Four decades of history say it’s not over until the 2-year yield overshoots the EFFR. It has undershot for a year, and inflation is taking off again.

By Wolf Richter for WOLF STREET.

Inflation surprised in 2023 with its sharp decline, driven by the collapse in energy prices and the drop in durable goods prices. Both of them have come off huge price spikes since mid-2022, pulling down overall CPI inflation from 9.0% in June 2022 to 3.1% in January 2024. But services inflation has remained high and accelerated in late 2023, which was not surprising, and then on top of this increase, it leaped in January by an annualized rate of 8.2%.

The Producer Price Index (PPI), which shows inflationary pressures deeper in the economic machinery, dished up another nasty surprise, with the Services PPI leaping by 7.1% annualized, and with the Finished Goods PPI jumping by 4% annualized in January.

The PCE price index for January hasn’t been released yet, but December’s PCE price index for core services accelerated to 4.0% annualized. So given the surge in the CPI for core services in January, we expect another nasty surprise, so to speak, in the core PCE price index for services.

Energy prices cannot plunge forever. Crude oil prices and gasoline have been rising recently; WTI is back to nearly $80. And durable goods prices cannot drop forever either, though they can drop for a while longer, given how high they’d spiked. If energy and durable goods prices just stall, overall inflation will accelerate faster because those two big categories are then no longer a counterweight to services. If energy prices and durable goods prices begin to rise again, then all bets are off.

So now we’re contemplating a scenario where inflation is accelerating again. When we look back at 2023 in a few months, we may see that it was another head fake, for which inflation is infamous.

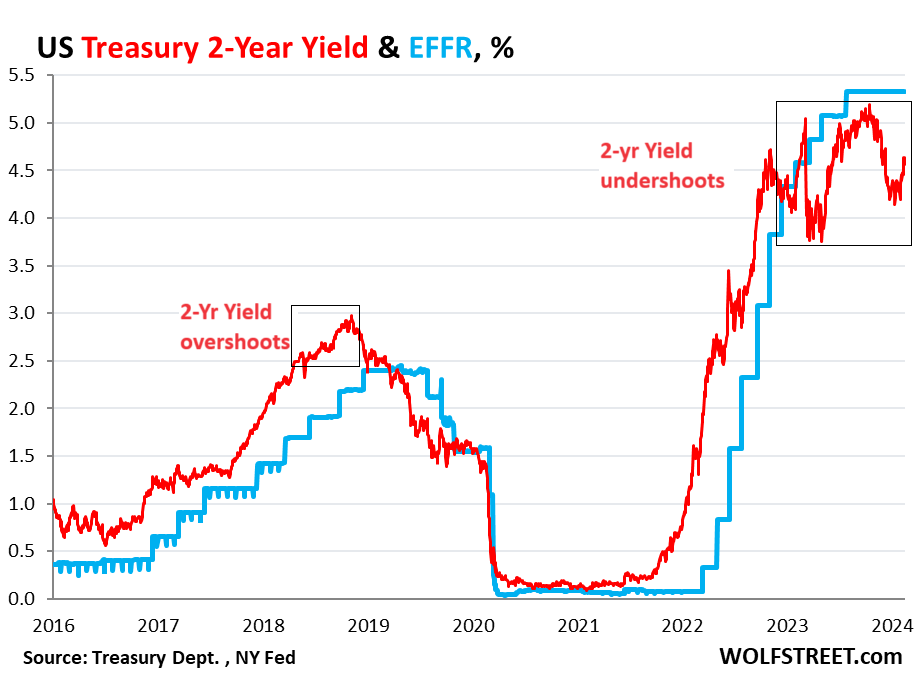

And we have an indicator that this may be the case – the 2-year Treasury yield compared to the Effective Federal Funds Rate (the EFFR is the rate the Fed brackets with its headline policy rate currently between 5.25% and 5.5%).

The 2-year yield hasn’t overshot yet.

The 2-year yield generally rises before the Fed starts hiking rates. It does so in anticipation because the Fed communicates the rate hikes well in advance, and markets, if they’re not in denial, are beginning to price in those rate hikes ahead of the rate hikes. The 2-year yield reacts first.

During the current tightening cycle, the 2-year yield started rising in October 2021, about five months before the first rate hike. And then it stays ahead of the rate hikes. It has done that for decades. And since it runs ahead of the rate hikes, when the Fed stops hiking, the 2-year yield overshoots between a little and a lot. It has overshot during every rate hike cycle over the past four decades – except in this rate-hike cycle.

But in this cycle, the 2-year yield undershot. In November 2022, the 2-year yield went into denial and started dropping, even as the Fed would hike four more times. By December 2022, when the Fed hiked, the 2-year yield (red) fell below the EFFR (blue) and it has stayed below the EFFR ever since.

During the 2018 rate hikes, the 2-year yield overshot to 3%, behaving in the classic manner. The Fed hiked a final time in December, and the EFFR maxed out at around 2.4%. The 2-year yield had overshot by 60 basis points, and that did the trick:

Obviously, the 2-year yield is not some ghost that does what it wants; it’s an index that tracks the market for Treasury securities, which is a huge global market where humans and algos trade and bet. And the classic overshoot of the 2-year yield with regards to the EFFR was a sign that these humans and algos took the Fed seriously, and didn’t blow it off, and didn’t go into denial.

The fact that the 2-year yield undershot since December 2022 is a sign that these humans and algos have blown off the Fed, have not taken it seriously, and have been in denial about inflation and rate hikes.

This shows up in a stunning loosening of the financial conditions, with spreads narrowing for risky debt and with longer-term yields falling, and these loosening financial conditions are part of the fuel that is now driving inflation higher.

In the past, it wasn’t over until the Fat Lady sang.

By tightening its monetary policy, the Fed attempts to tighten financial conditions in the markets, and tighter financial conditions make it harder for companies and consumers to borrow, which is supposed to produce a small-ish slowdown in demand, which is supposed to whittle away at the pricing power of businesses, and make consumers more careful about spending money, and slowly, this is supposed to get inflation back into the bottle.

But financial conditions have dramatically loosened in 2023, and inflation is now taking off again.

And the undershoot of the 2-year yield seems to tell us that higher-for-longer inflation and rates won’t be over until the Fat Lady sings, and the Fat Lady is the 2-year yield, and it sings when it overshoots the EFFR.

And if it overshoots the EFFR it’s because markets and humans take the Fed seriously, and therefore financial conditions tighten and play their magic on demand. But it didn’t happen this time.

So now we have the suspicion that inflation won’t actually go back into the bottle until after the 2-year yield overshoots the EFFR, and the Fed may have to hike rates further because the financial conditions have loosened so much, as markets have blown off the Fed, and inflation is taking off again.

There is another factor here that is fueling inflation: the huge and reckless government deficit spending, where fiscal policy is running effectively against the Fed’s monetary policy, which is making the enterprise of getting inflation back into the bottle even more difficult.

The prior instances when the Fat Lady sang.

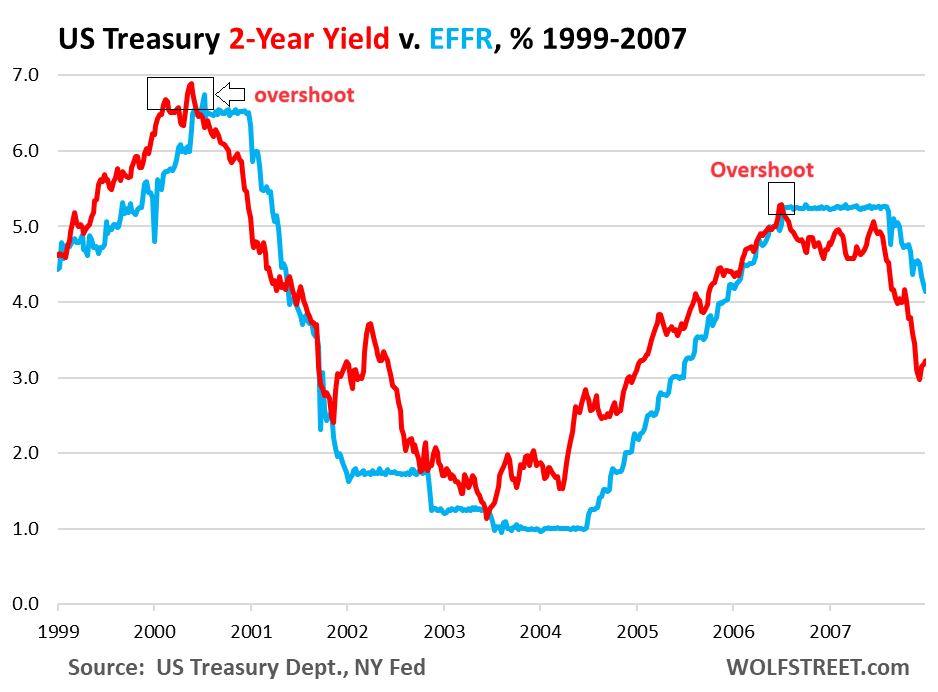

We have already seen the overshoot of the 2018 rate hikes in the chart above. So here are the prior two rate hike cycles in the late 1990s and 2005-2006. In both instances, the 2-year yield overshot the EFFR:

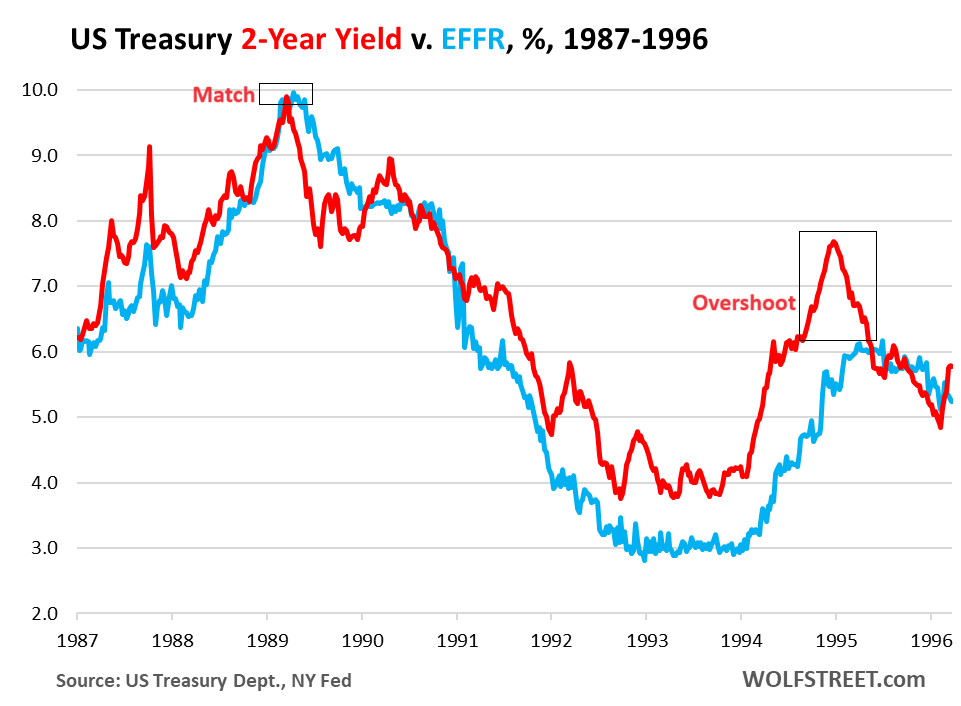

And here are the 1987-1989 rate hikes and the 1994 rate hikes. In 1994, the 2-year yield overshot by a huge margin (180 basis points), meaning that the markets took inflation and the Fed very seriously. In 1987, the 2-year yield overshot also bigly. But in 1989, at the peak of the rate-hike cycle, it matched the EFFR at 9.9%:

Do we hafta wait until the Fat Lady sings?

We’re not predicting the course of inflation. That’s a fool’s errand. But we know what is currently going on: Financial conditions have become loosey-goosey, which nurtures inflation. Government deficit spending is gigantic and also nurtures inflation. The demand by consumers and businesses is robust, and incomes started rising above the rate of CPI inflation in 2023. And there is just not a whole lot outside of the Fed’s short-term rates that is putting downward pressure on inflation.

We suspect that inflation and higher policy rates won’t be over until the Fat Lady sings. And this opera could last for a while as markets have been blowing off the Fed and are not doing what the Fed needs them to do: tighten financial conditions to bring down inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Causation or correlation? This seems quite tenuous.

While media seems surprised by sudden increase in inflation, this was always my plan. Why else would I stop raising rates and talk about cuts when core inflation is way above target.

How else can I take the stock markets and asset prices to all time highs. I know it sucks to not be in my billionaire club, but just because useful idiots keep whining, they don’t get less useful.

I first fooled them with “Inflation is transitory”, then with “Rates are high enough to defeat Inflation with soft landing”. Fool you twice, it’s your fault!

Dennis H.

Did you even read the article??? Just the headline, right?

The relationship of the 2-year yield to the EFFR is an “INDICATOR” — that’s what the article said. Not a “cause.” There is some discussion in the article as to what is fueling inflation now (loosey-goosey financial conditions, fiscal policy, etc.), and there is some discussion what the relationship of the 2-year yield to the EFFR shows, why it’s an “indicator,” and what it indicates.

This is a new information to me at least. I never noticed this pattern and I think it’s a good time for the Fed to stop parading out its members to speak every day. There should be just one voice from Powell and he had already said enough.

I love Wolf Richter – great work and please keep the articles coming!

The two year yield is irrelevant, the 30 has a higher yield than the 10 a bet that inflation will be institutionalized.

Howdy J Pow Gloating is a great tool box tool. Keep up the good work.

RTGDFA. He’s pointing out an indicator that has signaled top rates over the last 4 decades’ worth of tightening cycles. Nowhere in the piece does he even imply that this is guaranteed to happen again, let alone that there’s a casual relationship.

Exactly! It can be called experiential data, meaning we keep experiencing it over and over, so maybe we should pay close attention to it as Wolf has done.

This AM on CNBC from Cramer:

‘Face it: these rate hikes did little to slow this economy’

Now if Cramer of all people, tells you rates aren’t high enough…it’s kind of embarrassing for those who say the Fed should cut soon.

It’s funny watching the predictions of rate cuts slowly recede into the future. When will it strike the pundits that with services inflation at 8 % annum, there is more case for a hike than a cut?

Wouldn’t it be funny if Cramer said that? Would he be terminated?

What is funny is that people like you actually watch CNBC and listen to Cramer. The entire MSM is pure propaganda.

Cramer is an entertainer.

Cramer from the 90’s was awesome. Cramer in 2024 is just old and tired. I still love the guy tho.

He’s a gamer, went to H yard. Supahhh Hahhddd there

Cramer has mastered the ability to convince people that he has inside information about how the stock market really works. Never promising anything short of the respectability that comes from owning shares.

Kids don’t like CNBC? I’ll run gravel thru a sluice, altho over at the Zoo it’s getting hard to even find flakes. Of gold that is, lots of other flakes in the ‘over Burden’, lol.

How about this from CNBC re: the Mag 7

Jim Reid, Deutsche Bank’s head of global economics and thematic research, cautioned in a follow-up note last week that the U.S. stock market is “rivalling 2000 and 1929 in terms of being its most concentrated in history.”

You don’t hear the year of The Great Crash mentioned too often.

There is a fundamental transformation occurring that I view as a the mixing model of various ingredients rather than the view that the waters seek their way to the sea, regardless.

For what it’s worth, a propeller blade should be placed at one third off the bottom for optimum mixing.

Thanks for calling out the role of the deficit in causing inflation to persist. Everyone in the US seems to have forgotten about the role of fiscal policy.

The US is running a huge deficit, while unemployment is at a very low level. How high do interest rates have to be to counteract this, the answer so far seems to be, higher than they are now! Or at the very least, higher than people were expecting them to be by the end of 2024.

I totally agree with you. Good job to Wolf for spending so much time talking about how the politicians are undermining the inflation fight. It is not just the markets that are ignoring what the Fed is trying to do.

Or, and this is just a thought, we raise taxes to match the spending.

Wolf said it well, “There is another factor here that is fueling inflation: the huge and reckless government deficit spending, where fiscal policy is running effectively against the Fed’s monetary policy, which is making the enterprise of getting inflation back into the bottle even more difficult.”

In MacroEcon 101, this was called “The Fool in the Shower.” The water is too hot or cold, so the fool adjusts both the cold and hot water spigots each time, thereby overshooting or undershooting his/her mark.

Someone should teach that metaphor to US policy makers.

The goal of Congress as US policy makers is not to create policy that regulates anything but simply to create mostly false narratives and occasional policy that seeks to get them reelected.

@Glen, good summary of what happens in Washington DC.

Glen/AI – someone keeps sending Congresspeople to Congress (but subsequently fails in their PITA duty to always watch/hector them) the same way they continue to hire, and not vet, the stream of illegal immigrants.

(That someone is us).

may we all find a better day.

Dustoff, how’s it going, especially the family problems plus all the RAIN? Rough going off grid anywhere, but especially where you are. My record year was 76″ and I had a shovel in my hand most of the time.

Yeah, like Franklin said ….”if YOU can keep it”, and also Abe’s plea that that huge pile of dead bodies would wake people up to their much easier DUTYS………and it’s NOT just investing wisely.

NBay – always good to see your handle and thoughts, brother (I ‘m pretty sure I understand the weary feeling…)! (Hope Wolf might indulge us, here-) Been a rough year for casualties, a couple more down, one this week (and not even forty), but still hugging the dike, meself. Weather-wise this last go-round’s brought us to 67″ so far (96″ last season, hard to believe we had an alltime low of 27.5″ just four years ago), but the real issue has been high winds this winter and last-have to do some thoughtful house tuning when dry season returns…Best!

may we all find a better day.

We have 535 lobbyists for private interests, who salaries are paid by the American people, who placed their trust that the corporate lobbyist they were electing would have the decency to not kill my sacred cow.

That overshoot in the mid 90s looks pretty wild. I was just starting to invest a few years out of college then and reading books by John Bogle and Peter Lynch. I think bonds got hammered in the time, maybe something to do with the mexican currency crisis? I remember there was an Asian crisis and LTCM but it was all over my head at the time. Seemed like a crisis every other year or so back then. Good times!

Energy, especially gas prices have seemed odd to me this past year. It hasn’t gone below 5/gal where I live but I read about people in Texas and elsewhere paying half that. Even in California my brother was saying recently it was cheaper on the coast than in the SJ valley, something I can’t recall ever seeing and I lived there many years. And its not like its summer when the special blends are used. Utility bills seem to be more uniform in their increases, with everyone paying double digit increases.

Good morning Wolf; federal governments and central banks don’t seem to be pulling in the same direction.

I have to ask, do you believe the same trajectory (increasing yield from inflationary expectations) that has effected the US 2 year bond also applies to Canada’s 5 year bond in terms of overshooting and undershooting?

With meager gdp and employment growth in the face of record setting population growth (January set a monthly record – 126,000 I believe) – the BOC has to be under increasing pressure to start dropping interest rates. I respect that the BOC isn’t trying to choke our economy into unconsciousness, but feeling like we have to move rates lower in order for an increasing portion of the growing population not to be poverty stricken while faced against a potential backlash of inflation coming back to bite us – you’d think we’d stay on the side of caution and wouldn’t get overly rambunctious to drop rates. Canada is soaked with unsustainable private debt levels with government debt looking shaky (federal government just 100% downloaded road/highway maintenance on to provinces and municipalities).

Correction: not road maintenance- the expansion of existing roads and construction of new roads will relieve 0 funding from the federal government. With the current level of population growth? They want increased population density in cities and towns… maybe they want provinces to further increase fuel taxes so they don’t look like the only bad guys (carbon tax).

Only one datapoint, but there’s been weirdness in the distribution of gas prices here in San Diego County as well. When they hit their nadir in January, for instance, local news ran a piece showing where the lowest prices in the county were: 9 of the 10 lowest were up in North County (e.g., Carlsbad, Oceanside), where prices on average were about 30-35 cents/gal cheaper. Needless to say, this is usually not the case.

Could be nothing or due to some local circumstance I’m not aware of. But it was unusual.

Interesting, I lived in Cardiff for a number of years. Maybe being outside the city of San Diego had something to do with it? City loves their taxes, plenty of bills to pay

Yep 2.39 in Texas last week back up above 2.60 this week. Fed government wanting to curtail permits for LNG exports which have been a big boost to our economy for a decade !

Export capacity is going to double in the next three years as new projects are completed.

This is to benefit coal and oil producers.

Any person railing against the availability of fossil fuel energy as a cause of global discontent may be on to something, especially when it is so cheap. Texas is Texas.

A geographic miracle, that had more than a passing role in establishing the American hubris.

I think bonds got hammered in the time, maybe something to do with the mexican currency crisis? I remem

Or

the value of bonds declines in correlation with the decline in market interest rate. Which the Fed drove to zero (ZIRP) hammering bonds to an absurd level. At one point, I think Italy was selling a 50 year bond paying a negative 0.2 pct interest rate.

NYg – my anecdotal observation of gas pricing in the Bay Area over the years seemed related to the daily amount of highway traffic I encountered (…still commuting to work back then in an admittedly-different time). When traffic fell noticably, fuel prices almost-magically declined, as well. Makes me wonder about current traffic levels over in the Valley-is it heavy (…again, anecdotal, but for my Sonoma County supposedly losing population, it’s current traffic is the worst I’ve ever seen since arriving here in the late ’70’s. Fuel, after the recent drop from the $5gal (reg) level to high $3’s, has appeared to edge back towards the $4.5 point…)?

may we all find a better day.

I remember former NY fed Dudley was saying two years ago that the Fed has to let the stock market fall in order to beat inflation. Wolf here is also saying the same thing: tightening financial conditions. But Powell seems to be on the side of Wall Street and doing all he can to prolong the asset bubble which is fueling inflation. When core goods price stops falling and core services continues rising , the Fed could be in a big dilemma- either let the market crash or face higher inflation.

I detest Powell and think he’s a spineless coward, but what has he done exactly to not “let the markets fall?”

There’s a lot of FOMO group hysteria right now in the markets

Being way too timid on raising rates, and ramping up QT, to put an end to inflation once and for all. He’s far too worried about upsetting markets to get the job done properly. So now all the poors have to suffer for years and years as it persists.

Is he afraid of upsetting the stock markets or causing the credit markets to seize up?

The two are related to a degree, but I don’t think you can blame the current melt up on Powell

The primary objective is price stability and the secondary objective is full employment but we already have full employment. At this time, Powell keeps talking about rate cut is just pandering to biden and the wall Street. No wonder Trump is hopping mad at this guy he appointed because he knew Powell is a pushover.

The financial media has been frontrunning the Fed and telegraphing what the Fed will do. And Powell is happy going along with it. If inflation data continues to run hot, Powell needs to actually do a rate hike to surprise the market in order to to tighten the financial condition. But that is not going to happen because we all know what kind of character he is.

I guess we’ll see if he does go along with it. He didn’t throughout 2023 when the media was telegraphing cuts in the first quarter.

Powell has not talked the 6 rate cuts the stock traders needed to predict at the end of 2023 to get their profits in by the end of the year. He talked nothing about cuts. Leisman trapped him with a question about discussion related to the cuts in the dot plot. And then the ‘sentiment’ sculptors created the 6 cut scenario with an 80% vote of probability. It was all a manufactured scam.

I admire Powell who at least has more than you, leaving you with your pain of failure, while he relaxes in his hot tub.

A spineless coward is an epitaph generally recognized when one is looking in the mirror.

This is very good analysis not seen from the usual Wall Street media.

This macro environment reminds me more of the 1970s and so was wondering whether the 2 year yield stayed below the effr for that decade, leading to higher and higher inflation?

“… the 2-year yield went into denial …”

Excellent imagery.

Inflation deniers will signal an eventual transitory shift to lower rates, then?

Speaking of denial… The Fed “dot plot” shows that members think, on average, that inflation will ease and thus they will be able to (at least somewhat) cut rates. Are the Fed members also in denial? Succoming to pressure? Giving too much weight to recent months? Or right?

Brian-

“Are the Fed members also in denial?”

– Undeniablly!

“Or right?”

– Unlikely, seems to me, but I’m undeniably biased…

reminds me of my relatives who arrived and were convinced that they would be able to tour Custer’s last stand, Yellowstone, and Glacier on Wednesday. With the spatial perspective of the distance from Dublin to the other side.

dang – 🤣 brilliant! (…but in the same instant, sadly, and depressingly, true of too-many of us. An average ‘murican’s ‘mental map’ of the world, let alone their own nation, stands in evidence…).

may we all find a better day.

I would think the enormous increase in the money supply in recent years has a lot to do with the continuing inflation. Until the ratio of money to goods & services somehow gets back in balance, inflation will continue.

Amen!

Loved seeing a story in the FT today (Feb 20) talking about causes of inflation, they wven linked to a paper by Bernanke. Not a word about the deluge of money and asset inflation caused by shameless rate manipulation for decades. These guys should swing from the yardarm.

Well I”ll be Wolf! This is a gem of an insight I would never have known. I’m figuring my yields going out farther without being called possibly. This inflation I’m thinking could go on for years. Thanks again,

The last inflationary cycle lasted decades from its first appearance until it finally cooled down. One of the things that happened then was that inflation would appear to be going down for a while, and then it would go back up. This caught the Fed off guard in those days too. I would expect this cycle to be not much different. Especially since everyone is so reckless about it.

Interesting. Seems that federal government and central banks are more allergic to lacking economic results then they’ve ever been. Maybe it’s just me or maybe times have changed.

I think governments and central banks want to spur economic growth obviously; definitely more eagerness to drop rates then there was to raise them. Does this mean that governments and central banks need to brush up on their acting skills if higher inflation rates come back after subsequent interest decreases due to not wanting to take the “higher for longer” route?

As to slow moving shifts in bond market sentiment:

“[M]en are ever prone to regard existing conditions as permanent.”

— Phillips, McMahon and Nelson, Banking and the Business Cycle (1937)

The Fed never allows a sharp downturn (which would correct this fallacy) to persist, anymore. The Fed put sits in the background of people’s thinking. And credit markets do not restrain government spending by charging an appropriate rate on funds. It is another put assumed to persist. So, the kindling continues to pile up. Everybody seems to be complacently bobbing along assuming a backdrop of these government puts forever.

“… credit markets do not restrain government spending by charging an appropriate rate on funds.”

The hypocrisy exhibited by various administrations (and supporting economic experts) in accusing China and other countries of “currency manipulation” is egregious and somewhat disgusting.

Hypocrisy yes, but also purposeful. Politicians have to do everything possible for people to not look at the system itself and the other political party or a foreign actor work. Clearly Americans are happier with the chosen targets of asking why the wealthiest and most powerful country have no basic needs guarantees and so much wealth inequality.

If they don’t eventually allow a sharp downturn, they’ll eventually have a crack up boom. There is no third option.

I think the Fed has decided they would rather fight inflation than unemployment.

They were spooked by Trump and Brexit, and decided they couldn’t allow another ‘Great Recession’ to occur.

I don’t agree that everybody agrees. I suspect that the few that actually agree are the fools that need to be convinced that the turds actually look and smell like strawberries.

Only price increases generated by demand, irrespective of changes in supply, provide evidence of inflation. There must be an increase in aggregate monetary purchasing power, AD, which can come about only as a consequence of an increase in the volume and/or transactions’ velocity of money.

I’m not an economics expert but I lived through the 80’s.

Bought my house in 1981 with a 14% mortgage and they went up over 17% soon after. Unemployment has to go higher to prevent wages from going higher. Mortgage rates have to go higher to slow housing sales. Many people have and spend too much money to spend so prices go up and no one cares.

I feel bad for the low income families that will never afford a home or send their kids to college. Just my opinion.

This is a great article and mimics what I’ve been thinking for a long time. I think Powell has made a mistake forecasting lower rates too soon.

Those low income families are the ones who will lose their jobs and face total ruin if rates rise higher and kill inflation via crushing demand. There is no easy answer.

Ehh I’m not convinced of that. It’s long been my opinion that much of the current inflation we’re seeing results from the top 10% spending their stock and housing “gains.”

Get rid of that, and I think things largely return to normal.

Exactly.

Joe, don’t confuse cause and effect.

All of the economists predicted a recession last year along with a lot of posters here. They are all wrong.

Turns out, economics is more of an art than a science

Art is making it up as you move along.

It’s an election year. The markets are betting the

Fed won’t want to raise rates and politicians will

increase the pork. Seems like a good bet. There were

those on this site complaining that Powell and the rest of the Fed were too timid . In hindsight it appears they were right to complain.

“The demand by consumers and businesses is robust, and incomes started rising above the rate of CPI inflation in 2023.”

Is the 65+ yr old boomer demographic “to blame” for this demand? Various sources the last 2-3 yrs describe record levels of aggregate wealth in savings and home ownership in a huge group of people who’ve got maybe 20 yrs of life left at best. Maybe these drunken sailors are the ones passed out at the bar..?

Where does this endless boomer-nonsense come from? Retirees overall spend less than these people spent when they were working. And the boomers are now a diminishing generation.

The biggest spenders now are GenZers and Millennials. The Millennials have entered the peak earnings years, and they’re a much larger generation than the boomers today, and they’re spending lots of money because they’ve started families, and they’re the dominant buyers of homes, and those homes need to be furnished, and they’re buying school supplies and cars and what not. And they have received massive pay increases.

Here is disposable income adjusted for inflation. It increased 4.3% FASTER in 2023 than inflation increased. In other words, disposable income outran CPI inflation by a wide margin, and that’s where that spending growth comes from.

And don’t forget us younger GenXers who are also in the rush hour of life and are now at our peak earning years in our mid-40s. We’re smaller but we’re out there hustling and spending and buying things for our young families too. “Xennials” I think is the term for us now.

“Xennials” is a great term for us, no GenXer ever said…

Which cohort is inheriting residue wealth from expiring Boomer generation?

I’d assume they are spending some of this newfound wealth, no?

Early boomers’ kids are younger GenXers and millennials. So that’s where it starts.

Absolutely right. I am a retired Boomer and I literally spend a quarter of my income. I don’t buy anything because I don’t need anything. My children are all Millennials and they spend like crazy. Of course all of them are far wealthier than I am but that’s a good thing.

Yes this is true, But I retired butwent back to work 15 years ago because I hated it. I still work at 70 + training young engineers and inspectors in heavy construction and they respect it. However. you look around your home and think to yourself, Soon I will need to downsize from this 5 bedroom triple garage and a Den/ study + pool on 50 Perches. The twice a week help now wants $35/ hour and I cannot deny it, as we can no longer clean or maintain properly, this family home. I have no Idea what some of the things I have collected 50 years ago are worth but I suspect considerable. My Children are zero help because of distance. I don’t need a thing except a youthful spring in my step, and that is not going to happen, even prescription free. I feel I am trapped by the things that I have but I can’t let go of them. This leads to that thing called Cognitive dissonance and I can’t but wonder, I am not alone ?.

This is a topic the Wolf should set his mind to, it is the passage of time and the real effects of life and aging and just letting Go of wealth and its collection on anchors.

Thunderdownunder,

Close friends of mine, a couple now 83 and 84, were in a similar situation. They didn’t downsize when they were 70. They just now downsized (last year). They sold their house and bought a 2-bedroom co-op in a high-rise with views. Downsizing included getting rid of all the treasures. For him, it meant to sell his book collection, including some books he considered “rare,” and he loved books, is a prolific self-published author, and many years ago used to have a bookstore. So he sold all the books to the big used-book dealer in the area, and the sales price was just in the three figures, and the guy sent out two young people with a box truck that picked up the books. It was a brief sad moment for him, but afterwards, after the downsizing was done, and after they’d settled into their 2-bedroom co-op, it was a huge sense of relief!

Getting rid of stuff you don’t need — such as useless possessions, expenses, space, and chores — is often a big relief! It allows you to focus on the stuff you like to do.

I agree with what you say here but I would add some nuance.

Healthcare is a place where boomers would be spending more than other generations, and healthcare (services and insurance) is one of the big causes for inflation this past month.

So, are prices in healthcare increasing because demand increased, or because the goods and services the Healthcare system needs just increased over the last 1-2 years?

I think you’re all largely correct, but, at least in my area (South Florida), the Boomers are disproportionately spending on luxuries and “toys,” like restaurants, fancy cars, boats, etc.

General spending is more concentrated among younger people who have families.

Does it mean that I have to get rid of my R Crumb 50 year-old home made posters?

We’re doomed, nobody has ever come back from here alive. Breathe some of these herbs, It’ll give you the strength of ten, but only for a few seconds.

Thank you. Yes, your data- the objective data- clearly shows that Millennials and beyond have edged into the driver’s seat of spenders, displacing Boomers and the aging Gen X.

There is a perception that at least the Ability to spend lavishly on occasion – not exercised too often- still is there for the boomers, and the older Gen X.

And at least recently, it appears that that ability played a role in high home prices for existing homes – though as you have pointed out, not for new construction homes.

This author likely agrees with your analyses, but describes how the ‘endless boomer’ perception arises. (I realize it’s an apples/oranges, macroeconomics/microeconomics comparison situation.)

I realize it’s an apples/oranges, macroeconomics/microeconomics comparison situation.

On the first chart, it looks like the 2-yr yield already overshot the EFFR in late 2022 and early 2023.

The 2-year yield normally runs ahead of the EFFR, and is normally higher than the EFFR during rate hikes and lower during rate cuts. That was the point of the article.

But in 2022-2023, it fell while the EFFR was still rising. In other words, the 2-year yield undershot the rate hikes.

The overshoot is the moment when rate hikes end while the 2-year yield is ABOVE the EFFR. And that has not occurred in this cycle, but it occurred in the other cycles.

For example, in 2018 (first chart), the rate hikes ended with the EFFR at 2.4% and the 2-year yield was at 3%. That’s the moment of the overshoot.

Thanks for clarifying. So I assume that you believe more rate hikes are coming? I’m personally neutral on the topic, but I was just wondering.

One could argue that in 2019, the 2-yr yield ran ahead of the eventual rate cuts, which is what could be happening as we speak. But I’m not really sure either way. What are your thoughts?

I don’t predict inflation, that’s a fool’s errand, and rate hikes depend on what inflation will do.

If inflation continues to accelerate, the first reaction we will see from the Fed is that they move the rate cuts further into the future. The December dot plot indicated three rate cuts by the end of this year. Future dot plots could reduce this. And if inflation continues to accelerate, the rate cuts might all be moved out of 2024. So that would be the first step.

But we may be looking at a decade of higher and stubborn inflation. Once inflation is out of the bottle, it rarely goes right back into the bottle. So this will likely play out over years, not just 2024. The Fed is fully aware of that and has said so.

Interesting viewpoint Mr. Richter. Larry Summers, a neo Keynesian, mentioned that the Fed may have to raise rates again in 2024? The FOMC definitely fell for the “head fake” in 2023.

An overshot would be for the 2 year to be over the terminal FFR. That spike was above the FFR at the time, but not above 5.25% where we stand currently.

Sorry Wolf – I see now you also answered the question. I hadn’t refreshed the page in a while so did not see your response.

Two explanations are better than one.

Very interesting insight.

Among many many many Fed errors of the last 15 years, I would have to cite the slow pace of QT as a prominent culprit in the persistence of inflation. That and poring gasoline on the fire with asset purchases 2 years after the original pandemic, there was no reason for this, especially MBS purchases.

QT is more effective than interest rate increases, perhaps? What doest the FED’s balance sheet look like today, 7.5 trillion, I think. Crazy thought, but maybe they could reduce interest rates and increase QT at the same time. This would LOOK great, and with enough QT increase, be effective in reducing inflation.

The current explanation coming from the Fed is that rates and QT are separate. The rate cuts that show up in the dot plot (3 in 2024) would occur even as QT continues.

The Fed has staunchly refused to officially tie QE/QT to this surge of inflation. But in their private understanding, they must be linking QE/QT to inflation via the financial conditions. So it would make sense for them to use QT as one of the tools to bring down inflation.

Who is going to buy the junk and other stuff that the Fed is offloading in the balance sheet reduction? Lower interest rates won’t match the real rate of interest. China and EU can’t buy our bonds because of their disinflation. And EU faces rising relative energy prices because Biden won’t let ZUS companies expert natty gas to them any more.

“Who is going to buy the junk and other stuff that the Fed is offloading…”

1. These securities are not “junk” but pristine Treasury securities and government-guaranteed MBS (agency MBS).

2. The Fed is “offloading” these securities by letting the Treasury securities mature without replacing them. There is no sale involved. The Fed gets paid cash for the face value of these Treasury securities when they mature. The Fed is “offloading” the MBS by collecting the pass-through principal payments when the underlying mortgages are paid off or paid down. Those pass-through principal payments are at face value. And there is no sale involved.

I saw the fat lady downtown, she’s lost most of her flab. She won’t be able to sing in her current condition. My singing will have no effect on anything so I won’t sing but I will say that higher for longer works well unless it means prices of goods and services keep rising unrestrained.

You’re not wrong, but you’re burying the lede. If they hadn’t done such monumentally reckless QE for two solid years after the brief pandemic swoon, we wouldn’t be sitting here right now watching in horror as their cautious QT fails to defeat inflation or even to contain asset bubbles.

Just like the drunken sailors have too much money, the sober sailors have too much money and got used to poor returns in ZIRP years so they are taking lower yields. If bailouts slow so returns have to match risks again then yields will rise and you can get your overshoot. If bailouts continue, yields will continue to be suppressed. You’re right that deficits are making the Fed’s job harder.

The deficit spending is the major cause of inflation. It’s that simple. As you well know, a real increase in unemployment has to materialize for there to be any chance of core PCE inflation moving towards 2%. JPowell knows this as well. Initial claims have to move up towards 300K and stay there while continued claims have to move above 2.5M and get to at least 3M. And no one knows when & what will force Congress to move towards fiscal restraint. And as I’ve said for 2 years now, who’s going to push back agains the EWarren & the UniParty for their glutten push for rent & mortgage relief?

The problem with your theory is that when unemployment increases, Congress will just send out stimulus checks funded by more deficits.

I guess you didn’t read my last sentence?

Nope, sure did. I’ll even quote it for you:

“And as I’ve said for 2 years now, who’s going to push back agains the EWarren & the UniParty for their glutten push for rent & mortgage relief?”

You are right in everything you said except:

“And no one knows when & what will force Congress to move towards fiscal restraint.”

Congress will be forced into fiscal restraint when debt payments are an unsustainable proportion of tax receipts.

Ehh, I’m not convinced the Republicans will go along with it this time. They did in March of 2020, and grudgingly in December, but if there’s not the cover of a pandemic or other “emergency,” I could see them just extending unemployment, which is what they did in 2009-2011.

I’d like to believe you, but I worry Trump will do anything he can to goose the economy, without regard to the consequences.

ChS, I think the difference now is that there’s more of an understanding among politicians and the average person that the stimulus from 2020-2021 led to the inflation.

Some of it would have happened even had Trump been reelected, as all but the $2 trillion extra from March 2021 had already been spent, but in a lot of ways, Trump was lucky that he wasn’t reelected, and that Biden is getting the blame for the current inflation, which is why most Americans are sour on the economy, regardless of what the Wall Street shills and other elites say.

The only thing that can stop the government spending is the bond market and the knock on effects that will have to other asset classes

Meanwhile on WSJ (I couldn’t read the entire article)

“Former St. Louis Fed President James Bullard Says March Rate Cut Would Be Wise”

Addiction to ZIRP is hard to overcome. People want their free money punch bowl back.

Howdy Rick V. ZIRP should never have happened. Govern ment may have stabilized a persons residence for the coming decades of inflation on purpose? Millions maybe jailed in their own home for decades? HEE HEE

Bullard trying to get back into the headlines? It must be tough to just suddenly vanish from the headlines after leaving the Fed. And now he’s trying to get back into the headlines by saying some BS that supports the WSJ’s BS? Makes sense.

That’s funny. He’s the same guy who said a 7% terminal FFR may be necessary. He was probably joking and the WSJ didn’t notice.

Ironically, he might have been right about his prediction back then (Nov 2022) that the Fed’s target range might have to rise much higher than the 3.75%-4.0% where it was at the time, and might have to go as high as 7%, to get inflation under control. He caught some flak for that. So we’ll see. But I have to admit, 7% seems very high. We’d have to get a lot of inflation to justify that.

The first reaction by the Fed to higher inflation will be that the rate cuts get moved out further into the future in the dot plot, and that they’ll do a lot of “being careful” and “carefully watching.” If inflation continues to accelerate and the labor market remains tight, the next step would be telegraphing a rate hike in the future. And if that doesn’t do the trick, they might actually hike.

Is it healthy that stimulative monetary policy occurs in gallon-sized gulps, but restrictive policy occurs in teaspoon-sized sips?

Perhaps just another indication of the Fed’s inflationary bias.

Reform the Fed (especially the maximum employments mandate).

With Europe and Asia flashing recession, how much US treasury demand could be a result of foreign investors fleeing to the US? The real yield of a German 2 year bond is basically 0%. US 2 year bond real yield is 2.5%.

I thinks this global issue is also making the inflation fight hard; the massive amount of savings that exists in the world, and that needs yields. Thus buying us debt.

That is why US is such a global empire, everyone lends their time (immigration) and money to it. Roman Empire 3.0

“this time is different” is a refrain I heard leading up to ’08. Could the yield curve inversion actually be completely wrong or way off timing-wise this go around? There was an instance in the 70s or early 80s where the inversion/recession timing was very messy. I sold big during the 2022 inversion and just sold big again because how can we be both inverted and at an all time high!? Now I get to doubt myself for the next 6-12 months

I sold big on Friday as well. This market is way too irrational. The shoe shine boy indicator is screaming at us and nobody pays any attention to it. Moreover, I have noticed due to the volume of trade I won’t be able to log into my trade account on a busy high volume trade day. Better be wrong then sorry in my case.

I wonder if crypto correlates to the movement of the S & P – a measure of how manic the market becomes.

Crypto is behaving as a risk asset.

Fortunately because of American Exceptionalism and the greatest representative democracy to ever exist, all woes will be resolved in November. The power, compassion, and intellect of voters will save our great nation.

Hey Glen, I love the enthusiastic optimism!

Could be! I think it was a saying attributed to old Churchill; Americans, after exhausting all other options, will do the right thing!

I was being extremely sarcastic!

…use of the ‘/s’- switch, Glen, is now almost de rigeur among the patrons of this, Wolf’s most-excellent establishment…

may we all find a better day.

Glen, I was playing along! Not for moment did I think you traded in your dialect materialism for American exceptionalism.

Howdy Folks. Golly, I thought the March Rate Cuts were supposed to happen. HEE HEE. What a great show this time around. I was fooled so many years ago, but now armed with Wolf Street, life is better and more fun…………THANKS

Is the bond market in denial or just the traders want to get there first because there’s no money left if you wait and get your position late? Of course it’s also lucrative taking the money from the people who got there ahead of you and going the other with a headfake.

Guess we find out with who got a great buy with 4% yield for 10years vs who’s crying about holding underwater bonds.

(and never a “told you so” with people only reading the headlines, lol)

Three hypothesises, which are not mutually exclusive:

-Many bond traders are still in denial about inflation and think it will just go away.

-The Treasury as been restricting the supply of longer-duration paper in favor of more bills.

-Other countries’ yields are still lower, as Dan above wrote.

The UK is now officially in recession. Others, ones in the EU, may be also. Will they return to negative rates? Will Treasuries draw in more global capital? How will the Fed react if rates get pushed down due to the influx of money?

Higher, for much, much, longer. It would seem that Uncle Sam can no longer export inflation. The Fed and central banks around the globe have really made a mess of things.

Interesting times.

“It would seem that Uncle Sam can no longer export inflation.”

I disagree. I feel the Fed has done a great job maintaining foreign demand for treasuries (and dollar liquidity more generally).

There’s a reason that US Treasuries are globally recognized as the most pristine collateral to lend against.

I’m biting. The reason is the government ensures through things like imperialism, trade restrictions and limiting development of other countries it keeps the dollar supreme?

It’s only been able to do that because the global market is convinced the printing was a one time fluke from the pandemic. If it happens every 4-5 years when there is a hint of recession, I don’t think you’ll see the same level of foreign trust.

Why would the markets be convinced of that? I’m not denying that they *do* think it, but…have they not been paying attention for the last fifteen years?

Pea Sea, I agree with you it’s not particularly smart, but that is the only explanation that makes sense to me.

The only reason anyone would buy 30 year treasuries at 4% is they’re confident inflation will return to 2% over that time. If it’s 2% for 24 of the 30 years, and 6-10% for the 6 that have “stimulus,” then it’s not really 2%, and investors would demand way more than 4%.

So long as dollars are being accepted in global trade, but that is changing. Gradually, then suddenly…

This issue was more or less resolved in 2020 with the Fed’s addition of the FIMA repo facility. Now foreign gov’ts can borrow from the Fed (with treasuries as collateral, valued at par of course) for the RRP rate + 25bps.

If the Fed had not done this, I agree that other countries dumping their treasuries could be a big problem. But now they’re incentised not to, because borrowing against the par value of treasuries is a better deal than selling them for a loss.

MM, the concern isn’t just that other countries will dump their treasuries, but not buy new ones.

For what it’s worth, I think the days of being able to sell 30 year treasuries for under 2%, and 10 year treasuries for under 1% are over for good.

Why wouldn’t they buy new treasuries? Its not like they’re getting a better yield back home.

If the Fed makes an error and actually does cut rates, then I’d be concerned. But as long as their rates are higher than the rest of the world’s CB rates, treasuries remain the best deal for int’l investors.

MM,

there are plenty of global opportunities with greater return. Countries by treasuries because they need dollar funding. As less and less trade is done in dollars, that need will decrease as it already is. Yet, CONgress still refuses to balance the f*%#ing budget, so the treasury also needs to issue even MORE debt, IN ADDITION to the debt it has to roll over. More issuance and less demand means interest rates are going up. It’s no personal, it’s just math.

MM, my concern isn’t so much that they’ll decide they want some other central bank’s printed fiat, but that people realize there’s a global war being waged by the central banks, and decide they just want hard assets, and don’t want currency at all.

Only one way to explain the stock market: “Irrational exuberance”

My take is the vast majority of wealth is controlled by the few. They couldn’t spend it even if they wanted and use every dodge possible(Bezos moving to Miami as latest dodge) which most Americans have no access to. The wealth has to go somewhere since the vast majority is not spent, so take your pick of gold, equities, bonds, land and treasuries. If it flows out on one thing and into another it just moves it around. Cashing out equities does come with a high cost for many unless you can offset gains with losses. Tax more and put more of the wealth of the people and it will get spent and not accumulate into ‘dynasties”.

Don’t forget BitCON. The billionaire filth are heavy into that now, too. They are the “whales.”

Pretty much every American has the “move to a low tax state” option, and many people utilize it, not just Bezos.

And very few families keep and maintain dynastic wealth. 3rd generation tends to spend it down. It takes enormous discipline to do otherwise.

You can make it up but it doesn’t make it true. Plenty of research on billionaire families, the wealth they control, and how long it lasts.

You may be in the category of being able to pick up and move to a new state but for low income it would be because of cost of living but also means having that money to move. My point was those will money can completely avoid consequences such as Bezos doing business in Washington and bailing when he sees fit to save 100s of millions of dollars.

Yeah, because “pretty much every American” has no job or family considerations that might get in the way of their moving.

@ Glen,

The Williams Group study of multigenerational wealth in the US shows wealth squandered in 70% of 2nd generation and 90% of 3rd generation families. Cornelius Vanderbilt was wealthier than Bill Gates, adjusted for inflation, when he died in 1877. By 1970, he had no descendants with a net worth of a million dollars.

It’s astoundingly easy for people who didn’t generate wealth to spend it, or invest foolishly and lose it. This applies to billionaires as well as people of modest wealth. The exceptions like the Mars and Walton families prove the rule.

“We conclude that the concentration of wealth is natural and inevitable, and is periodically alleviated by violent or peaceable redistribution. In this view, all economic history is the slow heartbeat of the social organism, vast systole and diastole of concentrating wealth and compulsory recirculation.” — Will and Ariel Durant, The Lessons of History

John H. – in terms of the systolic/diastolic society and the generation to which an individual is born, ‘timing is everything’, then? Best.

may we all find a better day.

91B20 1stCav (AUS)-

The image I get is more toward economy as a complex body, and money/wealth as the blood.

The systole/diastole are repeating, complementary, equalizing and almost rhythmic movements of that wealth, constantly circulating to the next title holder.

Happy1 is right, wealth doesn’t stay in the family for multiple generations, as a rule…

Cheers!

John H. – …but the timing of an individual’s opportunity to successfully access the curve of an ‘equalizing (?) redistribution’ of the flow of wealth is a constant? (reckon that’s where the ‘violent or peaceable’ enters into it, historically, when the equalizing significantly lags the disparity. Although, using Hofer’s lens, certain populations will put up with extreme disparities as long as certain norms of their class are observed and aren’t molested…). Best.

may we all find a better day.

Paradoxically, the Fat Lady not singing is music to my ears, if her silence does indeed mean higher for longer rates.

Great article, thanks Wolf.

Shocka

I like the name, Shocka.

Great article. As soon as I saw the first graph going to only 2016, I started googling for extended historical data; all talks about SOFR; came back and continued to find you have given all :)

On

“The fact that the 2-year yield undershot since December 2022 is a sign that these humans and algos have blown off the Fed, have not taken it seriously, and have been in denial about inflation and rate hikes.”

It appears the big guns knew that the FED cannot go beyond the number they did (because of all the debt, CRE, world intertangled finance); the FED also indicated so by saying the hike is done (or almost done) or they can wait longer at this rate etc. So, the folks who are really running the show know or decided his (FED) hands are tied (the choice of jumping from frying pan to boiling water situation).

Now if the inflation takes off as you suggest (I have my doubts on that as 1970’s was induced by oil crisis — external — Vs now it is internal and outside folks are transferring money to us and deflating their resources values) in spite of what I said, we are going to be in a hell.

“as 1970’s was induced by oil crisis — external —”

Yes, the oil crisis triggered it and with the underlying conditions being right, it took off on its own.

This current bout of inflation was triggered by an external event, the shortages and free money, and with underlying conditions being right, it took off on its own. You can see that in core services inflation, which had nothing to with the oil crisis back then or with the shortages now – those were goods. But in both events, services inflation took off and stayed high even after energy prices plunged again.

So here is core services inflation (excluding energy services), and you can see that once inflation is triggered by some external event, if underlying conditions are right, it takes off on its own:

Thanks. I forgot to mention, 1970’s we had another big issue — the Vietnam war which split the country, reduced efficiency, productivity etc.; just like the COVID scar, right to work and kill themselves, the soul searching, giving up work — retiring (especially those who could). This time we also have the revenge spending, YOLO mentality, big uncle with free money ……..

Could this be simplisticly be reduced to “the inflation cycle will not end until the T Market dramatically overreacts (only knowable in hindsight), and the belief in higher / longer driving this overreaction will tank the equities market”?

No. You are confusing correlation with causality. The overshoot is caused by the markets pricing in the expectation that they believe the Fed will hold rates higher for longer than they actually do. Right now, the markets are pricing in (rather dramatically) future rate cuts from the Fed – despite bad economic data that should indicate a more conservative posture. However it does become a self-fulfilling prophecy to some extent – because if the markets continue to price in future rate cuts, those lower rates are seen TODAY which tends to fuel the very inflation the Fed is trying to tamp down. The data would suggest the Fed needs to, at the least, temper their rate cut messaging.

QE/QT weren’t yet tools the Fed was utilizing in the 90s, correct? I think that somewhat changes the 2yr/EFFR correlation, so might only be a relevant comparison for the QE/QT era.

Also, the only way an overshot could occur now would be if the market shifted to expect another hike. With the Fed’s dot-plot telling us to expect three decreases it doesn’t seem likely unless the data gets really ugly.

The surprise increase in recent data was only enough to delay market expectations for a decrease, imagine the data it would take to push the market from expecting three decreases to expecting another hike!

We have one example of the QE/QT era, and that was in 2018 (first chart), and it worked in the classic manner with a 60 basis-point overshoot. The reason it wasn’t impacted by QE/QT in my opinion was that QE/QT impacts longer-term yields. The short-end of the Treasury yield curve is fairly tightly managed by the Fed’s five policy rates. The two year is far enough from the short end to be somewhat free from the policy rates but not under pressure from QE/QT like the longer end.

Sure, something could have changed, and the relationship might not be anymore what it was. That is always possible. But it did behave in the classic manner in 2018.

You are talking about something that I have been wondering about for the last 18 months – the lag / stickiness of economic activity created by QE. Given the “unprecedented” QE through 5/22, it will take years to unwind that expansionary policy. The Fed may have increased its EFFR to try to tamp down inflation – but QE is still (by any historical standard) white hot. Those dollars are still floating around out there driving economic activity, and they are directly fighting the Fed’s efforts to take the steam out of the economy. When I keep hearing the Fed being “surprised and frustrated” about their EFFR not having the depth of impact that they wanted – the only other two culprits out there Federal deficit spending and QE.

Please notify us when the overshoot has occurred :)

You bet!

Irving Fisher (1925) was the first to use and discuss the concept of a distributed lag.

See also: “The Lag from Monetary Policy Actions to Inflation: Friedman Revisited” 2002

The fact is that after 22 months of deceleration, the distributed lag effect of money flows, the proxy for inflation, accelerated in Dec.

I’m a bit skeptical. Looking at the charts, couldn’t you circle many “false overshoots” along the course of each upward trend?

Take, for example, 1995, 1999, and 2004-2006 – there were many moments where conditions looked ready for overshoot, but in reality it took much longer.

This seems like it may be more of an indicator* (*with noise).

Either way, how the markets are responding and taking/not taking the Fed seriously, with a high probability for more inflation and higher rates, makes sense to me.

There is some confusion about the term overshoot.

The 2-year yield normally runs ahead of the EFFR, and is normally higher than the EFFR during rate hikes and lower during rate cuts. That was the point of the article.

But in 2022-2023, it fell while the EFFR was still rising. In other words, the 2-year yield undershot the rate hikes.

The overshoot is the moment when rate hikes end (terminal EFFR) while the 2-year yield is ABOVE the EFFR. And that has not occurred in this cycle, but it occurred in the prior cycles.

For example, in 2018 (first chart), the rate hikes ended with the EFFR at 2.4% and the 2-year yield was at 3%. That’s the moment of the overshoot.

Makes more sense to me, thank you for explaining.

I think it might be different this time. Because now we’re at 120% or so debt to GDP, and from what I’ve read they are going to run $2T+ deficta forever. Because if they don’t the music stops.

The Fed is going to claim victory and drop rates because $35, 36, 38 trillion in debt needs to be at 2% or it’s all over.

I’m prepared for 4-6% inflation from this point on. Real estate, gold, even quality used cars. Things will increase in FRN numerical value because the money supply is going to double every dozen years from now on.

“…because $35, 36, 38 trillion in debt needs to be at 2% or it’s all over.”

Nah. Big misconception here. Inflation pumps up tax receipts. So the percentage of interest payments to tax receipts is what matters (chart below). And tax receipts are going to look very good in Q1 and Q2 2024 due to the capital gains taxes to be paid for the stock market rally in 2023. General income taxes are also strong due the pay raises (wage inflation) and record employment. But in 2023, capital gains tax receipts plunged because 2022 was a shitty year for stocks.

The new data is coming out later in February. So make sure to check back:

The “elephant” over in the corner is Ai.

Without AI the stock market would not be anywhere near as high. Valuations on GOOG, MSFT and NVDA as well as a few others have goosed the market, changing perceptions on the entire economy, and complicating efforts to slow it down.

At the same time even the short term impact on the economy is unknown. Anecdotally a lot of the expensive programmers are about to be replaced, with some companies on the verge of major personnel readjustments.

Open AI’s Sora announcement this week potentially puts a lot of videographers, photographers, and actors at a huge disadvantage.

The best comment I heard is …. Just remember … this is the worst it will be (i.e it will only get more powerful and omnipresent). The next 3-5 years are going to be like nothing we have ever seen before.

Inflationary or deflationary???? I’d love to have the answer on that.

I, for one, do not have the answer. Your post, j w, prompted me to look up some you-tube videos of Open AI’s “Sora”. Astonishing! AI will only improve. It still creates some flawed video – at the first rendering. The content is only limited by the user’s imagination.

There are soooo many jobs/professions that will not be able to compete.

We might think that manual labor-related jobs will survive, but, if they do, workers may be directed by AI “supervisors” who can optimize their work – laborers working while being given constant instructions, for example.

Manual labor on job sites will not be replaced by robots anytime soon because the physical movements required are much too complicated.

Tesla and others are working on humanoid robots but they are still not ready for even the basic movements of a flat-floor factory job.

I recommend the ‘construction trades’ with an eventual eye toward contracting as a more secure future for many workers.

Unless AI is somehow going to bring a new energy source online (like fusion reactors) and a more efficient way to deliver that energy, we are looking at a very inflationary period. With 8+ billion mouths to feed and retirement population growing substantially, it’s not personal, it’s just math and physics.

A massive die-off would change things, but I don’t see that happening anytime soon.

“AI” is machine learning from the 70’s with exponentially faster processors and exponentially more data to search. While I expect some goods innovation to come out of this eventually, we will have to have some really smart humans sort through exponentially more crap first.

For me, the question is who will by the $34 trillion and growing in trillion dollar increments?

The Fed? Results in more monetization and inflation.

The public? Will ultimately demand at least 3% REAL returns.

And, where is congress in all of this? Answer: out to lunch.

Cheers,

B

“who will by the $34 trillion and growing in trillion dollar increments?”

We just bought some more, LOL. We got our annual dose of ibonds and we bought some new T-bills. We also bought some T-bills to replace maturing T-bills via auto-rollover. And we’re not alone, I swear! There is huge global demand for this stuff, or else yields would be a lot higher, and then there would be huge demand for these even higher yields.

Yield solves all demand problems.

I read about t-bills here not too long ago for the first time and I’m trying my first go at them. I have money from when I sold my house in 2020 (should have waited a couple more years in hindsight, but some external factors forced my hand at the time) sitting in a HYSA, and I just want to goose my returns a little more without having to deal with the volatile stock market.

I’m also planning on buying another house within the next two years, so I don’t want my money tied up for a long time. The rates on the 4 week t-bill are approximately 1% higher than my HYSA, and the 4 week term gives me flexibility to adjust if something drastic happens.

Probably just going to keep rolling them over after they mature while keeping an eye on the news, but it’s likely going to be the safest place for my money for the next two years. The election this year is really giving me jitters though…so much that I’m planning on residing outside of the US for most of the year. I’ve already spent a year out of the last two years in LATAM, so it’s just kind of a natural transition for me anyway.

One additional benefit of Treasury securities is that the interest income is exempt from state income taxes. So if you’re taxable in a state with high income taxes, that helps.

Yes, but how much of that is because the treasury has gone to shorter duration bills?

What yield will be needed to solve demand problems at the longer end, especially if the debt keeps growing by $2-$3 trillion a year, in the “good times.?”

Me too on the treasuries. Just filed my taxes with a 1099 from the treasury. Yes they are taxable.

My guess is that the market will need to work its magic as these massive deficits expand. I remember buying t’bills at 17% and long term treasuries at 15+ %.

Will it happen again?

Cheers,

Brewski

I’m getting 5% on a 1 year 100K CD from my local credit union. That’s $5,000 in interest for doing nothing. Makes another income stream. There’s competition out there. Treasuries will have to cough up a rate equal or above what local credit unions are offering, or it’s lights out for funding the 2 trillion Federal deficit. I’d like to see a return to Volcker’s 18% interest rates.

I haven’t read the comments section at Zero Hedge for years, but it was the source of my all-time favorite comment.

Someone asked, “Who will buy the trillions of yens worth of new Japanese government bonds?” (being issued at the time).

“That’s easy,” someone else commented. “Why do you think Japan is so far ahead with inventing robots?”

:Grinning face with smiling eyes: :Crying with laughter: :Rolling on the floor laughing:

Terrific article Wolf. If inflation does stay higher for longer, and yields rise as you say. That is going to make the interest on the debt even a bigger burden, increasing the deficits even more. Becoming a larger budget line item then defense. You wonder if at some point the Fed is going to have to do YCC.? To stop the spiraling interest costs from piling on the debt.

Inflation is also increasing the tax receipts, and it’s watering down the purchasing power (the burden) of the $34 trillion in existing bonds. Inflation is the classic method of reducing the burden of public debt.

When are they going to issue new dollar? You’d have to turn in 100 old dollars to get one new dollar. Sort of like they did in the Weimer Republic in 1923.

I don’t know enough about trade etc. to know how much the Red Sea ‘choke point’ being closed to container ships will affect inflation but having researched the military solutions a bit, this could be very difficult and long term. It’s almost impossible to find comparables Of course enemies have tried to interdict shipping before, but never through such a narrow channel, about 20 kilos at tightest with shoals and currents.

During early WWII most critical stuff was landed on west side of UK. And there were no cheapo drones, or targets as big as container ships.

If insurers balk, govts may have to reinsure.

To guarantee safety of lane, it might be necessary to occupy the area nearest choke point.

…. And now truckers refusing deliveries to NYC.

New York City wouldn’t make it more than a day or two before a real truck freight embargo would drive almost everybody underground, broke, or nuts. But there’s no short-term resolution to the trucker’s grievance. The judge made his decision and short of the appeals process there’s no legal remedy for that. The truckers can’t starve the judicial machine into reversing it’s decision. None of those judges and politicos are going to miss a meal. The standoff between Ronald Reagan and the air traffic controllers was ended pretty decisively, and the same thing will probably happen again, if the truck-out even catches on. The food and gas and water and trash hauling have to flow to prevent rioting, and the government does know how to move lots of stuff inefficiently and expensively.

The average New Yorker has no influence over city and state politics. They just pay for it. Or move to Florida.

By this standard, no one should ever take a stand on anything. I don’t agree with it. Everything has to start somewhere.

The scoreboard reads

Truckers 100

NYC 0

Red Sea is more important to Europe and Asia than the U.S..

Vice Adm. Brad Cooper, deputy commander of U.S. Central Command, told CBS’ “60 Minutes” in an interview broadcast Sunday that “15% of global trade flows exactly through the Red Sea…”

Brilliant article, you made your point very clearly!

I recommend reading or listening to ‘Memos’ by Howard Marks, Oak tree Capital Management.

In particular I recommend Sea Change, Easy Money, and The Price of Time.

These ‘Memos’ are all about interest rates.

Marks is one of the best in high yield/junk bonds.

The current “sea change” started in 2008. And Volcker wasn’t responsible for curtailing inflation. The DIDMCA of March 31st, 1980, was. The Act reduced money velocity.

The age of the population was the determining factor. At the time there was very few retirees due to the era of the baby boomers. The boomers hadn’t reached peak earning years at the time thus the collapse came because of their low net worth at the time.

Great suggestion TC. I love his moving walkway analogy of low rates.

Would the undershoot mean that for 2 years span, there is a strong expectations that the rates are going down? This seems reasonable to me.

I don’t see any special magic meaning here.

If overshoot then the 2/10 inversion would be even bigger bringing more panic for some. No panic please :)

So, the Fed has utterly failed on her price stability mission and will continue to do so for many years. Good job Chair Arthur Powell!

Wolf, just delete this if too big holes in here, just quickly, no time for more:

You cannot compare past and present. In the past FED under communicated actions. Any INITIAL raise, pause, lowering of rates were mostly surprises. Presently, FED over communicate everything. Also, in the past financial system was not as overleveraged and speculative as it is now.

On the other note FED will have to blow up economy to get handle on

the current inflation.

Lastly, there should be a new econ definition established. Currently FED is officially doing “QT”, but it’s problematic. As there is term DIS-inflation, there also should be term DIS-QE. FED is DIS-QEing balance sheet right now. Only when FED is not buying at all or selling, it should be called QT.

Although, DIS-QE is also tightening financial conditions and negative for assets and markets (less fuel poured on fire).

Or call it BS, delete this, I do not care. Will not be checking replies.

1. “In the past FED under communicated actions.” You’re thinking the deep past, and yes, in the 1980s, and before, the Fed communicated a lot less if at all. Through 1993, FOMC rate decisions weren’t even announced. Markets had to figure it out on their own.

But in 1993, this began to change. Releasing the minutes started in 1993. In 1994, the rate decisions were announced. The rate-hike cycle in 2005/6 was highly communicated in advance (“forward guidance” was by then an official tool in the tool box and that has continued). The Summary of Economic Projections (which includes the data for the dot plot) were being released starting in 2007. Here on this site, we followed the rate hike cycle 2015-2018 closely (started by Yellen and continued by Powell). It was highly communicated at every twist and turn, and there were no surprises. And the pivot was announced at the Dec 2018 meeting that led to a pause for several meetings and then a couple of rate cuts before the pandemic reaction in March 2020.

2. “On the other note FED will have to blow up economy to get handle on the current inflation.” Could be. Volcker finally had to do that. Let’s hope not. The double dip recession was really bad. I came out of grad school during the unemployment crisis of the second dip, and that was shitty timing, LOL. I don’t wish that on anyone.

3. The phrase “QT.” We would all like our own definitions of everything. During QT in 2018/2019, I tried to get my phrase “QE unwind” to stick, but it didn’t stick (you can google it, it still brings up some of my old charts and articles further down the search results). Since then, I’ve stuck to the now generally accepted phrase QT. It really doesn’t matter what you or I think something should be called unless we’re big enough to impose our will. Drunken Sailors, for example, has taken off beyond this site. There are a few other phrases we used for specific things that spread from here. But that rarely happens. Generally, we have to live the phrases someone else manages to impose.

Is it crazy to think that if the Fed keeps hinting that rates will drop within a year, that the 2 year rates will never overshoot?

Ever since the Fed raised rates, there has been the misguided hope (mostly from Fed hints) that the rates will drop within the next year.

Everyone always expects that within the next 2 years rates will drop dramatically so everyone is piling in on less than 2 year Tbills.

The Fed should change their wording to hint that rate cuts will happen in 2025 or 2026 instead of the prior 2023 or 2024.

Interest rates will be going up, not down, in the years ahead.

If only the Fed would hint at that and Wall Street would believe it.

Instead, the Fed hints at rate cuts in the short term ie end of 2023, 4 cuts in 2024.

May be the Fed does not want the market to drop like a stone. Just imagine what would happen if the Fed says there would be no rate cuts in 2024.

Once you have markets feeding out of your hands it is going to be very difficult to extricate your hands. The mumbler Alan Greenspan probably knew this but did not care about its repercussions.

This deserves its own rant, but I continue to see the following:

1. Buy a house now even though the payments are at record highs because the Fed will lower rates and you can refi.

2. Buy stocks now even though the fundamentals are terrible because the Fed will lower rates and money will flow back into the market.

3. The stock market reaches record highs because the Fed will cut rates 4 times this year.

What happened to market fundamentals.? Our market isn’t free based on rational analysis. It only depends on what the Fed does.

Done with my short opinionated rant.

The 2-year should not have dropped below the EFFR in Dec 2022 — by that time, the market wasn’t buying the rate hikes anymore, and financial conditions were beginning to loosen — and it should have stayed above the EFFR though July 2023, and then in the second half of 2023 it might have begun to drop below the EFFR.

Might take a listen to Barry Ritholtz’s recent interview with former NY Fed Gov Bill Dudley on the Master’s in Business podcast. Dudley basically admitted financial conditions (defined as market-set liquidity outside Fed-set short-term rates, conveniently ignoring QT/QE impact on long-term rates) have loosened a lot especially in Q4 2023. On the one hand, as Dudley and Ritholtz discussed, the market setting easier financial conditions while Fed desisted from lowering rates meant that the Fed didn’t have to worry as much about negative economic growth/unemployment. On the other hand, as Wolf points out, that exact thing might mean policy has been ineffective and lead to higher inflation.

I like these charts and the theory presented. Data is the most important thing to have, and when somebody takes the time to make some nice charts and correlations it’s much appreciated.

What seems to jump out, and what you mentioned in your comments, is the EFFR tends to follow the 2Y. In fact, it seems to follow the 2Y very strongly.