New Highs: Boston, New York, Miami, Los Angeles, San Diego, Washington DC, Chicago… Rate-Cut Mania subsides, price growth begins to slow.

By Wolf Richter for WOLF STREET.

Rate-Cut Mania, which started in November and peaked in February, left its imprint on the housing market.

The S&P CoreLogic Case-Shiller Home Price Index, released today and dubbed “April,” is a three-month moving average of home prices whose sales were entered into public records in February, March, and April. So that’s still in the Rate-Cut Mania time-frame. Since then, Rate-Cut Mania has largely subsided, and home sales have plunged.

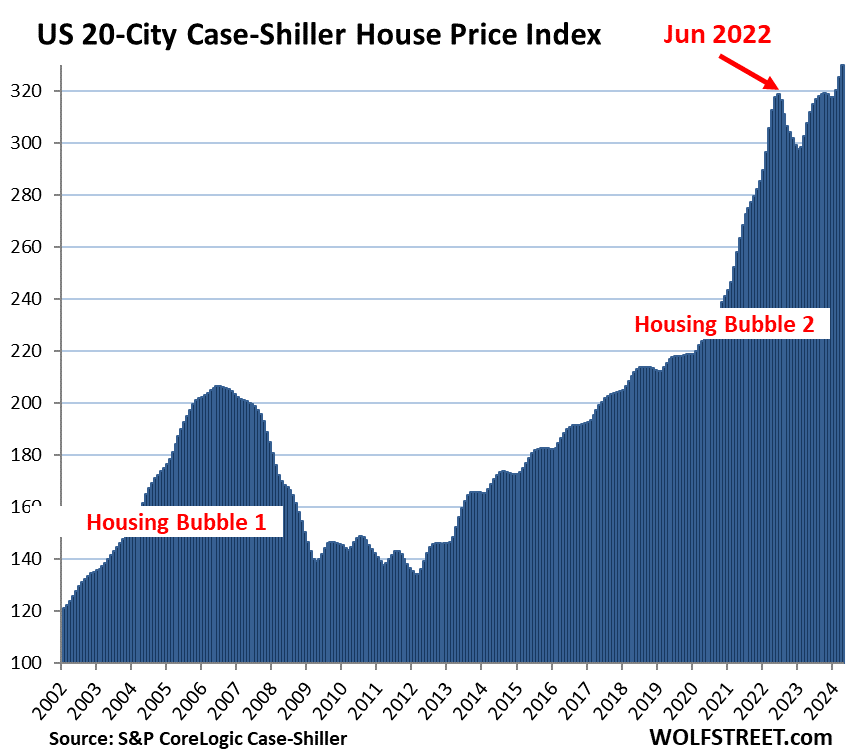

On a month-to-month basis, the 20-City Case-Shiller Home Price Index rose by 1.4% in “April” (moving average of February, March, and April), a deceleration from the 1.6% jump in the prior month:

- Month-to-month, prices rose in all 20 metros covered by the index, ranging from +0.1% for condos in the New York Metro to 2.2% for single-family houses in the Boston metro.

- Year-over-year, the 20-City Index was up 7.2%, a deceleration from the 7.5% increase in “March” and from 7.4% in “February.”

- Compared to the previous all-time high of June 2022, the index was up 3.5%.

Prices were below their 2022 highs in 7 of the 20 metros in the Case-Shiller index (month of peak):

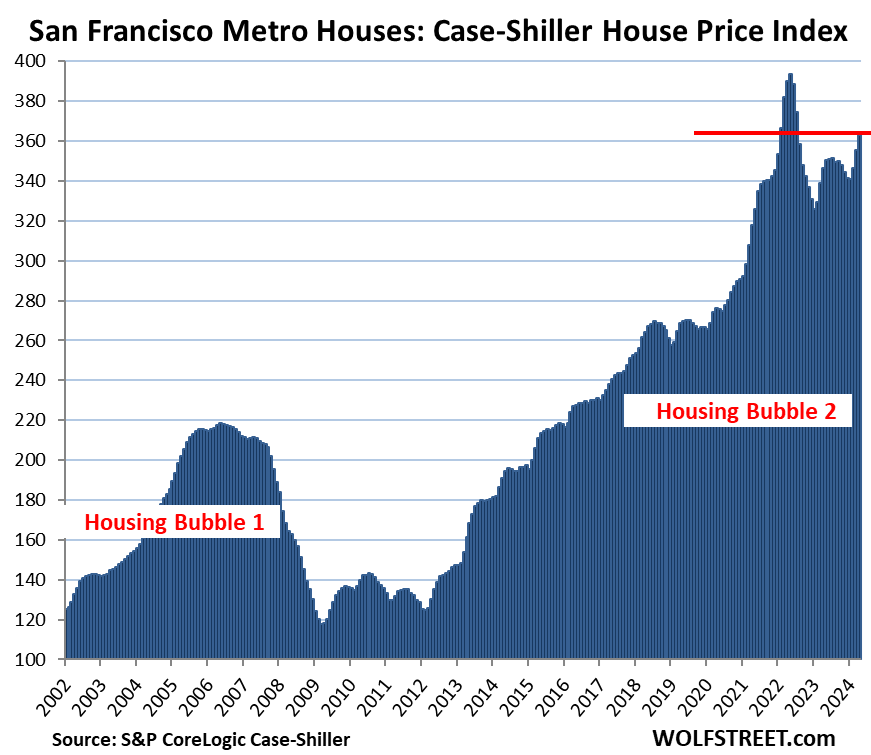

- San Francisco Bay Area: -7.9% (May 2022)

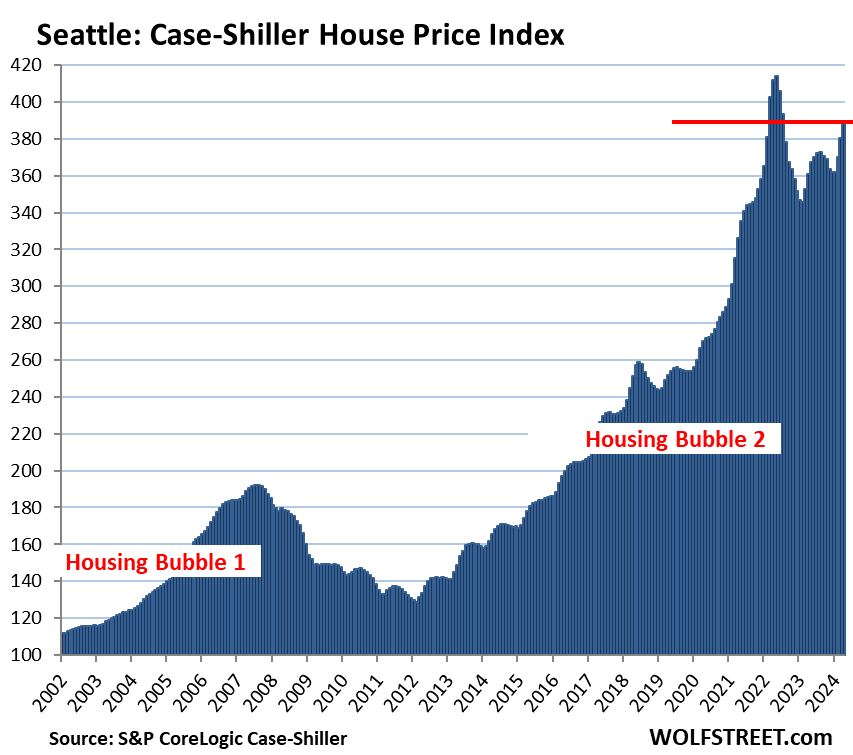

- Seattle: -6.3% (May 2022)

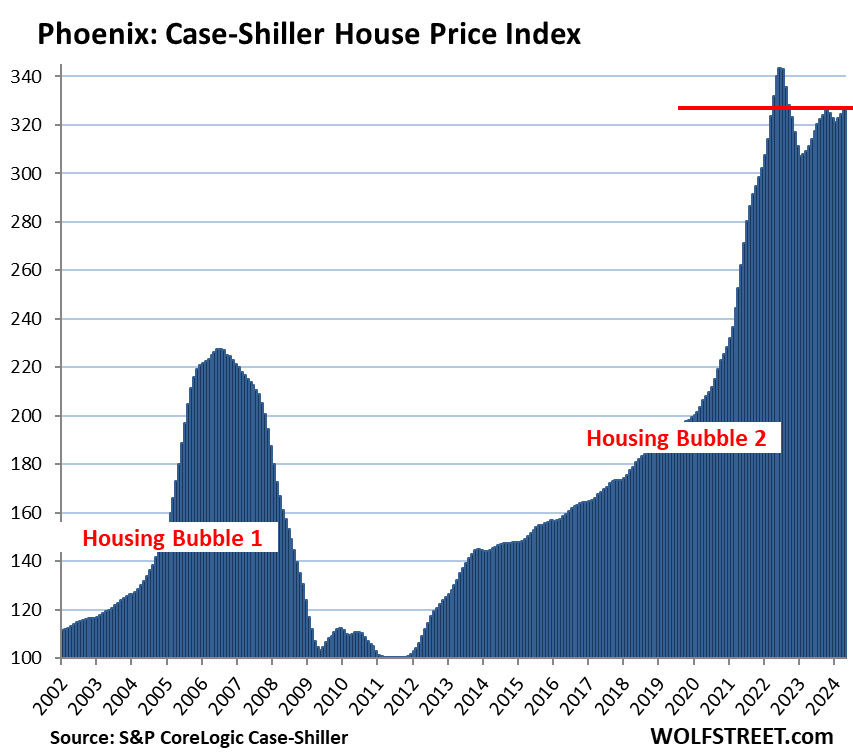

- Phoenix: -5.0% (June 2022)

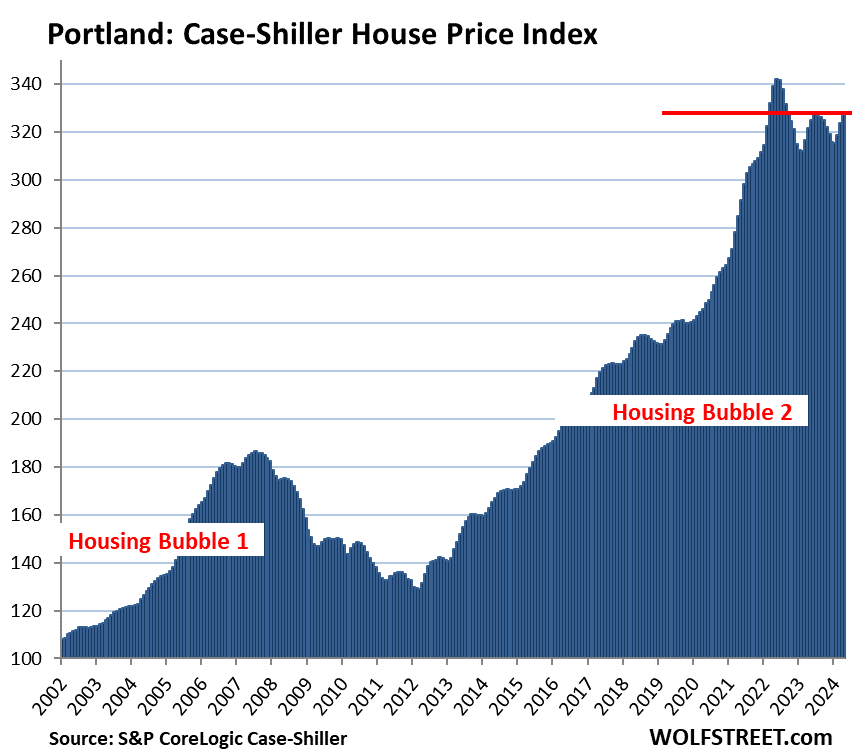

- Portland: -4.4% (May 2022)

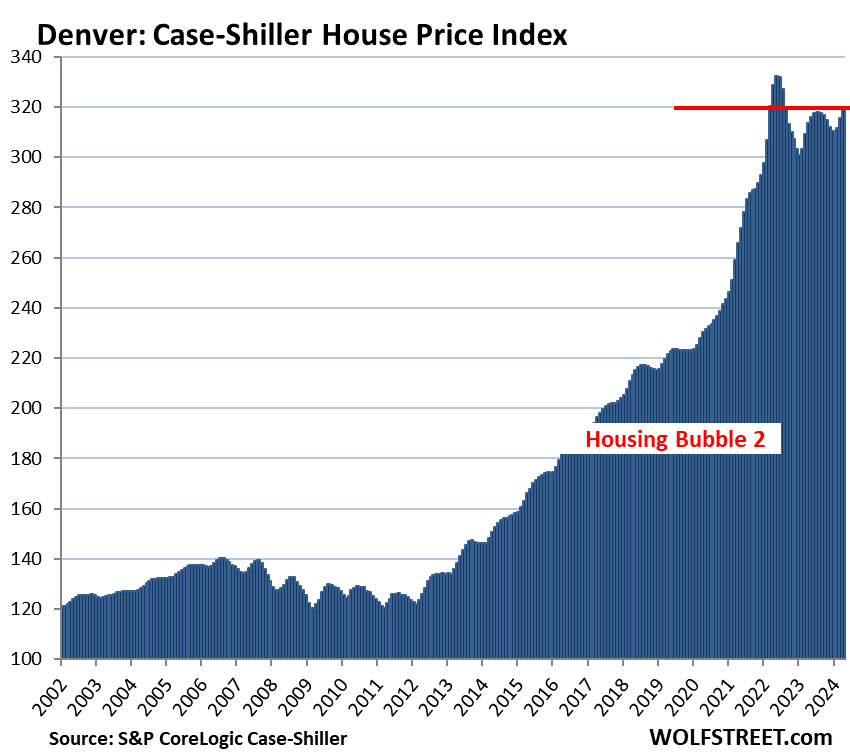

- Denver: -3.7% (May 2022)

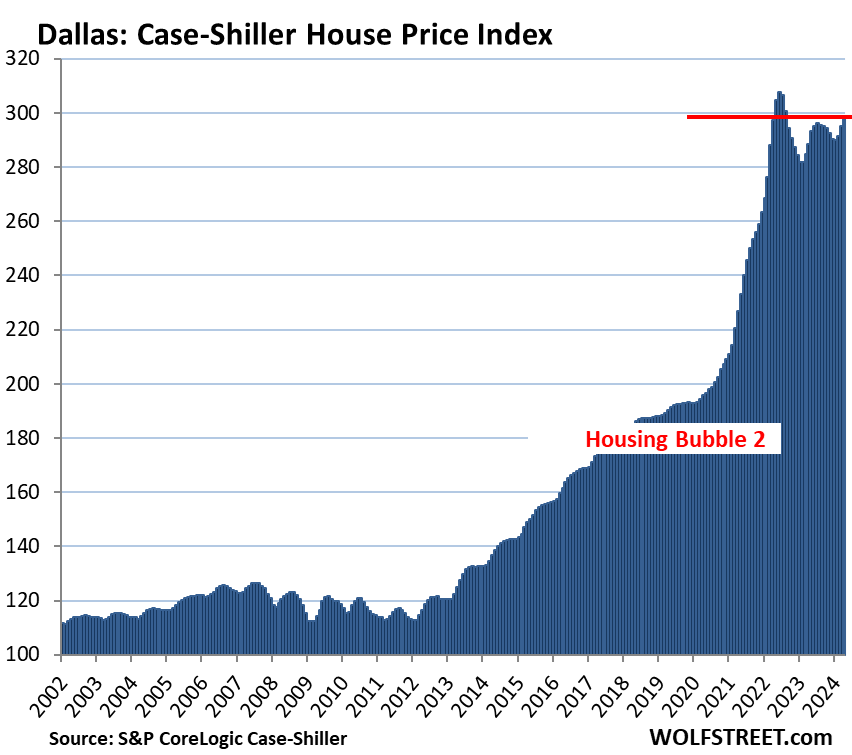

- Dallas: -3.0% (June 2022)

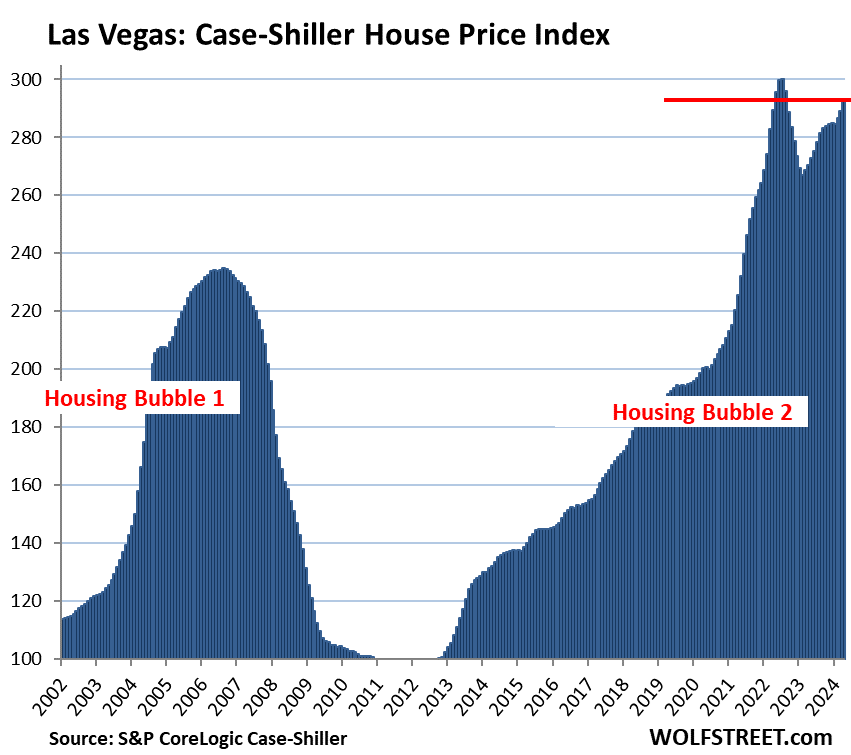

- Las Vegas: -2.5% (July 2022)

The most splendid housing bubbles by metro.

San Francisco Bay Area single family houses: the San Francisco metro in the Case-Shiller Index covers a five-county portion of the nine-county Bay Area.

- Month to month: +2.0%

- Year over year: +4.7%.

- From the peak in May 2022: -7.9%.

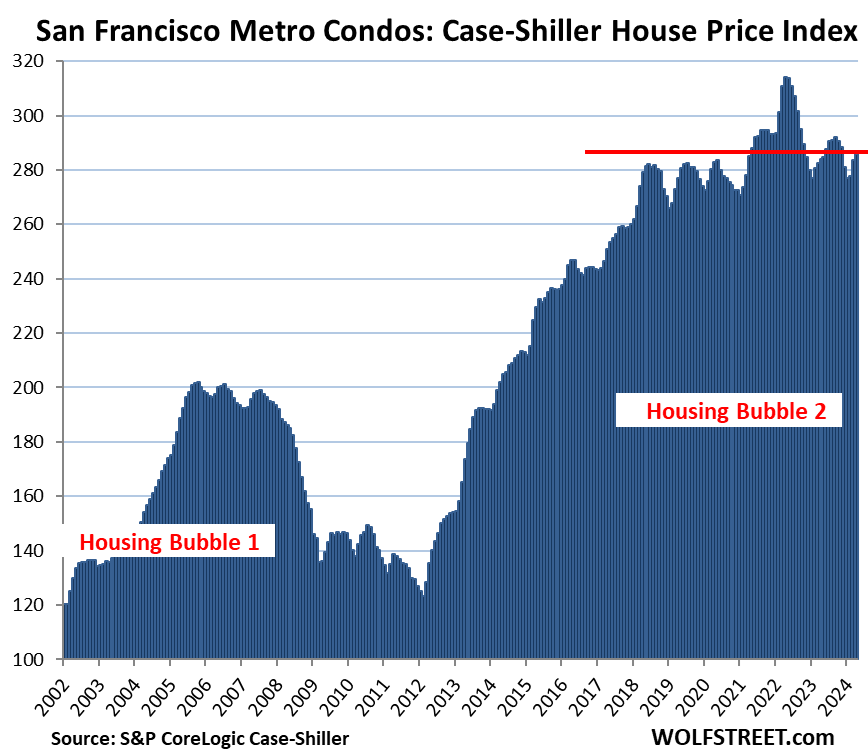

San Francisco Bay Area condos: Condos are a big part of the market in the Bay Area, particularly in San Francisco itself.

- Month to month: +0.8%.

- Year over year: +0.7%.

- From the peak in May 2022: -9.0%.

- Just a hair above May-August 2018.

Seattle metro:

- Month to month: +2.0%.

- Year over year: +7.5%.

- From the peak in May 2022: -6.3%.

Phoenix metro:

- Month to month: +0.6%.

- Year over year: +4.8%.

- From the peak in June 2022: -5.0%.

Portland metro:

- Month to month: +1.1%.

- Year over year: +1.7%.

- From the peak in May 2022: -4.4%.

Denver metro:

- Month to month: +1.3%.

- Year over year: +2.0%.

- From the peak in May 2022: -3.7%.

Dallas metro:

- Month to month: +1.2%.

- Year over year: +3.4%.

- From the peak in June 2022: -3.0%.

Las Vegas metro:

- Month to month: +1.2%.

- Year over year: +8.3%.

- From the peak in July 2022: -2.5%.

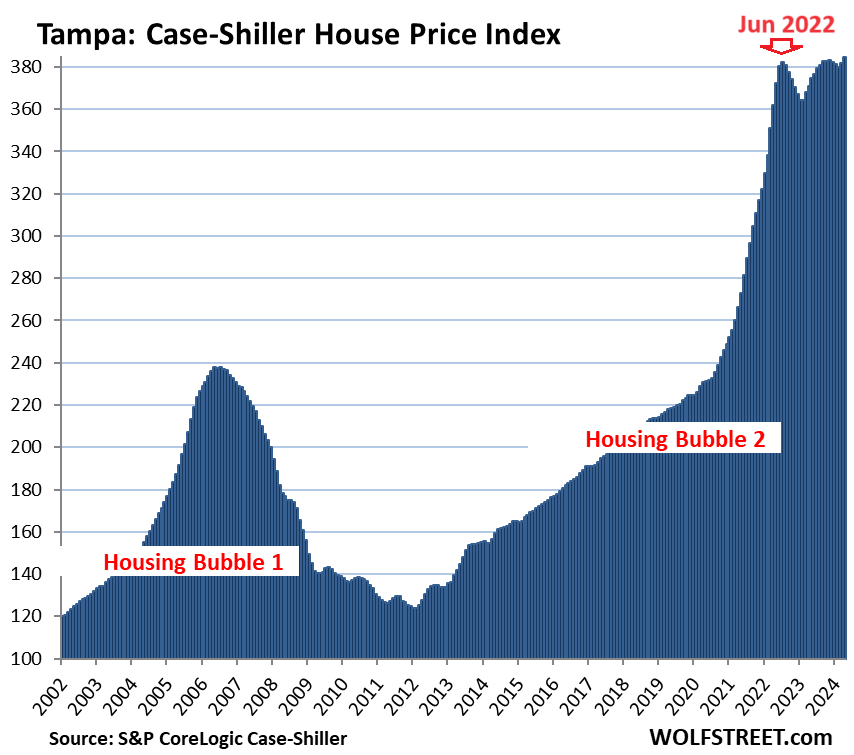

Tampa metro:

- Month to month: +0.7%.

- Year over year: +3.6%.

- Eked past its July 2022 high by 0.5%

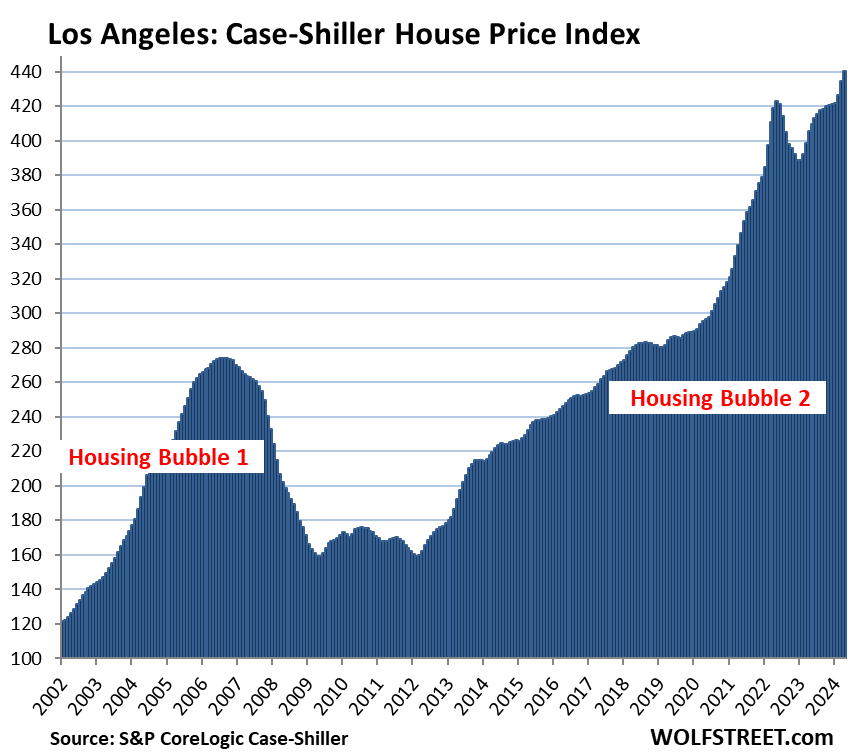

Los Angeles metro

- Month to month: +1.3%.

- Year over year: +8.6%.

- From prior high in May 2022: +4.0%

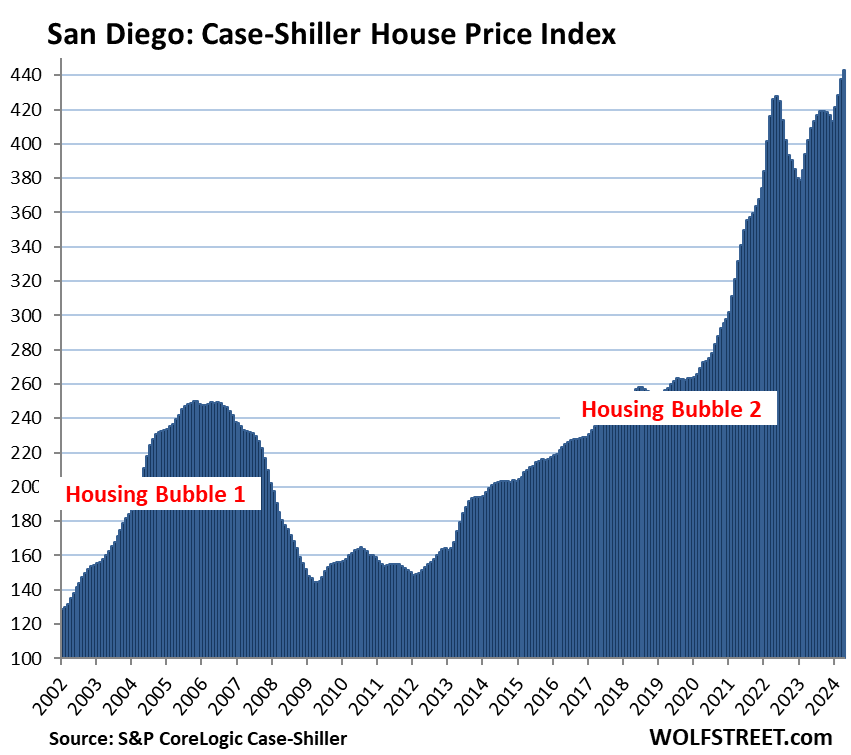

San Diego metro:

- Month to month: +1.2%.

- Year over year: +10.1%.

- From prior high in May 2022: +3.6%

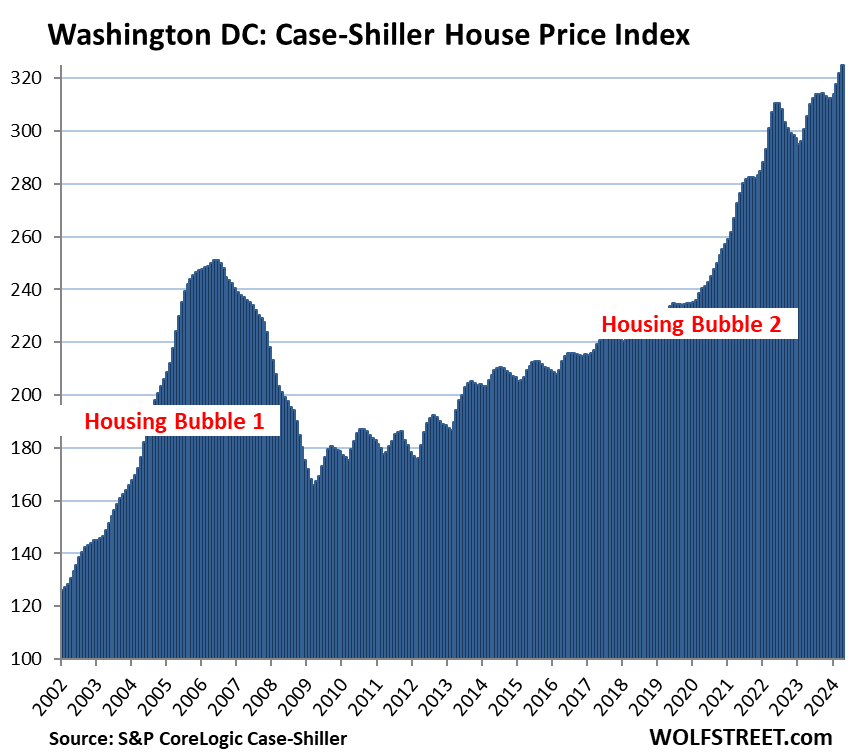

Washington D.C. metro:

- Month to month: +0.9%.

- Year over year: +6.4%.

- From prior high in June 2022: +4.7%.

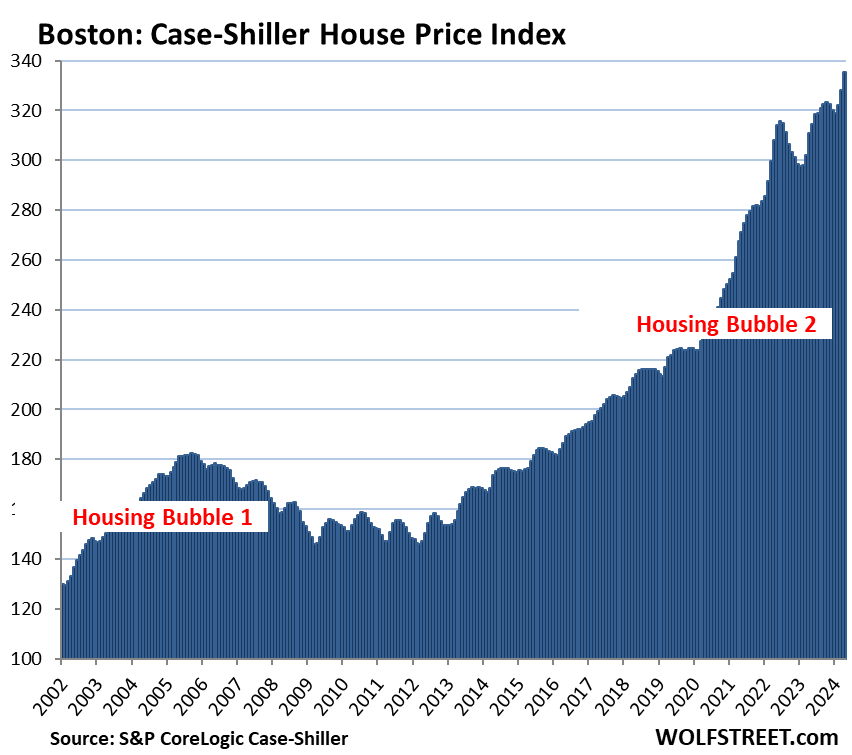

Boston metro:

- Month to month: +2.2%.

- Year over year: +7.9%.

- From prior peak in June 2022: +3.9%

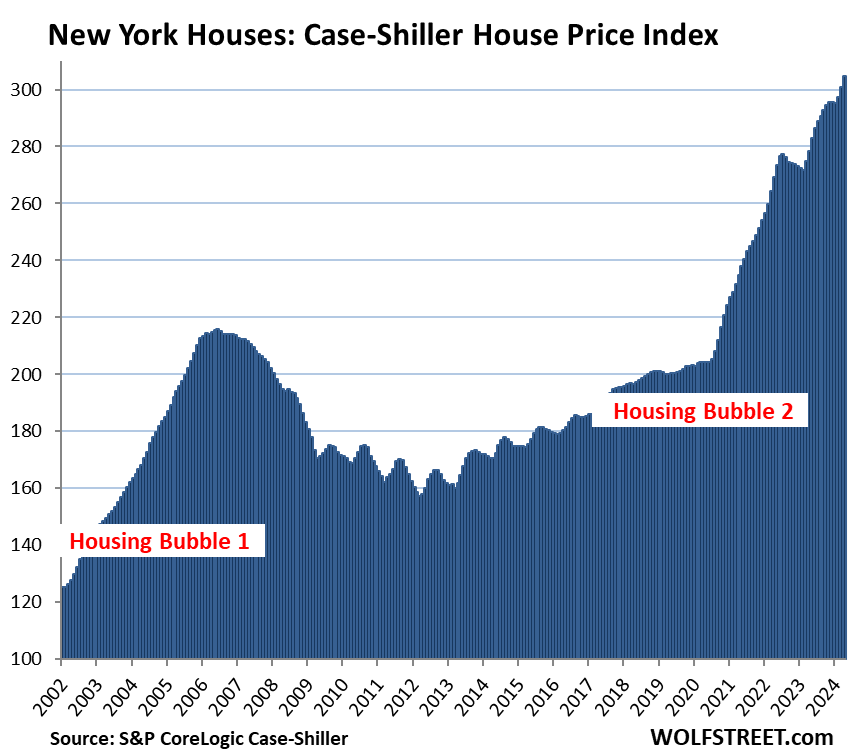

New York metro:

- Month to month: +1.3%.

- Year over year: +9.4%.

- From prior peak in June 2022: +11.4%

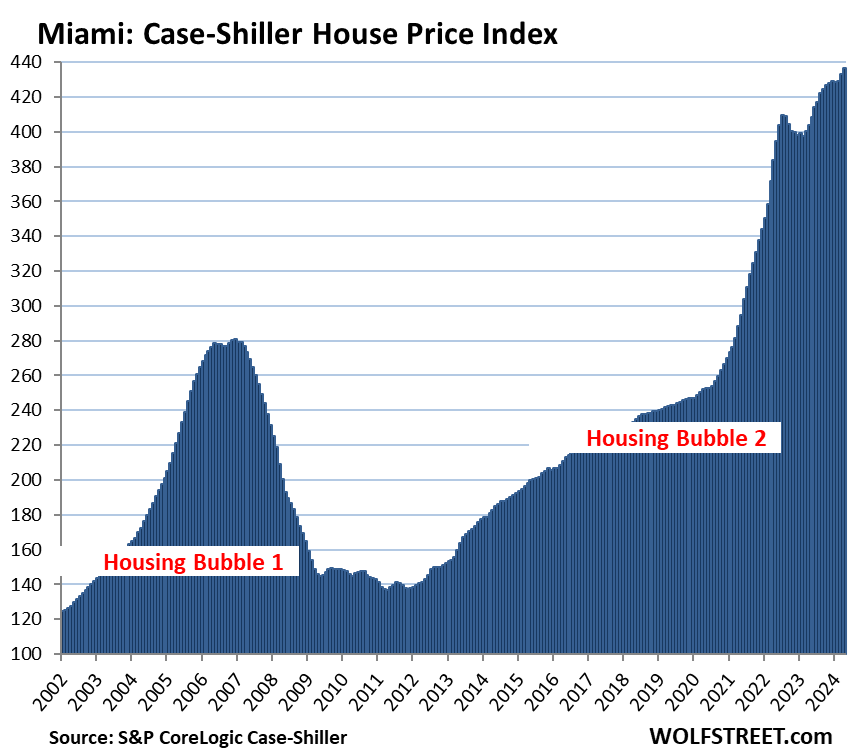

Miami metro:

- Month to month: +1.3%.

- Year over year: +9.4%.

- From prior peak in July 2022: +11.4%

To qualify for the Most Splendid Housing Bubbles, the metro must have experienced home-price inflation since 2000 of about 200% or more at the peak. The indices were set at 100 for the year 2000. Today’s index value for San Diego of 443 is up 343% since 2000, making San Diego the most splendid housing bubble on this list, ahead of Miami and Los Angeles.

Home-Price Inflation. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses were sold previously. Price changes are weighted based on how long ago the prior sale occurred. Adjustments are made for home improvements and other factors (37-page methodology). By measuring how many dollars it takes to buy the same house over time, the Case-Shiller index is a measure of home-price inflation. San Diego had 343% home price inflation since 2000. Over the same period, the consumer price inflation, as measured by CPI, amounted to 86%.

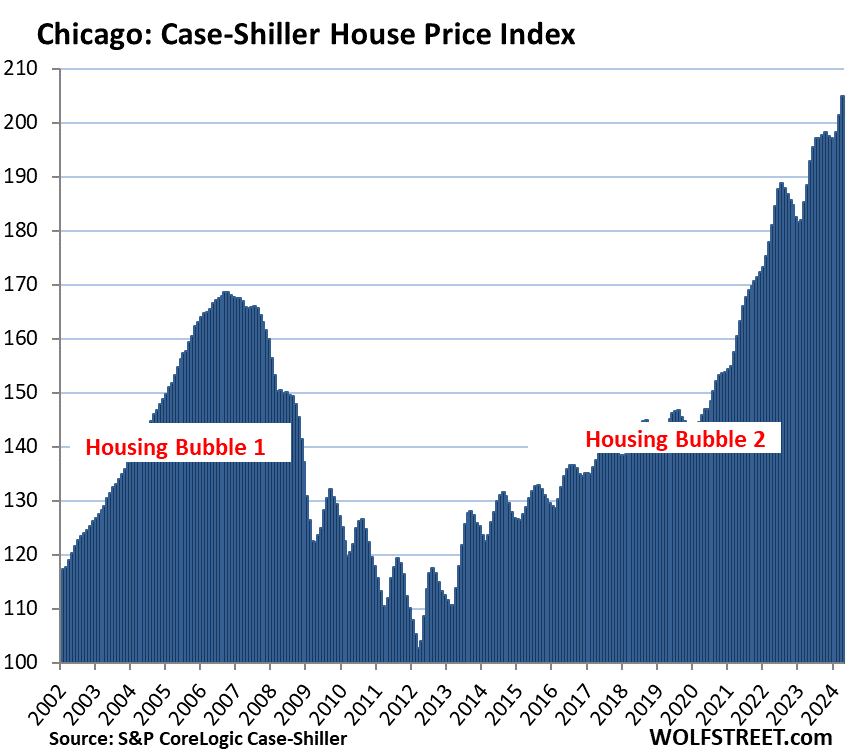

The remaining 6 of the 20 metros in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) had less home-price inflation since 2000, despite the price spikes in recent years, and don’t qualify for this list.

Chicago, with an index value of 205 is up by 105% from the year 2000, and therefore far from qualifying for this list. But the 44% price spike since the Fed started its money-printing binge in March 2020 has been splendid nevertheless, so here it is anyway:

- Month to month: +1.7%

- Year over year: +8.7%.

- From the prior high in July 2022: +8.5%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thank goodness inflation is under control! What’s the official statistic 3.2%?

You’re talking about consumer price inflation, which is measured by the Consumer Price Index (CPI) and the PCE price index.

This article here is about house price inflation, as measured by the Case Shiller Index. RTGDFA

There is also wage inflation, which is tracked by other measures. And there are other measures that track different aspects of inflation.

Yes I quoted CPI. House price inflation is much more!! Look at your article – NY is up 9.4%!! Boston up 7.9%!!

It’s not inflation though – everyone is making so much money they are bidding up house prices!!

“It’s not inflation though – everyone is making so much money they are bidding up house prices!!”

That IS how inflation works. People pay whatever. That’s one driver of inflation. If people stopped paying whatever, there wouldn’t be any inflation. Of course, people have to have the money to pay whatever, and that’s the other side of inflation. And we have both sides covered.

Exactly!

May be best to calculate your own personal inflation. That is actually hitting you.

Otherwise, it’s like worrying about harmful UV rays from the Sun while inside.

☀️ 🏠

sufferinsucatash:

You are absolutely correct. Personal inflation is the only calculation that matters. As an example, aside from my house insurance price going up, I personally have not been affected by the recent bout.

Louie — you have, you can just afford to be gouged, cheated, skimmed off, etc., without really noticing it. That’s great.

Wolf, is there a way to measure home prices in RURAL areas. My feeling is that big metros are holding up in large part because of both domestic and foreign migration to these big job centers. It’s a different story in rural America.

These smaller towns and cities are getting hit much harder in terms of lack of qualified buyers, price reductions and poor liquidity. I own properties in both big and small towns/cities. it’s much harder to sell in the smaller metros right now than the big ones, and liquidity in some small municipalities has dried up. Rents are stagnant as well.

Rural is last up and first down in pricing. Only local sales jdata will answer that.

Shark Tank stars claim it will only increase higher and higher 2X, 5X which is unsustainable. What will be the catalyst for change? (fill in the blank) CRISIS here. IE financial, war, foreclosure, homeless ect.

Concerned Educated Capitalist for America

Grain commodities have crashed since the peak in 2022.

Most prices are almost back to pre-covid.

Hmmm, I wonder if restaurants and grocery stores will pass along the savings? Lots of these food commodities are down 50% from the peak.

That is the thing with inflation, even when raw inputs drop, it seems like finished goods never do? No wonder the fast casual restaurants like Chipotle, Wingstop, Shake Shack and CAVA are on a tear. They probably will see nice profits from as their food inputs are dropping in price from 30% to 50%. LOL

From what I see it the commodity complex (metals, energy, grain, sugar) is a sort of “breakout/ backtest” behavior.

Yes, pandemic and war (Russia) prices were wildly distorted (as if people would stop using crude, or need only Ukrainian wheat), BUT

Prices have come down to NEAR pre-pandemic levels and largely appear to be basing or rising.

Energy is an input into everything. Sugar and wheat widely used. These things are at or above trend.

Pile on the labor cost, increasing overhead (insurance anyone?) and we see this inflation persisting at or above the current levels.

We have all heard the word, let’s say it together:

Stagflation!

Much of the food commodities are subsidized by all Governments to keep food cost down.

Actually, putting on the armor required to convince oneself, that there really is a reality behind technical analysis.

The charts all look like candidates for the your pantheon of another failed financial scams.

There seems to be a fundamental disconnect between the asking and getting price.

Dang: yes I agree that technical analysis is as useless as reading history books.

Don’t people know all that stuff already happened?

I have some simple solutions to these problems that will make housing more affordable for creditworthy borrowers.

– Print more money & reduce interest rates to zero.

– Make it easy for big banks & private equity to buy homes.

– Mandate that all landlords use rent “optimization” software like RealPage.

– Subsidize housing by handing out tax payer money because that will only reduce home prices.

– Give people veto rights to prevent new housing in their area.

Come, lets stand up and sing the US national anthem on this 4th of july, and swear that we will do all of the above things.

Who is buying these homes in places like San Diego? To finance an “average” $1.3M home, you’re looking at $12k/month on top of $260k down. Not an average income to cover that… otherwise you are paying cash… but I’m told buyers are “stuck” in their low mortgage homes. The math doesn’t make sense to me.

According to general consensus, everyone is rich or got 100%+ pay increase to which I guess I miss out on…Yeah $12K a month doesn’t scare people off, $6K a month rent, no problem…$500K down payment and then $8K…pssh chump change..

Urgh…maybe this time is different…still scratching my head how some people can still trample over each other paying this kind of absurd amount and just normalized it as “It is what it is” in their head. Guess people that can afford to buy like Ramit and decide to exercise buyer’s strike is about as rare as the dodo bird..quite frustrating and that’s also why we’re seeing insane market like LA and SD going higher and higher….bubble is soooo 2008, we lost the plot long time ago.

A A Ron,

“Who is buying these homes in places like San Diego”

Not many people. Sales volume is down 43% from the same month in 2019.

Is this for SoCal/SD or the entire US? Data is probably right but sure doesn’t feel like it in entitled city like Ladera Ranch. Price high and listing sold after 3 weeks..

San Diego.

The few people who pay the whatever price is driving this madness . Until when? Zero down mortgages are back.!

Zero-down mortgages have never left. There have always been lenders that extended down-payment loans. And there have been other ways. It’s costly, though. A lender providing a zero-down mortgage is going to charge a higher mortgage rate. So fine.

Stressing the point you made about a year ago(?) when they started hiking rates, they essentially shrunk the size of the realestate market!

I am not sure. Anytime you bring it up online people are so angry about even admitting there is a crash in some metro areas.

Makes me think there is a lot of anger of not being able to afford these homes.

Dunno it’ll be wild whatever happens that’s all.

yeah imagine that. people are angry and frustrated that they are living hand to mouth simply because they were born at the wrong time, while others live high on the hog having done nothing to deserve it, like buying a house in 2012 because it was the right time in life.

@Paul,

Another emotion in play is the FOMO on the pricing levels many sellers now see as an entitlement. Which is a selling price similar to what their comparable neighbor’s sales received in the past 1 – 3 years.

Wolf used an interesting term in another recent article comment. “Aspirational price.” I’ve always used the word aspirational in front of the word “spending.” As in, spending that reflects what we want to do or who we want to be at some point in the future.

But that term may very well be correct. You can bet many prospective sellers have a firm picture in their minds of what they’ll be doing with their (expected) windfall-sized profit from their home sale. And don’t you dare tell me I might not get it – I’ve already written out my aspirational plans.

A friend and I have jokingly been using the term “fund my retirement price.” Another term would be entitlement pricing. I continue to sense an attitude of entitlement on the part of some current sellers – sort of a “we are granting you a huge favor by permitting you to overpay for our house.” This despite the substantial mortgage loan interest rate hikes.

Whatever one chooses to call it, I’m also certain the agents continue to hear this aspirational pricing attitude from prospective clients. And I also think many of those agents are fully aware the current market will not provide the sellers with that price.

But they tactfully play along with it to get the listing – knowing full well the price will have to be dropped later. Honesty goes out the window once again. Aspirational sellers don’t want to hear it.

Yep Paul, more anger than hard facts. I just read how cumulative inflation for the past 5 years was 20%, but wages were up 26%, so net, net, folks are better off than before. And add to the 26% the 4-5% interest everyone is now getting paid on their savings, it’s the best of both worlds.

We aren’t in a housing bubble. We’re in a housing boom due to a shortage of available supply and more importantly, long term structural changes in the real estate market. People are staying put longer and they simply aren’t going to sell their homes unless it’s absolutely necessary.

This is very common in Latin America, Europe and many other places where homes are considered stable, loved places to raise families. They hold wonderful memories and are family legacies to pass on to future generations, rather than flip like they were penny stocks.

It seems like the angriest folks are mainly upset about how they or their children missed the best 10-year+ bull market in the history of real estate because they always thought prices were too high to buy.

They’re also the most vociferous about the lack of a housing crash and are the most likely to rant in comment sections here and elsewhere. Quite frankly, if you rent, you’re able to live in a home for half the cost of buying it and if you own property, it’s been a great long-term investment with huge price appreciation. So what’s to bitch about, regardless of whether you own or rent?????

CCBB — not a bull market, based on fundamentals — it was an asset bubble, stoked by freakishly low rates, helicopter money and other magical decimal stuff. Look at those charts above and tell me that’s anything like an organic curve…yeah…

Sounds like you got lucky in an aberrant market fueled by sleazy get-rich-qwik speculative serial manias. Great. Me too — well, kinda. My ex wife got it all (she really kinda deserved it, honestly). Only I don’t go around shaming would-be buyers like they’re some Johnny come-latelies lacking acumen & spine enough to sidle up to the roulette wheel with the drippings from their toil on the line.

Some slobs still just want a place to call home.

It might be that he’s blaming the policies put in place by well meaning, but misguided, politicians that cause the cities to go to heck in a hand basket.

It’s rarely purely a “red” or “blue” issue. By firing up a few neurons one might realize that civilized policies and enforcement of the rule of law is what makes neighborhoods desirable or not so much.

Lax enforcement encourages criminal behavior. The burned out, tarped roofed, broken windowed structures didn’t get that way by themselves. They usually had help.

Oops.. that belonged in the “blame the politician comment”. Sorry.

“Yeah imagine that. people are angry and frustrated that they are living hand to mouth simply because they were born at the wrong time, while others live high on the hog having done nothing to deserve it, like buying a house in 2012 because it was the right time in life.”

If they’re living hand to mouth, they shouldn’t be considering purchasing a home. Nor a “Bro-dozer”. Nor a Rolex. Or a Kit-Kat bar.

Hating on someone because of their good fortune is the sign of a small person. It’s like flying on SWA and being p*ssed because someone got a better boarding number and got that prized leg room exit row seat.

BTW, I’ve come to hate the word “deserve”. It implies entitlement. They took the risk of buying… it paid off. Had the house price fallen further and they lost their equity, would you shown any empathy?

cccb, one post so filled with crapola that it’s hard to know what to talk about. let’s start with a list

– inflation is much higher than 20% in the aggregate over 5 years. and on many essential services, like rent, insurance, child care, and medical care, it’s even higher than that. and house prices have gone up as much as 100% in some areas.

– what is this housing shortage? new things are being built constantly, and staying put longer doesn’t change the fact that houses are expensive, and many retirees will not be able to or want to afford the upkeep

– people here generally don’t pass on family homes. absurd comparison.

– no, the angriest folks are ones who were too young or unable to take advantage of the “bull market.” no one didn’t buy because they thought prices were too high. it wasn’t time for them.

I agree. There seems to be an organic resentment by people who have only known the benefits of the FDR and LBJ era reforms.

America was a grey society, back then, much like today.

My nightmare is that I cut the feet from under the next generations by acquiescing to the demands of an imperial economy.

There is a whole city of people who have been riding that wave to massive home equity in San Diego. 3x appreciation is how you get 500k down payments. There are whole communities of people in houses who caught the escalator 10-20 years ago and would never be able to afford the home they live in now.

Honestly just a matter of macro economic cycles being you favor, no magic planning.

I’m compelled to share a worthy proposition by Hussman about every decision comes with regret. In his example, regretting selling a half of a stock position that later increases in price is equivalent to the pain one feels when buying a stock that ultimately goes to zero.

The only reason I would bore you with my comment is too point out that markets are, hopefully, chaotic, not moribund, like the ugly San Diego market.

It will resolve itself somehow.

A household earning the minimum amount to get the loan? These people are biting off a lot.

I used to worry about a 250k loan. 1.25 Mill is 5 of them!

Volume is down but there are still plenty of buyers in San Diego. If it’s priced well? It’s straight up cash, any “good” house gets 10+ offers. For a minute in Feb this year we were looking for a second house, got outbid twice. The last one was a buyer working for google who paid in cash (1.25M). We’ve had quite a few bay area folks moving to San Diego where things “look cheap” in comparison.

Stock market gains

The same ” devil may care ” attitude in several other California locations that reminds me of a visit to magic mountain, 5 minute wait, to today, having to pay extra to go to the head of the line.

The result of monetary policy that subsidized graft and corruption on a Biblical scale.

As one who has lived in San Diego for 20+ years, it’s not the average citizen I can tell you that. Wages in San Diego have always been low compared to the Bay Area and NYC. Just look at the wages for the county, city and San Diego Unified School district which are all among the largest employers here. The Navy is the largest. Anecdotally, based on what I’ve seen, I believe it’s a lot of foreign nationals and of course, other HNW individuals from across the country. The middle class has been completely priced out if they did not buy prior to COVID. It will be interesting to see who is left in the next 5 years. I know people who never thought they would leave making plans to move elsewhere.

Well, what Mike Tyson is reported to have said, is that “everyone has a plan until they get punched in the face.”

Whoa,…where to begin.

Living costs are high because people want to live there…

Howdy Folks. Will this bubble pop or not?

Nah, not a bubble, this is the new normal I am afraid

Howdy Phoenix. YEP, could be right, I sure did not expect the Lone Wolf charts to show peak after peak…….

Till the next recession.

Which according to McDonald’s…

DFB: As referenced, I believe the bubble IS popping die to the metric: Volume.

In technical analysis of prices one looks at volume as a key indicator.

Yes, there’s a LOT of ask, and little bid. For whatever reasons (death, divorce, departure) the asks will eventually need a bid.

Anecdotally (and re the above mentioned “retirement funding price”) there’s a “poor-rich” that lives on my Lux condo property.

Offered maybe $3.75MM for his 1200sf. Condo. “Needs” to get $4.25, and the sale didn’t go.

Meanwhile a 5500 sf. Condo is under contract for $12.3MM. Likely because those who can “write the check” have to park their money somewhere before the inflationary/ bubble fire consumes it.

“Due to the metric: Volume”

Theres more ask than bid? Where?

Homes are on the market for 7 days in the Boston metro. Thats a lot more bid than ask.

The metric is supply. Ratio of homes to households.

As long as we maintain a critical shortage of homes in metros with jobs, we will have these prices.

The metric is “inventory.” A listing is an “ask.” In my neighborhood there are no listings below a million.

I know of one coming to market and suspect it will sell quickly to your point of certain neighborhoods.

I recently saw a headline that supports this concept of high inventory:

“Demand for Homes Drops to (Near) Record Low as Inventory Rises. Now Come the “Stabilizing Home Prices”: NAR”

Source: Wolfstreet

Guess it depends on when boomers start kicking the bucket in big numbers. Which could be a ways off. My parents are a perfect example of the older generation squatting on housing supply. They split up decades ago, so take up two houses. Pop’s is really 2 or 3 times too big for just him and his wife (remarried). It’s overwhelmingly too much for them to take care of. He should have long sold and downsized. Instead they occupy it and that’s one new young family that doesn’t get formed.

And my mom’s house? Way smaller but even so, my sister moved back in — and she is over 40. Makes into 6 figures and can’t afford a house of her own in the DC area.

If your father sells the house that’s too big for him and his wife to downsize and buy a home that is smaller, he puts one big house into inventory for sale and takes a smaller home out of inventory, and the net change is ZERO (+1 -1 = 0), except that the smaller home is now no longer available as starter home because your father took it off the market, and the big one that young people cannot afford is now for sale. In this situation that you describe (father + wife #2; mother + daughter), there are four people living in two houses. How is that an example of “squatting”???? You people need to learn how to do basic math.

It’s only when your father and his wife pass away that they no longer need housing, which is what you indicated in your first line, and it seems like you cannot wait for that day to arrive?

Exactly, what are these old Boomers supposed to do, move into a tent? They’ve got to live somewhere.

Point taken on the short-term math, but (1) in practice, pops would probably rent first, and (2) the larger point is in generating appropriate demand for building the right mix of additional housing.

Even renting doesn’t “fix” the market in the short term, but isn’t that just saying there’s a fixed supply of housing at a given moment? That’s kinda obvious.

Anyways, I don’t see a problem with houses sized for more than 2 people falling disproportionately in price so young (maybe not so young anymore) would-be families can grow into them…

Oooooh have father and mother attempt van life! 🚐 😆

Btw, gotta congrats Pow Pow, his fight to inflation is working super well, home prices highest in all history, must be some kind of reverse logic…higher home price = lower inflation. I am not smart enough to understand that one…just like the statement he made before, must be some jedi mindtrick at play…or maybe that reset is expect 90-100% of your income to go to housing if you want to buy a house…

“I would say if you’re a homebuyer, or a young person looking to buy a home, you need a bit of a reset,”

Judging by the charts, the “reset”, housing bust 2, was the second half of 2022. Blink and you missed it.

Welcome to housing bubble 3.

You’re misreading the charts. The month-to-month price growth slowed a lot in “April.” The year-over-year price growth came down. This thing has run its course. It was the result of rate-cut mania. We can see that in lots of other housing data as well, including surging active listings and price cuts in data that doesn’t lag so much.

I posted some of the charts in the comments below.

https://wolfstreet.com/2024/06/21/home-sales-sag-further-hit-by-mortgage-rates-price-reductions-active-listings-surge-median-price-skewed-higher-by-surge-in-high-end-sales/

Not yet Snotfroth, but it looks like we are heading toward a continuation of housing bubble 2, since that 2022 dip is hardly a “reset”.

Most of these metros have barely tripled in the 22 years since 2002. That’s actually slow price growth relative to the past. The national median price tripled in the 70s alone and doubled again in the 80s, nearly 6 times higher in the same span of time. It’s certainly possible that the median price could stay fairly flat over another 4-6 years like it did in the 90s, which could actually represent perhaps the most stagnant 30-year period on record. No bubble here. Anybody waiting for prices to fall 50% is going to be sorely dissappointed.

Keep in mind that many of these metros briefly doubled in price in just 4 years between 2002-2006. Now THAT was a bubble.

Housing will levitate until the stock market drops, and that won’t happen as long as Wall Street believes (or pretends to believe) that a Powell put is in place.

Nobody knows for sure if there is one, and I think Powell likes it that way.

If a Powell put were ever taken off the table by the Fed, stocks would immediately drop 50%.

….in my opinion.

Free speech baby. Just blast it till their ears bleed 🔊

The main reason we have asset bubbles is foreign money. Don’t try to explain san diego house prices by wage earners, because you can’t. It’s people from asia. Billions of them. Many have made big money and want to get it out of china/india/japan/korean gov’t control. Also, look at drug dealing around the world. Billions need to be laundered somewhere. No better place than friendly banks and real estate markets in places that have strong property rights.

When does the bubble end??? That’s the $10 million question. I’d say it ends when the dollar inflates too much and scares away investors. But then, every shirt is even more dirty, right??? So any correction will be temporary like it was in 2009.

it’s insane to me that any country with expensive housing allows foreigners to buy their limited real estate.

Agreed. If the local governments truly cared about their constituents and wanted to solve the housing crisis, they could help put an end to it tomorrow by heavily taxing second homes and those owned by non-citizens. But in this age where neoliberalism rules, that is clearly not happening anytime soon.

I see you’ve never met a real estate agent.

Elizabeth, you’re right. There are lots of ways to incentivize and disincentivize specific economic activity. Both state and national administrators (Congress, state assemblies) do nothing but collect campaign contributions, from day one to the next election. This national Congress has done virtually nothing for 4 years.

And there are fixes for illegal immigration. Guest worker programs and/or stiff, stiff penalties for hiring illegals (that would hit Tyson, Smithfield, Dole, the sugar monopoly, et al, where it hurts). Switzerland institutes penalties of 10% of annual income for fairly small infractions.

Your ideas about ways to alter the course of housing issues are good. How about running for office?

…I wouldn’t either.

Good point H:

Last time we were stuck on the freeway going South near downtown Los Angeles, every driver I could see was Asian; OTOH, last time going east it was very mixed ethnically.

LA definitely IS very popular with folx looking for more freedoms, far damn shore.

As it should be, eh

first person to say what i have been thinking a while. powell likes it that way because he gets to maintain the asset bubbles that benefit his benefactors, while maintaining this image that he’s not doing anything to further inflation. no one can say he’s been dovish without looking stupid as rates are still at the 5.5% and qe is still going on.

How can a Fed put ever be “taken off the table”? When interest rates were negligible, the “put” was more QE.. now that we have something approaching normal interest rates, the “put” is that rates can be dropped again? This makes no logical sense, as it ignores the effect of the higher rates themselves. But I guess people are free to be irrational en masse.

Nothing illogical about it.

In response to a stock market fall, the Fed can protect stock markets using a number of different techniques (e.g., QE, interest rate repression, dovish promises and language, etc.)

The Fed can take this “put” off the table by simply stating it will not step in with stimulus to protect elevated stock market valuations, even if a valuation correction leads to a temporary normal recession. They can say they will use emergency lines of credit to alleviate liquidity concerns, and such emergency credit will be expensive and issued only to clearly solvent borrowers. They can say general price support such as QE, rate repression, and other tools will be used only in response to unusually high unemployment levels, not as regular tools to manage economic growth or to prevent the normal functioning of the business cycle, which calls for temporary deflation and price corrections from time to time.

The fed put is definitely still alive and well as evidenced by the rush to save banks last year. Yes, SVB went under, but their uninsured depositors were all saved for no reason, and who can forget buy the F-in ponzi (BTFP) scheme, and now there’s maybe no FDIC-insured limits anymore? More magical bailouts. Who is to say what they will pull during the next crisis.

All of the fed’s inflation-fighting tactics are of no use if they don’t allow for the natural creative destruction of capitalism, with banks and companies going bankrupt, and even having reverberating effects in the economy. That’s what is supposed to happen. Taking outsized and nonsensical risks should have consequences.

I’m just not seeing a terribly distinct “put” in your or Bobber’s comments. Bobber is referring to jawboning, but not a lot of the dovish variety has been emanating from the Powell Fed.

The regional bank bailouts were more a FDIC and Treasury affair and honestly those weren’t terribly supportive as well. Saving depositors but folding 3+ major regional banks is a large way to Lehman. That’s something that hits Wall Street and institutions hard. And I’m not sure I see retail rushing in to buy stocks as a sustained outcome just because they saw depositors saved.

My theory is Powell is secretly a hard money guy, not dovish at all. I have my doubts as to treating the Fed like Bernanke is still at the helm.

A lot of it was the treasury, but I think you’re forgetting about how the Fed un-did months and months of QE basically overnight. And the BTFP was adminstered by the fed. That’s where they lent AT PAR for treasuries that were actually worth MUCH less. They already had a discount window but no, that wasn’t enough for this go-around.

Maybe we have diff standards, but that all sounds very fed put-like to me.

Re: JPow, I think he used to be a hard money guy before he became chairman based on his comments. But judging from his performance since, he is anything but. How does one call zero rates and a peak $9 trillion balance sheet being a hard money guy? Fwiw, I hope you’re right about him but I have yet to be convinced.

i am ambivalent on the regional bank bailouts, but i don’t see this as a fed put for stocks, but for the economy in general.

the test would be if powell starts taking moves when stocks drop unrelated to the larger economy and does things to save stocks, separate from jobs, banks, or whatever.

Housing +7.2%.

Deficit of +7% of GDP.

Housing is inflation, excluding food it is is the single most important component of our budget, and no price measure has correlated inflation better over the past one hundred years than housing prices.

Last week a major east coast paper ran an article on affordability. In the ten years prior to Covid, a median salary (60K) could afford a median home. Now with rates and prices going up it takes a salary of 120k to afford a median priced home. Only six percent of America makes six figures. If you are not at the 94th percentile of salary in this country, you can not buy a home.

This will not end well.

“no price measure has correlated inflation better over the past one hundred years than housing prices.”

No, during Housing Bust 1, home prices plunged. It took five years for home prices to get to the bottom. Yet CPI inflation persisted during that time.

Correlation between rents (CPI inflation) and home prices (home price inflation) is not great:

Wolf, based on your first chart, housing prices have nearly tripled in the last 22 years. Annual inflation is compounding at approx. 3%/yr. $1 compounding at 3% for 22 yrs. becomes $1.92. That’s nearly 200%. Yet housing has inflated by close to 300%. That’s a big friggin’ difference.

“Annual inflation compounding at 3%”, that is, over the last 22 years, inflation, averaged out, is 3%/yr. for that time period.

In terms of CPI since 2002 (“22 yrs.”), cumulative inflation = 75%. Not “200%”.

In the article, I took the comparison back to 2000. Towards the bottom of the article you will find:

Home-Price Inflation. The Case-Shiller Index uses the “sales pairs” method,…. By measuring how many dollars it takes to buy the same house over time, the Case-Shiller index is a measure of home-price inflation. San Diego had 343% home price inflation since 2000. Over the same period, the consumer price inflation, as measured by CPI, amounted to 86%.

A big difference indeed, one might even say it’s unsustainable.

In defense… I tried to find that cumulative CPI amount for those years and only found an “average” of 3% annually, so I did the calc. and got close to 200%. I stand corrected and assume your response was the true amount.

And I did RTGDFA. Just forgot some details once I got in the comments. Not Alzheimer’s but I am getting forgetful.

HowNow,

Tip: The easiest way to calculate cumulative long-term inflation between specific dates is to use the BLS CPI calculator:

https://data.bls.gov/cgi-bin/cpicalc.pl

HowNow,

You’re off to a large extent because you’re miscalculating the percentages. From your figures, the inflation is 92%. The cost of a one dollar item from 22 years ago has increased 92 cents (or 92%) to $1.92. To get to 200% you’re incorrectly including the original dollar in the inflation percentage.

Brian,

That analysis is too simplistic. About 60% of families are homeowners (+/-). Most of those are not recent buyers. So they have equity. Lots of it. When they sell, they have large downpayments, so their new payments are much lower than a first time buyer with only a minimal downpayment.

So, a whole lot of the country can afford the median home.

I’m just glad someone didn’t chime in and say that “BlackRock is buying all the homes, that’s who!”

“So, a whole lot of the country can afford the median home.”

No, they can’t, hence, the low sales volume. Many have HELOCs so their equity is not that great as well as other liabilities. Also prices are starting to tank in many areas now. It’s the high end sales skewing the metric.

Desert Rat, Wolf’s charts and headline show 7 (SEVEN!!!) of the markets are at ALL TIME HIGHS and a lot of the others are only off by single digits. Prices aren’t tanking in the vast majority of markets. Besides, even a 10-20% retracement after a 100%+ runup is normal. It’s not a crash or bust.

Gattopardo, Homeownership continues to run in the mid 60% range of the population, just as it has for many, many years and decades. This is normal. And home equity and wages are higher than ever. I agree, and stats do too – over 4.2 million people will buy existing homes this year and another 1.4 million will buy new homes. Polls show millions more plan to buy soon too. Markets are healthy in most places.

High prices will eventually cure high prices, but not in the form of a 2008 crash.

CCCB

Only because of extremely low volume and high end sales that it looks like markets are at all time highs. Seven is not even close to the majority of markets. It took years for the crash in 2008. I completely disagree with you on every point. I also disagree that many are planning to buy and that most markets are healthy.

Desert Rat,

Sales are not THAT low. Jeez, come on. And hardly any have meaningful HELOCs. No offense, it sounds like a lot of wishing in your views. Look, I’ve been saying for 20 years that housing was too expensive and overdo for a serious fall (I got to be right for only a few years). And it is still overpriced, but it’s because people are able and, just as importantly, willing to pay for it. Period.

We all know our own markets best, and I can say for all of coastal So Cal, which is a pretty big area, prices have absolutely not fallen and the market is “healthy” in the sense that places listed at prices within the comps sell.

Thank God those already with homes can afford homes! No problem with that… (The mindset that has undergirded our “pull the ladder up after you” housing subsidy system for decades which has produced the current inflated result…)

This is the fundamental in Murica mindset, F everyone else as long as I get mine…this also explains a lot of rampant NIMBYisim you see in SoCal, especially in areas like OC/South OC (Irvine, Ladera Ranch, Mission Viejo, Huntington Beach..etc) or Santa Monica..

Phoenix,

“F everyone else as long as I get mine”….that ain’t Murica. That’s pretty much all of humankind. And to pick on SoCal for NIMBYism, that too is pretty much everywhere IN THE WORLD. No one wants to pay for something only to have it be worth less because of some detrimental changes.

i don’t even care if people overpay for assets, as long as they don’t think they’re entitled to keep their value, and think governments should take steps to keep them up. but many do.

Watching other players move about the board buying up property’s, I went by St James place couldn’t afford to buy, then I landed on Marvin gardens, she had 3 houses on it, costs me 850$.

Ill pass GO soon and collect 200$.

Monopoly was invented by a woman, Lizzie Magie, in the early 1900s and she called it “The Landlord’s Game”. She was a Georgist socialist and wanted to prove that the game ends with one winner who created a monopoly that bankrupts everyone else, proving that capitalism ultimately ends in a single winner if left going long enough.

Home Toad, passing go and getting $200 (quantitative easing), in the long run, won’t help. Of course, “in the long run, we’re all dead.” (Keynes)

I was in RE for 40 years. People are ignorant of markets. If people think this bubble is going to continue to infinity they are out of their ever loving minds. I would not bee buying a house right now unless it was absolutely necessary and even then I would rent right now rather than buy. Eventually there will be a lot of hurting people. Now they are pushing 2nd TDs and HELOCS again. Those got people in a lot of trouble last time. I appraised thousands of homes that were applying for them and I would say 80% were not in the income class that could afford them.

Quark, I hope that the young people who are reading these comments and are super frustrated about the housing market, take your comments very seriously.

I’m sorry but I’m calling this BS advice. I’ve been “in the market” since I was old enough to consider buying a home — call it 2013. At every turn, I’ve told myself to “just wait, there will be a correction.” NOPE, couldn’t have been more wrong. I would be sitting pretty right now had I just bought. Luckily I had very affordable rent all these years and investments that have done well for me, but having a home would have augmented that substantially. I know several people who simply bought a house, lived in it, spent zero money on anything beyond the bare minimum repairs, and netted huge returns… even in areas that took a turn for the worse. I liken housing to the stock market – you can tell yourself you know what’s going to happen, but you really have no clue.

But not everyone wants to treat their domicile like a casino chip. I didn’t. I know jumpers like the ones you describe, too; people who literally scrounged to get a min down on a hovel in beautiful BFE only to sell it a few years later and walk away with a chunk. But the thing about sudden windfalls is that there’s a psychological component, which is almost ineluctable; it’s called SWS (Sudden Wealth Syndrome), the summary analysis of which shows that unearned money tends to get pissed away (EZ come/EZ go). It’s almost like the money isn’t real. It’s similar to how people who use coupons tend to spend more money when shopping than those who don’t. I’m watching one lucky girl slowly burn through her pennies from heaven now. It’s unnerving, but not surprising.

The few people I know who never jumped into this madness were the ones who lived in self-imposed austerity, scrimping & deferring in order to get a DP together. No fat parents and no sudden windfalls. These are the buyers who are striking; I think any capitulation at this point is coming from the former crowd.

@Bobert you have learned what many people never learn (timing the market almost never works) I’ve been “in the market” for 50 years now and real estate has “always” been expensive and almost everyone who bought a home they could afford when they were in a stable job and had plans to stay in the same area for a decade or more has done fine. The one change I have seen is that there is an increasing number of areas where the majority of the homes are bought with “wealth/family money” so unless you have a lot of wealth or family money it might be a good idea to make a plan where you are not truing to “earn” enough to buy a home in Atherton, Aspen, Beacon Hill or Nantucket.

Luckily, those bloodless bergs you mentioned are hideously boring and not worth living in if you possess even a trace amount of soul.

This may come as a shock to you, but you now have to have “wealth/family money” to buy a house anywhere, never mind Aspen or Nantucket.

to a point, but if you bought in certain bubble markets in 2007, you were underwater for 15 years, and may still be underwater if not for the covid helicopter drop.

if you buy a house in nashville today for 600,000 usd that was 275,000 usd in 2018, there’s a good chance you’ll get burned.

“just buy when you can and when you need a home” is generally good advice, but not during extreme bubble markets in my opinion.

Were you really “in the market” from 2015 to 2018? Average prices and historically low interest rates. What kind of a a correction were you waiting for?

You forgot to mention the recent offers for zero percent down mortgages.

Exactly, on every point.

Mission accomplished! Bold, brave Jerome Powell has vanquished housing inflation with his courageous hawkish holds!

He needs to hang that banner up on the aircraft carrier asap..

It would be nice if the Case-Schiller Index went back to the Great Depression. I wonder what it would look like in 1953.

You would be seeing loans for $3,000-$6,000 to buy a nice post war 1000 sq. Ft “You Kids Play Outside” home.

My guess is that this is the NVIDIA effect. Enough people cashing out to move the needle in big cities.

Some of these markets have a lot of foreign money pumping in as well.

Until more folks die off or otherwise don’t need housing and/or they build more, this bubble will hold steady. The market is stuck. Even if existing owners sell, if they buy in the same area, there is no net gain in inventory. In desirable locals, the few houses for sale (from someone who dies/moves out of the area) are plucked up by ample cash buyers. Only a demographic change or recession will break this bubble, at least in the popular locals, typically high employment centers.

Active listings are surging and price cuts are surging already:

https://wolfstreet.com/2024/06/21/home-sales-sag-further-hit-by-mortgage-rates-price-reductions-active-listings-surge-median-price-skewed-higher-by-surge-in-high-end-sales/

Price reductions rose to 35% of active listings, the highest for any May in the data released by Realtor.com going back through 2017:

Active listings surged to 788,000 homes, the highest since July 2020, and up by 35% from a year ago, according to data from Realtor.com, as more new listings came on the market amid very slow sales. Compared to May in prior years:

So, in spite of the mantra that there’s a housing shortage across the country, the supply of existing home listings is increasing.

It’s still about 400k below pre-pandemic active listings.

Yes, but demand and sales have plunged too by about 25% to 30% from pre-pandemic numbers. So it balances out.

The reason: People with 3% mortgages who would normally have moved to a different home (sell one and buy one) are now less likely to do so. In my calculations, both DEMAND and SUPPLY dropped by 20%-25% because these people are neither sellers nor buyers. They have left the market. So that portion of demand AND supply has dropped in equal measure.

I put some numbers to it here:

https://wolfstreet.com/2023/07/21/entire-housing-market-buyers-and-sellers-may-have-shrunk-by-20-25-because-of-the-3-mortgages/

The “housing shortage” mantra reminds me of the “office shortage” mantra in San Francisco and elsewhere in 2019. It’s all RE propaganda to create FOMO and drive up prices. Vacant office inventory too suddenly came out of the woodwork to form the biggest glut ever with a catastrophic drop in values and massive ongoing losses for investors and lenders.

“House prices aren’t going back up. You’re just a real estate shill!”

“OK, house prices are going back up, but they’re still below the 2022 peak. They’ll start going back down soon.”

“OK, house prices didn’t start going back down, but they’re still barely below the 2022 peak, and they’re unlikely to get back there.”

“OK, house prices got back to the 2022 peak, but they won’t rise above it.”

“OK, house prices rose above the 2022 peak, but look at that inventory!”

@Frank,

There are still around 10 million effectively vacant hoarded homes out there. The “housing shortage” is a myth.

So true. At any point in time about 20 to 25 units in my 100 unit condo complex in San Antonio are vacant. This place is like a ghost town and you rarely see people outside or at the swimming pools.

If these bubbles pop there’s the next recession. About the only way they don’t pop is if rate cuts start happening and the bond market and hence mortgage rates follow. I think the bigger question I have is how is there a shortage of housing if the population isn’t growing that fast? Is that people are abandoning homes that no one wants due to a declining area? Something else?

I doubt there would be any deep recession anymore.

What we’d experience is shallow recession and high inflation masked by doctored government metrics.

Bottom line.. currency devalution is the only game in town.

Home prices have not increased 65 percent in last 5 years in my neighborhood but dollar has lost that much value .

When Powell says higher for long he means higher prices for longer

The average number of occupants per household could be dropping as well to drive the apparent shortage. Roommates or family living together moving out to get their own place. I recall reading about this trend post-COVID.

“The average number of occupants per household could be dropping as well to drive the apparent shortage.”

I wonder about this too. I had a gazillion roommates at my first apartment and thought that was normal.

There is no terrible housing shortage. I know of plenty of 3 bedroom starter homes that sell between 150k to 250k fully refurbished and ready to move in. They are just not located where people want to live. People want to live in areas of great schools, lots of good stores and restaurants, low crime, etc. Well those places will cost you $500k to $1 million.

I bet there are plenty of house in East St. Louis or Gary Indiana.

They’re literally giving away “houses” in St. Louis.

I saw essentially condemned, falling down, tarped structures available. I’m sure someone has gone into these neighborhoods and “refurbished” some of these.

So, yes, for people who don’t need education, security or food but only dilapidated “shelter” there’s a bridge or culvert near you!

Otherwise why pay to live next door to a crack den?

There’s a difference between buying a house and buying a lifestyle. Getting both comes with a significant cost.

As you well know, EK, that applies to buying cars as well.

Cautionary tale of “housing incubator” ~ nytimes.com/2017/11/04/business/detroit-housing.html

Note: this article is seven years old, yet the story remains the same..

Btw Motor City has some of the highest auto insurance rates in the US.

Northeast has been all but IMMUNE. Crazy up here.

Why do you keep calling these bubbles? While you’ve been calling them bubbles the prices have gone up 200 percent. Someday, there will go down 10, 20 maybe 30 percent. But anyone who has been standing by for years has lost their chance to build wealth and has become part of the permanent underclass.

I started this series — “The Most Splendid Housing Bubbles” — in 2017 to document the crazy rise in home prices at the time. A “bubble” means prices go up a lot. When prices go down a lot, it’s a “bust.” But I’m not changing the name of the series, no matter what happens to prices, even if they go down 50%, I’ll still call the series “The Most Splendid Housing Bubbles…”

You mean standing by while the required down payment for a starter house or condo rises faster than they can possibly save? Those dum-dums!

Murrca, Not true. I’ve sold multiple properties, from raw land to trailers to single family homes to condos over the past several years.

All had very low down payments and most received a credit towards closing costs from me, the seller. I’ am in the real estate business and you’re talking ignorant crap like a lot of the bitter folks who comment here because they were afraid to buy or waited for the correction that never happened in order to buy.

As far as I know, all my buyers are happily enjoying their homes, building equity and have the peace of mind not worrying about rent increases or their homes being sold out from under them.

Why is it not surprising that you’re a RE agent…

Pfft. As far as you know. That’s quite a qualifier.

And is not a ‘credit’ — it’s just the illusion of a rebate. You’re playing on the larcenist premium that all small-time Charlie’s play on: something for nothing. In a truly healthy market, buyers wouldn’t need your cute little coupon.

The large-scale story is told by the charts Wolf posts here. Yes, there are corners of the country where there’s some affordable housing, but not everyone is portable to these far-flung locales (in our case, we have a brick-and-mortar business in a major metro that wouldn’t be transplantable).

Our next best hope is possibly building, in the not too distant future.

I’d wager some of those clients are unhappy. You really shouldn’t buy a home based on a monthly payment, little to no downpayment, and a high rate like the last few years. If you hit one rough patch for whatever reason. You could potentially lose that home without an emergency fund saved. If homes don’t appreciate enough or even go down a little. They have no way to refinance that high rate if it goes down. Surely their taxes, insurance, and maintenance costs are increasing in the meanwhile if homes only go up as you claim. So yes, maybe their rent isn’t increasing. But that’s likely not sound RE advice you have given folks. It’s actually probably advice on what not to do.

Oh gimme a break. You’re talking your book hard. Anyone who missed the tail of meteor will catch the next one. This country is a bubble machine.

Very nice article!

I see that the champagne and cocaine party continues to rage. We need to build more housing

People are so misreading Case Schiller. It doesn’t mean all houses are going up by a certain percentage. When you have low sales volume like now, higher end sales can definitely skew the results.

1) Most C/S charts are divided by two. They look like QQQ. The first half between 2002 and 2012 is the accumulation zone. The jump started in 2012. Most cities are in either in distribution or re-accumulation since 2021.

2) Those who bought a house in the first half are not “stuck”. They can sell their houses and for a huge profit. The rest are “stuck”. A few pairs : bought in 2004, or in 2012 sold in 2024 skew up the whole chart and lift it up.

3) A landlords who put a million dollar house in strangers pockets collect 4%/5% annual rent before inflation, mortgages, taxes, repairs, insurance, mgt fees and vacancies. Those who bought in the last few years might break even, at best, but they don’t care, bc they want to accumulate assets for retirement.

4) The front line of the boomers approached eighty. 77% of them own a house. In the next two decades the boomers will create a tsunami of houses for rent and for sale before moving elsewhere to the next phase.

5) All of the sudden the boomers fell in love with the illegal immigrants.

The boomers want them to pay social security and keep the current housing bubble afloat.

Nice to see you’re back, ME. But on #5, you jumped the rails, something you’re prone to.

5) Liberal politician wants new immigrants to pay SS and keep

the housing market afloat.

The immigrants…most won’t be going anywhere except to work, making money, paying rent and buying these houses. It’s a free for all….wang dang. Got to up your game any way possible, being a patriotic US citizen and playing by the rules is good but not a strategy, in many ways it’s a detriment…double take on that gnarly…that’s where we are.

The good ole USA, gotta love this place.

#5 has always been true. (But the official statement is “build the wall”).

Outsourcing became a dirty word (and of course, continued) and recently has become onshoring.

The massive expansion of the past 50 years has been largely on the backs of cheap labor (immigrants), many of whom have been paying into SS (and sharing the same number).

This is continuing but we have to consider the undersized impact on housing. I’m sure there’s some numbers regarding the Sf. Per person across varying demographics.

I have less than 250 sf. Per person in my household in a neighborhood with 10,000 sf. Houses empty for 26-50+ weeks per year.

Consider that 5% of people own a second home and they’re mostly not immigrants (although they may occupy some of these as caretakers?)

Your wrong about all the boomer homes hitting the market. At 70+ my kids are pushing 50. The three homes I spend time in, will get lived in or rented.

I love the illegals! Only people willing to work. So different than lazy entitled americans waiting for a handout.

Advice – learn Spanish.

The problem is this country subsidizes housing through mortgages (something socialist France doesn’t even do) and universally restricts building everything but cookie-cutter dead worm detached housing in subdivisions due to NIMBY zoning (also not very laissez faire). What does this have to do with “liberal cities”? Indeed, to the extent they follow the above policy maladies, they’re not actually very liberal.

Yes, blame a politician, rather than an economic or social structure.

We all know that the “right guy” (or gal?) will set things straight.

Where, pray tell, are the well run, affordable and desirable conservative cities we should be buying homes?

(Maybe including ru82’s “ great schools, lots of good stores and restaurants, low crime, etc.” as I am an entitled 1st world scoundrel who desires to fulfill basic needs)

It might be that he’s blaming the policies put in place by well meaning, but misguided, politicians that cause the cities to go to heck in a hand basket.

It’s rarely purely a “red” or “blue” issue. By firing up a few neurons one might realize that civilized policies and enforcement of the rule of law is what makes neighborhoods desirable or not so much.

Lax enforcement encourages criminal behavior. The burned out, tarped roofed, broken windowed structures didn’t get that way by themselves. They usually had help.

I think they need to update their sampling areas because it doesn’t include some of the largest metro areas and cities, including the Houston metro area, and Austin and San Antonio cities which are really becoming one large combined metro area. I know the Austin area has had wild price swings in the recent past, and the Houston housing market always seems to march to different drummer with boom and bust cycles based on the oil and gas industry conditions that are often counter to the rest of the country. It might not change the overall results significantly but it would give a more complete picture.

Matt S,

Unlike many states, Texas does not require disclosure of actual prices paid. Wolf would have better information on the methodology Case Shiller uses to compute the values for Dallas, but my understanding is that it is far more laborious than for houses in other states, which is why they don’t do it for other big Texas cities.

We should require actual disclosure of prices paid, but that would stop the games played by wealthy people to manipulate the property tax system.

When the appraisal districts assess value, they have a pretty good idea what the properties are worth in neighborhoods for ordinary people, even at the higher end of the scale, so their numbers are in the ballpark.

On the other hand, the houses of the super-rich tend to be more one-off. Someone will buy a house for $10 million that was previously on the rolls for $3 million (the seller had it for many years). The CAD won’t know the sales price but will know that houses have gone up, so they’ll appraise it at $6 million. But then our super-rich guy’s hired guns will argue it down to $4 million. So the county and school districts will lose out on that $6 million difference, and the burden will be shifted to those taxpayers who “suffer” from more accurate valuations.

I have been on appraisal review boards and have seen this play out. Price disclosure would end this. But the super-rich are well connected with the legislature, and the legislators themselves can sell non-disclosure to their constituents by implying that disclosure would make everyone’s taxes go up. They won’t, for the reasons outlined above, but Texas property taxes are high and the fear is there to be exploited.

Well stated. Good post!

In terms of Case-Shiller in Texas:

Back in the 1990s, when the CS was designed, they ran into big problems getting public records data in Texas, which doesn’t allow public access to deeds, which is where the CS data comes from.

To get the data for the Dallas metro, the CS people at the time worked out a deal with a Realtor association to get data from their multiple listing service.

And in terms of Houston, one of the founders of the CS said this:

“And when it was all put together, the decision was that was a bit of a hassle, so we’d stick with one city,” he said. Also, “we had Boston, New York and Washington so we decided that was enough for the Northeast, with apologies to Philadelphia.”

“argue it down to $4 million. So the county and school districts will lose out on that $6 million difference, and the burden will be shifted to those taxpayers who “suffer” from more accurate valuations”

Yes, or the state/county/municipality will spend less. Prop tax based on value has always rubbed me wrong. Why is it even relevant what a property costs? The same house on very small and very large lots pays different tax? Seems crazy.

I have been reading articles in the past few months that suggest that the 3-4 % rates we have experienced in the recent past were aberrations. The rates now are closer to the norm and may be so for years to come. I am reminded of my first house from 37 years ago where I was paying 10.5%. This house, which I paid off last year, had a 3.99% rate on the mortgage. I am sorry to say that relief for first-time home buyers is not in sight. Those that own homes are locked into their homes with low rates. It’s an interesting situation made much worse by rising insurance costs, making homes unaffordable to both prospective homeowners and current homeowners. The American dream of home ownership appears to be fading. Very sad.

No one who owns their home outright is locked into anything. About 40% of all homes are owned outright.

I doubt it. Things change, is all. The idea of a 30 year mortgage is ludicrous when you think about it. I know I would not have wanted to be welded in place since 1994.

I anticipate a new paradigm (I know I know) where residential real estate is concerned. Prices need to be rendered down and salaries need to come the hell up so that 10-15 year mortgages are the norm. Whatever happens, the old ways clearly aren’t working anymore, but we still have one foot stuck fast in a now mouldering last century.

Hope springs eternal.

You don’t anticipate that paradigm, you desire it. It’s never going to happen. Why waste time on fruitless thought? See things as they are and adjust accordingly. You can accept reality without agreeing with it and it is a peaceful way to live.

This isn’t snark, I hear and read these sentiments all the time, especially from the religious. In real life, NO ONE has faith in anything that is not already grounded in some semblance of reality.

You don’t hire a local teenager to fix your AC unit and HOPE he can do it, you hire a licensed professional that you already BELIEVE can do it.

I have no dog in this fight, so my desire doesn’t enter into it. Just a common sense observation. There’s always generational thinking which entrenches fast. People like thinking they’re right. Their temporal-parietal junction freezes over; they fear and reject the invention of new ways to live, which are inevitable. You can see it here even in your own knee jerk.

Of course, the refuseniks will be relegated to scrapheap city, where they can gnash & gurn and talk about the good ol’ days to anyone polite enough to listen.

The current system is flawed and the generations behind mine see it and want something else; something other than a negative sum game. It pretty obviously can’t go on. And it won’t.

Things change, for housing and everything else. When inflation was taking a big bite in the late 70s, there were some homes for sale with “assumable” 30-year mortgages, at lower rates than the rates that were then running high and climbing. Those were peculiar because the new loan had to be a 2nd TD, and those were more expensive. So it was kinda frenetic, but only for a brief time. The large, assumable loans were being snapped up.

In response to rising interest rates, the new, fixed-rate loans were no longer assumable. And then, as interest rates kept rising, 30-year fixed rate loans were being discontinued, replaced with adjustable rate loans. Banks couldn’t sell off those fixed rate loans, so adjustable were the only ones available.

There are many countries that don’t have 30-year loans. Some only have 5-year loans, fixed or maybe only adjustable. We could see that happening here at some point.

It’s silly to assume that what we’re dealing with right now in terms of home buying is permanent. Anchoring on these rates, prices and conditions is a fool’s errand.

Another question I have is how “reverse mortgages” or Home Equity Conversion Mortgage (HECM) fit in this picture. There is a lot of noise about how those evil boomers are staying in their homes longer because they were financed at very low interest rates, but there are also a lot of stories about how little money many people have saved for retirement. Are retired home owners tapping into the supposed equity of their homes? If the housing market crashes what happens to those individuals? How much do HECM’s impact home sales? The little stats I can find seem to indicate there are not a huge number of reverse mortgages, but is that changing?

Drawing equity out of your home is not a sale of the home. It doesn’t matter what method you use, cash-out refi, HELOC, 2nd-lien mortgage, HECM, etc.

Cash-out refis have collapsed with higher interest rates. So the equity withdrawal has shifted from cash-out refis to other methods. And those numbers are rising but still minuscule in the overall numbers. Here are HELOC balances, at $380 billion compared to $12.3 trillion in mortgage balances.

People still believe all the bs pushed out by the real estate crowd. There is no housing shortage other than location, location, and location. That is changing fast like SF. Lived there once and loved it, now I will not even visit.

Then there are those who think they are an investor because their shake went up in price. They will hang on till the last moment, even when they are loosing money every month.

It will take years to work out and most of the hold outs will loose alot of buying power.

An investor would take their gains and move on to their next idea.

Stagflation is rising prices with recessionary sales conditions, and that is what we have in the housing market. This will be the story for the remainder of the decade. Stagflation will kill any buyers strike.

An extended period of stagflation (years, not a few months) will kill RE prices because the economy and incomes fail to grow even as high inflation persists, long-term interest rates will be higher due to higher inflation, and people won’t make more money to pay for more expensive homes (and other stuff).

I don’t think we will get an extended period of stagflation, I think we will get just higher inflation and some economic growth. But if we do get stagflation for a long time, you can kiss this overpriced housing market goodbye.

If we get a recession, including a travel recession and a significant loss of employment, that would be another thing to massively trip up the housing market, with a flood of vacation rentals hitting the for-sale market as investors cannot get enough revenues from rentals to cover their costs; and with other people, who lost their jobs or fear losing their jobs, putting their vacant homes on the market that they’d tried to ride up the price spiral with.

That’s exactly what I’d be watching. When these new real estate investors’ income producing assets stop producing incomes, are they sitting on enough other income and savings to pay that mortgage?

Keep an eye on some of those companies like Airbnb, VRBO, and the major hotel vacation entities (Hilton Grand Vacations…). If they’re public, and hitting 52 wk. lows, their punishment may precede some of the homebuilders and related businesses. TRVL is an ETF with a huge portfolio of travel related companies. Right now, they’re still doing fine.

In contrast, recreational vehicle cos. are in the tank.

Totally disagree … that is not what happened in the 1970s. The mistake you are making is not recognizing the stagflation environment faced by the real estate market. This is fundamental. Remember, wages increase under stagflation.

@vadertime as I mentioned in a previous post, almost every American homeowner will tell you “Homes were “expensive” related to their income when they first bought a home”. Growing up on the SF Peninsula almost all the kids I knew had parents that moved to the Bay Area from somewhere else for a job. As a landlord I see less and less “kids” (people under 40) every year that seem interested in moving for a better job or lower home prices (they just rent apartments from me, complain about their jobs and high home prices while they have the DoorDash guys bring them coffee in the morning and dinner at night).

AI, I would add to that, they spend their future down payment $$$ to travel all over the world to be able to post pics of their lifestyles of the pretend rich and famous for people who don’t know them or care about them to look at and criticize.

My theory is they all know their baby boomer parents will kick the bucket before long and they’ll get nice homes or big bank accounts bequeathed to them, so party on! And if they don’t, they’ll get down payment help from the despised boomers, lol. (The percentage has doubled recently from 19% to 36% getting help)

The young ones hoping to inherit wealth often fail to look how much money their parents will burn up in assisted living and healthcare costs, but party on everyone

And when mom finally passes away at 98, the kid is going to be near retirement age.

A mom who is 65 now has another 20 years of average life expectancy, so till 85. But that’s average. If she’s fit, it could be a lot longer.

A mom who is 80 now has another 10 years of average life expectancy, so till 90.

A mom who is 90 now has another 5 years, so till 95, etc.

If people wait for their boomer parents to die so that they can get the Easy Ride for life, they might instead spend a big part of their lives waiting.

My (pushing 90) parents were just at a funeral for a 98 year old woman, her “youngest” kid was 70…

The Prince Charles syndrome?

Most end of life medical costs are covered by Medicare, except long-term care (think nursing home). If a person can stay out of nursing homes and memory care facilities, the healthcare costs should be manageable for the individual.

You can clearly see in the charts that homes are more expensive in terms of income than they’ve ever been. I don’t get the looking down your nose at people that clearly are responding to the incentives placed before them. You’ll never take your wealth with you no matter how hard you worked to acquire it.

@Mismeout I’m not “looking down my nose at people” I’m actually trying to help them, my Grandparents left Ireland and Scotland to come to the US for more opportunities and before the end of the last school year I was talking to a bunch of HS kids (many who had parents that left Mexico to come to the US for more opportunities) in a “Junior Achievement” group a friend runs and I was telling them that while it is possible to work hard and save up to buy a nice house on the SF Peninsula it is way harder than it was when I was younger (and way way harder than when my Dad was 20 and nice homes in Burlingame and Palo Alto were ~$20K) and they should look for other areas that may have more opportunities than the SF Peninsula (that has sky high rents and a ~$1.5mm median home price).

Very true but let’s also keep in mind that housing un affordability has never been this high and this is the crux.

The New York numbers shock me. 50% price appreciation on top of arguably the most expensive housing stock in the US with 7% mortgage rates.

It seems the money supply of affluent buyers is infinite. No home price and no cost of capital slows them down.

This is not New York City, but the vast New York City metro that spans these counties in four states (NY, NJ, CT, and PA):

Fairfield CT, New Haven CT, Bergen NJ, Essex NJ, Hudson NJ, Hunterdon NJ, Mercer NJ, Middlesex NJ, Monmouth NJ, Morris NJ, Ocean NJ, Passaic NJ, Somerset NJ, Sussex NJ, Union NJ, Warren NJ, Bronx NY, Dutchess NY, Kings NY, Nassau NY, New York NY, Orange NY, Putnam NY, Queens NY, Richmond NY, Rockland NY, Suffolk NY, Westchester NY, Pike PA

doesn’t shock me. when you print trillions and nearly all of it ends up in the hands of those who already have tons of money, they use it to buy stuff, including houses.

shouldn’t shock anyone.

Where do you come up with such totally false notions?

Hard to believe that San Francesspool hasn’t recovered. So idyllic.

In my part of Dallas, a small suburb called Coppell, houses are still selling way above 2022 prices. I do not understand what is going on with housing.

MW: Dollar Soars to Fresh 2024 High…

Yawn. Still 1.09 Euro. Wake me up at parity.

My continued interest in watching this circus, is the disconnect between the speculators that buy overvalued homes, then race to plow more money into upgrading and updating their lemons — in a race to flip it before a crash — that moronic game obviously is slowing, as fewer rubes have the ability to qualify.

Additionally, as fewer rubes qualify, inventory is expanding fairly rapidly in the buyer/seller strike. Unfortunately, sellers are trapping themselves into being over leveraged and all that’s gonna do is extend the length of bubble deflation. I think capitulation is years away.

MW: New-home sales plunge to lowest level since November

Chicago does not want to stop after having a milder increase in 2010s. Although we are finally seeing more inventory on the market than previous years which hasn’t been the case for a long long time so maybe the trend will start to reverse soon, or at least flatline.

The smallest four-bedroom single-family home next door is still on the market, asking 969,000. East Bay property dumpster-style living on a backstreet off MacArthur. Not close to Bart.

I think I’ll move to New Mexico and live like a king where people make, on average, 59k a year.

I would miss the caviar from the fisherman’s wharf and occasionally stocking Wolf at Peet’s Coffee in the Marina. But besides that, I probably wouldn’t even know I moved away from California.

Edit:

I would miss the caviar from the fisherman’s wharf and occasionally “stalking” Wolf at Peet’s Coffee in the Marina.

To err is human.

I am somewhat baffled as to how “market experts” prepare such intricate “current-market” analysis based upon data that is 30 days or older. It’s not the current picture. It is the same perplexing feeling I get when CNBC or Bloomberg report phenomenal (mind blowing “buy the stock”) corporate earnings which are over a month old and telling the world what “a great company” it is when I have first hand knowledge it is about to plunge.

With respect to the real estate markets, any market with any growth right now is going to be the first to hit the floor. For example, Miami, there are so many condos with residents that have not paid their HOA / maintenance in multiple months, and there are growing numbers of defaulted mortgages. And with all of the hype of new construction and name-brand designer and automaker buildings going up, Miami developers have failed to share that pre-construction deposit positions have been dropping rampantly. Obviously they don’t want to disclose nor do they have to because the developer has been able to secure 100% construction funding based on those pre-construction deposits which are mostly now to less than 50% committed. I’m just waiting for the day that they find out that the developer established multiple corporations for $150 and put the deposit up themselves to get the construction funding.

In short, I’m waiting for the day that we have true real-time non-manipulated numbers to use as a guide rather than hearsay and inflated self-serving data. It’s available but it’s obvious why they don’t want to provide it. The truth hurts and public wants to hear good news only…