We don’t even want to know what debt-to-GDP looks like in the next recession when it’ll get hit by a double-whammy.

By Wolf Richter for WOLF STREET.

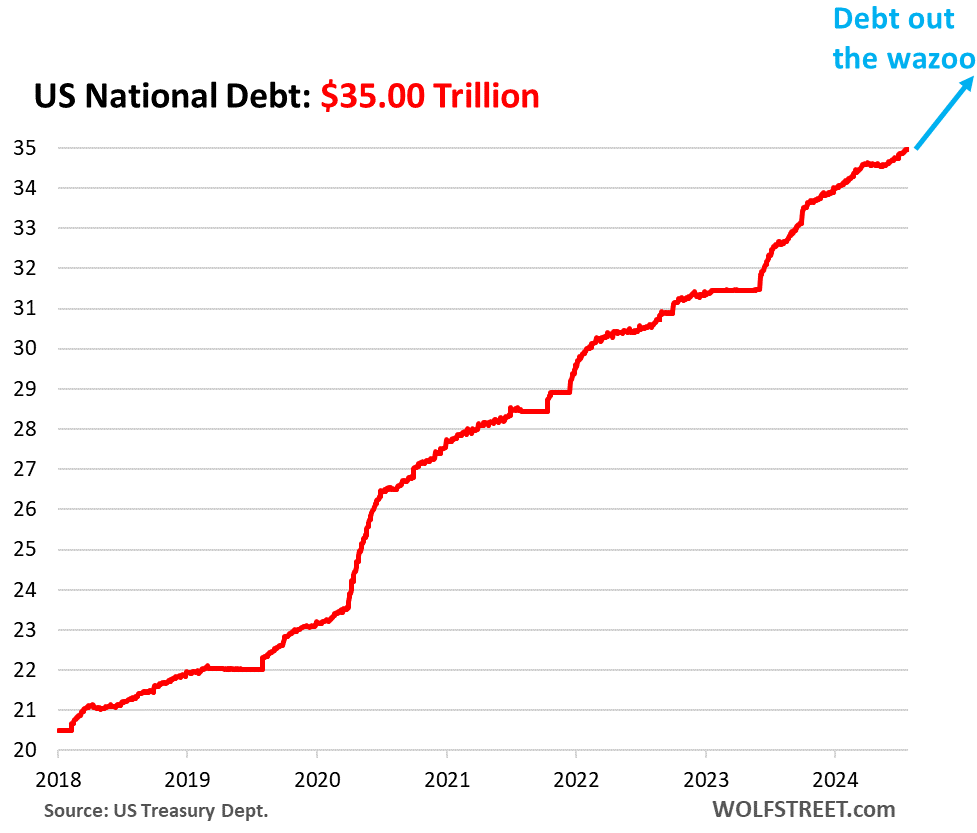

The US national debt – the total amount of Treasury securities – rose to $35.00 trillion, according to the Treasury Department on Friday. Since the beginning of the year, in less than seven months, the debt has jumped by $1.0 trillion. Since January 2020, the debt has ballooned by 50%.

The economy has been growing rapidly since the trough in 2020. Yet trillions in new debt were whizzing by so fast they were hard to see, like, “Oh wow, there went another one I think.” We don’t even want to know what this situation will look like during the next recession. But we know one thing for sure, this is nuts:

The size of the economy and the debt.

The chart above is somewhat tongue-in-cheek because the debt in a vacuum is kind of meaningless. It needs context. And the context is the size of the economy.

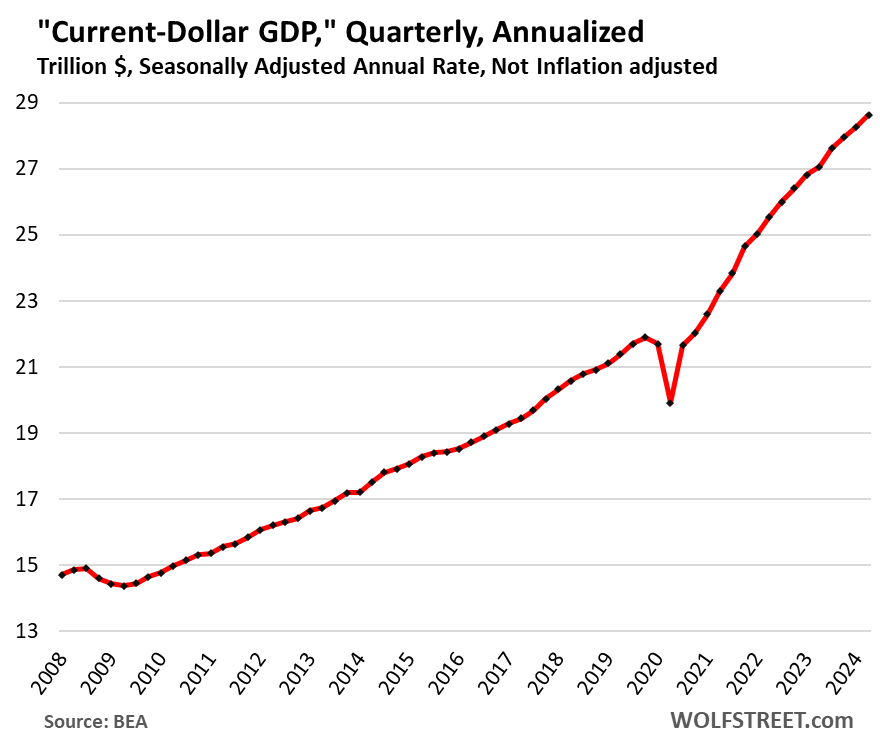

The debt is measured in “current dollars,” not adjusted for inflation. So we compare it to the size of the economy (GDP) in “current dollars,” not adjusted for inflation. Apples to apples.

If current-dollar GDP grows faster than the debt, the burden of the debt on the economy diminishes. That’s the hoped-for but for the US overall elusive scenario of “growing your way out of the debt.”

During recessions, the burden of the debt spikes because the debt increases and GDP declines – a double-whammy for the debt-to-GDP ratio.

“Current-dollar” GDP in Q2 rose by 5.2% annualized to $28.6 trillion, according to the Bureau of Economic Analysis on Thursday (adjusted for inflation, “real” GDP rose 2.8%).

Since January 2020, current-dollar GDP grew by 31%. That was a lot, see the steep curve in the chart above. Inflation had a lot to do with it. Stimulus spending in 2020 and 2021 and then deficit spending over the past two years also had a lot to do with it.

Over the same period, the debt grew by 50%. As current-dollar GDP grew 31% and the current-dollar debt grew by 50%, the burden ballooned.

The burden is expressed as the debt-to-GDP ratio, which soared from an already high 106% at the end of 2019 to 133% at the top of the spike in Q2 2020 when GDP collapsed while the debt exploded as the government was raising funds for the stimulus measures. Then an economic bounce-back brought the burden of the debt off its spike but never back down to prepandemic levels. Instead, it bottomed out at 117% in Q1 2023 and then started to rise again.

In Q2, current-dollar GDP grew faster than the debt. Quarterly estimated taxes, capital gains taxes on the everything-rally in 2023, and underpaid income taxes (including for interest income, which had ballooned) for 2023 were due by April 15. Tax revenues flooded into the Treasury in huge amounts, and the debt didn’t move much for a while around that time.

So with current-dollar GDP growing faster than the debt in Q2, the debt-to-GDP ratio dipped a bit to a still huge 121.7%.

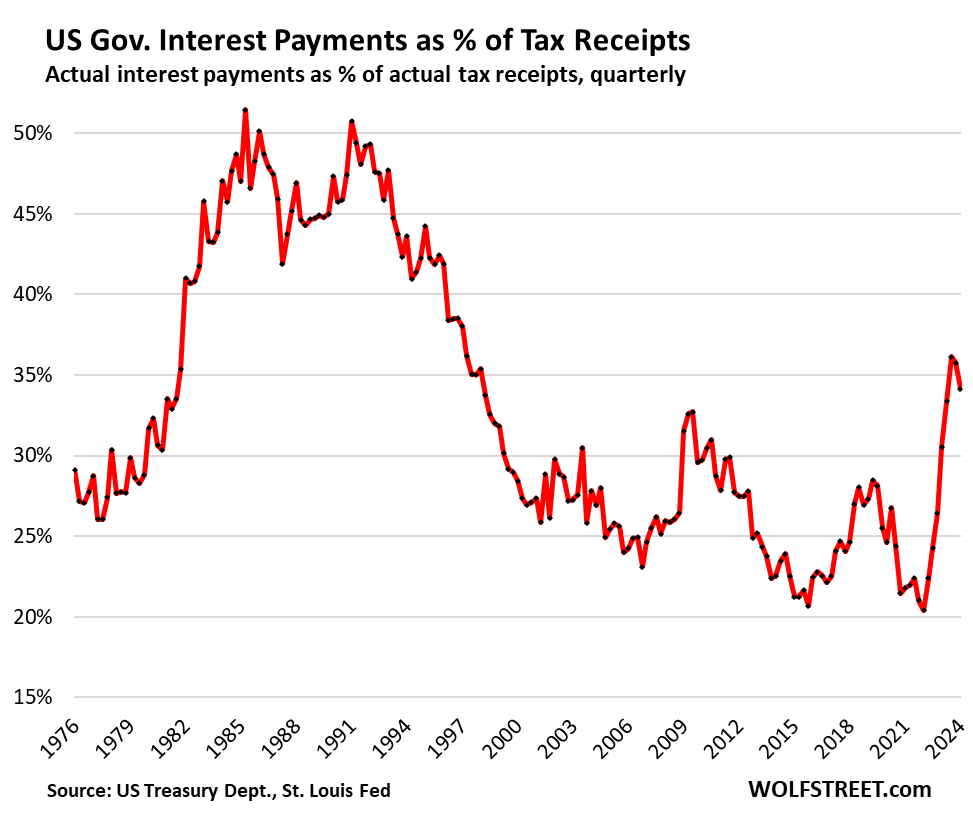

The burden of the interest payments. The relevant metric is interest payments as a percentage of tax receipts, that are used to pay for the interest. The BEA hasn’t yet released the Q2 figures for the relevant measure of tax receipts, but here is Q1 (our detailed discussion), where the ratio dipped due to the surge in tax receipts in Q1. In Q2, it will dip further as tax receipts surged through April 15. Our Q2 update will be out in about a month, so stay tuned:

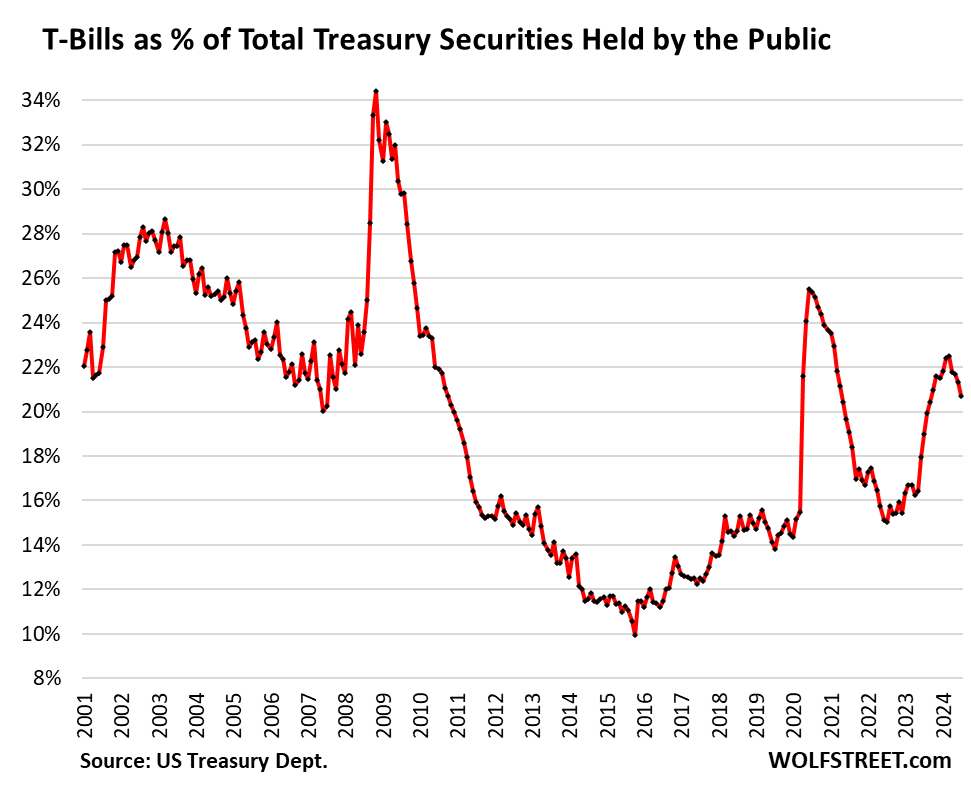

T-bills’ share of Treasury securities held by the public.

There are currently $5.76 trillion in Treasury bills outstanding. T-bills have terms of one year or less. They’re a very liquid form of interest-earning risk-free cash for holders.

The government has been issuing huge amounts of T-bills to take upward pressure off longer-term yields. Starting in the spring last year, the T-bills’ share of all marketable treasury securities outstanding surged from around 16% in April 2023 (when $3.94 trillion in T-bills were outstanding), to 22.5% by March 2024, (when $6.06 trillion in T-bills were outstanding).

In recent months, thanks largely due to the flood of tax receipts filling the coffers with cash, the Treasury Department has trimmed back new T-bill issuance, and the amount of T-bills outstanding has now dipped to $5.76 trillion.

Of the total $35.0 trillion in Treasury securities outstanding, a $7.16-trillion portion is held by government entities, such as government pensions funds, the Social Security Trust Fund, etc. This portion of the debt “held internally” is not traded in the markets.

The remaining $27.84 trillion is “held by the public.” The public includes international investors and central banks, which hold a record $8.1 trillion; plus the Fed, which holds $4.4 trillion after QT shed 41% of the pile it had added during its pandemic QE; US banks; money-market funds; bond funds; insurers; other institutional investors; and individuals.

T-bills now account for 20.7% of the Treasury securities held by the public, down from 22.5% in March.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Glad to hear that the US debt is rounded to the nearest billion, I was worried there for a minute…35 trillion sounds like a lot…

As a friend of mine once said: “a trillion here, a trillion there, and pretty soon you’re talking about real money!”

That was a paraphrase of a famous quote a few generations ago by Senator Everett McKinley Dirksen, R. Illinois, using the word “Billions” rather that “Trillions.”

At that time,let’s say 75 years ago, my grandfather in central Illinois said people weren’t used to seeing amounts greater than hundreds of thousands of dollars, so a billion dollars would have sounded like a nearly infinite amount.

aging in AZ

Yes – I’m dating myself but I’m from Illinois :)

It sounds like a lot, but only twice the value of 7 biggest companies. And if those 7 disappear, you wouldn’t even notice.

andy – context, thank you.

The entire S&P 500 has a market cap of $46 trillion. One year ago, that market cap number was $37 trillion. I guarantee you that if $35 trillion in market cap disappeared, you would notice.

$35T in debt is what can happen when you spend more than you make in 49 of the last 53 fiscal years. Sounds like a giant Ponzi scheme to me. Pay off old investors with money from new investors.

Yes, but everybody is in it.

Not everybody. I am not in it. I dont ride ponzi schemes no matter the (temporary)profit margins or (so called)guarantees.

uhhhmm.. steve?

i think you misunderstand.. being ‘in it’ or ‘not in it’ is not a matter of whether YOU personally live ‘within your (own) means’.

you pay taxes? then you are ‘in it’.

you receive any type of gov’t benefits? you are most definitely ‘in it’.

the only way you are NOT ‘in it’ is:

if you live completely independent of needing anything from others (society).. energy, food, water, shelter, etc.

i seriously doubt that is your situation.. i mean, that you are commenting on this website using the internet kind of gives it away..

body-less-one has it exactly correct IMO!!!

While the ”back to the land” movement in the EARLY 1970s was a heroic effort to not only become independent of the USA GUVMINT that some folx were absolutely sure was about to disintegrate due to various and sundry and extensive forces,,, only one guy I met did it,, and only for a short time…

He WALKED, with a large backpack, about 10 miles into the far reaches of southern Humboldt county,,,, grew his crops,,, and walked out to sell those crops…

Needless to say, the guy, living alone, was not only very ”handy” in SO many senses of that word,,, but very very hard working EVERY day…

Good Luck and God Bless everyone who might want to be out there on their own!!!

I assume the “crop” was pot, which was/is heavily grown in off-the-beaten-path hard-to-get-to regions of Humboldt County. That was/is apparently a pretty good business.

“Pay off old investors with money from new investors.” Sounds vaguely like the definition of a society? But I know, the rate of that payoff matters, and can unravel the scheme.

Sounds more like a ponzi scheme. It will not work long term

All debt works that way. The housing market works that way. The entire stock market works that way.

If you want to sell some shares to get out of them, you are the old money. And who the heck do you think will buy them from you? The new money, LOL. The new money always pays off the old money. This difference between what the selling old money thinks about the shares, and what the buying new money thinks about the same shares is precisely what makes a market.

Debt is constantly rolled over. And it’s normally easy to roll over. Old money gets its money back, and the new money piles in for the opportunity to earn a yield.

There are two types of capital:

1. Equity capital — you don’t get your money back from the issuer; to get out of these shares, you have to sell them. Equity capital cannot default, it just goes to zero.

2. Debt capital – the issuer promises to pay back your money at the maturity date, plus interest along the way. Corporate debt capital can default, and then what you get depends.

Governments don’t issue equity. They issue debt. And because a country that issues the debt in its own currency cannot default, the yields investors accept are lower than the yields on corporate debt, whose issues can and often enough do default.

The Confederate government didn’t default but it’s bonds were worthless.

And when you never pay off any of the debt. That is why gov’t programs are always money losers.

I wonder how much longer T-bills will be considered “risk free”.

Longer than you will be alive, for sure. So don’t worry about it. While you’re here on this earth, they’ll be risk free.

Wolf, I am reassured by your unqualified statement that T-Bills (applicable to Treasury notes and bonds?) will be risk free for a long time, particularly since you are orders of magnitude more knowledgeable than I am. But I am curious, what is your reasoning for your assessment which is, after all, a prediction about the future rather an analysis of data from the past?

If a country issues debt in its own currency, credit risk is zero because the country can always issue more currency to pay interest and principal on the debt.

A country that controls its own currency can never default on its own currency debt – by definition.

People have to get a grip on this.

Argentina didn’t default on peso bonds; it defaulted on USD bonds, and it cannot create more USD. Greece didn’t default on drachma bonds, it defaulted on euro-bonds, and it cannot create euros.

Countries can create inflation. But inflation is not credit risk. Those T-bills will be good regardless of what inflation will be. And as inflation goes up, T-bill interest rates go up. Since T-bills are short term, such as one month, or three or four months, and at the most 1 year, their value changes little when interest rates rise. So that’s not much of a risk either — and it’s not credit risk.

These drive-by one-liners about T-bills being risky or whatever are just silly.

In theory could the federal reserve refuse to print the dollars to fund the government if inflation gets out of control?

No, because the Federal Reserve Board of Governors (headed by Powell) is an agency of the federal government, all its employees are employees of the federal government, and its seven Board members are nominated by the Prez and confirmed by the Senate. It IS part of the government.

But it can and will hike interest rates if inflation takes off. Inflation will diminish the burden of the debt at the expense of the holders of longer-term Treasuries. Inflation is always the solution to over-indebtedness. T-bills keep their value and earn the higher interest rates as interest rates go up. Floating rate notes also keep their value as their interest rates go up. TIPS and ibonds are also inflation protected. But regular longer-term securities are not inflation protected.

Then at peak interest rates and at peak inflation, longer-term bonds will be good buys. But no one will know when “peak” is, and everyone will be too scared to buy them, and their yields will blow out and prices will fall, and that will be precisely when to buy them. Make sure they’re not callable though. There are no callable bonds issued currently. But there were, and in 1981/2 with rates and inflation at the peak, some crazy people bought 30-year bonds with a 15% yield because normal people were too scared to buy them. Those that weren’t callable turned into the deals of the century: a 15% yield for 30 years without credit risk. But those that were callable got called, and it deprived investors of the gains. It caused a huge stink, and the government then stopped issuing callable bonds. But if inflation takes off again, the government might start issuing callable long-bonds again and get away with it, because the people that got burned will have retired or died by then, and no one will remember.

My investment advisor at Fidelity advised my against too good to be true callable CD’s last week.

There is caution in the air.

“There are no callable bonds issued currently.”

Some agency bonds are – my 10 year 5.98% Fed Farm bonds were listed as callable when I bought them.

On the off chance rates do go down, I’m guessing this agency doesn’t want to be locked in to paying me almost 6% for the next decade.

Sure. For example, ALL agency MBS are callable. But we’re talking about Treasury securities, not agency securities. There are no callable Treasury securities being issued.

Is that still the case if Congress refuses to increase its debt limit? We’ve seen that play out a number of times recently (walking to the edge of that cliff, then stepping back at the last minute). But as Congress gets more dysfunctional, if they were to refuse to increase the debt ceiling, and the USG had to choose between paying SS, salaries, or interest on the debt, would that effectively lead to default, or would your original statement still apply that the US could just create more currency?

Not sure if I’m conflating two different topics (currency in circulation and debt ceiling), but a Google search of this topic just leads to the same doomer sites that rave of USG default and they’ve clearly got a biased agenda that isn’t conducive to answering my question.

“if Congress refuses to increase its debt limit? ”

Congress IS part of the government. The debt ceiling is just a charade that exists to extract political concessions from the other side. So the answer is no. They’ll go to the limit, and maybe go over the limit by a day or two, and then the stock market crashes right in front of them, and they’ll fix it. That has zero to do with fundamentals.

IMO there are two risks:

1. Excessive short term debt issuance keeps short term interest rates high, so the fed cant reduce rates and we careen off the recession cliff at some point.

2. Yes, the local currency debt doesn’t default, but the risk is excessive debt debases the currency through inflation and the “real” value of the currency – goods purchasing power, shrinks.

To me those are very real risks.

What if the US government committed to a $17 trillion clawback of tax cuts over 8 to 10 years? Would that do anything to stabilize our economy?

Granted, it might slow our economy, but it might stabilize it and bring long term confidence back to the US economy and the US dollar.

I’m saving this comment for the future.

Risk Free is the wrong term, as Wolf knows full well:

VERY or ULTRA LOW risk is the correct term for USA treasuries,,, of which WE, in this case the family WE, have about half our liquid $$, the other half in CDs of similar yield.

How long we are able to continue either is now a very good question, eh

If the gov’t stops paying back principal on its treasuries, we’ll all have much bigger problems to worry about than the balances of our portfolios.

@JS,

They are barely “risk free” today, and were definitely not “risk free” from April 2020 to April 2022. Inflation risk during that period caused huge losses. And as you know, considering Treasury bonds instead of bills, anyone buying a 30 year Treasury on March 9 2020 and selling on November 1 2023 lost even more money to Interest Rate risk. Under “normal circumstances”, US Treasuries are indeed risk free. The only problem is that “normal circumstances” is a theoretical concept that doesn’t exist in the real world. When the dollar eventually plummets, the currency risk will be a killer, due to price inflation. Your best bet is to curl up in a ball in an out of the way dark place. That has been my strategy.

Inflation affects ALL assets the same way: their prices all lose purchasing power at the rate of inflation. The only hope you have is that the yield or price gains are bigger than inflation. Inflation isn’t a risk only to bonds, it’s the same risk to everything, including your wages. But here, the discussion is about CREDIT RISK. It’s the CREDIT RISK that is zero with T-bills, meaning that you will get paid face value when they mature. And you will. And that includes the interest.

I totally agree. Investmest risk was an addendum.

Cleanest shirt in the dirty pile

We are all on the entropy ride. Death and taxes are mere lesser manifestations of its greater certainty. So, how we manage the path is all we can aim for. As I see it, walking is sort of like managed falling forward. The secret for me is to do it gracefully and without undue panic. With all its weirdness, the USA could be doing a lot worse on this, considering all the moving parts involved. Our financial system is quite elegant and has been very resilient, for the quality of life of hundreds of millions. All relatively.

I agree.

That is one way to look at it. The other way is to question why the wealthiest country in the world can’t provide basic things like affordable and quality healthcare, education, shelter and other basic necessities while 1% of the population controls 31%(rounded) of the wealth. We could of course be doing worse but we could also be doing a whole lot better. Admittedly I don’t see a path out of where we are at in the foreseeable future as 2 centuries of poor choices can’t be undone quickly.

Glen: “why is the wealthiest country…..”

Answer: we could. It would take an educated voting population to do it. It would take a majority of voters to stop voting against their own best interests. It could be done. Bringing back post WW2 tax brackets would be a start.

It’s the greedy self serving “educated” that’s got us into this mess…try again.

The educated are the best thieves, they make the best wolves and their lies are most spectacular.

If only the stupid people were smarter…

The educated are blinded by their own ignorance.

Oh, Louie, you are hilarious! “An educated voting population”? You are talking about the USA not Uruguay (a country which actually does have an educated voting population!) You should be a stand up comedian with zingers like these. An educated voting population!

Those propounding the elegance (shudder) of our financial system are probably inspired in no small part toward Panglossian overture because they’ve benefited handsomely from it themselves.

I’ve also enjoyed a fairly salubrious go of it — maybe even better than I deserve. I have been lucky. READ: I’m not coming from an aggrieved vantage point when I say that I see our system as a grinding negative sum game that’s gradually bled the landscape of its splendor and its people of their poetry, humility and the basic smarts enough to know when to stop. It’s built on too much concrete and plastic by greedy nepotistic boneheads who use sports analogies in lieu of philosophy and literally worship money. It’s a system that has helped create legions of human blight and treats the planet worse than a public toilet.

It’s amazing that any of it works at all.

We could take care of a lot more if we only allowed citizens to partake in the largess.

Government “providing” most of these things is not or should not be the goal, it should be providing secure borders and national defense, and basic K-12 education, and then allowing these other things to happen with the least possible intervention. Kind of what we had prior to FDR.

” why the wealthiest country in the world can’t provide basic things like affordable and quality healthcare, education, shelter and other basic necessities.”

A good part of it is due to private equity. They are now buying up hospitals, nursing homes, Emergency room corps. and other medical practices. Many of those organizations are having quality of service problems. For a much deeper look see Gretchen Morgenson’s book: These are the Plunderers.

only because you ”believe” ph,

Entropy is just one more ”theory” of how things work…

While it is still ”mostly” popular with the theoretical physics folx at this point in time, that is because of the fact that physics is still in early times… think only of when our most basic physics ”laws” were known if you want any confirmation of we are in the early times…

Mostly, these days, IMHO, THE most important thingy for most folx is to cultivate community…

Good luck for ALL Wolf’s Wonder readers and commenters!!!

Prettiest turd in the septic tank?

Exactly. People who have never traded FOREX don’t understand.

You wish! There are a few countries with a cleaner shirt and the biggest country is germany with a debt-to-GDP ratio of ~ 65%.

The prettiest horse in the glue factory?

What a mess. $35T and growing at $5-8B a day. That’s someone’s contact, salary, benefits. This economy is wholly dependent on that daily debt injection or the gears grind to a halt.

Its going to take a steady effort for many years to turn this around as far as reducing the debt to GDP ratio and debt payments as a percentage of tax receipts.

Fortunately the 10 Year Treasury was 5% in October 2023 and now is around 4.2%, and has averaged around 1.5% greater than the annual inflation rate over the last 30 years.

We shall see what happens when the Trump tax cuts expire next year, and if there is a compromise as far as allocating tax money to reduce deficits and the debt load.

Hopefully this also leads to federal government spending increases being kept just below the annual inflation rate.

I’m interested as well as basically individual tax cuts expire and impact can be significant and drive decisions on everything from Roth conversions to taking RMDs and of course this will essentially be a pay cut for many individuals or perhaps just less money for living if people prefer it defined that way. Read a few good articles but really all depends on Congress of course.

It’s going to take the elimination of lobbying. Nothing changes until legislators are no longer bribed. That environment brings in the worst of society to manage our country.

Sounds like a bunch of overpaid wazoozs.

A lot of those dollars are going to doctors through Medicare, Medicaid, Tricare and Obamacare.

Manipulative BS. These programs are self-funded by the FICA deductions that employees contribute to them. And they have accumulated surpluses.

Doctors get peanuts. The “not for profit” hospitals and the insurance companies are the beneficiaries of our very sick health system.

I believe Fica funds medical programs Medicare and medicaid which will require general budget revenue in 5 years as it uses its trust funds until that is fully drained in 12 years. Other medical programs come from general funds but do include some extra funding from Obama care special Capital gains surcharges. Like most things we still spend lots more than we bring in. One problem is that in general the elderly get a few times more from Medicare than what they put in so we are all at fault. Health care is a growing part of our 2 trillion dollar budget imbalance that is nearly impossibe to solve politically.

You are misinformed. In the US, only 20% of health care spending is on physician services (including mid level providers). The real problem is hospital spending. You could cut physician reimbursement in half and our health system would still be far more expensive than any other country.

I am biased based on my career choice but I can attest these dollars go towards (unnecessary?) testing that keeps docs out of litigation and mostly administrative salary bloat and fancy clean facilities and disposable sterile sh*% that we may or may not need to be so fancy and disposable. They don’t go wholesale go towards the docs pocketbooks.

Plus the docs crap I just learned about from wolf :)

The US has 35T in debt and 4.4T in yearly receipts (2023). Like someone who makes 44k per year with a 350k mortgage. And the country has a good credit rating so pays 4-5% for its money. Do I have this right?

Yes, but add one thing: you can without question borrow whatever you need to make your monthly mortgage payments forever without it effecting your ability to buy whatever else you need.

Comparisons of the government to individuals is a bit apples to oranges but of course get your point. Until the dollar loses its hegemony it can do this and doesn’t appear this will be something in my life time but wouldn’t bet on that for my teenagers. That wouldn’t imply anything happens to the dollar but yields might have to go higher.

US dollar hegemony? Isn’t that what BRICS is trying to undo for their own selfish purposes? Too many sanctions do create a blowback.

Why is a block of countries acting selfishly to not be at the impact of US sanctions and settle accounts in their own currency? Some might call that self determination. I am rooting for BRICS as the level of intervention is significant when you control the flow of money.

Countries have always been able to settle their accounts in whatever currency both sides agree to. The problem is that there are a lot of garbage currencies out there that get rapidly devalued, or that cannot be freely traded due to capital controls, and no one wants to have anything to do these currencies, so they cannot be used for trade because no one wants them, and so a third currency makes a lot of sense and takes risks out of the equation. The euro is a huge trading currency outside of the Euro area, paralleling the USD.

Yep. But they also have about 1.9 million of equity property they own on that 350k debt. (Government buildings, land, mineral rights, etc)

Columbus would have raised a brow to know this great discovery would owe such a sum.

.. Those were the days, sailing the ocean on the wooden ships…want something, you go and take it and put up your flag….shake your groove thing.

Kind of weird to have fond memories of genocide.

Not fond. I’m a descendent of an old Indian taxi driver.

The lives of the millions of Indians, just because they didn’t want to pay rent.

I think the country was free then?

Just the view from my window here on my reservation….no complaints, just happy to have a phone and Wolf street.

Since the beginning of time, that’s the way things worked. Read history.

Show us a country anywhere on earth where this is not the case. Human history is basically built on conquest especially before 1900.

Perhaps less surprising than you think: Charles V and Phillip raised large sums through the issuance of municipal bonds backed by tax revenues on Spanish possessions, facilitated by Columbus’s countrymen in the Genoese banking community.

During the period of historically low interest rates, particularly from 2020 to early 2022, many U.S. homeowners took advantage of 30-year mortgage rates below 3% to refinance their homes, securing long-term fixed rates. Concurrently, the U.S. Treasury, under Secretary Janet Yellen’s leadership, pursued a strategy of shortening the average maturity of government debt by issuing more short-term Treasury bills relative to longer-term bonds. This approach, while potentially offering short-term savings, exposed the government to increased interest rate risk. As rates have subsequently risen, this strategy has led to significantly higher borrowing costs for the federal government. The long-term fiscal implications of this debt management approach warrant careful analysis and should prompt a reassessment of Treasury debt issuance strategies in the future.

Hi Michael: Thank you for sharing your thoughts. You are clearly well-versed in finance. One only needs to look at other countries who have attempted this strategy with their debt issuances. They usually do it because they are afraid that nobody wants to buy their long term debt. If I were sarcastic, I might be tempted to call this “banana republic” financial behavior. And, as you astutely pointed out, it increases the volatility of the entire U.S. debt structure.

“We don’t even want to know what debt-to-GDP looks like in the next recession when it’ll get hit by a double-whammy.”

This is the forward looking question….When the recession hits will we go to the same playbook of rate cuts and government spending? Will it even work and if so will it lead to more inflation?

Perfect recipe for stagflation IMO

Consider yourselves lucky. Little Britain has an even higher debt to GDP ratio, still running at +5% inflation and an economy that is hovering around 0% growth, headlines if it reaches 0.1%. A true definition of stagflation and its politicians don’t have the faintest clue how to fix it.

Same could be said of several countries in Western Europe. After WWII many countries had very high GDP to debt ratios. It took about 10 years to resolve. The prescription was high inflation coupled with severe austerity – rationing continued for almost 10 years after armistice. Something similar may be required in the not too distant future.

For what it is worth, rationing did not end completely after WW 2 in the USA until June 1947.

There was talk of rationing gas in 1974. But that was dropped after they had already printed the ration coupons. If you are feeling nostalgic, you can sometimes buy one on Ebay.

Captain,

I have some of my WWII ration books left.

Could they be of any value?

I recall that being a headline today – so clueless even the newly elected pols admitted as such.

Our future?

I think that Little Britain refers to the smaller island of Ireland divided between the republic and the UK constituent of northern Ireland. Great Britain goes for the larger neighboring island that is home to England, Scotland and Wales. I do understand your slight but considered it pertinent to offer this clarification.

That is not correct. ‘Little Britain’ is scathingly used by some German politicians to belittle what is presently called the UK, or Great Britain.

HOW BAD AN IT GO?

One asks how much of income interest payments can increase without tanking the economy, either with a recession due to spending cutbacks or unbridled inflation. Or both.

For this look at the chart giving “interest payments as a percentage of tax receipts” and you will find it has been above 50% twice yet it came back down before the economy broke.

At about 34% it is nowhere near what it has been. For this I feel good.

While the chart on “the debt-to-GDP ratio” shows it hitting an all-time high does this really matter when interest payments are well below the historical maximum?

Also consider how many other countries, such as Japan, have much higher ratios (but do you want a Japanese growth rate for the US?).

Now when both charts hit all time highs is a time to worry. Will we find the will to contain the deficit enough to keep this happening? Lets ask this question in a year after the next election.

The economy is trading money for goods and services. The more of this activity (the more money spent for goods and services) the better the economy. How does higher interest rates change that? Interest rates are just the transfer of money from one spender (the borrower) to another (the creditor). There’s no change in ability to spend.

Now the problem may be on who each individual is. If the the borrower is middle class Joe, then there will likely be less spending on cars and houses, reducing that part of the economy. And if the creditor upper-class Trevor, there is likely to be more spending on stocks and debt instruments (and yachts), increasing that part of the economy.

try upper class is Joe spending on kids and grandkids who are barely getting by. People love their kids more than the next yacht I maintain

but children of older Joe are struggling more than you and I did and there isnt a great solution so the old Joe helps out. this is what I see around here. Not very sustainable long term for community and family construction of our society but certain groups have a grudge against all that anyway.

In my old age I am financially comfortable and I do not want for anything that money can buy. My seven children are all far wealthier than I am, in some cases astoundingly so. I doubt there are many who are in the situation you describe Joe in.

Escierto

With luck you and your family can stay healthy and live long fulfilling lives.

Congratulate yourself on raising these beautiful children…

Money is good … decent caring people are also good. Look again what JoyMickey said.

“There’s no change in ability to spend.”

Not sure I agree with this – the whole point of buying on credit is to spend more than your cash-on-hand. Higher rates are supposed to increase the cost of spending more than you currently have.

Wolf,

My understanding is that the Federal Government unfunded liabilities are 6-8 times the size of its Debt. True?

And if the Federal government had to present its balance sheet including the unfunded liabilities like a corporation does, what would it look like?

There are more;

federal debt obligations like guaranteeing mortgages ( FNMA , FHLMC & GNMA) , student debt ( Which this government wants to absorb for all taxpayers to pay)

It appears that the tether between government deficits and taxation has been cut. That the belief in “we can’t default on the our debt “has given government a belief they can do anything.

What is the end game?

More can kicking until sometime in the future it blows up?

The whole discussion about “unfunded liabilities” is ignorant bullshit. It assumes that everyone retires today, regardless of age, even 25-year-olds, that all companies shut down today, and that no one works anymore ever again and that no one contributes to anything anymore ever again, and that no one pays any taxes ever again, and then the amounts to be paid in all future years, but with future funding cut to zero (because there would be zero workers) would be the “unfunded liabilities.” It’s just pure ignorant bullshit. Comments of this idiotic nature routinely get autodeleted.

When I talk story with friends I always feel like citing this stuff like it’s some scripture… but try to I hold back… a little bit. And just say read this site :D. Thanks for expanding my brain.

Any discussion on Unfunded liabilities are “ignorant bullshit” ?

Welp, that’s helpful

I also explained why. All you have to do is read the comment.

Amen, brother! I wish more people would think about what the phrase “unfunded liabilites” would actually mean, but unfotunately they don’t. In fact, due to the nature of how capitalism actually work, it is abundantly clear that “unfunded liabilities” is a nonsense statement. The world never “runs out” of money. People take out loans to create more money every single business day, and capitalism falls apart complely without that mono-directional expansion.

Unfunded liabilities is like what I had in 1987 with a 200K 30 year mortgage at 10.5% and a 30K/year salary. $2500/month with insurance and property taxes.

It got paid and I didn’t panic and walk away.

Time and inflation eventually heals all debt. I don’t make 30K/year anymore and I doubt many do.

you doubt many do?

based on what exactly..

the median yearly income in the US is around 45k / year. the average is often skewed by large outlying numbers, so it is higher.

but that median is not far away from the number you cite.

there are still plenty of people making 30something k / year even today.

also, i wonder.. how ‘it got paid’ as you say?

2500×12=30000

so you paid no taxes? you didnt eat for the whole year, or were able to do so for free? you walked everywhere? you didnt use any electricity or municipal services, or got them for free? etc etc etc.

pretty mind boggling id say.

His parents paid, he left that part out.

I’m not understanding your math – so your monthly PITI payment was 86% of your pre-tax income? How does that work?

The sepia tones of an aging mind begin to twist reality.

Uphill both ways, and probably nobody doing worse than my 7 kids (Escierto).

Thankfully the homeless population in Ca. Is legislatively going to zero.

As long as mass incarceration remains Big Business, we’ll never have a social issue in our country (same as it ever was!)

Phew!

The capacity of the U.S. government, to meet its obligations is, and will remain, dependent on the taxing and borrowing capacity of the U.S Government.

Debt-to-GDP ratios are obviously contrived metrics. Unprecedented large deficits “absorb” a disproportionately large share of N-gDp (as gov’t spending is a component / factor of gDp).

To appraise the effect of the federal budget deficit on interest rates, it is necessary to compare the deficit, not to the debt to a GDP-ratio (a contrived figure), but to the volume of current net private savings made available to the credit markets.

“To appraise the effect of the federal budget deficit on interest rates, it is necessary to compare the deficit,”

Nonsense. The deficit is a government accounting entry. The changes in the debt is the actual result of the actual difference in actual spending and actual tax receipts.

The critical measure is “interest payments as percent of tax receipts,” see fourth chart.

Net private savings are lower than government outlays.

wolf,

in an earlier comment here.. you said:

“If a country issues debt in its own currency, credit risk is zero because the country can always issue more currency to pay interest and principal on the debt.”

a ‘deficit’ is a ‘piece/part’ that contributes to the debt, which is the aggregate OF ‘deficits’..

but concerning what you said before,

credit risk isnt zero just because a country ‘issues’ debt in its own currency, and can simply issue more currency to pay the debt.

clearly that isnt true, with the most recent example being: zimbabwe.

but aside from that.. in the purely conceptual sense, why bother with debt at all? a country could just print whatever it wants currency-wise and buy everything or give it out ad infinitum.

am i misunderstanding something here?

“clearly that isnt true, with the most recent example being: zimbabwe.”

Bullshit. Zimbabwe didn’t default on Zim dollar debt. It defaulted on foreign currency debt.

“am i misunderstanding something here?”

Yes, everything.

@ Wolf –

What happened to that Zimbabwe dollar debt? Does it still exist? Has it been accumulated y Goldman Sachs or Howard Marks, awaiting a repayment program?

What has happened to the Zimbabwe dollar that denominated that debt? Does it still eist? Does it have any trading power? Does it have any purchasing power? Is it government(Zimbabwe) backed for the payment of of debt and taxes?

I worry that the recent relief in debt/tax rev is just a function of tax season earlier in the year, and this ratio will resume its uptrend in Q3 and Q4.

“… will resume its uptrend in Q3 and Q4.”

Correct, it will. The April 15th tax take was huge this year. But there won’t be an April 15th in Q3 and Q4.

Right. Through the first 9 months of FY ’24, we’ve brought in $3.75T with a deficit of $1.27T. We probably will bring in another $1T at most in revenue, while the deficit is expected to hit $1.92T. Let’s do the math: 1.92/4.75 is 40%. And, the problem is this sort of % is now a structural issue.

I like your BS analogies. Mine is this. It’s BS to compare almost anything revenue or tax related to GDP. IMHO, it assumes that there’s this HUGE pile of money just waiting to be tapped into which, again, is a big pile of BS. We won’t just tax our way out of this. Far from it. What matters is the debt to revenue ratio and right now and well into the future, this is a really big problem. And it will only grow worse, especially when a recession arrives.

People who post on WS.com and say the debt is no big deal, because we print out own money. They’re completely wrong. We’ve entered into a super cycle whereby inflation is going to run higher than the Fed’s core PCE target of 2%. The final analogy is to nuclear fusion, which has ALWAYS been 30 years out. Well, nuclear fusion and our debt crisis are NOT 30 years out anymore. Far from it.

2030 seems to be a good estimate of when the old saying of yield always solves the demand problem. Well, yes of course it does. But what happens when the bond market expects 7%+ yield on short-term treasuries which is probably not that far down the road?

“But what happens when the bond market expects 7%+ yield on short-term treasuries”

We’re at 5% now and nothing bad has really happened.

A monkey can have a booming economy by spending government money without limit.

It’s all about inflation vs a depression……since in modern US political economics the depression is avoided until the last breath…..it’s inflation.

No one knows where the breaking point for the US dollar will be……but…..it does have a breaking point.

I am not one that thinks we are all going to be shoveling coal some day. I do believe that at some point or another, without a course correction, we may have to adjust our living standard…..with the caveat that since I believe in the power of technology (AI, Quantum, Fusion, etc) there is a good chance a hyper inflation never comes to past.

IMO the danger of the deficits is the loss of control of the dollar. The emperor may wake one day without clothes if the deficits do not adjust.

The US government is behaving in a manner that leads me to believe that they want the US to lose reserve status. After all……China, Russia, India and Brazil are no longer just four shit hole countries. We may have to get used to more than one system leading the world and out leaders may understand our place better than. we do.

If we lose reserve status…..OK…..yes there might be inflation…..or maybe not……

either way lots of jobs, lots of profits for our corps, lots of government revenue to pay for things like SS……its just the inflation….but what if the US lead in technology counters the inflation.

No one knows the answer to these questions except some genius folks in the NSA. As my daddy used to say……never bet against the Yankees……some day they might screw it up but most of the time they know what they are doing even if you can’t understand it.

I am positioned for continued higher inflation over the next few decades because of lots of reasons…..the deficits are one reason…..and some inflation is not all that bad as long as it’s moderate…..not hyper.

Unpopular opinion: the dollar will not lose reserve status due to inflation (hyper or otherwise).

If the dollar does lose reserve status, it’ll be for the opposite reason: dollars becoming so scarce on the global stage that it doesn’t make sense for foreign countries to hold them anymore.

Yeah, we can borrow as much money as we want. the Debt doesnt matter so much because GDP is keeping up thus saving the ratio. What exactly is GDP ? To the degree it’s production of stuff then the “economy” must be healthy.

However I keep reading thing like the story of the new US Navy Frigate program. Brought into existence because of the failed 40 billion dollar LCS program characterized by 5 year old ships that can’t perform their missions being retired.

So the answer is the Frigate program. Select an established design that is being built and crank them out at 800 million/copy. Such a great idea. But now we find that our very productive and growing economy is unable to build these ships. Of course the Navy tinkered with them a bit. But the 800 million dollar ships are now costing 1.3 billion and running 2 years late. The navy blames it on problem in the ship yard workforce related to Covid.

At the same time production of Virginia class fast attack boats has declined from 2 boats per year to 1 due to the same issues with labor force, supply chain and inability to replace skills of workforce retirees.

Delloite was recently given a 2.3 billion dollar contract to help figure out how US shipyards can find 100,000 new workers with the skills needed to build stuff.

Nobody yet is suggesting the obvious answer: build the ships in Japan and Korea.

We can see the same “progress” in aircraft production. We all know Boeings problems, now spending Billions (mostly in stock but also cash) to buy back Sprit Aero Space – the outfit “professional” management spun off many years ago (no doubt earning big bonuses in doing so) – which builds much of the fuselage but does not seem to be able to build them well enough.

Regardless, Mr. Wolf is doubtless correct and this prosperity can go on for years if not decades. There are still other balance sheets in the world that can be plundered….are you listening Europe ?

10 year debt increase rate %

1971-1981 = 246

1981-1991 = 359

1991-2001 = 166

2001-2011 = 247

2011-2021 = 197

Applying the past average of most 10 year periods to the future:

2031 = $68.4 T (total US debt)

Where, what, why, how, and when the debt is used is what Wolf does a great job of illuminating. The actual amounts while important in the grand scheme of things, the fact is we are able to handle the growth rate so far, albeit not without consequences.

Increasing by a constant % will cause the value to grow exponentially.

I don’t think we want that for our nat’l debt – especially given pop size isn’t growing at a similar rate.

I agree wholeheartedly.

I failed to make my main point which was that while debt is increasing at seemingly unstable rates, the nuances of when, where, how, etc. that money is produced by the FRB provides a certain level of stability that is surprising to me.

///

Newtons first law stipulates that no change can occur unless imposed on the object itself. If one wants to see a change, one must act upon the problem.

If you ask me, after setting a strong QT course, the managing of this debt monster would be my priority.

///

Wolf, I’ve been reading your explanation of how the US can never default on its own debt because it is in our own currency and has the Fed its own bank to print it. But my question is, what’s the problem with other countries doing the same? Why can’t they have their own banks to print money and take loans only in their own currency?

No one would give such loans.

Countries do raise loans in own currencies but FEX loans are required to pay off maturing FEX liabilities and interest thereon. And the most popular FEX loans currency is the USD due to its unique global status in trade, investments, reserves etc. that also spills over into debts, foreign aid/assistance and even under the table activities or outright global criminal transactions.

Other countries’ currencies aren’t the world reserve currency.

Can someone explain to me what the hell is wrong with the bond market? This SHOULD be getting more of a reaction.

I also noticed that both presidential candidates are proposing massive increases in government spending (unfunded of course)– one side, restarting the Reagan era Star Wars project, and the other huge Medicare and related enrollment expansions.

Long term treasuries have been in a bear market for over 4 years, and no one cares. There is only political appetite for deficit expansion.

Can someone please explain to me why the bond market is so slow to react to this?

Howdy Tulip. Long term bonds will probably rise in the coming years. ZIRP is hopefully dead for decades. Inflation is probably just getting started. The new president and new congress will increase spending. They always do. Good Luck

Bond prices are INVERSE TO YIELDS (interest rates) and when yields rise then bond prices fall. If there is inflation ahead that would be priced into yields causing bond prices to fall accordingly.

Howdy SoCal. Which type of Bond?

Already fallen significantly since rates started going back up again. Hundreds of billions of dollars of unrealized losses are sitting threateningly on banks and FED balance sheets and are hampering other core commercial banking functions.

Bonds/Bills/Notes are issued by DC, states. districts, municipalities and by others. Corporate Bonds and those issued by large commercial banks are further large segments of the bond market. A number of Bond types are in circulation including convertible bonds that can be converted into shares. So a lot of paper is floating around in the form of bonds. Bonds based derivatives also have a large and risky presence.

Almost all such paper has been adversely hit by rates rising primarily to fight inflation but also to sweeten the flavor of the ever-present Treasury Bills offerings.

All bonds of any type work that way, Bubba.

The last bond bear market lasted nearly 20 years (early 60s to 1981).

Yields have a lot more room to rise.

Recent blurb from FT that probably doesn’t fit into deficit discourse relating to Treasury issuance related to budget:

“Here are Bank of America’s estimates for 2024 and breakdown of debt issuance over next few years. As you can see they estimate that bills will account for about 40 per cent of net Treasury issuance this year (zoomable version), but that will still leave the overall outstanding share of bills to overall Treasury debt at a shade under 22 per cent by the end of 2024.”

RTGDFA. What does the last section and chart tell you????

You keep doing the same thing over and over and over again: You don’t read the article. Instead, you google around and grab something that you don’t understand and drag it into here for me to waste my time on. Go do this in the privacy of your own home.

Your summation, as always was excellent, but —

Re: “ The government has been issuing huge amounts of T-bills to take upward pressure off longer-term yields”

Both longer and short rate yields have been dropping the past year, apparently because of upward nominal GDP revisions.

In the big picture, taking pressure off the entire yield curve by magically boosting GDP doesn’t seem like a sustainable way to reduce the deficit — but if there is a serious deficit problem, falling yields don’t make sense — mission accomplished!

I will redouble my efforts to RTGDFA

“And as inflation goes up, T-bill interest rates go up.”

Not necessarily, Wolf. The rate on short-term bills moves with the FFR. If the Fed holds the FFR rate below the inflation rate, those T-Bill rates will not move up with inflation. Lots of historical data on the Fed holding the FFR below the inflation rate….. as in the Fed’s ZIRP policy post the GFC.

Temporarily, sure. But inflation (core PCE) was below the Fed’s target “post the GFC.” If inflation rises to the worrisome rates we have now or higher, the Fed doesn’t keep its policy rate near zero for long because if it does we’ll have double-digit inflation, and at that point, it’s tough to get that under control. And we were heading that way, which caused the Fed to hike to 5.5%

Howdy Fellow Squirrels. Great Party isn’t it????? We knew what was coming and prepared all our lives……Honestly Youngins, what did you think was going to happen????

What self congratulatory nonsense are hooting about now ?

Howdy Outside TB. Squirrels know what I am typing about.

From what I can tell, US Public Government debt has increases from 12 trillion in 2009 to 35 trillion. That is 23 trillion.

US housing has gained 24 trillion total value during that time. Housing is probably in a bubble and so is Government debt?

But if Government debt is not in a bubble….housing prices are probably is not too? They tend to correlate over the long term…..at least since 1970.

Interesting thought. Thanks.

More liquidity will surely increase the value of primary assets and the earnings and wealth of owners thereof. It is a favorite tool to stabilize unruly markets in times of crises. The USD being the leading global currency is at an immense advantage-due to the soft and powerful halo bestowed by global acceptability- and its governors use this means of market control to print with gay abandon.

What if we never have a recession again? Sure, there are industries that have corrections such as what autos and certain sectors of real estate are going through, but that isn’t a recession.

What if the worlds economy is now recession proof?

I feel like this has been thought and shared a few times before time began;) Reminds me of francis Fukiyama “the end of history” and stories anyone tells about how we have arrived… then Caesar gets killed.. or war starts in Western Europe … or whatever unforeseen circumstance the media says will never come… arrives. I feel like I know very little but I am skeptical what you say is true.

I question the definition of recession because it’s rather generic isn’t it.

Even during the early 80s and during the dot com bubble of the early 2000s,

and during the popping of the real estate and credit bubble of 2007, and during the oil embargos of the 1970s,

and other periods that were supposedly a “recession”

the “economy” kept right on going.

Grocery stores continues to sell food, money continued to have value, people continued to work for money, money continued to be spent and people continued to live their lives.

A “recessions” in the past was made to sound like the whole WORLD was coming to a possible end. It was just dramatics for the media.

Certain sectors of an economy are always either booming or collapsing in popularity and pricing but never has the economy in general took a recess and exited the room on us. Not even during the medical emergency known as Covid.

There is no such thing as ‘recession proof’ at all.

There’s a cadence to debt issuance by the Fed Gov. There’s a cadence for debt issuance to cover spending in excess of tax receipts. And there’s a cadence to debt issuance for rolling over maturing debt. It’s during this second cadence that interest on debt is covered. The parties that buy the treasuries needed to roll over debt (including paying out on interest) are the same parties that receive the payout on the maturing debt.

Many economist and experts including Powell agree US is on unsustainable Fiscal path. But Powell refrain for speaking further and taking any action based on Fiscal policy and say that is not their domain. In one way its true and correct. But FOMC should adjust Monetary policy accordingly.

Question is what Powell will say and do.Underlying inflation Pressures is still.

In one of Interview in SF, Powell very clearly said they dont think about US Treasuries debt/yields when they set Monetary policy. Not sure if we can take it on its face value.

Wall Street and all junky paid media have already started writing and advocating for Sept cuts. Just look at this week WSJ, ET, FT and any other print and tv media. All speaking united for setting the stage in July FOMC and start in Sept.

I guess we all looking forward to FED statement and Powell Presser on Wednesday.

Since all tiers of government are borrowing all the time with huge liabilities already accumulated reducing rates will be very difficult decisions. US TBs are global financial benchmarks and have to be priced attractively to continue to attract buyers in distant capital cities.

Any thoughts as to when the national debt hits 1Q (quadrillion)? 25 to 30 years seems like a reasonable estimate to me.

From $35 trillion to $1 quadrillion means the debt multiplied by roughly 28.5 times.

Back in 1983, the debt went over $1.2 trillion, times 28.5 times is about $35 trillion. It took 41 years to multiply the debt by 28.5.

So if history repeats, the debt would reach $1 quadrillion in the year 2065.

Unfortunately, the debt is not growing in a linear manner. The debt growth is exponential.

Yes, but it was growing exponentially too from 1981 through mid-1990, and then it flattened out till 2001. The debt is not fate. It’s made in Congress.

But you also have to consider population growth and economic growth and inflation. Like I said in the article, looking at the debt in a vacuum is kind of a tongue-in-cheek exercise.

Like you said Wolf. The U.S. government, can never default on it’s debt. However, as you and Alan Greenspan also stated, whether or not the FRN is accepted as payment for goods and services is NOT guaranteed.

Hopefully, CONgress doesn’t go the way of Argentina.

What are you talking about?? He said it grew by a factor of 28.5 and then calculated a potential future debt using the same factor.. which is, by definition, exponential growth! Assuming linear growth, it would grow by the same additive amount ($33.8 trillion) over the next 41 years. Dear God—you don’t deserve these comment sections, Wolf.

If you take the Fed’s own data (going back to 1966) and fit that data (using any rudimentary spreadsheet software like cricketgraph or Excel) the equation I get is the following;

y = 59,662 + 0.19x^(2.879)

where “y” is the debt in millions of dollars and “x” is the number of months since January of 1966. The best fit is an exponential equation and you could simply solve for x putting in a quadrillion dollars, but then again, “the debt doesn’t matter” according to Mr Bernanke.

And this is NOT an exponential equation. Please regale us with your knowledge of physics next.

If Wolf wanted a better comments section, he’d allow us to mute, block, up vote, down vote and filter comments (by date and by popularity).

It would make this section far better and more usable.

LOL! The exponent is the “2.879”…

Just in case you missed it. LOL.

Contradict yourself much?

” which is, by definition, exponential growth! Assuming linear growth, it would grow by the same additive amount ($33.8 trillion) over the next 41 years. ” –

Looks like there is a new troll in the comment section Wolf.

Wolf’s data confirms what many of us have been expecting. Greater T-bill issuance moving forward, similar to 2001/2008, more yield curve inversion etc., but unlike those previous time periods, when yield curve inversion signaled a recession, we will get our second wave of inflation. IMO the commodities market and monetary metals are clearly indicating this. The hyperfinancialization of, well, the global economy, will lead to global hyperinflation. None of this is personal opinion, nor should it be surprising. Barring world war, this is simply MATH and physics…

In my neck of the woods, just like 2008/2009 I am seeing more and more tradesmen doing business “under the table” or horse-trading for the things they need. CONgress has long been bought-and-paid-for by the corporations/banks, so do not count on any relief there and…

Hedge accordingly.

Out here we call them our neighbor.

Try to tell that to the folks moving out here.

Be a good neighbor…no uber or home depot needed.

Thanks WR for this report.

Here are my 2c which I am sure no one cares:

1. None of the two parties would curb in spending to reduce deficit.

2. Deficit would only keep on increasing.

3. US govt can never default on its debt obligations since they own the printing press and there is enough demand for USD over seas.

4. USD as reserve currency is not going anywhere as TINA.

5. It basically means more and more inflation, devaluation of USD over time.

6. FED may not have to to QE because 10Y at 4.35%, there is ample demand.

This is a good summary. The fundamental difference now is the size/scale of the funding demands. Since there literally is no alternative now, global hyperinflation is baked in. It’s just math, and people really have a hard time with exponential equations. To say nothing of the resources required for 8+ billion people to maintain a decent standard of living.

The available amount of money in the US has been CONTRACTING for years and will continue to contract as the rate of inflation continues to shrink and demand further plunges this year. That basically means more and more DEFLATION and the mandate for Congress to cut spending as US yields rise considerably ahead.

No disagreement on any of those points.

If the nat’l debt goes up, and we don’t want the debt to tax rev ratio to blow out, tax rev will have to rise with it.

Either taxes rise with inflation and people don’t feel it as much (their wages are also being inflated), or there’s no inflation and everyone just gives more $$ to the gov’t.

The only way to avoid either of those outcomes is to let the debt to tax ratio rise substantially.

Interest payments to GDP would have been a good chart. Interest payment to tax revenues is good, but it implies that the tax structure is perfect. Interest paid to GDP would show the capability to service the debt without assuming the tax structure cannot be changed. I guess a lot of people think things are just fine the way they are.

This article wasn’t about interest payments, but about the debt. ONE TOPIC AT A TIME. For interest payments and tax receipts, which is quarterly data that I cover when the data comes out (and which is where the interest payments to tax receipts chart is from), you need to read the article that is about interest payments, so READ THIS:

https://wolfstreet.com/2024/06/01/spiking-interest-payments-on-the-ballooning-us-government-debt-v-tax-receipts-and-inflation-q1-update/

It includes this chart of interest payment to GDP, through Q1 (not through Q2). The Q2 update will come with the Q2 tax receipts data.

Thanks. Interesting stuff always.