Re-accelerating inflation in Q1 hit “real” GDP growth. “Current-dollar” GDP growth only a hair slower than in Q4.

By Wolf Richter for WOLF STREET.

In Q1 2024, our Drunken Sailors – as we’ve come to call the all-important consumers lovingly and facetiously – spent very vigorously on services at the fastest growth rate since 2021, adjusted for inflation, but not so vigorously on goods. And private fixed investment jumped at the fastest rate in two years.

But dragging on GDP were the trade deficit, which worsened sharply on a majestic surge of imports, and federal government consumption expenditure and investment, after five quarterly spikes in a row. But we think that the slowdown in government spending was just a blip because we don’t see a slowdown in that department.

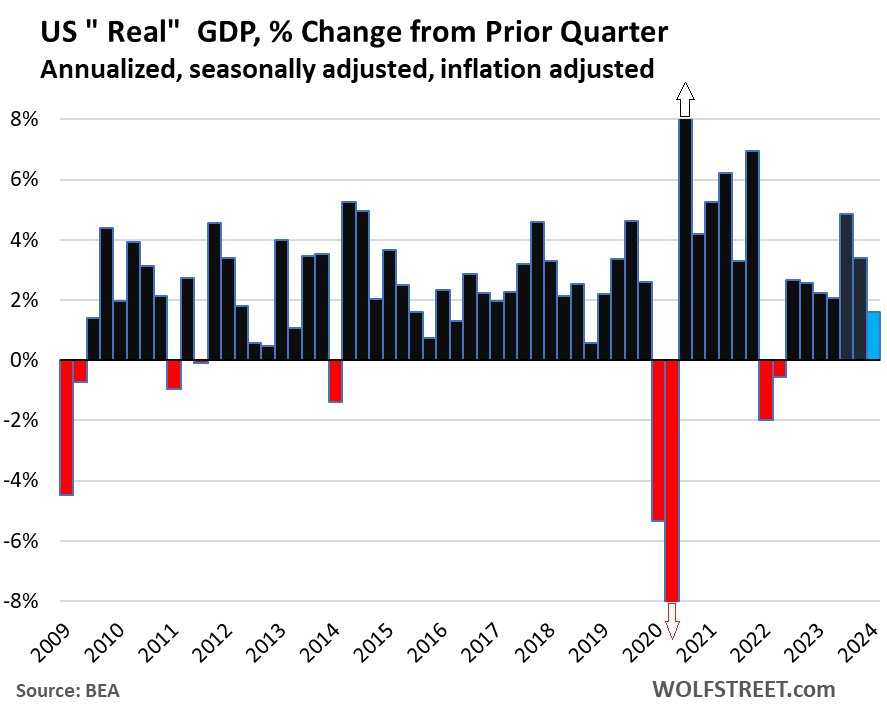

GDP, adjusted for inflation (“real GDP”), rose by an annualized rate of 1.6% in Q1 from Q4, following the 3.4% increase in Q4 , according to the Bureau of Economic Analysis today:

- Consumer spending (69% of GDP): +2.5%, on a 4.0% surge in spending on services and a 0.4% decline in spending on goods.

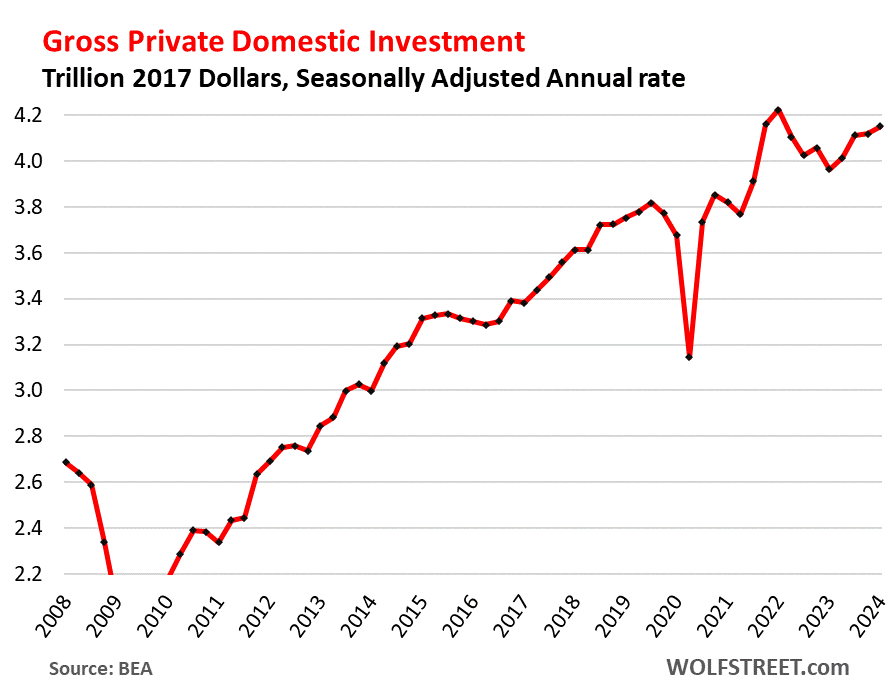

- Gross private investment (18% of GDP): +3.2%, pushed up by a 5.3% surge in fixed investments, and dragged down by a smaller increase in inventories.

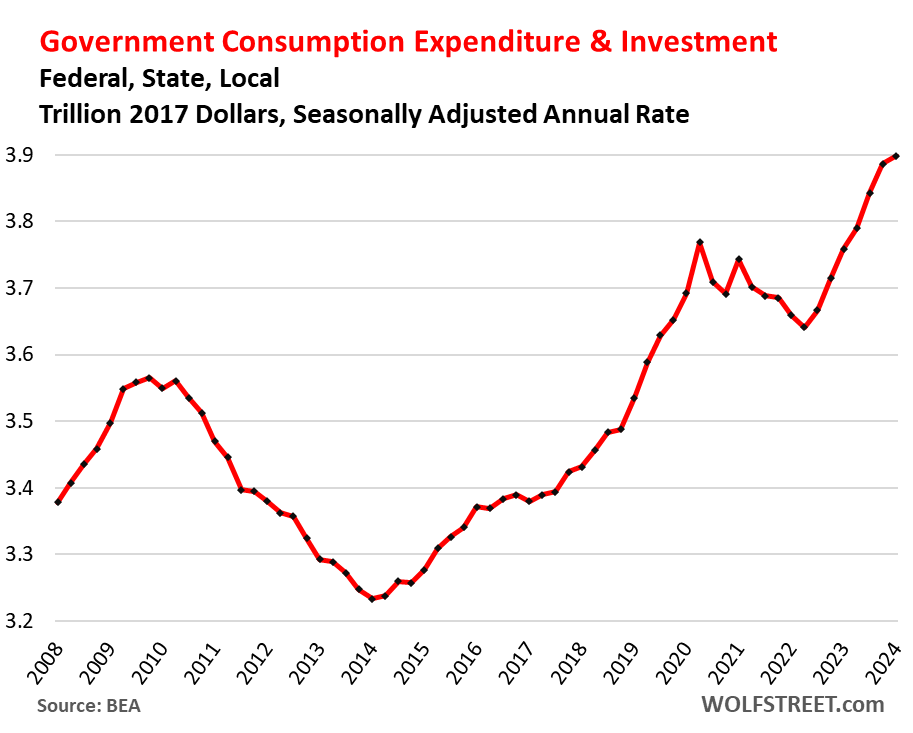

- Government consumption and investment (17% of GDP) dragged on GDP: +1.2%, on a decline in federal government spending (the “blip”).

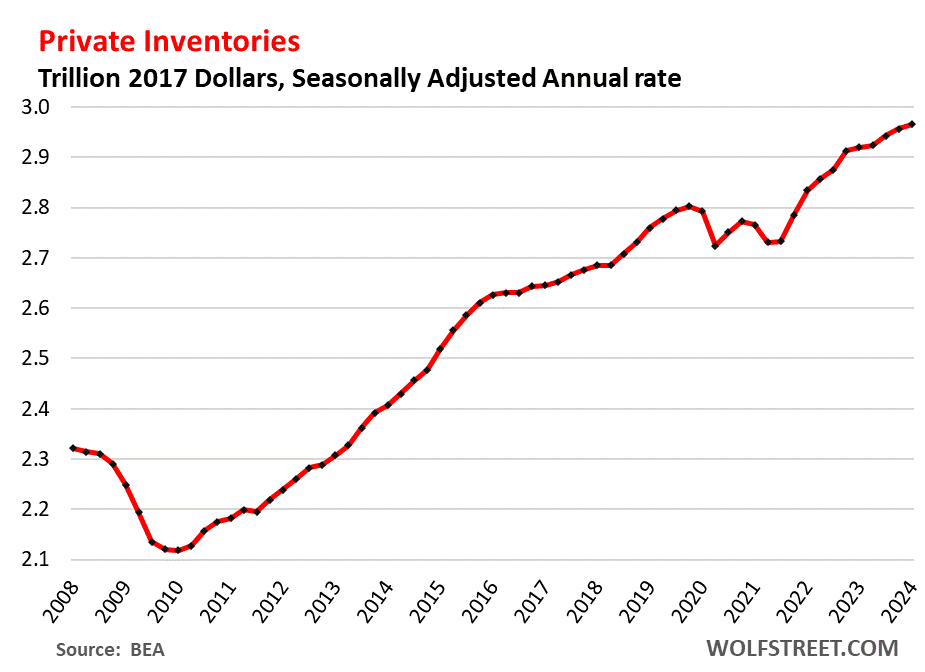

- Change in private inventories dragged on GDP.

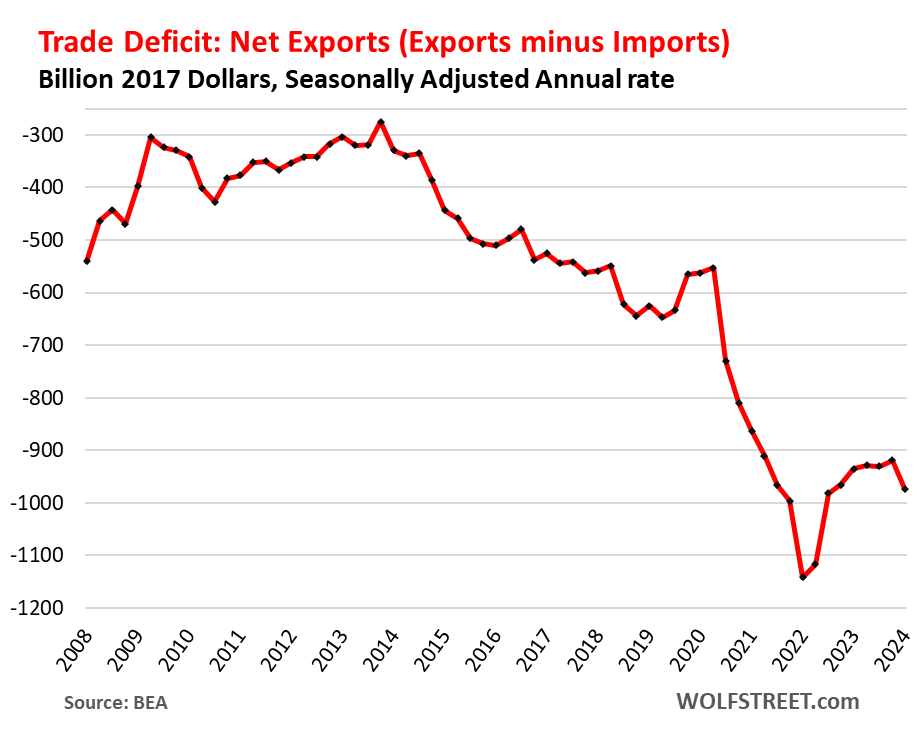

- Trade deficit worsened a lot, on surging imports, and dragged bigly on GDP.

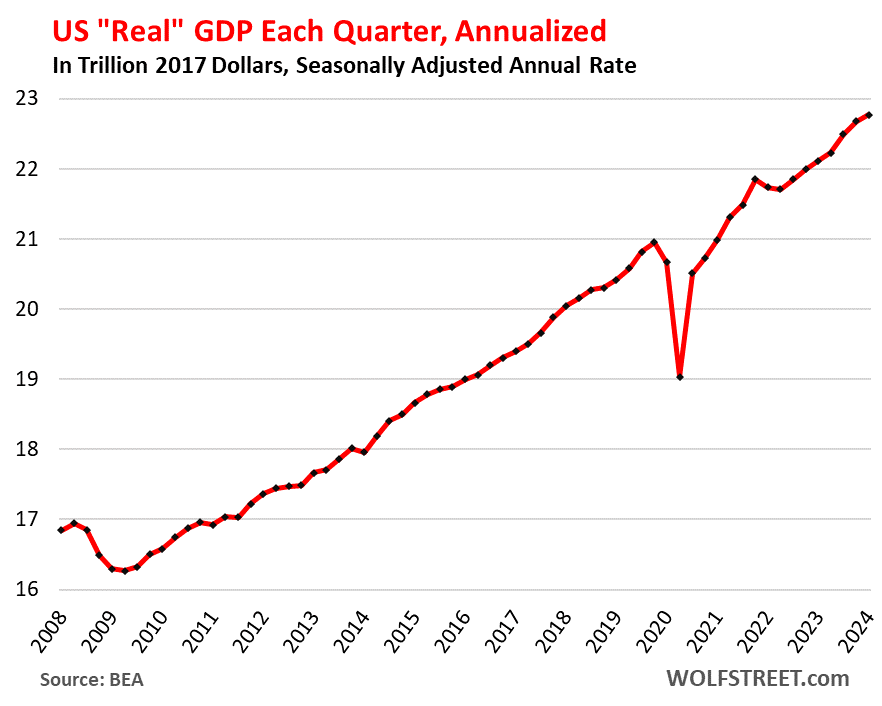

“Real” GDP in dollar terms, adjusted for inflation and expressed in 2017 dollars, rose to $22.77 trillion annualized in Q1:

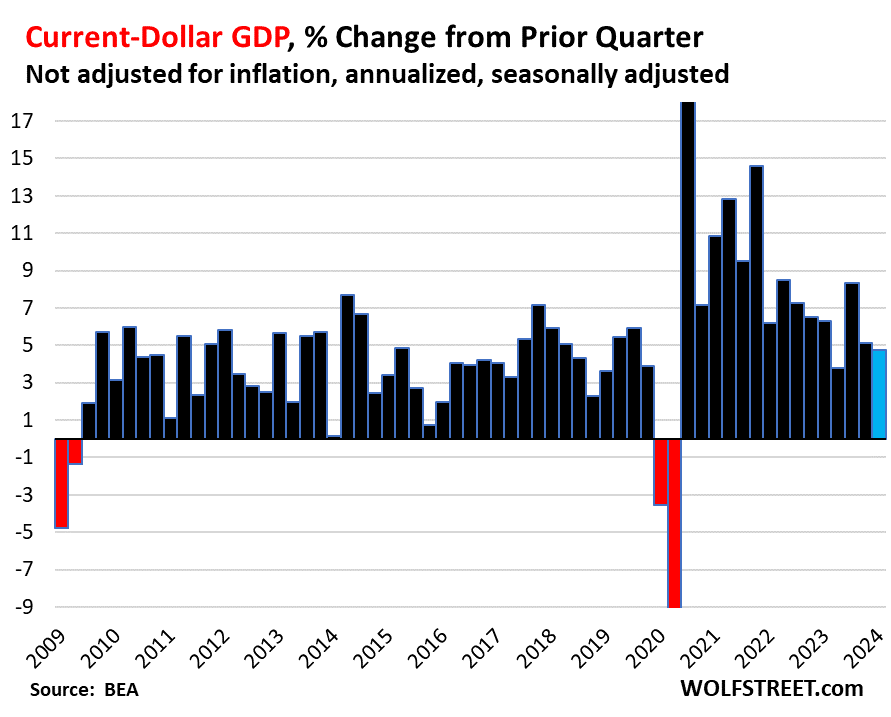

The size of the US economy: “Current-dollar” GDP (or “nominal” GDP, not adjusted for inflation and expressed in current dollars) jumped by 4.8%, or by $327 billion, to $28.3 trillion annualized. This $28.3 trillion represents the actual size of the US economy, measured in today’s dollars, and is used for the GDP ratios, such as the US debt-to-GDP ratio.

As you can see in the chart below, “current-dollar” GDP growth in Q1 was similar to Q4: 4.8% v. 5.1%. But what happened in Q1 is that inflation re-accelerated sharply, and so on an inflation-adjusted basis, “real” GDP (see first chart) in Q1 grew a lot less vigorously than in Q4:

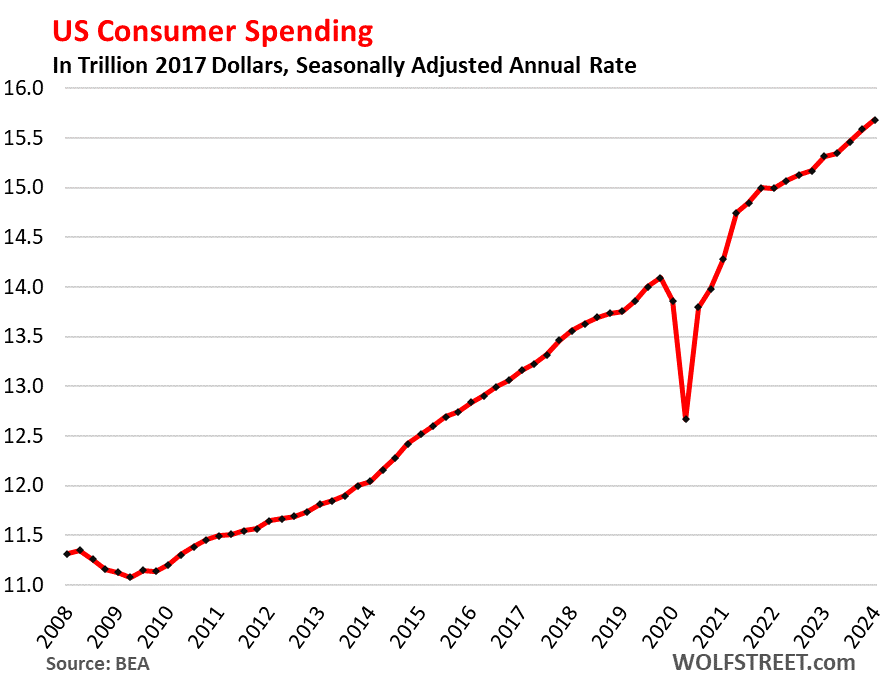

Consumer spending on goods and services rose by 2.5% in Q1 from Q4, to $15.7 trillion annualized and adjusted for inflation. This growth was slower than in Q4 (+3.3%).

- Spending on services jumped by 4.0%, the fastest growth since Q3 2021.

- Spending on goods dipped by 0.4%, driven by a 1.2% decline in spending on durable goods. Spending on nondurable goods was unchanged.

Adjusted for this re-accelerating inflation, Drunken Sailors still, despite 5.5% Fed interest rates:

Gross private domestic investment jumped by 3.2%, to $4.2 trillion annualized and adjusted for inflation, a sharp acceleration from the 0.7% growth in the prior quarter. Of which:

Fixed investment: +5.3%, the fastest increase since Q1 2021, of which:

- Residential fixed investment: +13.9%. the fastest increase since Q4 2020

- Nonresidential fixed investments: +2.9%:

- Structures: -0.1%.

- Equipment: +2.1

- Intellectual property products (software, movies, etc.): +5.4%.

Still not back to the levels of investment during the free-money pandemic spike:

Government consumption expenditures and gross investment rose by 1.2%, to $3.9 trillion annualized and adjusted for inflation. It was the smallest increase since Q1 2022, pulled down by a decline in federal government spending, after the spike in the prior quarter.

This does not include transfer payments and other direct payments to consumers (stimulus payments, unemployment payments, Social Security payments, etc.), which are counted in GDP when consumers and businesses spend or invest these funds.

- Federal government: -0.2% (national defense +0.3%, nondefense -0.6%).

- State and local governments: +2.0%.

Government consumption expenditures and gross investment had surged five quarters in a row with quarter-to-quarter increases in the range of 3.3% to 5.8%, adjusted for inflation and annualized.

So this smaller increase was likely just a blip, because we haven’t seen a slow-down whatsoever in spending.

The Trade Deficit (“net exports”) in goods & services got a lot more horrible:

- Exports: +0.9%.

- Imports: +7.2% with goods +6.8% and services +9.0% (services imports includes the surge in spending by Americans traveling overseas).

Exports add to GDP. Imports subtract from GDP. Exports are much smaller in dollars than imports, hence the trade deficit, or negative “net exports.”

The worsening imports dragged GDP down by 0.96 percentage points. This means that if had remained at the same horrible levels as in Q4, GDP would have grown by 2.6%, instead of 1.6%.

The stimulus-driven buying binge of goods in the US during the pandemic, the subsequent restocking of goods inventories, and the lack of foreign tourism in the US (considered “exports” as money from foreign sources is paid to US businesses) caused the trade deficit to totally blow out in 2022. It then recovered some, but is far worse than in 2019. And Q1 was a big set-back and a major drag on GDP:

Change in private inventories subtracted 0.35 percentage points from GDP growth. Increases in inventories count as a business investment. Inventories rose by 1.2% annualized in Q1 to $3.0 trillion. But this growth rate was slower than the growth rate in Q4 (+1.9%) and so the slower growth rate was a negative contribution to the GDP growth rate.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

With government running a deficit of 1.7 Trillion or about 7.5% of GDP. We can only generate a blip of < 2% on the GDP gain.

Something tells me that the economy is not really efficient right now.

Actually, the dip (-0.2%) in federal government consumption expenditures and investment in Q1 was in part responsible for the slower GDP growth 🤣

I think that’s his point. If we have to keep up such huge deficits to keep up GDP growth, then a more balanced budget means recession, which implies bigger structural issues.

Well federal government spending dipped 0.2% in Q1, and there’s no recession, but 1.6% growth (and despite the surge in imports). 1.6% growth is pretty good for the US. Long-run average is just under 2%.

I agree with you. A balanced federal budget means almost less than $2 trillion in GDP, and then there is the multiplier effect as that reduced govt spending results in less personal consumption as those people and businesses receiving that govt money have less money to spend also. Here’s a recent article which echoes some of what I’ve been crying about for about 20 years now, lol.

My favorite part of the Richter-verse is reading an article, and thinking that I understand the core message. Then scrolling down to the comments and watching our host explain exactly what he meant in increasingly stern versions of RTGDFA (below).

Now we just need to keep our eyes on the mainstream business media for Jamie Dimon cautioning investors not to read too much into the Q1 GDP nums due to the dip in government consumption…

We know you’re here JD, show yourself!!!

Then you picked a good screen name for sure.

Makes me wonder how often that is done. Wolf knows.

This is my only social media, but not knowing the players has always seemed pretty detrimental to me…..but the basic rule is it is NOT my website, and I know very few things about social media that have any redeeming qualities, or so I hear/read. I just want to know as much as I can about how we got here and where we MIGHT BE able to go in the future from the Econ viewpoint. Which to me is nothing more than how things are divvied up, and the basis (very plural) for it.

Although maybe it’s “fairer” to base it on wealth than skin color?….as long as they will play the national game? Does the planet have rights like humans do?

Rhetorical…of course it doesn’t, and it shows.

Wolf, Interesting stuff thank you. The GDP is made up of both consumption expenditure and investment expenditure. Is there ever a break down of the ratio of consumption to investment spending? The distinction between the 2 forms would be interesting? Are transfer payments such as stimmie checks and welfare payments regarded as investment or consumption? Invest in the health, welfare and happiness of the voter who will vote for you again, Not happening in Argentina where the voter has voted in a president who has promised to cut government spending to what the country can afford

1. Private investments are broken out separately in the article, and you see it. I didn’t break out public investment. It’s included in the government spending measures.

2. “Are transfer payments such as stimmie checks and welfare payments regarded as investment or consumption?”

Neither. They’re not counted in GDP per se. They’re counted when consumers spend this money, not when consumers get this money. I explained this in the article.

Federal government spending on goods and services was down, but does not include transfer payments. The deficit does include transfer payments. Those transfer payments drive GDP and inflation when spent.

I think Zards comment has some merit.

It has zero merit in a discussion of Q1 GDP. And that’s what this is here is, Q1 GDP. And that’s what “Zard” referred to, without having read the article.

He didn’t RTGDFA, he just wanted to post the first comment without reading anything.

DEI is ruining the efficiency of the economy which is inflationary. You need to call a spade a spade.

There is a Keynesian calculation that is the root of why the GDP measurement is so important. That is the equation

GDP = Personal Consumption Expenditure + Government Exp + Exports – Imports

By simple examination one would observe that a trade deficit of 7.5 pct of the American GDP will require US Government Deficit Spending equal to the trade deficit to prevent the GDP from being negative.

Three quarters of negative GDP is normally assigned as a recession.

“… spent very vigorously on services at the fastest growth rate since 2021, adjusted for inflation, but not so vigorously on goods.”

It seems as if people have to cut their budgets on goods in order to spend on services, which why the former is falling while the latter is rising. If both were rising perhaps it would indicate consumers are flush with money.

Some anecdotal evidence:

– Daycare or homecare (for the elderly) can wipe out a family’s savings. Some friends were faced with this situation last month and were very stressed on how to cover homecare costs for an elder patient.

– Replacing shocks or timing belt on a car can set you back between 800-1800 dollars, and when you look at the bill, it is mostly labor.

– A typical kitchen or bathroom remodel can cost 20,000-45,000 and is mostly in labor.

No sure if Powell can cut rates to even in September, and he may have to even raise them. He made a huge mistake in promising rate cuts late last year.

“…people have to cut their budgets on goods in order to spend on services,”

Spending on durable goods went through a HUGE bubble during the pandemic, which we documented here at great length. It’s coming off that bubble. People have all this stuff, what else would they need in terms of durable goods? How many sets of patio furniture are you going to buy? That has been going on for over a year.

That patio furniture — made in china — is now 3-4 years old, rusted, well past its first half life, ready to be replaced….

So then there should soon be a second wave when all this stuff that they bought in 2020-2022 wears out, rusts, becomes unfashionable, etc. This is the cycle with electronics for sure. But with cars, the cycle is much longer. Living room furniture, armoires, buffets, good dining room sets, etc. can last 10, 20, 30 years. A little rust on the patio furniture just gives it that right kind of homey patina.

Spray paint isn’t just for huffing, like glue.

Rustoleum used to be best…..pay the kid next door if you ignored exercise and diet all your life.

Diagnosis: Too much money, and lack of “American ingenuity”.

Who needs a “patio” anyway? (For proving mandatory macho BBQ skills like a real caveman, I guess.

Paul Krugman – My spending is your income. Your spending is my income. If both of us decide we need to cut back because times are tough, the end result is we actually end up reducing both of our incomes, we end up make ourselves worse off. That’s how depressions happen is because the economy adds up.

————

The FED wants us to spend money? I keep reading about the wealth that has been generated over the past 5 or 6 years. Should we be surprised at the spending of the drunken sailors?

The Federal Reserve provides data on the average wealth of households by age of the household head through the fourth quarter of 2023. New CAP analysis of that data shows that the average inflation-adjusted wealth of households where the household head was under 40 grew $85,000, or 49 percent, between Q4 2019 and Q4 2023—from $174,000 to $259,000. As a point of comparison, the average for households of all ages was $1.1 million per household. Average inflation-adjusted wealth fell 7 percent for households ages 40 to 54; rose 4 percent for households ages 55 to 69; and increased by 15 percent among households 70 and older over the same period.

…confirming my status as a lifelong underperformer…

may we all find a better day

Yeah, me too. Another loser.

Should seen the writing on the wall when I was expelled from kindergarten.

Today I’d just be put on speed and wind up as bonkers as my midwest relatives.

Totally interesting, assuming that is an actual expose by Krugman using his celebrity to convince the economic losers too accept their fate.

Just saw a us census report for 2021 saying median household wealth was $166,900. Can’t find median household size but average given as 2.6.

Good catch and point. It appears the report I read used averages while you are looking at median. Averages will be higher because of the top 1% wealth holders.

The more I look into the report, which was from the Center of Progressive Action. Not to be political, but this is probably a democratic leaning non profit group that is trying to paint a rosy picture for the current administration? Specifically if one does not understand the difference between median and average?

I just thought the numbers were interesting in the original post.

Damn we need more “parties” and no Senate. Maybe after Comprehensive Green New Deal gets going strong?

Seeing these charts makes me feel like the focus is all in the wrong place. So real gdp is up 50% or so over the past 20 years. Is quality of life any different? It doesn’t really feel like it, and certainly not 50% better.

Conversely, if everybody is happier, why should we give a damn if gdp falls? Does everybody simply working more increase real gdp (because it’s hard to argue that’s a good thing) or would that all come out in the wash with higher inflation?

More on topic, maybe this is the first step to that recession most commentators have been expecting for years.

Because salary has not been raised fast enough to catch up with inflation. Companies are doing great in inflation environment when they have pricing power.

GDP is a lot easier to measure than happiness or quality of life.

Russia’s GDP is markedly up (temporarily) because of a poorly thought out war that has killed at least 10’s of thousands of its citizens, seriously wounded hundreds of thousands, and notably weakened it vis a vis the fastest growing economy on earth, its neighbor…China.

Does that really seem like a “win”?

GDP just measures “activity” at a point in time (at best, and with large margins for error).

GDP really says nothing about whether or not that “activity” is productive or counter-productive in the longer term (Keynesian hole-digging) or net accretive across time (Krugman’s Alien Invasion Pearl Harbor).

Sometimes it *is* better to do nothing (and *think* things over during “idleness”) than to do something stupid just for the sake of “doing” something (“bridges to nowhere”).

“GDP really says nothing about whether or not that “activity” is productive or counter-productive in the longer term”

Wait a minute… Who gets to decide what economic activity is “productive or counter-productive in the longer term”? You? What if you decided that my economic activity is “counterproductive?” And to make the economy more “productive,” you shut down my “counterproductive” economic activity and send me to a labor camp to crush rocks with a big hammer to make gravel, which is a productive activity in your view. Do you want to live in an economy where someone gets to decide what is “productive or counter-productive in the longer term.”

Not wanting to make those kinds of philosophical decisions is precisely why we measure an economy by spending/investing (GDP) or by income (GNI).

To answer rhetorical (I hope) question:

Presently, such things are decided by whoever has the most money.

But the military doesn’t need the “businessmen” nearly as much as it did before the Bronze Age Collapse, my sources say.

And that thing made the Great Depression look like a bad quarter.

“I hope” means that is exactly Uncle Milty’s reasoning for having a totally free market and a “supply side” economic policy.

Which we got in spades in1980 and have been going downhill ever since.

The 50% increased real GDP is distributed over a roughly 10% larger population, and there’s been an increasing disparity in incomes, so the average person’s “personal GDP” hasn’t grown 50%.

Also, above the poverty line, one’s quality of life doesn’t increase that rapidly with income, so 10% more income doesn’t really mean “10% better life”. Not enough people think that through, but I think the best use of an extra 10% is to properly save for retirement, emergency medical emergencies, a better education for kids and grandkids…

In terms of your last paragraph: Nah, read what I said about government spending, imports, and inventories, which are responsible for the slower growth in Q1. Consumer is doing fine. Investment is doing fine. And the negative reading of federal government spending was a blip, as we all know.

I agree.

My younger friends are spending a lot and they all are renters.

They have given up owning a home and thus no pressure to save money for down-payment.

This opens up their wallets for other things.

I see something similar with friends 35 or so and under in the large overly priced metro I live in. None of them were adults during the last recession. All they’ve ever known is a good economy with plentiful jobs. All college educated and have decent jobs but spending like crazy. Their definition of “need” makes me a laugh. Most don’t save and are at the limits of their budgets but lots of vacations, nice clothes, nice cars. I often hear comments like the stock market only goes up (long term yes this is true), the housing is going to go up 40% every 2 years, and the expectation of 10%+ annual raises being the norm. I make significantly more than these people and I cannot image living this way.

I am curious. Why are they giving up on owning a home? I think there is a trend to not have to deal with the hassles of home ownership. I have some young friends who sold their home to rent a home. They just don’t like fixing things.

Sure, as Wolf has pointed out, existing homes are over priced in relation to new homes. People complain about the high price of existing homes, sellers are greedy, bidding wars, etc.

Why not just go to a home builder and have them build a new home and one will pay market price, no bidding wars, and it is not overinflated because of low inventory premium that existing home prices carry?

ru82,

“Why not just go to a home builder and have them build a new home”

That is not a bad solution…if done right…and our current institutional set up makes it hard to do right.

IDK the stats on one-off SFH construction but I’d have to guess they are very small in percent terms relative to subdivision developers.

1) Developers learn a ton from earlier mistakes – self developers can’t really and can’t spread risk near anywhere as well.

2) Construction loans then takeout loans are more complicated and fraught than vanilla mortgages.

3) Institutional support is much, much lower for self-builds. There are some books, some builders, some lenders to facilitate the process but nowhere near the army that supports the vanilla process.

4) Even cost data and material take off lists are much harder to come by for the one-off builder.

Fairly amazingly, even well thought of charities like Habitat for Humanity – which must have this data and could very easily share it – really basically, don’t. Data sharing would help many, many, many more people but H4H seems to have evolved into something much more performative and really corpo-adjacent (tons and tons of corporate “partnerships” with fewer and fewer actual houses built).

5) DIY SFH homebuilding can definitely save money by cutting out the shameless, gouging middlemen. But it is very, very, very easy for things to go off the rails for newbies. And when they do, things get very expensive very fast.

I assert that the quality of life is the commodity that has been commercialized, leaving a shadow of the empathic community that invented it.

A VERY good comment.

Quote worthy.

May steal outright or attempt fine tune/play with it.

Loving this new normal and these drunken sailors which under the new norm should better known as regular sailors.

Good luck to that 2% inflation target, rate cuts or lower home prices in hot areas anytime soon with these kind of strong consumer spending as the standard…

My opinion is that the best remedy for the chaos that has engulfed us is love.

An irrational emotion capable of forgiving the most detestable crime.

Aren’t sailors mostly at sea, and Amazon doesn’t deliver on the high seas yet, so why concentrate on them as being spendthrifts?

Argh matey….If you were in the navy 50 yrs ago docked in the Philippines for 8 months you would understand.

See that chart? The drunken sailors chart? It’s quite impressive.

Subic Bay….Sin City. Heard it made Can Tho look like a nunnery.

And very little risk.

In the US at least, it’s a commonly understood idiom that is appropriate for the context in which it is being used here.

Shore leave.

Even drunken sailors need a break… spend enough time at sea and you’ll still feel the boat rocking even when you’re on land.

Amazon does…I was on a sailboat recently off the Caribbean coast of Panama in the San Blas Islands….Amazon definitely delivers to the boats out there that all now have StarLink. Apparently it’s Miami distribution center to Panama city and truck to the pier and onto a boat driven by local tribal members (Kuna Yala people) to the boats.

Most of the US sailors I have come in contact with were in conflict with the civilian world as they transitioned from the military with a pension that was inadequate too finance the lifestyle they had envisioned.

The rude awakening.

This was an ugly report today and the inflation numbers are saying stagflation is possible. Not a given but I cannot see any way the Fed cuts this year imo.

RTGDFA. Federal government in Q1 was NEGATIVE growth (-0.2%). That’s what pulled down GDP. Imports were a drag, and inventories were a drag. Consumer is doing fine. Investment is doing great. And the negative reading of federal government spending was a blip, as we all know.

Welcome to stagflation. Take out all the government deficits and spending and the GDP would be negative 3% to 5%. ENJOY.

I was a kid in the 1970s, so I have no memories from that period but I understand it was ugly economically. What can I expect?

Worms, that’s about it.

If you have little you will have less because of the worms eating away at your profits.

What to do?…. Go fishing.

Seems a little different this time. In the later 70’s low level manufacturing took it on the nose through mass layoffs. it seems like this time around it is middle management and white collar taking it on the nose. Bought my house in 1977 with a rate of 9%. Is that where the mortgage interest rates need to go for next recession, who knows. Today’s rates seem to me to be more the norm than what they have been over the last 20 years.

Swamp Creature,

RTGDFA. Federal government in Q1 was NEGATIVE growth (-0.2%). That’s what pulled down GDP. Imports were a drag, and inventories were a drag. Consumer is doing fine. Investment is doing great. And the negative reading of federal government spending was a blip, as we all know.

Hi Wolf, I really don’t get what you’re trying to say here. If consumers are doing well and the cause of the reduced GDP growth was a blip, surely the demand from the strong consumers will tend to be inflationary?

“surely the demand from the strong consumers will tend to be inflationary”

Sure, yes, and it was, see article. Or at least read the subtitle.

Also note: consumer spending on services grew a hot 4.0% (adjusted for inflation), and it’s in services where inflation is hot.

As in my earlier comment, deficits include transfer payments which then drive spending.

Wait a minute about that “deficit.” The biggest part of transfer payments are SS and disability payments, and they have their own revenues from payroll taxes. They have run surpluses for years, have a big accumulated surplus in their trust funds, and don’t contribute to the deficit. If they have a deficit, it comes out of the trust fund.

So they collect the funds from labor (which reduced spending power) and then they pay out the funds (which increases spending power), which is roughly a wash over time.

Government provides freeways, all kinds of infrastructure (water, etc.), education (versus robbing liquor stores for a living) and originated commercial air travel, the Internet, the microchip. It supports a remarkable medical infrastructure where I live. Take them all away, sure. Then we are living in a different world.

Oh yeah let’s applaude the government…

Infrastructure literally falling apart all over the country

Education? Lol higher education system that doesn’t produce workers. Primary education system that’s only for poor people

Air travel… Again literally falling apart

The Internet.. That was fun for a couple decades until it gotten taken over by big tech and has now destroyed the countries mental health

Chips-hopefully ai robots can save us!!

Medical infrastructure-by infrastructure are you referring to the systemic vampire medical system we have to first get you sick then keep you alive long enough to take all your money

While accomplishing all these feats they’ve also managed to stuff there own pockets with billions of dollars year after year… yes you go government lol

I agree with swamp tho that this report screamed stagflation. The consumer is strong like wolf mentions but it’s a fake economy.

This “stagflation” stuff is ZH bullshit. RTGDFA

Plus for extra credit: 1.6% growth for the US is not bad. Long-run average in the years before the pandemic was just under 2%. The times of 4% growth are long gone. This is a mature economy. 4% = OVERHEATING

I lived through the stagflation of the 1970s. I was able to buy a house back then. We had a civil society. People generally respected each other. We didn’t have 3 wars going on that we didn’t need to be involved in. We didn’t have a 35 trillion national deficit with more interest payments than the entire defense budget. We didn’t have a 1.2 Trillion annual Federal deficit with no end in sight. I’ll take the 1970s stagflation over this current bull s$it any day.

via MSN: Reports show the U.S. National Debt increases by $1 Trillion every 100 Days.

So we throw a trillion dollars at the economy every 100 days and congratulate ourselves on 1.6% growth?

Does any of that money contribute to growth?

The first microprocessor the 4000. was developed by a 3 year old startup, Intel in 71. The govt had zero role in that or the use of them in the computers we are all using, the microcomputer, so called because the CPU is a single chip. The first such computers were sold as kits to hobby nerds. All instructions had to be entered as a 1 or a 0, the only inputs the chip ‘understood’ then or now. The kit company issued a requirement for a translator program that would convert our language into chip language. When Gates and crew arrived to present their version. the secretary thought they were the kids of the engineers.

When 2 + 2 was entered on the key board and ‘4’ appeared on the screen, the execs around the board all smiled. No one had seen it do anything before.

Commercial air travel? The only US govt contracts for

aviation in the post WW1 era were for mail. Travel by air was private, expensive and dangerous.

The early attitude of govts to aviation was more like brutal disinterest until the military aps became too obvious to ignore. Although they tried. The US navy’s reaction to Billy Mitchell sinking old battleships at anchor as proof of air bombing was to fire Mitchell.

Not that govt isn’t essential and does good things, like highways. But they usually only get behind innovation once it’s working. A big exception I guess is the universities.

Ugh. You really need to acquaint yourself with Mazzucato’s work.

This post is a total joke. Semiconductors were a total gummint project, and significant early development was explicitly driven by defence contracts. Plus NASA, plus plus plus. The hobby side was a total side effect for essentially surplus chips.

Ballistic missiles, fancy aircraft, high tech radar for the time. All coming from chip development. The PC was an afterthought from big gov and big iron. Even the internet was spawned from arpanet, etc.

Maybe I am just slow this morning, but .gov spent 3.9 trillion, and that had a negative effect on GDP? How does that work?

What would happen if .gov spent a lot less, or nothing at all?

But in Q1 GDP, FEDERAL GOVERNMENT SPENDING FELL from prior quarter (-0.2%), and so it pushed down GDP growth. This is what this article is about, and Swamp Creature just didn’t read it, and you didn’t either. He made a comment about Q1 GDP without having read the article and without knowing that federal government spending FELL in Q1 GDP.

Exactly. A trade deficit requires a government budget deficit to keep the domestic economy from being a sick stagflation that will ultimately be diagnosed as a recession.

This is an excellent and timely presentation of the drivers of GDP, a hundred times better than any analysis one will find in the WSJ. This is why I gladly chip in a small amount to the beer money pot that helps support Wolf Street. One thing that might add clarity to understanding the Consumer Spending component, would be a chart showing the total government transfer payments (social security, etc), with the understanding that there is a lag between when the transfer occurs and when the money is spent. Another component of consumer spending, which is not readily discernible from the data, is the impact of higher interest payments on the amount of spending. Thanks Wolf and team.

When I report on consumer spending monthly, I separate the two income forms, income without transfer payments and total income with transfer payments. We’ll get March consumer spending tomorrow, so hang tight. Transfer payments are not that big.

Our “Drunken Sailors” are the crew on the super country ship of fools led by a captain and crew of drunks and addicts spending and spending and more spending.

Our “unsinkable” ship will ultimately hit a big iceberg and then who knows how many lifeboats will save the passengers.

I’m not optimistic.

Cheers,

Brewski

Hard to right the ship when the captain is hammered.

In the 80’s the “drunken sailors” were the actual sailors that spent like crazy at San Diego shops (and tattoo parlors and strip clubs) when they came home to six months of direct deposits filling their bank accounts while they were at sea. The new “drunken sailors” are millennials (along with a lower percentage of GenXers and Boomers) who say “as long as someone will finance it I can afford it”. On the low end it is the people going to the “buy here pay here car lots” or putting concert tickets on credit cards and on the high end it is the huge number of people that live around me on the SF Peninsula that currently owe more than a million more than they originally paid for their homes and keep buying new $100K+ cars and trucks. P.S. I bought a single pair of jeans (for ~$50) last week on Amazon and they offered me a “six-month payment plan”…

I chuckle whenever I see automated financing offers for small dollar purchases.

Even 0% financing isn’t techniclly free… you’re missing out on the 2% or whatever cashback you could have gotten by just throwing it on a credit card.

What fantasy world are you living in? The Millennials make more money than they know what to do with! My own Millennials are all homeowners – some of them with multiple homes – and they spend money like there is no tomorrow! Financing Amazon purchases? Gimme a break. What nonsense.

I disagree with your reason for the ship of fools as addicts and drunks and submit that the reason has more too do with the entitled than the helpless.

Looks like PCE will be another hot print tomorrow…

Most goods and services I deal with day to day are growing worse in quality.

Basic commodities, gasoline, electricity, heating, water and sewer are becoming more expensive.

My biggest expense remains taxes of all kinds (property taxes +10% per year), followed by insurance of all kinds.

My biggest increase of income has been the 4%+ that I enjoy in online-bank HYS accounts and in treasury direct investments in 8 week TBills.

Perhaps the economy is doing great. But watching my kids (late 20’s early 30’s) all basically treading water – makes me skeptical. For my kids, the best thing they could do would be to get off social media and read more Bible, science, history, economics, philosophy as long as they read stuff written before 1995 or so

Hi DanF,

Very much concur with your assessment of written material post mid-1990s. “Political Correctness” anyone?

–Geezer

Is this written by a bot?

A serious question.

“and read more Bible, science”

Best humor of the day…

OutWest – check (probably should be considered (in its various forms) in its effect on the historical context, though-the recent Constitutional questions of declaration of a pre-US independence British edition as a ‘Tennessee State Book’ (not the only one) by its legislature comes to mind…).

To paraphrase R.A. Heinlein: “…one man’s religion is another’s belly laugh. Like dandruff, though constantly fiddled and fussed with, it will always be with us…”.

may we all find a better day.

Do you spend all your time telling your children (who are adults) what they should read? Maybe if you treated them like the adults they are, they would not be treading water? Just saying.

Escierto – ah, fair Eve’s great sin in tasting that apple…

may we all find a better day.

Reminds me of my high school years. Planning whether I would be selected to represent my country as a soldier in Vietnam in the upcoming selective service lottery.

“spent very vigorously on services at the fastest growth rate since 2021, adjusted for inflation, but not so vigorously on goods”

Worst thing you can do in an inflationary environment unless the services are in self-improvement and real education not “experiences” and “indoctrination”.

I spend on raw goods I can add value to for potential sale as finished product, if needed, and tools. It’s because I enjoy building and creating things now. Not my previous money maker before retirement, LOL.

It’s simply economodynamics. Get your self in a flow of money and eddy current some off. Ask Zelenski how.

I feel like the markets will brush off every concern by tomorrow morning and will go bull again like crazy. We are in a permanently distorted economy. Good news are bought with frenzy, bad news are forgotten quickly.

You guys bellow like ignorant pawns, unaware of the source of the money that makes it all possible.

It is the Federal Reserve bank that agrees with you that the synthetic asset prices are preferable too a loss of 65 pct that it is worth.

ehh, did Wolf just say bigly?

Sure’s heck sounds like it

I’ve now talked to over a dozen homeowners who refinanced their homes in the last few years. The average reduction in their payments is now just over 1000 dollars per month. I know Wolf doesn’t agree that this is a source of the drunken sailors financial engine but i think it is something to be considered. Expenses rise to meet net income. The spending is going to last for quite a long time. IMHO.

I refi’d my expensive house that I bought in 2017 to 2.5%. Sure, my payment is way less but all of that offset is eaten up by inflation and rising costs. My grocery bill and consumables take up any savings from my mortgage.

So no, I don’t agree that is the source of the financial engine. The actual financial engine is no one believing the fed will do what needs to be done so you might as well risk it all.

If there’s one lesson to be learned over the past couple decades, it’s that there’s safety in numbers. Stay in the majority. Don’t be a minority.

If everybody is drunk, join the party, because you’ll be helping to foot the bill in any case.

Your grocery bill? Who are you feeding? My grocery bill is hardly worth talking about and I deny myself nothing.

Interest payments come out of someone’s pocket, but they go into someone else’s.

Those who reduced their interest costs now have more to spend, but someone on the other side is now receiving less in interest, and will have less to spend.

Overall it should be a wash, but in Wolf’s context the question then becomes – which of the two is the less drunken sailor?

In theory interest payers are poorer than interest takers, so consumption ought to increase more and asset prices increase less. But theory and empirical evidence may or may not agree …

Apple pays interest on $110 billion in debt. It’s not exactly “poor.” There are all kinds of reasons to borrow.

The poor cannot borrow, or cannot borrow much. The richer you are, the more you can borrow.

I’d also add that borrowing for the purpose of investment is significantly different than personal borrowing. Borrowing for investment magnifies whatever return you are getting. So if you are borrowing to invest, which many do, be it for a business, or stocks, or even crypto, and you make money, you need to make more than your interest rate and then calculate how much. If you loose money, then you will loose that much more on your borrowed money when you do the calculation to include your interest payment. Higher interest rates in theory, should reward smart investments and penalize marginal or poor investments over time. Consumer borrowing is of course, a completely different animal.

1st qtr. total reserves and means-of-payment money up.

2nd qtr. total deposits, bank credit, large CDs down.

Looks like we’ve hit an inflection point.

Howdy Youngins. Don t forget about the sober sailors. ZIRP is dead and some of US will continue spending more till death. Its what we worked for and saved for and already lived through high inflation and double digit interest rates before. Fun times for some………….

“Adjusted for this re-accelerating inflation, Drunken Sailors still, despite 5.5% Fed interest rates:”

Wolf, I feel ‘splurged’ would be an appropriate addition right before the 2nd comma in this sentence.

This is a pointer at the chart. It’s a well-thought-out purposeful sentence fragment (MA in Modern Lit, 1981). So read it and look at the chart.

If anything, I might insert a comma between Sailors and still.

Federal government spending should be cut across the board by at least 20% and then many programs should be totally eliminated.

The Federal Government just gave the Ukraine and Israel 100 billion in US dollars to spend. Across the board spending cuts would not even touch the deficit problem.

It would only affect the normal citizens in favor of the wealthy tax payers who are ….

Import of goods up almost 7%

Consumer spending on goods a little bit lower.

Next quarters goods import must go down, or warehouses will be full of stuff.

Warehouses & lots.

Few yrs out from retirement. Small digger wont get me to the finish line.

Usually buy used. Checked out new. 3 different manufactures….2 are offering 0% for 48 months, 1 is @ 0% for 72 months.

If that happens, it will push GDP growth up.

Seems to me that everything is doing quite well and interest rates and quantitative tightening are perfect just as they are. The machine is humming along.

Maybe that’s what Powell needs to say next – things are going well with rates and QT and as far as he can see there won’t be any changes on the horizon. Why not? We can all live with roughly 5% ten years and 7% mortgages.