And yet, the Pandemic Money is long gone.

By Wolf Richter for WOLF STREET.

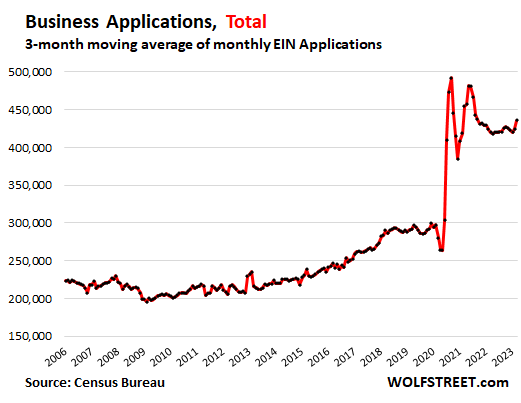

New business formations in March, based on applications for a federal Employer Identification Number (EIN) with the IRS, jumped by 4.5% from February, by 10% from the already high levels a year ago, and by 50% from March 2019, according to the Census Bureau today.

The three-month moving average, which irons out some of the month-to-month ups and downs, rose by 3.7% from a year ago, and by 50% from the same period in 2019.

The astounding thing: This is still going on! During the pandemic, the extra money the government was handing out served as startup capital, and with lots of people having lost their jobs, the creation of new businesses exploded. But now all this is gone, and business formations are still 50% higher than they were before the pandemic, and they’re surging again.

Note: You do not need an EIN to be self-employed or to start a business that doesn’t have employees; your Social Security number is enough. You did not need an EIN to get PPP loans; a Social Security number was enough. A business needs an EIN if it pays regular employees, if it is a corporation or partnership, and for some other purposes (trusts, estates, etc.).

EIN applications for trusts, estates, tax liens, etc. are removed from this data. This data here covers only EIN applications for typical businesses.

The big wave since 2020.

Between January 2020 and March 2023, a gigantic 16.1 million businesses were started – testimony of the large-scale changes in the economy that have occurred during the pandemic.

Not all of these businesses are still here today. Some were bought out, others folded because the owner found something better to do. That’s always the case. But the surge in new business creation is still an amazing sight.

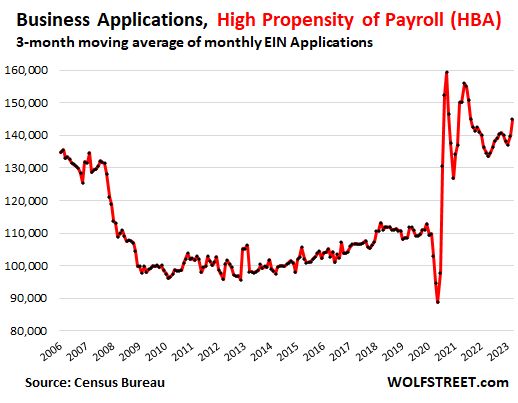

Businesses with “High-Propensity of Planned Wages”: one-third of total.

The Census Bureau categorizes businesses with a high likelihood of creating a significant payroll as “High-Propensity of Planned Wages” business applications (HBA), based on the information in the EIN application. About one-third of all EIN applications have been HBAs.

In March, the HBA applications rose to 150,169. The three-month moving average rose to 144,911, up by 7.6% year-over-year and up by 33% from the same period in 2019:

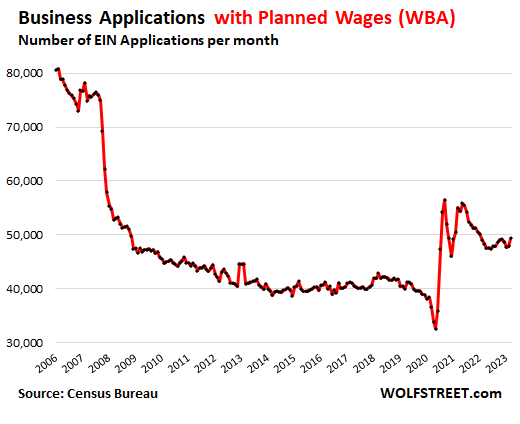

Businesses with “Planned Wages”: 10% of total.

“Business Applications with Planned Wages” (WBA) are a subgroup within the HBAs. They’re businesses that indicated on their EIN applications a date for their first payroll. They have funding to meet that payroll, and they’re ready to hire and pay wages. These businesses are most likely to grow their payroll and become significant employers. Only about 10% of EIN applications fall into this category.

In March, the WBA applications rose to 49,424 (three-month moving average), up by 2.2% year-over-year and up by 24% from the same period in 2019.

But this is far lower than in the years before 2008:

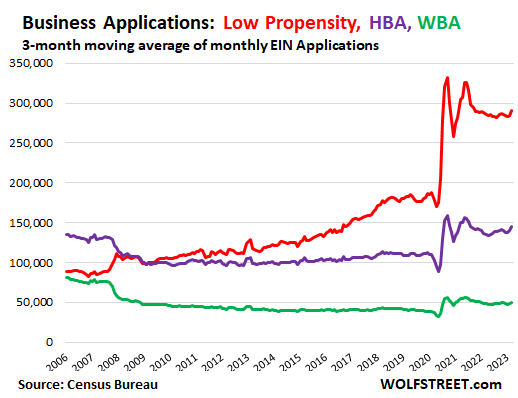

Businesses with a low propensity to become significant job creators: 67% of total.

About two-thirds of the EIN applications are for businesses deemed to have a low propensity to become significant job creators: 291,114 of these businesses were created in March (three-month moving average), according to the EIN applications. This was up by 59% from 2019!

EIN applications by businesses with a low propensity to create jobs were already on fire in the years before the pandemic. But it just exploded during the pandemic (red line in the chart below).

Since January 2020, over 10.7 million of these businesses have been created. Many of them end up employing only their owners – entrepreneurs chasing after their dream without VC funding, flying their operations on a wing and a prayer from day one.

But applications by businesses with planned wages (WBAs) fell off a cliff during the Financial Crisis and then languished for years at those low levels. During the pandemic, applications surged but didn’t return to those pre-Financial Crisis levels (green line).

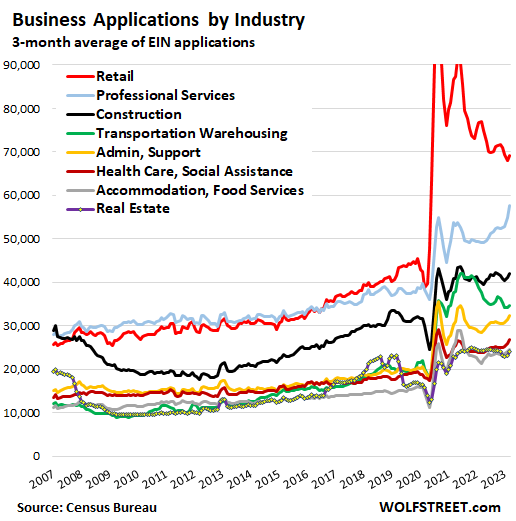

EIN applications by biggest categories.

Details below the chart:

Applications by retail businesses, mostly ecommerce, (red) blew through the roof during the pandemic when many brick-and-mortar retailers were shut down. People were trying to sell anything from specialty cosmetics to tools. They could use platforms, such as Amazon, and their fulfillment and delivery networks, for a quick way to get something going. But it’s dog-eat-dog on the internet, and results may vary.

In March, the three-month moving average of EIN applications for retail businesses rose to 69,136; while still a huge number, and still up by 66% from the same period in 2019, it was down 10% year-over-year, and down by 34% from the stunning peak in the summer of 2020.

Applications by professional services businesses (light blue) have been surging recently from record to record, to 57,722 in March, up by 17% from a year ago, and by 53% from 2019. This includes law firms, IT businesses, engineering firms, etc.

Construction (black): 42,002; +5.0% yoy, +27% from 2019.

Transportation & warehousing (green), much of it likely related to ecommerce delivery: 34,710; -7.6% yoy; +76% from 2019.

Administration and support (yellow): 30,407; +14% yoy, +66% from 2019.

Healthcare & Social Assistance (maroon): 26,861; +13% yoy, +50% from 2019.

Accommodation and food services (gray): 24,460; +14% yoy, +39% from 2019.

Real Estate (purple line with dots): 24,179; -1% yoy, +4% from 2019.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Only thing I can figure is that people suddenly have a bunch of money and are like ya know what I can be my own boss let’s start a business.

Could be a better money burning mechanism then qt

What people?

The people starting businesses….

Not something you do unless you feel some what financially secure

Or unless, say, you can’t afford child care and commute for one spouse, so why not have the at-home one do an Amazon selling gig?

Or you really just hated your last job (and maybe last X jobs) and are deluded about your ability to support yourself as boss in a new start-up since credit tightening has not yet caught up with you. Retail and professional may be categories that have experienced a high aggregate number of layoffs or quits all over the country unnoticed or just unrecorded by the data collectors. If so, once these new business/I’ll-be-boss tries wear thin, more than a few of these aspiring entrepeneurs will be back in the job-seeker category, like it or not.

Does the retail include the drop-shipping craze that many young people have been trying for the last few years?

Or maybe life is now about finding a way to build cash flow that cannot be cancelled and thus ruin your life at any moment in time. How can you build a stable life when the boss can walk in and cancel you by giving you job to his ne son in law? Or the government saying you are non essential?

When a Chinese man finds a grain of rice on the road, he opens a restaurant.

A robust labor force creates a thriving economy, who would have guessed! I hope everybody is ready for the next bull market. Years that end in 3 are always great. My advice: get in now, don’t wait!

This means higher inflation for longer, and higher interest rates for longer, and QT for longer. How are you going get a bull market when stocks needed HUGE QE and near-0% interest to get where they got in 2021???

I’m happy to wait it out and DCA. Lots of beat up growth that feared what rising interest rates could do but hasn’t done yet. Or for the more simple minded, a blend of SPY/SCHD will do fine.

The only way bad times materialize is with the labor market tanking yet it seems inflation is losing that fight. If you can make money in this economy, do it!! My first job in 09 was dreadfully hard to find. The labor force chart you post points to the economy having more room to run, more room to stay invigorated and hopefully with the help of technology, finds a way to balance itself with deflationary forces

“only way bad times materialize is with the labor market tanking”

That wasn’t the sequence in 2008.

Phonied up asset values (due to G interest rate strangulation/money printing) are more than enough to tank an economy when asset values return to reality/implode.

*Then* labor collapse occurs.

Defrauding people creates phony growth because they are deceived and act over-optimistically. When they wake up, they reverse their behavior.

The “wealth effect” cuts both ways.

@Cas127

If your bear case hinges on asset values falling, you’ve already lost. There will be no price decline. The devaluing of the dollar will balance out any ‘overpriced’ notions, and of course the economy (which doesn’t care about price anyway) will continue trekking along.

Mkt was at least 40% overvalued circa Nov 2021…likely still 20%+ overvalued. We’ll see what happens during another huge leg down.

And abnormally small “for sale” SFH inventories (like 65% of 2019 normal) is the only thing keeping home prices from a 2008 like collapse (SFH sales volumes *are already* down 33%…try getting 2021 prices selling into *that*…).

Assets were overvalued when 1 yr interest rates were 0% (for yrs and yrs). The overvaluations are much worse now that rates have soared (ie, finally been allow to approximate something like a natural level).

And “AppleTrader”, Apple is an excellent example. With a PE ratio of 25-30, it is valued like some hyper-growth new IPO with virgin fields…not an enormous incumbent that has BS’ed the world into paying for hundreds of millions of vastly overpriced cell phones (Apple $800, Android $20-$80) for many, many years…where is the incremental growth implied by a huge 30 PE supposed to come from…a newly discovered planet?

Financial projections are about weighing the probabilities of what is likely to happen…to be a bull when faced with these headwinds, you have to believe the most, in the least likely things.

The economy has been mostly fake since 2009. Or perhaps you didn’t know that? It still is now. Already a $1.1T deficit and the fiscal year is only half over. Monetary policy is still very loose.

@Cas127

Oh boy.. home sales being down must mean bears are right huh? Forget the fact that 99% of buyers have sub 6% mortgages and 0 interest in selling (yours truly included). Maybe low volume will in fact lead to higher home prices, then. Either way it won’t affect my situation one bit as I value my home on a use-basis not what the market says

I always laugh hearing the same bear case about Apple too. Yes, very overpriced, surely it will collapse. Never mind the fact it leads the two most popular indexes of the most productive country in the world, or is 40% of the most successful investor of all time’s portfolio. Who would dare pay $800 for a phone! Madness

It’s a silly argument because they cash flow so much they don’t even know what to do with it. So they buy back billions, grow the dividend at double digits and continue creating the perfect product LOL (fyi my first iPhone purchase was three years ago and I regret not getting one sooner). Androids are trash and always will be. iOS is simply too smooth

Either way I reiterate my original point: if the labor market remains tight as I expect it to, we will head not into any doomer’s fantasy but in fact the next bull market. We’ll see you there!

Record low unemployment rates plus a spike in small and micro business formations equals the tightest US labor market most of us have ever seen. Add to that very large federal deficits, a Fed rate that remains negative in real terms and trillions of Covid bucks ricocheting through the domestic economy, and a Fed pause at 525 basis points is likely to trigger a big Wall Street rally, loosening financial conditions and accelerating inflation. SVB and similar bank wobbles are in the rear view window already and so no contractionary help there. Accelerated QT could blow up long rates and so let’s hope the Fed’s bag of tricks isn’t empty when the commercial real estate market blows up and the Fed wants to print another trillion or two. That just might trigger a loss in confidence in the dollar that could make things highly unstable.

“equals the tightest US labor market most of us have ever seen.”

25-to-54 (prime age) employment-to-population ratio still below late 90’s peak. More broadly, labor force participation ditto.

You misunderstand “tight labor market.” It’s defined by not enough people actively looking for a job in relationship to employers looking to fill jobs. The Labor force participation rate measures people who are actively looking for a job or already have a job. When the participation rate is relatively low, it’s a CAUSE of the “tight labor market.”

In or their words, how can we get a bull market going again, unless we can rig the system in favor of the oligarchs, by sucking up all the wealth to the few at the top.

This comment, In My Humble Opinion, is worth 10 years of subscription cost… Oh wait a minute, it’s free.

Pure wisdom dispensed daily. Pure unadulterated, truth focused, continuously educational, open forum moderated by a genius whose passion is finance with tolerance of dissent and intolerance of untruth.

Get a Green Tea mug.

For financial success, Wolfstreet is necessary and sufficient.

Perhaps the bull market is planting its seeds on main street, and it’s called near-shoring, re-shoring and friend-shoring and all the spin-offs it supports. The commercial forces that link the US, Germany and China are setting up operations inside the North American trading bloc.

I have clients who were old enough to retire from corporate world.

Become their own boss. Experienced, decision making, and capable of completing a project without a “stress day” In a time of raging service inflation.

Not very surprising.

The big money went to PPP, which went to businesses, so people are preparing.

Lets say Steve Jobs started fooling around with a few circuit boards in his garage today instead of 40 years ago. He would have begun as a “business with Low Propensity to become significant job creators”. Today there is AI, the metaverse, DNA technologies, renewable energy, etc. What will the future bring?

Nothing good… unless one is an out of work pre-cog looking for warm digs inside a wading pool.

So two out of the three above categories would apply, am I right?

Wolf. Please don’t send out the spiders on my poor a$$, ok

Steve Jobs was a visionary, not an engineer. He had an engineer as a co founder.

Interesting article that articulates an anomaly from the business practices of the last two decades, which only history will be able too judge. But today and tomorrow is a result.

The conundrum between the ask and the bid has created uncertainty, a crack in the edifice of monetary control created and established by our favorite public servants, the so called Federal Bank of the United States of America.

I think of the conflicting projections of the likely economic outcomes as extremely interesting because I haven’t a clue while required to appear as if I do.

Nationwide monetary or social experiments are difficult too unwind. Especially in this period of institutionalized prejudicial prosecution. “The rich are different than you and me,”, from the Great Gatsby by F Scott Fitzgerald.

I suspect a very large group of “middle” class people banked enough during the pandemic cash give away – coupled with a tight labor market that allows easy reentry to the job market – that it inspired many people to start their own businesses. Maybe a new economic policy for the future.

Yet new business needs to borrow for the building and working capital. And borrow at higher rates from shrinking liquidity. I guess the rates are not high enough to be a deterrent. Plus, business is not too worried about charging higher prices. Indeed the Board(s) will wonder why a Company isn’t raising prices. I mean we all expect higher prices and that expectation is the catalyst for more inflation. I am no expert but it sure feels like “keeping up with the Jones” is something Humans really desire. So spend spend spend. Also, I noticed, after preparing a lot of tax returns, that Seniors have a lot of money. It pays tuition for Children and Grandchildren. Whole families move back into their Parent’s oversized homes. Money is inherited. So perhaps the whole 401k/403b thing has turned out to be an inflationary accelerator. Mostly due to timing with all the big stimuli. But it is a contributor. Very interesting that new businesses are increasing. I hope they are not just LLCs within LLCs so people can cheat. Too much of that. Thanks for the topic.

A lot of people create business entities for “side-hustles”. Selling things on online market places, contracting out time as a delivery driver, renting out those condos, or just managing one. As a corporation, it has never been easier to exploit people into holding the bag for depreciating assets.

I am not sure if it signals lucre or distress. Everyone thinks of starting a business when they’re underemployed. Don’t want to rain on any ones parade.

“Everyone thinks of starting a business when they’re underemployed.”

Misconception here?

“Everyone?” No. Lots of people when they’re underemployed think about getting a second or bigger job, not starting their own business.

I started my own business — the Wolf Street media mogul empire – because I wanted to be passionate about how I make my living, I wanted to create something, I wanted to love working. I didn’t want to waste my time doing stuff I didn’t like doing and counting days till retirement. Best job I’ve ever had. Worst boss I’ve ever had too, LOL

I agree. I’ve known many who are desperate and think starting their own business is their only hope. Sure, there are some like Wolf who have a passion, but many others are desperate. Some are desperate to get away from abusive bosses, some desperately need money. And there are those who are desperate plus have a passion. I dont necessarily see this as a sign of confidence in the economy or a sign of financial security except for the 10% planned wages group and maybe a few out of the other groups.

Ali Baba-to-Amazon “retail arbitrage” is today’s version of the 1970’s Avon Lady.

And those Avon Ladies had huge churn and were very, very frequently incremental (not primary) incomes.

Better than nothing, but not the Dawn of a New Economic Millenium either.

Cas127,

Where does your silly and disparaging attitude about small businesses and small startups come from? That small businesses are either just dabbling in it unsuccessfully or are phonies and frauds? I deleted a couple of your comments and that of a few others to that effect… those comments are just insulting to people who are getting off their butts to do something on their own, on their own gumption and initiative and courage, and taking risks in order to succeed.

I know several people who struck out on their own successfully — though it took a lot of work and time: lawyers, an event organizer, investment advisors, insurance agency owner, etc., and none of them fall into your stupid categories of phonies and frauds that you mentioned in your other comments. That BS just insulting to us small business people.

“Where does your silly and disparaging attitude about small businesses and small startups come from? That small businesses are either just dabbling in it unsuccessfully or are phonies and frauds?”

Probably from taking a look around? There really are a lot of “businesses” that do exactly the sort of thing Cas127 accuses them of. The fact that they had to get off their asses to do it doesn’t make the drop shipping arbitrage business model any less frivolous.

@Wolf,

Roughly 50% of all IRS audits were targeted at people making under $25K./yr Who the IRS decides to audit clearly indicates that some comments that were deleted are not fabricated. The “fraud strategy” of generating “earned” income starts to peter out once people make $36K or more a year in income, but it is definitely real, unless you think the IRS only applies audits for BS reasons.

JeffD,

This has NOTHING to do with EIN numbers. How you twist something like this into utter BS just drives me nuts. The people who claim the anti-poverty earned income tax credit — the poor people who get audited because they got a letter from the IRS that asks for info and they failed to reply — have part-time or full-time low-paying jobs with W-2s using their SS#, or they have gig work, and are getting 1099s with their SS#. This has zero to do with EINs. To claim that this poverty tax credit for regular workers and gig workers inflates the EIN data is just fabricated BS.

My answer is people tired of corporate bullshit,get laid off again . Opening a business on America is very lucrative everything is a tax write off .Just very hard to be successful.I retired when coworkers could go cry to HR ,when trying to teach a guy how not to get killed,wouldn’t listen after 3 times yelled at him .Now my brothers manager got fired didn’t talk to people right .This country is toast.I’m. Boomer got yelled at plenty of times in construction field ,usually deserved it ,pull up your big boy pants go back to work

“I’m. Boomer”

You don’t say.

Flea

Great comment. I got fired from all 3 of the true “career” jobs I had. Always the same reason: You get unbelievable results but you don’t follow the social norms of the office (don’t go to happy hours with co-workers, not seen as a “team” player etc). In the last job I had (age 50), as an effort to be more “teamy,” I bought little dinosaur trinkets, gave them to my workmates and nicknamed everyone with a dinosaur name (e.g. Nickasaurus or Joleen-adactyle) – including myself (I let them pick my name) – got fired (let go during probation period) because of it. F*** em. Have 4 LLCs for my business pursuits now and like Wolf’s biz – the boss sucks, but the end result is waaaaay more satisfying. ;-)

Work from homer’s starting small businesses and gig’s on the side as the boss is no longer watching over your shoulder all the time maybe?

[Not that this is bad at all, but perhaps in this way, WFH has become a sort of business incubator of some sorts giving people the ability to realize business ideas they always had?]

…but critical to embrace a Heinlein aphorism:

“…self-deception is the root of all evil…”

may we all find a better day.

I would think businesses should actually be happy under normal circumstances to hire a self employed individual vs putting one on payroll. They no longer would have to worry about SS, payroll taxes, healthcare, benefits, lawsuits, unemployment, insurance etc

Just a more cost effective “work from home” model.

No office,no coffee

As always, new business development is fueled by first generation Americans. That fact never changes. It is still, after all, the land of opportunity.

100%. This retiring generation also makes it very easy for an inmigrant thats shows even the sligtest hard working attitude and grit to be employed, because they want to retire ASAP!

Wolf, can you reconcile:

“Note: You do not need an EIN to be self-employed or to start a business that doesn’t have employees; your Social Security number is enough.”

And then when talking about the low propensity businesses to create job businesses you say: “Many of them end up employing only their owners – entrepreneurs chasing after their dream without VC funding, flying their operations on a wing and a prayer from day one.”

Are people proactively creating an EIN in case they make it big but most never? I suspect that there are tax breaks or some other difference between creating a business with and without an EIN no?

“Are people proactively creating an EIN in case they make it big but most never? I suspect that there are tax breaks or some other difference between creating a business with and without an EIN no?”

No, there’s no need to proactively create an EIN because they can be issued almost immediately when needed by the IRS.

An EIN is simply an identification number, like a social security number. It makes no difference in terms of taxes which are dictated by the business’s filing status: Schedule C (sole proprietor), partnership, C or S corporation. Some sole proprietors prefer to use an EIN rather than use their SSN for privacy purposes. For example, if a sole proprietor provides services for which other businesses need to issue them a 1099, they can use an EIN rather than disclose their SSN to the issuer of the 1099.

You need an EIN if you want to pay yourself regular W-2 wages. You need an EIN if your company is a corporation or partnership, no matter how small.

And yes, lots of entrepreneurs hope that their business will get bigger and employ people.

EIN is also a way to show people that you are a legitimate business.

I think most banks like you to have an EIN to create a business checking/savings account. Pretty necessary have if you want to keep your business and personal finances separate.

OTH

Agreed – it’s also one more layer of liability protection. If you end up in a court battle and payments were NOT tied to your SS number – it shows intent.

It can be beneficial to have an EIN and not use your SS#. Keeps things a bit ore separated.

Exactly.

Having to give out your real SS# to anyone you are doing work for that will cut you a 1099 is not desired.

You also need an EIN if you hire a nanny and use a payroll service. Have some higher income clients getting an EIN for this purpose, although I’m sure it’s a tiny fraction of the total.

“The 10-year US Treasury note yield, seen as a proxy for borrowing costs worldwide, consolidated above 3.5% on expectations of further rate hikes by the Fed.”

RE shillers are steaming mad. Inflation is here to stay high for a while.

It will be unfair to give the savers zero percent on their savings while the speculators get interest-free loans to create stonks and real estate bubbles.

One of our business areas is providing services to newly created businesses, US is a major market

During 2020-2021 there was a huge boost in demand. We even had to double our prices to reduce it. Did not helped much:)

In 2022 demand was back to normal levels. Prices are back to 2019 levels.

Since 3rd quarter of 2022 until now- demand is way below normal level.

Either our services are no longer needed, or new companies creation has some other purposes than starting an actual business activity.

LOL. Working from home in Spain, and losing business in the US? You said in a comment in 2017 that you came to Barcelona as a tourist and stayed. And now your IP address is still in Spain, and you’re losing business in the US? That’s how it goes if you’re more focused on having a good time. Maybe your company lost the edge, or has competition in the US that you cannot figure out because you’re spending your time enjoying Spain? Maybe you should do some serious navel-gazing WHY your company is losing business in the US?

…SWOT analyses conducted regularly, frequently, and vigorously…(…aka Wolf’s ‘worst boss’…).

may we all find a better day.

Spain is nice, like to spend time here. Good for health as well.

Our company has WFH / work from anywhere policy for more than 10 years. If needed can work for 14 hours a day with some breaks for food and sleep, same as other team members. Physical location doesn’t matter much

if there is an urgent task in to do list.

We use this side of business (services for new companies) as a proxy for our main adtech niche. Have been a very good indicator. At least our numbers from this proxy indicate a serious slowdown soon, but so far don’t see it in the main niche.

Guessing rojogrande’s point about 1099’s is a big factor. With the IRS imposing the $600 dollar transaction reporting requirement a single person LLC really needs an EIN. With inflation single person businesses would be handing out their SS# all over town especially trades people or landscapers. It used to be easy to get a second job but that has changed. Anyone old enough to have worked in the 80’s or 90’s will remember entry level fast food, delivery or grocery store jobs where you could put right on the application that you were a student, only have part time availability and the days/hours you could work and actually get hired. There were also a lot more fluff jobs were you were essentially a warm body watching the place during slow hours on a register or reasonably paced jobs like night stocking, night janitor, etc. Those jobs barely exist now. Part time employers now want full time availability, you show up when they want you, you better tolerate your hours being unpredictable and make sure you have enough extra energy to cover when other folks don’t show up. Your part time extra job could have you unloading a semi trailer by yourself for some retail business and not able to go home until it’s done because you are the only one who showed up. There are better part time jobs that make decent side gigs but good luck getting one. If the job is decent it’s a rare gem, turnover is probably low and a lot of folks want it. I believe that is driving a lot of folks to make their own jobs just to control the work pace and hours even though all the taxes and paperwork is such a nightmare. Also a lot of services have been popping up that are more affordable and help with all the confusing tax and other requirements for a monthly fee. There are also businesses that are essentially acting as an umbrella for that stuff and the workers are less like a typical staff and more like a bunch of independent contractors using the same billing, customer service and paperwork processing center. I’d have to look at this stuff to be sure, but I think these outfits make it possible for the workers to be 1099 contractors but the customers don’t have to do the paperwork because the umbrella runs as a corp.

Excellent summary, MM!

I’ve worked with mostly start-ups since the late 1970s and my best clients were retired executives or retired officers from the military.

I concur with this viewpoint, and find it funny that everything you describe goes against the “booming” economy the media keeps harping about. And this has been the case since at least 2008. Its remarkable how people can separate the wheat from the chaff. Esp. websites that claim expertise in it.

“…everything you describe goes against the “booming” economy..”

no, what he describes is the horrendous abuse of people working in service jobs in food-services and accommodation businesses (restaurants, hotels, etc.)

And these industries have been complaining about labor shortages because people have left in large numbers, or refuse to work there, because there are jobs out there for them in this tight labor market that offer better hours, better working conditions, and higher pay. That’s the benefit of a tight labor market.

How many new businesses actually manufacture products? “Business” as it’s practiced in the US now is just shuffling paper, reselling stuff, moving things, taking care of sick people, kids or old people, or doing gardening. Not that these are bad things to do, but they are hardly the activities that make a nation strong and prosperous.

The country / region that has the lowest ‘service’ sector as a percent of GDP is Sudan. The highest is Macao, just outside Hong Kong.

Pretty sure I know which one of these I’d attach my little wagon to.

I think the opening of so many businesses is due to a lot of money in the economy and people’s bad memories of the economy being closed due to COVID. Now people try to be their own boss and not depend on other people. But still QT and high interest rates will affect demand sooner or later and many of these small businesses will close. I think it’s the momentum created by the easy money, but that will change.

In my field (VC backed tech start up) the average tenure is 2-3 years. Eventually you’re on same-gig-different-company #5 in 10 years or so. And with remote work, you’re in the same office, same chair – you’re just logging into a different email.

Many people go do their own thing around that point. Sometimes in tech, sometimes not.

QQQ with the cloud for fun and entertainment, skip :

1) T is the highest high minus the lowest low of the last 9 TD (bars) divided by 2.

Today T will lose it’s Apr high. T might fall unless today will rise above Apr 4 high.

2) K is equilibrium. K is the highest high minus the lowest low in the last

26 TD (bars) divided by 2. From tomorrow K will lose 13 lows, since Mar 13 low. K will rise. The wide space between T&K clamps will narrow, unless

QQQ rise at the same pace. If QQQ fall T&K will flip : bearish.

3) A red flatbed is equilibrium, a magnet to price. QQQ is above the cloud, bullish. The cloud is green, bullish. Chikou, the lagging line, is above price, bullish.

Price is high > the cloud, bearish. Price is high > equilibrium, bearish.

The front end of the cloud, Senko A, the green line, might tilt down if QQQ

fail to exceed Apr high, bearish.

4) The cloud front end is a green, narrow neck, easy to penetrate.

5) QQQ backbone : Jan 25 2021 hi/lo, 330.32/321.41. Apr high @321.63 was an UT. In order to move up QQQ must breach BB.

6) 1Week : In order to move up QQQ must close Aug 15/22 2022 gap, inside

the BB. If it can it might reach Aug 15 fractal zone.

7) 1Month : In order to move up QQQ must have a monthly close > Aug

2022 high.

8) 1Month : If fail, Apr 2023 high might send QQQ down, at least for a while, possibly for a sling shot up, under Mar 2022 low, to help the regional banks.

Frankly this is not surprising. The debt investment financing in the past decades was friendly to anyone with money but not accessible for those without. Tax structure prevented the accumulation of seed funds making matters worse. The injection of a heap of money directly during pandemic helped small actors to take the first step.

So what’s the path to lending for these companies? Which ones are going to suffer if credit tightens? I could guess that the largest growth in retail will suffer the most in a recession, PPP is gone (but not forgotten)

The big threat to small businesses is loss of revenues, or insufficient revenues, or not being able to get revenues quick enough when they start their businesses – customers/clients cutting back, or competitors knocking you out of the game, or not letting you get that first foothold, etc.

Credit tightening is not the big threat because most small startup businesses cannot borrow much in the first place. Everyone knows that small businesses are mostly equity-funded, and “sweat-equity funded,” not debt-funded, because they’re having trouble borrowing – if they’re crazy enough to even try.

None of the small businesses that I know personally have ANY debt. Credit tightening won’t affect them at all. But a loss of revenues or insufficient revenues will damage or kill them.

Sure, the entrepreneurs can run up their personal credit cards, hoping that they will get the cash flow to pay them down, but that’s a losing game, and most entrepreneurs know that.

Lots of small businesses today have zero inventory and just some basic equipment. A laptop is all many of them need to start with. They may have receivables of two to three months revenues, so their working capital requirements are fairly small.

Some period of building “sweat equity” – working without pay while getting the company off the ground – solves that working capital problem. As the company accumulates working capital, and puts aside a cushion, the entrepreneur can start taking some money out. That’s how that works unless you have VC funding.

That’s why it’s so important when you start a business that you don’t need the income right away, that you can live without income for a while until the company generates big enough cash flows.

If you want to start a capital-intensive company, say in construction where you need lots of equipment and employees right off the start, you will need funding. You can lease the equipment, but you have to pay your people, and you may have to wait for a while before your company gets paid. So other than leasing the equipment, you’ll need equity funding to do this. You cannot borrow for working capital unless you have an established business with revenues and cash flows. I mean, sure you can charge some things on your credit card with a $100,000 limit, but that falls into the category of what I above called “crazy.”

Most of those new businesses are online businesses and that requires very little capital to start many of those businesses. The vast portion of the profits from these businesses actually goes to companies like Google and Shopify and Amazon and Facebook and Intuit. In many ways this is like the gold rush, where the people that really got wealthy were the businesses that sold supplies and services to all the gold miners.

Janet Yellen is coming to the rescue. The worst Sec of Treasury in US history just took a page out of the History books from a Commander in Vietnam, as you Vietnam Vets remember”

“We have to destroy the village in order to save it”

Janet Yellen said over the weekend that the only way to get inflation down to 2% is to create massive unemployment and bankruptcies. In other words:

“We have to destroy the US economy in order to save it”

She needs to be fired immediately along with J Powell.

Why should J Powell be fired? Rates should never have been at zero for as long as they had been, in fact he should have never lowered them in 2019 because of the hiccup in December of 2018. It seems to me that you people can’t make up your mind, you know low rates are bad, but you just can’t bring yourself to live without them. Yellen i agree with you on, she’s never done a thing her entire life but be an academic, then sell her insider access for million dollar speeches.

Starting several new businesses was the only way I could offshore the vast profits after selling my Beanie Baby collection.

Elon Musk was on Tucker yesterday and said he fired 80% of his workforce because they weren’t doing anything productive. The same could be said for most of today’s large corporations. Mostly deadwood from top to bottom.

I fear the irony was lost on most of the viewers.

“And yet, the Pandemic Money is long gone”

No. Not by a long shot. It has legs, and it’s running at full speed. The FED has completely failed to reign in speculators and suck liquidity out of the system. The stock market is near all-time highs. Crypto has doubled off its lows. Used cars are now appreciating again. Houses suddenly found bids and are going back up again in many markets. It’s an orgy of liquidity.

Fiscal spending still running hot which in the short term flows money to private sector. It’s making Fed job harder.

The debt ceiling will be raised or eliminated. More trillions to have fun with.

i think work from home has given people more time to start a “side-hustle”.

I sure thought the home builders stocks would be hurting with the slowing sales.

Some are hitting close or hitting ATHs again after dropping 30% to 50% in 2022. I bought some puts on these guys as sort of a hedge against my rental properties. Losing bet on the PUTs. My rentals are going up in price again though.

The 1Q earning calls in Jan or FED on some of these home builder stocks were ugly. But Wall Street is looks forward? Otherwise, I am not sure why these stocks are close to all time highs again.

An example from a friend. A retired full time RVing couple sells all final real estate assets due to the RE Bubble. Decided to get out while the bubble inflated. Established 2 new sole proprietorships for future (wink wink) maybe real estate investments.

Isn’t this what you might expect in the face of massive credit expansion. Free money means lots of businesses will be started that appear to be profitable while money is cheap and available.

It’s great for people to go into business for themselves, but won’t some portion of it also represent mal-investment of capital ?

Yes, and yes, but this is more likely to be banked pandemic-era free money being put to work rather than loans being taken out. Especially now that credit is no longer expanding.

Money has been cheap for 20 years, so take your thought and expand upon it. Nobody can still tell why the corporate world needed bailouts in 2020, almost like they needed it before 2020 and it was all a coincidence ;)

I wonder how much this plays into the “quiet quitter” phenomenon that the media, especially the WSJ was so obsessed about- people doing only what is required at their day job to pursue their side gig (I think “over employed” falls into this category, too.) Personally, I work within a large bureaucracy, where I can find time to do a lot of personal work on the company dime when I so choose. I have been playing a lot with starting a side business in my head in an area where I used to be a regulator, namely to keep pace with the increased cost of living and an expanding family. This could be a solution people be embracing, especially after seeing how much they can accomplish while working from home. In contrast, this may be one reason employers want people back in the office, keeping them dependent on their paycheck only.

Anecdotally, based on my work with small, retail and service concepts, at least 1/3 of these businesses will be be gone in 18 -24 months.

Many are started by 45-55 year olds who’ve been abandoned by corporate America and have retirement savings that allow them to buy a job.

Sadly, even the successful ones will be working more and earning less than their corporate gigs paid them. Worst case, these “entrepreneurs” end up personally liable for equipment and building improvements that have no value once the business fails.

These new businesses aren’t a sign of stretch. They’re a sign of a weak economy and of the desperation of the aging middle management cohort.