A game-changer is underway. Even the NAR concedes this “shift from a seller’s market to a buyer’s market.”

By Wolf Richter for WOLF STREET.

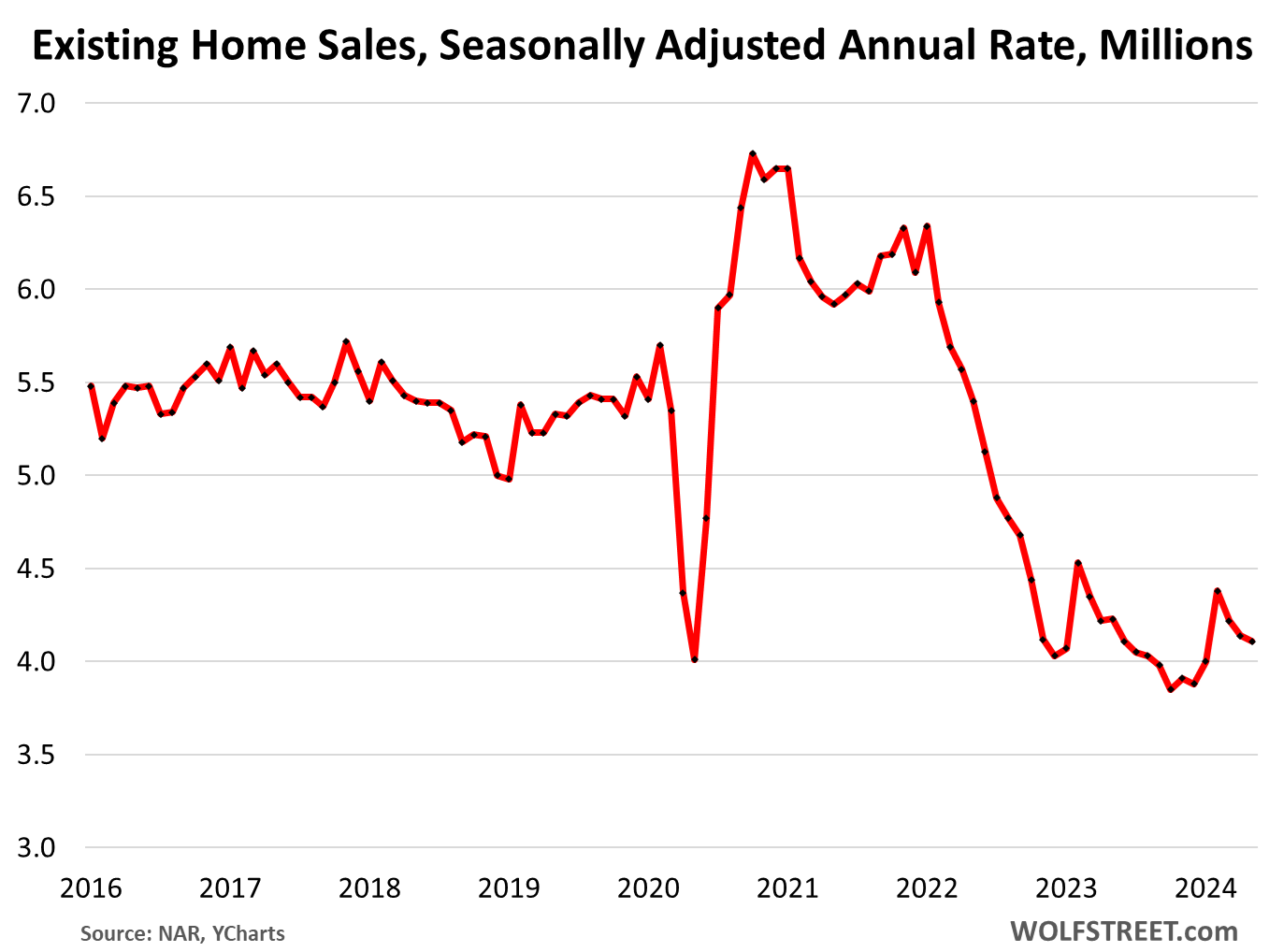

Mortgage rates have dropped to about 6.8%, down by a full percentage point from October last year, and yet sales of existing homes have plunged, and vacant homes for sale are coming out of the woodwork, the same vacant homes that the industry said didn’t exist, the second and third homes that people had moved out of but didn’t sell when they bought a new home over the past few years in order to ride the price spike all the way to the top. So now it’s time to sell those vacant homes. And supply in June spiked to the highest level in four years.

Sales of existing homes of all types – single-family houses, townhomes, condos, and co-ops – fell 5.4% in June from May on a seasonally adjusted basis, and also by 5.4% year-over-year to an annual rate of 3.89 million homes, the third-lowest sales volume since the depth of the Housing Bust in 2010, behind only October and December 2023, according to the National Association of Realtors (NAR) today.

“We’re seeing a slow shift from a seller’s market to a buyer’s market. Homes are sitting on the market a bit longer, and sellers are receiving fewer offers. More buyers are insisting on home inspections and appraisals, and inventory is definitively rising on a national basis,” the NAR said in its report (historic data via YCharts):

Sales in June were down from the Junes in prior years by:

- 2023: -5.4%

- 2022: -24.2%

- 2021: -34.8%

- 2019: -26.9%

- 2018: -27.8%.

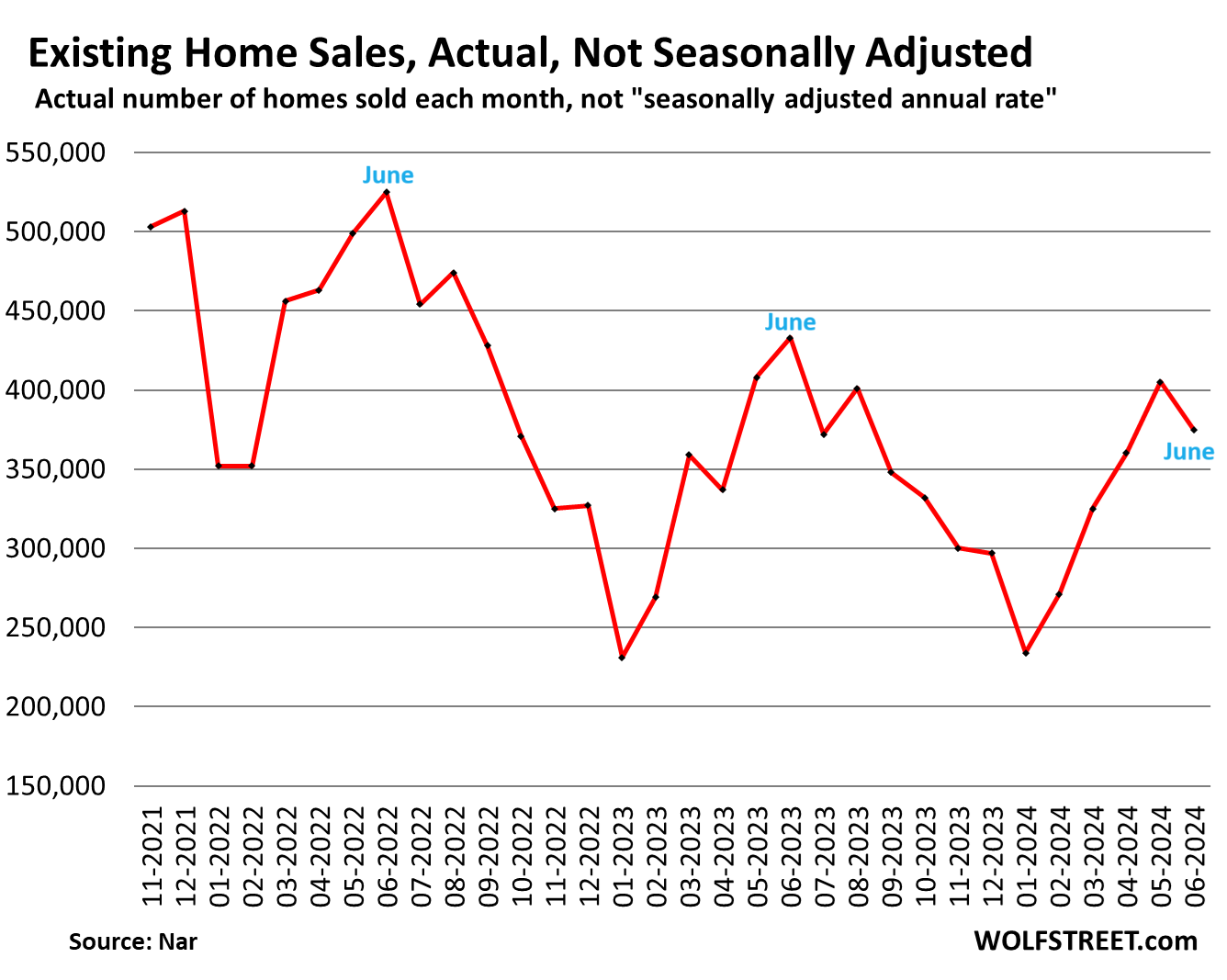

Not seasonally adjusted, and not annual rates, sales normally rise in June from May to form the seasonal sales peak in June after which sales decline through January.

But not this June. This June, actual sales fell from May, to 375,000 houses, condos, and co-ops.

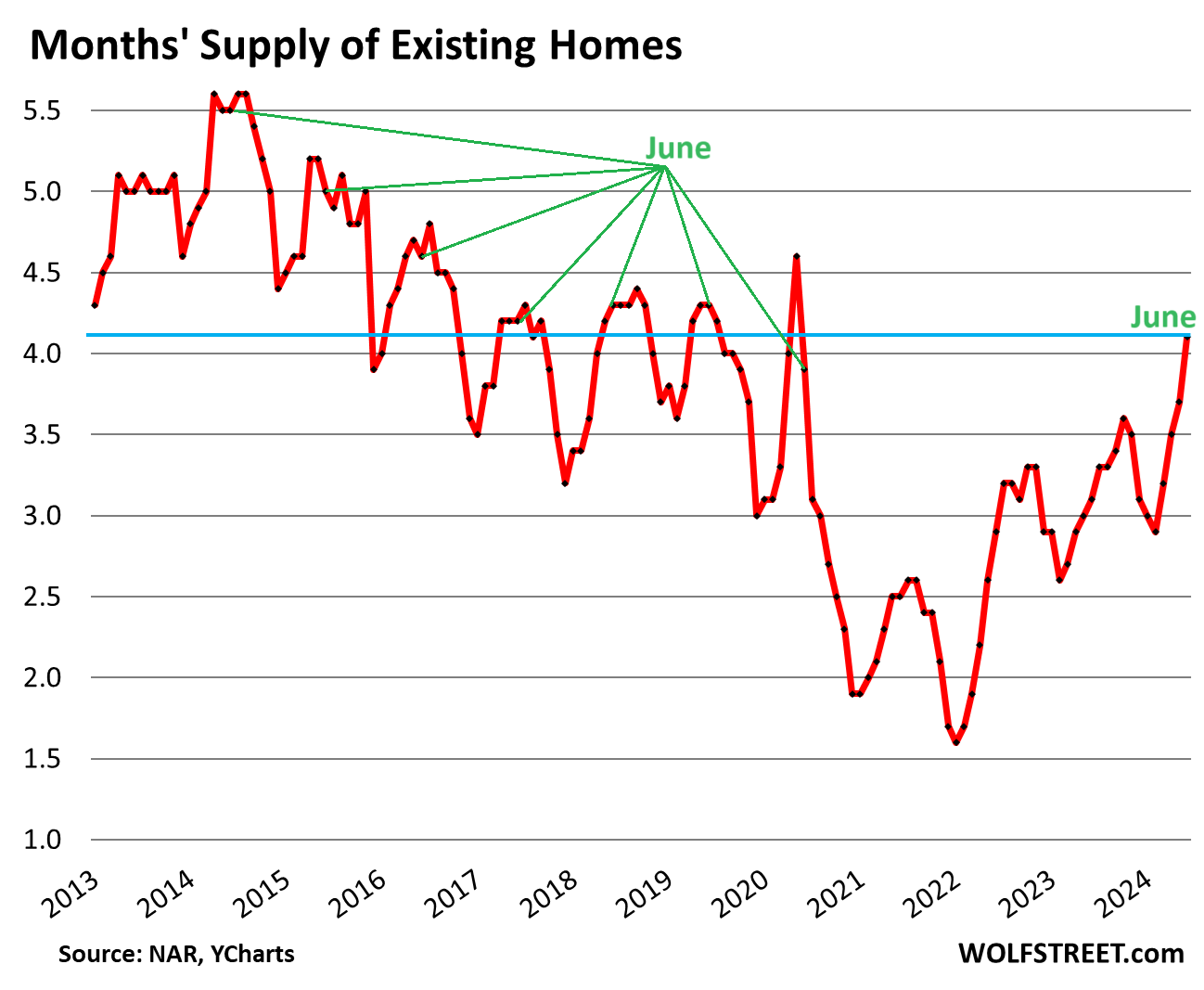

Supply spiked to 4.1 months in June at the current rate of sales, the highest since May 2020, and just a hair below the Junes in 2019 (4.3 months), 2018 (4.2 months), and 2017 (4.2 months).

Inventory for sale jumped by 23.4% year-over-year, to 1.32 million homes, according to NAR data. At the same time, sales dropped 5.4% year-over-year. This surge in inventory combined with the drop in sales caused supply to spike by one-third year-over-year, to 4.1 months in June, from 3.1 months in June last year.

And normally, supply remains roughly stable or declines from May to June, but not this June. This June it spiked. There is a game-changer underway (historic data via YCharts):

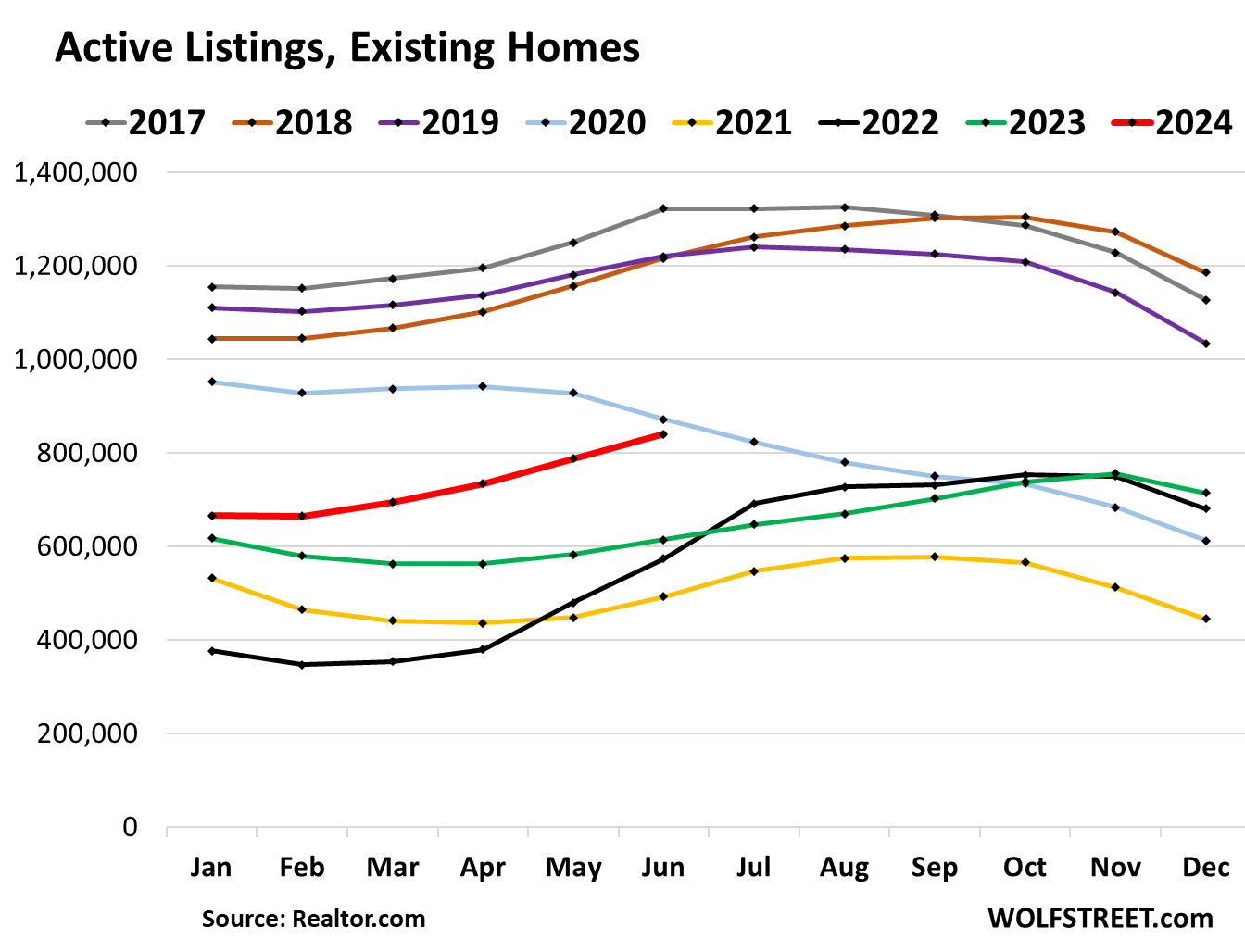

Active listings surged by 36.7% year-over-year to 840,000 in June, just a hair below June 2020, according to data from Realtor.com.

But active listings didn’t surge equally across the country, as we saw when we discussed active listings in the largest 50 metros here. According to data from Realtor.com, active listings surged the most year-over-year in:

- Tampa, FL, metro: +93%

- Orlando, FL, metro: +81.5%

- Denver, CO, metro: 78%

- San Diego, CA, metro: +72%

- Jacksonville, FL, metro: +70%

- Seattle, WA, metro: +62%

- Atlanta, GA, metro: +59%

- Phoenix, AZ, metro: +56%

- San Jose, CA, metro: +53%.

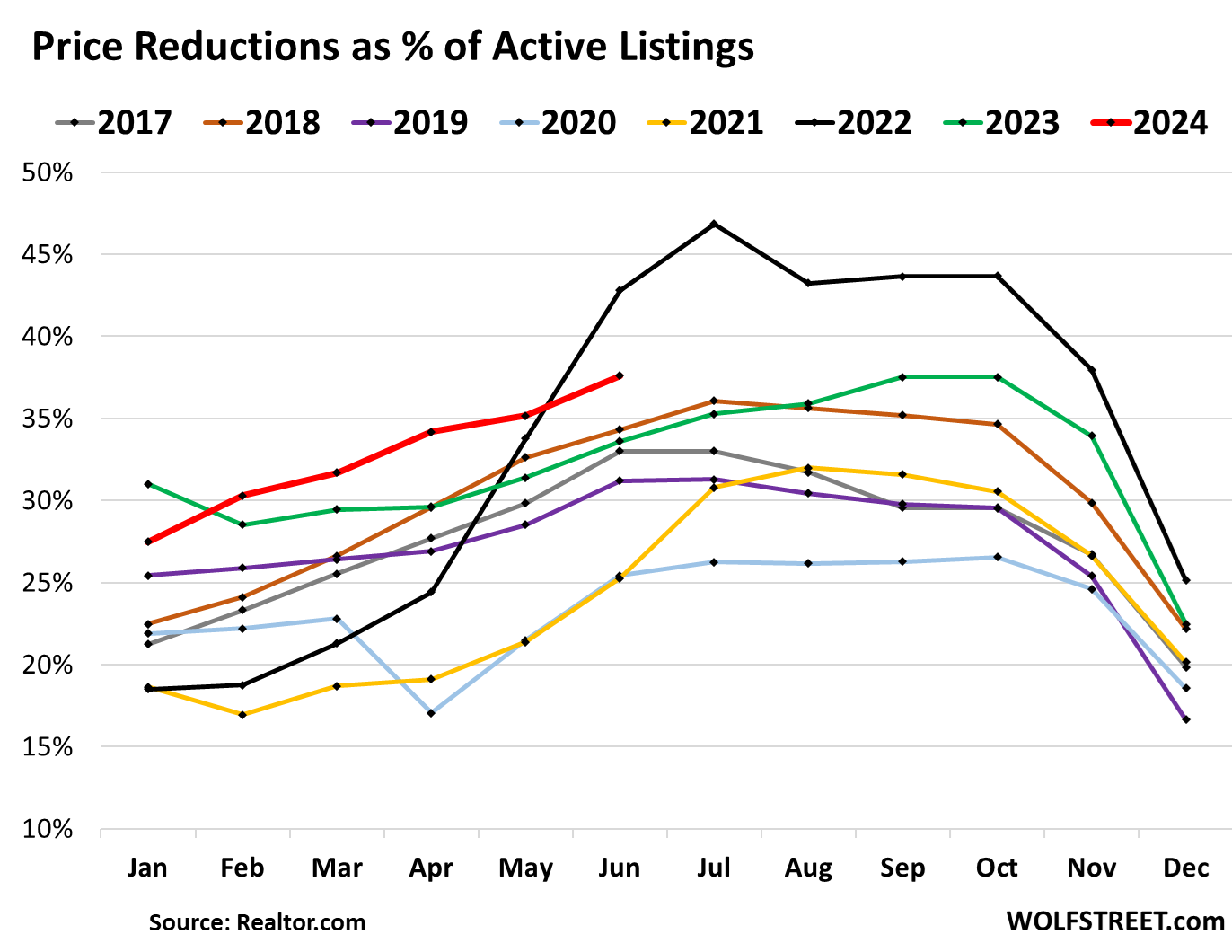

Price reductions continued to surge. Of the active listings, 37.6% had reduced prices in June, the highest share of reduced prices for any June, except June 2022, in the data from Realtor.com going back to 2016:

Median price was shifted up by the surge in sales of high-end homes.

According to the NAR, despite the 5.4% year-over-year decline in overall sales, sales of homes above $1 million actually rose year-over-year, the only price category where sales rose; sales in all other price categories fell. They fell the most in the price range below $750,000:

- Sales of homes of over $1,000,000: +3.6% YoY

- Sales of homes of $750,000 to $1,000,000: -1.9% YoY

- Sales of homes of $500,000 to 750,000: -7.6%

- Sales of homes $250,000 to 500,000: -12.4%

- Sales of everything below also fell.

The change in mix was very pronounced in expensive markets that depend more on stock prices than on mortgage rates, where many high-end buyers – including those now riding the AI bubble – pay cash, often with funds either obtained from the sale of stocks, or borrowed against their stocks.

For example, the luxury market in the San Francisco Bay Area. Luxury is over $5 million. According to Compass’ luxury report for the San Francisco Bay Area:

“It is in the most affluent counties where high-tech industry is concentrated – and the centers of what is being described as the “AI boom” – that luxury home sales truly soared in Q2.”

San Francisco County and Santa Clara County (incl. San Jose) “saw year-over-year increases in $5-million+ home sales in Q2 2024 of 54% and 63% respectively.”

“The circle of seven extremely expensive communities circling Stanford University – on either side of the San Mateo/Santa Clara County line – saw a year-over-year Q2 increase of 92% in $10-million+ sales.”

“The most affluent households are typically much more affected by changes in stock markets – and in the Bay Area, by the soaring Nasdaq in particular – than by interest rates: Many of these buyers pay all-cash…. And, of course, many employees of companies such as Nvidia have suddenly become very wealthy indeed.”

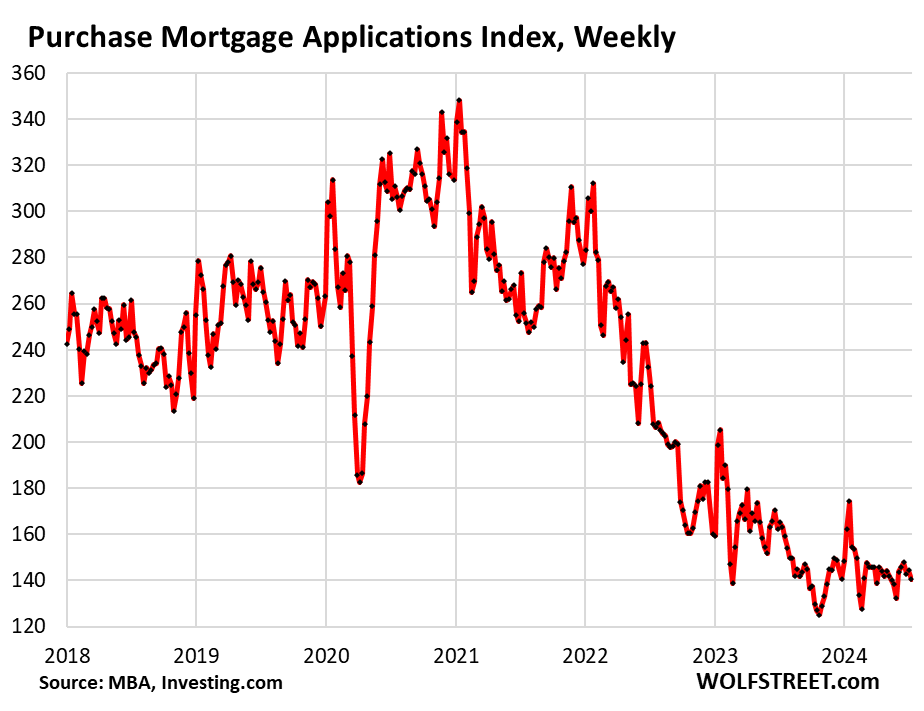

But sales of homes requiring a mortgage have plunged in the US overall, as applications for mortgages to purchase a home have collapsed by nearly half from 2019:

The median price was pushed up by this change in the mix of sales, with a larger number of higher-end homes selling, and fewer mid-range and lower-end homes selling (here’s our explanation and illustration of how the median home price is skewed by changes in the mix).

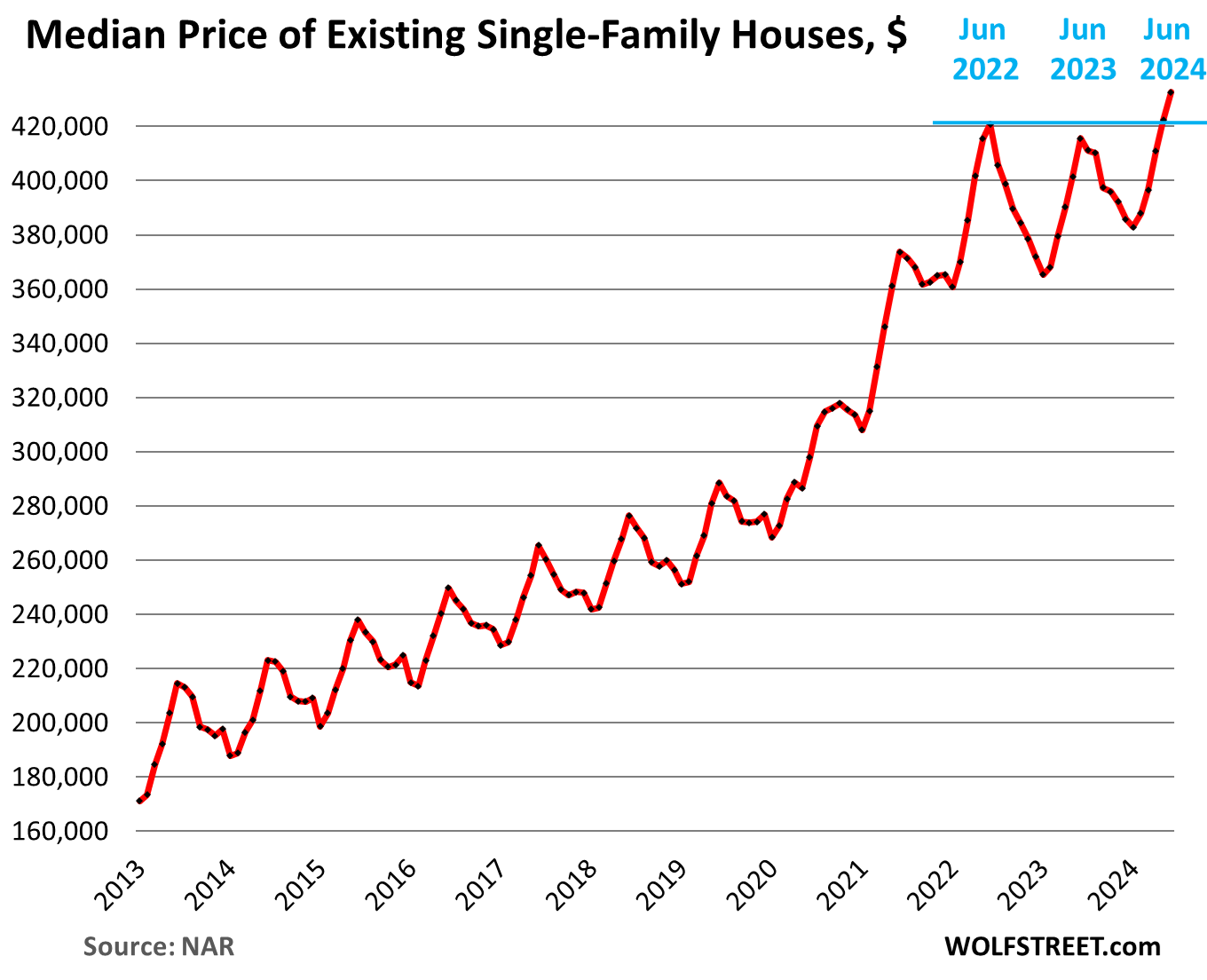

The median price of single-family houses jumped to $432,700, amid this surge in sales of high-end homes. It thereby surpassed the prior high in June 2022 by 2.8%.

And there was a down-revision: The median price for May was revised down by $2,100 from the figure reported a month ago, nearly wiping out the record price proclaimed in May, putting it roughly on par with June 2022.

“Even as the median home price reached a new record high, further large accelerations are unlikely,” the NAR’s report stated today. “Supply and demand dynamics are nearing a balanced market condition. The months’ supply of inventory reached its highest level in more than four years.”

For seasonal reasons, the median price will fall for the rest of the year into early 2025, as it always does this time of the year. June marked the high point for 2024:

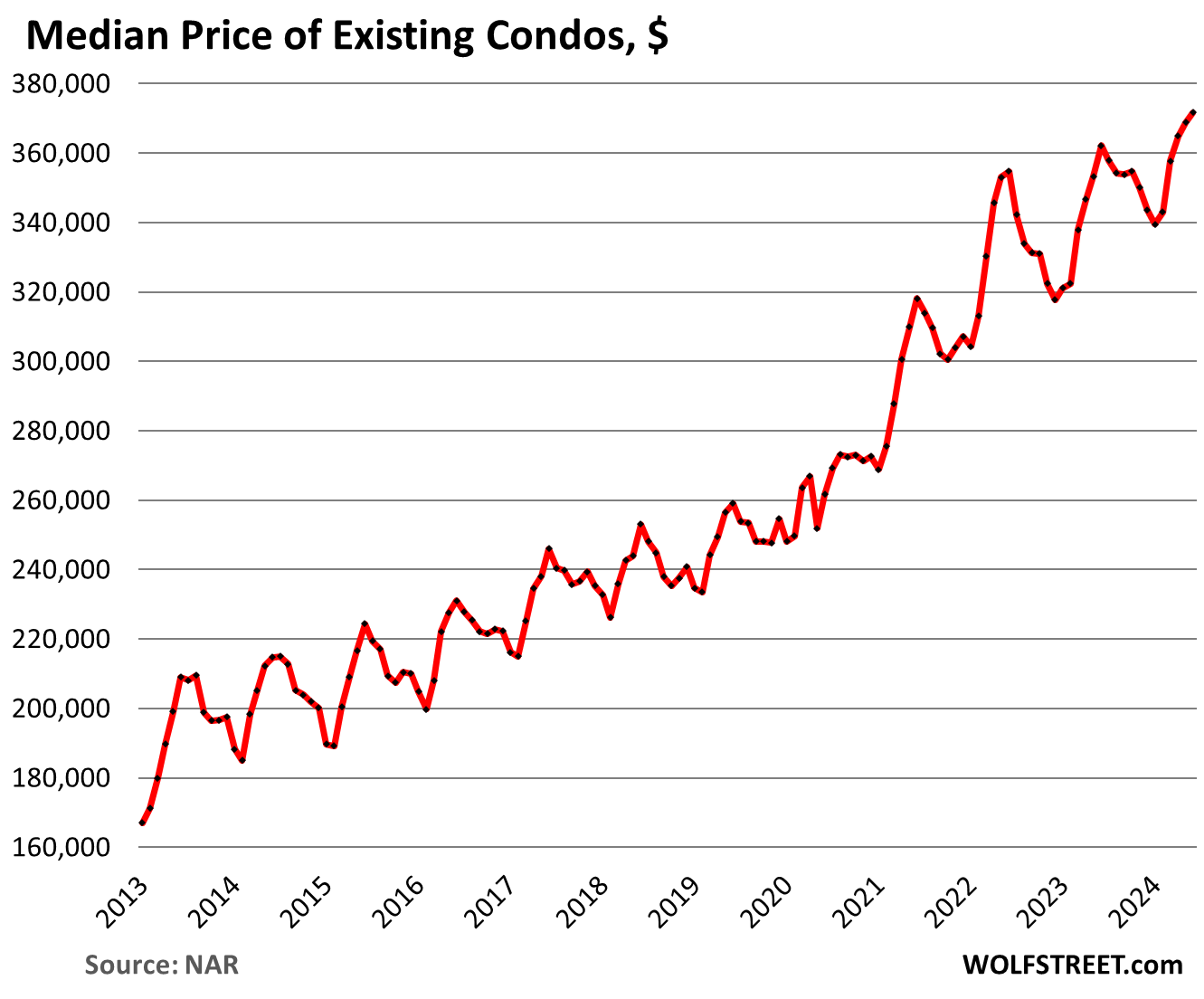

The median price of condos and co-ops rose to record $371,700, amid similar shifts in sales to the higher end of condos.

And there were revisions: the May condo price was revised down today from the originally reported $371,300 to today’s May figure of $368,900. So today’s June figure is essentially where May had been a month ago.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

1:04 PM 7/23/2024

Dow 40,358.09 -57.35 -0.14%

S&P 500 5,555.74 -8.67 -0.16%

Nasdaq 17,997.35 -10.22 -0.06%

VIX 14.53 -0.38 -2.55%

Gold 2,407.80 13.10 0.55%

Oil 77.27 -1.13 -1.44%

We’re still seeing prices of house soar upwards in the best areas of Southern California despite a substantial decline in listings and this doesn’t appear to be changing at all.

*Despite* a substantial decline in listings?

Excellent…(with my Mr Burns impression). This sure is interesting, quite a few on here still think SD will defy gravity much like LA/OC this time. On the flipside, not seeing the rest of SoCal on that list and even more sad is that prices still sky high across decent part of LA and OC. Crossing my fingers it will just be a lag effect and this time is no different. My real question is, can sellers hold out long enough to wait until rates hit 5% and still get the same level of insane asking price, the bet is that lower rates will bring the demand insanity back regardless of price.

“San Diego, CA, metro: +72%”

Also, how much of this build up can be attributed to seasonal change? We’re officially out of Spring season and typically in normal time prior to the madness of the last couple of years, inventory starting to pick up from now until winter. My fear is that come next Spring season, especially the way things are looking, it will be rate cut mania all over again, rinse and repeat and price in SoCal will just never come down to make sense, because of artificial constraint as long as sellers figure out the pattern.

Personally, I am still scratching my head trying to figure who are the people still taking out mortgage for what seemingly a basement starting price of $1.1M to $1.2M. Simple napkin math, even with $300K down and at current rates, factoring in tax..etc, you’re looking at close to $7K a month and require household income close to $$350-400K. Guess I must have missed the memo on that pay raise…

Once upon a time homes in SD were worth a little over half of those in LA.

@Xavier Caveat I’m a California history buff (specificially the history of real estate development in the state) and while there have always been “some” homes in SD worth half as much as homes in LA (a modest home in Brentwood has always been worth a lot more than a modest home in North Park) I can’t think of a time when the median home price (or median price per sf) in LA County was even close double that of SD County (for at least the last 75 years).

OK apt guy:

Just anecdotal historical note,,, far damn shore,,, but uncle sold his dad’s house on the cliff in La Jolla for $8K just about 75 years ago… Mostly due to hysteria re Japanese invasion that was a real possibility then.

Supporting your idea, at that time houses of approx. the same SF were selling in the city of the angels for way less than half of that…

Ocean views always get premium,,, SO FAR, eh?

SO, in reality as in realty, LOCATIONx3 still rules!!

And that was when SD was actually a decent place to live.

” not seeing the rest of SoCal on that list”

That list here was just the top 10 metros nationwide. The rest of Southern CA is on the whole list of the top 50 metros:

https://wolfstreet.com/2024/07/09/here-comes-the-housing-inventory-as-sales-plunge-active-listings-explode-in-tampa-orlando-denver-san-diego-jacksonville-miami-and-surge-in-other-metros/

Active listings YoY:

#16.: Riverside-San Bernardino-Ontario, Calif. +43.9%

#23: Los Angeles-Long Beach-Anaheim, Calif. +36.9%

Thanks Wolf. Music to my ears :) positive trend on multi-years long dogfight

for all the declines

multi-unit are surely super priced – with limited supply

and lots of NEW class A units out there

4 plex in Tucson $1,100,000 – was airbnb and those are rents they’re quoting for proforma price

30-40% to high YET – waiting

Need to see how long this increased supply will eventually effects the price and why prices are still growing !??!

If the prices specially in this damn Los Angeles are not coming down, who cares how many houses are for sale, no one can afford.

Prices in LA haven’t gone anywhere in four years, according to C.A.R.’s median price, to be taken with a grain of salt. Case Shiller and Zillow say that the price hasn’t gone anywhere in two years, so whatever. But over the past four years, there was about 20% inflation, with corresponding wage increases.

Just wait until the stock market crashes. You’ll see at least 2-3x inventory increase in much of coastal CA as tech goes in the tank and all the ancillary jobs like restaurants, furniture, car sales, etc go down with it. AI is a joke as far as viable products at this stage.

In spring 2004 SD inventory was around 3k and went to 15k in about a year and a half. LV went from I think about 5k to 45k roughly around the same time.

“In spring 2004 SD inventory was around 3k and went to 15k in about a year and a half. LV went from I think about 5k to 45k roughly around the same time”

It’s hard to fathom this time it will be like this, or a 30-40% correction but then again last couple of years were full of surprises and new normal so time will tell and I do hope this will be a thing in SoCal soon enough..

I don’t know how old you are, PI. Maybe you haven’t seen a major market sell-off. They don’t happen often, but when they do…

@HowNow Gen Xers, been around the block and seen the last 3 crash…I am just playing devil’s advocate and entertain the thought that maybe this time is different…am I truly convince of it, perhaps not but since I have been wrong for so damn long (since 2014) I am open to some humility and probability as well..

I just don’t know about the “bubble” popping. I wouldn’t hold my breath. Historically housing USED TO increase at about a 3% rate (Shiller). That hasn’t been true in the last 20 years or so. It’s due largely to the dilution of the currency/inflation, even though the inflation rate over the last 20 years doesn’t justify the outrageous increase in house prices (imo).

I dunno. But for the quality of life in the major metros and the cost of housing, I’d bail out of those places. Screw the “culcha”, the fancy-ass restaurants, and the celebrity sightings. There’s more to life than being stuck on a friggin’ freeway.

Talk about cultural bubbles…

Remember, there was a lot of Jingle mail back in HB1. People who had jobs and could pay their mortgage were walking. At one point between 2010 to 2011, 30% of all mortgages were underwater. It is easy to walk out of a house you are upside down on.

Why: so many of the mortgages during HB1 were no money down. HELOCs could be taken out up to 110%LTV. Interest only loans that did not pay down the principal. Plus we had the worst financial crisis since the great depression (probably will not see that scenario again)

This time, for the same scenario to occur as HB1, I read we would need to see a 35% to 40% drop in the median price of a house to hit 30% underwater mortgages. That would mean a drop to $260k. FICO scores are much healthier….etc. FED will step in before things would get that bad.

I am not saying housing cannot drop but jingle mail was easy when you have no skin in the game and acerbated the decline. A 20% drop in house prices could still mean most mortgages have 10% to 20% equity. The home owners will do whatever they can not to lose the equity.

Nah. The pandemic lottery winners are nosebleed rich now, and they comprise about a third of all households. It would take an outright multi-year depression just to return those people to their January 2020 wealth level, after adjusting for inflation. What happened during the pandemic years was morally wrong, whether it was through insidious planning or outright incompetence.

AGREE JeffD, almost totally:

Time and enough to either STOP all the hidden financial tranches,, , now estimated at well over a trillion,,, or, at the very very least make ALL such financial malarkies, and far damn shore there are tons,,, TOTALLY TRANSPARENT.

Without any such transparencies, WE, in this case WE the working folx who actually make things and do things are going to have another ”come to nothing” moment SOON, or perhaps exactly as was done by the oligarchy many times in the past to wipe out our net worth and make us beggars again, asking them to shine their shoes, etc…

Time will tell if this wonderful American Experiment will continue to increase the wealth and especially the long term well being of us folx who actually make stuff, etc., etc.

Is home insurance going up in Cali right now too? Someone told me insurers are looking to jack those up and dropping clients, they way it was explained to me it sounded similar to what we have in parts of Canada where ins. companies have to go through regulators to hike premiums.

Insurance in California is out of control. Can’t speak for home insurance but i know HOA fees has been going hog wild. For auto insurance and vehicle related. I have seen my own policy almost double with close to 30 yrs of driving record completely clean, no change of vehicles or status. It’s a wild west. Shop around, other companies are even more outrageous. That’s why it amazes me people in SoCal can just absorb and absorb higher cost of everything, buy a million dollar home and eat out all the time. Something doesn’t add up. I know a lot of people make good money out there but still a small percentage but yet you look around, it would be easy to fool you that everyone is making VP salary…wtf

I got my home insurance renewal quote last week.

It went up from 2200 4200.

5 years back it was 700.

@Phoenix_Ikki you would be surprised how many people have been able to “live beyond their means” by pulling equity out of their homes. I don’t know if is any there is any way to get statewide data on this but more often than not when I am looking at a home in CA (using my access to the title company database) people owe more now than when they bought the home. It is more than half almost everywere I look from multi-million dollar neighborhoods on the SF Peninsula to nothing over a million neighborhoods in Sacramento.

Ouch, sadly this is one factor many FOMO buyers miss their bet on or don’t consider it as much of a factor. Another factor is electricity, move to somewhere inland because it’s slightly more affordable but summer time it’s constant 100+ for months on end…AC bill of over $1K is not uncommon, especially if you got that big ol’house in Temecula or the valley to cool down. AC is pretty much mandatory for survival.

Near coastal or non-valley you can still outlast the summer without running AC 24/7 but if you intend to buy a place to stay for 10 years or more, is that something you can safely bet on consider we’re seeing hotter and hotter summer every freaking year..

P.I. you should get the hell out of CA. $1000 electric bill??? Maybe you need to close the windows and doors when A/C is running. I’m in NC where summers are always hot, always humid. We run A/C for about 3 months straight. Haven’t gotten an electric bill over $150, ever.

Electric rates in SoCal are the highest in the nation. I know multiple people that work in local utilities that are making $160K+ and wouldn’t make it in the private sector. Our utilities are run super inefficiently with no motivation to reduce costs. That and the mandates to provide a steadily increasing % of power from unicorn farts and other green initiatives, and that translates to some of the highest rates in the nation.

From CalMatters:

PG&E customers pay about 80% more per kilowatt-hour than the national average, according to a study by the energy institute at UC Berkeley’s Haas Business School with the nonprofit think tank Next 10. The study analyzed the rates of the state’s three largest investor-owned utilities and found that Southern California Edison charged 45% more than the national average, while San Diego Gas & Electric charged double. Even low-income residents enrolled in the California Alternate Rates for Energy program paid more than the average American.

Running the AC for three months in North Carolina? That’s nothing. In San Antonio, Texas the AC runs from April through October – that’s seven months. That’s not all – it runs a few days in the other five months. Yes, including December and January. I expect to see a time when it runs 365 days a year! Welcome to Hell!

Ouch, I thought I had it rough where I live. It’s crazy though how “wealthy” some areas in SoCal feel. I remember visiting a friend who was out there working somewhere south of LA so I had a free place to stay, flew in and rented a Challenger since I never drove one before, I had no idea about the area and immediately felt like a total redneck driving around all the Mercs, McLarens, Ferrari etc.. 😆😂. But Cali has like 39mil people living in it, I imagine most aren’t as well off, I don’t know how they get by with that kind of cost of living.

You guys have AC? How lucky, some people in Houston still have no electricity.

Phoenix_Ikki

Always interesting to see how different places in different countries and their heating bills. No shock that AC can cost large amounts (we don’t really need AC apart from seven days a year or so) My total bill for heating (gas+electric) in dollars is about $800 for the year. We don’t have HOAs, that’s a USA thing.

As we also have a mild climate,(temperate) with the very odd really windy period, sometimes it snows but we do get rain……so home insurance is not too bad, about $370.(up 20% sadly)

We don’t have percentage property taxes but a rateable based system but they did go up 5% this year to approx $1500 dollars (less 25% for being on my own.)

As you appear to reside in the SD, LA/OC area, you should be able to fairly closely follow the shifts in the market.

As the data indicates the market shift in the area you speak of has begun.

Depending on a number of factors including interest rates, amount of inventory.

Many homeowners have a significant amount of equity, and some have low interest-rate loans.

In some areas, there is a significant percentage of homeowners who may own their property outright.

It seems that lenders’ standards these days are tougher,

No head-scratching is needed; the people still taking out mortgages at the current market prices and loan rates have the desire and ability to do so. As you point out that is a specific demographic.

While there may be some commonality among the current buyers, each has its unique circumstances and reasons,

Are you among the many who are priced out of the current market?

It appears there are those who have opted to sit on the sidelines and wait.

There may be some commonalities amount the current cohort of people opting to wait in anticipation of some change in the house purchasing equation presumably that will be beneficial.

Lending standards aren’t tough right now. I got pre-approved for $200k over what would be considered financially reasonable. Yes I have a good credit score could make that payment if I didn’t contribute to a 401k and only purchased food and gas, but that’s just dumb.

Similarly had a friend buy a house at 7.5% this spring. Couldn’t get approved for the loan amount needed. So the lender had him do a 2-1 buy down to bring the payment within the allowable debt to income ratio. He said no big deal because he’ll just refi in 6 months when the fed cuts.

Also hearing lots of people who maxed themselves out to buy in 2021 panicking a bit. Sure they have 3% mortgages but they hit their max monthly payment. Now their homeowners insurance has gone up and property tax increases for those nice 40% equity gains are finally hitting people.

I’m sure lots of mortgages are also in great shape and lots of people own their homes outright. So not saying everyone is struggling. More just that everyone claiming lending standards have been so much more responsible this time around seems questionable.

The thing with a 2-1 buydown is a borrower still has to qualify at the highest rate. Not sure how that person qualified even with a 2-1 buydown as it doesn’t magically make a better debt:income ratio since it’s temporary.

They put more money down that they made from selling existing homes that also went up a lot. So unless you’re first time buyer, you will pay down a lot more than 20%

Price reductions sound great, but with so many sellers and agents still over inflating original lists there is still a ways to go. And if I get one more mailer from local yokel agents trying to use close to list ratio instead of close to original list to pretend they’re getting top dollar I’m gonna puke.

Hubris of RE agents still plenty in SoCal. Many take to Social media to brag about or maybe perhaps create this illusion that we’re still deep in 2021 or 2022. High price certainly help them sell that point even better.

Just saw another flyer from a RE stating how they sold a house in Cypress for $60K over asking and this isn’t something listed for well below market, ordinary house that still sold for over $1M. This kind of dynamic is still giving sellers and RE agents confidence and of course this is market by market dependent. RE agents in certain part of Texas or Florida might not be singing the same tune.

Get a grip. Dial down that R.E. sh*t. Take a shower, meditate, visit SRF in Cardiff or Brentwood, or better yet, visit an animal shelter.

Real estate agents biggest threat is that people don’t buy (or sell) because they don’t like the buyer agent BS and feel like the RE agents are ripping them off. There *are* RE agents that *will* take advantage of the confusion and *will* rip people off, giving a black eye to the whole industry as rumors start circulating. If RE agents don’t self police, they will be in trouble until procedures are put in place across the industry to shake out bad behavior. What Pheonix_Ikki is saying has some truth to it, because some agents *do* suck, and there are likely to be a lot more of those agents in the near future.

Thanks for the breakdown of % change in sales by price groups! Really interesting to see how the high price homes are diverging from “lower cost” groups. Appreciate all your work on reporting this.

Seeing foreclosures in my market (outside Charlotte) for the first time in 4 years. Most are entry level flips gone bad… but there are a couple of high ticket ones. Looking at a listing right now $2.3 million – foreclosure.

Assuming you mean the one in The Point. Seems like it needs some major work done to it. Interesting. Deed of trust shows it was a 15 year mortgage, should have been paid off in 2020. Surprised it took this long to foreclose on it considering the location and how much prices leaped at the lake the last couple of years.

“We’re seeing a slow shift from a seller’s market to a buyer’s market.”

Riiight. It’s still a real-estate-agent sales-commission’s market. Buying at the top of any bubble is not a “buyer’s market”.

I’d wait at least a couple years after unemployment hits cycle-highs before pulling the trigger.

This is the correct answer. You either need to be born with exceptional tech oriented brain and/or hope for the misery of foreclosure on others. In big cities, those are literally the only two paths to getting a home besides being an awesome doctor or lawyer.

Its ok. There are no signs of recession. Not in 2023, 2024 or maybe even 2025. Thats what I heard anyway.

Correct as far as 2023 and the first half of 2024 is concerned. We already nailed that one. The much hoped-for recession didn’t come.

In terms of the future (Q3 and Q4 2024 and 2025), well, we’ll just hafta wait till we get there.

Rates-of-change in short-term money flows, proxy for R-gDp, have been increasing since 2023.

TDs to DDs only fell by 7% in 1966. They have fallen by 18% with C-19. That has heretofore kept us out of a recession.

With a federal government pumping $3trillion+ of debt into the economy per year there wont be a recession, just a never ending depression once the debt has to be cut off

Nope, we skipped soft and ultra soft landing and changed course for back to the moon again. Wait until those rate cuts are for real, then it’s off the shizzle.

the long end of the yield curve might disagree with that prediction.

No…rate cuts signal trouble…the stock markets and everbody’s confidence will drop like a stone….unless, that is, they drop rates into a boom and then inflation up to 20% is an easy hit.

State and local governments are busy spending or committing the last of the pandemic manna from heaven, but next year’s budgets are showing the strain. What will be the impact of these budgetary cliffs? At a federal level, will deadlock continue in the next Congress? It’ll take time for all that liquidity to find homes, but after that? Who knows?

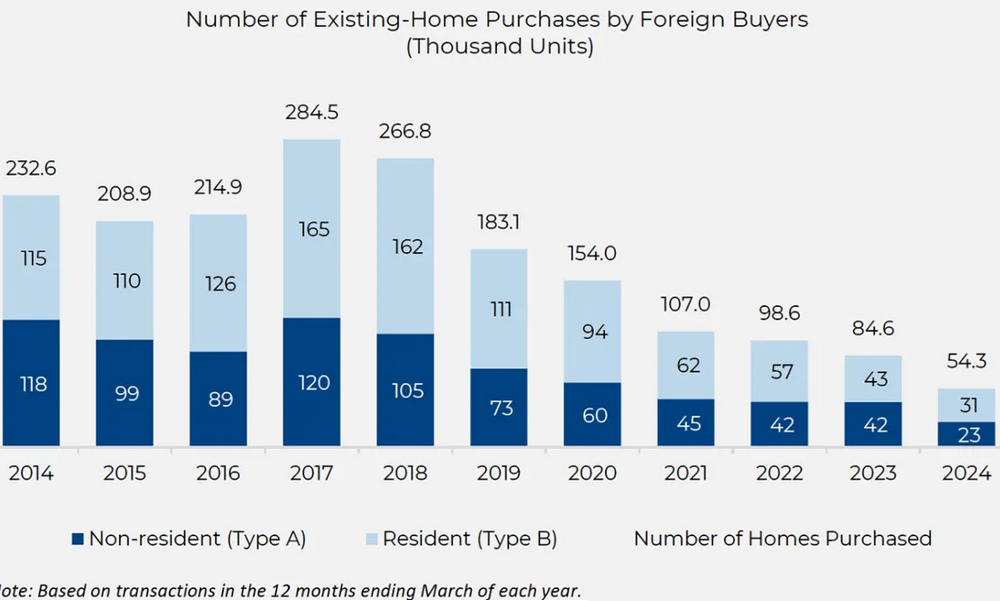

As a wild footnote, I recently partially read a fairly new NAR report for 2024:

International Transactions in U.S. Residential Real Estate

This report is based on an online survey that was conducted from April 4–May 19, 2024. The survey was sent to 150,000 randomly selected REALTORS

$475,000 – Foreign buyer median purchase price (compared to $392,600 for all U.S. existing homes sold)

50% – Foreign buyers who paid all-cash (compared to 28% among all existing-home buyers)

45% – Foreign buyers who purchased a property for use as a vacation home, rental, or both (compared to 16% among all existing-home buyers)

I’m curious how this might impact the inventory dynamics as the bubble seems to be hissing?

What you “forgot” to mention is that purchase volume by foreign buyers has collapsed by 81% since the peak in 2017, according to the NAR report. Volume has plunged every year to lower and lower levels, to where foreign buyers are now almost irrelevant in terms of volume.

That was in nearly all the headlines about that report you’re citing.

I’m curious why you’re so deceptive and manipulative to not mention the headline part of the NAR report that foreign buying has collapsed to such low levels that it’s irrelevant? Which makes your questions irrelevant nonsense.

Click on the chart to enlarge:

In South Florida, at least, even wealthy foreigners can’t compete with the obscene amounts of money piling in from Wall Street private equity partners, money managers etc. A lot of latin americans buying in Portugal and Spain. Lower prices and supposedly better lifestyle.

Traffic from Mexico is picking back up as a result of their new leftist president.

LOL…I think as Gen X SoCal kids would used to say…”you just got moded” by Wolf..

Yes, I’m the person at Wolf’s fireside commentary party that continually fails to read more than a few sentences of some random report — then gets busted by the omnipresent host that helps me get it right.

Nonetheless he mistakes my sloth for deception — I have never made comments to deceive — and I’ll honestly admit that I cherry pick information, then fail to put into proper perspective.

I keep trying to improve but have bad habits — I used to be better at this (damn it).

It didn’t sound to me that you were trying to be manipulative, just that you had a question based on something you read (partially read you even admitted :)

You know what though? It may make Wolf mad, but getting those kinds of responses out of him makes for an educational comments section for me 😆.

I like both your comments. They expand on the split in the market mentioned in the article.

Howdy Folks. Has the Lone Wolf Charts shown the final peak???? Is Housing Bust 2 finally on the way down ????

@Wolf Is there any way to tell if a “vacant home for sale” is a home that “people moved out of so they can stage and get top dollar” or a home that “people had moved out of but didn’t sell when they bought a new home over the past few years in order to ride the price spike all the way to the top.” When I was a kid (working part time for a real estate agent) I never even heard of a “staged” home and even in Hillsborough or Atherton most homes for sale in the 70’s still had people living in them, while today most high end homes are vacant and staged when they are for sale.

Howdy Apartment Investor. I am not the Lone Wolf, but the local MLS and access to it and knowing how to use it, is the tool needed.

We vacated our property in SoCal and staged it to get top dollar. That is a sad statement of the quality of our home furnishings but oh well – they all went to charity :)

This is a national figure — 1.32 million homes for sale. You want to know if an individual home was staged? I mean, go locate that home and look at it, you’ll see.

I’ll just use this as an opportunity to make this clear: when sales plunge and inventory spikes, it’s the result of vacant homes that come on the market many of which have been sitting in the shadow inventory for months or years.

When a regular homeowner wants to move, they buy a home and they sell a home (maybe not in that order), so one goes on the market, and one comes off the market. So inventory stays the same overall in the US (+1 -1 = 0), but there are TWO SALES in the US.

But what we have here is plunging sales and spiking inventory – and that’s the impact of sellers putting homes on the market that they have moved out of some time ago

90% of the homes we appraised in the last 3 years were empty. When we get one that is occupied, we try to cancel the appraisal, because it’s too much of a pain in the ass. Like a dangerous dog on the premesis, bad tenants, filthy setting etc. I would say 75% or more of these empty properties are part of the shadow inventory. The owners have been holding on hoping for a higher price and have decided to throw in the towel.

Could some of the inventory spike be from a break in the consumer cycle of :

1. Save up a down payment

2. Buy a home

3. Load up on credit card, auto, RV, and other debt.

4. Cash out Re-Fi the home

5. Pay off credit card, auto, RV, and other debt.

6. Repeat

If they can not obtain a cash out Re-Fi or HELOC this time could they be forced to sell and become a renter for a while? This would also add to inventory.

Great news for private equity & mega landlords. They will be ready to pounce on new unsold homes en masse either soon if they already have cash, or when the FED predictably drops interest rates to zero again (its our tradition to be at zero, just like tipping). Most of those waiting in line to buy their 1st tiny home will again get outbid by big investors & keep renting from them or tech couples who own 3 or 4 homes. Fvck the fed, fvck the govt & fvck america. Not voting & not doing any combat duty for these parasites.

BS. The biggest landlords are NOT paying those high prices, LOL. They’re TAKING ADVANTAGE OF THOSE HIGH PRICES and are SELLING the houses that they bought in 2012 — and they talk about it in their earnings calls.

Instead of buying individual houses scattered all over the place, the big landlords of SFR have all been building their own for-rent communities WITH THEIR OWN HOMEBUILDING DIVISIONS, or buying build-for-rent communities from homebuilders. That is the biggest development in residential real estate. It’s far more economical to manage a community with 500 purpose-built rental houses, a leasing and maintenance office, and common amenities for tenants, than managing 500 houses scattered all over the place. The big landlords are selling those scattered houses at these ridiculous prices, and they are building their own supply of rental houses. They all talk about it in their earnings calls because it’s such a huge move. Build for rent has exploded over the past three years.

I’ve been talking about it here for a long time, and you completely missed this biggest move in residential real estate? So here is the latest one. READ THIS:

https://wolfstreet.com/2024/04/24/biggest-landlords-pile-into-build-to-rent-single-family-houses-but-are-selling-older-houses-into-this-overpriced-market/

Agreed. In Colorado longtime landlords are also selling due to new stupid progressive laws driving costs and risks higher. Expect rent increases! Investing instead in states with more reasonable laws.

Wolf, do you know how these firms are dealing with capital gains?

Is it possible they’ve found a way to 1031 exchange into their new build projects?

Otherwise, even with huge profits from selling their houses all over the place, it doesn’t seem like it’d pencil out.

Some of the big landlords are structured as REITs, and they get to deduct the dividends they pay from their taxes. And since they pay out a big part of their income in dividends, taxes are not a huge problem. Other big landlords are funds held by PE firms or pension funds. Some homebuilders have big rental divisions. So it depends, as they say.

It seems likely that they are benefitting from 1031.

Also, I imagine they are moving their tenants from the scattered SFR homes into BTR communities…

That business plan makes total sense for those big landlords. They probably can get a school built in or on the edge of the subdivision. They can make sure the subdivision is safe with private security. etc.

Not voting against someone who would use the Fed to inflate their own assets by restarting QE seems counterproductive to your sentiment. Try to resist “cutting iff your nose to spite your face”.

“or when the FED predictably drops interest rates to zero”

Almost like you made this silly comment just to get a bunch of replies.

That chart for “median price of existing single-family homes” from 2013 to present is stunning. Takes one’s breath away.

Yowzers!

As always, great charts and information Wolf.

In the 1960s practically every house (cottage) in the SoCal beach city of Hermosa Beach was in the $10,000 to $15,000 range including their tiny little postage stamp sized 2400 square foot lots – and many went unsold for a long time as few people wanted to live in that damp and windy beach city. Now those same tiny little junk cottages are selling in the $2,000,000 to $3,000,000 or higher range and don’t even have places to park cars. I’d say things are way out of whack now in terms of valuation.

and what’s funny is back in 1960s, 405 or any other freeway isn’t a giant parking lot on every freaking day on the way to beach cities…nowadays Sat/Sun parking lot traffic is quite common to try to get to Venice, Malibu or any of the beach cities

Just as Wolf brings “perspective” to the subjects he writes about, I do appreciate your perspective, SCBD. I grew up there and, yep, in case people don’t believe it, it’s twoo.

Few wanted to live in Santa Monica because of the cooling onshore breezes and morning fog. The most expensive areas were more inland: Bel Air, San Marino/Pasadena, Beverly Hills.

Ocean Views: not a biggie back in the day. Few wanted to stare out at a black ocean at night; they wanted “city lights” and homes were built in Sand Diego with the large, family-room windows facing east, not west toward the ocean.

Things change.

Yep, and back in the day really nice huge houses often with considerable land were all on ‘the hill’ which is the Palos Verdes Peninsula comprised of Rolling Hills, Rolling Hills Estates, Rancho Palos Verdes, and Palos Verdes Estates. We laughed at the lowly beach cities of Hermosa Beach, Manhattan Beach, and Redondo Beach, but they were very affordable for poor hippie surfers!

I beg to differ on the “hippie surfers” idea. Surfers and hippies were very different types. Both were pretty rare birds although they got a hell of lot of press.

Now… it’s nearly the opposite. What used to look like a hippie is now a tattooed redneck and everyone is surfing or pretending to.

I ran % reductions on active listings on Reatlor.com data on a set of a few cities in Orange County, California (‘huntington beach, ca’, ‘irvine, ca’, ‘cerritos, ca’, ‘cypress, ca’, ‘garden grove, ca’, ‘la palma, ca’, ‘anaheim, ca’, ‘artesia, ca’, ‘costa mesa, ca’, ‘stanton, ca’). I’m sad that it is not looking as nice as the nationwide plot!

https://i.imgur.com/qX9tXXY.png

Sales have collapsed, even in OC. So inventory itself is useless. What you need to look at is inventory in relationship to sales, so “months’ supply,” which is inventory divided by the current rate of sales, which is the chart I posted above for the US.

So there are 2.5 months’ supply in OC, the highest for any June since 2020, up from 2.0 months’ supply in May, and up from 1.9 months’ supply a year ago, according the California Association of Realtors. So that’s lower than the national average of 4.1 months’ supply. But it seems to be rising at a pretty good clip.

Thanks, Wolf! I will take a look at months’ supply in the cities I am watching to see how those numbers look, too.

Wolf – two questions on supply of inventory. First, what sales figure is used for the denominator — last month’s total sales or a moving average etc?

Second, if inventory, the numerator, stays flat, and the number of sales, the denominator, declines, then inventory will rise. But isn’t that then skewed and not telling us much?

Lastly, curious as to your thoughts on what impact on supply a cut in rates might have. For instance, if rates went from ~7% to say ~4%, then perhaps demand rises or surges or whatever. Do you think supply would surge in an equal or perhaps even greater amount and potentially, therefore, weigh on prices? I get that it’s speculative but perhaps you know of a comparable period at some point in the past or somewhere else that could be informative here.

Thanks!

“…questions on supply of inventory. First, what sales figure is used for the denominator — last month’s total sales or a moving average etc?”

The CAR provides the supply figure.

“Second, if inventory, the numerator, stays flat, and the number of sales, the denominator, declines, then inventory will rise. But isn’t that then skewed and not telling us much?”

Inventory rises when more new listings are added to inventory than sales take place — and this is what we have.

What you may be referring to is supply, which is the number of months it would take for inventory to be sold down to zero if there are no new listings coming on the market. Supply is inventory divided by the current rate of sales. It puts inventory in relationship to sales. It’s the most crucial inventory metric.

Hey Wolf! Yes, that was a typo, meant to say “supply”. But my question remains.

For example. 1000 units in inventory. Mortgage rates = 3%. Monthly sales = 500. 1000/500 = 2 months’ supply.

Rates go up to 7%. Buyers strike. Sellers strike. 1000 units in inventory but now just 250 monthly sales. Supply = 4 months.

I guess my question is does this tell us anything, really, about the supply v demand balance in a situation like the one we’re in? I would think that in this case the inventory number is a better indicator of supply of homes versus # of months supply given the rapid drop in sales. Thoughts?

p.s. thought the theory on supply being skewed by technology, which you’ve covered in the past, was really interesting.

FYI, 6.0 months is traditionally considered a balanced market, so we’re still 1/3 below balanced. Folks got a distorted view of normal during COVID with homes selling in days or weeks rather than months.

That said, until rates drop the DOM will continue to increase.

“6.0 months is traditionally considered a balanced market,”

That was back when it took a month from listing with a broker to the printed listing appearing in local papers; today, they appear the same day on Zillow and everywhere; back then, it took a month to get a mortgage approved, today it takes a few days, sometimes same day. Back then it took a month-plus to mail the paperwork back and forth. Much of this stuff has been automated and put online. These long waits have been wrung out of the system. That figure of months’ supply has shrunk every year since the Housing Bust for that reason. The whole process took a quantum leap forward during covid. 6 months’ supply today would be a total glut.

I grew up in Cerritos. Cerritos and Artesia are both cities in LA County.

Once the everything bubble begins to pop, I would imagine the ensuring job losses will begin to drive these insane prices back to some semblance of reality. Should be lots of inventory and at much better prices in a few more years.

Over 70% of the Federal debt is in short term treasuries that require roll overs. On top of all that debt, you have mountains of new borrowing. This at a time when the biggest buyers of treasuries overseas are drastically cutting their purchasing. 4 trillion a year is a mountain of debt to find buyers for in a global recession.

Not quite 70% 🤣❤️ That would be scary.

There are $5.76 trillion in T-bills outstanding (1 year or less).

Total debt: $34.95 trillion; T-bills = 16.5%;

Marketable debt: $27.79 trillion; T-bills = 20.7%. So that’s high, 20% was considered sort of a red line; but recently, the government went right over it.

How high would the T-bill percentage need to get before it would concern you?

I’ve heard that since 2018.

Interest rates could drop to 0% and it wouldn’t be enough to stop the coming avalanche of more price drops. Home prices were driven too high by the fools who rushed in and bid up prices during the pandemic.

If mortgage rates drop to zero, that must mean we’ve had a nuclear conflict and the houses are radioactive. Things at true fire-sale prices.

I’d buy one! What’s a little radiation if the mortgage is 0? ;)

Or by then if everything is radiated, you might be paying your mortgage in bottle caps and instead of fighting FOMO zombies, you’ll be fighting feral ghouls for prime RE inside a Vault

At least beach front property will be dirt cheap but watch out for them Deathclaws…

I didn’t say they would drop to zero, but even if they did, that won’t be enough to stop this housing bubble from popping.

Or…those “fools” have fallen arse-backward into the greatest financial “decision” of their lives. Perhaps the phrase “he who panics first, panics best” applies on the way up as much as it does on the way down.

Could be another round of QE on the horizon. Just sayin’.

My wife just flew out today to look at retirement properties and there is something unusual going on. Some seller’s agents are not happy that she is not bringing a buyer’s agent. I think the owners of RE businesses are not happy about potentially losing their share of buyer’s agents fees. Some seller’s agents have refused to show the property unless she signs a buyers agreement with them. A couple changed their minds when she passed on the showing. The RE mafia just can’t let go.

The proper response is, “If you’re not happy with me giving you your seller’s commision, I’m perfectly happy walking away.” After all, it is the buyer that pays the seller’s commision, not the seller.

Worse yet, the seller entered into a contractural agreement with a seller’s agent to sell the home, and the agent refuses to sell to a buyer? Isn’t that illegal in addition to immoral? Isn’t it the seller’s decision to turn away the big bag of money, considering it was the job of the agent to sell the house? If not, there are about to be a lot of “for sale by owner” properties on the market, or a lot of lawsuits directed at “seller’s agents”.

Sometimes (most times) it is advantageous to educate yourself about the inner workings before spouting off about things you haven’t well researched. Sorry, but that’s not at all how it works.

OK, so what did I miss? I talked to the seller’s agent who insisted that we sign a buyer’s agent contract before she would show a property. That agreement, according to her, would allow a buyer’s agent “from her firm” to represent us if we decided to go forward with the purchase. Tell me again how that is not a form of collusion.

why would a seller’s agent care? he’s getting the same either way.

The house next door has been sold and is in escrow. It’s a four-bedroom house in an okay neighborhood in Oakland, likely suitable for a family of four, including two working parents. It took a while for the home to sell. Its proximity to the school may have influenced the decision to buy. I plan to wait for prices to decline before buying or entering the market. My goal is to purchase within the next three or four years. I’m a first-time home buyer in my forties. My rent is substantially lower than the Zillow price of the two-bedroom single-family home I’m currently renting. I could move elsewhere too remote worker earning decent income.

I wouldn’t go around saying that out loud, about your rent being low and/or reasonable. Don’t want to jinx it or have the landlord take notice.

Either your landlord is a good one and value and care about keeping a good tenant rather than chasing top dollar as if they are running a AirBnB or he/she hasn’t woken up the surrounding market price and you’re lucky for now. Either way, count your blessing and don’t expect that to be the norm sadly.

Unfortunately, there are plenty of landlords even mom and pop that want to milk their tenants to get top dollar, raise 20% rent on a year seems reasonable to them. You expect professional landlord to get the max ROI but these mom and pop, unlike corp landlord also won’t do any adjustment down or incentives (like free1-2 months rent) when the market goes south. You seen that in existing home sellers too, new builders react first while mom and pop hang on looking in the rear view mirror for aspirational pricing.

It’s fine they want to ask for top dollar but hope these landlords know when you fly too close to the sun, it’s easy to get burn. All it takes is one bad tenant then it’s nightmare for days..

In Canada if you don’t have a mortgage there’s no sense taking out insurance because all the value of the property is in the land not the house.

Not true, and I own two houses. Each policy specifically indicates every aspect of structure replacement costs. And I own vacant property. The only insurance on that is for liability.

“pay cash, often with funds either obtained from the sale of stocks, or borrowed against their stocks.” – do you get a lower interest rate when you borrow against your stocks?

Compared to unsecured, yes. And it keeps your investments intact. From the seller’s view point, you are a “cash buyer” and thus more desirable.

BTW, check with a CPA on the deductibility of interest. It may not be in some cases.

Vlad the Impaler

“do you get a lower interest rate when you borrow against your stocks?”

Depends on lots of factors, the broker, and how big the amount is. The bigger the amount, the lower the rate. Interactive Brokers lists a margin rate of 6.2% for $1.5 million plus in margin loan. Schwab is much higher than that.

In addition… I knew a banker at First Republic (years before it failed) whose entire department did just that, including lending on shares of startups before they went public. They used ultra-low rates to do this. It was one of the reasons First Republic was such a favorite among the San Francisco and Silicon Valley rich.

Lending against shares of startups is an industry here. These people are sitting on tens of millions or hundreds of millions in non-traded stock, and the financial industry is more than eager to lend against that at relatively low rates.

Very insightful, I wasn’t aware of this practice. Thank you, Wolf.

The pandemic “pay whatever” lottery winners are buying houses, so prices continue to rise. Everyone else? Not so much. Mix has a lot to do with prices, which again points to pandemic “pay whatever” lottery winners.

Wolf, why do you suspect Orlando, Tampa, Denver, and San Diego to be spiking in active listings? Are these where vacation homes or vacant properties tends to be?

People are trying to sell the vacant homes that they’ve moved out of a while ago but didn’t sell because they wanted to ride up the price bubble all the way. But carrying costs are high, and when they see that prices no longer rise as expected, then it’s time to take the profit and run. This is happening everywhere.

Watching as the crowd in the huge auditorium slowly realizes the fire is spreading and there are only a few doors, and they weren’t first in moving to the exits….priceless.

I watch central Florida closely and I’m pretty sure that is what is happening there at least.

Please note that in none of these cites has the spike actually resulted in falling prices on a year over year basis, not yet anyway.

Denver is showing year over year decline in Case Schiller index.

The biggest thing these cities have in common is “premier travel destination”. Most likely, a lot of short term rental owners see the writing on the wall.

Not sure about the other markets, but Denver and all of Colorado benefited greatly from lock down moves during pandemic, and things got pretty speculative until summer 2022, since then there has been accelerating cooling of the market, in the mountain towns this may be sales of vacant homes used for STR, but in Denver it feels more like winding back a speculative bubble. Prices ran up 40-50% since 2019 and now with QT and a slowing economy and fewer people moving here because of high costs, things are unwinding. I think this is going to go much farther here, listing are way up and almost every property has cut prices.

“More buyers are insisting on home inspections”

What a crazy market we’ve been in that people have been expected to drop 7 figures on something they’ve just toured for half an hour.

Buyers with FOMO knew that an offer with no inspection contingency was more attractive than one with inspection. FOMO is part of what brought us to this point.

It’s not just FOMO. In my area at least, if you wanted to buy for *any* reason, you pretty much needed to be cash, no inspection, or you weren’t going be buying anything.

Let me start by saying that Lawrence Yun and the NAR have no credibility. Back in 2007-2008 at the start of the collapse of the real-estate market, Yun was trumpeting that it was just a blip. His co-cheerleader was that idiot Bernanke who echoed the same mantra – it’s just a blip. Sound familiar? We now know that loose lending practices, subprime mortgages and other bad financial tools like packaging those mortgages into securities and derivatives bankrupted Wall Street firms, collapsed our financial system and forced the government bailout of our financial system.Yeah, inflation was supposed to be a blip according to the idiots in the Fed and that idiot Treasury Secretary of ours. Here we are 3 years later dealing with inflation. Growing up in the 70s I remember how bad inflation was even though I didn’t understand it.

My guess, and I’ve been studying real-estate and finance for a long time (I also have an MBA), is that something else is happening. Either those who were going to buy homes at these 7% rates have bitten the bullet and done so. Meanwhile. sellers deluded themselves into holding on to homes of hopes of interest rates dropping back to the 3 to 4 percent range, which was historically low and probably and aberration brought on by the pandemic.

There is something different going on. It’s not as simple as saying that home sales have swung in favor of buyers. We may be headed for a different kind of real-estate meltdown caused by a combination of high rates and high prices. The reason million dollar homes are selling well is, because these buyers are wealthier and have the means. It’s in the middle and lower end of the market where sales have dropped.

Why? Probably because the buyers in this segment do not have the ability to buy and make the payments. That my friends is a structural issue having to do with income classes. It’s a much deeper issue than just saying it’s a buyers market. Cheers.

NAR says affordability index for people is now lower than 2020 based on loan data.

Why. This index is not based on the US median family. Only the subset of who have taken out a loan. So those who are buying in 2024, the price of the Median home is only 4x their income while it was 6x in 2021. They earn more money. So even in a crash, these are pretty well off families that are making purchases in 2024. But this also could be why there is low sale volume. The pool of people who can buy is smaller.

2021:

-The home buyer median income was 85k.

-Qualifying income was $57k.

-Median price home $357k @ 3.01 Mortgage rate with $1.2k P&I

-Payment as % of income = 16.9% (but home price is 5x income)

Affordability index = 148

2024

-Median home buyer median family income is 102k,

-Qualifying income is 109k.

-Median price home $427k @ 7.14% with a $ 2.2k P&I monthly

-Payment as % of income = 26% (but home is only 4x income) lol

-Affordability index = 93

NAR is good at massaging numbers to make things look good.

Just curious about the chart showing sales of $1M and above increasing whilst the $750k to $1M and the tiers below, are decreasing.

Would continual RE asking price increases suck sales out of the lower tier price buckets to feed the above $1M figures? Or is that just not meaningful.

At one time I was a RE Broker. I moved on once I learned there are only two types of agents. Honest ones and successful ones.

Happy thoughts – they may be qualified to work for uber?

AI will replace every low end white collar and sales job.

If house prices stay flat or even drop a bit between 2024-2030, and inflation is allowed to run around 3%+/-, then in six years houses will have effectively lost about 20% of their “value”. Time heals all wounds, we just have to wait for the Fed’s rate/MBS damage to subside. The Fed has to know by now that getting involved in MBS at all was a serious mistake. I hope.

“The Fed has to know by now that getting involved in MBS at all was a serious mistake. I hope.” LOL nice one, IMHO, you’re giving them wayyyy too much credit. I think these people truly convince that they did that to save the economy.

I still struggle to comprehend why MBS was needed to carry us through pandemic time. You can make an argument that QE was the right thing to do, maybe even short term rates decrease (not 0 bound though) but MBS when home price was already high before 2020….

Probably because perceived housing wealth is even more important to middle class financial confidence than stock prices. For some reason everyone believes that artificially jacking up the price of houses makes people “richer”, even though what it mostly does is increase home insurance and property taxes.

“Honey, this website says our house increased in value by $100k!”

“Really?! Let’s go buy a new car today!”

But what if inflation averages 4% over the next few years? Or 4.5% or 5%?

Well,it’s a start but still on buyers strike unless I see a fair deal,not seeing it yet.

I am looking for a small home with a minimum of 25 acres for a large work shop/small critter raising and a on the move firing range,want out in semi-totally rural area in NC/TN/WV region,prefer NC.

“More buyers are insisting on home inspections and appraisals”,these buyers are just crazy asking for these reports…..,the horror!

Nice to see an “actual” not seasonally adjusted chart. The actual chart depicts the real trend.

Mid-atlantic area for June:

New Listings up 4.1%

Active Listings up 17.5%

Showings down 11.7%

Buckle up, buttercup. It’s about to get bumpy.

To clarify, those are YoY numbers, not MoM.

Thanks for sending me the PDFs on the Mid-Atlantic housing market.

What is interesting is as existing home sales are dropping new home sales are still steady. Big Home builders are showing nice growth. Crazy scenario.

Lennars 2Q2024 earnings:

-New orders increased 19% to 21,293 homes

-Deliveries increased 15% to 19,690 homes

Toll Brothers 2Q2024:

-Home sales revenues were $2.65 billion, up 6% compared to FY 2023’s second quarter;

-Delivered homes were 2,641, also up 6%.

-Net signed contract value was $2.94 billion, up 29% compared to FY 2023’s second quarter; contracted homes were 3,041, up 30%.

During HB1, they both dropped big time. Now existing sales have dropped big time but not new homes. I guess if you can get a new home for the price of an old home…why buy an old home.

So among homebuilders, we have seen a bifurcation: the big builders are doing OK, but small local builders are not always doing very well, perhaps in part because they don’t have a mortgage subsidiary that can buy down mortgage rates. John Burns Real Estate has released some homebuilder survey results on this some time ago.

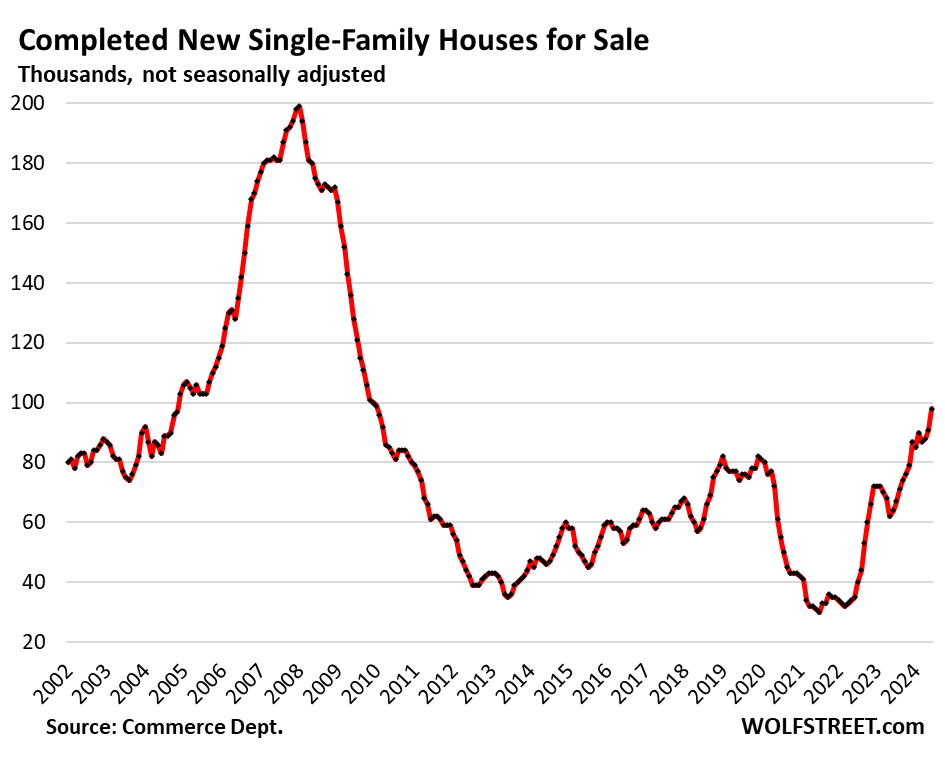

Also watch the increase in spec inventory (unsold completed houses – see chart below). That became fatal during the Housing Bust. But with new-house sales as high as they are, we’re far from it.

Hot off the press:

https://wolfstreet.com/2024/07/24/new-house-prices-solidly-below-existing-house-prices-inventory-piles-up-sales-hobble-along-supported-by-big-incentives-mortgage-rate-buydowns/

The list of inventory rises might be shocking on the face of it but in reality it’s rather meaningless given that it hasn’t had any negative effect on price. Here are the latest sale price per square foot YoY chance for the top 5 metros in Wolf’s list:

Tampa 0%

Orlando +1.85%

Denver 0%

San Diego +4.73%

Jacksonville +1.43%

Wake me up when prices actually start moving down.

I stopped building in Fort Worth, Tx in 2022 and new home prices are now about 10% lower than last year in the area I was building. Averages may be different.

Denver Case Schiller index peaked in 2022 and is now lower.

I agree with Vadertime

Even though the months’ supply charts indicates that the month of June is more or less equalizing with the years prior 2020. The active listing of existing home chart tells a different story. Before 2020 the active listing for the month of June (and for the whole year) is still substantial higher for the years 2019, 2018, and 2017 compared to 2024. And we know that in the year 2020 the low interest rates/QE increased the housing bubble in an artificial way. In that case comparing the last four years inventory would be more or less inappropriate. Seeing the years prior to 2020 are more telling as a whole to the housing situation. I don’t think inventory is at that stage where we are going to see price reductions as a whole. I think the market has a long way to go, if ever.