Going to be tough for a recession to gain momentum with this kind of demand-overhang going into it.

By Wolf Richter for WOLF STREET.

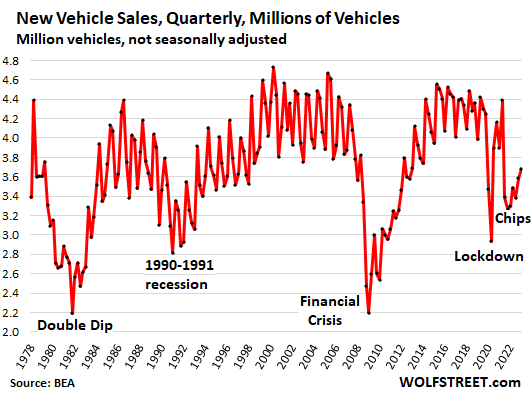

Sales of new cars, SUVs, vans, and pickup trucks in Q1 rose by 11.7% year-over-year, to 3.68 million vehicles, according to data from the Bureau of Economic Analysis. It was the best quarter since Q1 2021, when the chip shortages began. But still far from normal-ish: Q1 sales were still down by 7.6% from Q1 2019:

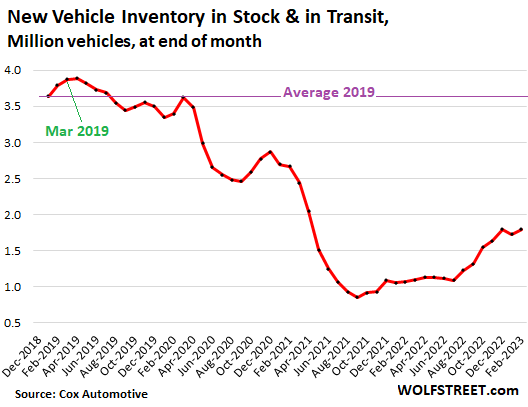

New vehicle inventories are recovering, but still woefully low.

Supply chain issues have been getting resolved step by step, and production has been ramped up, and new vehicle inventories have been rising for months.

Overall, inventories remain far below healthy levels, with some models in short supply or out of stock, and customers still have to deal with waiting lists and long waits after they order. But other models – including many truck models – are in ample supply.

Inventories of new vehicles on dealer lots and in transit have more than doubled since the low point in the fall of 2021, to 1.80 million vehicles at the end of February, according to data from Cox Automotive. But this was still less than half the inventory in 2019:

Massive pricing distortions to be worked through.

Dealers and automakers have pushed up prices into the absurd, and in addition, automakers have pushed their models even further upscale over the past two years, to where the average transaction price (ATP) in the industry is now nearly $46,000, according to JD Power, up by $13,000 from 2019, which is crazy.

Automakers have worked hard for years to turn the average new vehicle into a luxury product that the average hard-working American can no longer afford. At first, those efforts were backed by artificially low interest rates. Then, as automakers were grappling with supply shortages, they prioritized the high-end to protect their dollar-sales, given that production and vehicles sales had collapsed. And now supply is picking up, and interest rates are much higher.

The way this gets dealt with is with cuts to MSRPs – we’ve already seen some price cuts among EV models – and with bigger discounts, incentives, and rebates as inventories begin to build. There will also be a shift in production to less-loaded and more affordable models.

Pent-up demand grows to 6 million new vehicles.

Yes, it’s a thing in the auto industry – always has been. Americans love their motor vehicles, and they’re not going to just drive them into the ground and then switch to riding bicycles or whatever.

Most people can continue to drive what they already have for a year or two or longer. And when the supply shortages hit, and when the ridiculous pricing games started, some consumers decided to wait for supply to arrive and build to adequate levels, and for these shortages-driven pricing games to end. But eventually, those who’ve been waiting a couple of years to buy a new vehicle will buy one. This is the pent-up demand.

We can estimate this pent-up demand: Over the seven quarters since the chip shortages hit vehicle sales (starting in Q2 2021), automakers sold 24.1 million vehicles. Over the equivalent seven-quarter period just before the pandemic, automakers sold 30.1 million vehicles. So by now, consumers and fleets (rental fleets!) have bought 6 million fewer vehicles than over the equivalent period before the pandemic.

This piggybank of 6 million new vehicles of pent-up demand will continue to grow until vehicle sales and supply reach normal-ish pre-pandemic levels.

So if there is a slowdown, enough consumers with money or borrowing capacity will be desperate enough to buy a long-delayed new vehicle when supply is adequate and when the pricing games stop.

Normally, the pent-up demand builds during a recession as consumers, who’d splurged on vehicles before the recession, cut back spending, thereby triggering the recession, or making it worse. Inventories pile up as sales drop. So there is this supply-overhang. Automakers react by cutting production and laying off people, further worsening the recession.

Then, at some point, buyers are coming back out to make their recession-delayed purchases. This pent-up demand, created during the recession, supports sales in the years following the recession – hence the recovery.

So, normally, there’s this supply-overhang going into a recession. Now there is this demand-overhang going into a potential slowdown.

But this will be the first time I can think of that the US economy might enter a slowdown with pent-up demand for new vehicles fueling sales even as other parts of the economy slow.

Now we have this pent-up demand for 6 million new vehicles – on top of regular demand. And given how important auto manufacturing, component manufacturing, auto sales, and everything around them are to the US economy, this pent-up demand might put a damper on the hopes for a recession.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Do you have the CURRENT average sales price? With so much more inventory on lots these days and higher interest rates, you’d think the average sales price declined or Ford, GM et al are ramping up incentives which basically is like lowering the price.

Just wondering.

1. “Do you have the CURRENT average sales price?”

Yes, under this section in the article, quoted:

“Massive pricing distortions to be worked through.

“Dealers and automakers have pushed up prices into the absurd, and in addition, automakers have pushed their models even further upscale over the past two years, to where the average transaction price (ATP) in the industry is now nearly $46,000, according to JD Power, up by $13,000 from 2019, which is crazy.”

2. “With so much more inventory on lots these days…”

It seems you may have missed my inventory chart, second chart down. Inventory is HALF of where it was in March 2019. So just to make sure, here is the chart again:

Now I know why no one can afford homes. Payment on that car with good credit and a 5 year loan is $936/mo. x 2 = $1,872 PLUS insurance, fuel, maintenance etc. $2,500 – $3000 in family car expenses per month.

I guess folks would rather drive fancy new cars and keep renting than buy a home that will appreciate over time and force them to save money.

Many people lease their vehicles. That’s where the manufacturers put their incentives as they can be hidden from the prying eyes of the media and it doesn’t look like distressed merchandising to the general public. A lot can be hidden in residuals, money factors, and other hocus pocus many people can’t fathom.

So… not everyone is carrying a retail note. You can get a Ford Exploder XLT 4WD for $539/36/$4889 due at lease signing… plus tax and tags. Yeah, you have to spit up a chunk to drive off, but even that can be manipulated to get you spot delivered.

I’m guessing that with prices as high as they are the average loan term is probably closer to 7 years instead of 5.

Still crazy payments tho!

Certainly not over the longer term but buying a car right now might actually be a better investment then a house lol

wow, guess I’m glad to be rid of my 2015 F-150

got $30,000 for it in March

used it as down payment on HOUSE

—-

in return I got 2003 F-150 with 300,000 miles

runs good and I use it for work truck – ie locally

I’d say I’ll keep it til I run it into ground

but it’s already been there and hasn’t died

—

no interest in buying anything right now

but if I do it’ll be steal

from someone who NEEDS CASH right now

I’d buy back that 2015 F-150 – for about 1/2 what I got for it

“than buy a home that will appreciate over time and force them to save money.”

The days of homes appreciating year over year are done imo.

I think your numbers are a little high. Take a 2023 Acura RDX, cash price of $50k, even higher than that $46k average:

https://www.edmunds.com/acura/rdx/2023/cost-to-own/?style=401970285

Cost to own for 5 years is $64k, which includes interest and depreciation, as well as fuel, maintenance, etc. It does not include principal pay-down, but depreciation is the right thing to track here instead of that, since you can trade in the car at the end of the 5 years for an amount greater than $0. That’s $13k per year, which is below the bottom range of half of your monthly family car expenses estimate.

That lower 2019 price still seems way high to me. I seem to remember a time when cars at $10g were regarded as very expensive. And don’t they last now for something like 200,000 miles?

Yes, my Datsun 280Z that I bought new in 1978 was just under $10 grand, LOL. While ago. Time flies.

Timing is important when buying vehicles P5:

Friend bought a new toy pickup for $3200.00 cash in fall of ’75.

Another bought a new ’89 chevy 1/2 ton in early ’89 for $10,000.00.

2007 chevy 1500 LT, w all the bells and whistles, MSRP $35k-ish for $25K w unneeded financing, paid off in six months …

new 2007 chevy 3/4 Ton 4×4 MSRP $40K-ish bought for $15K in early 2009 !

2019 Ram 1500 ”tradesman” w lots of extras MSRP $45K-ish, paid $32K in April of ’19, sold for $31K Jan of ’21.

etc.

Wolf, I like the way you modified the Z.

I had few, but I didn’t use a turbo with inter cooler. 40 mm side draft six-pack & headers was my thing.

The new BMW M2 is a modern version, but 3,800 lbs. $65k give or take.

That car inventory chart looks like many housing inventory charts.

I told you soft landing.

“With so much more inventory on lots these days and higher interest rates, you’d think the average sales price declined ”

Well, we have such “tight” monetary conditions from “fed” that the 10 year fell to 3.3% and bitcoin rose to $28K.

Bitcoin has been around $28k for weeks.

The average age of the U.S. fleet must be spiking.

I wonder if NADA and Kelly will extend their value estimates beyond 12 years? It would make sense in a market where a 20 year old Ram diesel can still book will above $20k.

It seems to me there’s an opportunity for lenders in older vehicles. These days, electronic nanny systems prevent catastrophic failures in ways that weren’t possible 25+ years ago.

But I suspect traditional lenders will lag the buy here pay here lots for a while before getting a clue. Maybe they’ll try lifetime financing for new cars first? I dunno.

I was thinking along similar lines. This pent up demand which Wolf speaks of is almost surely driven by vanity more than the need to replace an end of life vehicle. Even the low end models today have a lot more longevity than 20 or 30 years ago (for those of us who remember what a carburetor and distributer were).

Another factor may be the diminishing telecommute trend. During the plandemic people were not only driving less but more importantly not driving into the office in an 8-year old car. As many employers are now backtracking and insisting on coming back in, the urge to upgrade (or at least update) the carriage which your coworkers see you arrive in each day will likely increase.

Then again, pulling into the parking lot in a new Benz while waving ‘Hi’ to your boss and later asking for a raise might not go so well.

There are already value books for older vehicles. Black Book has one as does NADA. KBB has traditionally served as the “wish book” (as in I wish my car was worth this much). Any book issued monthly is worthless as it’s out of date by the time the ink dries as used vehicle prices change daily based on auction results and the better publications are regional (convertibles don’t sell so well in MN during January). Dealers will often show you the KBB on a vehicle when they’re selling it to YOU but will use online services like Manheim Online or BlackBook for trade values (plus shopping it with their gyppers if it’s not something they want on their lot).

A newer car is a rolling computer. I fear that the technology you vaunt will make a perfectly *mechanically* good car turn into a brick under the wrong circumstances (like salt water, sunroof / windshield leaks, excessive heat, or vibration). Plastic deteriorates and the connectors (CANBUS that allows the components in your car to *talk*) will crack. The latest “hack” for the failed connectors on injectors is a zip tie to replace the tabs that snap off – otherwise you have to replace the wiring harness. Oil pans are…… plastic. Valve covers are…… plastic. Intake manifolds are….. plastic. The valve covers warp if not installed properly after a gasket fails. Variable valve timing and turbochargers are nightmares if not properly maintained (some turbos require oil changes – 99.9% of the owners don’t find that out until it grenades). CVT’s require maintenance (the belts stretch) unlike an old Powerglide. Guibos. Rubber suspension bushings.

The above explains why 20 year old Dodge pick-em-ups are still worth $20K. You can fix ’em.

I think you would find a large difference in pricing between a 20 year old dodge gas pickup vs 20 year old diesel. Both are easy to work on. Diesel emissions standards have changed significantly in recent years, and are still tightening (like the fed, maybe) . Every improvement in emissions typically results in lesser fuel economy overall and lesser reliability overall. You cannot beat the simplicity and reliability of a 5.9 12V dodge Cummins, and the market has figured this out. Older diesels are more fuel efficient (mpg wise) and have way less to go wrong engine/exhaust wise, primarily due to the lack of emissions standards back then, but also due to Cummins knowing exactly how to make a great engine. The amount of engineering and technology that has to go into newer diesels results in them being unaffordable, less efficient, and unreliable after so many miles. DEF, particle filters, EGRs, Regen cycles. ‘Clean’ is complicated. It’s just the harsh reality, and the market has come to realize this and they know nobody is making more of these, which has drastically pushed the prices up, IMO

Your comments are absolutely spot on.

You tube has many videos discussing CVT, turbo, eco boost, plastic this and plastic that and how the problems go on and on. This does not even included various reprogramming requirements on repairs that force use of dealer, because specialized equipment and yearly software cost is prohibitive for independent shops.

The day of long term quality and maintain ability has fallen away to cheaper and disposable, while costing much more. All of which benefits auto manufacturers and dealers at the expense of consumers.

“The day of long term quality and maintain ability has fallen away to cheaper and disposable, while costing much more. All of which benefits auto manufacturers and dealers at the expense of consumers.”

This is why Tesla will wipe them out. Legacy auto manufacturers predatory business models will fail. They are currently in the denial stage, in time they will move to the anger stage.

Cool, it’s good to know America’s never ending hopium is finally cementing into a reality…looks like this good time will never end…

I guess I better pivot now too and go from fearing of a pending recession to party like it’s 1999…good thing is I guess I can still overpay for a car and a house and won’t look that odd doing it…

Pent up demand or totally broke? The latter is my belief.

Some people are always totally broke.

Lots of people have somewhere between adequate and huge amounts of money.

Add up the deposits, money market funds, bonds, stocks, private businesses, and other assets, and that’s the overall wealth of Americans. It’s HUGE.

This Americans-are-always-broke stuff gets old.

“This Americans-are-always-broke stuff gets old.”

How true, especially when it’s so easy to get credit terms on a new (or used) car. And you don’t even need a good credit score, but you may end up with a 12% note for several years! (we have a family example of this – LOL)

For many, it’s all about the “payment”.

I’m so tired of this stuff.

1. This is about NEW vehicles. Only about 5% of new-vehicle loans being originated are subprime.

2. Average wealth by wealth category, per households, Fed data:

Bottom 50%: $70,000 (meaning the bottom 20% or so are broke)

So the top 50% of households = 65 million households:

Next 40% (between bottom 50% and top 10%): $558,000

Next 9%: $4.4 million

Top 1%: $19 million

Outside of a few cities, you need an automobile to live and work in the US.

I agree. All I hear about is how everyone has no money. Funny though, they always have money for anything and everything they want.

It’s just the medical bills, child support, etc etc they don’t have money for lol.

And some of the ones I know, when they don’t, just file bankruptcy and end up getting what they want anyway.

There is always money around these days, always.

If you live in a middle class neighborhood with nice houses but nothing special, with a mix of old timers (retired teachers) and newcomers (younger professionals and self employed business owners) you will be surprised to find that a good number of them are top ten percent households. The G Wagons and Porsches are one sign. There is a lot of money out there.

I’m going to point out again, people have not been making payments on their student loans for the past 3 years. Lets see what happens when they kick in again. That extra 500$ a month prob really boosts the economy when you multiply it by all the borrowers not making loan payments (hoping its forgiven, ain’t gonna happen)

I’m actually not sure any of these payments will ever be made. I stopped calling them student “loans.” They’re really just grants. People are NOW taking out new student loans assuming that they will never have to make payments on them. There is no political will to tell people to make payments on their student loans.

Won’t happen, otherwise they’re going to have to forgive homeowners their debts, but then again after watching all of their halfbaked ideas the past three years, that may be their plan.

I’m thinking this pent up demand may be in part caused by a “Last Hurrah” for the Baby Boomer generation. Just a thought. I’m a boomer myself.

Can we be sure “pent up demand” will return to pre-pandemic levels? How much does the work-from-home movement eliminate the need for a second car, or a third.

Beliefs are the cream filling between the wafers of wants and needs. Reality is the awareness that you’re just holding two crackers and some sugar while asking “Where’s the beef?”. Most of the monkeys will tell you to check places like Amazon for a “swinging” deal. Ignore them. They get paid more bananas than they are worth. The fruit distributor is up to his neck in unpayable debt.

You gotta hook me up with your supplier, man.

Sorry, that title is currently unavailable. Please conduct a new search to find any old piece-o-crap that nobody wants to watch but our advertisers approve of throwing their money away on. More fat, less filling!

Wealth is skewed. Averages don’t mean much. Lots of highly indebted barely skirting by who in turn are boosting the highly leveraged but also asset rich class.

These credit “barbell” ends are the ones set to be hurt as many with savings will run out later this year.

As for auto stats, clearly a pricing turning point. Inventory balances plus lower prices for CPO cars (heavily cross shopped vs new) means we’ll see a drop through the year though pent up demand will keep the pace of decline modest.

I must live in a different country because most of the people I know are not broke nor do they remotely resemble broke. And, no, they’re not all “Boomers”. My kids aren’t “almost broke” (30’s and just over 40). They live higher on the hog than I do and have assets to back them up.

What is alarming to me is that there appears to be a significant level of financial ignorance among the general populace. I was recently talking to a 40 YO male who was brought up in a dysfunctional, but relatively affluent, family and it appears that he was never taught about the most basic financial tools such as CD’s, budgeting, nor how to manage his 401K or even what amount to feed into it. He spends most of his time playing online games….. All his money is either in a checking or passbook account. Which is simply stupid.

The banks are hoping his stupidity persists.

Its both. Income inequality is extreme now from inflation. Many people have assets, high paying jobs and a substantial bank account. My guess is around 30%. But the rest are living paycheck to paycheck with no savings(mostly). I sell used trucks cash only 12-20 yrs old $8k-$12k Clean low miles. Its gone completely dead. But the debt borrowing part of the new car economy keeps on buzzing, for now. The 30% look like they’re sitting strong for some time.

Not sure I agree with that 6 million pent up demand concept. I think that making cars last longer is more than a short term trend.

There was also a massive drop-off in public transit ridership from COVID. Some people might go back to public transit and get rid of the car, selling it to someone that needs it.

Demand is a function of price and the ability to pay those prices. If someone needs/wants a new car but cant afford it, they simply wont buy it, either turning to public transit or buying a used car or getting their car repaired.

Increased interest rates plus increased car prices will kill volume. I say wait for the economy to turn south for 2-3 months and then look at car sales. They will be down in the dumps and inventories will rise rapidly. I see inventories back at 2019 levels in less than a year.

Look at the long-term annual chart. It’s a little clearer. Sales will go back to where they were. That’s not in question. That’s where the pent-up demand comes in, it did every time before.

Do you see what pent-up demand did after the Great Recession? That pent-up demand was build up DURING the Great Recession. Now we built up pent-up demand during the shortages. We know how pent-up demand in auto sales works.

The question is why haven’t sales grown since 2000 like they grew before 2000:

I find no fault with your analysis and did similar work in heavy truck for years.

That said, I wonder where miles driven is going. Is there any trend that will offset WFH?

As you stated, the question is why the long term demand has been stagnant when the population is growing (222 million in 1978, 331 million now). I assume that means the average lifespan of a vehicle is longer and used cars make up a bigger percentage of cars on the road, or lower percentage of population drives, or more old people who cant drive anymore, or more people using public transport.

What I do hypothesize is that if we are headed into a recession, job losses and declines in real estate values plus declines in stock market equities/bonds (this is my base case because I am a pessimist), then we are more likely to see LOWER sales in the near term (similar to 2008), than a quick rebound to pre-COVID levels. Because car dealers/manufacturers will take a while to adjust prices down to where consumers can afford them.

i think that car sales are somewhat similar to home sales, where the monthly payment matters far more than the actual purchase price. the problem is that average monthly payments on new cars at current interest rates times purchase prices have risen dramatically (much more than car prices). so if we looked at supply-demand graph at given monthly payments, it wont move back up until the supply at lower monthly payments increases dramatically. unlike the home market, where many people are not willing to sell at lower prices, car manufacturers are a business and make rational decisions and will cut prices to move the higher production volumes they will be able to build this year. so i see a lack of near-term demand leading to rapidly building inventories and alot of cars sitting on dealer floors soon.

tesla is an interesting case. the wait time on a new Model Y was once 3-6 months, now it is down to 1-3 months, but they have even cut prices to sustain that demand level.

also, according to your theory of pent-up demand, we should have seen sales in the post-great recession period peak out higher than before that dip, as the rebounding demand was added to the trendline, but we didnt. the peak was about equal to the years before the great recession. or maybe there is a very long term structural decline in vehicles sales now, so the post-Covid pent-up demand did increase sales above a reduced baseline of demand.

i just dont see some big pent-up surge in car sales this year or even next, as we head in a looming bank melt-down, stagflationary environment. and then China invades Taiwan and everything falls collapses.

No imminent recession in autos as far as I can see. Still running full bore and people still paying top prices, even with interest rates up. When we hit the oversupply point then yes I do see prices coming down a bit. But that leads me to my second point, which is that the multi decade trend of importing deflation has come to an abrupt end. Prices are going to continue to remain elevated because component costs are continuing to increase. There is a strong tension that will develop between the cost of doing business and the price of a car that people can afford. If demand falls and prices come down suppliers will close and inventory build will slow. I get the sense that the price floor is higher than many expect.

Reponse to Tom – I think that everyone is forgetting the impact that the banking crisis is going to have on the economy. It hasnt really hit yet, but there is going to be a financial crisis here in the near term.

Wolf had shown us charts that showed there is still 900 billion extra savings and credit card balances are just returning to prior normal levels. But credit card balances are heading up very fast right now and that extra cash is being spent. The biggest asset for the middle class – their home – is also in a bubble right now. So people feel like they are rich.

By the end of this year, it all changes. No more stimulus spending from the government. Bank supluses spent. Employers pulling back on wage growth and jobs. Credit card balances going off the charts. Real estate finally turned down.

This quarter we are on the edge of the financial melt-down. Another 3 months and we start to see the slowdown. six months from now recession is real and consumers are pulling back. a year from now we are in a crash that makes the 2008 recession look mild.

By end of year, new car inventories are high and sales are much lower than today, not higher.

Because we’ve been in a depression since 2000 and government takes over more and more of the economy each decade until it all falls apart?

Hell why haven’t sales grown since the 80’s Wolf? Population is much higher, please explain.

I’ve been publicly musing about this question for years here.

My two main answers are price and durability.

People are buying used vehicles instead of new because they cannot afford a new one because every automaker had gone upscale because that’s where the profit margins are; and vehicles last a very long time today and look good for a long time. A 10-year-old car can look like new today. Paints, rubber door seals, leather and plastic interior components, etc. have gotten very good.

Then there are the urban and demographic changes: in many big cities, a household of two wage earners doesn’t need two cars; and in some cities, including San Francisco, they might be able to make do without a car. You see that with younger people a lot here. They don’t have a car. And good for them.

Thats a nice story to tell yourself, i think the economy has been stagnant since the dot com boom and every bubble they inflate after has a shorter half life and diminishing effect on the overall economy. You pretend that economics has anything to do with this, the only thing that has been growing since 2000 has been the government and the “businesses” they decide to support based on politics.

Federal budget in the year 2000:$1,788,950 trillion

Federal budget in the year 2022:$6.27 trillion

And lets not forget about the states who i’m sure have also been expanding their budgets year in and year out.

Federal Debt 2000: $5,674 trillion

Federal Debt 2023: $30,824 trillion

Almost like a leveraged buyout, sell off the good assets, load the place up with debt and pay yourself absurd amounts. Tell everyone they’re a terrorist if they question you.

@Mr. House – My adult chillrens do not own cars and we now have 1 car instead of two. Also, I only drive for work once a week now and GF does short errand runs, so the mileage is way down from past years. BTW, never owned a new car, but do like the smell. :) So, where that would have been a minimum of 4 cars in the past and probably more as chillrens have spouses, its now 1 car.

I hate the new cars with the electronics. My old Toyota and Honda both got over 300K (333K and 356k) and were very comfortable to drive.

@QQQball

Would the car manufacturers survived 2008 without government favoritism? I’m curious how your answer disproves my point. We keep making more and more excuses for a declining standard of living.

Fe2O3 takes a lot longer to show up.

“The question is why haven’t sales grown since 2000 like they grew before 2000”

The answer to this question is well known: cars live longer and the number of registered vehicles steadily grew until 2019, increasing by circa 36 millions in just 6 years since 2013. Since then we have a significant slow-down and the number of active registrations increased only by about 6 million since 2019.

But then again the market is saturated. With approx. 290 million registered vehicles in the US in 2022 and with less than 240 million active drivers licenses, there is no more space for serious additional growth. New sales will be correlated with two factors: number of cars that cannot be fixed for a reasonable price and the introduction of new “needed” features in new products.

So stagnant sales plus better product equals higher prices eh and higher gas prices?

@Mr. House, Apr 6, 2023 at 12:37 pm

A lot of people with a lot of money for a temporarily (at least) limited in availability product. Hence the crazy price increases. Plus a lot of money given away during what some call the “plandemic”. Means the prices won’t really come down, even though I anticipate they will behave much more rationally until the next crisis.

But it has nothing to do with car sales levels.

Agree in general with you and Wolf woj; how some ever, what appears to be coming are ever more opportunities for our socialistic friends spending our grand children’s money these days are combinations of ”forbearance” such as:

1. CASH for CLUNKERS -#2, and that will have to be adjusted for inflation, so say $10,000.00 for anything that can be driven into the crushing yard.

2. FOOD for FAMILIES – #?, and that ditto, with many more folks eligible for many more $$$

3. INSURANCES for IDIOTS -#? – and that will have to be both inflation adjusted as well as climate change adjusted –always up of course.

4-xxx… etc., etc.

Basically, when ya take the MERIT out of a meritocracy, ya end up with a bunch of crap—and here we are.

agree with that assessment. When houses drop new car demand buying desire will drop. There is always demand building from existing vehicles being worn out. That will always be there. The ability to pay may diminish though and its already happening with many. If fear kicks in with a bad recession, people cut back on major purchases, even people with money.

Nowadays if you buy a new vehicle and take reasonably good care of it you might get 300,000 miles out of it before cost of repairs make it impractical. That line used to be 200,000 miles not too long ago, before that a vehicle was considered wore out at 100,000. People like to say that “they don’t make things like they used to” and that’s true, some things are made better.

I wonder how much of a factor this might be for sales in the long term?

This is very true. The benchmark keeps changing. Soon it will be 400k miles can be expected out of a quality made car.

I wanted to keep my 3-series til it was a pile of rust and 4 wheels. Unfortunately in NY nothing lasts forever, it’s only a matter of time until someone hits you or pulls out in front of you and your number is up, and your car is a total loss. Even if you’re a great driver. Then you’re forced to have to buy another car at the worst possible time. Right now my X5 has 168k on it and cruising along just fine, although I refreshed the entire suspension and have maintained the drivetrain quite regularly.

All that recession talk was just that…talk from defeated bears. We just entered a new bull market and honestly the economy looks pretty solid here. Restaurants packed, houses selling, cars still in high demand . I think the no landing camp is proven right day by day.

In terms of the economy, that’s what I see too. No way inflation is going away in this type of economy. There’s still way too much money around. I just don’t see a landing.

This means higher rates for longer, and lower asset prices due to higher rates for longer, and continued QT.

Wolf, I agree with Holden, and I also see the Fed continuing with tightening, but I fail to understand the Treasury rate market. I hope you can cover it in another article.

Holden confirms what I have been seeing since the Fed began raising rates and tightening. 95% of my tenants are either wanting to expand or are doing OK. I have had a couple leave, but that’s out of a group of over 200.

The problem is at the government finance level. That’s where things will break – inflation, currency, deficits, banking.

The economy will buzz on printed money until there is an abrupt system-wide financial break. Joe will spend until he can’t.

The bond market is saying the break will occur this year, while the US Treasury is trying to issue tons of new treasuries. Let’s see if the US Treasury can do this at palatable rates, at a time when the Fed is also selling treasuries, other central banks are selling USD assets, a cohort of countries are trying to rid the system of its USD reliance, and the equity-light banking system can’t afford to take on more duration risks.

Banks and pension funds were big buyers of LT treasuries in the past, and they were scorched. They might not do it in the future.

Bobber wrote:

”other central banks are selling USD assets, a cohort of countries are trying to rid the system of its USD…”

Looks like maybe US ”peeded in it’s own nest or cut off it’s nose to spite it’s face” when it decided to start ”sanctioning” ”foreign” folks for their behaviours considered noxious, eh?

Why would any self respecting ”ruler”, oligarch , or foreign political power player want to put their money or other assets into USD when they KNOW USA will be happy to confiscate it at the earliest opportunity, as has recently been demonstrated SO very clearly?

All these anecdotal observations are true for now, but that doesn’t take away the fact that we haven’t even seen the impact of a meltdown in value of Commercial loans on bank’s balance sheets that have to re-financed at the new rates, which will go higher with each inflation report. No more zero% free money loans. This will impact on Regional banks through massive defaults on these loans. Depositors will run like scaulded dogs, if they haven’t already. The banks that have failed so far are only the beginning. I wouldn’t keep one dime in a regional bank even if it were insured. .

Isn’t there a scenario where unemployment remains low even as the banks tighten lending? Think of how many people would need to be laid off to really move the needle in the job market. So in the short term, businesses closing might actually be inflationary due to the supply side of the equation.

Tom S., did you notice how fast jobs were lost in the 2008 financial crisis? Look at the past charts. The speed of the job losses was harsh.

The bubble today is twice as precarious because no meaningful structural changes were made to the system after 2008, yet risks are sharper and broader. Up until a few months ago, everybody was saying banks were strong and well capitalized. We all heard it on a regular basis. A few months later, we find out the entire banking system has zero equity on a FMV basis, regulators were snoring, and oversight is riddled with conflicts of interest.

Confidence in the system is poor and waning.

Doesn’t look good.

The time for empty solutions, fiscal band aides, and narratives is coming to a close.

Bobber,

I’m not so convinced that 5% is going to pop the bubble. Neither is the bond market. And there doesn’t seem to be a lot of willpower to go much higher, either. But yes, I agree we will know a lot more by the end of this year.

Yep — everyone’s loaded, and getting loadeder.

Could be other reasons but Wolf has been in the vehicle business for decades and I would not bet against his perception of the markets. If from a different source for the data then I would guess differently.

There is the work from home piece that led to fewer miles driven. The trend of lower fuel sales has been going on for 15 years though. Btm line is manufacturing of vehicles won’t slow down soon and won’t impact inflation number’s regardless of reasons . Who cares .

Miles driven in 2022: -2.8% from 2019.

But from 2007: +4.6%.

And look how many vehicles were sold in 2007: 1.6 million. It’s easier to see on this annual chart:

Looking at the statistics Wolf has been reporting, may be our thinking was wrong. May be this is the new normal – tight labor market, high customer spending, high inflation, okish interest rates (as compared to inflation), more importantly highish asset prices (i know i know residential real estate and stock indexes has come down a little but they are very very high as compared to fundamentals/historical prices), and the last but not the least HIGH DEBT.

Savers or fiscal responsible = Looser

Over spender or excessive fiscally irresponsible = Winners

Anything I forgot?

I guess if by winning you mean getting to the top of the bottom before anyone else does, sure.

It’s one thing to hew cavalier for a few seasons, living right up to the outermost reaches of your means, running the AC with the top down & not giving half a damn as you squander the spoils of your toils in certain dissipation. It certainly beats the hell out of wringing your hands over that dime you forgot on the dresser in your hotel room before checkout. Relying on debt to underwrite luxe doings is something else again. We’ve all known that guy, but I’m not sure he ever reeked of winningness.

It’s like coming upon a house with a great smoking chimney on a freezing cold night, only to get closer & discover that its occupants are burning the very timbers of their house in order to stay warm.

Concerned_guy,

“okish interest rates (as compared to inflation), more importantly highish asset prices”

Higher interest rates = lower asset prices, not higher asset prices. Yield works that way.

Remember the banking crisis and the unrealized losses? These lower prices are a function of higher yields. CRE works that way too. Dividend yields work that way. The whole schmear.

I said “highish” asset prices not “higher” asset prices.

I agree that “ Higher interest rates = lower asset prices” but this time something is off here. Asset prices are stubbornly still highish (still very very high. Look at Shiller’s latest statement)

The mortgage rate have gone from 2.5% to 6.5/7% but the homes prices (nationally) have not come down proportionately.

Fed rate have gone from 0.25% to 5% but stock index have not come down proportionately (only measly 20% down).

Unless there is a deep recession in next 6 months in full force, situation will not improve much.

You’re ignoring the time dimension. Declines in some assets, such as housing, take time. The reason? The average home buyer is an idiot.

The housing market is the slowest changing market. A lot of this market is psychology because there is a lot of money involved. In a market crash the seller is the last to know, in a boom it is the buyer

Some lessons are needed in interest rate impacts on valuation. Fed Funds isn’t the relevant metric, rather 10 or 20 year bonds are. They have not gone from 0-5%. A company’s value isn’t based on one year’s change in rates. Some seem to miss this point…

As for some big collapse, while regional bank issues are a clear credit event (tightening) they aren’t of the same hidden systemic nature as in 2008-2009. Not even close.

House prices? Again, not nearly the bubble of 2008-2009 in the US. Some other markets, sure, and some POCKETS within the US, sure. Nationally? No. We won’t get any major corrections in the vast majority of markets.

The autos market. There will be reductions in prices through this years as competition for volume continues to intensify and as supply chain conditions have eased tremendously vs 2020-2021 and even 2022.

Solid deflationary pressure in housing and cars – plus tighter credit overall = a recession coinciding with inflation turning into a non-issue. The bond markets are correct. Degree / severity of recession will depend on the arrogance of the Fed.

It’s funny how the “savers and fiscally responsible” are described as “losers” and then later vilified because they have assets to invest which then results in their being to blame for all the societal ills.

There’s a readily discernible dividing line separating prudence from greed, and it’s serrated along the edge; some call it versus of the halves and the have yachts. No-one I know is out there castigating the former, minus maybe some suggestible slobs who fall for language campaigns designed by think tanks to foment self-hatred among the middle classes.

Too much of anything is too much, Mr. Katz. After all, you can only eat one lunch at a time.

USA needs to Build Manufacturing WAY WAY UP our Cars have been Way behind and now still are with some exceptions but all in all we Lost the Auto market out of Stupidity and its a Long Way Back baby / All in All rather then compete we just bought Crap and still are buying a Huge amount of crap > Now the Crap is getting better rater then competing

we invented a New Inflation where the Rick get Richer and the Poor shall suffer never most likely to recover as ;long as the Rich are in control .

Read Wolf’s words / research > and then think humm:

********************************************************

Automakers have worked hard for years to turn the average new vehicle into a luxury product that the average hard-working American can no longer afford. At first, those efforts were backed by artificially low interest rates. Then, as automakers were grappling with supply shortages, they prioritized the high-end to protect their dollar-sales, given that production and vehicles sales had collapsed. And now supply is picking up, and interest rates are much higher.

If the Drop Rates Now or just endless on again off again Pause Pause Pause the Game of the Rich this will end the middle Class

MC:

Almost all vehicles sold in the U.S. are manufactured here. Domestic manufacturers (like GM) market vehicles made in China (Buick) and transplants (like Toyota, Honda, VW, BMW, etc.) manufacture their cars here – some with mostly U.S. sourced components.

The key difference is (and always has been) that the domestic manufacturers play a short term game and the transplants (particularly Japanese) play a long term game. GM and Ford concentrate on stock price, executive bonuses, private jets for execs, dividends and the like. At my old alma mater, our execs flew commercial. If they did use a private jet, it was “rented” for a specific trip (and the key players never flew together – which is why they rarely flew private). We constantly reworked plans looking forward 100 years. Think about that. Stock price wasn’t even a whisper and our CEO made in the 6 figures with zero stock options (of course, he has a guaranteed lifetime income stream as a company advisor)

The vehicle supply shortages / increased prices were the result of needing revenue to continue operations and not let a skilled workforce go. Things are moderating and I am aware of one manufacturer that has put their middle priced trim models back in production that were suspended for the past few years. Rest assured, the prices were adjusted accordingly. These people aren’t stupid. They can see the same things you see…. and adjust accordingly. Some just don’t trumpet their moves.

That “average hard working American” doesn’t want a basic car and would rather go into hock for 7 years to buy a lifted pickup truck with spinning rims so he can one-up his neighbor.

It’s not that cheap basic cars don’t exist. It’s just that Americans don’t buy them. After all, we have a so-called car culture with popular songs with lyrics like “I love you for your pink Cadillac”. Regardless of its reliability or value for the dollar, no one ever wrote a song about getting laid in a Honda Civic.

Btw, that car culture may be coming to an end with millennials and Zoomers. Many of them don’t even have a driver’s license and don’t want one. To them, cars are far less of a status symbol than the latest iPhone. So maybe we actually are witnessing the peak of the insanity of manicured suburbs being filled with soccer moms driving F150s. But I’ll believe it when I see it.

I’m one of those pent up buyers. I have wanted for a couple years to switch from my 2017 VW Alltrack to a VW Toureg. Just a little bigger, without have to taco myself to get into it. So I’ve been waiting for inventory to rise and incentives to reappear. Inventory is up, some incentives, but interest rates are 6.9 rather than 1.9 or 2.9. I won’t pay 7%, nor will I put cash into a new car. So I’m on hold, and will continue to take care of the great-condition Alltrack that has only 30,000 mile on it and looks essentially brand new.

I should clarify, I won’t reallocate cash from investments into a car, not now anyway.

Make sure to buy a few boxes of elbow-length rubber gloves for whenever you have to reach up your backside and produce a vital organ or two for the inevitable and serial repairs.

As a finance guy, I wouldn’t recommend it. You know why.

“This piggybank of 6 million new vehicles of pent-up demand will continue to grow until vehicle sales and supply reach normal-ish pre-pandemic levels.

So if there is a slowdown, enough consumers with money or borrowing capacity will be desperate enough to buy a long-delayed new vehicle when supply is adequate and when the pricing games stop.”

That’s the key, isn’t it? How many unqualified buyers can still get financing at subsidized interest rates qualifying under basement level credit standards.

There isn’t pent up demand by 6MM who can afford it under noticeably tighter credit conditions without bubble wealth and a fake economy.

Longer term, the interest rate cycle turned in 2020 meaning below market rates are a price cut. The inventory shortage will support collateral values, for now.

There is always the possibility of payment forbearance or repossession moratorium to further kick the can down the road.

Augustus Frost,

You’re stuck in your subprime fantasy. This is about NEW VEHICLES. There is little subprime lending in new vehicles. Only about 5% of new-vehicle loans being originated are subprime. Subprime mostly takes place in used vehicles.

New vehicles now cost on average cost $47k. You have to have pretty good income to buy something like that. I pointed out all this in the article. New vehicles are not for the bottom 20% that are broke. They have to buy a 20-year-old used vehicle.

Actually, 25% of that bottom 20% likely are getting new cars out of reach – and are the subprime 5. Then another 25% are just barely scraping by through buying new cars but at the $20-$25k price point.

Then you have those top 1 percenters who buy CPO due not to necessity but rather value. Getting a car with 20k miles at a 30%+ discount to new and an equivalent warranty.

Not to mention all the net worth at the more leveraged end of the spectrum that has already been unwound (even if not fully “realized” in the official data).

The captive finance companies work with the manufacturers to provide below market rates and can work the credit tiers, unlike normal financing sources.

At my old alma mater, they had their own scoring system and, if you were a previous customer who paid religiously (even with a few late pays), they’d find you a home at a competitive rate better than you could find at your local credit union. That’s what captive financing arms are for. As a result, “tighter credit conditions” don’t apply under all circumstances.

It’s not only the inventory shortage that supports collateral value: it’s the customers that can’t qualify for a new vehicle who want or need a new ride. Manufacturers are extending the model years that qualify for their certification programs (which covers major components) and the captives will finance those with funny money as well to keep the factories running (pulling people out of their leases in advance – aka “pull ahead programs”) and feed the used car demand.

The the new car side of the business doesn’t operate in a vacuum. There’s lots of levers that can be pulled. I know. I pulled them.

A “cash for clunkers” part deux could be served up by Uncle Sugar to *save* the auto industry if things go that far.

1) In the Last year and a half, – the last six quarters, – sales retraced only 38% of 2021 chips plunge. That’s a thud. The next wave down might breach the lockdown low.

2) In the last 7 months inventory is rising, taking a break in the last 3 months.

3) This “spike” in sales brought us only to 1979 high. 1979 had the biggest plunge during the 70’s/ 80’s slump.

4) Somebody put a spell on car sales.

There were a lot of life changing events that occurred over the past few years. Some couples, working from home, let one income go as it wasn’t necessary due to eliminating the need for commuting costs, clothing, lunches at work, and child care. They also may have let one of their cars go because it’s unnecessary when both are home.

70’s and 80’s slump was the result of a lot of dynamics. Key to that era was EPA standards and the garbage cars built with EGR valves and smog pumps that were so anemic that they couldn’t pull a sick kid off a commode. There were also fuel shortages (OPEC embargo), the first time gas went over a dollar a gallon, and a host of other things that affected the auto industry. Then there was the consolidation of a bunch of weaklings (American Motors in Chrysler for one) due to BK’s… with the only thing saving Chrysler was the K-car and Lee Iaccoca’s marketing skills. “Buy a car… get a check!” “If you can find a better built car – buy it.”

Manufacturers are now putting the squeeze on their dealer networks. Emboldened by Tesla, they want to bring new products online under new “brands” that would operate outside the existing dealer franchise laws. It’s has the ingredients to become a popcorn worthy spectacle. Some states are already pushing legislation to block it.

The point is: Right now, I wouldn’t look at ancient history for a pattern of what’s on the horizon.

El Katz, your comments are as good as Wolf’s articles! Whenever the subject is motor vehicles, I perform a “Find in page” for your comments.

Sales volume could be in a secular decline due to increased durability and consumer uncertainty. I plan on keeping our ICE Toyotas until next generation battery technology is developed for EVs and more charging stations are available. With all of the US money dedicated to the EV buildout I expect that within five to seven years there will be the start of a secular bull market for vehicles.

Car dealers are exploiting customers,just bought new Toyota in Wichita is . Traded in vow passat warned a Honda cry but wait to long in Omaha ne ,told dealer in is what Honda dealer offered ,they matched it made deal . A month later called me wanting another 1,000$ because car had extensive hail damage 2 small dents in roof,told jerk off to pound sand we had legal signed contracts. And he charged me full msrp,gave me $12 k for my car and put on lot fir 19.7$ . This is why dealers suck

Used trucks are at a premium, I just missed out on a 2021 Crew Cab Chevy 4WD trade in on lease by a military veteran, only 4500 miles $40,000. New Ford or Chevy truck start $55K plus options. My 2007 Chevy with 197,000 will have to keep carrying the water. I will eventually buy, but will not be ignoring the market again, it’s completely competitive with plenty of buyers. Im using Car Fax for nationwide searches, buying locally used is not an option as everything is high mileage and extremely overpriced. As parts and labor cost continue to skyrocket, I don’t buy the myth of anything going back down to 2019 prices. Price stability not important where there is demand.

Trucks are a dime a dozen here in Southern California.

As each year ticks by, Americans are getting poorer and poorer. The Boomers were the last generation to experience the unbridled wealth created by cheap fossil fuels as well as American economic superiority that came from WWII. But by the 1980’s, things were starting to lose their shine in this country; albeit in a slow motion manner. The Tech Boom in the 90’s put the shine back on but it was lots of smoke and mirrors. Then everyone tried to get some wealth back with the housing bubble.

The first wave of Boomers (1945) starting retiring in early 2000’s. The early ones were the most financially successful if they didn’t squander it or lose it gambling on the markets. The last wave (1965) will be retired by or before 2030; not far away. With the exception of the wealth transfer that is taking place, the next generations are not going to have it near as good as the Boomers.

So as far as new car sales are concerned, the stagnation simply is mimicking the overall economy and decline in discretionary income. Those that might “want” a new car simply aren’t going to have the means to buy one.

Sorry, Mike — but no. You need to update the drivers on your harbinger. In case you hadn’t noticed it’s been an ez money-go-round for ar least the first past decade and the western world is now awash in brass rings.

You’ve made my case. Easy money (debt) is not wealth. Economically, the majority of Americans are hitting the wall with the recent inflationary impulse and higher interest rates.

Mike did you forget ,this will also be the greatest wealth transfer in history of the world. Just need to be diversified.house,car,stock,457. Gold silver food and guns .Wish I could afford a bug out place .

+1.

Politics is important, but it’s always subservient to demographic and technological change IMO. Our leaders are mostly just responding to those two factors when you zoom out far enough.

If I was a politician, I would want to be in office during a population boom. If not a population boom, I’ll take a credit expansion. And if not a credit expansion, I’ll take a technological breakthrough. It’s just so much easier to balance budgets when the top line never stops growing…

MR:

From what I, a ” vintage ’44 war baby” read, these younger so called ”boomers” are, officially, the generation born between 1946 and 1964, so you might want to revise based on that.

Other than that, all I can testify to is that my offspring born between 1974 and 1980 are not only doing better, relatively, than I did at their age, but are also doing better than any of our ancestors since at least the earlier 1920s…

Of course it is very hard to compare generations these days with those of ancient times, including at least my great grands and before… but IF one considers at least Some of the improvements, (Music alone will do IMHO,) ,,, ALL generations since the development of LP vinyl records have actually been more like the elite of the 19th and every century before…

Gotta keep focus on the vast improvements of EVERYONE…

Just one example: how many folks were able to hear any of the wonderful music by Bach,,,

not to mention SO many others???

It’s great your kids are doing so well. Do they do the same type of employment you did or do they do something else?

I ask, because my Father was also born in 1944. My brother and I were born in 1966 and 1970, respectively, and have done relatively better than him financially. However, we have graduate degrees and he drove a cement truck for 28 years. That said my father retired with a pension at age 54, purchased a house in SoCal at age 26 with help from the GI Bill, and my mom didn’t work prior to the divorce in 1980. I don’t think his lifestyle is readily available to most working class people today. All things being equal, I think it is tougher today for most people. It certainly would have been for me if I had followed in my father’s footsteps.

rojo:

They do the exact same work,,, they just do it relatively better apparently.

That’s great for your children. I almost stayed in a union job that had good pay and benefits after college, but fortunately I left before the union was gutted. My father started taking pay cuts in the early 1990s and retired as soon as he qualified.

Will EVs radically drop the price of a new vehicle? I think so. Like a sack of beans or rice a commodity is just that…easy to produce and functional.

About 4 decades ago I did some hitchhiking in Switzerland…EVs were all over the place.

Tesla dropped their prices hugely in January.

Um, EVs were everywhere in Switzerland in 1983??

In 1883, a hundred years earlier, EVs competed with steam-powered cars. The first automotive fatality in the US was caused when an EV hit and killed a guy stepping off a streetcar in Manhattan in the 1800s. There’s a plaque near Central Park commemorating that moment. EVs have been around longer than ICE vehicles.

But tbh, I didn’t see a lot of EVs in Switzerland or anywhere in Europe in 1983, except small utility vehicles (forklifts, small cargo vehicles, etc.).

We all are different economic actors. Instead of using IRA distributions to buy a $46,000 car, I convert about $23K a year to a Roth to try to hit the sweet spot on lifetime taxes. I have about five years til the dreaded RMD’s start.

My car hasn’t moved in a week. It’s all scooters for the next 6 months unless its raining.

Re: median household wealth – if consumers are doing so good, as Wolf mentioned average household wealth then you read a story about most people dont have $500 saved…….”household” wealth may be misleading as more people are living with their parents/inlaws ect

I gave up waiting for the insanity in the car market to end. Sold my commuter, paid cash for an old bronco two years ago. Most frictionless purchase of any vehicle I’ve ever had. And I get to keep my bronco.

Take delivery of it Friday, no finance office bs, no bs markups, no run arounds. Bought online in 10min, get it delivered less than a week later at 5.5%. Car dealers are diggin their own grave.

“Massive pricing distortions to be worked through”

Just another absolutely disgusting example of the FED’s reckless money-printing. With a mandate of “stable prices” they destroyed pricing. With their diabolical $135,000,000,000+ of QE PER MONTH they painted the land with cheap money – money that was hoovered up by pig-faced bankers who in turn lent it out to anybody with a pulse, oftentimes under onerous terms.

Fog-a-mirror financing returned with a vengeance, and dealerships were straight price-gouging and ripping people off in remarkable, unprecedented fashion. 150%+ LTV (loan to value) on a car was common. Think about that – the underlying value of the asset didn’t even have to support the purchase price. These were essentially unsecured personal loans.

And in the used market it was the same. There was a story of a poor, unsophisticated black couple who were celebrating buying a mid 90s Ford sedan with high miles. They got a 7 year loan at $280 per month. That’s almost $25,000 for a clapped out piece of garbage. Predatory lending much?

The entire US economy is one GIANT financial crime scene, brought to you, once again, by these repulsive pigmen bankers.

Bank biz burned by inventory & duration.

Realty ripped by unwanted un-leased office space.

Car sales crash into… what? Higher inflation plus 15% APRs? Or maybe recession/secular deflation? Supply chain smoothing leading manufacturing breakout and showroom glut? Maybe additional bank failures and tight lending get ugly again.

And then, of course, who’s crying next? I’m thinking it will be something highly discretionary. After that, then maybe Uncle Sam liquidates IRAs and converts/forces us all to hold Treasurys.

If AI was really AI, then ChatGBT or Bard would have an answer.

I would note that the “6 million units” of pent up demand may not be duly realized.

This period of high prices has been unlike anything I’ve ever seen. Prices have been so high that problems that would typically total a car are worth repairing and extending the units service life. Things like rebuilt transmissions, engines, car crash body work, and complete suspension updates. I don’t think that happened in previous booms in the last 40 years.

My personal car was due to be replaced in 2021. The transmission needed a rebuild. In normal years I would have junked it and gotten a replacement. In 2021 I paid for a rebuild, but doing so dipped into the finances to replace the car, keeping it in service longer.

Such is life.

Annual miles driven dropped sharply during Covid and has never recovered to pre-covid levels. All it takes is people generally keeping their car a year or two longer and suddenly the baseline for auto sales has completely changed.

In 2022, annual miles driven were 2.8% below 2019.

It might be possible that new auto sales don’t recover to 2019 levels. The average price of a new car is approaching 50K, which is out of the budget for most working folk. Furthermore, the introduction of 84 month or longer loans will prove detrimental to trade-in and used car values down the road. As more car manufacturers get on the EV bandwagon, gas vehicles might become expensive and exotic leftovers of a bygone era. It’s be interesting to see what happens over the next few years. Cheers

For business purposes, we have three vehicles ordered and one of those will most likely will not show up. For the second model year in a row, we have ordered a Platinum F250. Every 45 days, I get we’re sorry email from Ford. We ordered a Platinum F150 Powerboost in February and were told it would take four months. A few weeks later, it’s scheduled for Mid-March. We received an its in production email, then crickets. A couple of weeks later, we got an email saying it was postponed due to supply issues. We have a VIN and a window sticker, so I guess it’s sitting in a parking lot, waiting on a module. I just ordered an Expedition, and it’s supposed to take a few months.

We’ve been looking into ordering a Corvette, and those orders had been taking 18-24 months in 2021 and 2022. Now if you order from the Top 2 Corvette dealers, an order takes 4-8 months, so demand is slowing a bit on Vettes.

Wolf.

Careful walking around your city.

LOL. The other city I lived in for a long time, the City of Tulsa, had 68 homicides in 2022 and 78 in 2021. The city is half the size of San Francisco.

San Francisco had 56 homicides in 2022 and also 56 in 2021.

Tulsa’s homicide rate per 100,000 pop is 2.5 to 3 TIMES the rate of Tulsa:

City of Tulsa homicide rate: in 2022 = 16.5 and in 2021 = 18.9 per 100,000 pop.

City of San Francisco homicide rate: in 2022 = 6.8 and in 2021 = 6.8 per 100,000 pop.

San Francisco is one of the safest major cities in the US. That’s one of the reasons we love it here.

I wonder if we’ll see a resurgence of inflation soon. Definitely going to a shorter or non existent rate hike pause, too.

Wolf,

Love You, people certainly need you.

I just reached sixty and moved to Phoenix. Worked in Wall Street for years and I am glad to be done. My grandfather told me if one starts a 500 a month car payment when 18, and keeps that insanity up till 60, that will be many millions of dollars wasted. Always bought two new cars a year and paid cash. CAR OR LEASE PAYMENTS ARE CRAZY. Pay cash, nothing and I mean nothing feels as good as an eight figure bank account at retirement. Think about that.

Save, save and save some more.

Happy Easter

This might sound dumb but besides saving it’s also good to be paying taxes, especially for ssi. The max ssi payment is currently about $4200 per month BUT to get that you need to earn about $160k, just 5-6 years ago it was in the low 100’s – inflation lol

I appreciate the article and comments. With current car market conditions, as they are / stay that way for the next two months, how would one consider factors / look at choosing between ”buying new”, leasing new, or buying your current lease at the ”residual” price, or buying certified pre-own car thats 2 or 3 years old? This shoppers age 62. Thanks.