The banking turmoil is seen as next test for consumers. Would be a hoot if they just go ahead and blow that off too.

By Wolf Richter for WOLF STREET.

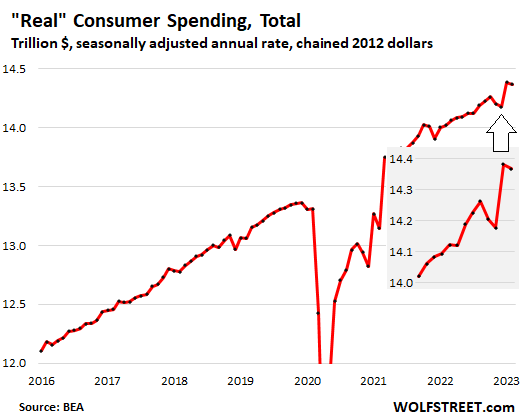

Consumer spending, adjusted for inflation and adjusted for seasonal factors ticked down by 0.3% in February, after a huge spike in January that had followed drops in December and November, and a big jump in October, according to data by the Bureau of Economic Analysis today.

Tamp down on that noise? The gray insert shows the details of this baffling noise that makes the underlying trends harder to see. But we’ll cut out that noise in a moment to see those trends.

Compared to February a year ago, consumer spending, adjusted for inflation, rose by 2.5%. This is solid growth.

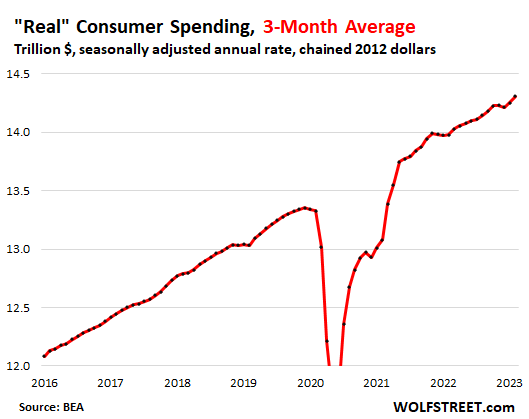

The three-month moving average shows the trend.

Overall consumer spending, adjusted for inflation, when seen as a three-month moving average (which smoothens out the month-to-month zigzags), has been on a solid uptrend: Americans are doing what they do best: spend money, and they’ve been outspending inflation just fine.

The three-month moving average of “real” consumer spending for February was up 2.4% year-over-year.

By comparison, during the Good Times in 2015 through 2019, when interest rates were a lot lower, “real” consumer spending grew by 2.9% on average.

So growth recently has been a little slower than during the Good Times. But it’s still amazingly strong, despite inflation and the highest interest rates in many years.

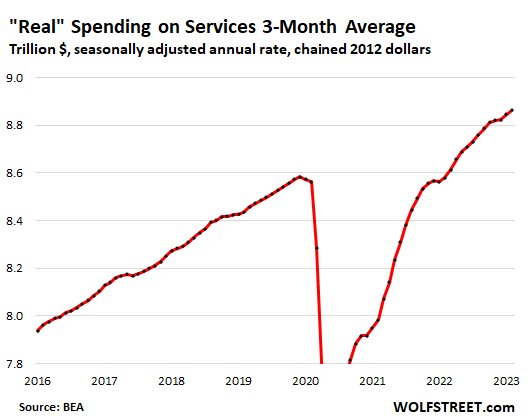

Spending on services, adjusted for inflation, and expressed as a three-month moving average has been rising at a steady but faster pace. In February, it rose 3.3% year-over-year.

This growth exceeds the five-year average in 2015 through 2019 of 2.3%, amid what may still be ongoing revenge spending on travel, personal care, and other services that were curtailed during the pandemic.

Services accounted for 61.8% of total consumer spending. It includes housing, utilities, insurance of all kinds, healthcare, travel bookings, streaming, subscriptions, entertainment, repairs, cleaning services, haircuts, etc.

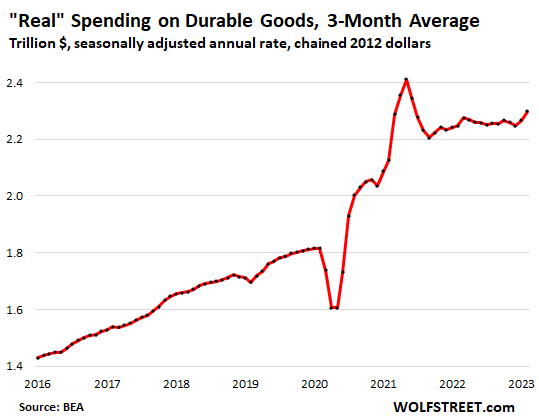

Spending on durable goods, adjusted for inflation, still grew by 2.7% year-over-year, even though the stimulus moneys have long run out. It seems, Americans aren’t about to give up buying stuff. Durable goods include new and used vehicles, appliances, furniture, electronics, tools, etc.

The three-month moving average in February grew at a slower but more realistic rate (+2.2%) than February by itself year-over-year (+2.7%):

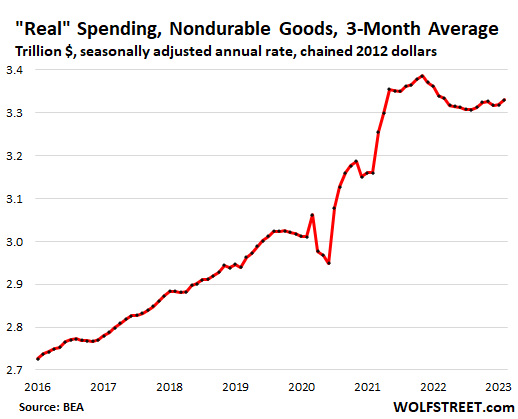

Spending on nondurable goods, adjusted for inflation, has slowed quite a bit and is now barely growing, and in February was up less than 1% from a year ago. Nondurable goods are dominated by food, fuel, apparel, shoes, and household supplies.

The three-month moving average was actually down a tad (-0.3%) from a year ago. This is where food and fuel inflation whacked Americans in the first half of last year. But note the recent upticks in the trend from the low points last summer: Over the last six months, the three-month moving average rose by 0.7%

The Trends: Quite amazing, given how much interest rates have jumped.

Consumers have been outspending inflation, largely due to the strength in spending on services – including revenge travel? – while durable goods spending growth is still holding up. Spending on nondurable goods flatlined last year but recently has started to rise again.

Consumers are in no mood to slow down, they’re out there making money and they’re spending it, despite the higher interest rates.

And it seems they’re starting to live with inflation, they hate it obviously when they’re confronted with it, and they complain about it under their breath, and they’re trying to dodge it, but life goes on, and this inflation is now part of it, and consumers are adjusting to it, and spending goes on.

The next test for consumers: the banking turmoil.

So far, consumers have passed all the tests: They got whacked over the head by inflation, then they got whacked over the head by higher interest rates, then they keep hearing stories about mass layoffs, and asset prices have fallen from the peak, and a bunch of them have plunged, but nothing has slowed down consumers so far.

In March, which is not reflected in the spending figures here, consumers got whacked over the head by a new thing: worries about the banks and worries that credit conditions might tighten.

Fed officials from Powell on down have suggested the consumers will cut back because of these worries and the tightening credit conditions.

And it could be that this banking turmoil is finally what will cause consumers to slow down their spending, but the banking turmoil is already subsiding, and consumers with deposits below the FDIC limits – the vast majority of consumers – weren’t worried about it anyway.

So it remains to be seen if this is just another thing that consumers will just go ahead and blow off too. And that would be a hoot, if even the banking crisis cannot slow down those consumers.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Some of it might be that inflation psychology, spend and get it now before it cost more tomorrow. And people don’t save their money.

Yes, that mindset can develop, and it would be very inflationary. It’s that kind of mindset, if it spreads widely, that can push inflation to the next level.

And every union in the country is going to go on strike. Spiraling inflation. Hence the importance of the stable prices mandate. Ignored.

And every business in the country is going to jack prices. Spiraling inflation. Hence the importance of government excess taxes on profits. The 1950’s had stable prices.

We have had high inflation for too long. People are literally getting screwed. Forced to work more due to fear of layoffs, when they can buy lesser with their salary.

So, no wonder they want to spend that cash asap. Keeping it in banks is now unsafe and it keeps depreciating even if they put it in T Bills!

called THEFT by govt

a devaluation of fiat $dollar

I agree with you that money depreciates in the banks, but if you have, say, 300k in the bank, you have it and when property prices or car prices or whatever fall, and they will fall, you have that money saved and you could to buy a property in cash or with minimal credit. But if you spent that money for fear of inflation eating it up, then you have no money.

Juliab: Save your money prudently. And wait for better prices. Good luck with that!!!

gary 2

Even today, asset prices are lower than they were in 2021 and 2022. And looking at how things are going with interest rates, they will be even cheaper in a year. As the wolf says, be patient

PMs for me.

Totally this, and it’s not just US consumers getting frustrated with the way their hard work and earnings are getting de-valued by bad monetary and fiscal policy. One of the biggest consequences globally of the dollar’s erosion from inflation is the acceleration of de-dollarization across the world, and not even for the political or strategic reasons the media likes to talk about to sell headlines–it’s simply that the dollar is faster losing its value and the Fed still hasn’t been aggressive enough in fighting it, so the rest of the world is more and more reluctant to hold a relentless declining asset which US dollars are now. Paul Volcker got this decades ago, but though Fed moves lately have been in the right direction, it’s not enough, and the oil and commodity exporters and big manufacturers are getting angrier about the USD basically depreciating and exporting inflation to their shores, and raising the danger of social unrest. Literally in the past 2 weeks, Brazil, India and France all moved to unload dollars and do trade (in the RMB, euro, dirham, yen and other currencies) in whatever way bypasses the dollar. The big oil producers are going in the same way, so are Nigeria and Kenya with their mineral riches. And despite the stock response of “there is no alternative”, there is in form of a more diversified portfolio.

Like our econ prof said years ago, in reality there’s never just one reserve currency, and the major banks and asset-holders abroad too have options like commodities and resources to store their wealth in. There’s a big basket to diversify with. The dollar won’t simply drop out overnight, instead it’ll lose it’s luster as its ability to store value continues to erode and people and institutions will find more varied ways to store their money and preserve value, that’s after all how pound sterling ultimately lost its own status as the British Empire collapsed by the time of the British defeat in Suez. Again Volcker had foresight here, he doesn’t get enough credit for how sharp he was about history just like economics, he wrote a lot of books, textbook chapters and articles about how inflation unravels societies like nothing else.

Volcker came from an old German family with a lot of relatives who lost everything with the Weimar inflation and he knew full well how inflation has brought down more great countries than any war ever has. But still the Fed and Congress right now don’t seem to get it. When inflation rages like this, the mass speculation and asset bubbles have to be fought hard–not just interest rates, but aggressive QT and taxing of the ultra-rich speculators who keep re-inflating the housing bubble and other asset bubbles still fueling the services inflation. And it’s not enough to have disinflation or whatever other dumb meme the squawkers in the media like to bring up–prices actually have to come down from these highs in a lot of areas where Americans and hurting, incomes just can’t keep up with the inflation that’s already kicked in, not even considering what’s ongoing.

@Miller:

The move by the current (and previous) administration to weaponize the dollar by confiscating and freezing the assets of other sovereign countries *might* have something to do with their moving to different currencies.

They may have overplayed the sanctions hand… just a teeny bit.

Inflation ain’t all of it.

Berkshire Hathaway famously has $150billion in t bills…

Much to chagrin of its shareholders.

I think having dry powder at the fire sale is always smart. Why is this so unpopular?

Yes, absolutely true. Also….I know this is not the space for it, however, I firmly believe the spiritual void is now a chasm trying to be filled by… as comedian George Carlin said – “buying things we don’t need with money we don’t have”. Carlin was prophetic – the video I am referring to was made some 25 years ago and can be sound online. Very funny, if it weren’t so true. The end result will be devastating for many, very sad. Take care all.

T – to your point, the term ‘retail therapy’ has become a less-than-joking part of the lexicon…

may we all find a better day.

Retail therapy is proven to be ineffective other than a short-term boost. It’s like a line of coke; you’re back for more in 30 minutes and want twice as much.

But GWB told us to get out there and shop or terrorists will have won. Groups in the Pacific NW tried to start up a Buy Nothing New movement post Financial Crisis and were attacked for being anti-American and commies.

The game can’t continue. It’s exponential (geometrical) growth which has a limit. That limit is very close. Given that humanity is incapable of saving itself, you might as well enjoy the final fruits of civilization while you can. Order Pangolin fried in crude oil with a side dish of Bald Eagle in a copper pan.

“buying things we don’t need with money we don’t have” in order to impress people we don’t like. Thats human nature.

Wolf,

I recommend two books;

1. “When Money Dies” by Adam Fergueson

2. “When Money Destroys Nations” by Philip Haslam

Pretty much everything I bought during lockdown is now worth the same or more than what I paid. I’m currently buying a musical instrument secondhand and the guy is basically getting what he paid for it new two years ago.

There’s no point holding cash if there is something you want. You’ll probably beat any other investments, plus you get to enjoy the asset. I think this realisation is a huge driver of demand right now.

The fed has to make holding cash worthwhile again. It’s way behind the curve right now.

Ah, instant gratification and the accompanying justification. That’s what they are hoping you will do. I’m stubborn. I am purposely cutting back except for necessities. I won’t be manipulated.

Same. Have been in that mindset since I saw my Amazon previous order we’re increasing 25%, 50% then 75%. It’s just ridiculous to pay more for the same thing when you are earning the same wages.

I’ll wait all this out thank you. The Corps are making enough profits to be holding out a “support the VP” tip jar. Or the “white collar 2nd housing fund” lol.

Ha, wait it out. You guys have not seen anything yet. What happens is the things you need will disappear. You will kick yourself for a while, then pay 4 times the price. Read a book or something.

Andy: Whatever. If I can do without it now, then I really don’t need it. Maybe you should start reading the right books or something.

Man, I wish I can get my wife onboard with this. She’s not one for sacrifice in any form.

“I won’t be manipulated.”

Unless….it’s what “they” wanted you to all along!

Gatto: doubtful.

Are you sure you are not being manipulated? At the moment they want you to reduce spending not keep spending. This is in contrast to 2010-2020.

Same here. We scolded one of our (now in high school) little ones when she started asking for the latest and greatest overpriced iPhone for her birthday a few weeks ago. Apple products were outrageously pricey even before this inflationary spiral and they’re even worse now, inflation has given an excuse to raise prices for too many free spending Americans to get sucked into paying more for “the brand”. A brand which seems to be providing less and less value with each “upgrade” compared to less expensive models that cost less for better value. The same with outrageous car prices and restaurant menus with prices getting jacked up seemingly every week. To be honest even we got sucked in a bit with the pandemic stimulus, but now we’re joining the growing buyer’s strike, shopping at the dollar store or Aldi, cutting coupons and just refusing to buy junk we don’t really need.

Fortunately we are starting to see more signs of our neighbors and fellow shoppers going on strike too at these higher prices and opting only for discounts, conserving what they have and just eating smaller meals with less junk at home. Immigration is slowing down (it’s a big driver of higher home prices in the US and Canada) as opportunities dry up, and our old friends are starting to get more budget conscious in their vacation plans. But even as that mindset starts to take hold, there are still too many over-spending idiots who are perfectly happy to go deep into debt for the overpriced junk, and their spending hurts the rest of us by giving retailers and landlords a pass for jacking up prices further or basically stealing value with shrinkflation, with little incentive to bring costs down more. Americans credit card debt is now around record levels and going higher, this binging on credit can’t hold for much longer. And it’s not just a matter of walking out and “finding a better job”, most of us have things like kids in school, families or work specializations that make it very hard to just pack up and move somewhere else for a higher income, so this inflation is kicking us in the teeth.

@Fed Up and @sufferinsucatash,

Bravo. We need more common-sense thinking like this and resistance to paying these ridiculous prices in the US if inflation is ever going to get under control.

I’ve started to notice that the prices of certain items is falling dramatically…. not necessarily the MSRP, but due to promotional “sales”.

Case in point: I am (or was) an ice cream junky. My preferred poison is Tillamook Ice Cream. First they didn’t raise the price, but shrank the size of the container. Next, the retail price hit $7.99 for a less-than-a-quart container (The quart used to be $5.99 but could be bought for $4.99 all day long). I threw in the towel. Decided enough was enough. Not an economic decision: more of a “FOAD” decision. (for the uninitiated, FOAD = “F*** off and die)

Lo and behold, this week it was on sale for $3.99 and the freezers were loaded.

But then I looked at my reflection in the glass freezer door as I pondered that tub of Caramely Swirly goodness…. I’ve lost 20 pounds since I stopped woofing ice cream every night after dinner. Ultimately, I passed on the purchase and will likely not resume my slovenly ways as my current weight is easier on the joints.

English muffins are another weakness. The criminals started charging $5.69 per package of 6. Nope. They can put ’em where the sun don’t shine. That’s nearly double what they once were. This week? On sale for $1.89.

There’s many more examples of the above grocery phenomena.

Car prices? Coming down. Used Tesla’s are less expensive (somewhat) after the last downward price adjustment on the new. For grins and giggles, I watch certain models of vehicles in the event I lose self-control and simply must express my individuality by being like everyone else. Watched one SUV drop (it’s the exact same car) from $76K to $49K (been there since September 25 as the dash displays the date which shows in the photos) with no takers. Now starting to find “double secret discounts” if you search manufacturer’s websites. Even my ex-employer has gone back to offering employee sales on their brass hats (they suspended them during the pandemic) as the auctions aren’t as lucrative as they once were and the cost to transport, store, in addition to the auction fees, outstrip the delta between what I would pay for it and what the auction would yield after all costs are considered.

So, IMHO, the meme that “don’t hold your money as it’s inflating away” is not borne out by observation. The “inflation” statistics are only valid if one purchases all the services and goods tracked and reported. We, personally, have no need to buy everything in sight and, where we do need to purchase something, we can mitigate much of the increase by being selective about what we choose to buy or walk away from. It’s a form of silent protest.

I watch used motorcycle prices. Mainly because it’s an alternate form of transport with excellent gas efficiency.

Prices have been doing a swandive. We are back to a world where you can purchase a motorcycle for $600-800 (granted not much of a great one)

The dependable models are retaining value well, but there are more and more “deals” to be had in used goods. RVS are in a similar position.

You can buy a pop up camper in ok shape for like 300$. Pull behind for 1300$. People are feeling the heat

Daniel – YMMV, depending on the machine. Given amount of usage, good tires (fantastic grip but

less mileage than auto tires, esp. modern mc radials) and good-quality drive chains and sprockets can be costly, frequent consumables, as well as less-than-great actual gas mileage and required maintenance (valve service on shim-adjusted ohc engines, particularly). Given the general price rise/availability in autos, though, I concede a moto may be more affordable at present…

In my years in the business, and (apologies to DanRo), still the ‘supersportbike’ era, I had ‘the talk’ with many potential customers thinking if they got one of those Gixxers or CBR’s they could save money on their daily commute. I would ask if they needed to sell that idea to the spousal unit

just to have a motorbike. If so, I advised that if the spousal unit had any say in the family budget that trouble was ahead as best, a sportbike would pencil at breakeven compared to a lightly-used econobox. Many then wound up passing or discovering the happiness of motorcycling on that Victorinox of two wheels, the KLR, instead (perhaps, in some small way, contributing to the rise of the current ‘adventure bike’ scene…) Don’t get me wrong, I remain a committed, if ‘ vintage’ sportbiker in my dotage, but because it’s my passion (with a passion’s attendant costs…).

Best, and happy biking to you (head on the swivel with good visual horizon…).

may we all find a better day.

Nothing goes to heck in a straight line…… err…. except US Dollar. That shit keeps falling like rock!

I encourage you to look at a long-term chart of the DXY Dollar Index. Today at 102.6. Before April 2022, and going back 20 years, there were only brief periods when it was (barely) above 100. It has been over 100 for the past 11 months. It has come down from the spike last fall, when it hit 114, which was a 20-year record.

For big part of the prior 20 years, the DXY was between 75 and 90.

When I said US dollar, it was wrt purchasing power (inflation) and not dxy.

I don’t hold dollars to buy other fiat currencies. I cannot eat Euro bills to satisfy my hunger :)

So much this! I often sell things that I don’t need anymore and I am yet to suffer a loss at least in non-inflation-adjusted numbers on pretty much anything durable – most of the time I’m even getting ahead and get more for some used thing than I paid for it new.

One of the most recurring complaints I’m hearing now from family and friends is “omg, why haven’t I bought this / did this (e.g. renovation) X years ago???”.

Sorry, can’t type this comment for too long, it’s Sunday morning and I need to go on another shopping spree!

I disagree Rico.

People are still paying their gardener… they just pay him more.

Changing habits is hard and Services Inflation is sticky.

Joe White-collar isn’t suddenly changing his oil and mowing his lawn.

You can put off another Lego set or your 13th pair of shoes a little easier imo.

Honestly, most consumption is over-consumption anyways.

Real interest rates are still negative, federal deficits are still in the two trillion dollar range, and Wall Street believes that a pause by the Fed is locked in, to be followed by rate cuts. Fiscal and monetary policy are still very stimulative and the Fed will create as many dollars as it takes to avoid damage to the US banking system from duration risk. Wall Street likes what it sees, assuming the ECB is willing to eliminate duration risk on its side of the pond.

Duration in Europe.

Precisely.

Ursula and Macron off to China. France buying Chinese (Russian) LNG with yuan, not dollars.

kam,

That stuff is just too hilarious. Why would the US care — even if it were true — that some company in France is buying a tanker load of LNG from China and pays for it in RMB?

China is the second largest economy in the world but has a tiny minuscule currency in terms of international trade and reserve currency. That’s not good for anyone, not for the US either. But it has to do with the capital controls in China and lacking convertibility of the RMB, not anything the US is doing. As the RMB inches up a little as global currency, from very low levels, that would be a good thing for the US.

This only works as long as Americans the rest of the world are happy to eat the ongoing inflation, there’s less and less willingness to do that now, the Fed can’t just keep creating dollars out of thin air if those dollars continue to lose value. I actually think kam’s and Wolf’s comments above aren’t opposed and get to a common point, and I agree it would be a good thing especially for the US for the RMB and other currencies to take on more of a reserve status, the dollar’s overvaluing isn’t a good thing for anyone and least of all for America. Some re-balancing would help our own exports and curb some of the pricey imports also fueling this inflation.

In terms of the PPP purchase power calculations for GDP, China is already the largest economy by a big margin (they’re the biggest trading and commercial partner for most of the world by now) so the lack of RMB convertibility is getting a lot harder to justify. I’ve been skeptical about a lot of the trade war proponents but they honestly have a point about the Chinese institutions doing currency manipulation, it’s maybe too much to expect them to let the RMB float overnight (the Plaza accords hold lessons there) but any common-sense evaluation says they should be pressed to allow the RMB to do at least a gradual rise a lot more than they’ve done so far. And contrary to the “fall of the dollar” doomsaying, that re-balancing would be very good for the US, one of the best things to happen for us in fact.

I think if you look at 50 year m2 chart it gets you in the correct ballgame of where we are. The spike up in m2 during pandemic was like nothing that has come before. M2 has rolled over, but we are so far above the 50 year trend and if Powell wants to break inflation he is going to have to put us in a recession, maybe a hard one.

Debt based consumers are by definition not long term thinkers in my opinion. They will not see it coming and pandemic kind of trained consumer that maybe you don’t have to pay your obligations if its a systemic problem.

That’s true, and that’s another problem with debt based consumption at this level, it’s a sugar high that can’t be sustained for very long. The pandemic stimulus probably did lead to a lot of faulty short term thinking about debt obligations, and the student loan pause was if anything the least of it–PPP money got handed out like candy with poor oversight and no need to repay the loans, and the level of corruption and crooked misuse is a big driver for the inflation and asset bubbles we’re still seeing. And there will be a reckoning for it, the sooner all this excess liquidity and debt binging is confronted, the less painful it’ll be to get spending patterns back in line.

In my neighborhood the only people that do their own yard work are just a handful of us geezers.

I agree, I don’t and I miss it but I make more working than i pay for a service cutting my lawn and then I have kids i enjoy spending tme with. There is just less leisure time at this juncture and I suspect that’s true of the 35 to 55 crowd, i tend to think our work loads are higher than they were for our demo 20-30 years ago.

This for Blam actually:

Can’t say much about these days,,, but ”back in the day” when I had two young kids, about 40 years ago, I worked five days a week from 0330 to 2130,,, Saturday from 0330 to noon,,, and then Sunday from noon until whatever to catch up from the 24 hours OFF…

Worked out very well until the divorce because,,,

” I wasn’t paying enough attention to the baby mommy. ”

Now at late 8th decade, finally really and truly ”retired” ,,, I still wake up and am absolutely

” ready to go” at some now obscene hour similar…

May the GREAT SPIRITS bless us all in our various and sundry efforts!!!

I’d love to do my own yard work. And when house prices become more reasonable, I look forward to it. Became to de conditioned during Covid. Now I love going to the grocery store to do some shopping and get some exercise.

These work from home people might be feeling this as well. Hopefully they get out and enjoy a sport or hobby to burn some calories.

Really looking forward to some gardening, mowing, raking, house projects etc etc. keep the osteoporosis at bay. Get off this stupid phone. Haha

i would say that consumer flunked all their tests. They failed to save any of the stimulus money. They failed to realize that real estate is a big bubble that will cause tragedy.

Not passing grades. Straight F’s. And the bill is coming due.

There wasn’t that much stimulus money actually paid out to the average citizen, so there was little to save to begin with. There was far more money paid out in extended unemployment benefits and from the PPP loan fiasco, and much of the PPP money went to businesses which didn’t need it in the first place. So you need to stop blaming the average person about the stimulus money.

Spot on. I started working full time in my business in 2020 right before pandemic. Didn’t have formal payroll per se yet, so no PPP money for me. Luckily my customers didn’t slow down, but neither did established businesses in the same field as I am. Crafty accounting and inventory control on their part and guess what, they got millions in PPP money, which they didn’t need, because all of them were essential and never even slowed down – quite contrary.

All of the sudden everybody jumped on making ventilator parts etc. They have used PPP money to purchase new equipment. Worse part is, they didn’t care how much they overpaid, since the window of opportunity to make those parts was limited and since most metalworking machinery comes from Japan, shipping distributions only added fuel to that fire. There was no discussion with machine dealers for discounts, extras etc when buying equipment (process that usually takes months of negotiating etc). When there was machine available for delivery it was sold right away.

My customers also got busy, so I also needed to expand. I couldn’t afford overpaying that much and ended up importing used machinery from Italy. Luckily it was before oversees shipping and freight prices went through the roof.

@gametv and @728huey

You’re both right here. There was way too much abuse of PPP money and way too much reckless spending and leveraging by wealthy interests with connections, but also very poor savings habits and lack of thrift by a lot of consumers who go out and pay stupid prices for things they don’t need. Then again there’s also outrageous prices for necessities like healthcare and homes. Both are a problem, it’s fuel for the inflationary fire and it’s why monetary and fiscal policy both have to be a lot tougher to fight it. Even without Volcker style interest rate rises, the Fed can have a big effect by speeding up QT and taking a tougher stand against the wealthy speculators, and fiscal policy has to pull back some of the dumber areas of over-stimulus and restricting immigration more to stop fueling these bubbles in the real estate and rental markets.

They believe government will provide for them (bailouts, handouts).

As if the politicians were working hard to farm food, manufacture goofs in factories, run hospitals and provide Medicare,….

They forget that government doesn’t produce shit and lives like parasite on our work.

I agree. I was just reading a book from 1920 that described money, and capital, as”stored up work.” Now we have a generation coming up that for along time, whether by extraordinary pandemic measures, or plain Fed status quo, got “money” and credit on top of that, issued not for work. As in the recent banking wobbles, the technocrats instantly imagine “systemic contagion,” and their one reflexive lever to pull is, print free money. So the slide continues.

Basically agree with this, being fair there have been some things like the research that led to the Internet, funding libraries and good roads or emergency responses, where the government can be productive for citizens and provide for the general welfare. But the problem is when we actually do the math, Americans actually are paying around the same taxes like Europeans are–the idea of the US as low-tax is a myth when we put together all our taxes, state and local, property and payroll (Texas being “low tax” is a joke to anyone who’s lived there, don’t look at your property tax bill if you’re at risk of a heart attack). But we don’t even get the actual benefits the Euros get for those taxes like healthcare and childcare that won’t bankrupt us, we still have to pay out of pocket. What are our taxes even going to when they don’t even provide basic services the rest of the world takes for granted? If Americans knew how much they were getting robbed by corruption and how much of their tax dollars were wasted, there’d be a lot less docility about it. Or maybe not, the way we’ve been getting ripped off and still do so little about it.

@ phleep

“I agree. I was just reading a book from 1920 that described money, and capital, as”stored up work.”

Also well said, the savings we build up from working are exactly that, and inflation is theft of that stored work and contribution to the economy. Another reason why badly controlled inflation like this is basically a crime against the citizens. It’s nothing more than a failure to measure up to the most basic obligation of making sure a country’s currency, and the money in that currency people earn for working, preserves it’s value.

Leo,

Lol “They believe government will provide for them (bailouts, handouts).”

Isn’t every American paying $74 to bail out SVB????

I understand some think the banks will absorb this cost, but I believe they’ll just pass it on to customers.

Bank profit margins are paying for that.

We are buying nonperishable goods in anticipation of higher prices. (I am stuck with lots of canned food and dry lentils, etc., due to earlier prepping for more of the pandemic.) However, there will be a limit given the mean incomes of Americans as their rising expenses outstrip their income increases. Indeed, only the truly vast, hidden wealth from the tax shelters of America’ ultra rich (who used the loophole of US persons’ foreign income exclusion from US income taxation to squirrel away trillions in Ireland, the Cayman Islands, Panama, etc.) may keep major item consumption from collapsing.

Many fear for their fortunes in China, which reportedly is blocking them from taking their money out. Read what billionaire Mark Mobius said as to that.

Not sure what you’re talking about. The Foreign Earned Income Exclusion for US Citizens and Residents Aliens in 2023 is $120,000. The exclusion amount is adjusted annually for inflation.

And you have to live outside the US for 330 days for it to apply.

Dear Rojogrande,

That is what the ultra ricb want you to think. You may want to read the fact sheet about Apple and tax avoidance on $252 BILLION plus in foreign earnings (not tax evasion which is practiced also by many, many US persons as to their foreign income) by the Institute on Taxation and Economic Policy. In 2018, Gizmodo explained how Apple avoids paying $50 billion in American taxes, along with other companies. Most estimates ignore state taxes, which are substantial in California.

A gross UNDERESTIMATE of the sums stashed overseas is in $4 TRILLION In US Wealth is stashed overseas, much of it in tax shelters by the tax policy center. Actually, historically, US companies’ foreign income not brought back to the USA was neither reported nor taxed, UNTIL FORMALLY BROUGHT BACK. Thus, if you put it in a UK Commonwealth territory trust (one of the safer, more conservative options) the companies that trust “bought” (formed often with local politicians or police) could purchase or invest trillions in US, EU, and South American companies or assets. Good luck getting them to confess. LOL Only a wealth tax with 100% forfeiture provisions would compel disclosure or as to UK Commonwealth tax shelters, a tax shelter focused treaty.

RH,

You seem to be conflating two different tax situations, individual and corporate, to come up with a nefarious conspiracy that doesn’t exist. When you said “hidden wealth from the tax shelters of America’ ultra rich” and “may keep major item consumption from collapsing” in your first comment, you seemed to be discussing individuals who are hiding money in foreign tax shelters. When someone thinks of the ultra rich, they think of individuals, not public corporations such as Apple who you mention in your second comment. Individuals, including the ultra rich, are required to report all foreign accounts and trusts. If they don’t, it’s not a loophole it’s tax fraud. These reporting requirements and the resulting income taxes are why some wealthy individuals renounce their US citizenship.

American corporations operating foreign subsidiary corporations are taxed differently. At this time, as you note in your second comment, the US has a policy of not taxing the earnings of foreign subsidiaries unless those earnings are paid to the US parent corporation. Occasionally, Congress lowers the tax rate to encourage the repatriation of earnings by foreign subsidiaries. This is simply a tax policy choice and Congress could choose to tax those earnings immediately. Public corporations with foreign subsidiaries, such as Apple, lobby against this to defer paying US corporate income taxes on the earnings of their foreign subsidiaries. This is a well known tax issue and this wealth is not “hidden.”

I do not doubt tax fraud and a failure to disclose foreign assets occurs, but that is not the result of a loophole as suggested in your first comment. It’s a crime. How the foreign subsidiaries of US multinational corporations are taxed is a policy choice Congress has made.

Dear Rojogrande,

You seem to be ignoring my references to foreign trusts. Wage income earners make chump change, even CEOs compared to the historic ultrarich. The 55 trillion pounds. discussed in BRITAIN’S SECOND EMPIRE: THE SPIDER’S WEB just in Commonwealth tax shelters are in TRUSTS.

If you are only a trust beneficiary to trillion dollar trusts (and each parent or grandparent will often have a separate, foreign trust), you do NOT have to report the many, many trillions in foreign trusts nor their income. That is legal.

That is the US wealth that has come to own our banks, controls our media and (at least in LA) our legal system, while the class of established ultrarich successfully avoids taxes. Of course, crimes and money laundering also occur. The ultra rich have long been above the law (mostly, unless some annoy richer persons), pay only pretend taxes to appear respectable, and just gave themselves even tax cuts on those pretend taxes in 2017.

If you can control whether a corporation pays dividends and survive of beneficiary payments from relatives’ foreign spendthrift trusts (and crony “loans”), you can elect not to pay taxes and live FREE in a corporate condo, fly in a corporate jet, drive a corporate car, and enjoy your private, beautiful, young personal ” assistant” or secretary. I got in trouble once for polishing a beautiful, trophy “secretary.” LOL

I wouldn’t worry about being stuck with non-perishable food. You can always eat it yourself or donate it. How much can you possibly have invested? A few K? You can lose that in minutes with other investments.

I wouldn’t worry about WWIII either. The US is far too unable to absorb homeland damage. Talk is cheap until you get punched in the face.

RH is just wrong.

They aren’t using a “loophole.”

People just literally hide money in shell corporations etc and illegally don’t report it.

To be clear the US is also in this business. US citizens cannot hide their money in the US, but foreigners can.

He referred specifically to the typical US dodges: Cayman, Panama, Bahamas etc.

It is illegal, but many wealthy people do it. I believe there were US politicians in the Panama Papers, correct?

Typically, one needs a minimum of 3-5 million to make it worthwhile according to NPR.

I won’t link it, as I believe Wolf doesn’t want links.

You can Google “Want To Set Up A Shell Corporation To Hide Your Millions? No Problem” if your curious.

Another dodge is to set up a perpetual trust or to only borrow money from assets, but never sell them. These are both legal though :P

I was wrong. I couldn’t find politicians in the Panama Papers or the Pandora Papers.

This was interesting tho:

“One of the more surprising findings of the Pandora Papers is the explosive growth of offshore banking inside the United States.

Specifically, South Dakota and Nevada are among the U.S. states that have “adopted financial secrecy laws that rival those of offshore jurisdictions,” the journalists found.”

I do find it hypocritical to complain about Panama, etc while also providing the same services in the US.

Once again, NOT for US citizens:

“Over a veto of President Trump, on January 1, 2021, the Corporate Transparency Act (“CTA”) went into effect as part of the National Defense Authorization Act (“NDAA”).”

IRS and law enforcement will get you if you’re a US citizen :P

Not that I endorse any of these lol. Honestly, the legal means to avoid (a lot of) taxes are already really good in the US.

The ultra-wealthy don’t need to hide their money in Panama or the Caymans. It’s the Just-A-Bit-Rich who do that, the 1%. The top 400 pay 8% income tax; no tax haven would be cheaper.

Here next to Chicago, the price of lentils and split peas has doubled.

Still a good thing to eat.

Rico, too funny! The average consumer sits in front of his TV and has no idea what’s going on. The TV tells him to spend his money on aspirational products so he can be *cool*. The TV tells him inflation is a short term blip, caused by Trump.

TV tells him what to think and what to do. Since he has a very short attention span, he might forget in 3 minutes. But they’ll be there to remind him and remind him until they get the result they paid for.

Only older people watch TV now a days.

I bought a regular can of garbanzo beans today for $1.39. This was the cheapest brand on the shelf. It should have cost 75 cents.

Food has nearly doubled in price lately but you have to eat. Yep, inflationary spending.

Ccat

No, it’s because I have no choice but to pay more.

It costs more to feed my family.

My total housing costs have gone up.

My other bills have gone up.

The only things I have to cut is discretionary spending, restaurants, entertainment. And that is being slashed.

But the amount I can save has gone down slightly. And it’s going to continue to go down at this rate.

So stop blaming the victims here.

I think most people spend everything they earn and then some. Mortgage rates only affect a small percentage of households, new automobile purchases affect more but not the vast majority.

Gasoline has gone up and down. Food seems to be up across the board. Restaurants appear to be doing well. People are getting the biggest raises in years.

The average family is struggling but that’s not new. I think many expect another round of helicopter money so why not keep spending?

Millions if retirees welcome increasing interest rates, care not about layoffs and decreasing asset prices, and are more than willing to spend into inflation at the proper time. Bring it on! Did anyone care about zero interest rates while fomo’ing ballooning asset valuea? Sit tight, and take your medicine! The party is NOT over.

If consumers weren’t spending like no tomorrow to fill all their insecurities and desires, what else would the American economy even be running on?

If Americans weren’t constantly spending their way out of depression, we’d see a depression like never seen before.

This is exactly true.

Americans have been programmed to buy everything and more that they all have money guess what?! They’re buying everything.

Bought all the stuff during lockdown and now still playing catch up on buying good times back

This isn’t stopping until the money runs out I think we have at least another trillion to go😂

This here. Bravo. Wow. It’s possible to kick the can with your social life, emotions, health, and spirit – but in the end the bill comes due and unlike finances you can’t outsource most of those other things to someone else to take care of for you.

Those that have wasted all the money on current consumption have pawned the debt off onto their children and grandchildren.

Oh how the mighty empire flails about.

Digital and spiritual toxicity abound. All from shell games sold in place of substance. Look at the fragile people out there falling through the cracks, cracking up, even as the cash flow has been maintained. Yes, everything has a cost. And the financial component of that, at some point, at long last, will not be papered (or digitized) over.

“Rocket Mortgage launches a credit card to help you save for or pay off a home.

The Rocket Visa Signature Card earns 5X points on everything you buy and allows cardholders to redeem rewards on closing costs and down payments with Rocket Mortgage, as well as homeowners who have mortgages serviced by Rocket Mortgage — to pay down their home loans.”

Hmmm — one would have to run the numbers. And then there is counter-party risk. Can Rocket unilaterally change terms later? Lots of diligence to do there! I prefer something with a universal adapter in it, called “savings.”

Christof – a VERY long running state of affairs.

As a geezer, meself, I recall one of my U.S. History teachers (this was in the early ’60’s) remarking (referring to Veblen’s ‘Theory of the Leisure Class’) that the nation had to decide what to do with itself in the wake of being the last one standing in the wake of WWII. The decision being to go all-in as a ‘consumer’ society.

(…and, although the West was temporarily the MOU, science and public attitudes had yet to reach an acknowledgement of a real possibility of a planetary carrying capacity…).

may we all find a better day.

“The banking turmoil is seen as next test for consumers. Would be a hoot if they just go ahead and blow that off too”

IF????? LOL. There is no IF. Of course they’ll just blow it off, or rather enough consumers will blow it off (because there are always thrifty/savers). They’ll keep doing so until they can’t.

An awful lot of those consumers are piling their cash reserves into money market funds, big time. I can’t fully articulate it, except to say, some alarm goes off for me, whenever everybody in a boat crowds to one railing. The red flag says “capsize risk!” For one thing, this could starve the economy of bank credit, while everyone indirectly collects interest from treasuries (many MMFs are now in).

I’m guessing this could be very recessionary, and systemically so. It could induce further asset runs at digital speed, even from MMTs, all hard to model. This consumer is a less reliable being (and this consumer’s balance sheet less reliable) than I would wish. I am sticking to explicitly federally-insured banking, because if something breaks big, it could also become a political clash in Congress. Who gets saved?

Who gets saved? Yellen has already explained this in congressional testimony. She admits a blanket guarantee cannot be extended to all banks and depositors. Therefore each will be decided on a case by case basis by a committee including her, Biden, and other regulators. Figure that out for yourself.

As for me, I am diversified under the $250K limit. If they renege on that, I figure a little gold will hedge as it explodes. If FDIC (a corporation, not part of the government) pays you back with Zimbabwe bucks, the gold should also hedge against that.

Is it just me, or is it more than a little strange these charts don’t go back more than 10 years, and are all marked in 2012 dollars, but don’t even show 2012 on the charts?

A part of me even wants them in logarithmic scale, or all plotted on the same y-axis, because it’d be easier to see that the gains from the bottom left to the top right are only 20 or 40% increases.

1. This is not a Smorgasbord. You don’t get to pick and choose what you want and complain if I don’t serve matjes herring. This is Wolf’s Kitchen. You eat what I serve, or you don’t eat.

2. Only people who want to hide reality about money and deceive readers will use log scales in finance and economics. Don’t ever forget that again (it’s OK in engineering and science for specific purposes)

3. Charts start in 2016 so you can see the DETAILS, you silly thing. DUH. Did you accidentally microwave your brain this morning? The key period is 2020 through 2023, with strong emphasis on the past six months. That’s the time frame that matters here. The rest is irrelevant.

4. You’ve been trolling my site with your braindead BS for years from a distant country (with different logins). You were one of the inflation deniers in early 2021, when I started screaming about inflation. You trolled the comments and then my inbox with your BS about inflation being a nothingburger, and just temporary, and just nothing at all, and it’ll just vanish on its own. I should pull out the shit that you wrote.

5. I let this comment get through so that you could receive and benefit from your scheduled smackdown.

Love the smack down Wolfman! That said it would be good to see some long term trend lines on these so we could see how far off the mean we are.

Perhaps it’s Christine Lagarde?

I wonder if we’re seeing government bots trying to twist the honest reality that we are treated to here like every other media?

I had a Fed troll on my site for a while. He was hilarious in his twisted way. But he was well informed about the mechanics of what the Fed does. I think he was part of a Fed outreach program that tried to explain via comments on various blogs across the US how loving and great the Fed is, and how much Americans benefit from it.

Nice. Well done.

I really enjoy the way you slap down the trolls and the idiots, and the idiots who are trolls. I live off my investments (all equities) and I have found you to be annoyingly and consistently accurate. Keep it up!

…no fish for Harry!…

may we all find a better day.

A log scale is useful if you want to plot the purchasing power of the U.S. dollar. If you plot on a linear scale, it looks like purchasing power is leveling off (1st graph link). Plotted on a log scale, one can see the true loss (2nd graph link).

The reason is because on a log scale, a given percentage decrease in purchasing power represents the same vertical distance on the graph:

https://fred.stlouisfed.org/graph/?g=124bu

https://fred.stlouisfed.org/graph/?g=124bC

On comments in general you always have a lot of paid writers work for government organizations of different countries, NGO’s, services etc. in order to manipulate the results of a blog and the opinion of the readers so alternate its message. With that you have to live even more as more public your vlog attracts. But you do good. Give a sh.. on some comments. Just steels your energy.

HH – unclear if you meant your energy was augmented by auto-c when you meant stolen…

may we all find a better day.

Harry, you should talk to our local expert demographer William. He’s not happy census data is not collected every year.

Funny how you could do the work yourself maybe….? have an original thought or two, god forbid

I know it’s anecdotal but I haven’t had a single person I know tell me that bought that SUV or RV or new furniture or exotic landscaping etc etc etc because they feared it would cost more next year. In every single case it’s been an I wanted it now, so I bought it now mentality. I think for the most part it has been that simple. Delayed gratification is extinct.

I can’t even tell you how many realtors and mortgage brokers I know who are making oh about zero $$ these days and they are still spending hand over fist. Not one but 2 new Teslas in the driveway, Aspen ski trips, it goes on and on. The Great American Consumer is about as stubborn as they come and they will just keep on spending as we are seeing, until Armageddon dawns.

Also anecdotally, lots of people I know have said they’re buying cars, houses, other hard good before they go up in price more.

Home prices are going down in price

My neighbor bought tesla and it has gone down in price 20 percent part of price cut made by tesla

No banking crisis will concern most consumers unless it results in mass layoffs.

Interesting that almost all responses relate to sure lets spend. What happened to conserve and save?

My plan has always been save and conserve for tomorrow that way you can ride out what is happening now and hopefully tomorrow

At the risk of sounding like a broken record, the world has just slogged its way out from the doldrums of a global pandemic where we all felt a bit afraid and schizoid and struggled with protracted bouts of existential anguish. Nothing really feels quite the same or **right** ever since, either; there’s a lingering pallor to most things.

It seems not unreasonable to think that this has had a reverberating impact on the idea of deferred gratification. It’s not that people are buying & horsing now before being priced out later — it’s that collectively, we’ve all been put in touch with the finitude of life, and of youth.

Just my observation. I’m a saver, by the way…but damn…why, anymore?

Sorry, not me.

I’m pretty frugal, somewhat have to be.

Being single and retired the pandemic didn’t affect me much.

My spending patterns not changed one iota.

I happen to think some parts of the middle class and the upper middle class are overpaid. Very job dependent.

Compensation is under discussed.

Should this car mechanic get paid half what this HS teacher gets paid ?

Should this other HS teacher get paid only half what this other auto mechanic gets

paid ?

Should medical specialists get paid twice or three times what a PCP gets paid ?

Hah. Never discussed in the media.

In my opinion that is quite bizarre.

It is what it is ? And that’s it ?

Agreed bullfinch. I have been retired for 10 years now and have the same net worth as when I retired. A conundrum for economists has been…why have retirees not spent down their savings like the economists planned? Well now maybe we are spending…

“I’m a saver, by the way…but damn…why, anymore?”, for peace of mind. Savings are like storing water in reservoirs. Lakes Mead and Oroville were down but they weren’t out and now they’re coming back. I’ve been retired a few years myself and now peace of mind means more to me than things. It’s frustrating that till recently my nest egg couldn’t generate any real income, but I’m frugal and got by. Maybe now with higher rates I’ll treat myself a bit. I see stories of people waiting in line at food banks trying to get by for another week and am thankful I’m not there with them.

I’m donating food to food bank,there is a real need only going to get worse,I buy everything on sale . This month 1$ peanut butter, cereal $1.29 pasta 1$ 1$ spaghetti sauce.If you can afford even $20 a month .Might stop some kids from starving. I was food deprived as a kid ,nothing worse

My ex-wife and I saved and lived a decidedly spartan if not colorless life for over a decade. Didn’t go out drinking, no vacays no razzle dazzle. We were punished as savers, but we still socked every extra anything away. Long story short, I lost most of it and my dream house in a divorce a few years later and fell into a protracted season of wayward exploits and to-hell-with-it-all. During my little Rakes Progress, I rented a glorified dojo with a mattress, a desk, a percolator and a fridge full of Carlsberg. I saved nothing and did whatever I wanted without reservation. “I’ll figure it out,” was my mantra, and I always managed to sneak by.

Those were some of the most deeply satisfying years of my entire life. I didn’t expect them to be at all. But the anarchy of your life burning down and being forced to start again from scratch really forces you out of certain fright/freeze/fawn loops that you didn’t even realize you were stuck in. I recommend it.

I’ve since returned to my previous parsimony and let me tell you — it’s a drag. Peace of mind is that the sun is going to come up tomorrow. That’s about the surest thing you can bank on.

Lake Mead is not coming back btw. Oroville may be, but we don’t know for how long. Just wanted to correct that. Mead and Powell are still in bad shape, but I know that wasn’t the point of your post. I will always be a supersaver. I like the security it gives me, even if it is a false sense of security. I also hate how excessive and superficial our society has become in the past few decades. And I loathe the corruption in our financial markets.

I am trying to walk a path somewhere between Tom and Bulfinch. I was pretty frugal during the pandemic (and before), but a health crisis has made me realize “it is later than you think”. So I am spending a bit to improve my comfort at home, yet managing to do some CD laddering with the rest of my modest savings. And I still work and earn an income.

I understand not wanting to end up on the bread line, but I also understand wanting to enjoy some of the fruits of one’s labor before the final buzzer rings.

HQ

I get it. I’m out here in NE Texas and would love to be back in the Pacific Northwest of my birth using my national parks senior pass to revisit National Parks and go camping in the National Forests, see the sights, and frankly just be a big kid again. I don’t know what you want to see, but maybe there’s a way you can pull it off on a budget. When I used to travel I camped along the way, made sandwiches, or whatever. That’s all I could afford. Years ago I scraped together enough FF miles for a trip to Alaska (a bucket list item). I had to go in the off season after Labor Day when all the lodging prices dropped, but who cares. The bugs weren’t there, the tourists weren’t there, the glaciers were there. Had a blast just seeing the sights and taking lots of pictures along the way. I hope you can work something out and get to do some of the things you want while you still can.

Many of us are running out of tomorrow’s.

Flashman, I wish you well.

Others are deeply discounting the future, and spending as if there is no tomorrow anyway. No worry, someone will take care of them, right? They’ll dance and sing until they aren’t hungry anymore. The world, the job market, and the financial system magically provide, right? It’s very subjective, until the wolf (not this one) arrives at the door. Then we see whose reality holds up. I’m a cautious guy, since about age 40, and thankful I found my footing.

The parable of the cricket and the ant is a handy bit of propaganda to keep people fearful and fast to their harness.

bul – and presume either would be ruthlessly extirpated if found in the house…

may we all find a better day.

Perhaps it’s even more pernicious than a “buy it now, because it’ll cost more tomorrow” mindset.

That sense of apocalyptic doom that gnaws at us:

“Buy it now, because they’ll be no tomorrow.”

But then you won’t need it and can’t use it, so why bother wasting the last few hours of our life by going through the hassles of buying something, LOL

Lol…Because you’d enjoy it right now, and tomorrow’s credit card bill is uncertain?

In any case, I’m still looking forward to tomorrow, if it includes your great content. Thanks Wolf! 🙏🏽

…that powerful,delicious, (but usually habitual and transitory) dopamine hit (see older term, ‘the flashpoint of money in a pants pocket’)…

may we all find a better day.

Hi Wolf, Right now there’s a bank crisis, but how big and how big an impact do you think a commercial real estate downturn will be? and if you had to guess how will it play out? Thanks

As soon as unemployment picks up they will force people back into offices.

Where are consumers finding the money to support this kind of spending?

The majority have to be feeling like a boa constrictor is around them. Because costs are going up faster than any tiny raise they receive. If they get a raise at all.

This has to lead to more consumer debt, I would think.

Yes, but the top 5% to 10% of the income and wealth distribution account for an outsized proportion of discretionary spending. The asset mania supports spending by these people, with fake wealth. That’s been going on for several decades too.

I wonder how much money is from reverse mortgages aka money from bubble (fake) equity valuation. Whatever happens to those reverse mortgages when there is a default? Anyone know? Taxpayer covers. Hence moral hazard and wild spending?

Housing should go down but its not. Inflation should cause people to stop spending but they are not. Its almost like Covid made people realize life is short and everyone has become desperate and are willing to spend everything to experience life like normal…

What happens when the um rapture doesn’t happen and life must go on? Everyone demands government pays and we enter hyperinflation. Should i invest in Japan or somewhere else? Ugh…

Tom Selleck is out there hocking those. Dang you Magnum PI! I trusted you and your smooth Hawaiian shirts.

The public will clamor for “bread and circus” but will be thrown “under the bus” along with the economy and markets to save the USD in order to preserve the Empire.

Policy toward Ukraine should make that obvious. There is no sacrifice which the Neocons who control foreign policy, the MIC, and their lapdogs in Congress won’t impose on the American public for that purpose.

No hyperinflation until the US suffers a major military defeat and the USD loses global reserve status anyway.

AF, IMO there will continue to be bread — as in soup kitchens, food banks, etc., as well as food stamps, all as now,,, unless and until there is total shut down of USA GUV MINT…

Ditto for the circus, aka the propaganda machine continuing, as now, turned on an average of 14 hours per day per house plus all the nonsense going on on phones and computers for entertainment,,,

In fact, WE are already at the bread and circus stage, in this case at least WE the PEONs AKA the PEEDONs, and it is clearly one reason we have not had major riots, etc., YET — emphasis on major!!

Not so sure we will have hyperinflation when USD stops being the ”major” reserve currency.

When I traveled throughout Britain approximately 14 years or so after Suez IIRC, food, beer, and lodging were very cheap there as compared with USA,,, and the wages were waaayyy lower than USA.

E.g., a 20oz Guinness was one shilling or about $0.12 everywhere in Ireland except Dublin, etc.

Navies were getting 2 pounds Stirling per day, almost exactly what I had been getting per hour doing that same kind of work in FL, CA, OR.

As retired lifelong savers, just the 4 point rise in interest rates has us smiling. We doubled our income and spend all the extra interest earned on our children and grandchildren. Plan on spending even more as we get closer or older toward the end. Scares my wife but finally spending is fun.

Whacked by Inflation ,They’re Still Not Slowing Down :

Bubba : Your smile is going to enlarge if things stay on current course

We are seeing those changes in in Wolf’s Charts

Still a Minus – Offset $ amount amount however as Inflation is still over

current Interest earnings > The rate increase ” is working and in a good way Slow , Sure and Steady

Let Hope with time passing The Minus and Offset will change to a + with actual earnings over Inflation . Only if the Fed Chickens out-that may happen will the course revert .

How does one double ones income with a 4% rate increase during a 5-6% inflation cycle?

Did you have an annuity settlement but called the number at JG wentworth? “Have a structured settlement but Need Cash Now!?”

Lol

Don’t know the couple.

But say worth 10M all in bank. They were making 0.5% … 50k.

Now making 400k on 4% (money markets, CDs, whatever). Lucky them !

My perspective.

Their costs went from say 80k to 87k

(8% inflation).

I guess they came out ahead. Way ahead.

No wonder they are happy.

They are “ahead” from a cash flow perspective.

Their “seed corn” (purchasing power of their assets) is also being eaten alive in your example. where they actually lost $470,000 in one year.

It’s just that $10MM is enough where it will take a while to notice it in their ability to afford their current lifestyle. Given enough time, they will still end up in the poor house. Look back to the 60’s and project forward to the early 80’s.

Augustus,

My simple example:

10M + 400k – 87k at end of year.

How did they lose 470k ?

You are reading something into this that I did not intend. Or you are bringing economic forces into account that I mistakenly (?) ignored.

Please clarify.

Look at my response to the post below yours. The answer is they aren’t better off, which is obvious to anyone who understands economics and math.

This outcome is inevitable, in the aggregate for the entire economy, because there is a complete disconnect between the amount of household “savings” (aka, “wealth”) and the supply of goods and services in the economy.

The notional value of these paper claims has been expanding far faster than actual production for decades since the early 80’s during the entire disinflationary period of falling interest rates.

If there really has been a LT change in the inflationary mindset, this alone is enough to make the majority of Americans poorer or a lot poorer and gut their living standards, with or without losing their jobs and/or a major bear market in asset prices.

A recession, much tighter credit standards and end of the asset mania will just make it far worse.

Augustus,

You can ignore my previous response to your reply.

Ok, I think I see your point though

not entirely sure.

The couple’s seed money, 10M, is essentially reduced to 9.2 or 9.3M

due to inflation. This does make sense unless the items they need to purchase or will choose to purchase going forward aren’t being affected by inflation at a 7 to 9% clip.

But yes I believe I see your point (?).

Augustus,

While you make an excellent point the couple said they were pleased with doubling their income.

My example was simply meant to demonstrate they could easily have doubled their income if they had enough money already saved.

Your point hits home too well with my own situation… not 1M let alone 10M in savings.

To sufferin

An old couples math goes like this. Never touch our savings $. Income + Interest earned is what we spend. Now doubled. Life is good with no debt. Old school way that youngsters dont understand and that is OK. Just stay happy is the way to go.

It sounds like you have an excellent understanding of your situation in life. Keep enjoying your retirement.

My income more than doubled last year thanks to rising interest rates. Simple, everyone with money in interest bearing certificates got murdered in 2020 and 2021 thanks to Covid-19. It wasn’t like they made a whole lot more it was more like their income went down the drain in 2020 and 2021. I live in Canada and unlike in America retirees got zero stimulus money during Covid-19.

Job market and easy credit have supported this behavior for decades.

Until credit standards tighten noticeably (actually, not by the basement level standards of the media and economics profession), this won’t change.

This won’t happen until the credit markets tighten the noose on the lenders who provides this easy credit. Non-bank lenders will probably feel it first.

With the boomer retirement wave at or just past it’s peak they’re flush, especially after the ridiculous run up in assets in the last few years.

I expect it to last for a couple/few years then start to tail off as they party out their excess funds, unless some big nasty black swan pops up and nails em.

Many I imagine are loading up their credit cards with no intention of ever paying the money back, and will default when fully maxed.

Yeah… I wonder about this myself. Or they have access to SECURED debt (like HELOCs) and know that inflation favors the debtor rather than the creditor as long as the debt’s interest rate cannot be reset. So buy it now and pay it off later with cheaper dollars.

There is a limit to heloc capacity as asset prices decline. This story was already told.

We are on the cusp of a spending drop as two forces converge. Depleted cash savings plus higher rates.

Patience is a virtue. Impatience and short-sightedness limits appreciation of excess on the way up, and down.

As an anecdote (and as someone highly attuned to prices, despite my income) discounting is returning. Automotive OEMs are starting to offer rate and other incentives that they did away with entirely for the past three years. Retailers (furniture, electronics) are finally having deals. Of course the deals are just unwinding price hikes but the relative movement (and impetus) is there.

Service prices are still ambitious but the key driver there will be when employment headlines no longer bolster confidence. The last shoe to drop.

“They got whacked over the head by inflation, then they got whacked over the head by higher interest rates, …”

Hey, that’s why The Prairie Rider always rolls with a helmet on!

But my motorbike insurance policy renewal notice for this season arrived today. I checked in with my agent, who looked at a few different insurance companies for me. His answer: “At first glance it appeared to be high to me, but based upon the high performance motorbike, it really isn’t.”

And some of the other insurance company’s quotes out there are much, much higher. Staying with the same company. No, I wasn’t wearing a helmet this morning, and yeah, I got whacked over the head, damn it.

There are so many higher costs if an insurance claim happens now. It is carrying all kinds of inflation baggage. What if one of those ultra-expensive vehicles is damaged? Not to mention things like medical. I have zero tickets and no collisions, old car, super-low mileage and my insurance almost tripled this last two years.

But at least I don’t have a house in coastal Florida!

The issue with insurance is that some vehicles (like BEV’s) are totaled if there is any damage whatsoever to the battery pack. The entire car may be pristine, but the batteries are not repairable and the insurance companies don’t want the liability associated with battery fires. Even if replaced, there’s controllers and other items that can be called into question.

Ford trucks have a lot of aluminum in the bodies and frame components. Normal repair methods (a BFH and some bondo) don’t work on aluminum. The shops require specialized equipment to repair them and, in some circumstances, “training and certification” – which not many shops have nor can afford/justify the investment in the equipment necessary to qualify.

Airbags are expensive to replace and many tear up a significant amount of the interior when deployed. The side curtains tear up the headliner, some deploy out of the seats (and the seat belts have “pre-tensioners aka explosives), the dashboard, and steering wheel, and the knee bags as well.

As a case in point, our technomobile was involved in a minor accident this summer. Front bumper cover, one headlight, and a tip of the LFF. Forgetting the delays due to weird parts being unavailable, the vehicle was out of commission for 7 weeks. The cost to repair, due to the active cruise sensors, etc., was probably 4 times what it should have cost because the labor to install and calibrate all those systems was much higher. The headlight, alone (LED) was $1,500.

It’s no longer the same as fixing your 1972 Maverick.

Your old car has a higher cost of replacement than it did a few years ago. So, if it’s totaled, the payout is higher.

Not defending the insurance industry, but reality is reality.

Sounds like there’s gonna be a huge market in dismantling these cars for parts.

I know my local recycler has already had a battery explosion and fire from someone hiding one of these in the back of a normal car and not telling him about it. The local association of recyclers are having a big meeting about how to deal with them too so gotta ask him how that went…

Well, what if all these people who moved their money to a 4.5% yielding account instead of 0.1% after the publicity the SVB debacle generated around treasury bonds, now feel they can use all that extra return to buy more?

Yes, that has been happening. People with income products, such as CDs, Treasury bills, MM funds etc. are now seeing a real cash flow for the first time in 15 years, and they’re spending some of it.

Wolf can I move 457 money into short term treasuries

You need to ask your plan administrator. They may have a way to buy Treasury bills. But maybe not. It’s all about fees for plan administrators.

If you buy Treasury bills, you shouldn’t have to pay fees to do so — same with buying CDs.

:and they’re spending some of it.”

The key of course is who gets to “spend it”.

Essentially, for the past 14 yrs, the Federal Govt got to “spend” the money that was not paid out in interest due to rate suppression.

Now the lenders are being paid, and they are spending it.

So in a sense, either way, it gets spent and is an economic engine.

(the government would have you believe that is not the case.)

The difference is when rates are suppressed and fake, the spender is the govt. When rates are real, the “spender” is the lender of money who is getting his fair return.

The lender is the “wiser spender” … and “wise” is good, rational, logical, good and efficient. Govt spending, not so much.

A move from .1% to 4.5% means if you have a $500K IRA you move from $500 to over $22k – an amount equal to your SS check. That a lot of extra buying power.

I wonder if we have a cart before the horse problem. Did the government move to zirp to make people pay for their own social security? Now that zirp is gone, Heaven help those who don’t have a $500k IRA.

Those that do have had their income doubled. Isn’t this inflationary? Not going to work out too well for those that don’t. But the government can’t rob from Peter to pay Paul just so they can balance their books.

That $22 K income in the IRA is not taxable until it is pulled out, also.

Well, there is the Required Minimum Distribution that requires you to pull out the bulk of it.

The answer to your question is yes generically. It was an income and wealth transfer from savers and creditors to spenders and debtors.

I also get your point but look at what $22K buys.

When I finished my BBA in 1987, the starting salary for graduates from my university with a generic business degree was +/- $18K. Now $22K doesn’t even pay my rent for the year. I live in a good area of town but nothing close to luxury.

“laissez les bon temps rouler” – Let the good times roll. Post COVID round 2 Shock and Awe continues. We’ve seen to the run on the banks, the run on paper towels and tissue, the run on housing, the run on crypto, the run on EV’s and over priced vehicles, and the run up in food and groceries. America is T-Totally phucked up right now, there no rhyme or reason to the chaos. I look to leadership in Washington, confident that no one really gives a damn. There will be another AIG failure in the near future, the current pattern of destructive storms and tornadoes will uncover more white collar executives swimming naked under government supervision. I’m staying in my foxhole, the rat race to the bottom plays out everywhere.

“… revenge travel” certainly, and pretty understandable after a generational pandemic derailed/postponed so many plans. Not that the pandemic cooperatively went away in time for the start of the party 😏

Perhaps the most hopeful outcome ahead is where the Fed has just enough cover from tentative “disinflationary” reports, like we saw today, to avoid ‘breaking the bank’. Most banks are themselves only earning about 4.7% on invested assets, before expenses, so there is a temporal LIMIT before the banking system breaks… and we don’t want that. IMHO, the “hold” part of the Fed’s interest raise strategy is the only one that can work (for the ordinary citizen with skin in the investing game while hoping to retire someday) from here.

Great job reporting Wolf!

Americans will spend, spend, spend until they don’t and/or can’t. It’s become part of the culture and the American Dream – to consume goods and buy services. It’s a far, far different mindset and American culture than the one I was born and raised up in. The pendulum has swung just about as far as it can – in my erudite opinion. And once socioeconomic gravity pushes the razor-sharp pendulum the opposite direction it shall slice in half the ignorant masses…

Of course in this case the fish both spends and rots from the head down. Just look how government spending has increased and will continue to increase until it doesn’t or can’t. And just wait until the war expands in Ukraine. Then we shall see some more really BIG spending, borrowing and wartime inflation and supply shortages. And perhaps some mushroom clouds.

And if we are really lucky we get to live through WW3 and tell the tale to our grandchildren. I’m very glad I was born and raised in a completely different time; a time whereupon we built our lives by saving more than we spent; we only bought quality; we planned well for our future; and we stockpiled extra food, water and other supplies in our fallout shelter. Yes, I’m not kidding. We were even ready for nuclear war. Just look at most Americans now.

I bet tens of millions of Americans couldn’t raise $5000 in cash for an immediate emergency. Pathetic. Nothing wrong with being poor, but the poor people I knew back in the day could at least hunt, fish, farm, cut firewood, make clothing and shoes and in general provide everything necessary for human survival, e.g., food, shelter, water, clothing, heat and medical care. And most could raise enough money in an emergency without government handouts. Just look at Americans now. Many don’t even know what gender they are.

Conclusion: I don’t think this new generation can keep Western Civilization from totally collapsing. And I think that Americans will suffer massive casualties on American soil during the next great war. But until then Americans will surely eat, drink and be merry and post it all on social media and continue to spend, spend, spend right up to the bitter end.