The ridiculous spikes, fueled by the Bank of Canada’s interest rate repression and QE, unwind metro by metro, some lightning fast, others more leisurely.

By Wolf Richter for WOLF STREET.

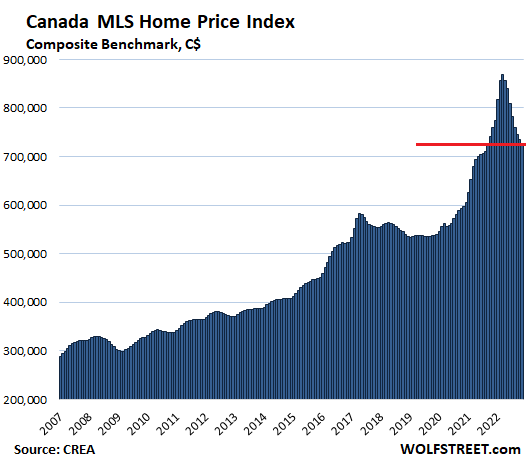

The Canada MLS Home Price Index, which tracks all types of homes, dropped by 1.3% in November from October, and is now down 16.4% from the peak in March 2022, according to data from the Canadian Real Estate Association (CREA). This brought the year-over-year decline to 4.4%.

In Canadian dollars, the composite benchmark price dropped by C$142,300 in the eight months since the peak, to C$726,000 – about where it had been in September 2021.

In the eight months up to the peak – so from July 2021 through March 2022 – the benchmark price had risen by C$162,800. In other words, it has plunged a little less fast than it had spiked on the way up during the final phase of the Bank of Canada’s interest-rate repression and money-printing binge, which ended in March 2022 with a first timid rate hike, which was when home prices peaked.

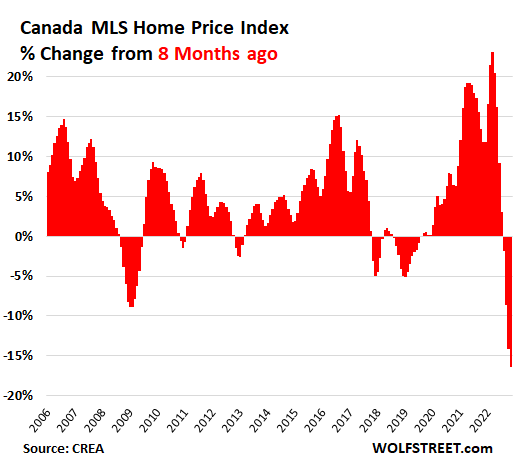

Sales volume in November plunged by 38.9% year-over-year, according to CREA. Buyers have gone on strike due to the combination of still sky-high home prices and now much higher mortgage rates. Potential sellers have gone on strike too; instead of putting their vacant homes on the market, they’re thinking, “and this too shall pass,” and they’re waiting for the sudden death of inflation and a Bank of Canada pivot. Each month that they’ve waited, they’ve been rewarded with further price drops. Turns out, he who panics first, panics best.

That eight-month drop in the benchmark price from March of 16.4% was by far the largest eight-month drop in CREA’s data going back to 2005. Part of this is that there hasn’t been a real housing bust since the 1980s, and this data doesn’t go back that far:

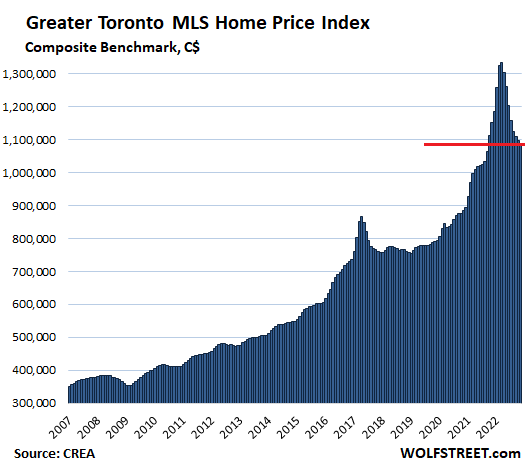

Greater Toronto Area: The composite benchmark price dropped 0.8% for the month to C$1.09 million, down by 18.4% since the peak in March, and down by 5.5% year-over-year. The price is roughly back where it had been in September 2021.

Plunge speed versus spike speed: Over the eight months since the peak, the benchmark price plunged by C$245,200. On the way up, over the eight months to the peak, the price had spiked by C$309,900:

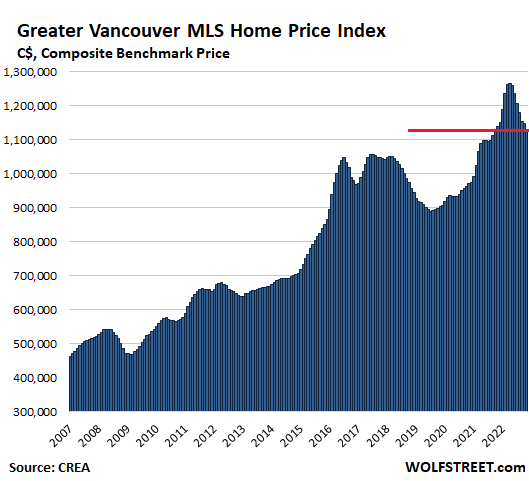

Greater Vancouver: The MLS Home Price Index composite benchmark price dropped 1.5% for the month to C$1.132 million:

- From peak in April: -10.5%

- Year-over-year: -0.6%

- Drop in 7 months since peak in April: -C$133,100

- Jump in 7 months to peak in April: +C$152,700

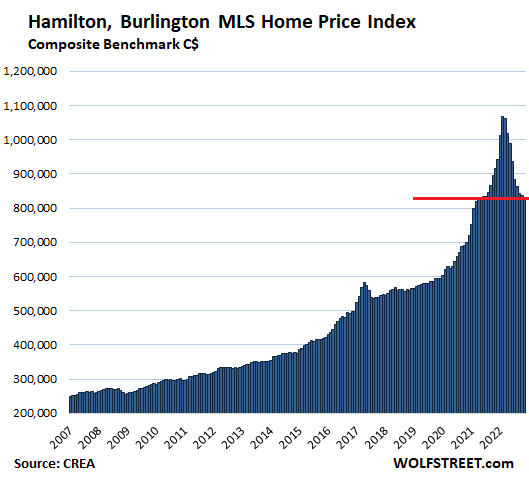

Hamilton-Burlington metro: Prices tend to move in parallel with Toronto though at a lower level. But in the 22 months between the beginning of the Bank of Canada’s money-printing spree in April 2020 and the peak in February 2022, the composite benchmark price exploded by 71%, which is totally nuts. But then it started unwinding, and has now plunged by 22.2% in 9 months.

The composite benchmark price dropped 0.7% for the month to C$831,000, and is down 9.4% year-over-year.

Over those 9 months since the peak, the price plunged just a tad faster than it had spiked in the 9 months to the peak:

- Drop in 9 months since peak in February: -C$237,900

- Jump in 9 months to peak in February: +C$237,100

Spikes like these in real estate are just funny – and a testimony to the utterly silly consensual hallucination that pervades bubble markets:

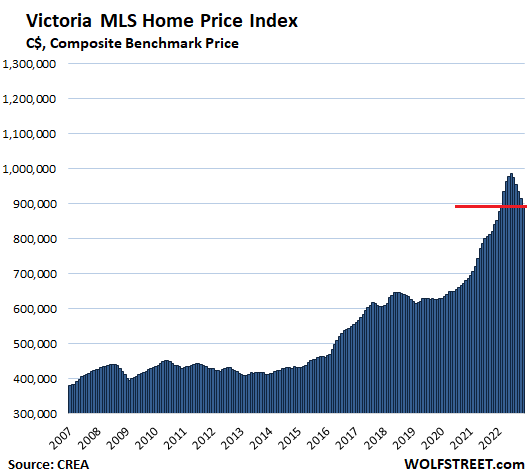

Victoria: The composite benchmark price plunged 2.3% for the month, and by 10.5% from the peak in June, to C$894,000. But given the late start of the decline, on a year-over-year basis, the price is still up by 6.4%

- Drop in 5 months since peak in June: -C$91,100

- Jump in 5 months to peak in June: +C$107,000

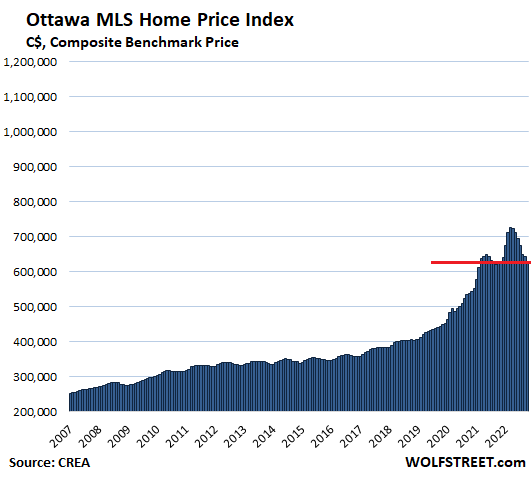

Ottawa: The composite benchmark price dropped 2.1% for the month to C$631,000, back to March 2021:

- From peak in March: -13.4%

- Year-over-year: +0.8%

- Drop in 7 months since peak in March: -C$97,400

- Jump in 7 months to peak in March: +C$103,200

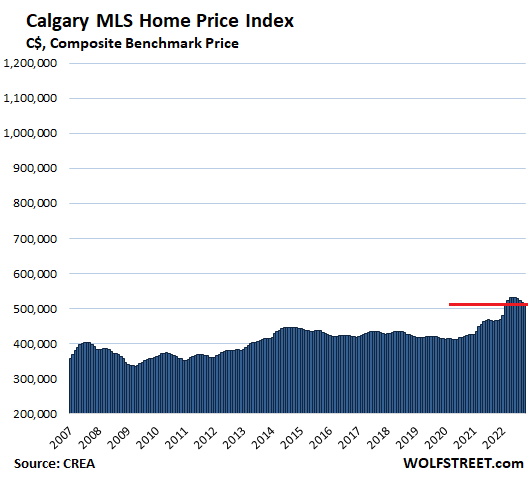

Calgary, Canada’s oil capital. Despite the oil boom that started in 2021, prices have now turned south. The composite benchmark price dropped 0.7% for the month to C$513,000:

- From peak in May: -3.6%

- Year-over-year: +10.4%

- Drop in 5 months since peak in May: -C$19,200

- Jump in 5 months to peak in May: +C$63,900:

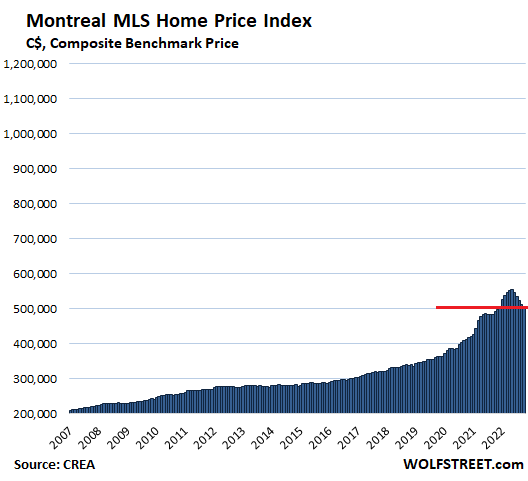

Montreal: The composite benchmark price dropped 1.3% for the month to C$505,000:

- From peak in May: -9.1%

- Year-over-year: +2.8%

- Drop in 5 months since peak in May: -C$50,800

- Jump in 5 months to peak in May: +C$54,500:

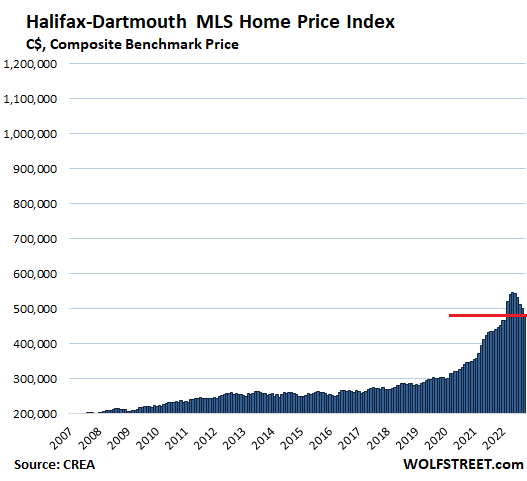

Halifax-Dartmouth, a normal-ish housing market until it suddenly went nuts starting in April 2020. Over the 25 months from April 2020 to the peak in May 2022, the benchmark price exploded by 82%, just WHOOSH, as QE and interest-rate repression turned buyers’ brains to mush. And this is now unwinding.

The composite benchmark price plunged 3.0% for the month to C$484,000:

- From peak in May: -11.5%

- Year-over-year: +9.5%

- Drop in 5 months since peak in May: -C$63,000

- Jump in 5 months to peak in May: +C$95,600:

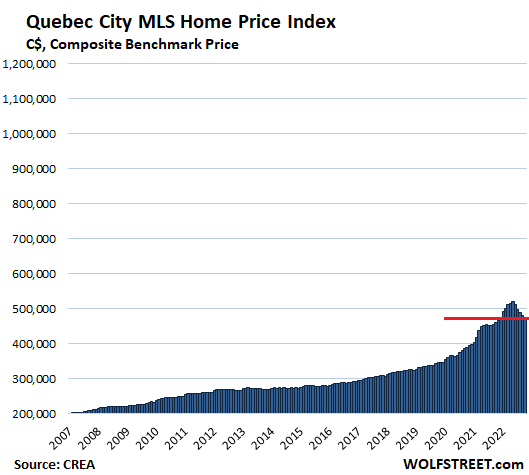

Quebec City: The composite benchmark price dropped 1.1% for the month to C$475,000:

- From peak in May: -8.7%

- Year-over-year: +3.0%

- Drop in 5 months since peak in May: -C$45,400

- Jump in 5 months to peak in May: +C$50,600:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

These are some serious loonie toonie drops.

so friend shared his MLS data with me for november in Tucson

closes – Nov 2021 – 1,600 —- Nov 2022 – 780

Listings Nov 2021 – 3,000 —- Nov 2022 – 3,000

days on market Nov 2021 – 19 — Nov 2022 – 26

didn’t get prices – but STABLE with a few coming down 5%

I went to Tucson a few times while living in PHX. I thought the place was a total dump. I could never understand the appeal.

Last time I was there was with a work colleague who was looking to buy an undeveloped lot to build during HB1, as speculation of course. He never did fortunately. It seemed to be in a remote but supposedly desirable area, near the foothills. Dirt roads where we went, at the time.

I lived in Tucson for three years. I enjoyed access to the Catalinas, Sabino Canyon, and the beautiful desert outside the city. It was hot, but cooler than Phoenix at an elevation of 2,600 feet. If it wasn’t quite so hot in the summer, I wouldn’t hesitate to move back. To each their own.

AF,

On Tucson’s appeal,

1) Warm/Hot and dry

2) Until maybe 2018/2019 was one of the cheapest housing mkts of the top 100 metros.

There always was a sort of run down (never built up?) desert town vibe to most of Tucson…but the weather was good (except for blinding summer heat…but a *dry* blinding heat…).

And the truth is there aren’t many metros in The Southwest (currently known as “Escape from California”).

If you pass on Tucson, where are you going to look? Yuma? Tucson is Paris compared to Yuma.

The truth is, the Southwest is pretty inhospitable to human habitation – plenty of empty, buildable land but nowhere near enough water.

Now that California (coastal) is Paradise Betrayed/Fumbled, the reverse Okies are going to find few warm havens between San Diego and…Oklahoma.

I lived in Tucson for a couple of years and learned to appreciate the desert. I spent a lot of time on horseback on those dirt trails and glad that I did. It is not Phoenix and offers something different; just not for everybody.

stable only means that the prices are about even to where they were a year ago, not at the peak in mid-year. just wait until the new year and people start to dump homes on the market with minimal demand.

Can’t happen here (USA)…

– everyone wants to live here

– no one needs to sell

– no one will sell and give up their 3% x 30yr fixed

– there’s a housing shortage

– everyone has so much equity, no pressure

– sellers aren’t going to just give it away!

Signed,

About 10 regulars on this site

It is quite reasonable for anyone who owns/ invests in real estate to be a cheerleader and in denial of reality. This type of mentality happened in the last bust and even some die hards held this mentality even after the bust started awhile. It helps keep depression away so this can be expected… All the way to final insolvency.

Lol just so true. Down in Texas last year there was basically a big group of people moving in with dreams of mass purchases and basically becoming slumlords. They’re the poster boys and girls for the ones who constantly insisted the Fed would never stop QE. Then the Fed would never raise interest rates. Then the Fed would start QT.. Their whole business model was built on denial.

Everyone wants to live here 😂😂😂

Like America…. This America… Sure about that?

Not to fret, Canucks. Trudeau’s got your back. The legal annual immigration target has been raised to 500,000. The idea is, they can’t all live on the already overcrowded streets.

What…zero comments still? Okay, I’ll open the bidding at one half ounce of silver for each property up in iceberg land. Hell, you can’t even get a decent tomato from a place that close to the north pole! On second thoughts, one sixteenth ounce is generous enough.

Here is wake up call for US in coming spring. As Fed Pivot fantasy is evaporating, mass layoffs will start in nex quarter, and the folks in H1B will have to force sell their houses in 60 days (H1B grace period without job), because it’s hard to go back to India without a really good job and maintain a depreciating house in US.

So these sellers would be pricing their houses at 20% below market, given thugh mortgages. This is because, in Seattle area and Silicon Valley, 80% of houses priced at fantasy Zestimates have been on market for > 120 days despite consistent price cuts or have been pulledboff market due to no interest. This is because Zestimates are seriously lagging house prices on the way down.

So coming spring, we can expect more than 100,000 houses going on sale at 40% below peak price (20% from market and 20% more from forced selling).

I believe that’s when the media coverage on real estate will really get negative and cause sellers, who were postponing for Fed Pivot to suddenly reevaluate.

So coming spring may be a good time to buy.

given the 100% premium for physical

you nailed it

The really difficult question is ‘ How do we recognize a bottom when it occurs?’ The top has obviously occurred.

Usually when nobody wants to have anything to do with the market is a good indicator.

Doesn’t it seem like this time around we won’t have such a rapid recovery from the bottoms in markets? Housing in particular should have a longer trough even thinking back to the last housing bust in Portland it took a while before it got crazy again

blood in streets

Yeah it took around 5 to 6 years if I’m recalling right for the bottom to hit after the GFC and the Great Recession started. (officially in 2007 Iirc) There’s constant denial and rationalization that makes resistance for each drop, until the unavoidable facts can’t be denied anymore. One difference now of course is the Fed raising interesting rates and QT, really for the first time like this in 40 years. But it’ll still probably take a few years for the full effects to be felt. And Canada’s housing bubble is even worse than the USA’s which is saying a lot. Australia and NZ still worse. Used to be just Toronto and Vancouver that had such bloated home prices that even the surgeons and execs were struggling to afford them, now it’s spread even to the lousy, bitterly cold and thinly populated mini-towns throughout Ontario, Manitoba and the Maritimes. Same is Australia with the negative gearing they’ve had going on there.

*raising interest rates, man must be more tired than I thought from the holiday shopping.

the big difference last time around was the Fed was able to lower interest rates to prop up home demand. this time, they have to be careful about inflation.

@Harry Houndstooth

Sideways action. That is, central banks will eventually pause (not pivot, per se), and a new equilibrium will take hold. I think the new equilibrium will be obvious to notice.

So Wolf, how does one short this thing? Do the big Canadian banks have exposure or does the government simply pick up the tab?

Canadian banks have recourse against buyers, not sure if that is meaningful, but Canadians cant just turn over the keys and walk away.

aren’t canadian loans 30 year amort with 5 year resets?

joedidee: yes. There is a 25 year option as well. There is flexibility in the term, but 5 years is most popular.

There is no more 25 yr option in Canada anymore.

Oops, I meant to say there is no more 30yr option

Short the listed private mortgage insurers if you think home prices will keep falling. That would give you the most leverage if everything falls apart in 2023. They’ve yet to “break” the Chinese. The city of Richmond Hill, Ontario which is a Chinese city is holding up the best in the greater Toronto area.

When it’s cheaper to buy a house then it is to rent it, then you are somewhere near a bottom.

Correct HM… In fact, folks can use the rent to price ratio to help determine when it might be the time to buy, versus continuing to rent.

That’s true but many of the cities in Alberta, Canada have been cheaper to buy than rent and they’ve still fallen from 2010 to 2021 the last 11 years.

Hmmm, I guess I can see that. My rule doesn’t take in to account the effect of real estate investors. Maybe my rule would be valid if the housing market only consisted of people who are looking for a primary residence?

Alberta is special. We have far fewer restrictions on development, hence the lower prices.

The beginning of the bottom usually occurs when some bigger players go BK. Then depression sets in and the market wallows in that for a bit.

These are probably early days as long as the Fed stays around current interest rate levels. It doesn’t matter if there is demand; if people can’t show the income to hit the mortgage payments then they can’t be buyers.

The only thing, imho, bailing out the housing market long term is if there was real, not nominal, wage inflation. But that’s evil and bad as far as wall street and the Fed are concerned, with the Fed willing to put the economy into a recession lest -3% real wage inflation lasts. So, some sort of correction pretty much has to happen, with the big question being whether people buy/build a ton of MFDs with SFRs getting corrected over the long term through inflation and weak prices, some kind of sustained declines, or a combination of the two.

Canadian houses are expensive, even compared with the United States. Hopeful smaller, cheaper houses are still available in both countries.

Good luck to people everywhere, trying to be self-sufficient.

The thing is though, whereas there are a lot of cheap places to live in the USA, damned near most all of the populated areas of Canada have really expensive real estate.

True but there are areas of affordability in small towns in the Prairies and Atlantic Canada. Some of these places have lost a lot of population and there are many excess houses as a result.

Sold my 40 year old 4 bedroom bungalow in a pulp mill town on Vancouver Island for 780k.

How to estimate a bottom? I will take a kick at it, using the Royal Bank of Canada’s (RBC) affordability stats from April 2022. Affordability compares housing costs to income.

Let’s compare the affordability of a house in April and compare it to the affordability in earlier times. To get back to the affordability of October 2018, (which was a crazy peak, but not as crazy as the current peak), house prices would need to fall about 22 percent. To get back to an affordability more in keeping with the long term average, house prices would have to fall back by about 38 percent.

You could argue that interest rates are higher now than they were in April 2022 so that current affordability is even worse than the RBC stats that I used.

I already know the bottom it will be when the first corner lot property sells in Richmond Hill and in Markham. The Chinese will always buy a corner lot property over any other property and a local non-Chinese person will always buy anything but a corner lot property. The Chinese are completely out of the housing market as buyers and are usually one of the last buyers but when one Chinaman buys all the Chinese buy at the exact same time resulting in a one month double digit increase in home prices.

World cup : Canada (-)1 : (-)2 Qatar.

Ayn Rand (Atlas Shrugged) enrolled in Social Security for the last 10 years of her life. Medicare is another welfare program covered her medical bills due to smoking. Rules for thee not for me.

And she was the breadwinner – supported her husband throughout their time together. How’s that for Libertarian self-sufficiency?

Lots of drama in her novels; characters were 2-D, black and white, good/bad. Pitiful morality fantasies. Big medicine for adolescents, though. Too bad Greenspan swallowed her tripe without chewing. I do think he came to understand that his idealism about “markets” and “invisible hands” were truly imaginary.

Upvote

1) Greenspan did not follow Rand’s ways, if he had we wouldn’t be in this mess. Rand was also not a libertarian.

2) Rand’s books are brilliant. Literature and entertainment need more black and white and less pseudo-clever gray BS. Her villains walk among us too. Alexander Dugin is a real life Rand villain of immense negative importance.

We The Living > Crime and Punishment

I’m not sure this example is really relevant.

People who think taxes should be higher generally don’t pay a higher tax bill than they should. And then people talk about the “rich” should do this or that but it is never themselves even if they make the top 10% (which is only like $100k)

Just because you think the rules of society should be different doesn’t mean you follow how they are today.

She paid massive amounts of money from taxes on her income, book royalties, and the cigarettes that killed her. Her opposition to those programs is the other reason she had the right to them.

From a Toronto Star headline: “… it now takes more than $200,000 in income to buy a typical Toronto home” – in Canadian dollars.

The Bank of Montreal is selling shares to raise capital in case of a housing price downturn.

USDCAD reached a lower high. When McC takeover the House, the holes

in the house ceiling might rain on USDCAD sending it below May 2021 low.

Canadian RE, in US dollar terms, might peak.

Blue for u Canada…

8. Friendly purposes only…

9. I want a job that is not jobby. Where to find a work that is not worky.

US Personal Retained Earnings (saving) dropped from $6.5T to $426B.

Canada Personal Saving might be worse. RE is up, yes, but stability is down. The more we spend, the higher the nominal GDP. But

there isn’t much left in real and nominal terms.

Liquidity went south.

It had to take a team of higher educated

To simplify the word “savings”.

Thanks for my morning chuckle.

Canada can do all kinds of things internally than the US, but it can’t have an independent interest rate policy, at least not for long.

Mortgages reached 21% in the early eighties. I had one, taken out a year earlier at 14 %, selecting a one- year term because ‘obviously’ they could only decline from 14. But they didn’t reach 21 % because of a Canadian decision, they did it because of Paul Volcker’s decision.

I agree with his decision now, but whether anyone agrees or not, Canada can not afford interest rates significantly different than its largest customer and competitor for capital, with a three thousand mile shared border and no capital controls.

If Canadian interest paid on bonds etc. was much lower than US, its capital would flow to the US. If significantly higher, the C $ would rise to levels bad for the trade balance.

Canadians like to chuckle a bit about the brief period of parity for the C$ and even a bit above the US$ but the C Ministries of Finance and trade were not amused. Nor was C tourism, cross- border shopping at border towns, exporters, etc.

No doubt the BoC does lots of work, but its interest rates could be set by an AI robot, with one variable being most of the input.

Yes BoC probably has 10 people who’s job it is to call their Fed friends and ask them what they should do next.

It’s like Industry Canada, who manage our radio waves by copying and pasting the FCC regs, but only after going out for a few dozen long lunches.

Any data on the value of Canadian ARMs scheduled to reset in the next 6 to 12 months? Maybe ARMs are not a “thing” in Canadian real estate this time around?? If they are a “thing”, those sitting on their properties awaiting a resumption of appreciation may need a plan “B”.

Also your observation that the drop from recent peaks in almost all charts is steeper and faster than past peak/drops on the respective charts. I think Vancouver and Calgary were the only ones still with smaller historical past drops from past peaks. But maybe those areas are just getting started on their drops. Guess time will tell.

Very interesting article. Thank you.

ARMs in Canada generally reset in 90-day periods. And ARMs are rarer than variable rate mortgages (VRMs) which reset instantly. And variable mortgages are definitely a thing in Canada. In the peak months from end of 2021 to early 2022, something like 50%+ of overall mortgages were taken as variable rate instead of fixed rate as the differential was hovering at 1-2.5% at that time. Traditionally, fixed rate in Canada had always been the majority of mortgages. From speaking with people working at the big 5 Canadian banks, almost all VRMs taken a year ago have hit the “trigger rate” where payments need to increase as the new interest is greater than the original payment. For those with ARMs, payments have increased by 50%+. I would say prices are down 5-10% YoY in most metro areas. No meltdown yet considering interest rates which is crazy as a $1M mortgage in Toronto is $5k a month in interest at current rates. That’s about the entire take home of a $90k CAD per year job in Toronto, which is above median.

Antwan,

Damn; a monthly mortgage payment doubling for a person with an ARM? Maybe it’s a good thing it’s a rare type of mortgage. And resets 4 time a year?

“Hey man, you going to Vegas to play some blackjack over the Holidays?”

“Hell no. I just bought a house with an ARM. When I’m gamblin’, I go all in, eh!”

And I said math was easy. Not quite doubled. Up by a hell of a lot still to go from two-thirds to one.

ARM vs VRM is 2 sides of the same coin. Your interest cost is roughly the same with either. Do the payment increases hurt? Absolutely not for us. Does the interest cost hurt? Yes, in the context of hindsight, the difference between taking fixed and ARM would currently be a car payment in interest. That said, our mortgage is modest and we have relatively safe growing income. For those who took out an ARM at 5x income and might have a job loss in the household? I expect them to contribute to the economic contagion we’ll see in the next 2 years. Welcome to Canada, expensive housing, collapsing healthcare, criminal impunity, wage suppression, and falling living standards. But at least Trudeau is working to take away some firearms.

Apparently foreign buyers are barred from buying Canadian real estate starting January 1st 2023. This should have a big affect on Vancouver and the province of British Columbia but not much affect on Toronto and the province of Ontario. The foreign Chinese drive the market in British Columbia but the local Chinese drive the housing market in Ontario.

They aren’t banned but they are going to pay a 30% tax.

Last I heard it was a tax. Not an outright ban.

Yes, Canadians are dumb enough to scapegoat a hand that feeds them. Just in time to desperately need that hand too.

Interesting definition of scapegoating.

On upper end properties the chinese have been the marginal buyer (with the willingness to overpay). Now surrounded on all sides by chinese immigrants with $2 million plus homes. Canadians can’t/won’t bid that high.

This also drags lower priced properties higher.

Hence price appreciation extraordinaire.

BTW – my new chinese neighbours claim everyone in the educated/skilled middle class in china is trying to leave. So sell a crappy flat in Beijing for a couple of million (not hard given their insanity), and buy a lovely house in Canada for less, with a nest egg to live on.

1) US retained earnings went south. Canada is depleted their savings.

2) The Fed hiked. UST6M is the highest. US 10Y minus reached

minus (-) 0.91% last week.

3) Raindrops from the House ceiling might cause an extensive damage to US dollar and US Treasuries floors.

4) The front end is hooked to the Fedrate, but the 10Y might popup above the 2Y, because there will be no buyers for a house marked for demolition.

5) Slightest wind could come from behind when yeast expected.

Hi Wolf – quick question about US housing.

30-year mortgage rates seem to be dropping despite recession fears and the FED’s recent hawkish comments. I know you don’t concern yourself much with day-to-day data, but do you know why this is happening? Do you think it’ll continue to settle over time around 6%, and if it does, will house prices stabilize or continue dropping for some other reason?

I’m still new to analyzing economic data and I’m confused as to why mortgage rates have dropped for a month or so. Thanks.

This is the chart I gave you the other day. As of Friday, the mortgage rates were still above the low end of the trading range. What happened so far is a classic retracement, and it’s within the normal range. I explained this last week. The 10-year yield has already bounced off:

https://wolfstreet.com/2022/12/04/drop-in-10-year-treasury-yield-mortgage-rates-is-just-another-bear-market-rally-longer-uptrend-in-yields-is-intact-with-higher-highs-and-higher-lows/

“Greater Toronta MLS Home Price Index”

“Toronta” is certainly easier to remember than “Tkaronto” (which is growing in popularity to address concerns about oppression of Indigenous people). In Mohawk the word Toronta” means, if I am not mistaken, “where there are mortgages under water,” which is not dissimilar.

LOL Thanks

That’s like when you translate “La Quinta” to English… “Next door to Denny’s”.

I was looking at the 2022 CBOE estimates through 2032 and what strikes me is that interest rates have already exceeded the projections they had.

As the Fed keeps liquidating assets, I wonder if there comes a turning point where the markets just wont absorb the debt without much higher long term rates.

Treasuries have always been the safe haven in turbulent times, which represses rates, but I really think we are heading into another “sell everything” time, when equities, real estate and Treasuries all fall together. Many companies are trading near all-time highs due to price increases to the consumer.

Maybe. But not everyone is as pessimistic. Jeremy Siegel said today that “inflation is history”. Over. Peaked. On the way down. And he’s anticipating a 15% stock market rally next year. And he’s said he has never seen everyone so bearish as now, which is usually indicative of a market bottom.

I hope I live long enough to see the U.S. stock market ponzi finally implode some 80+ percent back down to fair market value. Like everyone says it can go on forever as long as none of the bankers are arrested and locked up.

None of the bankers are going to be locked up because they didn’t do any of this. To the extent that there’s a bubble it’s because of fed and perhaps US treasury policy.

I’m going with Gareth Soloway on youtube he has one of the best track records for calling the markets. He says the S&P500 index will drop 30 percent in 2023 and the best asset class will be the precious metals in 2023. He also points to a ten year bear market in stocks.

He could be right about precious metals. Right now they are universally hated and despised which is exactly when you should be buying.

Does not sound as if he has firm grip on reality. But then that is what Wall St. pays him for, to keep people buying stocks… In the business world, people do not often say what is true, as much as they say what they are being paid to say. Smart people know the difference.

Neil – My problem with that idea is that we have not yet seen the impact of home price declines on the economy and markets. I seriously doubt the Fed will lower interest rates in the first half of the year, which will be enough time for cause home prices to establish a downward trajectory.

The Federal Reserve has 8 trillion dollars of Treasuries and MBS on its books and it needs to sell to someone. The US Fed is not the only country that is selling assets, nearly all the central banks, from the ECB to Fed to Swiss bank are selling…which means that buyers must first absorb all those sales to just keep prices flat. Markets are fungible to some extent, so debt sold in Canada and Europe and England also impacts prices of US assets.

Google “Jeremy Siegel: Stocks Will Continue Their Upward Trend.” That should thoroughly discredit anything this degenerate clown says.

Tell Jeremy Siegel that inflation isn’t over until they reverse the 20% three year inflation spike from 2021 to 2023. If he’s OK letting 20% inflation stand, he has zero credibility.

I think I get what you’re saying, but maybe not the right terms. The Fed is not liquidating assets. The assets are coming off the books as they mature and they are not selling them before maturity. As far as the markets not absorbing debts, that would be because the Fed is no longer buying them from the market so as buying demand falls the rates have to go up to entice others to take it on. Not absorption issues via more debt available by Fed selling as they are not doing that. Wolf, correct me if I’m wrong.

But isn’t it ultimately the same thing? As the Treasury pays back these assets as they mature, if they were held by private investors, that would be money that would need to be re-deployed somewhere, putting downward pressure on prices. Here, the money is destroyed as the Fed is paid back for its assets, so that money is no longer “out there” needing to be redeployed.

Home equity loans will probably add to the dynamics of the bust. Lots of late model expensive cars on the road in Toronto. If ppl had borrowed money of their home equity to buy bitcoin , well, well, well.

I wonder if the 500,000 permanent residents a year is a desperate attempt by the Canadian government to keep the real estate bubble going, while driving down wages?

Also to try and replace the people dying and leaving Canada for good. Canada is seeing a mass exodus of people leaving the country especially in Ontario.

Are they moving to Florida?

100% false.

Population growth

Ontario’s population reached 15,007,816 on April 1, 2022, with a increase of 55,991 people during the first quarter of 2022. This compares to an increase of 36,452 people recorded in the same quarter of 2021.

My favourite real estate measure, a horrible coastal town on Vancouver Island that nobody wants to live in, but which still experienced a jaw-dropping spike in prices during the panny (don’t worry, I hate myself for this, too, but it’s what the kids are saying), is full of price reductions. And plenty of empty houses, many of which have been on and off the market over the last year or two at various fantasy price points.

Anyways, this unlovely smear of a town saw peak prices of nearly a million (excluding waterfront and acreages) for the average shabby detached house, despite local incomes being significantly lower than the national average. Lots of people I know were buying houses as “investments” with plans to flip or rent, or just hold for capital gains. Not sure how that’s working out because the latest VIREB stats show the average price of completed sales in November was 750k. The peak here was early, in January of this year, but since then, values have dropped around 20k a month.

Frankly, as a frustrated, reasonably well off, sometimes 1%er stuck renting in this town because my value-conscious thinking just cannot handle paying a million bucks for soggy glue-and-wood-chip bug nest, I hope it continues. That might sound like sour grapes, but it’s been rather galling to watch people get rich (or, think they are getting rich) buying and hoarding houses, and blindly creating the narrative of a housing shortage in the process. Sort of like a virtuous cycle, but with none of the good vibes. Maybe call it a greed cycle?

I’d just like a return to prices where being able to buy a house and being able to afford it are the same thing.

TEMPLE

I understand your frustration… but what is so bad about this town? I thought the whole area of Vancouver Island was beautiful.

Bah ha ha…good one! VI has some great surfing on the West Coast, with some towns that are good to live in if you like pounding surf and rain most of the year. Aside from that, civilization consists of the southern tip (Victoria + Langford) and the Saanich peninsula. Victoria itself is nice but too expense. Saanich peninsula is better. The rest is just deadmill towns and reserves. Just…absolute nowhereholes with nothing but rain and unemployment.

…is it Duncan? Cuz this sounds like Duncan.

For a short time next WCS might rise above WTI. Canadian NG will rock.

I doubt WCS will ever gain parity with WTI, let alone exceed it, unless pipelines build out east or west or Canada starts refining more of its own crude (the latter propositions are fantasy). Has WCS ever risen above WTI? The reason often cited for the increased spread (now that’s typically WCS losing more value relative to WTI) is pipeline bottlenecks (TC Energy’s leak in Kansas has exacerbated this).

To Wolf’s point about the lack of long term data, the last housing bust in the Toronto area was 1989 (I remember because a colleague bought at the peak). Prices didn’t begin to rise again until 1997 or so.

TBH it’s good to see some sanity emerge with respect to affordability. And still it isn’t enough. The 400k+ immigrants expected per year for the next 5+ years will provide further stress on on the system, and with a deficit in new builds. Where do people expect to live? Speculative earnings of 20% + per year are immoral as well as unsustainable. Supply and demand will always eventually dictate market conditions.

They will double and trip up, just as they do in the third world.

Canada (or the US) isn’t exempt from physics (or math).

The basements of Brampton and Scarborough are already full or at capacity.

I am house hunting in southwestern Ontario right now.

There is no shortage of houses, plenty of houses are empty but not listed on the web.

Driving around lock boxes hang on the door and the “for sale” sign is in the front yard but no listing on the web.

There is quite a bit hidden supply.

See when higher carrying costs will bring the sellers to market.

For fun I checked the mortgage calculator.

589 k price, 5,7 % down, 5% rate and 25 year amortisation. 3300$ mortgage, some 300$ utilities plus property tax.

An average paycheck here may be in the 2000$ range twice a month.

That would be tight for a couple with two average incomes.

I remember in 2015 I thought the stock market was fully valued and I was thankful to have made money since GFC so I sold out. To me the real bubble in assets began around then.

During the pandemic things dropped and I bought some stocks but sold in about a year as bubble really took off.

Bottom line is there is a lot of money made as the bubble price turns exponential, but these gains are temporary unless you can find a bagholder at the right time and I am too risky averse to play that game.

If central banks stick to the 2% target, we could wipe out asset prices back to 2015 or 2016 pricing in my opinion.

I keep hearing about $80 Trillion in “off balance sheet” debt that is now “current”, meaning due within a 12 month period. With rates higher, is there a risk of significant defaults here?

Seems almost like VRM debt, or do the repayment agreements specify the rates to be paid. Seems like a shadowy thing to me.

I heard nonbank sector has more loans out than highly regulated banking sector. That is where the rotting fish are in my opinion.

$80T in commercial debt agreements (might not be correct name) coming due in the face of recession? Holy bankruptcy Batman!

I haven’t had a mortgage in a while but hear that variable rate mortgages, VRM, became very popular in Canada in recent years.

I guess the difference from ARM is that the payment remains the same but the interest to principle ratio is changed to reflect higher interest rates. Thus, if the payment is insufficient to pay all the higher interest, that deficit is added to the principle. Eventually putting the anesthetized mortgagee into a coma only to awaken to some default covenant that sells the home out from under him. Like being poisoned by slow acting poison isn’t it?

I envision that Dracula is at the other end of this blood transfusion hose with control of the flow valve, and keeps opening it up more and more with a huge smile on his face.

Wolf, the last housing bust in Canada was ’90-’92, not the ’80s.

Several of my high school friend’s parents lost their homes. Hard to forget.

That bust was somewhere in the region of 50% – 60% where I live. Took nearly 20 years to get back to the same prices.

I suspect we may be in for a repeat here.

Prices in Toronto reached meteoric highs in February and are simply coming back to earth. They’re down 20% since the highs. They may have a little further to fall but once they stabilize Toronto remains one of the top destinations worldwide for real estate investment in spite of the absolutely despicable Trudeau government. Locally the market has basically frozen. Canada plans to continue to attract 1/2 million immigrants a year and most settle around the GTA (Greater Toronto Area). Toronto is the financial capital of the country and the only city that really draws attention from investors to relocate. It also has the biggest tech presence, media, arts, universities, medical etc and a very diverse population. It’s the 4th largest city in North America behind only NYC, LA and Mexico City. Vancouver has really hallowed out though it remains a top money laundering destination from what I’ve heard.

And despite Trudeau’s dictatorial moves during the Trucker Convoy Canada still has rule of law, universal (but failing) healthcare, low tuition, low crime and relative stability.

I’m extremely critical of the country, Covid mandates were immoral, but also extremely bullish on it long term, particularly in light of expected rise of global temperatures.

My prediction is the worst is over for Toronto but we’ll see what 2023 brings.

Wolf – on Toronto you say priced dropped to $1.284 million but chart shows a different level, maybe you meant $1.084 million.

Thanks. Yes got into the wrong column. That was the price of the single-family benchmark home, not the composite benchmark. The composite (which the chart shows) dropped to C$1.09 million. The percentage changes and the C$ changes are from the correct column though, and are correct.