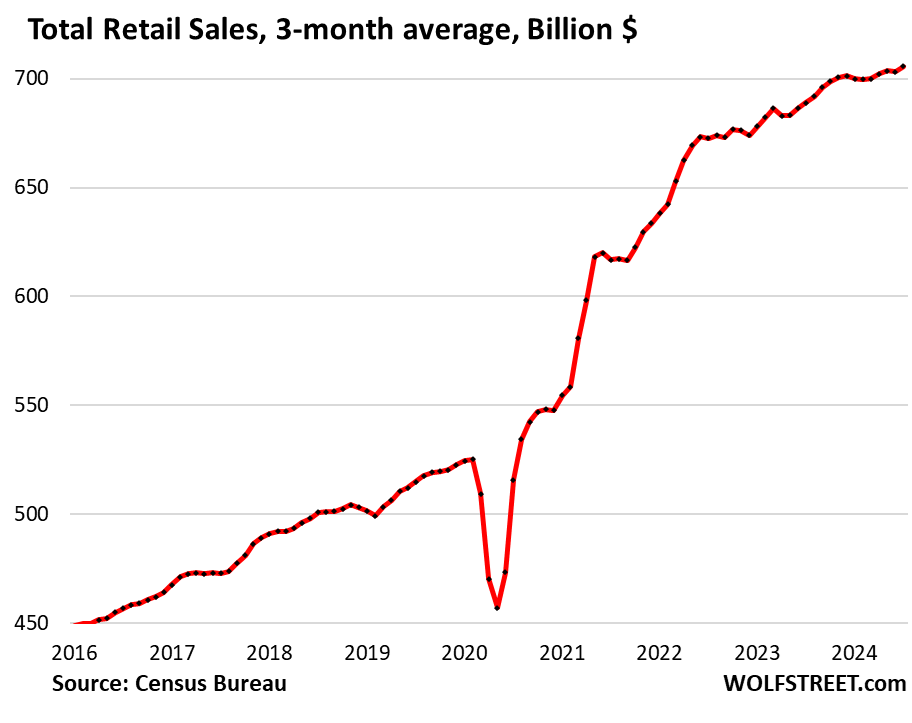

Our Drunken Sailors, as we lovingly and facetiously have been calling them for over a year, the pillars of the US economy, are still at it, splurging at retailers. Retail sales jumped by 1.0% in July from June, seasonally adjusted, the biggest month-to-month increase since January 2023. Year-over-year, not seasonally adjusted, retail sales rose 4.0%, to $724 billion.

To see the trend beyond the month-to-month squiggles, we look at the three-month average, which includes all revisions. It rose by 0.3% in July from June, and was up 2.4% year-over-year.

The big winner was ecommerce – the second largest category, behind auto dealers, with 17% of total retail sales: The three-month average jumped 1.0% in July from June and was up 7.4% year-over-year! That’s where much of the growth in retail sales is. Ecommerce sales are on track to surpass auto dealers in a year or two.

Big price drops in goods make these retail sales even stronger.

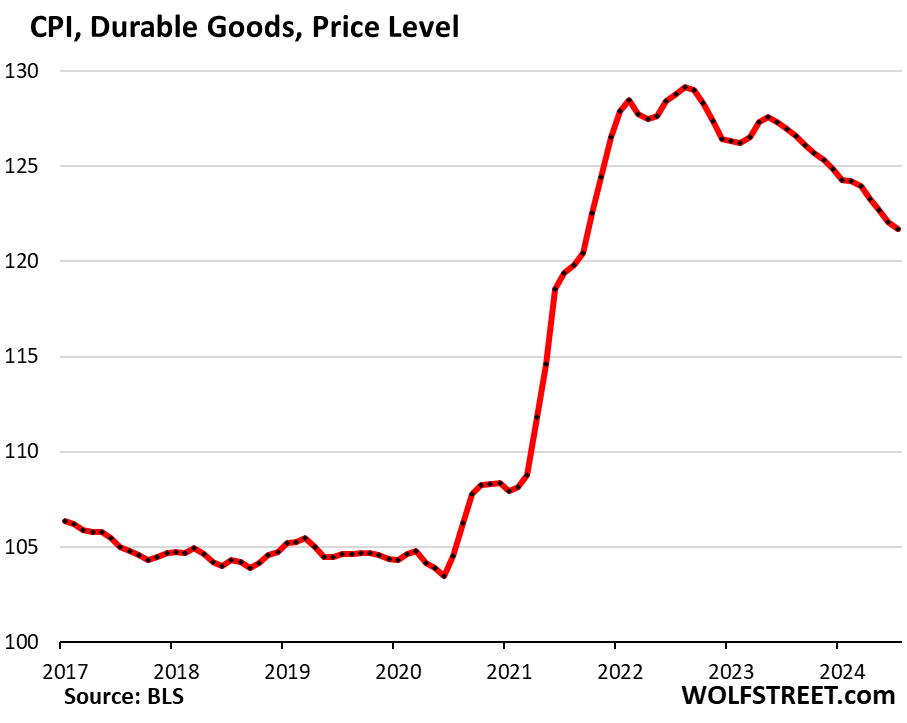

In the chart above, the steep increases in retail sales in 2021 and 2022 were caused by massive price increases in the goods that retailers sell, including new and used vehicles which account for 19% of total retail sales.

These price spikes started to unwind in late 2022, with prices spiraling lower in many categories. Food is one of the exceptions. Gasoline prices plunged. Prices of durable goods, including motor vehicles, are in a historic downward spiral from the crazy spike during the pandemic. The CPI for durable goods has dropped by 6% from the peak two years ago. Prices for used vehicles have plunged by 19%. New vehicle prices have dropped 2%. Consumer electronics, appliances, furniture, sporting goods, etc. have all seen price drops.

Adjusted for these price declines in goods – so, on an inflation-adjusted basis – retail sales look even better. Those price declines should have pushed down retail dollar-sales. But dollar sales rose despite the price declines, as retailers sold more merchandise at lower prices.

And this will show in the inflation-adjusted consumer spending and GDP data. This type of retail sales growth, despite declining prices, supports solid GDP growth.

Sales at the largest categories of retailers.

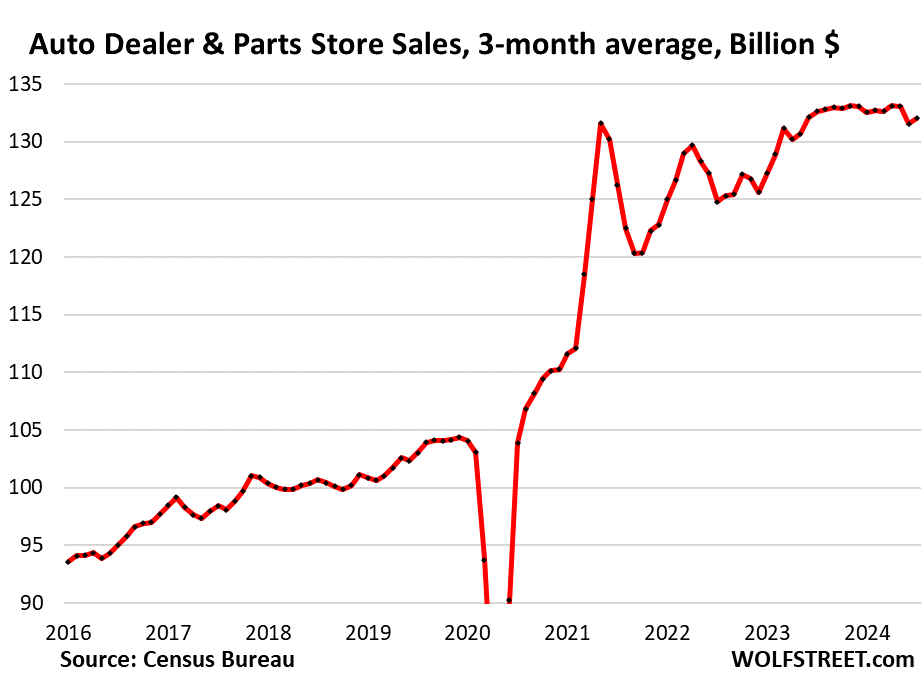

Sales at new and used vehicle dealers and parts stores, the largest category with 19% of total retail sales, bounced back partially in July from the chaos in June following the CDK hack that had put thousands of dealers on ice. And so the three-month average in July rose 0.4% from the beaten-down June level.

But the three-month averages of July and June – both of which include the steep effects of the June CDK hack – were down from May. The relatively flat dollar-sales for the past 18 months, despite rising retail unit sales, are due to dropping prices. All figures based on three-month averages, seasonally adjusted:

- Sales: $132 billion

- From prior month: +0.4%

- Year-over-year: -0.5%

The spike in dollar-sales in 2021 and 2022 was based on price gouging by dealers and automakers, even as unit sales volume plunged due to vehicle shortages. It’s these price gouges that have been getting unwound since mid-2023:

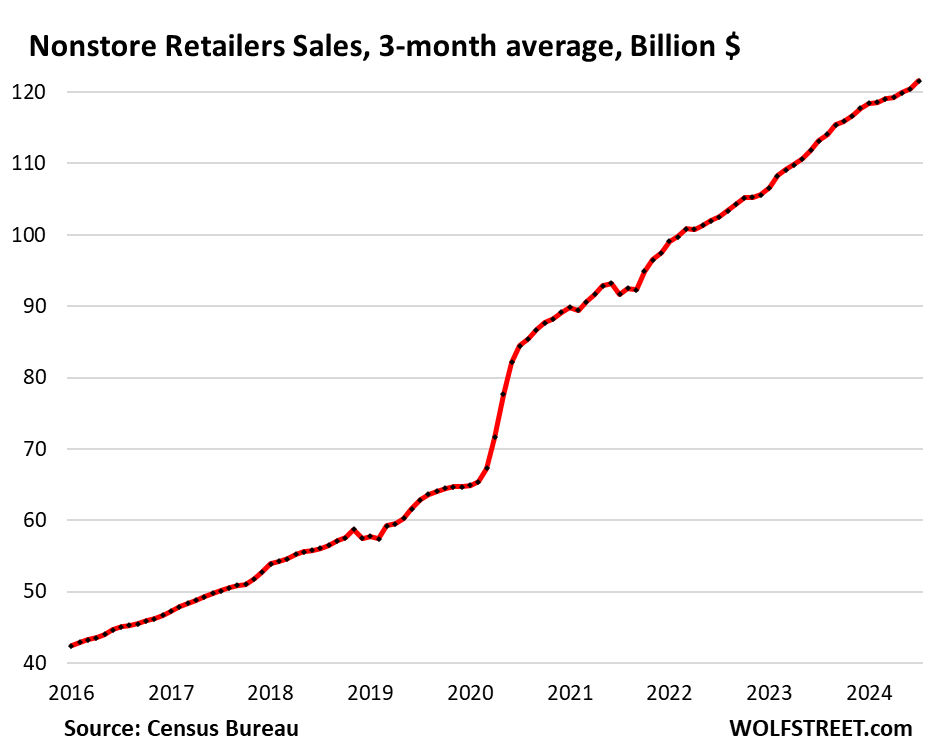

Ecommerce and other “nonstore retailers” (17% of total retail trade), includes ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets, three-month averages:

- Sales: $122 billion

- From prior month: +1.0%

- Year-over-year: +7.4%

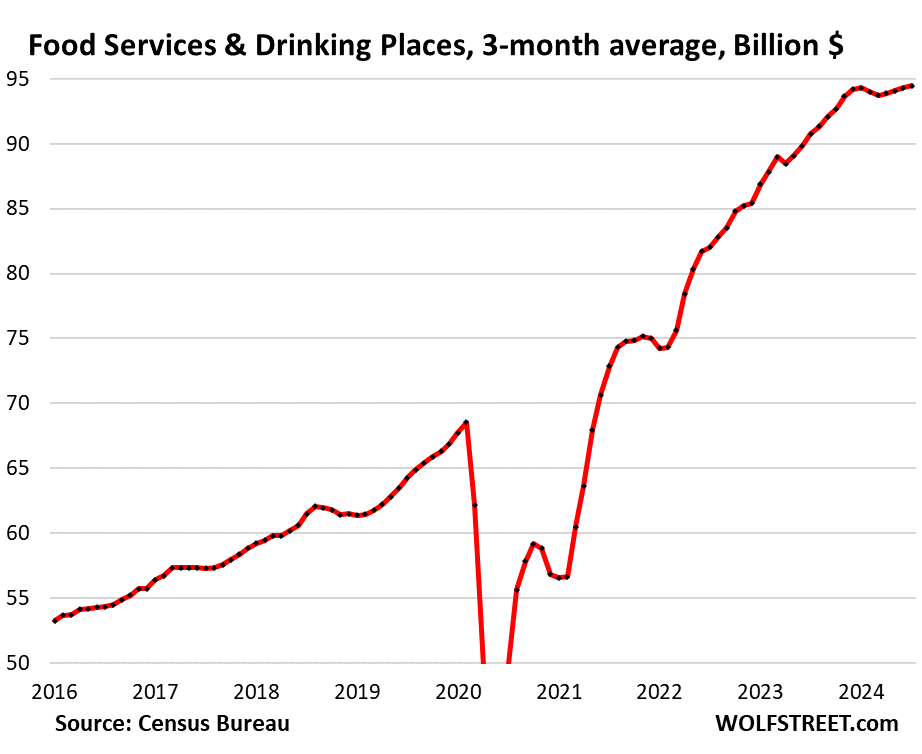

Food services and drinking places (the third-largest category, 13% of total retail), includes everything from cafeterias to restaurants and bars.

Sales have been essentially flat all year. But if you hold your tongue just right, you can see the slow-down earlier this year, and then slow growth out of the trough over the past four months:

- Sales: $95 billion

- From prior month: +0.2%

- Year-over-year: +4.1%

Food and Beverage Stores (12% of total retail). Generally, only price increases and population growth increase sales.

Prices have nearly flattened out at very high levels after spiking massively into early 2023. In July, the CPI for food at home was roughly flat with January and up just 1.1% from a year ago.

But the population has been surging: The Congressional Budget Office, using ICE and Census data, estimated that in 2022 and in 2023, the US population grew by 6 million people, nearly exclusively through the waves of migrants arriving. These people work (nonfarm employment rises), or are looking for work (pushing up the unemployment rate), and they’re buying stuff, including at food and beverage stores, thereby pushing up their retail sales, which is what we can see here (three-month averages):

- Sales: $83 billion

- From prior month: +0.4%

- Year-over-year: +2.3%

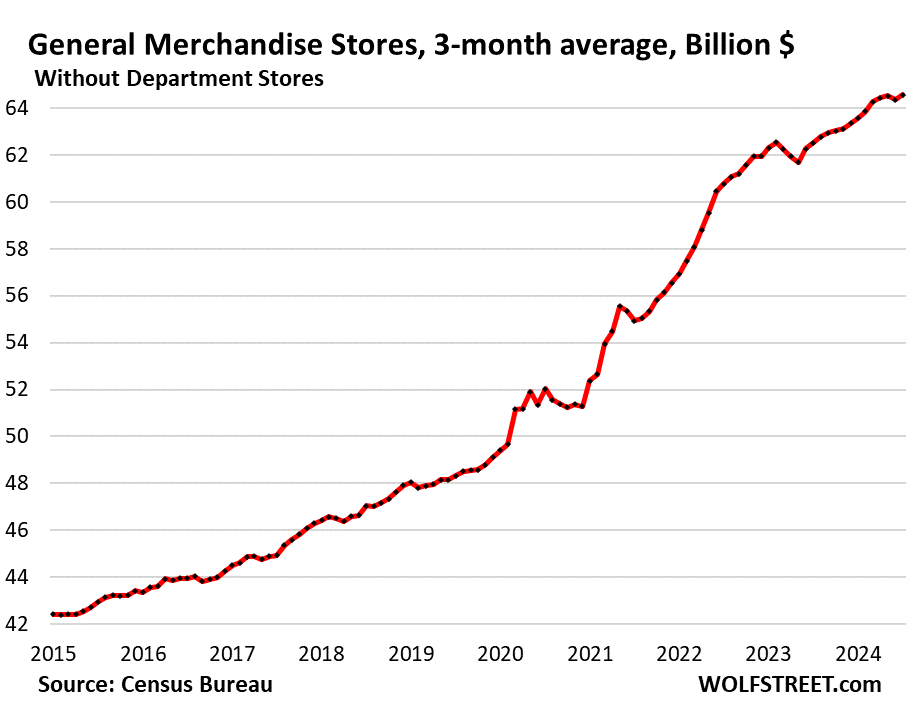

General merchandise stores, without department stores (9% of total retail). These stores are also places where the 6 million additional US population buy their essentials, such as groceries at Walmart, which announced price rollbacks on many items.

- Sales: $65 billion

- From prior month: +0.3%

- Year-over-year: +3.3%

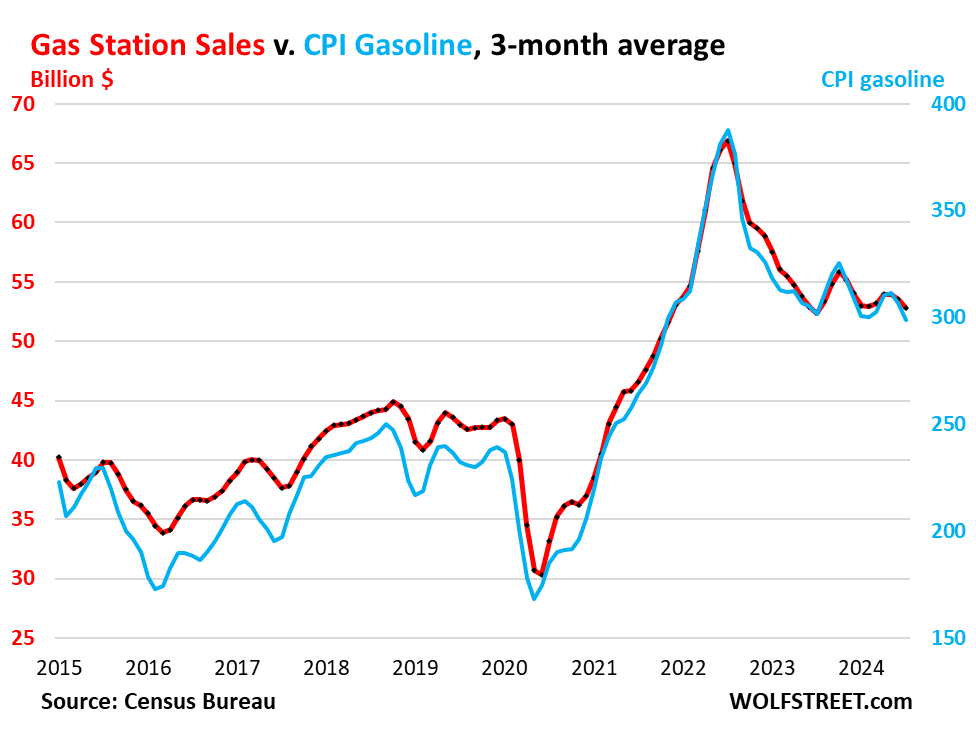

Gas stations (8% of total retail sales). Dollar-sales at gas stations move in near-lockstep with the price of gasoline. The price of gasoline plunged from the top of the spike in June 2022, but over the past 12 months has roughly stabilized:

- Sales: $53 billion

- From prior month: -1.3%

- Year-over-year: +0.9%

Sales in billions of dollars at gas stations, including other merchandise that gas stations sell (red, left axis); and the CPI for gasoline (blue, right axis):

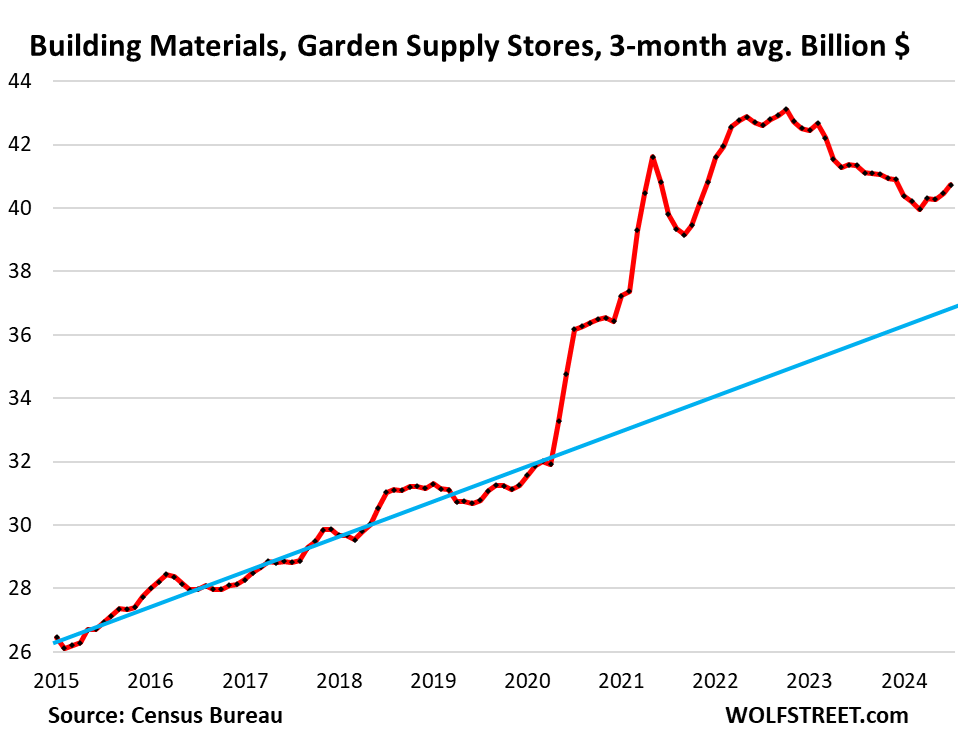

Building materials, garden supply and equipment stores (6% of total retail). The prepandemic trendline in blue. Home Depot was singing the blues about this the other day. The mindboggling remodeling boom started fizzling in late 2022.

- Sales: $41 billion

- From prior month: +0.6%%

- Year-over-year: -1.5%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

No rate cut needed in September! Good news

I totally agree, although market is now pricing in .25% cut vs .50% as 100% certain, some lunatics out there are still screaming deeper rate cuts now even after the last 4 days market action made the previous week another nothing burger, steam release valve event as predicted.

The real question is, will Pow Pow at least cut .25% in Sept? I hope I am dead wrong but I am betting he will especially since the latest round of inflation data will give him some cover to get away with it, well until it comes back again which is a real possibilities given how strong spending is..

If it does then I guess I’ll pour one for start of the demise to a decent return from risk free investment like Tbills….one rate cut, the return is good but if this is the trend…TINA we go again..

The median Federal Reserve policymaker thinks any rate above 2.6% restrains the economy over the longer term, once inflation has reached the 2% PCE target.

That means by their estimates, the “real” neutral federal funds rate is only +0.6% above PCE, or pretty much ZERO relative to CPI (which always tends to run at least 0.5% higher than PCE)

To be fair, their estimates have been ever-so-slowly shifting upwards in the last several SEPs, but they’re still laughably low & markets know that.

On the June dot plot, you see that:

4 FOMC members see the longer-run rate as 3.5% to 3.75%;

5 FOMC members see the longer-run rate as 3.0%-3.125%.

10 FOMC members see 2.75% and lower. The lowest sees 2.375%

And the upper end of the range has been creeping up in every dot plot.

The range in the June 2024 dot plot was 2.5-3.5%.

In March 2023, the range was 2.4-2.6%

In March 2022 (when the rate hikes started), the range was 2.3%-2.5%

So the top of the range has increases by a full percentage point since the rate hikes started. And this process may continue. At this pace, top of the range may be at 4.5% in two years.

There will be NO RATE CUT at all in 2024 prior to the November 2024 election as the Federal Reserve does not ever involve itself in political matters.

I’ll bet he won’t because he will not want to be accused of trying to influence the election, especially since there seems to be no compelling reason to cut. But ya pays yer money and ya takes yer choice about what will happen.

I’m not even sure which candidate a cut would help. :-)

It’s too late for a measly 0.25% cut in September to materially affect the economy before November’s elections. Rate moves take months to ripple through the economy.

Also, the current governing party hasn’t suffered any political pain or faced any electoral consequences for the recent inflation spike, because the mainstream media has diverted blame to external factors (supply chains, Ukraine, etc etc)

Canada already cut .25. Didn’t do much.

Rate cuts and QT?

What will lending look like without all the free flowing money available?

“waves of migrants arriving”

Usually, there are 3, 4, 5 or more working age persons living together. This means they’re collectively able to afford rent more than say a mom & dad only. So, they have more money left over for discretionary spending. Not a ton like the top 10% but usually more than the bottom 40% or so.

True.

Although MORE than the bottom 40% is NOT saying much about NET WEALTH……or even income.

Just like the tenement livers. Including those who worked 6 12hr days died or were maimed in Carnegie’s steel factories (1 in 11) during the gilded age when capitalism ran COMPLETELY amuck with little regulation or taxes. Not to mention child labor.

Will we play that sick game again? The Heritage (whose heritage?). Foundation is all for it plus just having NO Democracy at all.

Should say Capitalism AND Corporatism……The two together and unregulated or taxed is a HUGE EVIL…..

……..all words have can have definition problems…….BIG ONES.

Since retail sales are not inflation adjusted, were more units sold than comparison periods, or is inflation pushing this number higher? Thank you.

This is discussed in detail in the article.

Thanks WR for these reports.

Looks like consumers are doing great and splurging. Happy for them :-).

Or just paying more corporate profits for the regular items we all need.

Kroger admitted to the FTC today that it is price gouging Americans by well more than $1 billion per year and offered the FTC to cut price by $1 billion a year if the FTC allows their merger with Albertsons to go through so they can become the largest monopolist in the grocery business.

Alberstons near me is the same price as Walmart across the street. Cheaper on some items. Are all the grocery stores in on it?

I took it to mean the merger would give them cost savings to pass on. Their profit margins have been quite steady. They must hide it well…

Pass on savings to the consumer? BAHAHAHAHAHA!

Huh?

After the merger Kroger wont even be the largest grocer in the US in fact it will be less than half the market share of the largest = Walmart.

Sometimes people like you…….

The only reason retail sales are up at all is that massive price gouging has become prevalent in that arena and more and more people are just saying no to purchasing discretionary good at those prices.

MW Stock Market Today: S&P 500 and Nasdaq post best 6-day stretch since November 2022

Why adjust for inflation, which gets sliced and diced by the powers that be, when we could adjust for the M2 money supply, which actually shows how many dollars are in the system?

M-2 is a BS figure. It excludes lots of stuff, such as CDs over $100,000 (but it includes CDs of less than $100,000), cash in retirement accounts, etc. So if you cash in a $250,000 CD, M-2 jumps by $250,000. There are lots of weird things like that in M-2, to the point where it’s meaningless.

A growing economy with profitable economic activities automatically creates money as it grows. That’s what an economy does. That’s not the problem. The problem is the money that the Fed created artificially. So you can look on the Fed’s balance sheet to get that.

https://wolfstreet.com/2024/07/05/fed-balance-sheet-qt-34-billion-in-june-1-74-trillion-from-peak-to-7-22-trillion-lowest-since-november-2020/

Your saying M2 excludes things even though it grows much faster than CPI inflation, which I don’t understand. Wouldn’t that mean CPI inflation is excluding even more than M2?

If your open to adjusting by the Fed’s Total Assets, than I’m game.

Look at the Fed’s balance sheet chart. That’s what caused the growth of M-2. That Fed created this money that bubbled up M-2. That’s not a secret.

FRED M2 (DISCONTINUED)

From 1985 until 2020 M2 grew from $2 trillion to $20 trillion.

Starting on February 23, 2021, the H.6 statistical release is now published at a monthly frequency and contains only monthly average data needed to construct the monetary aggregates. Weekly average, non-seasonally adjusted data will continue to be made available, while weekly average, seasonally adjusted data will no longer be provided. For further information about the changes to the H.6 Statistical Release, see the announcements provided by the source.

Before May 2020, M2 consists of M1 plus (1) savings deposits (including money market deposit accounts); (2) small-denomination time deposits (time deposits in amounts of less than $100,000) less individual retirement account (IRA) and Keogh balances at depository institutions; and (3) balances in retail money market funds (MMFs) less IRA and Keogh balances at MMFs.

Beginning May 2020, M2 consists of M1 plus (1) small-denomination time deposits (time deposits in amounts of less than $100,000) less IRA and Keogh balances at depository institutions; and (2) balances in retail MMFs less IRA and Keogh balances at MMFs. Seasonally adjusted M2 is constructed by summing savings deposits (before May 2020), small-denomination time deposits, and retail MMFs, each seasonally adjusted separately, and adding this result to seasonally adjusted M1. For more information on the H.6 release changes and the regulatory amendment that led to the creation of the other liquid deposits component and its inclusion in the M1 monetary aggregate, see the H.6 announcements and Technical Q&As posted on December 17, 2020.

I am assuming you are an adult and are able to communicate your ideas with more than copy pastes from the FRED website.

The current M2 measure is located at this address:

fred.stlouisfed.org/series/WM2NS

BlueSky,

It’s a good idea to paste the explanation into the comments so people can actually read it. I normally don’t allow links, and if I allow them, people only click on clickbait links; practically no one clicks on the informative stuff, such as a description of M-2.

The Federal Reserve discarded M2 as being of any importance back at the end of 2021 exactly as stated.

Bluesky- last year the M2 dropped slightly, but prices paid by consumers rose steadily.

M2 is interesting to economics nerds. CPI is interesting to everyone who buys… anything.

grant – Because M2 spiked to 26% YoY in 2/2021 and the 4% YoY drop in 8/2023 was not enough to reverse the spike. M2 is still well above trend.

I don’t have the patience for this level of discussion. If you guys don’t want to use M2, more power to you.

Blue Sky,

I am VERY glad you don’t like this “level”, and I believe I have just learned a lot……retaining Econ info, is, for me, quite another thing. But if I keep at it……..

Like I leaned about links pretty quickly.

We are in the midst of a raging Everything Bubble which shows no signs of abating. In fact, it looks poised to tear higher in another parabolic move. The FED has destroyed pricing in the economy. They paused too soon, and now they will cut rates too soon, to fuel the bubbles even more. They are diabolical maniacs.

Good… Another reason I think they won’t cut.

I think they’re going to cut, to try to juice the market even more before the election. These people are, again, maniacs. They paused early, and will cut early, always to err on the side of wealthy speculators.

There were Citi analysts on CNBC today morning screaming for the Federal Reserve to cut by at least 1 to 1.5% over the coming months, or there’d be a severe recession. Remarkably they did so with a straight face after the retail sales report and all the other positive economic data released this week.

The S&P 500 has already clawed back all of last week’s losses and is now positive month-to-date. Since October 2023 and Powell’s pivot to talking about rate cuts, April 2024 (likely triggered by tax-related selling) has been the only negative month so far.

These analyst have no shame, here’s a good headline from them to front run the rate cut narrative and the return to promise land.

“Why Wells Fargo says investors may face a rerun of 1995 once the Fed cuts rates”

Tom Lee is not the only game in town when it comes to perma bull/pumper

It’s better to cut rates DURING A RECESSION, you know, when it’ll actually do some good.

That fuels public anger more than anything, and the problem is hard to undo by then. Exhibit A: the Fed raised rates DURING INFLATION, getting massive blowback about doing it too late (up to this day).

Still down for the month. Could you make some calls? 📞

Thanksss

Only a purple swan event can cause a recession at this point, with so much past QE liquidity, extra cash from rising wages and massive income from 5.0% returns on savings.

Black swans are already accounted for by quants and AI. It has to be really catastrophic, like a massive ????????

Black swan is so 2008…I think at this point we need a neon color radioactive swan to begin thinking the market will correct by any meaningful measure and major assets like RE to go anywhere near fundamentals value..

Another word, not holding my breath this will happen in my lifetime..

Excellent my house in Florida will be worth triple what it was worth last year and all you little sissy boys will be crying crying crying that you couldn’t see the forest through the trees.

🤣❤️

Enjoy that insurance bill.

Blame is not all on the FED. You need to lump in all the other G7 Central Banks. Lower for to long allowed for a lot of cheap money to flood the system and many Governments where the biggest borrowers. The FED lowered rates to help the economy but the Government jumped in and started borrowing and spending like a drunken sailor.

Government debt spending is inflationary. I am not pointing fingers at any president because the people who really control spending is congress. Only a few are concerned about spending. The rest need to promise free stuff to get elected. And many time the free stuff is not for the people but mostly benefits big businesses. Big businesses is really who congress tries to help…not the people.

What I am trying to say is that any law or bill that is designed to help the people of the US has big business lobbyist fingerprints all over it that is tied to some future campaign contribution.

I challenge anyone to show me a big money spending bill that does not have lobbyist fingerprints all over it.

VERY close to Impossible.

But there is always hope……

“Simultaneously our greatest strength and greatest weakness.”

– The Designer of The Matrix

Per Steph Pomboy on a Kitco interview today, retail sales peaked, in nominal terms, in mid 2021. More than 3 years ago. I don’t know if that is correct, but it sounds so to me.

But hey, I’m for anything that will keep the FED from cutting rates.

Goldbuggery bullshit. These morons are adjusting retail sales (sales of goods!!!) to the CPI dominated by services. These people are idiots wrapped in morons and topped off with nincompoops.

To adjust used-vehicle sales to inflation, you don’t use the rent CPI, but the used vehicle CPI.

Given that, the Fed is truly in a box – with services CPI being so sticky along with demographic problems that are only going to get worse, it’s fair to say IMO that we see a continuing trend of durable goods CPI plunging with services CPI that stays range-bound. Ironically, IMO, the Fed now has to decide which of its two mandates is more important. Cut and maintain ideal employment figures which will ignite durable goods CPI again, or hold to bring inflation to target via same DG CPI, while UE continues creeping higher.

Pomboy has been calling for recession and stock market crash for last 2 plus years.

She like Daniel Di Martino and others has been utterly wrong.

These folks have made lot of money by building their client base but they failed how things would unfold

They may be right one day but timing is everything

Their clients are losing money for sure.

Reminds me of the book – “Where are the Customer’s Yachts?”

All of them, of course, the customers paid for them didn’t they?

Cpn Obvious

Daniel is a Lacy Hunt protégé. Their economic theory is based on pre 2010 Federal reserve rules. Too much Government/corporate debt eventually leads to a recession. But Congress in 2010 or 2011 told the Federal Reserve they can create any program they want to help the economy or stave off a crisis without approval from congress. So the FED can move at light speed now. Prior to that they had to get most programs approved by congress.

I used to think these people and sadly a lot of their guests on Thoughtful money have some valuable and good information to share and maybe even sounding the right alarm before MSM…

Unfortunately, they have prove time and time again, they are more in the camp of Meet Kevin than true expert that offer unbiased information…now if I watch, it’s strictly for a good meme and laugh and once a while tickle my own little confirmation bias..

Wolf,

Do you know if “sales” for new cars counts actual end customer sales, or does it merely count an inventory build due to transfer from manufacturer to dealership?

Mike Shedlock stated, “Motor vehicle sales are counted when shipped from the manufacturer to the dealer no matter how long the cars sit on the lots.”

These sales figures here (“retail sales”) are sales by RETAILERS, reported by RETAILERS, so by dealers — what dealers reported as sales to their retail customers. This has nothing to do with automakers. Mish is wrong about that.

But on their financial statements, which are irrelevant here, automakers report revenues based on when they invoice the vehicle, which occurs well before the dealer gets the vehicle. That’s what Mish was referring to. But he’s confused. That’s not retail sales. Automakers call these sales “wholesales” because they sell to dealers, not to consumers (except for Tesla and some other EV startups that sell direct), and these sales by automakers to their dealers count as wholesales in the wholesale data, and not in the retail data here, and has nothing to do with the retail data.

Hopefully, he reads your comment sections. :-) He just repeated the statement in a second article about retail sales, but referring to GDPNow there, where given what you just said, I think his statement is more accurate.

Mish is wrong about a lot of stuff. And he looks a LOT older than the picture he uses.

What the heck

Car sales by volume peaked in 2016 at 17.5 million units. They have been on a downward trend since then. The reason car makers are making these gigantic profits and paying their executives exhorbitant compensation packages are the price of new cars, which have gone up enormously in price since 2016.

Yes. That’s why I love what Tesla has done. It has barged in on the self-satisfied oligopoly with price cuts, with actual price cuts of the sticker price, and big ones too. We need to see more of that. The legacy automakers need to be kicked in the nuts by competition. And then, as prices come down, maybe new vehicle sales will increase again.

Chart below shows total new vehicle sales (retail and fleet) by volume through 2023. So far, 2024 is tracking higher than 2023, but still well below 2019 (the linked article also includes sales charts by automaker, very revealing – ugly charts for US legacy automakers. But sales by some other automakers have zoomed to new highs.

https://wolfstreet.com/2024/01/04/ugly-charts-of-auto-sales-by-gm-toyota-ford-stellantis-oh-my-got-crushed-by-hyundai-kias-record-sales-tesla-has-arrived/

Wolf,

I sense from reading all your latest articles that you are trying to prepare us for the distinct possibility that the Fed will not cut in Sep. Or even if they do, it won’t be many cuts for a long while. Between today’s post showing a robust economy and the very interesting post on 8/13 about the inflation numbers from 12 months ago foreshadowing higher inflation numbers for the next few months based on comps, I’m now less worried about a recession and a lot more worried the market will have a temper tantrum when they don’t get all these predicted cuts. I’m sure your readers would welcome your thoughts.

I have said this many times: The Fed will cut someday, unless inflation gets a lot worse. But in September?

Inflation has come down a lot, and the Fed’s policy rates, at 5.5%, are well above all major inflation measures. So it CAN cut. There is room to cut.

But for now, the Fed doesn’t NEED to cut. There is no rush to cut: The economy is doing well, the labor market (check today’s initial claims!) is doing well, though jobs growth can no longer absorb the entire massive waves of migrants entering the labor market, so the unemployment rate, while still low, has ticked up — but it ticked up with jobs growing, not because of layoffs.

And there are lots of reasons for the Fed NOT to cut, including the possibility that inflation will re-surge if the Fed cuts. Powell and others have discussed this issue, and it scares them. The scenario where they cut a couple of times, and then have to hike three times is not good. So they’re trying to stay away from cutting prematurely. They might also want to stay out of the political quagmire.

But there is HUGE pressure from Wall Street and their goons in the media, and from the chieftains of Corporate America on the Fed to cut, and the Fed, with inflation where it is, is losing its political cover to hold rates in place.

So there is a possibility that the Fed will cut in September, but I think it’s far from a certainty. I think there is a good chance that the Fed will not cut in September.

The Treasury market has been dialing back the rate-cut expectations as well. The 4-month yield is still at 5.33%. The 6-month yield has come up a little. It still sees a rate cut in September, but with less certainty. The 1-year yield, which looks at rate cuts this year and into next year, has risen about 20 basis points since Aug 2, to 4.52%. So it has taken one rate cut off the table between now and next summer.

Fuggit. Let these clowns cut 75 basis points and let’s sit back and watch more of their carnage.

I said the same thing in a comment a few weeks ago about cutting in July. I’m pretty darn sure a first cut in July would have reignited inflation within six months of that cut. It would have been a Fed put on lifestyle choices, meaning it would have been a clear signal to wage earnerd that the Fed was endorsing people living above their means. That’s what happens when you cut on the cusp right before even the sightest bit of pain.

Couldn’t one argue that bernanke’s inverted inflation numbers for 10+ years paired with the opening the floodgates of tax cuts in 2017 sort of had more of an effect on inflation than the pandemic funds?

Or all together they made the perfect storm?

The “Perfect Storm” won’t be found in econ textbooks or history or investing to avoid it.

The FN elephants WILL SOON REFUSE to be ignored…….”Excessive Lifestyles” meet fossil fuel caused CLIMATE CHANGE…..you all have no idea what “inflation is…..

Enjoy that big pile and everything it bought you…”you earned it”……the poor FN kids didn’t…and you call them LAZY/

The SHEER STUPIDITY AMAZES ME……blather on, buy another rental….

Growth for the sake of growth is the ideology of a cancer cell.

Sorry……rearranging deck chairs or planning the evening meal will only earn you the curses of the recipients of your “lifestyles” when you are dead and DON’T CARE!

My back hurts and I have to save pills for bank, shopping, and misc, before refills 23…..IF they don’t give me “day early” shit….they tend to ignore 31 day months, which is most of them. The want to keep their jobs. I don’t blame my doc for putting his career before my pain….thank the FUCKIG SACKLERS and all others of their ilk. And kids AND ADULTS CHOOSE to take their chances with fentanyl…why?

Please delete ALL of my lack or cordiality and econ speak, even if it’s ALL TRUE.

At least I’m not on the street or in a hospice…..and never will be.

Crap!….I expected deletion…..and instead got exposed as an old whiner…..many are worse off than me…so no excuses.. have been hard on whiners myself here…..said F it……took pain pills, and will run out before 23…..hate to do it, but maybe will take sister up on offers to shop and then pick up pills on 23rd….no pain if I just stay in bed.

Want to stay with this blog at least till Wolf is FORCED to incorporate effects of climate change and possibly the worst case election results, into his econ notions and backup data. Sure trying hard to avoid it….I think it’s to please most of his generally guiltless wealthy followers. (top 10% = “wealthy”).

Wonder if this will be deleted?

A good summary of your thoughts, thanks Wolf.

And I think next week at Jackson Hole, Powell will be giving hints on what he’ll do at the September meeting.

FWIW, I think there is far too much speculation in the risk markets , a Fed cut could accelerate wildness and that should be a part of the deliberations at the Fed. I hope they sit still.

“… what he’ll do at the September meeting.”

It’s not “he’ll do.” There are 12 voting FOMC members. And they will vote. And they’re very protective of their power. They will not be preempted. Powell has been trying to build consensus for the decisions. There were a few dissents in 2022. Since then, the decisions have been unanimous. But the consensus was strained at the July meeting when all voted for no cut, unanimously, but one said afterwards that he’d preferred a cut. There is a good chance that in September, we get “no cut” with some dissenters voting for a cut.

So Powell cannot say what will happen at the September meeting because it’s not his decision. And they haven’t voted yet. He cannot and won’t preempt the other 11 voting members. He’ll stick to the big “IF inflation continues to” and “IF the labor market” generalities.

People can then interpret whatever he says however they want to. And they will, as we have seen over the past two years of incessant “Powell was dovish.”

Thanks, Wolf. I appreciate the insight and candor here.

I don’t think there is a better summary on the internet. Thanks.

“They might also want to stay out of the political quagmire.”

YUP!

At the current moment there is never even a mention of the Fed by the political talking heads on the various news networks. If they change rates even by a tiny bit in September then the Fed will be front -and-center of those nightly discussions all the way to the election.

“Which candidate does it benefit?”

“Why did they do that?”

“What does this mean about the economy and the election going forward?”

The questions and debates just write themselves. At the moment the Fed is right where they want to be… in the background of a contentious election year. All they want is to get past their meeting in September and they can stay in their snug little niche until after the election… and then do whatever the heck they want. It is going to take an awful lot more than last week’s various economic data to get them to give up the safety and security of that niche.

All this talk about Fed not intervening in election years but since 1980 the Fed has hiked or cut rates in every election year except 2012. It’s a nothing burger except to a very certain someone with a very certain base of supporters that are making an issue of it.

Matt,

LOL. I’ll just address your election-year BS, and let you stew by yourself in your other BS:

Over the past 24 years, there were 3 rate-hike cycles: the current one (Mar 2022 – Jul 2023) plus 2015-2018 plus 2004-2006.

Last time the Fed hiked during an election year was in 2016, when it hiked in December, after the November election. The prior hike was in December 2015. Specifically to avoid making a hike-decision before the election.

In the rate-hike cycle before then, in 2004-2006, the Fed hiked during an election year, but it went on a mechanistic path in June 2004 through July 2006, hiking 25 basis points at EVERY meeting without fail for two years, starting well before the election and lasting well after the election. The path was signaled in advance, and each meeting had a predetermined boring outcome until close to the end, when uncertainty started creeping in as to how far it would go. This mechanistic path was done SPECIFICALLY to avoid the political quagmire.

So that’s the practice going back two decades.

Changing the rate-path two months before the election, in a key meeting that everyone is watching like a hawk, with political accusations swirling all around, and with pre-election rate cuts even coming up in campaign rhetoric (Trump) is a very different ballgame. This is a delicate situation for the Fed. And it has come up in the recent press conferences. The Fed may still cut in September, but the issue is not a “nothingburger.”

That’s interesting. I got this data from JP Morgan. To me it’s a nothing burger. I just don’t really care if the fed cuts in Sept or stays the same or raises.

I sort of agree that the political angle is silly, at least smart people should see it that way. The media and some politicians portray it as momentum: the Fed has been holding steady, so if they suddenly cut it must be a political move. In reality, Fed has been making a data driven decision each meeting, so if they fail to make the obvious data driven decision in September, THAT’S the political move. And we don’t even know what that move is yet. So the Fed members should vote they way they believe it’s right based on the data, otherwise they’re being political. The media will scream foul one way or the other, just like they always do, and the Fed should laugh it off.

“But there is HUGE pressure from Wall Street and their goons in the media, and from the chieftains of Corporate America on the Fed to cut, and the Fed, with inflation where it is, is losing its political cover to hold rates in place.”

Why does the Fed care what these people think?

Honest question – it’s not like these corporate goons have any power over over the Fed. Why can’t Powell just tell them to pound sand? It’s not like they’re showing up at the Eccles building with torches and pitchforks.

Inflation might be dropping because the bottom 50% has run out of money and credit. The top 50% might still be spending away. The Fed has created a two-faced economy with its trickle down, wealth effect policies.

Does this mean the Fed will reduce rates, recreating that chase for yield and further concentrating wealth?

Fed policies make it tough for the working class to get ahead. Home ownership is already out of reach in many locations.

The Federal Reserve has nothing to do at all with housing prices.

Lol, lmao, etc.

Lol!!!

SCBD, you usually have solid comments. This one, not so much.

So the massive home price spike from 2021 to 2023 has nothing to do with the Fed buying MBS and pushing 10 year treasuries lower with QT?

OMG, how ignorant.

If the Fed has “nothing to do with housing prices” then why did they have to buy all those MBS is the first place?

Why don’t they sell them all immediately?

What a disingenuous and ignorant statement, not to mention the influence of buying treasuries and the influence of the ten year yield on all kinds of credit markets. You must be in real estate.

“The Federal Reserve has nothing to do at all with housing prices.”

Guaranteed replies…

The bottom 50% is nowhere near a situation where they run out of credit. Considering credit cards alone, Wolf’s chart on credit card balances vs limits makes that clear. And now, with the new HELOC loans from Freddie (soon to be followed by all the GSEs)? The party for available credit lines is just getting started!

The bottom 50% have virtually no assets.

Since about 1/3 of all households are renters, at least 15% of the bottom 50% own homes (about a third of the bottom 50%). I’m betting more than 2/3 of the bottom 50% own cars. I’m betting most of the bottom 50% have some form of credit account.

That has been true of 100 years. That is probably not a new thing. Well, now that I think about it more….it probably used to be the bottom 30% and it has risen to 50%.

But I remember in my twenties I had no assets. I slowly grew my assets over time.

A huge issue in the US economy is what do we use to measure money. The US banking system only consists of around 7,000 or fewer banks with only around $22 trillion in assets. Then there are the stock and bond markets which are said to have around $60 trillion in asset value. Then there are real estate markets with around $20 trillion in value. Then there are the financial service non-bank companies such as life insurers and others with an untold amount of funds. What is the real total amount of money we are really dealing with in the US economy? The Federal Reserve by contrast only controls around $7 trillion in assets so what is its real influence these days on anything?

The Fed has a lot of regulatory levers it stopped pulling, long ago. Those levers have a gargantuan impact.

Have you ever heard of Paul Volcker? He, eventually, shut down the economy. Does that count? The Fed controls the banking (credit) system, usually. Sometimes it doesn’t control the banking system, and we know what that looks like.

SCBD said: “The Federal Reserve by contrast only controls around $7 trillion in assets so what is its real influence these days on anything?”

FWIW: $7Trillion is not nothing. The combined market cap of the S&P 500 companies is just under $46 trillion.

As other commenters have pointed out, it certainly plays a role in regulating the flow of money (credit), and obviously they have the ole’ “Control-P” money “printer” which is turned on at the first sign of panic.

They have a major role in overseeing the biggest economy in the world, and have a direct influence on most of the interest rates in this economy (and for that matter others to the extent they are in concert or competition).

They basically serve as the economic firefighters, spraying dollars or liquidity at anything they deem “bad” or “uncomfortable.”

Finally they have an important job in wagging the dog. They can create the programs that will consume and cap any contagion, from MBS to Corporate bonds (2020) or anything else that a rational market would rather flee from.

They can then package up the broken pieces and sell them to JPM or whoever’s the BFF at that time.

The economy and stock markets are bubble inflated by the 2.5 trillion$$$ annually borrowing and spending by the federal gvt! This is more stimulus than the height of QE. The EU mandates its countries to keep deficit spending to 2.5% of GDP. Well, Uncle Sam is borrowing and has been on a borrow and spending binge of 8 to 10% of GDP for over 4 years now. Currency crisis, market crashes and hyper inflation is inevitable. Watch out in 2025!

Good article as usual Wolf!

I am also wondering when the politicians will start talking about and be concerned about how, in a good economy, they are running trillions in deficit and what will happen in the case of a recession if, now when times are good, they are spending like this. I remember how Germany had a surplus when the economy was doing well. That’s real. This is fake growth that is not sustainable and there will be a serious reckoning soon or a later.

i’ll admit that i thought the u.s. federal spending was unsustainable when the 2008 american recovery and reinvestment act was passed, bringing the debt to $8 trillion or whatever, and here we are at $35 trillion, and people are still falling over themselves to buy 10 year treasuries at crap yields.

so clearly i was wrong about how long this can go on.

“so clearly i was wrong about how long this can go on.”

You are not the only one, but then again, Uncle Sam has a lot of guns with which to enforce/force the use of the FRN in international trade. Trade is all that matters. In addition, the U.S. is actually extracting and selling more oil (the real lifeblood of the modern economy) than ever, so this has also helped.

I’ll admit I thought the exact same after TARP in 2008. 700 Billion seems like a pittance now.

Uncle Sam doesn’t need to use guns. Other countries *want* to trade in dollars and hold Treasuries as assets, since they can be used as collateral for a cash loan from the Fed.

The Fed’s offshore dollar complex (including Eurodollar mkts) has done more to ensure USD supremacy than anything the military has done.

Short TLT,

“The Fed’s offshore dollar complex (including Eurodollar mkts) has done more to ensure USD supremacy than anything the military has done.”

LOL! Read “confessions of an economic hitman” The military is essential to ensuring everyone uses the FRN, especially to purchase oil (the lifeblood of real economies). Has been this way since WWII (Prior to this, the British Sterling was the reserve currency). See Korea, Vietnam, Iraq, Afghanistan, Libya, etc. etc.

One thing is assured: Increasing govt deficit either funded by FED, and/or other people/govt etc.

US govt can never default and they print their own currency.

USD is still the reserved currency of the world.

USD is much better than other currencies ie cleanest shirt in the dirty laundry.

WB,

That book is on my to-read list. I know the gist of it but have yet to actally dive in.

Re oil: that’s certainly how it was 50 years ago, but now we’re a net oil exporter. We don’t need oil from the Saudis anymore, but they’d much rather get paid in USD than literally any other currency.

Isn’t QE and stimulus generally meant to be an economic multiplier?

Ie, you spend X and get X + 20% or whatever, making it worth the debt.

Is the $Tns in USA fiscal stimulus giving an according GDP boost (after interest) or not?

If the spending is a net economic positive, and the spending is helping all those living in the USA, then I can’t see an issue.

But I’m guessing it’s not?

The “economy” doesn’t reach equilibrium. It’s either expanding or contracting. The 2% inflation target is a growth target, not a steady-state target.

Embrace the wobble.

This. Two thirds of USA gov debt is held by the American public as well.

I don’t think 2025 though, its going to be a gradual default. In 1942 the USA treasury capped the interest rate on long term loans to 2.25% even as inflation blew up through to 1951, this is before the Nixon default on gold in 1971.

Avoid all government debt it’s not just the USA. They never pay the money back!

Complete BS. Even Argentina has paid the “money” back. The issue is whether or not anyone actually wants that money in exchange for the fruits of their labor…

Of course US debt is safe, or if it isn’t no one’s is.

However: Re: Argentina. One of Canada’s Big Six, the Bank of Nova Scotia, is still recovering from its Argentine presence.

Like folks in many countries that have been racked by inflation and the intro of new currencies, Argentines liked to save money in US dollars. The BNS in Argentina

offered US dollar accounts, just like it does in Canada.

Then one day the Argentine govt swooped in and seized them. Something was offered but can’t remember what, except it was in pesos.

For months the BNS had women outside its locked doors banging pots and pans. It sold out for whatever it could get and left Argentina. Its Latin presence is now mainly Mexico.

LordSunbeamTheThird,

“Avoid all government debt it’s not just the USA. They never pay the money back!”

🤣 That “They never pay the money back!” is such ridiculously dumb BS. Obviously, you never held any US Treasury securities at all, and you’re just making up bullshit because you had too much beer? Or else you’d know that every single Treasury security that ever matured was paid back in full, including every dime in interest.

I think the sentiment is that people may be unlikely to get their money back with as much interest as they wanted, in hindsight, against the inflation that turned out worse than expected for them over the duration.

But yes, utterly daft way to say that.

You take your choice on risk vs reward.

I can see lots of very upset treasury owners through 2012-2022, vs stocks… they’re not young to “get their money back” (using hyperbole)

But then none of those people in the hall of fame of crashed stocks will either.

Kenny,

I am sorry, but your comment makes no sense. When you buy a treasury or T-bill, you know exactly what the principle is, and you can calculate EXACTLY what the interest will be when the note matures. There are NO surprises here.

I think what you are inferring is that the purchasing power of the FRNs that you do receive may be less than anticipated… Regardless, you will know EXACTLY how many FRNs you will get when the note matures, and even the bond holders in Argentina have always received the pesos that they where promised. Of course, those pesos were greatly devalued. Hopefully, CONgress doesn’t go “full Argentina” on us…

I even got paid back on time for Treasuries that matured during the debt ceiling drama.

Uncle Sam is the safest counterparty.

Ahhhhhh yes. Gold. Since Lord Sunbeam brought it up. It looks like gold might crash thru the $2500 mark today.

Anyone know why?

$2,500 is the new floor for Gold, for many reasons. The big one is that international trade must continue at all costs and gold is the only monetary metal or, more specifically, the only globally accepted form of collateral with no counterparty risk. The BIS and IMF made that clear by making gold a “tier one” asset again and bumping US treasuries down a notch…

In general, for global investors and global central banks, gold is SLOWLY replacing US treasuries as a reserve asset.

“for global investors and global central banks, gold is SLOWLY replacing US treasuries as a reserve asset.”

In general, gold isn’t collateral for dollar funding (loans and repos), whereas Treasuries are. The Fed’s FIMA repo facility allows int’l counterparties to post Treasuries as collateral for dollars.

I wonder if gold might be accepted for the riskier ‘other collateral’ category on BNYM’s triparty repo platform – but that wouldn’t affect int’l demand for dollars and quality collateral (Treasuries).

When and if the market goes down, Gold would also go down with it.. Just wait and watch.

Gold going up along with stock market is testament to the fact that we still have too much money sloshing around.

Check how much gold went down in the last mini crash-

Hardly slipped.

Thanks Wolf

QT hasn’t received much talk at all compared to rate cuts.

The first rule of QT is don’t talk about QT.

These data are solid, there is still plenty of cash sloshing around, 0.5 basis point hike in September!

Hooray!

Interesting times

I love these pretty charts with the graphs. They tell us nothing about what’s to come. In differential calculus, we have formulae that help us determine “the rate of change”. This allows us to look into the future to see whether the curve is going up or going down or flattening. We use this a lot in economics and a lot of econometric models have this “rate of change” as the core of the equations economists use with numerous other variables. I want to know what is going to happen in 2025 after the 2024 holiday season is over. Give it a shot, Wolf.

Comparing a hard science like math to a SOCIAL SCIENCE like eCONomics, is a fool’s errand, and I suspect that Wolf is no fool.

WB – triple check. (have yet to see Wolf consider economic ‘books’ to talk, especially ones about an, as yet, unarrived future…).

may we all find a better day.

vadertime,

You’ll find out when you get there. People have asked the same question all the time year-after-year. The collapse is always nigh. So it didn’t happen last month, bummer, but maybe in four months? And there’s always next year.

Even during the Great Recession and the unemployment crisis, with 10% unemployment rate, and the mortgage crisis, etc., and with the entire global financial system on the brink, retail sales fell only 14% from top (end of 2007) to trough (end of 2008), and a big part of that was due to auto sales, which plunged. And then they started rising again.

You know how I’ll know when the next great recession/depression will happen soon? When DiMartino Booth or her likes are telling us the economy is booming and we need to raise rates like crazy again…

That which is unsustainable can not be sustained. Charts tell yesterday and today assuming they are accurate. Nobody knows the future, but logic, common sense and math can help. As a mathematician, using probability theory to examine the law of total probability, one can reach conclusions that may be more accurate as a percentage. But remember abstract variables such as social unrest, black swans and divine interventions like climate catastrophe should imho also be considered as major world events appear to be speeding up with a cascade or domino type inertia. Said about bankruptcy – slowly at first, then all of a sudden..logic, common sense, and math..or we can see happy drunkards(sailors), if we choose.

This might surprise you: Economics is FULL of math, it’s based on math, including calculus. Back in the day, in our economics classes in grad school, we had to calculate regression analysis, complex differential equations, etc. on a piece of paper, helped by our then brand-new HP 12c calculator, which made it easier. Now this kind of stuff is a lot less work because computers do a good job at it, if you know how to set it up.

So people who juxtapose mathematics as somehow reliably good, and economics as BS are clueless. Economics is based on math. Math is just a tool.

Well…..maybe……housing starts and permits look sick……what is a leading indicator……housing……I bet cuts are coming…….more than one.

Do I want one……nope……but the crazies are in charge.

Yellow rocks think it’s a done deal.

Where do you live in FL?

I use to live in SW FL and inventory is through the roof with prices dropping quite a bit. Move to Jacksonville last August, prices are not dropping as fast but the inventory is climbing.

‘Subway has called an “emergency meeting” with the franchisees that run its 19,000 restaurants amid tumbling sales and profits.

The sandwich chain – with more locations than McDonald’s but much lower sales – will reveal plans to lure in more customers. such as deals and new products.’

This item was taken from the Daily Mail and ’emergency meeting’ was in quotes there so the assumption is that is Subway’s wording.

Subway is not only player in fast food feeling a push back from consumers. Suddenly everyone is offering a ‘value meal’

The McD franchisees were not happy when HQ announced its 5$ value deal, some saying they couldn’t so it unless the Mother Ship was going to chip in.

There are many ways of trying to gauge consumer sentiment. Fast food might be a good candidate. For almost everyone it’s a optional, discretionary purchase. You have to buy gas, and unless you are on a tight budget, you don’t ration your miles. Maybe cutting back on miles is late indicator of a slowdown while fast food is an earlier one.

It may be hard to convince teens or teen mentalities that a visit to Mc D is a treat and not a necessity but it won’t harm anyone to make food.

I will fess up to being a geezer. When growing up we got take out once or twice a year and it was NEVER delivered.

Nick – are these service-coalmine canaries of a genuinely-productive economy looking peaked due to bad air? Old age? Both? Best.

may we all find a better day.

Subway is seriously sick. Have been for years. They’re restructuring. Nothing to do with consumer demand but with their own inept management decisions over the years. Don’t ever extrapolate from a company with issues to the overall economy. You will be led astray.

True. But Subway isn’t the only one. Nick mentioned McD.

The other large chain that has gone through reduced same-store sales is Starbucks. whose CEO was ousted just a day or two back. They have more problems in China than in the US (where the middle east issue resulted in some boycotts).

Of course, Walmart came out yesterday predicting increased revenues.

Seems to me that there is a tug-of-war between increased splurging and belt-tightening.

Man, I see those exact 2 companies (minus subway, havent heard much about them for a while personally) touted all over social media accounts and mainstream articles as a signal of economic slowdown for the past few weeks. Both have good reason to see revenues slump, with McD’s though you just have to look at the pricing, locally where I live proper sit down restaurants are touting near McDonald pricing but you can eat at a table with cutlery and porcelain dishes instead of chemicals and cardboard from a bag in your car, hence the lower price options coming in at McD now.

As for starbucks they’ve made the decision to close down a significant percentage of locations right across Canada over the last couple years (not just last quarter or something) and I’m assuming it’s similar in other countries. At the same time they’ve been renovating most remaining locations with each reno reducing seating space inside and some locations even have 0 seating now. I’m sorry but how do you grow revenues when you reduce locations and seating areas in existing spots bit sell coffee with a premium? In response in my city there’s been independent shops popping up in their place, in the last town I lived in independents even offered longer hours for people like me who like to do a bit of work at night, guess where I went, a lot less starbucks.

I mean I could be wrong, could be “belt tightening” going on, I hear and read about it weekly, but at the same time individual companies make individual decisions and suffer the consequences good or bad. I’m a little bit skeptical that these are canary in coal mine type situations because they seem to be getting singled out by so many authors and “analysts”, and there seems to be very little consequence to calling recessions over and over again like so many have been doing for years now, but there’s a lot of reward the one time you get that right.

Seba – mebbe a case of the longterm ”WeWork’ out of Starbuck’s’ paradigm being slowly-replaced by more WFH or? (the average ‘seat rent’ time/turn from latte profits no longer pencilling against the CRE/data access overheads+price competition from home/office-brewed java…).

may we all find a better day.

I want my $5 footlong back.

All the fast food franchises are leaning hard into ordering/paying on the app. I figure its a few minutes of labor they can trim off every transaction. Kiosks too. Even my beloved Togo’s has gone kiosk, although the don’t require you to use it.

Fast food work will become factory/assembly work, workers cooking burgers and making sandwiches from orders displayed on touch screens. Finished orders will go onto a rack with a number matching the customer’s app.

Notably this is exactly how the 3 company cantinas function at a well-known high tech company where I work.

If you’ve watched the movie “The Founder” it shows how the original McDonald’s excelled by very efficiently producing a very limited menu. I see an opportunity to feed the country’s burger habit with a completed automated dispensary of say 3 kinds of burgers, one size fries, and one size of a selection of soft drinks. It could probably be done in something the size of a food truck. Mobile, no land or building required. Order on the app, wait for your order to appear in the rack on the side of the truck. Buzz could be generated by being mysterious about who/what is inside the truck. Is it people? Is it robots? Is it Oompa Loompas?

Excuse me I have a business plan to work on…

Ross…makes me think a bit of Henry Ford’s “…any color you want, as long as it’s black…” for the T-model, a successful, similar, limited-option availability used by the Japanese firms in establishing their initial U.S.-market bridgehead (auto segment having wandered away from this in recent decades, market fancies/vagaries never making the necessary SWOT-analyses/adjustments facile. (Management,instead, often appearing to make a choice to ignore them altogether…)).

(…or, a (very) rough analogy referring back to my response to Seba, above-by the ’50’s the Big3 had become a ‘Starbuck barista’ business culture (no disrespect implied/intended towards baristas) in terms of the multiplicity of brands, models and ‘options’ of their products. The Japanese imports of the ’60’s were then, in contrast, discovered to be an excellent-value, if no-frills, gas-station ‘cup of coffee’, for the price…).

may we all find a better day.

I agree. People used to go to restaurants for a break to hang out and talk as a treat. It was enjoyable. Now all anyone is restaurants do is stare at their phones.

All the FED needs to do to get some insight on the taxpayers/investors/public opinion is to read and study all of the comments here. From that he and the others on this committee would actually make some smart decisions that would benefit the above instead of the Big Companies and WS……

Are there any serious economists that believe that the CPI understates inflation? I know it is an idea held by some fringe types. Or is everyone here going to characterize as “not serious” any economist, regardless of their degrees, who holds that view?

There are LOTS of economists who think CPI OVERSTATES inflation because of its big housing component that has been pushing UP CPI (I disagree with that assessment, but they’re there, including at the Fed).

There are also LOTS of clickbait newsletter sellers that came up with their own bullshit formula about CPI in order to sell their newsletters. Those people can easily be debunked with basic compounding math, and I have done it here a few times. Their crap is only appealing to people who cannot do math.