Total debt rose over the years as a larger population financed more costly collateral. But income rose too.

By Wolf Richter for WOLF STREET.

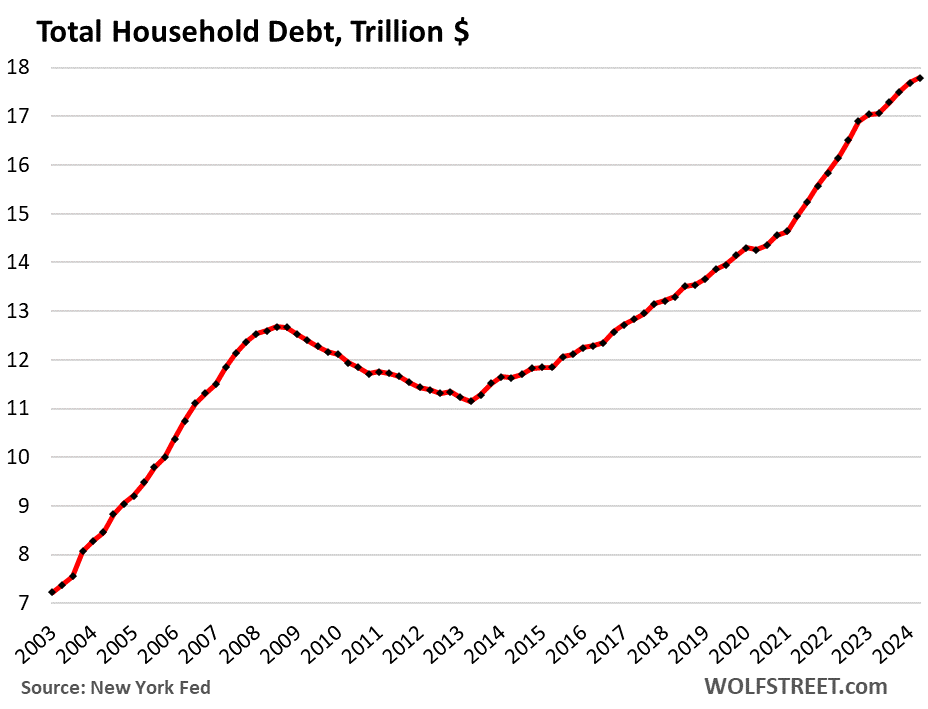

Total household debt outstanding in Q2 ticked up by $109 billion, or by 0.6%, from Q1 – the smallest percentage increase since Q2 2023, and the second smallest increase since Q1 2021 – to $17.8 trillion, according to the Household Debt and Credit Report from the New York Fed today. Year-over-year, total household debt grew by 4.3%.

Why the debt grows: Homes, vehicles, and many other things that people finance got more expensive over the many years — particularly, home prices have exploded over the years — driving up the amounts financed, and so overall debts grew.

In addition, the population grew over the many years, with more people getting mortgages and auto loans. So total amounts borrowed have risen over these years because a larger population is financing more costly collateral.

All categories except student loans increased quarter-to-quarter. Student loan balances dipped – not because borrowers were suddenly following a new religion of prudence and responsibility by paying down their loans faster than new borrowers were piling them on, but because the government forgave waves of loans and wrote them off at taxpayer expense:

| Loan balances by category | |||

| Trillion $ | QoQ % | YoY % | |

| Total | $17.80 | +0.6% | +4.3% |

| Mortgages | $12.52 | +0.6% | +4.2% |

| HELOCs | $0.38 | +1.1% | +11.8% |

| Auto | $1.63 | +0.6% | +2.8% |

| Credit card | $1.14 | +2.4% | +10.8% |

| Student loans | $1.59 | -0.6% | +1.0% |

| Other | $0.54 | +0.2% | +3.2% |

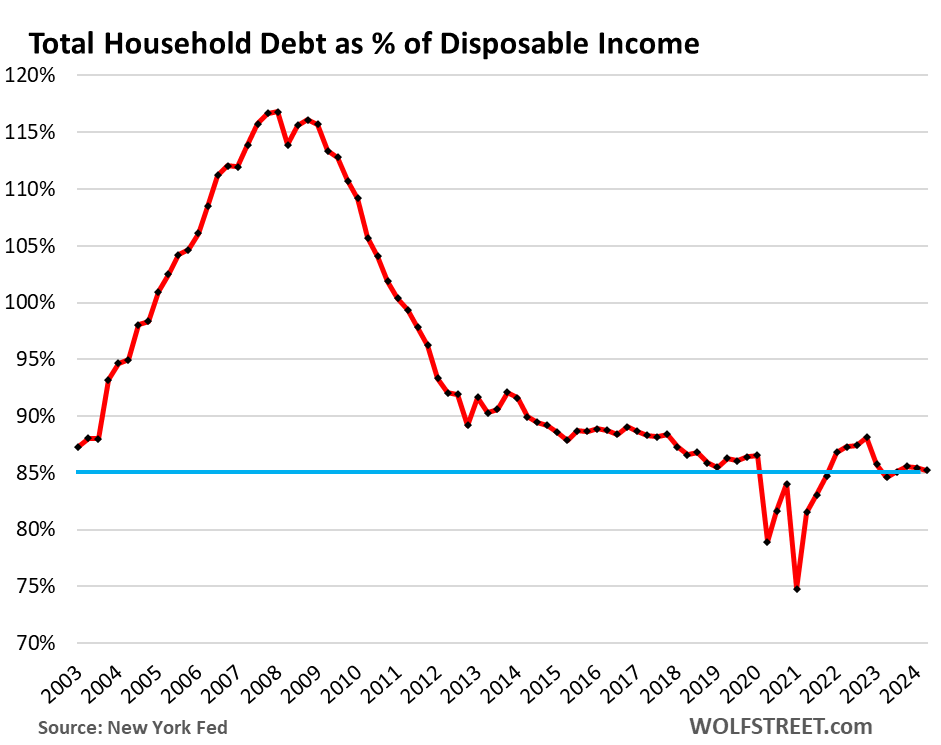

The relative burden of household debt.

Households have to pay for this debt service from their income. One of the ways to measure the burden of debt is to compare the debt to the amount of income that is available to pay for debt service.

“Disposable income” has risen due to the growing population and higher wages. “Disposable income” is income from all sources but not capital gains; so income from wages, interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc., minus taxes and social insurance payments. This is essentially the cash that consumers have available to spend on housing, food, cars, debt payments, etc. And what they don’t spend, they save.

Disposable income (according to data from the Bureau of Economic Analysis) grew by 0.9% in Q2 from the prior quarter. The total household debt grew by 0.6% in Q2. So the debt grew more slowly than income.

At $17.8 trillion, the debt amounts to 85.2% of disposable income, down a hair from the prior quarter (85.5%), and roughly unchanged over the past five quarters, and a historically low burden, bested only during the free-money-stimulus era which had inflated disposable income beyond recognition.

The chart also shows why households were hit so hard during the Financial Crisis that slammed them with an employment crisis as they had been heavily overindebted. That’s not the case anymore. Our Drunken Sailors learned a lesson?

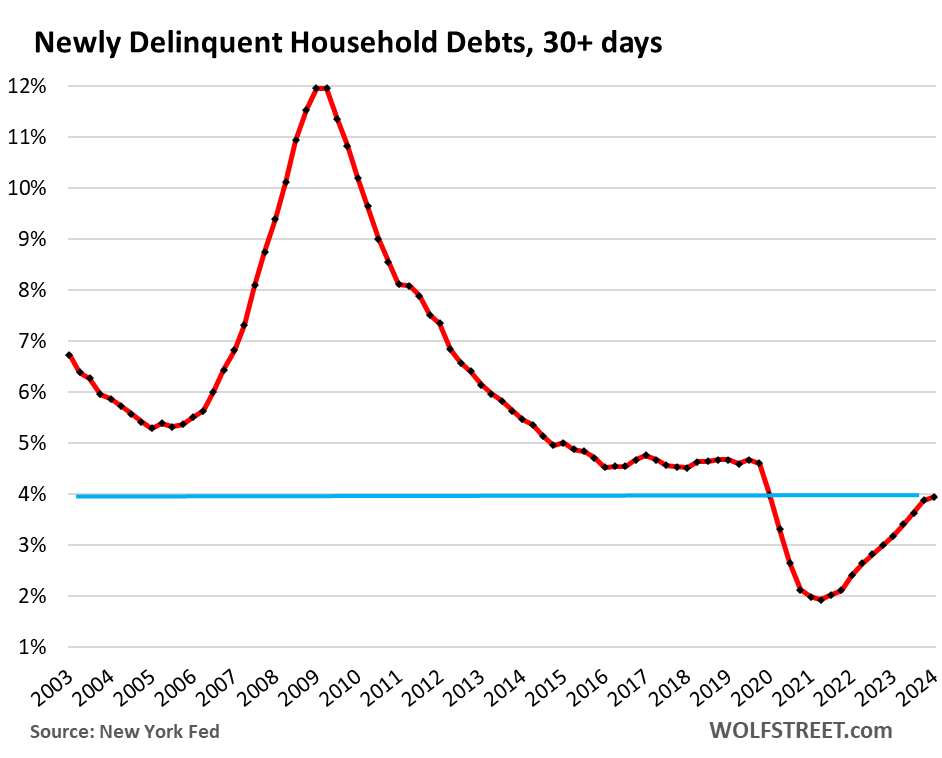

Delinquencies still lower than normal, barely tick up.

Our Drunken Sailors, as we have come to call them lovingly and facetiously, have been sober enough to keep their balance sheets overall in good shape, with the debt burden moving along historically low levels.

A small portion of the people is always in trouble, subprime is always a factor, but subprime doesn’t mean “low income,” it means “bad credit,” and goes across the income spectrum. And there’s always some of it. And some people get into trouble, while other get out of trouble when they cure their credit problems. And it’s always in flux.

Newly delinquent: Household debts that were 30 days or more delinquent at the end of Q2 ticked up to 3.95%, from 3.88% of total debt balances — a minuscule increase that shows up in the flattening of the curve. The delinquency rate is still lower than any time before the pandemic.

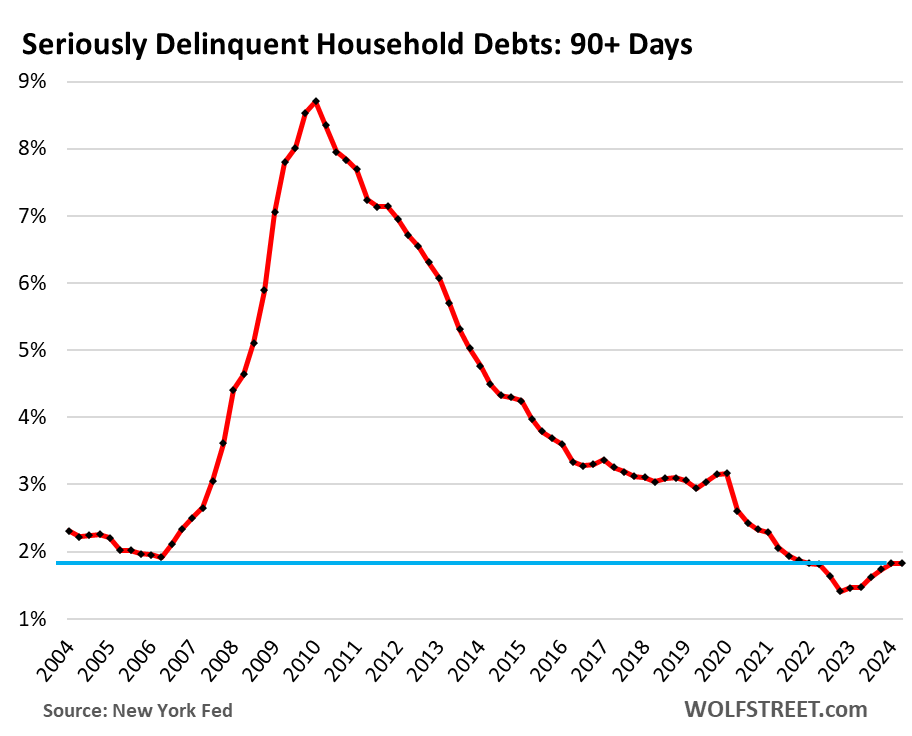

Serious delinquency: Household debts that were 90 days or more delinquent by the end of Q2 remained unchanged at a historically low 1.83% of total balances, still lower than any time before the free-money pandemic.

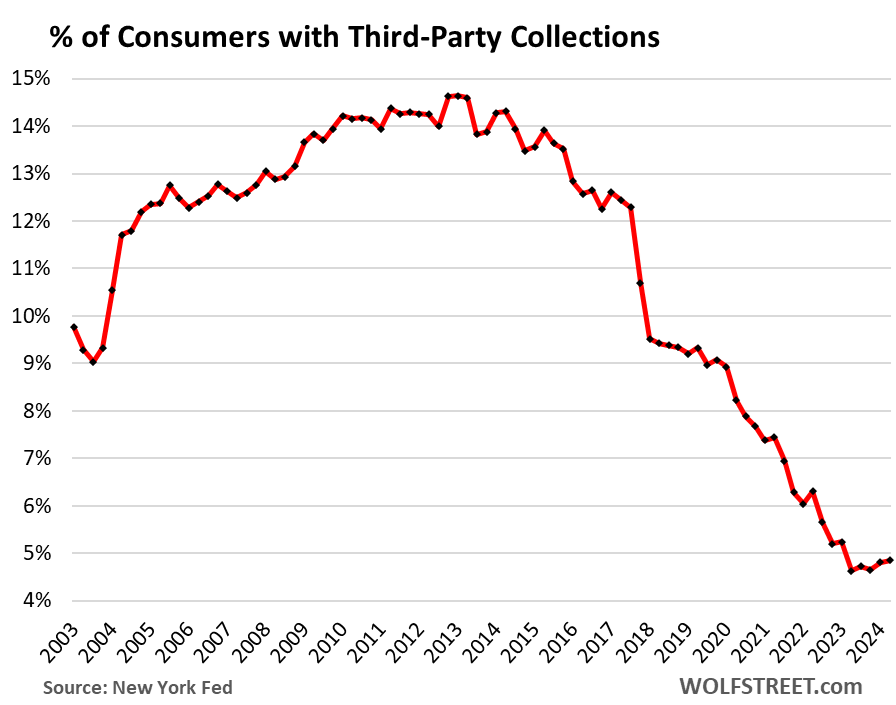

Consumers with third-party collections still near record lows.

A debt goes to a collection agency – the third party – after the lender has thrown in the towel on the delinquent loan, has written it off, and has sold the account for cents on the dollar to a company that specializes in hounding debtors to squeeze some money out of them.

The percentage of consumers with third-party collections inched up to 4.85% in Q2 from 4.81% in Q1. This chart is almost funny:

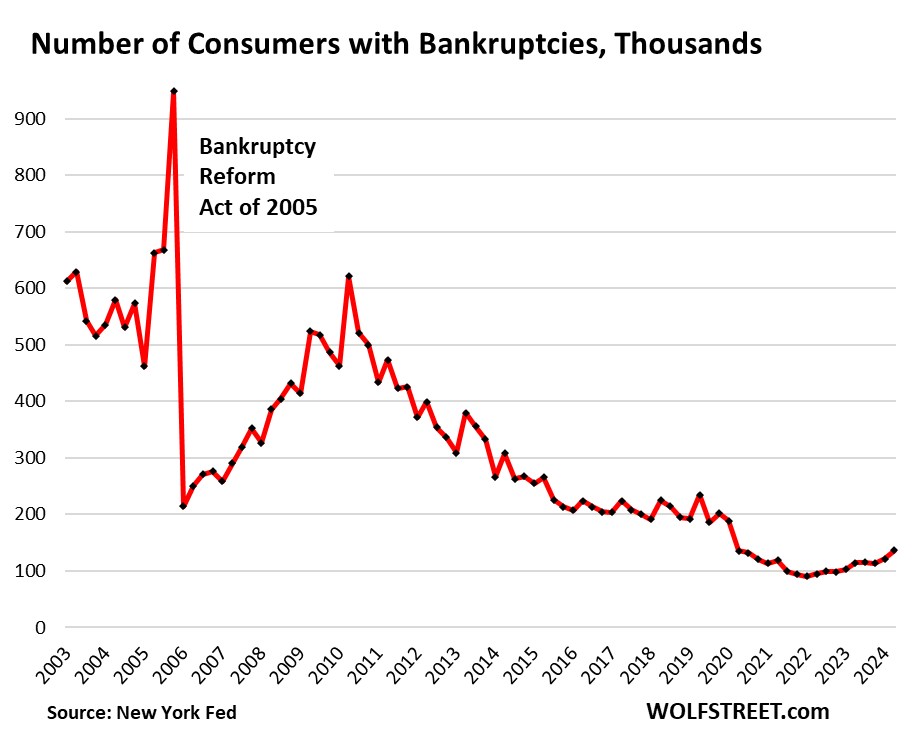

Consumers with bankruptcies still near record lows.

The number of consumers with bankruptcy filings are easing up from the historic bottom, and are still far below prepandemic normal. In Q2, there were 136,180 consumers with bankruptcy filings. By comparison, in Q2 2019, there were 234,280 consumers with bankruptcy filings – and that too had been relatively low historically:

We’re going to dive into the details shortly with separate articles for housing debt, credit card debt, and auto debt and their respective delinquencies. So stay tuned.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

No debt here. Minimalist.

Got some debt on my side, 50k on mortage, 5k on car and 3k on CC that should be 0 in a couple of months. One car household earning 90 with dividends. Maybe not bad for 32?

Pay down that CC ASAP because the interest rates you pay on it are always terrible.

Nothing wrong with low-rate, long-term, asset-backed debt with a low LTV – especially when complemented by a big cash pile.

What about inflation? Wouldn’t inflation adjusted show a better picture?

getting ready to create some new mortgage debt

for buyer of my home

owner carry that is

Not bad at all!

Now the trick is to stay healthy/sharp, don’t get divorced and avoid terrible soul-crushing work.

And body trashing work……guess fewer do that stuff anymore, with robotics and lots of fossil fuel to run them……and immigrants…….running on low or even “what 10-20 extra hrs?….and just what are YOU going to do about it” (which is understood, maybe even said) wages.

Many robots don’t LOOK like robots…like computers..and from the kind I worked on at P/O (letter sorting machines) to the laser item/price reader at the grocery……and round-up ready corn seed…just drench it all…..zero weeding.

The early Luddites were just worried about jobs in a nasty capitalist world…..now it’s the planet at stake and nobody gives a shit as long as they have a regular paycheck big enough to keep them off the street or out of jail.

….and then there’s the “lifestyle and need expanders”……Stokely Charmichael had a good phrase for them……referring to an unfulfilled need they hadn’t thought of.

Excellent balance sheet at 32 my hat is off to u!

PDG, pretty darn good!

Howdy and row well 42. Sorry, that was 41. Anyway, Deft Free is only way to be…..

Live withen your means and revel in the magic

#42,

I agree – and act – 100% the same way.

I think this is frightening …

“ At $17.8 trillion, the debt amounts to 85.2% of disposable income …”

No, it’s not frightening at all. It was 115%-plus in 2007/8, and that was frightening. 85% is near historic lows. Consumers have massively deleveraged over the years.

But government is leveraged out the wazoo, and businesses are highly leveraged. That’s where the leverage is, NOT consumers. And THAT is frightening. And we have already seen a lot of this leverage blow up, such as in CRE.

Wait and see. Repossessions are actually on the rise and within the next year as more layoffs happen and home prices fall, people will be unable to pay their bills. They will start opting to let things go back to the lenders instead of paying their bills. This cycle is about to hit.

John Dixon,

It’s the same BS about these tapped-out collapsing consumers day after day, month after month, year-after-year, driven by clickbait bullshit on YouTube. It never changes.

When the debt was in the hands of households, at least it was somewhat managed and reset on a periodic basis. If not self-managed, there were bill collectors and credit agencies that kept debt in check. Periodic write-offs would lead to a recession, but not existential crisis.

National debts, on the other hand, seem to keep growing without check or governance.

Our monetary and fiscal “leaders” have traded periodic recessions for some sort of massive, unknown, credit-based, and system-altering event in the future. Is that a good trade?

They act like the dimwit who smokes two packs a day, knowing it will kill him. Until an irrefutable diagnosis come in, luck is in the air, so they add high balls, ribeyes, and cherry pies to the mix.

Wolf,

Thank for the clear explanation. It is why I visit here daily.

anon

and auto repossessions up 23%

From what level??? LOL, near zero? Contextless bullshit.

It’s not that bad those charts

Merrill lynch says household cash is 18 trillions how could that be possible

Yes. Here is a big part of it — something we’ve been covering many times, Americans are loaded with cash. That doesn’t even count what they have in RE equity, stocks, and other assets.

https://wolfstreet.com/2024/04/27/money-market-funds-t-bills-large-cds-small-cds-americans-learn-to-arbitrage-the-higher-for-longer-interest-rate-environment/

MMFs held by Households: jumped to $3.8 trillion at the end of Q1, up from $2.6 trillion during the 0% pandemic era, and up from $1.6 trillion before the rate-hike cycle of 2017-2018.

Households are indirectly among the holders of institutional funds because the institutions include employers, trustees, and fiduciaries who buy those funds on behalf of their clients, employees, or owners.

Total MMFs held by households and institutions (including for households) spiked to $6.44 trillion by the end of Q1, according to the Fed’s data.

Large Time-Deposits (CDs of $100,000 or more) surged by nearly $1 trillion since the Fed began its rate hikes, to $2.37 trillion by the end of February 2024, up from $1.40 trillion in March 2022. Last month, they dipped a hair to $2.36 trillion in preparation for Tax Day, according to Federal Reserve data released this week.

Small Time-Deposits (CDs of less than $100,000) surged from just $36 billion in May 2022 to $1.1 trillion in January and have stayed there through March, according to Fed data.

Treasury bills: There are currently $6 trillion of T-bills outstanding. We don’t know the amounts of T-bills that households have stashed away, but it’s significant.

Howdy Lone Wolf. AMEN. Squirrels do it better

well if you count IRA’S with over $35T

Which saver fell further and went up less. And why? We are all in the same “economy”, right?

Care to preach and brag some Squirrel man? Maybe some content, too?

How funny is thay? It looks like the drunken sailors are the smart ones after all. Theyve been enjoying years of partying and free drinks, borrowing at rock bottom rates and now they can get even top dollar returns on their cash they saved by going to hapoy hour!

The teatotalers who quit drinking (borrowing) and gave up debt and spending after the 2008 crash are the ones with the hangover and the headache because they quit when rates were low and now its too expensive to borrow.

They drank water during happy hour and now that happy hour’s over, they want to get drunk, but drinks are four times the price!!!!

Holding cash makes sense because it actually pays a yield now.

Berkshire Hathaway’s $234B stash of T-bills says that Buffet feels the same.

US public debt would be the debt replacing private as growth driver of last chunk of years. Still running deficits like this is sustainable. Really going to have issues if growth stalls, inflation still running hot and treasury yields move higher.

Lower household debt seems to be a big difference vs the GFC… but now we have gov’t debt out the wazoo instead.

Uncle Sam is the biggest drunken sailor.

So, Uncle Sam is coming with his hand out, to tip the scales back his way?

I sure hope so Cory…..that 1960 Tax schedule is a thing of pure beauty….plus a few years of heavy “Death Taxes”. Get some wealth BALANCE here!

ENOUGH trickle down, and horse and sparrow, etc,etc.

Then we change some laws so this crap doesn’t happen again!!!!

Probably too late climate-wise, but there is always hope for a MASSIVE Green New Deal with gov’t help.

Thanks for those charts. I did not realize consumers with debt issues were this low when compared to historical data. ‘

There is trillions of home equity that can be tapped yet too.

It doesn’t look like so-called “disposable income” takes account of inflation – how about a chart of *real* disposable income reflecting the G money pumped into the system to get that *gross* disposable income up…at the cost of real asset inflation.

If “disposable” income goes up 10% but prices are up 20% – that ain’t a win.

The debt is not adjusted for inflation either. Apples to apples. Nominal debt divided by nominal income. Debt to GDP works the same way, all the ratios do, apples to apples. Think, dude!!!

@wolfRichter

I just finished reading another article that said, “Companies return to Debt Markets, Pushing Sales Pass $1 Trillion — fastest clip since 2020 of ZIRP era”

I know the yield curve is inverted meaning LT rates are lower. Still they seem to be paying some 200 basis points above 10 year treasury, meaning around 6%. Are they signaling 6% is the normal going forward which implies mortgage rates may not go below 6% either. Any thoughts? TIA.

Yes, huge amounts of debt are being issued. The public debt markets (bonds, leveraged loans) and the private debt market (nonbank lenders) are very loose right now, lots of investors are jostling for position to buy this debt, and lots of companies are issuing this debt, lots of junk debt too, at these rates.

So leveraged loans are junk-rated and usually come with a floating rate, so they’re not a bet on rates. They’re hot right now.

But bonds are mostly fixed rate, and they ARE a bet on interest rates. So the eager issuer thinks that rates are about as low as they’re going to get, and they want to lock in the still low-ish yield; and the eager buyers think that rates are going to drop, and they want to lock in the still high-ish yield. They both think in the opposite direction, which is what makes a market.

Who is going to be right? It’s really tough to draw conclusions from the debt markets right now.

And Tuesday’s Atlanta Fed GDPNow estimate for Q3 is 2.9%. Sounds dreadful. Definitely requires at least 12 rate cuts.

We’re nowhere near a recession with defaults this low.

JeffD

🤣❤️ that’s what I thought too.

Abolishing the Fed put is the best thing the Fed could do to correct the devastating effects of pandemic policy actions. The K shaped recovery is the one thing that stands in the way of lowering inflation, so it would be a mistake to cut due to market behavior.

Furthermore, the Fed would be doubly wise to delay the first cut until at least November, in support of the data, since a delay would remove public perception of a politically motivated cut. In the grand scheme of things, whether a cut happens in Septemer or November is irrelevant to the medium term path of the ecomy, but has a very large impact to the credibility of the Fed.

Wouldn’t choosing to wait to November when everyone has been talking about September be considered politically motivated?

who is “everyone?” shills have demanded it, but the fed hasn’t promised anything.

Everyone being the market. Is the entire bond market shills?

You’re the one advocating for a politically motivated delay.

fausterion, the bond market doesn’t get to decide what short term rates are. the fed does. pricing in things that the decision makers haven’t promised and then claiming that it’s politically motivated not to go along with the market’s prediction is absurd on its face.

Fausterion:

The “entire bond market” would consist of the yield curve and the credit spreads etc.

The “rate cut probability” is derived from the derivatives markets and therefore relies on the actions of gamblers.

From Investopedia:

The CME FedWatch Tool uses the prices of fed funds futures to predict how the Fed might act concerning interest rates. The futures, which are traded on the CME,

*allow investors to speculate*

or hedge based on what they expect in the future direction of this key interest rate.

I think the 10y-2y has historically been the most accurate “recession indicator” in the bond markets.

That particular spread has raced towards the zero line and hesitated to cross: the inevitable “next recession” may still be postponed.

I also personally believe it WAS a good prediction of the pandemic induced recession/ black swan.

No, Kent. It wouldn’t. The recent drop in long bond yields has done a lot of heavy lifting for the Fed concerning financial conditions. On the other hand, elevated inflation persists, well above Fed target. The right move with *current data and conditions* is to hold rates steady in September.

It’s pretty Simple:

Paying interest to borrow money- BAD! 😠

Receiving interest on your money- GOOD! 😄

That’s right. I’m trying to figure out when I should start buying longer term treasuries at these rates before they head back towards zero…

I resent being called a drunken sailor. I think ma’ boy Jerry down at the shelter ran off with my investment money. I couldn’t find him anywhere yesterday. So much for sharing some tall boys with him.

I’ve never even been on a boat before. All I got is this Cuervo. Maybe if it was some Captain Morgan’s I could at least pretend to be a pirate for a while. I’m no pirate. All these homeowners don’t seem like sailors to me either. Meanwhile, I’m just here in my storage unit hoping to be like them one day. Things aren’t looking good. Right now, right after the Bank of England finally cut rates, look at the headline:”UK House Prices Rise the Most in 6 Months”. As if that’s a surprise, how could those bankers have known that would happen. Things are not looking good for me, especially if the FRED Flinstone cuts rates too, yabba dabba boo hoo.

For some supposed drunk sailors, they sure seem like some landubbin’ land locked golden handcuff wearing freedom selling compliers rewarded for being greedy. All I wanted was a simple home, just a roof over my head with a plumbed toilet, a refrigerator, and a few tall boys. I’m feeling like it’s never going to happen now.

My investor-class buddy was moaning about the stock blow-off lately. I told him it cleaned out gamblers (with calls on margin, and such, along with crypto bros and their ilk), and showed markets are at least somewhat working. I also said there is a generational problem, from ten years+ of cheap money and credit creation, and the lofty effect on asset prices. And, I said, part of the cost of that now, is the high interest rates and high prices facing small businesses and now low-end consumers, with the consumers ditching purchases, squeezing the small businesses’ margins. I told him the way out now, from all this built-up kindling, to avoid a wildfire, if managed responsibly, involves pain for all. It involves some steadiness with rates, I said. I think I offended him. Meanwhile, my total debt (for the whole remaining year) is 0.31% of my assets, marked to market. No vodka for me, not even the cheap stuff, for 27 years running.

Are you saying that you know Jerry too? Where was he yesterday? Tell him I want my 50 bucks!……that grimie grifter.

I’m not living above my means. There’s no Sam Adams bottles in my dump pile out back, just Bud Light cans.

I’m hoping to get hit by someone driving a G-Wagon and get the big bucks payout that will get me to where I need to be in life. Good luck drinking rubbing alcohol since you don’t want to splurge for Vodka. Been there, done that, don’t want to again, I put in work to get to where I am today.

Popov…..$1.39 half pt……I’m an 1980’s recession victim….Reaganomics…first time I ever drank alone….medicinal…prevented worry heart attacks…..many never made it out…I was lucky.

Wow, that trickle down economics sounds like it filled up your cup. $1.39 for a half pint……just wow. Rubbing alcohol costs more than that these days. I miss the Covid era where hand sanitizer was everywhere. That stuff does the job and you could get it for free in a lot of bathrooms or building entrances. Those were the days.

Hand sanitizer (while it is related to the pandemic) was a poor choice for your attempts at your “humorous” writing style.

Methanol would have added more genuine alcoholic creds.

We used to have a guy here called “unamused”.

Have never seen his writing style topped…..ever….MANY experiences and much financial education to draw on, plus I think ,computer info retrieval equipment/ability.

Not saying to quit trying, there is always a place for humor….I even enjoy and sometimes try it.

In other words, that was a REAL and BAD experience for me, NOT a joke, and like I said, MANY never escaped that recession…..watch “Cops” to see what happened to them, especially the whites, who thought they had special status in this system. Almost normal for those of color.

There is a place for empathy here, too.

I worked with a guy who’s 64 Chev could easily DO a TALL BOY. Still waiting on that sensual six-way folding tailgate bed dance.

Hmm. These numbers feel like they might be hiding a major bifurcation. Do any of them get broken down by home ownership status?

Disposable income has gone up. Obviously the definition is what the definition is, but personally I always though of “disposable income” as “after essentials”.

If you’re a homeowner, you likely have, or refinanced to, a very low mortgage rate, and your “after essentials” income may well have gone up substantially over the last few years. You’re also generally sitting on plenty of equity, so you have a decent safety cushion to tap (the rise in HELOCs is interesting to note)

If you’re not a homeowner, it’s probably level at best or gone down, crushed by rental inflation in particular.

So when does the party stop? I suspect for non homeowners, it already has. Homeowners still seem very confident their equity is real money that’s not going anywhere, so they’re happy to spend. I wonder how quickly things would grind to a halt if the equity starts to disappear?

great comment. the fed can either crush inflation or it can maintain asset bubbles. it cannot do both.

random50

65% of US household are homeowners.

35% are renters.

A good portion of those renters are “renters of choice” with incomes well above the median who rent houses, apartments, and condos that are at the higher end of the scale. Renters of choice is who the big single-family landlords are targeting; and just about every apartment tower that was built over the past 15 years is targeting renters of choice with their high rents and luxury apartments. Why? Because that’s where the money is.

The bottom 20% of households (on the income sale) have to rent in older rundown buildings. The bottom 20% are the households that don’t have anything, and it’s really tough there, and it has always been really tough there. They’re also not big spenders, obviously, and so they don’t move the overall economic needle much, one way or the other.

That’s the bifurcation of which you speak.

Anecdotally (read meaningless), i see a few things right now.

People that owned a home before 2019 have refinanced to a tiny payment and have seen an amazing increase in wages meaning way more disposable income.

People in the above category occasionally taking HELOCs and blowing it on dumb stuff. AKA disposable income.

The upper age demographic having insane stock market returns and cashing out some of their retirement funds. More disposable income.

The younger group getting “good” wages but not anywhere near the kind of money to buy a house. Even spending 2k a month on an apartment they have plenty to blow on toys or the latest influencer instagram crap. They’ve resigned themself to the idea that owned housing will never be attainable and so eff it, party now.

The 35 and under demographic have given up and live the YOLO life recklessly, the 45+ group are raking in dough due to hitting the financial lottery if they were even remotely responsible in life in the past 20 years.

Unless you are making subway sandwiches for a living and had 5 kids by your 21st birthday or you went on disability at 30 and have been in section 8 housing for 20 years; you likely have the life of a king right now.

I barely know anyone who is not riding in nice cars, have expensive hobbies, and toys. Just depends on where that wasted money came from.

The only people somewhat strapped for cash are the working class who bought a housing during the covid years.

You must live in the nice part of town.

“The 35 and under demographic have given up and live the YOLO life recklessly… They’ve resigned themself to the idea that owned housing will never be attainable and so eff it, party now.”

This is my age group and I see this attitude a lot.

I hope they understand capital gains tax. Especially higher earners, they can pay 35% I think?!

That’s a ridiculous tax rate.

I sort of feel like couples earning less than half a million these days are falling behind.

Yeah man, one near me is a fitness company who is going to build a luxury tower.

A luxury fitness company tower!

Who would have thought it?

I just remember towers being negative because of that HBO show The Wire

“I sort of feel like couples earning less than half a million these days are falling behind.“

Some rather serious financial dysmorphia going on if people think they’re flagging in life because they make less than half a mil a year. That perfect # gets pushed out each year by an ever-dramatic margin. I know only one (palpably miserable) couple who I estimate are pulling in about that – he’s a spinal surgeon and she’s a contract lawyer. No kids, just two insane dogs. If they’re the new benchmark…

In five years people will cite millionaire status as the bare minimum for a functioning middle class

How about “homeowners” in 70s double wides (like my brother) all the way down to old camping trailers….are those all defined as “homeowners”?

Not being snarky, I really don’t know.

But there are an awful lot of them….just in my pretty wealthy area.

Central Valley is much worse…..then there’s the South……

Much more vicious game of Social Darwinism played there. And more “good Christians”, too…..go figure.

Just called him. Total fees are $686, in kinda dumpy park right next to 101. It’s an 800 sq ft 1977. He has no car…walk and bus and sister.

But he is a “homeowner”

( which is better than me…..my rent is just about twice that.)

But he has to pay regular maintenance for roof (almost no pitch), swamp cooler, leveling, and other assorted work. It IS 50 years old and not built too well as homes go. Paneling on 2×3 stud walls. I did a lot of electrical, plumbing, sistered new joists and flooring/linoleum under bathroom toilet area, and built new porches before back went out totally end 2013….mixing concrete….mainly moving bags around…mixing in wheelbarrow is almost a break.

I knew income was going up (lots for gov employees) and I was thinking this would infuse more investment activity as many people invest a percentage of income.

For many, debt goes up when income goes up. Thanks for making that connection.

The 10% YoY credit card balance increase is eye-opening. Is that being paid off each month (revolving), or is it being held for multiple months?

You’ll have to wait for details until my credit card report comes out, maybe tomorrow. The YOY increase is largely a reflection of the travel boom, especially the business travel boom where luxury hotels and business-class tickets rack up large amounts in no time, but are reimbursed and paid off every month (confirmed by Visa, AmEx, and MC reporting), plus higher prices, and population growth with more people using credit cards to buy stuff. Credit card balance as percent of total consumer debt are near historic lows, same with credit card balances to disposable income. Details in my report out maybe tomorrow.

Looking forward to it!

Curious how Buy Now Pay Later and other nontraditional schemes factor into the story (I dont believe they are incorporated into the published debt figures).

You’ll have to wait until my credit card report comes out maybe tomorrow. It also covers other revolving debt, such as BNPL. Let me just say here now that BNPL balances are minuscule in the overall scheme of things, and payments via BNPL nearly vanish in the $11 trillion in payments a year run through debit cards and credit cards.

I think a lot of consumers are realizing BNPL just isn’t a good deal.

Why would you take out a 1-month loan when you can put the purchase on your credit card, get 2% cashback, and still have almost a month to pay it off?

Thanks to Wolf I held off with the doomsday bunker and put my money in a 5.15% CD. The house is paid off and will remain so. I do not see it as equity, I see it as a cozy tomb. That’s about as deep as I get anymore. My crystal ball is defective, so I will stick with the charts and I will RTGDA if it doesn’t go over my head.

Anecdotal, but was talking to a large “toy” dealer and at a recent event. He sells UTVs, ATVs, motorcycles, etc. He said they are moving vehicles, but the number of people doing all cash deals is really eating into his biggest profit center – financing. People getting smarter and returning to old-fashioned values of delayed gratification?

Or are they simply drawing from a HELOC or other type of debt to CASH buy, instead of financing through the dealer?

If you use a heloc, wouldn’t you just transfer that to your checking account then use a credit card or write the dealer a check?

Perhaps a cashiers check for the total.

Maybe you guys don’t mean actual cash in a briefcase. 💼

“Good evening Mr. Bond.” 🤵♂️

“Cash” in this context almost certainly means a check or wire transfer.

no, it’s more that the rich are flush with cash.

also, stocks have recovered all of monday’s losses. so much for needing a 75 bps emergency cut.

I don’t imagine rich people buying UTVs and driving around with a 30 pack of Busch Lattes, but I suppose it trickled down from wealthy people spending money, and a chunk of the middle class got a little more upper than lower. A good concrete flat worker around here can charge whatever he wanted the last few years and still have more work than he could handle. I remember reading some articles on services inflation somewhere! /sarc

Rich people blow money on all that “white trash” crap. Maybe not billionaires but in my neck of the woods, the northwest is covered with yuppies tooling around in 50k dollar tricked out SxS UTVs.

It’s just a financial calculation: Assume you have cash that earns 5%+ in T-bills and MMFs, which is taxed income; but you can SAVE 8% in interest buy paying cash, and forgoing 5% taxed interest income, and not pay taxes on the 8% savings. It’s a very basic calculation. People with cash earning 5% are paying cash for everything now, including homes if they have enough cash. There’s a lot of that now. The 0% era caused a lot of distortions that are now getting worked off.

Great point. Thanks Wolf.

Surprised to read that about nine percent of auto loans behind in payments. A bit ominous cuz since assuming most are subprime, that seems to equal working poor.

I don’t think I ever bought a car with a loan. But I did buy a brand new Cadillac once with a credit card. It was half off MSRP and they wanted full payment today. Paid it off next day.

Last time I bought a car I asked if I could pay with a credit card (to get the 2% cash back). They didn’t let my buy the entire car but they let me put $10K on the credit card (for $200 cash back).

The car lots of the rental car companies (I know Enterprise does or did) will let you buy the whole car with a credit card. Their rental CC volume is so huge that they pay the lowest fees, such as 1%. So they can afford to do it.

Holy Shite; was the lot desperate or was MSRP hopium?

MSRP was $39K which was normal at the time (plus dealer options – sporty oversized rims, so sticker was $46K).

I paid $21K plus tax. It was CTS with manual transmission at Cadillac/Nissan dealership. Perhaps people don’t look for manual on a caddy.

Bought it without even test drive (it was inside the showroom and they’d have to remove the glass panels to get it out). I asked to replace the rims back to original, so got it the next day.

Well, the auto loan delinquency rate is not 9%: 30-day delinquency is 8%, and it’s unchanged from Q1, and in the Good Times during the pandemic, it was 7.5%, and during the bad times it was in the double digits.

90-day delinquency is 4.3%, and essentially unchanged from the prior quarter, and below the 2017-2019 range and below 2008-2012 range

Fewer than 40% of used vehicle buyers and fewer than 80% of new vehicle buyers finance. And the delinquency rates are of those that financed.

Most of the delinquencies are in the small corner of subprime. About 14% of used vehicle loans are subprime. There’s almost no subprime lending in new vehicles. Delinquency rates in the prime segment are in the 0.3% range.

I’m surprised you drag this contextless bullshit into here. You should know better. You’ll just have to wait for details until my auto debt article comes out in a day or two.

I was surprised at what I thought was the number nine which

is why I’m pretty sure I read it. By one measure it’s eight but I didn’t think it would be even that high. There are are degrees of being behind in a loan payment. Why some report said ‘eight’ if there aren’t that many seriously behind I don’t know. But I wasn’t predisposed to manipulate or cherry pick data. I think I read it somewhere but if I repeated bad data or had a memory lapse and recalled ‘nine’ instead of ‘eight’ that was an error.

TulipMania,

If this bounce does not hold for 2-3 weeks (which it may not), the next leg down will have to be a doozy.

The ‘bounce’ didn’t even hold for today let alone for 2-3 weeks and the markets are continuing on their way down globally towards much more reasonable valuations.

In the meantime the financial media are still talking about rate cuts!!!

Liquidity junkies, all of them. They would love the 0 environment when most of America is poor and wealth is concentrated at the top only.

Hopefully we don’t go back to that.

Whether there SHOULD be a rate cut is an entirely different question from WHETHER there will be a rate cut. One can argue quite reasonably that the govt SHOULD balance the budget and decree that from now on all expenditure must be met by taxes, and if budget cuts from entitlements like Social Security are needed, so be it.

But that isn’t going to happen and neither is ‘no rate cut in September’.