As China unloaded Treasury securities and Japan propped up the yen, other countries loaded up.

By Wolf Richter for WOLF STREET.

Who is buying the ballooning US government debt that has now reached $32.5 trillion? That’s on everyone’s mind. For now, there is way too much demand for long-term Treasury securities, or else the 10-year yield wouldn’t be 3.8%, but 6.8%, and the 30-year yield would be further north. But maybe someday yields will have to rise to lure more buyers. Yield solves all demand issues. If you can’t sell them at 5%, try 5.1%. Just about anything will sell if the yield is high enough. That’s why even junk bonds find eager buyers. But we’re not there yet with Treasuries.

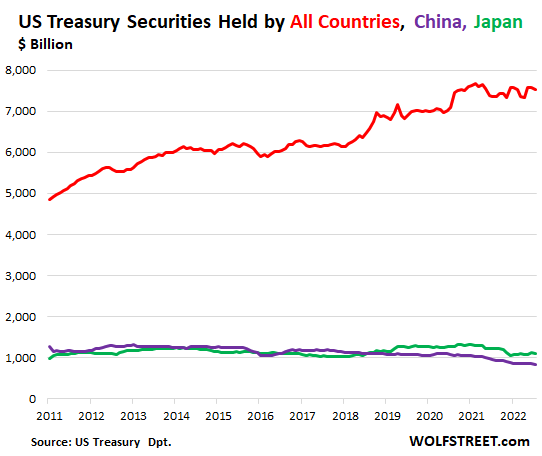

Even foreign buyers are still loading up, particularly in Europe. But China and Japan, the two largest holders of Treasury securities, have been unloading.

In total, all foreign holders held $7.53 trillion in Treasuries in May, down a hair from the record holdings in April, but up by 2.4% from a year ago (red line), according to the Treasury Department’s TIC data today. By contrast, the holdings of China and Hong Kong combined (purple) fell by 6.6% from a year ago, and the holdings of Japan (green) fell by 10.1% from a year ago. Both countries have for years been losing importance among foreign holders of the US debt:

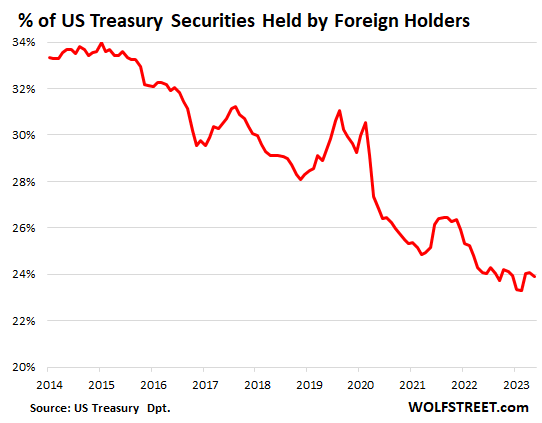

Foreign holders became less crucial. As the US debt has ballooned over the years, but foreign holdings have increased more slowly, the share of foreign holdings as a percent of the total federal debt has declined from the 33% range in 2014 to less than 24% in May. In other words, the US debt financing has become less dependent on foreign holders:

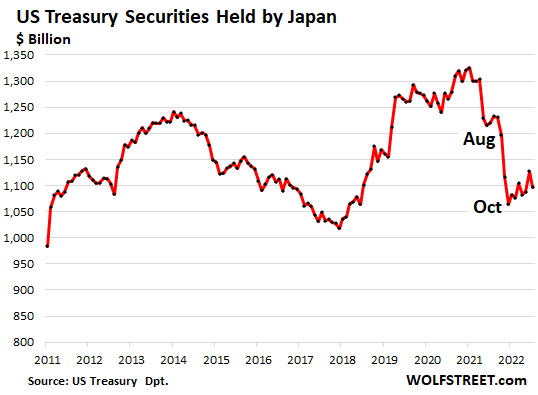

Japan’s Ministry of Finance late last year cashed in some US-dollar assets, presumably Treasury securities, and then blew $68 billion in dollar-cash to buy yen in the foreign exchange market to prop up the yen after it had plunged to ¥150 to the dollar by October.

And we can see that the MoF prepared for propping up the yen in advance. Japan started cashing out in August 2022, and by October, it had unloaded $132 billion in Treasury securities.

Since then, its holdings have zigzagged higher again, and remain in the historical range. In May they dipped to $1.097 trillion, down by 10.1% from a year ago:

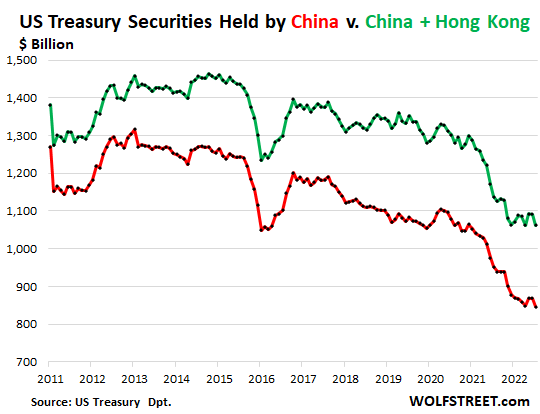

China has been unloading Treasuries for years. In May, its holdings of Treasuries fell to $847 billion, the lowest in the data going back to 2011 (red in the chart below), down by 11.0% from a year ago.

During the capital-flight panic in 2016, China sold Treasury securities to prop up the RMB. It then brought its holdings back to the declining trend. Since Covid, the decline of its holdings has accelerated.

China and Hong Kong can be looked at together (green). Hong Kong’s holdings increased by $30 billion year-over-year (+16.4%), while China’s holdings dropped by $105 billion (-11.0%) year-over-year. Their combined holdings fell by 6.6%, to $1.06 trillion, matching the prior low points in October and February:

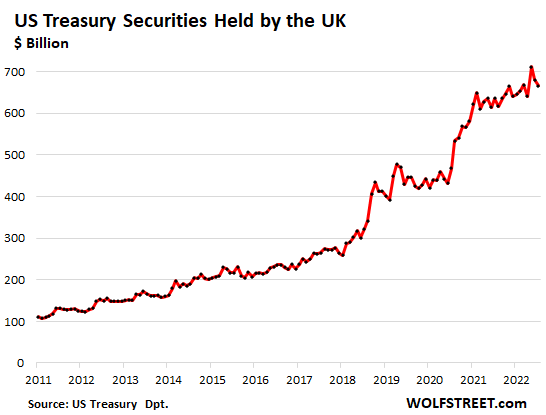

The UK, third largest foreign holder.

The City of London is a global financial center, so this isn’t the UK government or the Bank of England propping up US Treasuries, but it reflects activities of the financial center. Holdings had reached a new record in March, and have dipped for two months to $667 billion in May, up by 4.7% from a year ago:

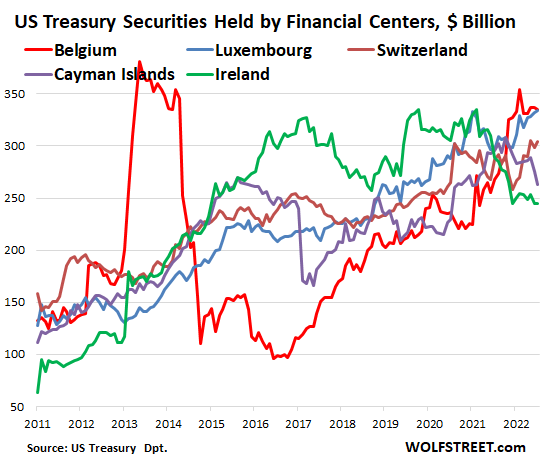

The financial centers. These are tiny countries that specialize in handling and often obscuring the financial holdings of global companies, individuals, and governments. And they have huge holdings of Treasury securities. Ireland is favorite place for US companies to store their profits and wealth:

- Belgium, red, (home of Euroclear): $335.5 billion

- Luxembourg: $334 billion

- Switzerland: $304 billion

- Cayman Islands: $263 billion

- Ireland: $245 billion

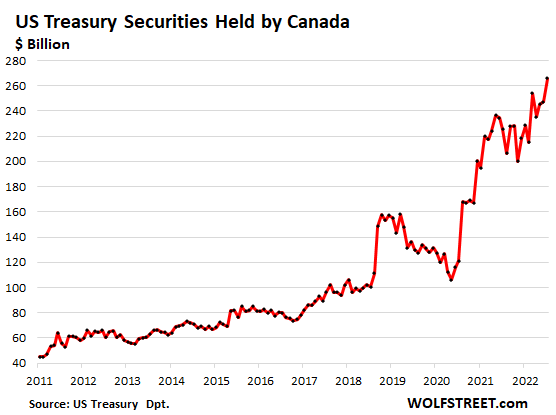

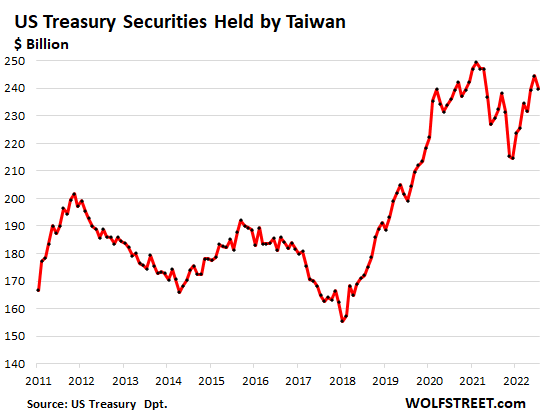

Other top foreign holders:

Canada’s holdings rose to a new record of $266 billion, up by 17.9% year-over-year:

Taiwan’s holdings dipped for the month to $240 billion, but were up 4.7% year-over-year:

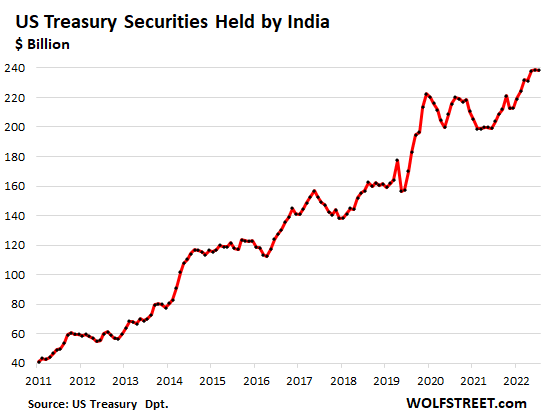

India’s holdings have been zigzagging higher for the entire period of the data going back to 2021, and for the last three months have been roughly flat at a record $238 billion, up by 17% year-over-year:

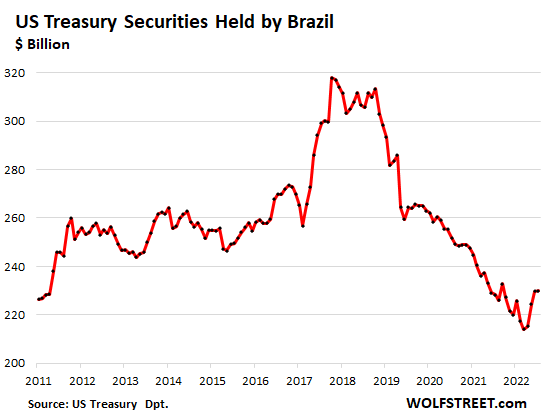

Brazil’s holdings, after dropping for years, bounced off the record low in January and in May rose to $230 billion, roughly unchanged from a year ago:

And there’s another thing that is important to keep our eyes on these days: US Dollar’s Status as Global Reserve Currency on Slow Long-Term Decline, but Not Going Down in a Straight Line

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

China do then have less ability to put pressure on the US dollar for political gain and private enteprises has increased their leverage on US politics.

The bankers have sent their representatives to the CCP, apparently to pledge loyalty, presumably so they will be protected, allowed to sell whatever CCP Ponzi shares they could not foist off on gullible US investors (as they foisted off sub prime securities before 2009), and not suffer losses as the shares of the CCP’s Ponzi companies circle the drain. The danger to the bankers and their golden goose, their not really “Federal” Reserve, will be when the US government can no longer pay its budgeted expenses and the increasing interest payments in rolled over treasuries. Only rapid, CCP, economic collapse might tame inflation before that happens.

If you think the U.S. will ever reach a point where they cannot pay their expenses, you do not understand how fiat currency works.

“For now, there is way too much demand for long-term Treasury securities, or else the 10-year yield wouldn’t be 3.8%, but 6.8%, and the 30-year yield would be further north.”

Absolutely. I have asked the same on another post of yours: why doesn’t the FED sell its long treasuries a bit faster? I got your answer Wolf of wanting to crash the market by this. No. A) the demand for long treasuries seems to be high B) the FED could reach its goal of reducing its balance sheet a bit faster C) the FED would act stronger against still high core inflation.

They’re terrified of “surprising the markets,” that’s why. And the markets know it, and that’s why the markets continue to laugh in their face.

Pea Sea, I love the Wall Street excuse machine. When markets rise, investors are “bargain seeking.” When markets fall, investors are “profit taking.” And, of course, the Fed doesn’t want to “surprise the markets.” For some reason, the markets are never surprised by swift and massive rate cuts, but I suppose that’s what the markets always expect.

On your mark, get set, trigger : when SPX will close above 4,600 the Fed will stop the drunken party. The countdown is over ==> Boom. The Fed is a party breaker.

China + HK might get back in pushing US 10Y below 3%, because Chinese

traders are sharper than Gundlach the bond king.

The Fed is a party breaker.==> this would never happen

I’m hoping the USA can change course a bit with the sanctions and confiscation of sovereign holdings over Ukraine and try to maintain trust so we don’t see countries lose faith and look elsewhere lowering demand.

Commenters on this site seem much more sophisticated than the average of sites on the internet. Still though, I think you are hoping that people can see the forest for the trees. They seem to have no inclination to do so. The foundation of our money is effected by what you are talking about but most people seem to think we can do whatever we want, no matter how illogical, forever.

Good point. The US has been pushing some countries to diversify out of the USD as a reserve currency as we used the USD as a weapon via sanctions to often?

Another facet of US dollar credibility is military credibility, a cornerstone of a world economic framework and order. And this stands alongside a “rule of law” financial system that perhaps paradoxically must sometimes, as the military must do, just stretch principles and inflict some wreckage as a demo. There’s nothing for effect of showing a fence works, like electrocuting something with it, or enforcing even outside it. Just wondering aloud ….

phleep – well said. (We’ve never honestly embraced ‘speaking softly’, but that ‘big stick’…).

may we all find a better day.

*now reached $33.5 trillion? Oversight?$ 32.5?

Yeah, I posted the same question just a moment ago.

“Trillion here, trillion there, pretty soon you’re talking real money.”

Used to be billion.

Used to be million.

Money printing is used to mitigate/obscure the perpetual policy failures of our political betters.

Yes, typo, thanks. It was late (for me).

Wolf,, if foreigners are holding less debt isn’t it good news? Reason then interest payment would go mostly inside our borders. Spending happens to be here

I don’t see it as good or bad news.

Debt by itself is never a good or bad thing. Neither is who holds it. One person’s liability (loan) is another person’s asset. Even when those loans are held by foreign entities it isn’t a big deal.

What is the old saying? If I owe a bank $1000 dollars then I am indebted to the bank and it has power over me. If I owe a bank millions, I have power over it.

Just sayin.

Wolf, may i know how much total 10 year treasuries are outstanding?

Marketable Treasury securities outstanding (held by public and intragovernmental holdings):

Bills (up to 1 year): $4.5 trillion

Notes (2-10 year): $13.7 trillion

Bonds (20 & 30 year): $4.2 trillion

TIPS: $1.9 trillion

Floating Rate Notes: $0.58 trillion

Why do you think the Fed didn’t term out it’s debt when rates were low?

Do you think they will have learned their lesson the next time around (unfortunately starting from a higher base)?

Thanks Wolf.

The simple reality is that only the dollar is liquid enough to carry the load of international trade. It’s ‘transaction value’ is 100%. No other monetary sovereign nation can haul the load. It’s in everyone’s best interest to keep the dollar stable. IMO the Treasury should ‘buy’ the debt, as is done in Japan. Keep more of it in-house. Based on the historical record, Japan has been good at maintaining a low interest rate–thus making it’s domestic commerce cheaper to maintain. If it wants to lower its holdings, all it needs to do is to ‘wipe off’ however much debt it wants to make disappear. Simple. With no effect whatsoever on Japan’s future ability to fund its spending.

The difference between Japan and USA is trade balance. The US trade deficit may make it difficult to keep the debt «in house» without importing inflation.

Actually, the debt and trade deficit will eventually show up as price inflation.

curious to hear from wolf why the treasury is primarily issuing bills as part of their recent market operations?

a couple days ago i looked at the upcoming issuance and there was something in the neighborhood of 180 billion short term and only 39 billion that was 2 year or longer.

is this because they dont want to drive long term borrowing costs higher?

are they afraid there is not enough demand for longer term debt?

or do they believe that interest rates will fall rapidly and therefore it is better not to lock in rates for a long duration, so it is better to pay the higher interest rate for a shorter time period?

Your last question is what I wonder. However, they could have gone long back when rates were really low, and they didn’t. Maybe they’re just stupid.

Note and bond auctions are scheduled well in advance. Bill and CMB auctions are much more flexible and can be announced on relatively short notice. Here is the tentative auction schedule from May through October:

https://home.treasury.gov/system/files/221/Tentative-Auction-Schedule.pdf

There are auctions all the time for longer-term notes and bonds. For example, last week, they had a 30-year bond auction. Today there was a 20-year bond auction ($12 billion). Tomorrow, there will be a 10-year auction. Next week, there will be auctions for 2-year, 5-year, and 7-year notes.

The Treasury will likely be increasing the size of the scheduled note and bond auctions starting in August. That’s the expectation.

A lot of the bill auctions just replace maturing bills, since they’re short term and are turning over all the time. They’re just refinancing auctions and don’t actually add to the debt.

The arbitrage must be gigantic…

foreign nations with low interest rates…(ie Japan) , converting to dollars then buying our higher interest paying debt.

Maybe that is the strength behind our ten year. (.5% to near 4% in the case of Japan)

And, of course, a support for the dollar due to the conversion into dollars.

A crowded trade to be sure….and what of the ‘unwind”? Weaker dollar, higher rates in US.

Pricing is relative. Ten year treasury rate around 4% doesn’t seem crazy when cap rates on many rentals are about 4%, dividends on utilities are about 4% and dividends on many blue chip stocks in the 3% range. I think if you average the earnings yield of the magnificent seven it is about 3%. Seems like you might as well stay in 5% cash til something breaks.

Exactly what I’m doing.

Very interesting that Canadians have bought so much.

Is this Canadians fleeing CAD?

Also: time for another Canadian housing bubble article please!

I have read that the Bank of Canada has dumped its gold holdings in recent years, so maybe it is replacing most of its gold holdings with US government bonds.

If so, they never should have taken lessons from the con men to the south on how to tell shit from shinola.

Dumped gold decades ago at around 400 per oz.

You may be right but where is the evidence for this statement?

feels to me like canadian government loves a good ponzi scheme

Meaningful price drops in Canadian real estate won’t show in most data until the end of this month

What do you think of what Ray Dalio says:

” With the enormous size of US debt assets and liabilities outstanding, plus lots more to come, there is a high risk that the supply of government debt will be much larger than the demand for it, which will cause too-high real interest rates for the markets and the economy, leading to debt and economic pain that will eventually lead the Federal Reserve to switch from raising interest rates and selling debt (QT) to lowering interest rates and buying debt (QE). This will lead real rates to fall, which will lead to a high risk that there will be more selling of debt assets because of the bad real returns that these debt assets are providing. While people are now not thinking about the next interest rate cut and QE of the Fed, we should because the timing of these is probably less than about a year away and that will have big effects. I think that there is a good chance that it will produce a big decline in the value of money. So, it looks likely to me that the financial/economic picture over the next year or two will be tough

“

I don’t think the Fed will publicly and visibly switch QT to QE. They have many ways to hide accomplishing the same thing, e.g., off-the-books swaps. Remember when they had BlackRock buying, through special purpose vehicles, stuff they were prevented from buying by law.

I want to know if the Fed is still paying 6% dividends to their commercial bank owners. Seeing that they have negative equity with their legacy bonds. Why aren’t the banks that own the Fed responsible for recapitalizing the insolvent Fed?

Agree. But I don’t think they’ll allow any real cleansing to take place. They’re willing to tolerate a mild recession, but not anything close to what is needed. If the choice is unemployment above 5% or more printing/ZIRP/bailouts and major inflation, they’ll pick the latter, every time.

joe2,

“hide” and “off the books” — nope. The corporate bond buying (managed by Blackrock, biggest bond fund manager) was disclosed on the Fed’s balance sheet every week, so it was “on the books,” with additional details provided in news releases and spreadsheets and reports to Congress, including amounts and company names and maturity dates, etc., and I reported on it in detail. There was nothing “hidden” or “off the books.” That’s just fabricated nonsense. They did have to set up fig-leaf legal entities that held the bonds, all of which was publicly disclosed and duly reported on right here.

It was a nasty thing to do, but it wasn’t hidden and off the books, but done in all its glory in full display. Public display of bond buying was a big part of how QE works… they hype it all the way, that they’re thinking about doing it, that they’re planning to do it, that they’re doing it, and each announcements is hugely hyped in the media.

Wolf, I was referring to currency swaps with foreign banks that are off-the-books as technically the value remains the same. During the monetary crisis it took an act of congress to find out the magnitude of the swaps which as I recall were in the trillions. I believe they were all finally settled.

What I would expect is the Fed to swap with a foreign bank which uses the dollars to buys Treasuries. It could all be well hidden. How would you know if they did not want you to know?

The BlackRock trick was just an example of how devious they can be.

But serious questions – are they still paying dividends to the owning commercial banks? Is their capitalization really negative? Do you know?

Currency swaps are disclosed on the balance sheet. You’re referring to the worst misreporting in Bloomberg (?) at the time — and not just on swaps but also loans, and other short-term instruments: someone added up all the deals. So a deal might mature in a week, and then get rolled over, and then get rolled over again, each for $1 billion, and someone added them all up and came up with $3 billion, when in fact the amount never exceeded $1 billion, it was the same $1 billion that got rolled over multiple times. In this manner they came up with $15 trillion over an 18-month time span, if I remember right. This was among the worst misreporting ever, and it has been debunked. But no one ever reads the debunks.

That is just crazy conspiracy talk not related to reality.

All of what happened with Blackrock was very publicly disclosed.

By definition the FED is not insolvent. Again, crazy talk.

What Dalio is saying is that holding fiat currency denominated debt is a losing investment all around. That doesn’t portend well for the longterm prospects of the fiat system.

I am not a Dalio fan but I agree with him.

Bottom line is: FED would do QE at the slightest excuse. Cash is not worth a lot. Just look at asset markets for last few decades. More QE coming.

FED needs to support Govt deficit and also support their wealthy masters.

People here thinks inflation s roaring high ( looking at last few articles here ). But FED and Govt ( who has control over policies ) think that inflation has been tamed.

Bottom line: FED won’t let true price discovery of everything including money happen. More QE coming if not in the very near future, then after year or two.

jon

“FED needs to support Govt deficit and also support their wealthy masters”

Look how many small countries, hedge funds, shadow banking in Cayman islands, Luxembourg ++ buying/holding the treasuries

In any kind of global financial distress, the demand for treasuries go up, mostly 10y. TINA. As Wolf has mentioned more than once, if there is no demand, the rate goes up to attract the buyers.As long as there is no default in interest payment, Govt can run on deficit and more debt. Of course the purchasing value of US$ will keep going down

“… the supply of government debt will be much larger than the demand for it,..”

I posed this question….What will the Fed do? Will they stand back and watch….and point the finger at the debt creation machine called Congress?

Or will they begin to buy to keep rates from exploding…..and any anticipation of a Fed balance sheet under $8 Trillion evaporates.

And now stocks up 8 days in a row and seem motivated by some unknown event or force. Where are the bad earnings?

It seems the markets and the economy are resilient in the face of 5%+ interest rates which begs two questions…

1. Are interest rates still too low?

2. Why in the world were we ever at 0% with real negative returns?

It seems there is still $4 Trillion too much money out there and the slow QT has had no effect.

The markets are resilient not because of 5% rates, but because they’re “forward looking” to a Fed pivot. They figure 5% rates as an alternative are good now, because they’ll be back to 0% next year, so might as well load up on stocks.

I’m not saying that that is true, but that’s what they’re banking on.

“…which will cause too-high real interest rates for the markets and the economy,”

Still waiting for it. Patience. 6.8% would be about right for the 10-year yield, not 3.8%.

In terms of the rest, it’s bond-fund and hedge-fund manager dreaming and book-talking. If the Fed lowers the rates and restarts QE while inflation is still hot, or even warm, you can expect wonderful fireworks of inflation to burst all over the scene again, and everyone knows this, including the Fed. Then markets and everyone will have a huge problem, because it will be truly run-away inflation. Dalio just talking his book.

Wonderful fireworks of inflation are coming anyway as soon as oil prices hit bottom and head north again.

I don’t know. I mean no offense towards Ray or people with Parkinson’s in general but it almost always affects cognitive abilities. He might be getting a bit off track with his tendency towards a sort of predictive model that is reductionist in essence. I didn’t know Ray ever and not 15 years ago, so I cannot compare.

re: ” US debt financing has become less dependent on foreign holders”

You’d then expect the U.S. $’s exchange rates to move in sympathy.

The contraction of the E-$ market has been going on since 2007. It was accelerated by Basel III’s LCR, and Sheila Bair’s assessment fees on foreign deposits, which changed the landscape of FBO regulations.

It helped make E-$ borrowing more expensive, less competitive with domestic banks (the exact opposite of the original impetus that made E-$ borrowing less expensive, when E-$ banks were not subject to interest rate ceilings, reserve requirements, or FDIC insurance premiums).

And now Powell has eliminated required reserves.

I think a lot of the smaller countries are using these US Dollar funds as a hedge against the devaluation of their own currency. Countries like Brazil will sell these to help stabilize their currency against devaluation if they need to.

“For now, there is way too much demand for long-term Treasury securities, or else the 10-year yield wouldn’t be 3.8%, but 6.8%, ” – the question is , can the Fed allow the yields to jump that high? How will it impact economy, mortgages, car loans, stocks?

Emil

vs the question is how high the Fed is ready to let inflation go higher?

My projection for a top in equities is the 5th seasonal inflection point on 7/21/23.

I think we should subtract the $5.1 trillion in “debt” that is held by the Fed and was purchased with printed money via the quantitative easing process.

Yes, the treasury originally borrowed the money in an arm’s length transaction. But as soon as the Fed went into the secondary markets and bought the debt back, the lender was paid back, and the borrowing characteristic was extinguished. It becomes purely arbitrary to characterize this “print and spend” as “borrow and spend”. This whole QE exercise is a kind of “intelligent design” rationale to explain Weirmar Republic economics.

QT is a process where the money is re-borrowed. But until that happens, I look at the debt as $28.4 trillion ($33.5t – $5.1t) and the percentages and so forth should be calculated using that number and not include this placeholder amounts that was simply printed up.

Yield apparently doesn’t solve all demand issues since the point of QE was specifically to reduce demand and yield.

No, the point was to increase demand and thus lower yield.

Thinking about it, the demand remains the same. They’re reducing the supply of debt available to borrowers while the demand remains constant, and that results in lower interest rates.

The process is sometimes called “yield control”.

“Weinmar Republic economics”.

LOL

Wolf, I wish more of your readers/posters lived under Weinmar Republic economics so they would be able to tell the difference between runaway inflation and mearly high inflation.

…and don’t forget the ‘whinemar’, ‘winemar’, and ‘weimaraner’ variants, as well as the original ‘Weimar’… :)

may we all find a better day.

Wolf,

I appreciate the effort and significance that such internationally oriented posts involve, and that comparative international productivity (as distinct from cross-national monetary manipulation) in the end means almost everything.

But the lede may be buried in these sort of posts, namely the fact that foreign buyers hold a *shrinking share of DC debt* (you do mention it, but only once, in the middle).

And how is this miracle (of illusory self-reliance) purchased?

By the Fed and its unmoored money.

Via the pitch-black magic of the MMT’ers, wherein ever engorged DC debt is fed by means of money-printing, and DC converts its self-induced problems (perpetual deficits) into the general public’s burden (inflation).

Foreigners have been fleeced once too often and recoil from payment in perpetually diluted scrip.

So the definitional patsy (the Fed) has to mop up the aftermath of the bumblers’ orgy.

At this point in National Decay, the latter is the bigger story.

The “lede” is in the second chart right near the top, which shows the share of foreign holders as percent of total US debt, and it has been declining.

So here it is again, because you seem to have missed it:

Foreign holders became less crucial. As the US debt has ballooned over the years, but foreign holdings have increased more slowly, the share of foreign holdings as a percent of the total federal debt has declined from the 33% range in 2014 to less than 24% in May. In other words, the US debt financing has become less dependent on foreign holders:

Wolf,

At what percentage of foreign ownership does this translate into higher rates due to supply/demand dynamics?

It might *never* translate into higher rates…that is the whole point of the Fed “We’ll eat anything” put.

1) Fed has power to print unlimited money at will, unanchored to any real assets existing/produced in/by the US.

2) This means that politically contaminated Fed can *always* buy *any* level of US Treasury debt, thereby determining “desired” interest rates. The Fed hasn’t paid attention to Federal deficits/debt levels for over 50 years – immunizing DC policy failures from their worst consequences.

3) But there are no diamond pooping unicorns in the real world. Increased money supply with far lagging real asset increase = empty inflation (with a lot of toxic consequences).

4) But, historically, they were DC deniable consequences…”Don’t blame us, insert private sector villain here.”

5) With the internet and the rise of non-uniparty media, inflation accountability is getting harder…but DC will give it a shot.

Lots of Americans are buying. Many of them right here in the comments. Also American institutional investors (pension funds, bond funds, insurers, etc.) And banks of course have loaded up on them — at the wrong time, as we now know. As long as yields are high enough, Americans have enough money to buy it all.

They might hafta sell some other stuff though. Dividend investors might finally sell their AT&T shares and switch to 10-year or 30-year Treasuries. Not the best deal, but at least you can sleep.

The problem is “if yields are high enough,” it will result in all kinds of other turmoil.

You need to also show the actual Treasury term issuance chart with this data. The dearth of long term treasury issuance is actually the more important story.

I would really like to see this data. If treasury is not issuing much mid and long term, that would imply that they expect the fed to relapse, just like so many others. Except in their case they might influence what lies ahead. If so, we outsiders could read their issuance profile as a predictor for future fed behavior. Let the speculation rage…

I have been wondering the same thing. Does the market take the sign that the Treasury is not issuing long term debt to mean that it thinks rates will fall?

I know that during COVID there were some people that said the Treasury should issue 30 year debt (or maybe it was longer), so that they could lock in very low interest rates. The Treasury didnt do that and now we have interest expense shooting off the charts for the budget.

It doesnt seem that the Treasury has the brightest minds at work.

Ample demand for USTs and if the demand falls off, FED would come in and FED can also be used to make money cheaper aka decreased yield.

This all means that US Govt can afford to run deficit. This also means that assets won’t go down and inflation can be controlled by manipulated govt metrics.

Exactly.

Are we trying to be Japanese at some point?

1/2 of Japanese-Treasury is owned by Japanese Central Bank.

We will beat them to that someday.

And it hasn’t had all the effects claimed by the proponents of this approach in the comments above.

Odd question to ask when the FED’S holdings of U.S. treasuries has been falling (sure, slower than I would like, but still).

About 15.6% of US Treasuries are held by the Fed.

The Fed has shed $690 billion in Treasuries since April 2022. At the same time, the US government debt has increased by $2.2 trillion.

So the percentage of the US debt held by the Fed dropped from 19% in April 2022 to 15.6% now, going in the opposite direction of Japan.

And 20% is held by the Federal Reserve, which is captive to their own debt policies so that percentage can easily rise to soak up supply.

I agree.

FED balance sheet would definitely increase over time. Just look at the long term trend.

Some people here are happy and excited that FED has fasted hikes and is doing QT. For these people, I ‘d say: You are missing the forest for trees.

Inflation would be side effects of this but it can be easily manipulated via many metrics.

Big Picture: Increasing FED balance sheet and devaluation of USD over time.

I meant fastest hikes.

A person has to be to pretty much ignorant of reality to say that the FED’S balance sheet is increasing, let alone the dollar is being devalued.

Howdy Folks, we are just months into higher for longer. Gotta wait awhile longer……

First or second quarter of 2024 is when the landing might finally occur, as the last remnants of the Covid trillions leave consumer hands over the 2023 holidays to nest in the balance sheets of businesses and banks. There could be a big drunken sailor hangover in 2024, but it will be buffered by all of the Covid bucks still sitting on balance sheets in the Wall Street economy.

Howdy Occam, YEP, long way to go. Debt clock is flying high at Ludicrous Speed……

MW: Carvana’s stock has roared back from the brink. This chart shows its meteoric surge.

CVNA 40.20%

Can-kicking extraordinaire! They are issuing a boatload of new stock, diluting current equity holders by something like 13%, while using the proceeds to pay off loans maturing in 2025.

From a Seeking alpha article:

“It is worth noting that the firm is obligated to repurchase its 2025 principal outstanding through cash raised from this new equity issuance and that is obligated to issue at least $350M in new shares to accomplish this.”

They still have a few years to reach the Bed, Bath, and Beyond death spiral where they’re issuing new equity just to pay off the interest on their debt.

I wouldn’t say that Japan “blew” $68 billion defending the yen when the the yen is now in the 139 – 141 area.

It looks like to me that they not only defended the yen, but made a profit on it as well.

And speaking of profits the Japanese must have a huge capital gain on their holdings of US debt holdings when converted back to yen

Their interest income in yen terms on that US debt also increased in yen terms too.

So it makes/made sense to sell some of those US dollar demo.ated debt instruments and repatriat the funds back to Japan.

These facts can be seen in the latest financial data released which showed them having the biggest balance of payments surplus since around 1985… all due to foreign income….

Wolf, can’t the long term interest rate stay low without a large demand for the treasuries? The elephant in the room is that the Federal Reserve can start buying massive quantities of treasuries (Quantitative Easing – QE) anytime they want; so take or leave what the Federal offers. Also, producing asset bubbles everywhere nakes the Federal Reserve the only game in town.

If the Fed starts buying that is demand. Yields go down if there is more demand, and they go up if there is less demand.

Who needs foreign countries when you have the Fed? At the end the Fed can remit the interest payments and principal back to Treasury.

What’s that I hear? It’s a Ponzi? Have you heard about this thing called Bitcoin? Call 1 800 BITCOIN now to learn about how you can preserve your wealth!!!

“Stock prices have reached what looks like a permanently high plateau”