Powell to Congress: Higher rates are “the absolute best thing we can do for the housing market…” – “…particularly for younger people who are not yet in the housing market.”

By Wolf Richter for WOLF STREET.

However we want to interpret this, it’s fascinating. Powell told Congress on Tuesday: “There’s no question that higher interest rates are making it harder to buy homes in the short term. But in the longer term, this is the best thing, particularly for younger people who are not yet in the housing market.”

Did he mean that younger people would benefit from lower home prices, or at least an end of the home-price increases, and that higher rates are going to accomplish that? I don’t know. To speak that truth would be, sacrilege?

“Higher interest rates” means higher than they used to be, so even if the Fed cuts its rates a few times in the future, they’d still be much higher than before the pandemic, and mortgage rates would still be much higher as well.

The purpose of the higher rates is to “get back to 2% inflation for the whole economy,” he said, according to MarketWatch, “so that the housing market can be on a better foundation.”

These higher rates are “the absolute best thing we can do for the housing market and for the economy [so as] to sustainably bring inflation back down, so that people aren’t talking about it anymore,” he said.

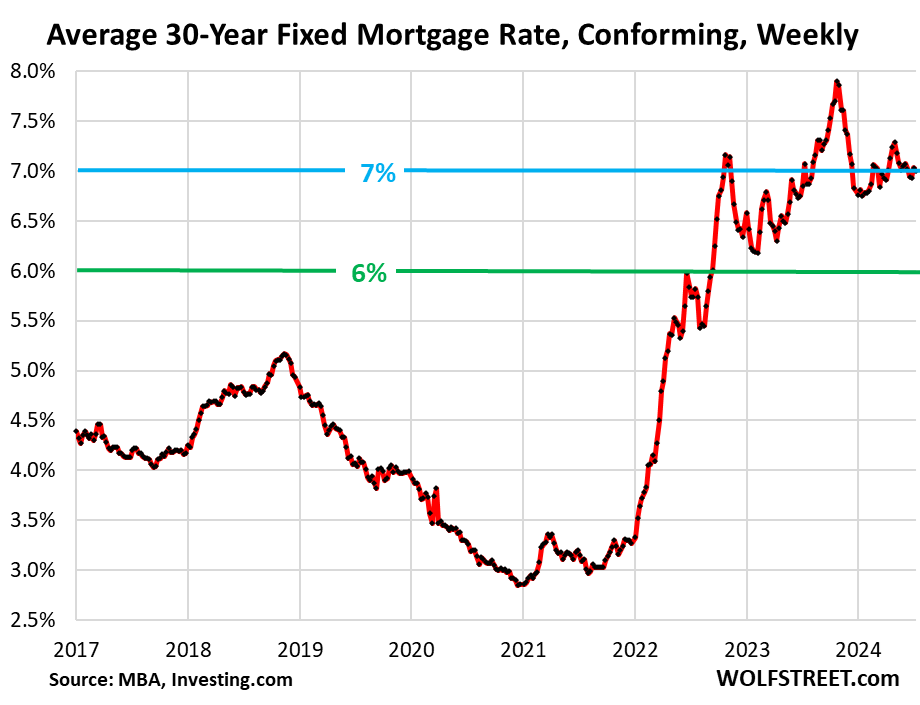

Higher for Longer: 7% mortgages a year so far.

According to the Mortgage Bankers Association today, the average conforming 30-year fixed mortgage rate was 7.0% in the latest reporting week.

The 7% mortgage has been a fixture in the housing market for a year. This measure of the average mortgage rate has hovered around 7% since July 2023, ranging from 6.75% at peak-Rate-Cut Mania in January 2024 to 7.9% in October 2023. It has been above 6% since September 2022.

People who financed a home purchase with mortgage rates at 6% or 7% or over 7% since September 2022, hoping that they would be able to refinance that mortgage quickly into a 4% mortgage, have gotten stuck with their mortgage payments.

These new homeowners with 7% mortgages and big mortgage payments may be forced to cut back spending on other goods and services, thereby lowering demand for those goods and services. The Fed is counting on them to do that. They’re one of the official transmission channels of Fed policy rates to the overall economy, to lower demand, and thereby lower inflationary pressures.

Potential homebuyers today have to do the same calculus: When will mortgage rates drop far enough to make it worthwhile refinancing a 7% mortgage, given the points and expenses involved in a refi? This is a tough call – especially since renting an equivalent house is now a lot less costly on a monthly basis.

Compared to the pre-QE era, a 7% mortgage rate is not breaking new ground: From 1970 through 2001, mortgage rates ranged from 7% to 18%. Lower home prices made those higher mortgage rates work.

But ultra-low mortgage rates fuel housing bubbles. When mortgage rates dropped as low as 5.5% in 2005, they fueled Housing Bubble 1, which led to the Housing Bust from 2006-2012. The pandemic-era below-3% mortgages did a wonderful job inflating housing prices in a historic manner.

But now, these 7% mortgages conflict with the too-high prices. And something has to give.

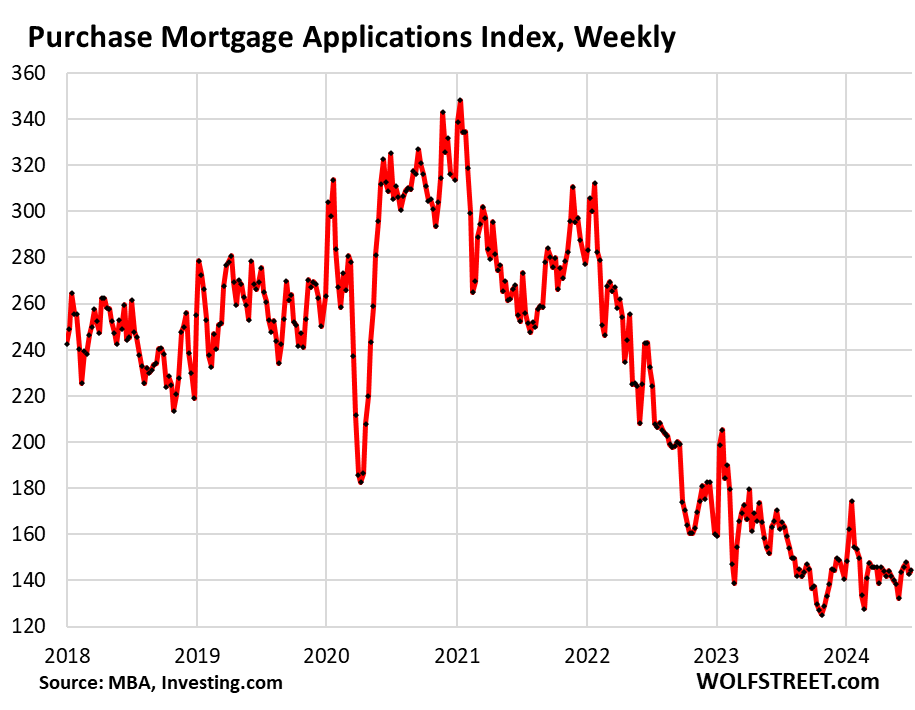

With prices too high, buyers’ strike continues.

Mortgage applications to purchase a home in the latest reporting week remained near the historic lows in the data going back to 1995, and have been there over the past 12 months. The record lows in the data were set in November 2023 and February 2024. Note the mini-spike in January 2024 at the peak of Rate-Cut Mania.

Mortgage applications to purchase a home in the latest week plunged by almost half from the same period in 2021 and 2019:

- From 2023: -13%

- From 2022: -36%

- From 2021: -47%

- From 2019: -48%

Mortgage applications are an early indication of home sales volume – an early indication that buyers who need mortgages remain on strike because prices are too high with those rates:

Inventory has been rising, as sales plunged amid rising new listings, and so active listings exploded in some metros on a year-over-year basis in June, and for the US overall, they jumped by 37% year-over-year. And there’s now plenty to choose from, but prices are too high.

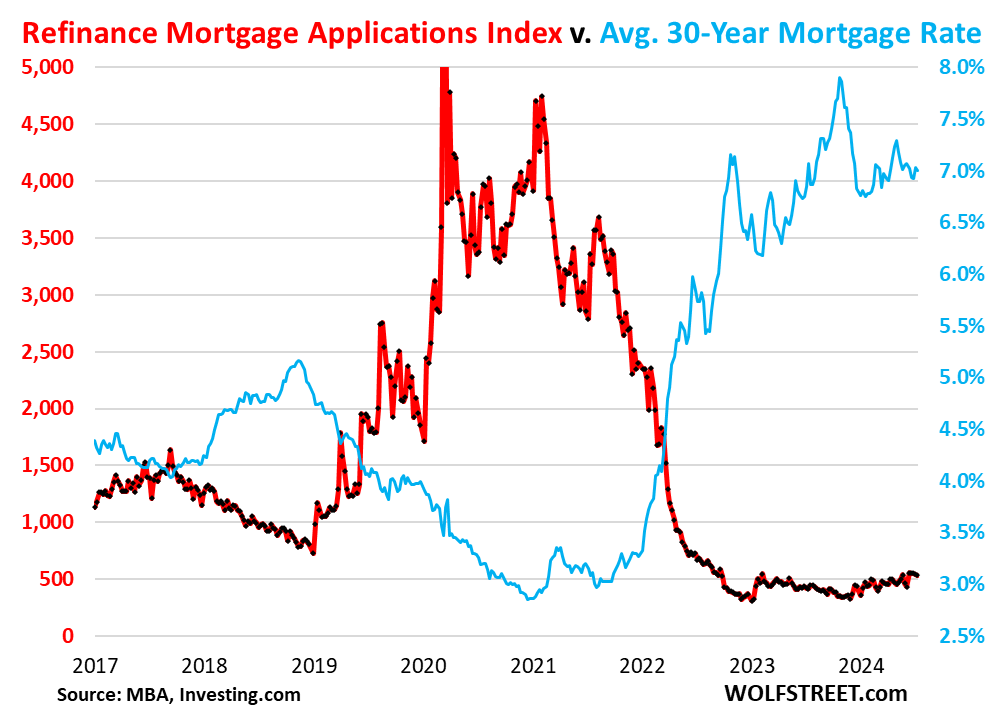

Mortgage applications to refinance a home collapsed in 2022 when mortgage rates surged, and have remained steadfastly at these collapsed levels. Refis without cash-out have nearly vanished. Most of the few refis that are still taking place are cash-out refis.

In the latest reporting week, applications for refinance mortgages edged down further and were down by 84% from the same week in 2021 and by 70% from the same week in 2019.

Refis are a function of mortgage rates. They had experienced a historic boom when mortgage rates plunged to the 2.5%-3.0% range. And they collapsed when mortgage rates began to surge starting in early 2022.

The chart shows the inverse relationship between refi applications (red) and mortgage rates (blue).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The housing market needs a complete and total price collapse. 70% off in many areas is what’s needed based upon incomes. We are in the most disgusting everything bubble imaginable, and it is still going. The FED whiffed with their pause. They should have kept raising, but instead chose speculators.

Collapse is a bit extreme, just reasonable decline to bring us back to 3-4x median wage fundamental would be a reasonable thing to do to balance things out for future generation, but nowadays even asking things to go back to fundamental is an extreme ask..

The time period is what is extreme.

“Collapse is a bit extreme”

So was, and is, the spike.

#RedBullCulture!

Gimmie more! I am losing my BUZZ

Struggler,

Red Bull and just plain Bull.

In my hood, in last 4 plus years, post covid, home prices increased almost 70% plus. Insurance increased 300% plus and lot of insurance companies flying out

CRE seems to be off about 70% and I don’t see a rush to buy in at new levels, of course I seldom buy high rises.

1981 was the best time to buy when rates peaked but it didn’t work out that way in 1990 when rates peaked. Still rates peaked about 9 months ago in this current interest rate cycle.

Each decade further into the MMT global experiment is a less opportune time to be unwealthy.

The knife has already trimmed the fat, and keeps trimming. Only the fattiest ones will be allowed to own, as they are being made “too fatty to fail.”

Who indeed WILL be allowed to OWN…..?

May you live in interesting times?

“Too Fat To Fail” DOES have a nice ring to it……good one!

MMT gets too much credit now, though…..FISCAL POLICY….TAX POLICY….

OUR WEALTH DISTRIBUTION LAWS……….should get more.

Powell finally came out and admitted that the neutral rate has increased. No surprise that he didn’t mention a number, but EVERYONE knows it ain’t 2% anymore.

What REALLY matters though is what do Congress & the Fed do when a real recession arrives? Do they trot out rent / mortgage relief along with generous unemployment benefits.

It will be COVID all over again, helicopter money falling from the sky.

Humphrey-Hawkins law requires stable prices. Stable prices is not 2% inflation! Do you actually believe what he (and some sites) say? Garbage in/Garbage out.

Fair enough but the problem with your 70% plung in home prices is that it would put the large majority of Americans in the unemployment line, including guys like you who pound nails for a living.

OutWest,

how is it that you know he ‘pounds nails for a living’?

is that a smug retort to people in general who work in a labor intensive job?

you know, not everybody can push paper around and make cool graphs with ‘dot plots’ and other really really important stuff like that..

and i guess you might be correct in your assessment that many people would be facing hardship.. except for you of course, presumably.

“is that a smug retort to people in general who work in a labor intensive job?”

As someone with both a basic office job and an ‘outdoor workboots’ job, I honestly enjoy working outside more…

I’m betting the bottom is in on housing prices.

How so, with some areas still setting record highs?

Is the bottom in for the S&P?

Time for more hikes? Take note: a Fed cutting cycle is rarely (never?) bullish.

This dynamic has become more global than in past cycles (IMO), with more areas exposed to foreign money. I also think that it’s more market-specific than ever before, with some “arbitrary” outside factors in play (such as insurance rates or availability of coverage etc.).

I am not a housing market guy, but I see tumult ahead.

The other side of this story is SELLERS are on strike too, which is why prices haven’t collapsed as everyone keeps predicting. In fact, the new consensus is prices will go UP A LOT MORE once rates come down enough for the buyer strikers to start buying.

6.0% mortgage rates aren’t going to suddenly cause 3.0% mortgage holders to stupidly give up the next 25 years of rock bottom house payments and sell their homes unless they absolutely have to.

Funny how one of the two fed mandates is stable prices. They managed to cause unstable house prices to the upside for the past 12 years. Now they want to create unstable house prices to the downside. Brilliant! I’d give them a 0 star rating in this category

but I am sure you gave them 5+ star rating when the price unstable was on the upside..

Yeah assuming he has the balls to stay the course with rates and not start cutting because unemployment tick up 0.1%…At least right now, SoCal existing sellers are stubborn in thinking they will win this Mexican standoff and play chicken with Pow Pow, perhaps they are convince Pow will blink first hence price barely decline around here, if at all. Existing inventory still painfully low and new home inventory is not as big part of the equation as other states. If rates does drop, who knows, maybe these sellers will get their wish as I can see FOMO buyers in SoCal rushing back in.

““There’s no question that higher interest rates are making it harder to buy homes in the short term. But in the longer term, this is the best thing, particularly for younger people who are not yet in the housing market.””

I know someone who just sold a high-end house on the California coast (literally, it’s across the street from the ocean). It took two years and a 40% haircut from the original price.

How cute that Powell is pretending to care about the young people now, after he’s done everything in his power to financially destroy them.

Exactly! He’s financially destroying a lot more than young people. Not everyone owns stocks. People living paycheck to paycheck can’t earn interest and surely are not getting 4% raises every year. My wife nor I have gotten a raise that high in years. Both companies are trying to cut back on costs. I want to live in this fantasy world I keep hearing about.

.. but the government data shows that everybody is getting huge raises!! so it must be true then I guess

Exactly, the 1% have no clue about the rest of us except that we are paid to much. Leading to the GREAT RESIGNATION.

And as for the 2008 bubble bursting, that bubble was based on the BANKSTERS TEARING UP ALL UNDERWRITING SANDARDS OF THE LAST MILLENIUM. YES MILLENIUM.

“When mortgage rates dropped as low as 5.5% in 2005, they fueled Housing Bubble 1”

sure, this added a bit of fuel, but stated income(liar) loans with a 2-3% entry rate with a 1 to 2 year fuse till adjustment up above 9% were insane. The PTB just watched.

Let’s not forget the 500k tax free profit for primary homeowners that turned millions of boomers into serial flippers roaming the country from bubble to bubble.

The fundamental error in the early 2000s that led to the RE bubble was artificially low interest rates. This kicked off the increase in prices well before banks made any changes in underwriting standards. Without artificially low rates, there would have been no bubble and no liar loans.

2008 was the destruction of massive supply, in the housing industry, much on the back end as it compounded but all along as well. Local collapse became national collapse as the fed financial-lized housing in line with banks and real estate interest. Clear as air corrupt. It was a changing guard in demographics and as family creation plummeted vs previous generation. Immigrants had more stability at ‘base’ jobs while Americans were sold Higher Ed fantasy that benefited very few. Now to their acknowledgment lots of bad loans there as well. The opposite of what they were told, and then basic needs inflated and pushed to the forefront of investment as we all have seen. Distract and rob, classic thief protocol that continues with marginal fine at the most. Americans were dubbed by their parents, government, and corporate world while they we’re ‘bettering’ themselves they we’re been robbed. Now if they fight the corruption they are left voiceless, homeless, saving less etc etc. Housing regulation, inflation, save the climate with more fiberglass tactics while housing rotates further into financial fantasy land and sits empty. Housing for occasional hotels or second home visits and it’s paid for by nothing but financial hot air.

“Recession is contained to young people” — the Fed, very soon.

It amazes me anybody trusts to Fed to do anything correctly. They’ve created such an inflation monster they won’t be able to cut rates till it’s far too late again (thanks, stupid dual mandate), at which point unemployment is going to moonshot and we’ll have asset fire-sales again. Cash will be king again.

“It amazes me anybody trusts to Fed to do anything correctly.”

Definitely agree that keeping rates too low too long was a big policy error, but to me they’re genuinely trying to keep things restrictive in order to quell inflation.

“they won’t be able to cut rates”

Why would they want to? That’ll just make inflation worse.

Sorry Wolf, forgot to change the autofill on a different device.

You: “genuinely trying to keep things restrictive in order to quell inflation…”

hahahaaa..hahah.ha wow, you got jokes huh??

thats cute you believe their ‘genuine’ efforts.. actually, no wait.. its disturbing.

when they telegraphed 3-4 cuts for this year, back late last year, was that a ‘genuine’ display of keeping things restrictive?

hahaha thanks for the laugh.

n0b0dy,

The Fed envisioned three rate cuts in 2024, as per their the median projection of the FOMC members in Dec 2023.

A year ago, inflation was cooling a lot, in an amazing manner, and everyone was amazed, and they were expecting the cooling to continue, but instead, we got some really ugly numbers the first four months of 2024, and so 2 of the envisioned 3 cuts vanished, as per their last projections, and they haven’t cut yet. And it has been wait-and-see all along.

Well they haven’t actually cut rates have they??

“they’re genuinely trying to keep things restrictive in order to quell inflation”

That must have been sarcasm, no one could be that gullible.

you: “Well they haven’t actually cut rates have they??”

what does that have to do with anything?

you do understand and realize that what the fed merely IMPLIES has a dramatic and outsized impact on the markets at large, right?

there is no doubt about it.

and why is that the case?

well, because the fed is the ‘magic money man’ (my label) and waves the wand of mystical ‘policy’ around at its leisure.

it doesnt matter if they ACTUALLY cast a spell, so to speak.. that the markets BELIEVE they will/wont is.

so PROJECTING such a large number of rate cuts, when it wasnt clear the battle was over yet had just as much of an effect.

want proof?

look at any chart of the s&p, nasdaq, or dow since late october 2023.

____there is literally no valid reason i can think of to be a fed apologist.____

unless you are in the millionaire/billionaire class… which i sincerely doubt you are.

Professional economists are stupid. They have achieved their objective, that there is no difference between money and liquid assets.

Don’t need to cut rates. Just increase the primary homeowner cap gains exemption from 500k to 1m and you’ll see a flood of inventory that will make the Fukushima tsunami look like a garden that was left on for an hour too long in the front yard.

ps. That will also unleash untold billions of equity for boomers to buy Treasuries with.

two birds, one stone.

No, make ALL real estate capital gains taxable, at the same rate as gains from stocks, no exemptions at all. Capital gain is capital gain, regardless of what asset class led to it.

I prefer treating all gains equally. I also think gains should be paid on appreciated assets that are inherited by fortunate heirs. These gains can be paid when the heir chooses to sell Grandma’s home.

No reason for a “step up” for rich folks who inherit assets. The government has a piece of all my gains, so why manipulate the system?

Check and balances went out the window with a tweet in 2017. It’s a bunch of clowns masquerading as gov officials coordinating as shady business investors

He’s a typical political hack. It’s almost like they pretend we went through a wormhole and magically find ourselves in this disaster of an economy when it’s been their policies, day after day and year after year that has brought us to this point.

Hanging is too good for them.

The only talent that gets you to the top of the DC sh*tpile, is the ability to shift responsibility/blame.

He’s just pretending. Asset bubbles are their number 1 priority. We’ve seen it time and time again.

The worst policy errors were made before Powell became Fed chair. Greenspan, Bernanke, and Yellen were the ones who created this mess. Powell has the unenviable task of trying to unwind the excesses created by his predecessors without crashing the economy. It’s a delicate balancing act, with an end we do not yet know.

That’s actually not true. Powell has been the Fed chair since its creation, and everything including fiscal policy is totally all his fault.

No, it began with the influx of Keynesian economists in the FED in the early 1960’s. The Gurley-Shaw thesis.

The coup d’é·tat was the DIDMCA of March 31st 1980 that turned the thrifts into banks. Reserve requirements were then scheduled to be eliminated.

except..

that he’s putting on a show of ‘unwinding the excesses’. not actually trying very hard. yah those other geniuses created quite a monster. but powell is cut from the same cloth.

the guy isnt a volcker for crying out loud.

perhaps you didnt know.. but sometimes economies need to ‘crash’. its called the business cycle. its what happens over time, since the dawn of commerce.

“People who financed a home purchase with mortgage rates at 6% or 7% or over 7% since September 2022, hoping that they would be able to refinance that mortgage quickly into a 4% mortgage, have gotten stock with their mortgage payments”

I believe those people are your perfect case of putting the cart before the house or sucker audience from their RE agents…oh yeah date the rate and marry the house right? LOL

Howdy Phoenix. YEP, anyone silly enough to purchase anything because some salesperson told them too ???? They deserve what they get…..

“have gotten stock with their mortgage payments”

If that was Nvidia stock that would awesome!

I was looking to rent a house a few months ago, the RE agent almost had me convinced to buy a new home instead because of the builder incentives.

I was considering it, then I went to bed and woke up the next day and realized interest rates, insurance, and home prices all were too damn high and returned to sanity. I rented a two bedroom apt instead.

Interest rates are not too high. Just the home prices, which will be brought down by higher rates.

Howdy Youngins. Have no fear, they will figure out a way to create a new bubble even if ZIRP is dead for decades……7 % interest to mortgage a home? The Horror? HEE HEE

Over 7 houses since 1979, 6 1/4% was my lowest mortgage rate. Highest was 18+% (1981).

Best purchase was in 2010 when I bought a 3 year old, 2,200 Sq. ft. brick home in Texas for $62/Sq.ft cash. My daughter lives there now.

Now debt free.

A drop in rates isn’t going to stop what is coming. In fact, it might drive more inventory. Which ultimately will bring down prices. Sure it’s anecdotal. But it foretells what is coming elsewhere over the next 3-5 years.

In January 2022 a 1000 sq ft 2BR 2BA fully furnished condo right on the beach in Sunset Beach SC could be had for 250-275k, in a large complex with all the amenities. Just today, came the first listing in that complex for the ‘same’ unit, under 150k. I’m betting you could buy it for 140k or less, given that there are a dozen others for sale. Next year at this time they will be 125k and heading lower from there.

It’s coming to your town, it’s just a matter of time.

It’ll happen even faster if a hurricane hits there this summer.

Eric can you provide Sunset Beach SC zip code? I can’t find it, only Sunset beach NC, would love to know where these condos are really located. Maybe complex name also.

me too

I’ll bet if you provided a zip code, prices would rise, as there are so many here who would love what you described

Are people finally realizing that beach-front properties are going to be underwater (in more ways than one) pretty soon?

Maybe I’m the only one who heads for the hills…

MW: Dow closes up 429 points and logs best day since May, S&P 500 ends above 5,600 for first time…

assets like stocks and houses are not priced for 5.5% interest rates, they’re priced for 0. the collective hope is that the natural order of rates is zero and if you can just hold off long enough, you’ll get them again. stock valuations are worse now than y2k.

Everyone is still fighting the fed?

I called that yesterday.

My S&P gains were noice!

The view from this summit is pretty pretty good!

Another house of cards. This too shall pass/implode. Will be the best thing to happen if it does.

I hate the whole situation of the unaffordability but… I am glad that Powel et al isn’t lowering rates (even though I perceive lower rates would benefit me in the short term I think it would reheat every asset valuation). I am in the camp that I wish rates were higher for a small time but I feel like maybe.. just maybe JPow is going to slowly unscrew this crappy situation without a crash… but I go back and forth between views of wanting a high rates/crash asset prices vs no crash vs stupidly zirp the can down the road forever. Thanks wolf!

Wolf, I think you meant “October 2023”, not 2024.

Good catch

7.9% in October 2024. I believe it should be 2023. Will just tag along rather than start a new post

Yes, thanks.

“ have gotten stock with their mortgage payments.”. I think you meant “stuck” not “stock”. But I guess if they had bought stocks instead of a house they would be better off…

“There’s no question that higher interest rates are making it harder to buy homes in the short term. But in the longer term, this is the best thing, particularly for younger people who are not yet in the housing market.”

I may be stupid, but wouldn’t NOT lowering the FFR to ZERO in the first place, and NOT purchasing massive amounts of MBSs ever (among some other things), have possibly accomplished something similar to this goal by not even creating the damn bubble in the first place?

I swear, these jackholes are just evil.

not evil, just stupid and incompetent, and unwilling to admit it.

Highly unlikely.

Deliberate, malicious, deceptive, and fraudulent are observable and experienced. It’s not what they say, it’s what they do.

People fall for it over, and over, and over. Not sure why. Personally, I don’t listen to a word they say.

I read here for wolf’s recap, simply to gauge which way the winds of public psychological manipulation are blowing. Then I look into the possibilities of whatever is opposite that.

franz,

that you, or anybody else for that matter, have the opinion that,

ohh.. they’re just stupid and incompetent

is a major part of the problem.

these people are NOT stupid. you just dont understand the difference between a ‘stated purpose/mission’ and the ‘real purpose mission’.

how one deduces the ‘real purpose mission’ is taking into account the actions and their effects, not so much the words being spoken.. although certain words dont necessarily mean the same thing when they say them as they do to you and i.

what was it george carlin said? about the ‘big club that you arent in’ ?

yeeaaaahh.

Not like they can go back in time and undo those decisions.

Yeah, this. Maybe don’t hold rates at zero and buy MBS hand over fist well after the pandemic finished? You think maybe that wouldn’t have been a little better for the young people? What a clown.

Not to mention NOT blowing off inflation as “transitory” when he was apparently the only one of 320 million Americans oblivious to how bad it was and what was causing it.

Absolutely! Came here to say this.

“But in the longer term, this is the best thing, particularly for younger people who are not yet in the housing market.”

This would be the case if it were not for the weak temperament (to put it lightly) of JPow and the Bailout Boys (fed). They don’t have the stomach to even hurt the FEELINGS of asset holders let alone cause any real pain enough to force homeowners to sell and reduce home prices even a little bit.

At the first sign of any pain in March 2023 they threw away all their hard work and rushed back in to rescue the banks (SVB uninsured depositors, extending FDIC insurance to everyone), making sure no one else would have any worries at all (forget about any semblance of pain or forced selling). Hence the current standoff situation.

They are the most pathetic institution I have ever witnessed and have caused more pain and suffering to all on the wrong side of the wealth inequality spectrum than anyone.

The solution for many urban areas is rent control. It has worked for the good of the working class around the globe. Almost surprised it has not already caught on in California.

Rent control is the solution??? You must be joking. Ask renters in rent controlled apts in NYC or any other urban city how their apts have been maintained. Landlords lose money on rent controlled apts, stop making repairs, stop all capex needs, tenants eventually have to leave the rat infested tenements leading to urban blight, deteriorating neighborhoods, etc etc. Cruise through 1/3 of Detroit that has been shut down / closed off to see the results of rent controls.

That is your take. Have two friends in NYC who could not afford their flats without rent control. Nor are their homes rat infested, etc.

Not a good time for slumlords etc!

Then they probably shouldn’t live in NYC.

Crazy idea that if you can’t afford to live somewhere, you shouldn’t. Because we live in a world where everyone has the right to do whatever they want regardless of their ability to pay for it.

Some California cities have had rent control for decades and the entire state of CA (and OR) have had rent control since 2019.

From my name people know what I do for a living (and why I think about this), but I have always wondered why we just have “rent control” and not price controls on other things like cars, food and gas (when gas in CA often costs twice as much as gas in TX).

It would be easier to keep rents low if my insurance has not doubled in the past five years along with the cost of carpet and many other things.

ApartmentInvestor,

As you know, it’s NOT universal rent control in California or in cities in California. Only certain buildings are under rent control.

In San Francisco, only multifamily buildings with for-rent apartments built before 1979 are under rent control. Everything else is market rent. And when the rent-controlled unit goes back on the market, it’s at market rent.

Condos regardless of age are not under rent control. Apartment buildings completed after 1979 are not under rent control. Single-family houses, townhouses, ADUs, etc are not under rent control. They all rent out at market rent.

After this law went into effect, landlords started converting their pre-1979 apartment buildings into condos to escape rent control. They didn’t sell those condos, they just rented them out without rent control. Those conversions were eventually stopped by the city.

Rent control means that annual rent increases are limited to the increase of the local CPI – fair enough. So if the local CPI is 4%, you can raise rent on your pre-1979 rent-controlled unit by 4%. And you can raise the rent of your 1980s unit by 20% if you want. This type of rent control has advantages for landlords: they retain stable tenants that pay their rents because they don’t want to lose the apartment. So a landlord doesn’t have a vacant apartment, and thereby doesn’t miss the rent payments, and doesn’t have the expenses getting a unit ready for listing it again. So it works out in many cases.

When the unit goes back on the market, the landlord can ask for whatever rent they want to see if someone bites.

The state-wide rent control is a lot looser than the SF rent control, including much bigger rent increases.

New York City has a rent control law that gives rent control a bad name. It’s a huge mess. That’s not the case in California.

Thera are other essential services with price controls, such as property insurance (insurers have to get state approval for premium increases), electricity (PUC has to approve rate increases), trash removal (city contract), etc.

It’s a fundamental rule of economics: an artificially low price creates a shortage.

Rent control is Exhibit A of this phenomenon.

I guss we studied economics at different schools.

Food is a good example. There were no shortages when there was goverment price supports for many basic commodities.

Just like there is no housing shortage. Put the screws to the owners and they will sell all those empty shacks.

Perhaps a yearly federal tax on all non primary homes. 10% of value seems about right.

Before I sold our portfolio of homes every home was owned by an individual LLC. Good luck finding out who owned each LLC the government can’t even tax the 1% adequate you think they can administer that type of stupid tax?

Lawyers can easily pierce the corporate veil, kracow.

@kracow those LLC’s income flow into your 1040 still. It’s not as hard as you think to track. Former CPA and current software engineer. Depending on how the data is stored that could be as easy as a couple hundred lines of code. Since it’s the government and my guess is their system designs aren’t great. I’m thinking maybe a 4-6 month project with 3-4 contract engineers. Even at year it’s still not that expensive or time consuming to do and conceptually it’s easy code to write.

What school of economics did you attend? A 10% tax on non-primary residential property will increase rents by 10%. Unless, you intend to somehow only tax those that have a second home, non-investment/rental property. AirBnB would then create an easy loop hole for that tax.

How about keeping the government out of housing and understanding the critical flaw in logic that prices create unaffordable houses. If they were “unaffordable” no one would be buying them, and the prices wouldn’t be going up. Mucking around with the market creates unaffordable and lower quality housing.

A good many baby boomers recently retired with more than they expected in their retirement funds. Do we blame them for paying cash for the property they want? Not me. I’m loving these retirees and big city transplants that are driving up prices in our Midwest market. It’s about time we got to enjoy some of the crazy appreciation usually only seen on the coasts.

I’m doing my part and cashing in. That’s a few less rentals available, but a few more “affordable” houses.

The government (Federal and State) heavily subsidize Agribusiness of all sizes in a myriad of ways including property tax deductions, not charging sales tax (in OH anyhow), government crop insurance, preventative planting.. the list goes on. Look at the size of the Farm Bill. We’re all paying for cheap food.

Commodity price floors are artificially high prices, not low. That guarantees plenty of supply… artificially low prices depresses supply.

Perhaps your tax on all non primary homes purchased after 12/31/24. Don’t penalize me because I was smarter than the average white boy.

Yes, but savings are supposed to match investments.

Rent control leads inevitably to a shortage of rental properties. No free lunches.

Nah. But it does make millionaires out of frugal renters who know how to hustle…ask me how I know…

My friend Rob made more than $1,000/month for close to a decade from his San Francisco “rent control apartment” in Presidio Heights. When he bought a home on the Peninsula he subleased his apartment to a friend for more than his rent, but less than the market rent so it was a “win win” for both of them. He leased to others before his landlord went into a rest home and her kids were able to prove he didn’t live there and end the lease.

ApartmentInvestor,

yes, landlords have to stay on their toes. That’s all you’re saying. If you’re on autopilot as landlord, it’s going to cost you, that’s what you’re saying.

RE: All the above

We have systems of “deed restriction” in our area (Telluride CO). There are all sorts of different flavors and styles of it, some cap appreciation (mine), and most have some income or net worth restrictions too.

All are meant to house people who will work in, and contribute to the local economy (some can be owned by anyone and the occupant is subject to the requirements).

All this to say: if there’s a rule, it’s because someone has played the system. Also, all the rules have a workaround (I am sure it’s not “legal” to arbitrage rent-control. Similar things happen here).

The first thing I would do is get rid of the RealPage cartel and at least incentive landlords to get back to something resembling a competitive market. Still waiting on either the Senate bill or the DOJ investigation on that. I’d be really interested to see what prices do if landlords were forced to just pick a price and stick with it. Price the units in reference to what they cost. I think we’ve taken this whole “highest price the market will bear” thing too far when everyone is using algorithms and coordinated artificial scarcity to wring every last dime out of people.

I do some volunteer work, medical and disaster response stuff. Our coordinator was telling me that every organization has been struggling to find people, especially since COVID, since everyone is working two jobs to survive. Capitalism where profits are derived from artificial scarcity rather than production is obviously corrosive to society. Do we serve the market or does the market serve us?

Ok I’ll get off the soap box.

Thanks Wolf! These last 3 articles on housing and autos are all great coverage/context. I was looking at the raw data this morning, finally got power back after the hurricane here.

People wishing for 1% Fed rates and 3% mortgages should get a clue. The only way that is going to happen is if we have another GFC or equivalent, and it will not be worth it. Accept the FACT that interest rates are at historical norms RIGHT NOW.

The new normal is the old normal.

Well if this is the “historical norm” that means half the time they should be HIGHER. And I’m fine with that. Cash actually earns interest and is an alternative to the stock market. Taking on debt had a cost and involves risk. This needs to happen to a greater extent.

Waller: “central banks were disillusioned with policy analysis that was focused on monetary aggregates”

Too bad. Nothing’s changed in over a century.

Wasn’t just the Realtors, back then you had the financial pundits claiming six rate cuts coming in 2024.

“We have to destroy the village in order to save it”

That’s what a commander once said in NAM. He took a lot of flack for it and deservedly so. Unfortunately, the housing market today has been so distorted by the pandemic’s ultra low interest rates, massive federal budget deficits, and the Fed’s irresponsible money printing over the last 2 decades that there is NO WAY OUT of this housing debacle.

We may have to destroy the housing market before it can be saved.

blame the people, not just the fed. the people have demanded stuff way beyond what the country can afford. the fed was just the dope dealer, not the junkie.

There’s a monologue in the movie “Margin Call” where the Paul Bettany character expresses a similar idea.

Jesus, Seth. Listen, if you really wanna do this with your life you have to believe you’re necessary and you are. People wanna live like this in their cars and big fuckin’ houses they can’t even pay for, then you’re necessary. The only reason that they all get to continue living like kings is cause we got our fingers on the scales in their favor. I take my hand off and then the whole world gets really fuckin’ fair really fuckin’ quickly and nobody actually wants that. They say they do but they don’t. They want what we have to give them but they also wanna, you know, play innocent and pretend they have no idea where it came from. Well, thats more hypocrisy than I’m willing to swallow, so fuck em. Fuck normal people. You know, the funny thing is, tomorrow if all of this goes tits up they’re gonna crucify us for being too reckless but if we’re wrong, and everything gets back on track? Well then, the same people are gonna laugh till they piss their pants cause we’re gonna all look like the biggest pussies God ever let through the door.

Franz:

I have never observed a court in which they dismissed the cartel leader in order to pursue the junkies.

The rumor was that the G-man let crack into minority communities in the 80s (while the regular old powder was still “dignified.”). They proceeded to create the most highly incarcerated population ever.

They have now done it again!

The Federal Reserve has been SHRINKING the money supply and has in engaged in QT involving TIGHTENING CREDIT for a long time.

2 years of QT doesn’t cancel 20 years of drunken sailor.

I thought it would have, at least some.

Drunken sailoring?

lets draw up a little scenario..

someone has been eating anything and everything for a decade or so, and they now weigh 400 lbs.

then, they decide.. hey i weigh too much. im going to ‘shrink’ my waistline:

by eating one less box of donuts a month from now on…

uh huh? u see now? your ‘ALL CAPS’ hide the fallacy of your logic.

LMFAO!!!

Sadly this is the same philosophy Milton and his Chicago boys applied to other countries around the way and wreck havoc across countless lives …

Best thing we can do is to hopefully not glorify these Aholes and document truly how terrible their ideas were, similar to how we all know trickle down doesn’t work, at least not in any economy reality, in a certain fetish segment, perhaps trickle down is a thing..

Milton would never have advocated for QE and ZIRP, that’s for certain.

There is only one way out. Waller, Williams, and Logan seem to agree. They “believe the Fed can keep unloading bonds even when officials cut interest rates at some future date.”

Yes, that has been the announced plan since shortly after they started QT — so markets don’t get their hopes up. They have separated interest-rate policy from the act of “normalizing” the balance sheet. And that makes sense.

If we destroy it, it will not come back in the same form. We sit upon the precarious edge of the baby boomer demographic shift. The aging population, is top heavy in both age and wealth. The age (retirements and older millennials) are driving more movement in housing and the wealth is pushing up the price.

When that top starts shrinking (dying) the property values will fall. Some of the wealth will transfer, but that being invested in properties today will evaporate.

I’m predicating life in the U.S. is going to feel a bit less first world and look a bit more like the 1970s, but with many more empty commercial spaces.

I may add, if you read Powell’s comments from Wolf’s post, I think he said the same thing I said if you read between the lines. For once Powell is on the right path. Keep up the good work JP.

Today:

“ Homeowners were sitting on a collective $17 trillion in equity at the end of the first quarter of 2024, according to CoreLogic. In just one year, homeowners gained $1.5 trillion, or $28,000 per borrower”

Then:

“ When home prices began to fall in 2007, owners’ equity in household real estate began to fall rapidly from almost $13.5 trillion in 1Q 2006 to a little….”

Ny fed paper, Household Debt and Savings during the 2007 Recession, is a locked pdf, but it continues…

To a little under $5.3 Trillion in 1Q 2009….

There’s a lot of cash trapped in this housing bubble and a sellers strike just delays a very rude awakening

After 2009, I remember bagholders all over the place decrying “where did all the money go?”

I, as a non-bagholder, was curious about this, so I did some research and came to the following conclusion:

All money paid by buyers above fair market value was simply value that was willingly transferred over to sellers, and the price at that level was an illusion.

The money didn’t disappear, you just paid $30 for a $10 steak. Enough grifters lied about the steak being worth $30, and lying even further that it was headed to $60 in the future, that you paid it.

Far too many who had lost their houses at that time that were underwater due to taking out a 95-100% mortgages or they had previously refinanced out their equity.

Its hard to shed any tears for someone that lost their house after leveraging it for cash.

Squeezed:

Except that we’re all instructed to do so!

Invest in yourself they told me. Increase your velocity of money (unlock your equity!) they told me. You can trust this business, government and market they told me!

I have struggled with trying to “up” my financial game. Even working in the sector myself for a time. To discover the rotten truth and lies underpinning SO MUCH of the system!

In 2006 I bought two homes from a Sacramento investor in his 80’s that wanted to get out of the rental business and like the millions of others that bought homes from 2005-2007 I had homes in 2009 that were worth way less than I paid. Like the majority of the millions of people that bought from 2005-2007 I kept paying off the loan and today I own two homes free and clear that Zillow says are worth more than double what I paid that have gross rent of over $3K each per month. I’m sure that we are going to see more home values drop and some people will lose homes to foreclosure, but for those that just keep paying down debt will be fine.

Equity != cash

And all those mortgages are being traded as securities. Perhaps it is in the best interest of the security holders (or whomever holds whatever holds these mortgages) to prolong their holding for as long as possible. Because once Powell makes it easy to sell AND buy, people are going to start moving all over the country again. Thereby resetting the cycle and bubble 3 will start forming.

re: “And all those mortgages are being traded as securities.”

Excellent point. That was the prediction in May 1980.

High housing prices go to sellers and builders; high interest rates go to oligarch bankers, the same kind that are stockholders and voters in the Federal Reserve. It is left to the student to determine the path the FOMC will take.

Residential mortgage rates have NOTHING to do with the Federal Reserve and are based on the yield of 10 year US Treasuries plus around 3% which would put them around 7.25% now and headed much higher.

Except when fed buys trillions of 10-year treasuries and hundreds of billions of MBS. Which of course they did.

The small purchase of those securities had little to no impact on the yields in those asset classes.

🤣❤️

Sure, just like the small amount of house purchases in 2021/2022 that were funded by a small amount (Trillions of Dollars) of MBS, created with printed money out of thin air, had little to no impact on house prices (only 40% increase, no biggie and mostly shrugged off by 25-year-olds just starting their career).

LMFAO!!! (again!!)

“buyers who need mortgages remain on strike because prices are too high”

@Wolf,

Is it really that people are on strike, or is it that the majority of people would be more than happy to over-extend themselves, but just can’t qualify for a loan?

Rates are NOT too high, however the cost of housing is.

Exactly. It’s a matter of qualifying *total household income ex pre-existing debt*, not rates or prices.

The most affordable of the 50 largest metros in the United States is Pittsburgh, PA, where 26% of renter households can afford an average priced home. That is the tippy top most favorable situation!! At the other extreme, we have San Diego, CA where 2.6% of all renter households can afford an average priced home. Also, I get it that average is higher than median, so being ultra-conservative, you double the percentages, and the picture is still horrific.

Damn that’s a sobering statistic. Back in the old days the Midwest was filled with small towns where $35k a year got you a house and a car and clothes for your kids. That would be maybe $75k now. I hope those places still exist.

About half the apartments in America are studios and one bedroom units. Very few single guys or gals in the US “renting” a studio or one bedroom have EVER been able to buy an “average” priced home (that in most markets has 3 bedrooms and costs more than half the homes in the market aka more than the “median” priced home). If you talk to realtors that have been selling homes for decades they typically show couples moving from apartments the “cheapest” or “oldest” homes to buy for their first home, not an “average” priced home. My first homes (and investment properties) were all low priced fixer uppers and with rare exceptions (inheritance, family money or stock option cash in) everyone I know bought a first home that was cheaper than “average”.

By the way, about 183 million people live in the top 50 metros.

Probably a combination – I know some people sitting on the sidelines with large down payments earning 5% and I’m sure others can’t qualify. Although not qualifying seems harder to believe, I got pre-approved for an amount that seemed ridiculous and irresponsible – like sure I could make that monthly payment but I’d probably barely be able to afford food, cell phone bill, and gas and would have to skip the 401k contribution and have nothing go wrong in life like a car repair being needed. Mortgage lenders are desperate for business.

I’ve experienced the same silly high approval, as have both of my daughters.

It’s the same same old game. The bank is happy to approve you for the fees and sell that mortgage (risk) to Fanny and Freddy (investors).

Real estate is not a national or regional thing. Its still location, location, location. Many live in “big metros” 25mil or so in the TOP 10 largest. That’s a small fraction of our 330mil US population. According to my Alexa :)

The market does not seem to be cooling here in Northern Illinois. That said, second and third cities tend to lag behind in both run ups and run downs.

There are many new pressures in the market. Remote work, sky high stock portfolios, historic level of retirees, climate disaster concerns, and chasing “affordability” all driving the migration people. None of these are directly controlled by the fed.

STR’s are the X factor in this housing skid, they didn’t exist back in 2007-2008 and the owners don’t live there, so not much in the way of social ties to keep them there, nor do their kids go to the local school, nor do they know their neighbors, who might be another AirBnB, so no great loss there.

It’s a very different dynamic from the usual homeowner, and cities are coming down on them now, as they realize what a detriment they are.

@Xavier Caveat it is important to remember than there have always been short term rentals in the US. When I was a little kid you needed to call a Tahoe or Outer Banks rental firm to rent one, by 2000 most rental firms had web sites where you could book the homes and AirBnB and other companies made it cheaper and easier to rent a vacation home without paying a management firm 30-50% of income so the number increased, but it has always been around 1% of the US housing stock and if STRs go back from a little over 1% of homes and apartments and condos to a little under 1% of homes and apartments it will not crash the US housing market (people are not going to stop renting homes in Tahoe or the Outer Banks any time soon).

I don’t know how it worked 20 years ago, but none of the rental companies in the outer banks charge short term rental guests fees for the management of the house. The fee is charged to the home owner for managing the property and varies based on the size of the house and comes out of the Gross Rent, which is what you see advertised. The guest pays the occupancy tax and cleaning fee, any mandatory or optional insurance. Some companies try to add a nominal booking fee or other BS fee but that is rare. They all advertise the same houses on AirBnB, and you pay another $300 or so on top of it all if you decide to book through another website.

The price of everything will continue to rise when printing a trillion dollars every 100 days just for interest regardless of interest rates. Zimbabwe 2.0.

Nobody is printing any more. The deficit is offset with taxes and treasuries. The Fed is tightening and the money supply is falling. Inflation is falling.

“The deficit is offset with taxes and treasuries.”

kent? are you…. i mean, WHAT???

a DEFICit is a DEFICIency of something.. a shortage.

a treasury is a bond… an obligation OWED. that in itself is a DEFICIENCY.

you cannot ‘offset’ deficiencies with other deficiencies. that should be completely obvious, yet.. your statement illustrates there is a DEFICIENCY of understanding, seems to me.

and as further proof of what im stating here.. treasury securities are treated like what in the financial system? LIKE CASH. so, by creating more treasuries, to fund ever increasing expenses/outlays, its effectively the same thing as printing the banknotes via a different ‘pipeline’, so to speak.

and as a last point.. if there was ANY ‘offsetting’ to the ‘deficit’ you cite here, then the national debt wouldnt increase, would it?

In Kent’s defense:

I saw a headline cheering the IRS for collecting a BILLION dollars of back taxes from the wealthy!!!

All they have to do is, THAT! (100X a day, every day, forever?!?)

Thank me later….

n0b0dy,

There are two types of capital that companies can raise from investors:

1. Debt capital (by selling bonds, borrowing from banks, etc.)

2. Equity capital (by selling shares)

Debt capital matures at the end of the term and then has to be paid back (unless it’s “perpetual” and then it’s a hybrid, such as preferred stock). Companies usually sell new debt to raise the cash to pay off the old debt when it matures, and so debt capital cycles on.

Equity capital does not mature and does not have to be paid back, and so it cycles on by itself. That’s the big difference between the two.

Governments generally don’t raise money with equity capital. They raise money via debt capital (selling bonds). And debt capital matures and has to be paid back, usually by selling new debt, just like companies do.

On the other side of debt capital and equity capital are investors that hold these assets with expectations of some kind of return.

There is no issue with any of this. The issue arises when debt capital is so large that the issuer has trouble paying interest on it, and raising new debt capital from investors to pay off the maturing debt capital. Governments that issue debt in their own currency generally will always be able to pay interest in their own currency, and pay off maturing debt in their own currency, but they can and do destroy their own currency – THAT’s the risk here.

…hmm. Reckon we must reckon with the certain ‘immortality’ of a national debt, vs. our own personal sure exit and acquisition/administration of the same (…would also not suggest trying the national system at home, kids (I mean the ‘kids’ term inclusively for us of ALL ages before you fire those mortars), though many seem to…). To rephrase a recurring statement of another poster: ‘…not sure if this was is EVER gonna end…’.

may we all find a better day.

@#$&! – artificialautowhatever. ‘war’, not ‘was’. Apologies.

may we all find a better day.

The FED could nationalize the banks, reinstate reserve requirements, and raise levels to whatever level was required to cover deficit financing.

I would love to see a Fed Fund’s rate cut in July. I’m now at the point where I’d like them to get it over with, and see what happens. Worst case, it drives long bond yields much higher, which is also the best case for renormalizing the economy.

Interest rate manipulation was started by William Mckensey Martin in 1965.

“I would love to see a Fed Fund’s rate cut in July”

How about no.

you know what i think might be the solution to this whole problem?

it sounds crazy, but it just might work..

the fed should INCREASE or DECREASE the interest rates at random every single policy meeting. like im talking put -0.5%, or +1.0% on a piece of paper in a hat type of random..

now, im not suggesting it be so crazy to the extreme that it would potentially increase/decrease by more than say.. 1-1.25% max, so there would be a ‘cap’, so to speak.

this suggestion would take the feds ‘magic money man’ effect out of the equation, nothing they can say will have any effect anymore since the action will be limited to a random event. so there wont be the minute analysis of every single word they say, or how many times they say, something, which happens at present.

the market would then be much more ‘free’ to go in peace without being slapped around and pushed to one corner or another by its pimp the fed.

of course, what im suggesting will NEVER happen. but i think it would work wonders for the situation we are in now.

we live in crazy times, and a ‘crazy’ solution might be the one needed…

n0 – …kinda like a casino promotion hyping ‘loose slots’?

may we all find better day.

When are you going to get it straight? Even the news media panders to their keep their ratings up. A student of the economy understands. Interest Rates are NOT too high. Take a look at the average interest rate on a 30-year fixed rate mortgage over the past 30+ years. The average rate is close to 7.50% – 7.75%. It is NOT the interest rates, it is the cost of the house!!!!!!!!!!!!!!!!!!!!!!!! There is little affordable housing available. Corporate investors have purchased a boat-load of homes in recent years. Builders have not built enough to keep up with demand.

Prices are too high, not rates.

Absolutely. High real rates of interest need to be firm

Not sure why anyone thinks wealth concentration will not just continue to happen and accelerate. Good luck for new home owners getting in the market. If a drop comes then cash buyers will move in. Sometimes a new normal just arrives and there is really nothing that can control it. Admittedly solutions exist but not that will work in this country.

A lot of the inequality and income that has happened in the last 20 years has been because the Fed artificially held interest rates below market. This greatly benefits private equity types and large stockholders who can utilize the low rates to leverage their businesses. It also impoverished average retired people who rely on Bond portfolios and CDs for most of their retirement income. If interest rates are allowed to reach their natural norms, it will be good for inequality.

The other part of inequality which will not get better is that there is just much more value for certain types of high-end mathematical and analytical skill in the market than there was 50 years ago. This is not going to change going forward.

A friend just had a kid graduate from Cal with a math degree (and an interest in data analysis) his “starting” salary was $178K.

It has been just over 100 years since my grandparents (who all had less than a 6th grade education) came to the US from Ireland and Scotland and soon got married and bought homes for just under $3K in San Francisco and raised kids making ~$100/month before WWII.

It has pretty much been getting “harder” for most kids to get ahead every year I have been alive (my Dad who didn’t go to college was making about $10K/year when he bought a home on the SF Peninsula for $24K in the early 60’s that Zillow says is worth $2.8mm today).

It is still possible to work hard and get ahead by spending less than you make and investing the difference, it is just harder…

Apt. – would venture it has been getting harder for all classes of our citizenry to even consider putting their own skin in the game for our uncertain nation to soldier when the time arrives…(past performance is no guaranty of future (beyond next quarter) results)-so rolls history’s wheel.

my we all find a better day.

The world is changing. We will or be left in the dust. Put your money where money is going, not where it was.

Best comment of the article!

Complete collapse coming. $12k Mortgage payments? Sell now go into rental for 2-3 years and pick up nice hefty $300-500k. Same cycle yet people forget.

Or most think this time is different. Go to SoCal and you’ll hear this as the gospel being spoken by the majority around here. Housing will never go down they say….it’s such a blasphemy to even think it can..

…at least until the water runs out…

may we all find a better day.

This time is always different, until it’s not.

Although any suffering of anyone has become unpopular so the politicians will probably do anything it can to keep the bubble inflated. Instead maybe they’ll come out with buyer assistance or 50 year mortgages. So this time might be different.

We need a mild downturn to push a lot Airbnbs and second homes onto the market. If prices actually start to decline, the panic selling to not be the last one out the door will start. Instead we have National Realtors association and most popular media talking about rate cuts and prices skyrocketing. If the narrative changes I think we’ll see a lot more inventory.

Agreed, but not sure on the time line. Who would of thought back in 2019 that we would be where we are now.

Yeah Wolfman, I’m seeing 3 bedroom 2.5 bath 2 car garage townhomes in Panama City Beach (that were selling for a peak price of $330,000 when the 30 year rate was 3% back in early 2022) are now listed for $290,000.

Also same townhomes were selling for around $230,000 in spring of 2020.

Even rents are now $2000 to $2100 for the same townhomes, which were the same rents a couple of years ago.

Perhaps income will steadily increase at a greater rate than housing costs, so it will be more of a soft landing as far as housing price correction.

Half the buyers typically for these townhomes are investors, and they are remaining on the sidelines for now.

A figure the bottom for these townhomes is around $264,000 which is a 20% correction from February 2022 peak price, while local household income went up at least 15% since then.

“There’s no question that higher interest rates are making it harder to buy homes in the short term. But in the longer term, this is the best thing, particularly for younger people who are not yet in the housing market.”

Glad ne said that. And good old ZH and other usual suspects have their rate cut propaganda (hopium) in full force. The Fed chairs who created this monster (Bernanke, Greenspan, et al), should be exiled.

a slightly lower inflation rate at least by the headlines has caused the 10 year to drop 8 bps. pathetic.

I’m tired of it. There is no reason to cut. Inflation will accelerate again, and now we will inflate the fake stonk market and housing further. I hate this and everything this country has become with its fake economy. If you even believe the inflation numbers. I don’t. And we are stuck with all the damage done the past few years. This country is a mess. Hope Wolf is correct and they cut slowly. I have my doubts.

Yeah but looks like under pressure, Pow Pow might just fold like a cheap lawn chair from Aliexpress..he is embarking on this journey of Fxxk around and find out. Maybe he learned something by studying what happened in the 80s or also think this time is different. Afterall, if he is convinced that we will get a soft landing, he might have more conviction to think perhaps this time is different..

The Fed’s rates are at 5.25% to 5.5%, WELL above all inflation readings. So “real” rates are high. If inflation stays in the current range, the Fed is going to cut, and Powell said that too. But it will only be some cuts over time, and rates will stay a lot “higher” than they were before the pandemic – that’s how I read the situation.

CPI just came out, and it was low. So that builds the Fed’s confidence for A cut. There are more CPI readings coming this year, and we’ll see. But with that range of inflation, the Fed will cut some, though maybe not as fast and as much as some want.

But a couple of ugly inflation readings, as we saw earlier this year, could keep the Fed on hold for a while longer.

Shelter inflation remains >5% yoy

Bingo!

Contrary to Bankrupt-u-Bernanke (who “taught a highly mathematical economic course at MIT”), an injection of new money may be robust, neutral, or harmful.

I commented a couple weeks ago about the many price drops I was seeing and inventory increasing, and I was mocked by someone 😂🤣

It can be localized. The housing market moves in waves and you might be seeing ripples.

It is indeed localized. In some zip codes you could argue prices have already crashed, and others are about to with 100-200% yoy increases in available inventory.

cnn is saying “US stock futures rose on the news as investors hope the good inflation news will pave the way for the Federal Reserve to lower painfully high interest rates.”

gaslighting all around. 5.5% is painfully high. pathetic.

It’s nauseating. They want to keep you in debt forever telling you how much they are doing for you by keeping interest rates low, giving you the illusion that you are doing well with the fake stonk market and fake housing equity gains. And hurting many people in the process. Corrupt people in charge

Mortgage apps plunged because most buyers now just pay cash for homes, with their NVDA profits. How can you smart people not get this? Everyone is now insanely rich with stocks at all time highs. The few losers in the country still poor…well, their EBT still stimulates the economy, just look at how well Wolffs city is doing for evidence. Or watch Metal Leo for a real-time update…

“most buyers now just pay cash for homes, with their NVDA profits”

Got a source for this? My understanding is investors are net sellers of homes right now; this is the group I’d expect to pay cash *if* they were buying, but they’re generally not.

I think the simpler explanation is that mortgage apps plunged because the housing market is freezing up.

He was being sarcastic.

All bank-held savings originate within the payment’s system. Demand deposits have just been shifted into time deposits. Bank credit remained the same. This is the source of the pervasive error that characterizes the Keynesian economics, Keynes “optical illusion”.

The FOMC’s proviso “bank credit proxy” used to be included in the FOMC’s directive during Sept 66 – Sept 69.

Net changes in Reserve Bank Credit since the Treasury-Reserve Accord of March 1951 are supposed to be determined by the Reserve bank’s policy arm, the FOMC.

Interest rates are high? Relative to what? Take that first chart back 30 years. 7% isn’t “high”. Deflation benefits the productive, inflation benefits the banks and Wall Street. Sad that the productive in society have no say anymore.

Wolf’s data just confirms, to me anyway, that the powers that be will cull the herd. Whether or not the culling is deliberate or not is another discussion.

We did a nice affordable condo the other day in a high crime area for a Verteran. Price was only $185,000. While I was waiting in the car, 2 police cars came by and arrested a dude right in front of me. The property was a real bargain and had easy access to the downtown Washington D.C. I liked the location because of the convenience to the center of the city. Deals are out there if you look carefully enough.

In 1989, when I bought my first house, I had a 30 year note at 10% fixed. Fast forward to 2017 when I bought my 5th and final retirement house on a 15 year note at 3.99%. I paid this house off last year after cashing out a pension plan from a former employer. Sorry to say that sub 4% rates are never coming back. Those 2% and 3% rates were an anomaly as a result of the pandemic and subsequent monetary stimulation from the Feds to prevent the economy from tanking. It’s not coming back. The very fact that this article highlights the 7% rate that has hung around for the past year is proof. People over the past 4 years are locked into some very low rates they used to purchase their homes. They have no incentive to sell and get saddled with a much higher loan rate.

Now, in the past 24 hours the Fed has signaled that lower employment numbers suggest a cooling economy. There is speculation that a rate reduction may be offing in September and perhaps another in December. Those folks waiting to plunge into the housing market with expectations of really low rates are going to get a healthy dose of reality. Rates may drop to 6.5% or even 6% by next Spring. Home prices show every indication of staying high for the near-term and mid-term. Only when baby boomers like me start dying, and we are in the millions, will our homes come on the market and saturate the supply side. At that point, homes can be affordable at even 6% morgage rates. Cheers.

I bought my first house at 2.7% on a 30, at the end of 2020. I doubt I’ll ever see this rate on anything in my lifetime.

(except the crappy rate that the local 5cent savings bank pays on deposits, that is)

If the current trend of non-stop rising price of the real estate and the stock market continue, which I believe it will, then in 20 years US will be a class society.

Top 10% will own most of the assets (RE & Stocks) and the other 90% will be living paycheck to paycheck with no hope of home ownership.

USA is already class society. You don’t need to wait for 20 years.

It is right here, right now.

Just look at asset ownership.

In 20 years?

I am not sure of the exact numbers, but the future is (seemingly?) now!

From Federal Reserve Bank of St Louis webpage ” The State of U.S. Wealth Inequality ”

For the 4th quarter of 2023:

The top 10% of households by wealth had $6.7 million on average. As a group, they held 66.9% of total household wealth.

The bottom 50% of households by wealth had $50,000 on average. As a group, they held only 2.5% of total household wealth.

I think those numbers are not truly reflective because the “average” and “median” figures are so distorted by the household wealth of the people who have over 100 million dollars in wealth.

I doubt 10% of households in the US have 6.7 million in wealth.

If you have 6.7 million you are probably much closer to the top 1% in net worth.

Yeah, my household is a negative regarding net worth.

I am a mortgage owner with little in assets beyond that, meaning: my mortgage is someone’s asset.

I understand the script should flip for me in another decade, but the road is steep in all directions.

Howdy Folks. Who else is waiting and watching for the Lone Wolf CPI report?????

And when rates come down lots of homeowners will want to tap all that new found equity, assuming home prices stay highish. And that will push inflation some. All that covid stimulus was wrong in hindsight. But here we are.

No recovery in housing sales until prices are one cent on the dollar. Given what the homeless get paid even that might be expensive.

I just ran a “buy vs rent” calculator for my current situation here in Orange County, California. My net cost to buy is $11,514/month and my net cost to rent (a 1000 sqft apartment) is $2435/month. According to the calcular, I will save $217,902 dollars over 30 years by staying in the apartment, and that number factors in a $500,000 capital gains tax exclusion when selling the home, and rent going up 2% faster a year than the home appreciation rate *for 30 years*. It is a lose/lose/lose situation to buy a home in Orange County at this point. I’m surprised *any* homes are selling.