Here come the “Marketable Borrowing Estimates,” showing by how much the pile of marketable Treasury securities will increase.

By Wolf Richter for WOLF STREET.

The Treasury Department’s Quarterly Refunding announcements, normally cause of a global yawn, have turned into a market-moving circus: Longer-term Treasury yields surged from August through October 2023 after the Treasury Department said in its Quarterly Refunding announcement at the beginning of August that it would issue a tsunami of longer-term Treasury notes and bonds. Then three months later, at the beginning of November, the Treasury Department attempted to undo some of the damage and said that it would shift the huge borrowing needs more to short-term Treasury bills, which caused longer-term yields to fall sharply.

And today, the Treasury Department announced in its “Marketable Borrowing Estimates” that – despite the fiscal deficit that has ballooned in recent months – it would have to borrow less in Q1 than it had forecast in the October announcement, and that it would have to borrow relatively little in Q2. And yields fell again.

Today, in its announcement, the Treasury department said that:

In Q1, it plans to add $760 billion in new debt to outstanding marketable Treasury securities, which is a huge amount, but that’s $55 billion lower that the estimate announced in October for Q1 ($816 billion), assuming a balance in its checking account – the Treasury General Account, or TGA – at the end of Q1 of $750 billion.

It said the $55 billion reduction in borrowing needs was due to higher tax receipts than previously expected and a higher Q1 beginning balance in its TGA – which started Q1 at $766 billion (instead of the projected $750 billion).

In Q2, it plans to add $202 billion to outstanding marketable Treasury securities, assuming an ending balance of the TGA of $750. On April 15, income taxes and estimated quarterly taxes are due, so there are usually huge inflows of tax receipts.

On Wednesday, the Treasury Department will release the Quarterly Refunding details, including projections of the amounts of Treasury bills, notes, and bonds to be issued.

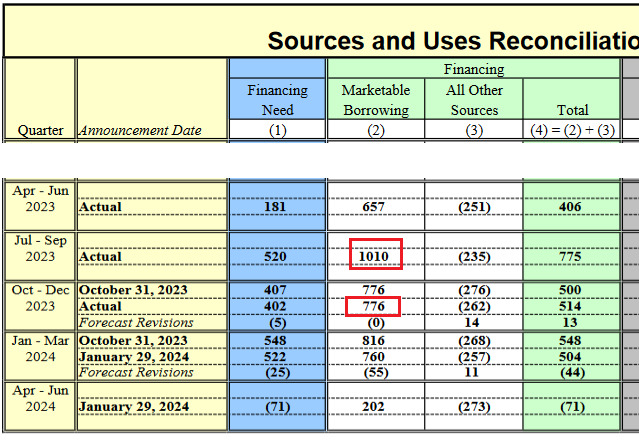

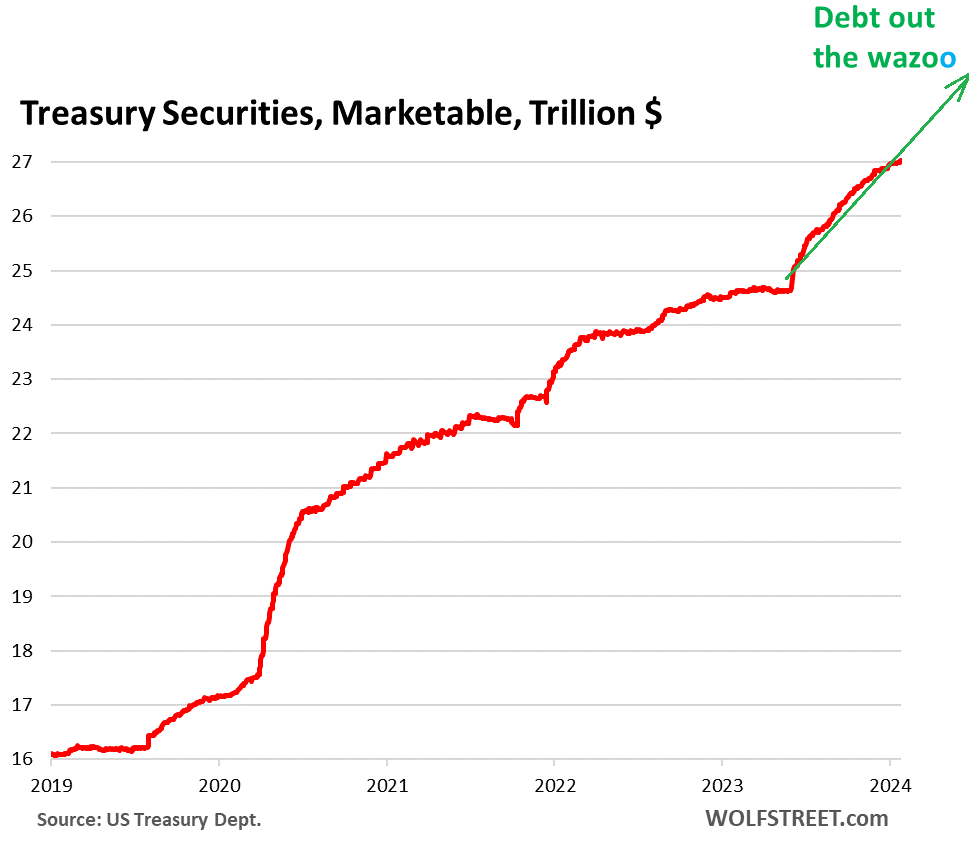

The total Treasury securities outstanding ($34.1 trillion currently) come in two portions: marketable securities ($27.0 trillion currently), which all kinds of investors buy and trade; and non-marketable securities ($7.1 trillion currently), which are held by US government pension funds, the Social Security Trust fund, etc. The Treasury department is talking about issuance of marketable securities.

The Treasury department said today that it added $1.01 trillion (“actual”) in Q3 to marketable securities and $776 billion (“actual”) in Q4, or $1.786 trillion combined. We marked these in red on the “Sources and Uses Reconciliation Table” released today (excerpt; total table here):

$2.55 trillion in nine months?

If the estimate of $760 billion for Q1 is on target, and the increase in total marketable securities is actually $760 billion in Q1, marketable securities will have increased in by $2.55 trillion over the nine months from July 1 2023 through March 31 2024.

As of today, marketable Treasury securities are $27.0 trillion, up from $24.7 trillion at the beginning of Q3 2023. And if the “Marketable Borrowing Estimates” estimates today for Q1 are on target, marketable securities will be at $27.8 trillion by March 31.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Would it be wrong to call this fraudulent? How is it even possible?

It’s not fraudulent. The Treasury department publishes the actual actual® figures for marketable securities on a daily basis (which is where I get them from). So the data is there and public. But the Quarterly Refunding announcements have turned into a market-moving dog-and-pony show. They can kind of say whatever, no problem.

“But the Quarterly Refunding announcements have turned into a market-moving dog-and-pony show. They can kind of say whatever, no problem.”

– This!

Tomorrow morning, Powell will announce no change in either the FFR of interest nor the rate of QT runoff, which recently has come into focus as a potential pre-election source of stimulus funding.

A conservative post crash investigator would point to the dovish Fed as the principal cause, for now, it’s all good. Asset prices seem to be impervious to the antics of the fool FRB.

Wall St. sees what it wants to see, but is the finance media really so gullible as to rely on these announcements when, as you say, the daily data is easily available?

“Is the finance media really so gullible… ?”

Yes. My heavens, yes. A million times yes.

Maybe it’s like the Magnificent 7 stocks. Portfolio managers might not believe, but they have no choice but to pay along, least they lose their nice job at the casino.

Well, the PE is at a record, the 5 year growth expectation is at a record, which gets one to getting back 30 % of the purchase price.

The other 70% of return of capital relies on the expected growth over the next 50 years. At which time the profit will begin.

So yeah, I think the Fed is doing a disservice too the best people in this country by allowing the salesmen to entice them to buy at the top.

so sorry wolf

but Treasury is a FRAUD and so is FEDERAL GOVT

wish you had up/down voting

Maybe I’m misunderstanding, but the 1.010T number has been out there as an “actual” number for a while now–it was on the October 2023 Sources and Uses Reconciliation Table, and it’s there again on today’s table. One might reasonably believe it’s an actual representation of what the Treasury added to marketable securities in Q3 2023.

But now we have different data released elsewhere that apparently says those numbers are wrong, the Treasury really increased marketable securities by 1.354T in Q3 2023. Both figures are publicly available, but one is presumably right and the other isn’t. And the one that presumably isn’t was repeated today.

Does seem a bit…underhanded, doesn’t it? Disingenuous? Slimy? Certainly not confidence inducing.

Old saying which seems to be apt here; You can’t change the circus by moving the clowns around!

Wait, have they trademarked the term actual actual, or have you? I mean is actually actual theirs or is it actually actually yours??? 😂

It depends on the evidence. “Actually” may not actually mean what the alleged perpetrator intended it too mean.

Wolf said: “But the Quarterly Refunding announcements have turned into a market-moving dog-and-pony show. They can kind of say whatever, no problem.”

—————————————–

this is not fraudulant?

because it’s not illegal to lie?

They’re estimates and projections.

Thanks WR for this report.

I can see the govt and Fed trying their best to keep the asset markets at higher plateau and so far they have been very successful

I also assume the this week Fed would come out with ultra dovish statements.

“Fed would come out with ultra dovish statements.”

YOU will certainly read that in between the lines that Powell never said, for sure, for sure, that’s guaranteed, LOL. Your entire cohort will do that, you all will neither look at the statement nor listen to Powell because you only read in between the lines that no one said. We know that; you all have demonstrated this with relentless persistence for well over a year, maybe close to two years.

Well, you can’t deny the irrational rises in asset prices, which is hardly the hallmark of a determined Federal Reserve Board, willing too punish the speculators for their excesses. Which automatically places the FRB decision as dovish.

Queue up Kansas Point of no Return. At least we can listen to some good tunes as we crash over the wazoo waterfall of absurdity.

Wolf, what data source did you determine the “actual actual” numbers?

US Treasury Department daily statement:

https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny

We’ve become so dependent on credit that it’s the new cash! On with the show.

“marketable securities will have increased in by $3.0 trillion over the nine months from July 1 2023 through March 31 2024.”

Is that just not a very big WOW moment or what?

I’ve been saying for about two years now that I expect the debt to become an issue somewhere in between $35-$40T. Exactly what that means I’m not sure, but I suspect that $40T mark creates several issues for the Treasury & Fed that they themselves know are coming but won’t talk about publicly.

In other words, sometime well before the $50T that everyone seems to talk about as being a “possible” breaking point, the Fed / Treasury will become increasingly boxed in and forced to push Congress towards the fiscal restraint / cutting budget deficits.

Debt is just a number and it does matter.

Just look at Japan.

When debt was at 20T people said the same thing about dent at 30 T.

I meant .. debt does not matter as long as Govt can print their own currency and there is demand for us debt.

The Fed Can’t print money because there is inflation

Replying to Julian..

I dont trust government inflation metrics but inflation was under 2 percent after GFC when fed did many QEs.

Btw.. current core inflation is already in the striking distance of feds target rate .

It matters because it crowds out investment since someone has to buy the bonds.

Having drawn that equivalence as policy, suggests that you prescribe to let the bloated deficit continue to increase, since it already has been compromised, it should be allowed to be abused in the same manner.

I disagree with the grift that politics has become since the Citizens United decision, handed down by a corrupt Supreme Court,

“..the debt to become an issue somewhere in between $35-$40T”

So by end of summer then?

Maybe the week after the election

BINGO mad md! Give that commentor a cigar,LOL.

Always been that way, or at least since we were going to the stock brokerage to watch the tape displayed while moving as uncle traded -1950s.

What is the source for actual, actual data? Thank you

US Treasury Department daily statement:

https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny

On the bright side, the level of deception and ” everything is fine” narrative tip their hats that things under the surface ain’t so hot.

I RTGDFA 3 times and I am still confused. What is the advantage of driving down long term yields if short team yields stay high? Do they think they can spend higher for longer by shuffling the deck? It seems like smoke and mirrors but I am pretty ignorant on this subject so maybe its the smart play for them.

The Treasury Dept. can issue 3-year to 30-year securities with yields barely above 4%, rather than over 5%. From the taxpayer’s point of view, this is a good trick to reduce future interest expense for years and decades 🤣

Yea that is where I get confused if the short term yields are higher but you issue them more frequently is it just an accounting trick that doesnt really save the taxpayer in the long run or am I missing something?

Steelers Fan-

It strikes me as a “can-kicking” exercise: sell the larger portion of bonds to those who MUST keep money short, thus avoiding upsetting the much more volatile long-bond market; but thereby technocrats resign themselves to the fact that in short order, as the shorter bills and notes mature and require renewal, they risk the possibility of having to roll them at ever higher rates.

Of course, if the long awaited recession comes to pass, perhaps rates will temporarily blip downwards, in which case the whole gamble will have temporarily succeeded until the next wave of inflation strikes.

Kind of a hail-mary pass…!

The Fed more or less controls the short-term yields with its policy rates. But that’s only a smallish part of the debt: T-bills amount to only about 20% of the total debt.

The other 80% are longer-term notes and bonds (2 years to 30 years), and the coupon interest rate at with they’re issued remains a constant cash expense for the government for the duration of the bonds. So a 10-year note sold with a yield of 4.1% will cost the government that interest for the next 10 years, no matter what the market does. Notes and bonds is where the majority of the interest expense comes from.

I’m left wondering what resources are actually getting scarce enough to drive the increase in inflation that would move the long bond. Oil? Cause I’m pretty skeptical wages are going to go up enough to push it. Still seems more likely to me for a recession to hit.

Yes, but keep an eye on the middle ground, the 2yr treasury.

If concerns about our financial future were this administration’s focus Yellen would have aggressively extended maturities of Treasury obligations when long term rates were at rock bottom. She didn’t.

Druckenmiller called that the most egregious error of any Treasury Secretary’s in the history of the republic.

Sadly, this is more about goosing the market to help get Biden reelected

I think Yellen too had come to believe in near-0%-forever. She was part of the team that instituted it. Under her, the Fed timidly raised interest rates 6 times by 150 basis points, spread over two+ years. I don’t think she ever envisioned that inflation and Fed rates could be higher than 3%… that was before the pandemic. And by 2020, she was probably in the camp of 0% or negative rates forever. That’s the only way I can explain her decision, and it makes sense because lots of people were in that camp at the time, including big bond fund managers, and banks.

Yup… don’t forget that it was Yellen who first declared inflation in 2021 to be “transitory”… not Powell or the Fed. She has always been an inflation “dove” ever since her time in the CLINTON administration. She simply lacked the imagination to imagine inflation spiraling out of control again… and that lack of imagination had enormous consequences.

I think it could be the opposite, she knew that rates would not stay that way forever and that flooding the market with bonds that she knew would lose a large chuck of their value in few years could lead to all kinds of unforeseen problems.

Does this provide some cover for them to increase the long end issuance on wed now that the total amount is lower?

As if they care.

Is U.S. Treasury Secretary, and not coincidentally, former Fed Chair, Janet Yellen, now taking her cues from the Fed playbook? This is where the Fed “jawbones” the stonk/financial markets with weekly (now almost daily) speeches, announcements, policy statements, press conferences, etc. Is this now also Janet’s strategy for the Treasury market? Are we there yet?

The cost of interest payments is becoming a problem for U.S. Federal Government, esp. since Congress can’t stop spending other people’s (taxpayers) money. Beyond drunken sailors. Beyond sanity.

Is the U.S. Treasury now understating the debt to make it look better (smaller)? Lipstick on a pig? I think everyone knows at this point that the emperor isn’t wearing any clothes.

Also, the issuance of more bills over coupons isn’t a sound way to fund debt; it provides market liquidity, helping to keep stonks elevated, but it’s not a long-term solution. Maybe this is the strategy up until the November election? I’m sure this is fine.

The U.S. debt and deficits are clearly unsustainable and have been for a long time, but especially since the GFC and pandemic. All enabled by the nation’s central bank, the Fed, via debt monetization.

“Trees don’t grow to the sky.” – German proverb

Stein’s Law: “If something cannot go on forever, it will stop.” – Herbert Stein (1916-1999), Economist

Re “If something cannot go on forever, it will stop.”.

Inflation evidently defies this law. It may go on slowly but will forever. Fiat.

Please stop calling it a “crisis”, it wasn’t. 2008/2009 was financial FRAUD. Hank Paulson and numerous people from wall street should have gone to prison. Numerous banks and insurance corporations should have gone bankrupt and had their assets sold to pay back the creditors.

Watch/read “The Great Taking” and you can get an understanding why no one went to jail and the big banks came out smelling like a rose. It will be the same only more so when the fan gets hit the next time.

Well of course Yellen is furiously applying lipstick to the swine that will determine, which corrupt administration will be able to generate the most income from their win.

I think that Yellen is in control of the Fed’s pantomime of independence, which it clearly is not. The last 20 years of ZIRP policy and the asset bubble expansion, have convinced me that there is no such thing as a free market.

I’ve been waiting for this one announcement to come from Treasury, and had been wondering if we might not see in it some disingenuous, manipulative language in Treasury’s accompanying messaging, intent on supporting markets and suppressing bond yields by downplaying imminent borrowing. And here it is. Now I wonder at what point does reality come to bear with a big reveal.

John H., thanks for the reply and what you said makes sense but on the flip side of that coin if the recession doesnt come and infaltion stays elevated wouldnt they be better off having hooked a bunch of suckers at the lower yields for a longer time?

Steelers Fan-

Yes, I agree with you that the more prudent path for the Treasury would be to continue their tradition of over-weighting longer maturities for the lower annual rates, and also for the longer duration.

It’s interesting to me that the Treasury can effect rates as a supplier of inventory to the $27 trillion (and growing) US treasury market, while the Fed dances around the edges with it’s $3 trillion (hopefully declining) of QE/QT maneuvers. Both desire “stable” markets, but both seem to be leading us toward unprecedented INstability. And our elected officials dictate policy to both.

You couldn’t find a better combined argument for smaller government.

I thought the QRA was supposed to be Wednesday based on what I read. Was that wrong or was this a pre announcement to juice the market?

This is always a two-day event. Today was part one (the “Marketable Borrowing Estimates”). On Wednesday, we’ll get the details — how much in notes and bonds, and how much in T-bills, that kind of stuff. If I have time, I will also cover it (but it’s Fed day, and I may not have time to cover it).

Thanks. Weird, so it’s a 2 day event over 3 days? What do they do on their off day, hit the bars? Or given this is yellen, hit the local head shop?

Nobody should be surprised by what the Treasury is doing. It is manipulation in my opinion and it is for political gain. Dang thing happened to stop bonds from collapsing further in October when they pushed long term yields down.

Eventually all the buttons will have been pushed and the market will make them answer for this insane spending

I keep waiting for that day the casino makes them answer.

There is an argument that can be made that long term bond rates are artificially suppressed by the excess liquidity provided by the obese Fed balance sheet. The Fed is actually the market maker, sculpting the shape of the interest rate curve to satisfy the demands of the inside traders that own the Fed.

Test message

The G fund rate in the Thrift Savings Plan(401k for Federal employees), is

based on treasury securities of 4 years

or more. I think they are manipulating

the longer term rates down to reduce

their interest expense for various programs including pension obligations,

Social Security, etc…

This is probably it. Supress the growth in the inflation adjusted portions of the debt. If there were no COLA obligations, they could monetize debt out the wazoo.

Thanks for keeping us all informed of the Treasury’s ongoing…erm…Creativity In Truth-Telling Initiatives, lol.

Question for Mr. Richter, please. Is there a way of knowing how much of this debt issuance is expected to be “foreign owned” versus domestic? Is there any way of understanding whether the new debt explosion (since 2020, say) now relies more, or less, on foreign funding than before?

I ask due to a wish to better understand/track the ramifications for debt servicing and repayment (lol) options that an over-reliance on non-domestic funding (or a sudden drop in foreign interest) can create. Thank you again.

In terms of foreign holders of US Treasuries, I report on that in detail from time to time, most recently here:

https://wolfstreet.com/2023/12/20/are-foreign-holders-finally-bailing-out-of-the-incredibly-ballooning-us-national-debt/

Seems to be a way to do it, from december:

https://wolfstreet.com/2023/12/20/are-foreign-holders-finally-bailing-out-of-the-incredibly-ballooning-us-national-debt/

Nevermind, wolf’s responded 😂

Foreign ownership of the US government debt is enigmatic of the confusion that the normal American feels as they try to deconscript the bundle of political lies that they are bombarded with. They will mindlessly find their way to the polls and cast a vote for one of the two shameless grifters that the uniparty has offered them.

I read Wolf Articles and they all make sense. Govt is biggest drunkard sailor. Borrowing and spending like Debt doesn’t matter. Debt is rising in scary manner. Even how deceptive today’s announcement is.

But then I saw Stock and Financial markets. Everyday everything is going up. This week record breaking All Time Highs. Genius Treasury guys presented the data such way that markets went crazy after the announcement. Till announcement all indices were flat. Bonds went up too.

Treasury did same thing in October end. From then all indices have gone 15-20% up. Why bonds are not falling and yields going high, as much we expect them since so much debt and QT. It just shows how much liquidity FED created during Pandemic. FED is talking about some rate cuts in some time-frame. As per Dec 2023 SEP there are 3 in second half. There also Markets are running ahead of FED.

I am sure tomorrow Treasury will show some genius way. Minimize 10 year amounts as it drives too many things. Increase bills. Kick the can till next year at least.

When will this Debt matter? Will it ever matter? Will we ever have price corrections in all assets? Too many Questions I guess.

I think you have described an economic prescription to buy more, deny your doubts.

Even your kids think you are a loser for cautioning them to be careful about over paying with a flimsy contract that waives your inspection rights.

Call me old fashioned.

So… (1) why isn’t all this Treasury buying crowding out the money that would have gone into corporate bonds and (2) why aren’t the spreads on corporate bond rates vs Treasury rates rising significantly? Finally, (3) do you know if there is a source of an analogous set of data for corporate bonds that could forensically determine what is going on over there?

The last thing someone should buy is corporate bonds which are priced like it’s in the bag, A 30 year bet, several pct interest rates below where they would if risk was an independent variable. In that specific case long term corporate bonds may constitute an attractive bet, or investment, which ever one chooses to rationalize it as.

First thing one should ascertain is how old are the principals ? Are the of Christian upbringing, all the usual preliminary questions that the police might ask one while loosening them up to admit to a crime the didn’t commit.

I am a law and order thinker that thinks that we are filling the industrial prison system with bodies according to a business contract between the state and the private incarceration system that manages the prison without empathy for any loss except revenue.

The only thing that may actually be mistaken as one redeeming quality of human beings is love.

But, what are the actually actual®️ amounts? LOL!😱

Calling it ‘debt’ implies it is a liability that has to be paid back. That is a gross misunderstanding of how governments fund themselves and how monetary operations work.

You have a “gross misunderstanding” of how bonds — any bonds, including Treasury securities — work. They all work on the same basic principle.

LOL! Every one of the T-bills I have bought recently has been paid back, with the 5+ % interest to boot.

I don’t think you understand how this works…

The bond vigilantes have to stay steadfast and buy nothing to drive yields higher.

OK, work with me here, the “bond vigilantes” is an urban legend. Since the bond market became numb and unresponsive while taking QE, one would surmise that long term interest rates would naturally rise once the Fed had gotten through the QE withdrawl protocol which calls for a significant decline in over priced assets prices.

So far, with the election threatening us, it is incredibly difficult to discern what the heck is actually going on.

I can’t believe that the American people are paying for an extravagant party that their kind is not invited too.

The people that made it all possible are forgotten.

When my parents decided to send me to a private school, they payed the tuition and the tax for the public school. There was no public funding of private schools, like now.

Don’t forget that these estimates only include spending under CURRENT law.

Congress is currently operating the government under a CR, with agencies budgets frozen at last year’s levels.

However, the CR expires March 1, with some other agencies on March 8. House Speaker Johnson and the Dems have already agreed to higher spending levels, based on some deal they reached over Christmas holiday.

As long as Congress passes the 12 appropriations bills, there will be higher spending in Q2.

Then, there is the $104B Biden wants for Ukraine, Israel, and border security. That is not accounted for either in the QRA. Anyone seriously think that at least some of that won’t get passed, this year?

If not, kiss Ukraine goodbye.

The Fed owns Billions (Trillions) in Treasury debt.

Is that considered “marketable securities”?

If that is considered as such, it is a misnomer. They never sell (market) the Treasury paper they buy.

“Is that considered “marketable securities”?”

Yes. In that respect, the Fed is no different than another bank, or a bond fund, or whatever: It buys bonds and holds them to maturity.

“… it is a misnomer. They never sell (market) the Treasury paper they buy.”

No, it’s not a misnomer. Bonds were designed to be held to maturity and collect the coupon interest until you get your money back at maturity. Bonds are ancient, trading them online with the click of a mouse is new. A few decades ago, it was hard and expensive to sell bonds, and not many investors did. There are still many bonds that essentially never trade. What “marketable” means is that they can be sold to others. But they don’t have to be sold – and most investors don’t sell them.

Nonmarketable securities, such as our I-bonds, cannot be sold to anyone, you have to redeem them directly from the government.

Correct. I can still remember my grandfather taking the physical paper bond out of his safe when it was time to redeem them.

Full FAITH and credit…

Don’t buy anything paying less than the 3 month or longer than than the same. Ignorant farmers and miners like us should not accept the outcome as inevitable without considering how much one can afford to lose if they make such a bet and they lose.

Nice overview, but i think the more interesting comes on wednes day when the Treasury will announce the exactly amounts for each type of securities. Maybe we see a shift more to the long end? For sure makes sense, because the yields for the longer end are lower as on the short end.

Overall, these change nothing on the fact that the US have a massive debt problem.

We will not see an increase in the long end interest rates until the liquidity that is the source of reckless liquidity is extinguished Looking at the obesity of the Fed balance sheet I predict that tomorrow, the Fed, rather than taking the speculators too the wood shed, will support their agenda in a manner that suggest they are more a gumba than an agency. I may be wrong

As we rapidly approach $40T in total debt you can understand why the fed govt is desperate to keep a lid on their interest costs. We are the classic story of the big-spender running out of their credit limit and struggling more and more to just pay the interest “carrying costs” of their debt. As the fed auctions get worse and worse there will be more calls to stop QT and drop rates.

Their idea of cutting back on spending is to cut back on interest payments on the massive debt they create.

They leap to part B (interest payments) and forget part A (debt creation).

The ratio of debt created per dollar to the resultant GDP dollar increase can not sustain itself, IMO.

Wow, lots of angst in the comments here.

I don’t see the national debt as a problem at all. All debts are cleared in all cases. Either the borrower repays or the lender takes a haircut. Regardless, all debts are cleared at some point. The lender in the case of government bonds just not realize how this will happen now nor have they ever realized it.

Now, deficits are another matter. Deficits under the GOP reign has always been treated as if they don’t matter. Truth is, they matter a lot. And always have. (Reagan, Bush, Cheney, deficits don’t matter as they pushed for and received enormous tax cuts for the rich). Congress could fix this but as long as we believe that our congressman is great, there will not be a solution. if readers want to fix this, they will have to replace their particular representatives.

As Greenspan said a long time ago, the Fed can (and will) never go bankrupt and make sure that the treasury always pays off debt and interest. What the Fed cannot guarantee is the purchasing power of the currency (FRN)…

CONgress is fully owned my friend, 2008/2009 made that much obvious.

Louie-

“Either the borrower repays, or the lender takes a haircut.”

If the lender takes a haircut (either through repudiation OR through inflation), the holders of US$ will have lost confidence around the world.

So long dollar dominance, hello austerity, and prepare for civil unrest.

(I’ll leave the political comments for someone else to quibble with.)

The lender always takes the haircut. In the long run, always. and he always has. I can remember in the late 40s my dad and uncle having a conversation and the statement from my uncle banker was, “the dollar has lost 75% of its purchasing power”. Now, all those decades later, I just heard the same thing in only slightly different language. We humans learn nothing from history and likely never will. It’s our nature I guess. The lesson: when you loan money, which is what you do when you buy a government instrument, you run the risk of not getting back what you hoped to get back.

Why fix it? The national deficit keeps adding to our “National Savings Account’! /s

New poster here except for one post two years ago under a name that I forget:

If Treasury is faking numbers here for future funding requirements, what does that say about all data controlled by the current administration? After all the heads of all agencies such as the BLS are probably also political appointees, not just Yellen at Treasury. How accurate are the CPI, PCE, and the Employment numbers? Example: The Cleveland Fed Nowcast predictions for PCE and CPI have consistently overstated actual Govt. inflation numbers for the past seven or eight months. Of course, the Cleveland Fed data is not as complete as the BLS data but, shouldn’t differences between the two be more random than always in one direction if all the numbers are at least honest?

“The Cleveland Fed Nowcast predictions for PCE and CPI have consistently overstated actual Govt. inflation numbers for the past seven or eight months.”

This is BS. The Cleveland Fed uses the Exact SAME Data that the BLS and the BEA use — it uses THEIR data, but it applies some algos to it to trim some stuff out. There are gazillions of these “trimmed” or “sticky” or modified CPI/PCE versions out there, it seems every one of the 12 FRBs has its own collection. Some are higher some are lower than CPI/PCE.

So you’re using your own misunderstanding of what the Cleveland Fed does to support your BS theory?

Tin foil hat stuff.

The BLS numbers are determined by thousands of non-political bureaucrats, most of whom also worked for the prior administration.

Furthermore, any conspiracy by the political appointee at the head of the agency to fudge the BLS numbers would require these thousands of non-political bureaucrats to get on board with the deception and keep quiet.

You are falling prey to the tin foil hat nuttery in right wing media. Why do you let them take advantage of you like that?

So, massive demand incoming and The Fed and treasury are simply jawboning.

Hmmm, “higher for longer”, OR is there some way to scare people back into treasuries…

War, what is it good for? Follow the money folks, always tells the truth.

It took a long time to persuade Janet the benifits of “jawboning”. But she has finally come around.

“The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.”

Ernest Hemingway

And, his quote on bankruptcy in “The Sun Also Rises” gives us a forecast.

Cheers,

B

Higher for longer…?

“How did you go bankrupt?”

Two ways. Gradually, then suddenly.”

― Ernest Hemingway, The Sun Also Rises

Yes, I read that book. I am referring to the Fed. They should NOT cut at all this year.

While we are quoting

“”A democracy cannot exist as a permanent form of government. It can only exist until the voters discover that they can vote themselves largesse from the public treasury. From that moment on, the majority always votes for the candidates promising the most benefits from the public treasury with the result that a democracy always collapses over loose fiscal policy, always followed by a dictatorship. The average age of the world’s greatest civilizations has been 200 years.” DeToqueville 1850 (or Tytler 1757) Socrates made similar comments.

What, me worry?

one trillion dollars is equal to 1012 sec)/( 3.16 x 107 sec/yr) = 31,546 years. 1.786 trillion dollar debt increase is equal to 1.786 X 31,546 years

= 56,341 years.

The Federal Reserve Act of 1913 needs to be repealed and let market forces

and supply and demand decide everything. We are in for a very rough economic ride

Let’s just get the Fed to honor their mandates first…

Stable prices not 2% encouraged inflation, or any inflation.

Moderate long term interest rates……the Fed has no business in the long end….inflation and employment are current and real time. The Fed stayed out of the long end for almost 100 yrs. Then Bernanke won the Nobel by violating that precedent.

Next get the Fed back to be there primarily for short term banking issues.

The “intent” of the Constitution is that Congress controls the “minting” of money, yet the Fed does the digital “minting”. At least Congress is accountable to voters.

Wolf,

Not sure why my comment was put on hold for the last 3 hours. Is it because I am new, and you need to do a background check? Is my statement too political? If too political I disagree because I believe your whole article is about Treasury misrepresenting their funding needs for political (interest rate) considerations. Actually, I dislike both major parties equally. As for implying that if Treasury will misrepresent their funding needs, other agencies also may not be completely honest as well, this is entirely logical. I do not believe BLS dramatically understates CPI as is claimed by Shadowstats, but, even small differences matter these days since the market always needs to believe that actual inflation beats (is lower than) expectations. January for instance in the Cleveland Nowcast, showed core PCE expectations to be .25% whereas actual turned out to be .2% Similar differences for other months are very frequent and always in the same direction, especially for CPI. Thanks and don’t post this. I am not calling you out. I just want to know what I did wrong.

It was on hold because it was BS, and I didn’t want to waste my time on it. Now I had to waste my time on it to shoot it down.

Your Cleveland Fed theory is BS. The Cleveland Fed uses the Exact SAME Data that the BLS and the BEA use — it uses THEIR data, but it applies some algos to it to trim some stuff out. There are gazillions of these “trimmed” or “sticky” or modified CPI/PCE versions out there, it seems every one of the 12 FRBs has its own collection. Some are higher some are lower than CPI/PCE. You just don’t know, and you’re reading some stupid blog and dragging this BS into here. And you’re using your own misunderstanding of what the Cleveland Fed does to support your BS theory?

There may be “gazillions” of modified CPI/PCE Fed models out there at the various Fed offices but there are three major ones – the Cleveland model, the Philadelphia model and the St. Louis model, (to a lesser extent). The Philadelphia model compiles banker and WallStreet projections of CPI/PCE. The Cleveland Nowcast model compiles daily actual data in various categories, as you say, and forecasts what is not yet available. As far as I know, Nowcast is the only Fed model to try and mirror the actual monthly CPI/PCE and publicly claim that is what they are attempting. If this is a “misunderstanding” please explain why.

I did not read “some stupid blog” to wonder why the Nowcast and the actual CPI/PCE differ. Each month for the past year I have gone to the Cleveland Fed website and I have copied down the Nowcast predictions. Later I compare these predictions to the actual inflation numbers.

Actually, you need to work on your temper.

Here is the underlying inflation dashboard by the Atlanta Fed. It includes the 7 major FRB inflation indices. THREE of the 7 are higher than core CPI and ALL of the 7 are higher than core PCE. The highest one is the San Francisco Cyclical Core PCE index (5.8%).

https://www.atlantafed.org/research/inflationproject/underlying-inflation-dashboard

Why does he have to work on his temper?

That implies he needs to be more tolerant of people who are willfully ignorant in order to try and support some crackpot conspiracy.

WOuld it be fair to say the Fed is quite keen to keep the yield curve inverted by a certain amount to help the equity market?

I wouldn’t say. I think they’re comfortable with it being inverted, and they expected it when they pushed rates to 5.5% so quickly.

Hi Wolf,

Sorry I can’t seem to calculate the same “actual actual” figure that you calculated – here is what I am doing.

From here:- https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny

For Q4 2023 – your calculated figure is 894 billion.

I try by subtracting 10/01/2023 – 12/31/2023

ie, $26,938,517,614,684.59 – $26,339,002,538,627.28 = 599,515,076,057.31 (599 billion)

Where am I going wrong?

Thanks, yes, got my quarter shifted. I deleted that part.

I know very little about treasuries but I saw this in the Financial Times Wednesday morning:

“The US Treasury department has announced that it will conduct its largest-ever debt auctions in the coming three months, an effort to fill a wide federal budget deficit.

The Treasury will increase the size of its two-year and five-year bond auctions by $3bn a month for the next three months, it said in its quarterly refunding announcement on Wednesday. The $69bn in two-year notes that will be sold in April would be the biggest-ever coupon auction.”

Rather lacking that the Federal Reserve Chairman always talks about their strategy to assure their mission being addressed without addressing the political winds that influence their efforts.