Down faster during the bust than up during the bubble: special feature in some cities. Vague humor wafts around the charts.

By Wolf Richter for WOLF STREET.

The overall 11-City Teranet-National Bank House Price Index dropped 0.8% in October from September, and is down 7.7% from the peak in May, the largest five-month drop in the history of the data going back to 1997. It slashed the year-over-year gain to 4.9%, from the 19% range in March and April.

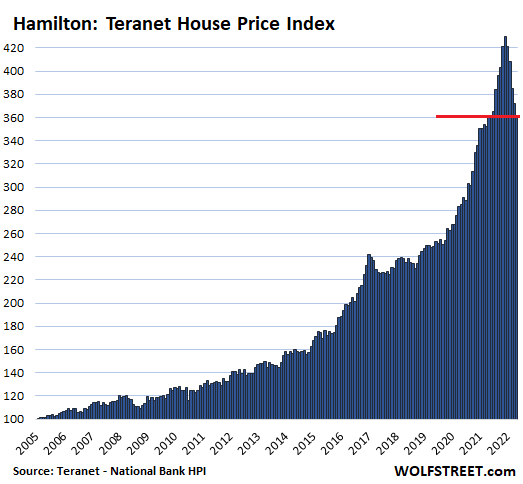

Nine of the 11 cities in the index had month-to-month drops in October, topped by a 5.7% plunge in Halifax. In Hamilton, prices have plunged by 15.9% from the peak in May after a ridiculous spike, and are now about flat year-over-year. Only two cities in the index had month-to-month gains: the oil towns of Calgary and Edmonton, whose housing markets had been asleep for 15 years.

Hamilton, where prices tend to move in parallel with Toronto, had become the #1 All Time Ever Most Splendid Housing Bubble in Canada after surpassing Toronto and Vancouver in 2021, as measured by the Teranet-National Bank House Price Index.

And it’s now #1 in terms of the percentage drop from peak. In October: -2.9% for the month, -15.9% from peak in May; about flat year-over-year.

Going down faster than up: The index plunged faster over the first five months of the bust (-69 points) than it had spiked over the last five months of the bubble (+65 points).

Vague humor wafts around these kinds of ridiculous price spikes that then unwind. This stuff make you wonder about the functioning of the human brain:

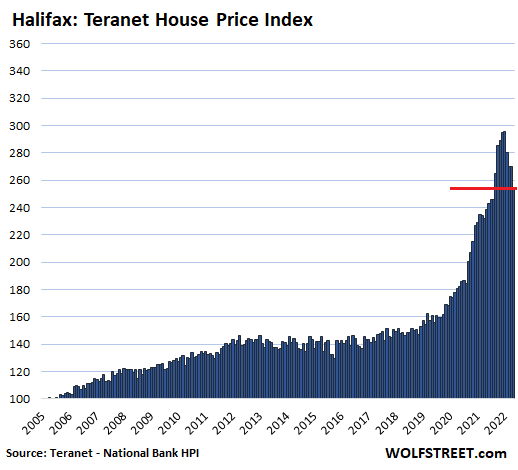

Halifax is #2 in terms of the drop from peak. In October: -5.7% for the month; -14.0% from the peak in June, which slashed the year-over-year gain to +6.7%, down from over 35% in early 2022.

Here too, the index plunged faster in the first four months of the bust (-41 points) than it had spiked during the last four months of the bubble (+31 points).

This chart proves once and for all that central-bank interest rate repression and QE – the entire free-money era – spawned a virus that turned the human brain to mush, a phenomenon that I previously observed with my Imploded Stocks. And then, when central banks end the free-money era, the brain begins to heal, and look what happens.

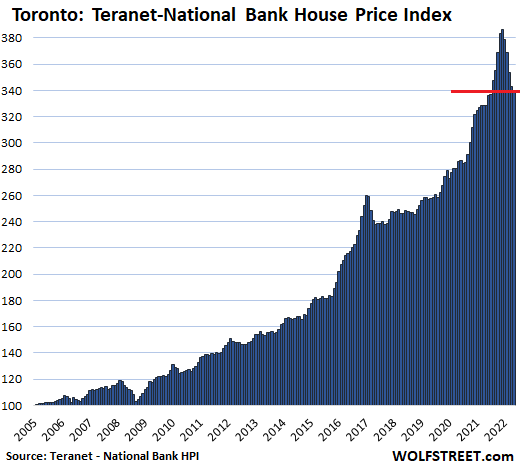

The Greater Toronto Area is #3 in terms of the drop from peak. In October: -0.9% for the month, -11.9% from the peak in May, slashing the year-over-year gain to 3.6%.

The index fell at nearly the same pace over the first five months of the bust than it jumped over the last five months of the bubble:

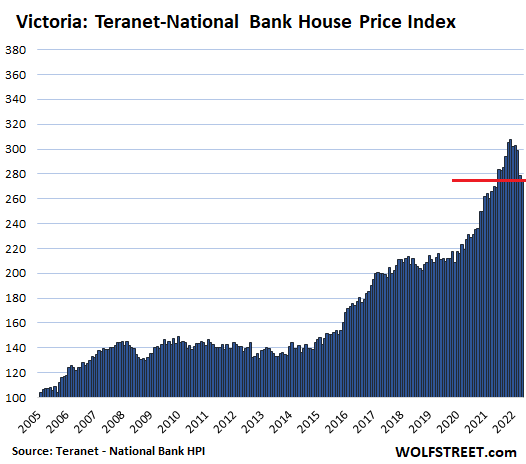

Victoria is #4 in terms of the drop from peak. In October: -1.2% for the month; -10.4% from the peak in May, which slashed the year-over-year gain to 2.1%.

The index plunged faster over the first five months of the bust (-32 points) than it had spiked over the last five months of the bubble (+24%):

Canada’s house prices reacted faster to rising interest rates than US house prices – though they’re now reacting too – largely because in Canada, most mortgages are either variable-rate with all kinds of guardrails or fixed-rate for terms such as two years or five years. So when interest rates began to surge, existing homeowners started to face the prospect of higher mortgage payments in the future. This is in addition to potential home buyers looking at mortgage payments at these rates and prices that they cannot afford.

The methodology of the Teranet-National Bank House Price Index is based on “repeat sales” that tracks the price of the same home each time it is sold over time. Unlike median prices, the “repeat sales” method is not impacted by a shift in mix of the homes that sold. The index was set at 100 in June 2005 for all cities. My charts here are all on the same scale.

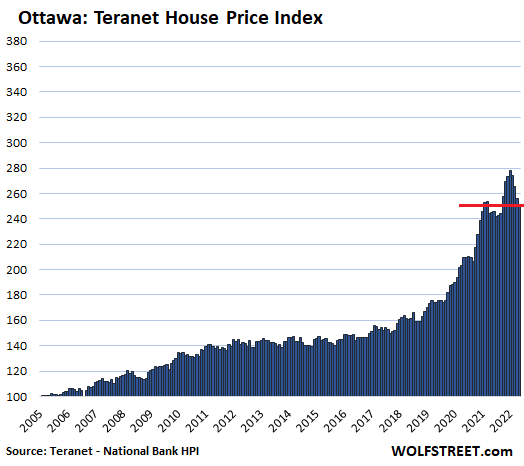

Ottawa is #5 in terms of the drop from peak. In October: -1.8% for the month; -9.6% from the peak in June, which slashed the year-over-year gain to 2.8%. The index is now below where it had first been in July 2021.

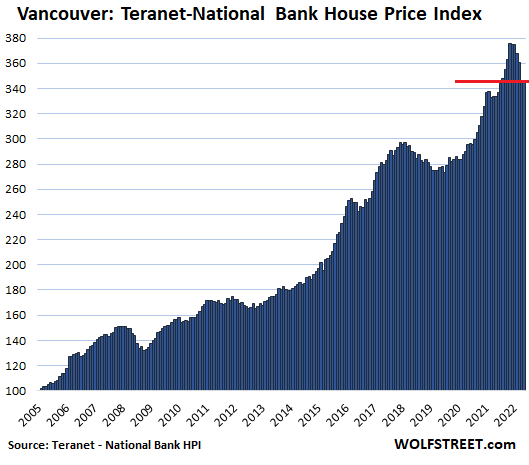

Greater Vancouver is #6 in terms of the drop from peak. In October: -0.1% for the month; -7.9% from the peak in April, which cut the year-over-year gain to 3.7%.

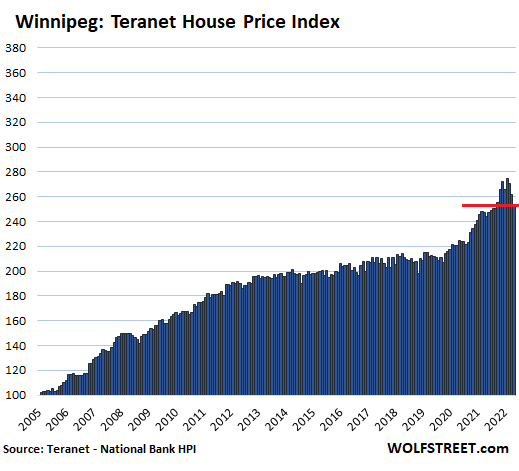

Winnipeg is #7 in terms of the drop from peak. In October: -3.1% for the month; -7.5% from the peak in June, which cut the year-over-year gain to 3.9%.

Down faster than up: The index dropped faster during the first four months of the bust (-21 points) than it had spiked during the last four months of the bubble (+19 points).

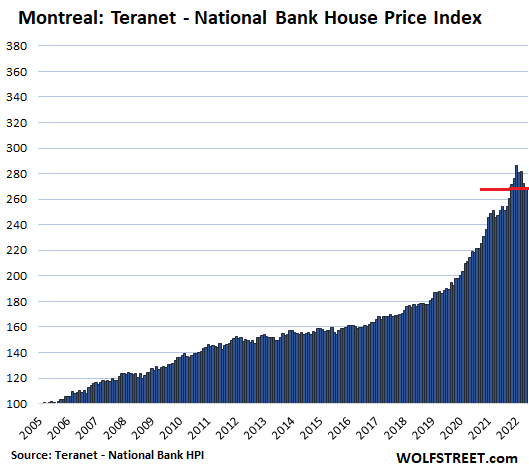

Montreal, in October: -1.5% for the month; -6.4% from the peak in June, which cut the year-over-year gain to 8.4%:

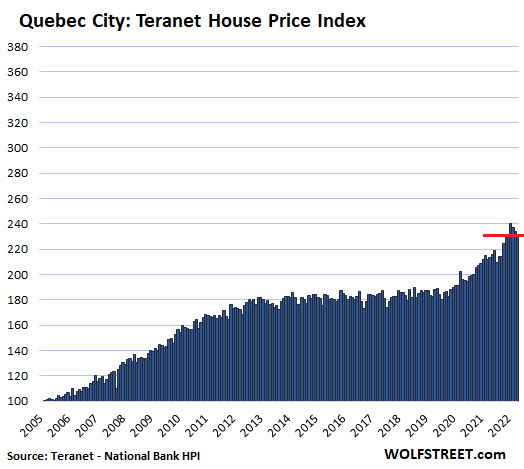

Quebec City, in October: -1.2% for the month; -3.6% from the peak in July, which cut the year-over-year gain to 8.6%:

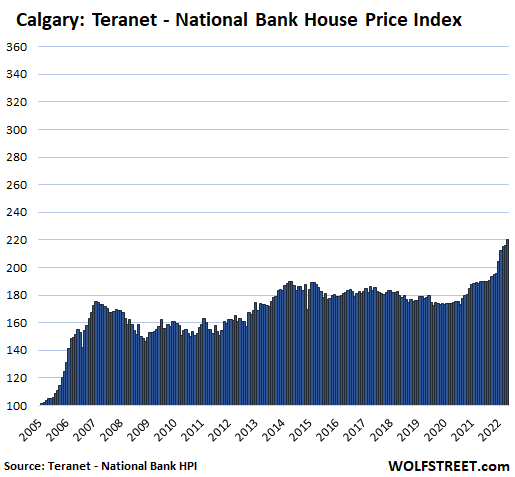

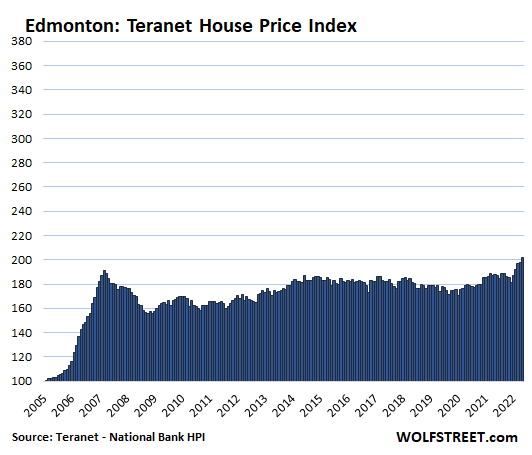

The Oil Towns are still the exception.

In Calgary, oil capital of Canada, in October: +2.0% for the month to a new record; +16.2% year-over-year. Prices had been roughly flat from mid-2007 until mid-2020:

In Edmonton, also in Canada’s oil patch, in October: +2.1% for the month to a new record; +7.5% year-over-year. The index is now just a hair above where it had been in mid-2007:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

While the good news is that housing prices are going down the bad news is that they are still very high. Unfortunately people who bought at the peak will be hurting when prices become affordable again. No it is not different this time. Paying at the peak of a bubble is always painful.

In US, the housing market is freezing as most sellers are still waiting on a Fed Pivot.

Every week the mainstream media spins a new Pivot story (latest one is that inflation has been defeated) that causes bond yields to drop despite raging inflation.

The scumbag is still busy selling his soft landing story.

Uh have you been reading the same headlines as me? Different newsfeed maybe? I am seeing a surge of lots of ‘pivot is dead’ type headlines. The paradigm is shifting.

By Scumbag, I mean J Pow.

The 30 year mortgage slipped by 47 basis points last week. Only Pivot stories cause such moves.

JPow is 1) not selling that anymore, as far as I’ve heard and 2) is not a scumbag and 3) is at least tied with Yellen for best post-Volker FRB head we’ve had. We could do so, so much worse than a guy who made mistakes and wants to fix them. We HAVE done so much worse for the past 3 decades+!

In my hood san diego I am seeing home prices down from peak and price reductions galore.

Prices won’t be defined by the folks waiting for the pivot but by the marginal sellers who are forced to sell for multitude of reasons.

Last week 4 sigma upwards on the `Fed pivot` topic from investors’ sentiment data, followed over the weekend with a 3 sigma mean reversal.

Next week markets will be under major stress.

I agree RE prices will come down substantially. I was surprised central banks could raise mortgage rates to 6-7% and not kill the housing market. That tells me mortgage rates were WAY too low for many years, and those days are never coming back. The fact that no economic disasters are happening, despite the higher rates, gives central banks power to keep rates high for decades. Each month, home prices will fall as rates remain high, and there will likely be no pivot. I predict we’ll see a 3-5 year steady, relentless price drop from these nosebleed levels.

Additional inventory from layoffs and retiree downsizing will be hitting the market soon, at the same time investors leave the market.

Not sure where you’re living but there is definitely some economic disaster happening and even more to come. Canada’s only growth is from RE, which is driven by immigration, we removed ourselves from manufacturing, which we are now feeling the pain of, and became a country of customer service providers (lazy asses). Rate increases will more than likely ease or end by end of first quarter 2023, at that point the market can start to absorb these rates and move on. Our problem has been no time to absorb when rates are increased at every rate announcement, @ every 58 days, for the last 8 months. To put in basic terms, a boxer who gets knocked down usually gets a 10 count to stabilize themselves, the RE market been getting a 5 or less count to do so.

It’s interesting to look at the Cisco stock runup and subsequent crash in the tech bubble to see how crazy things can get when speculation runs with cheap money.

What’s the value of real estate if financing costs stay high for five years? You can’t go from free money to very tight money without cratering an asset that depends on financing.

Houses in Ontario, three or five hours from Toronto are priced at 1M+. All of them, wilderness or not. This needs to drop by 80% more to give any realistic opportunity to Canadians to own a house and live a normal life. Barely anything sells, all the owners are dropping ask price by 20-30%. Go see it on housesigma.com. It’s crashing.

Who are the owners/sellers? Long-timers or recent speculators/second homes?

Based on my research it’s both, with notion that a long-term owners are setting the prices, i.e., actually selling for a profit, while those who bought in 2016 and after are now trying to break even, even ready to sell at a loss. Also, keep in mind that a lot of houses were bought in the last five-seven years, razed, and re-built much bigger and lusher; they are not moving at all. This complicates the things, as many of these buyers were foreign owners, “raped” by the local builders, so even in the “value add department” they have a minimal room for price negotiation.

“This stuff make you wonder about the functioning of the human brain:”

If only you had the displeasure of experiencing Hamilton in person Wolf, you have no idea how on point this statement is.

We are missing problem solvers that don’t keep kicking the pan down the road.

Today, we have the types of J Pow that quote Volker, but keep -ve real rates (Fed rates – inflation).

Wait till Horvath takes over Hamilton, it’s about to become even worse.

If she comes in and builds a boatload of government housing people will love her though. Looks like early 90s ghetto housing boom is coming back, lots of immigrants, high skilled locked out of high paying jobs because we won’t recognize their training need a place to stay while they get Canadian training. At least the city housing will have some educated parents there to be a good influence on the community, even if it’s not fair to all those foriegn drs and engineers.

Lol

It’s a nightmare of a drive to Toronto for the people who live in Hamilton and work in Toronto. Oshawa is almost as bad and Barrie is the worst for people working in Toronto. The only good thing about Hamilton is the bars there.

STOP LIVING IN ONTARIO MOVE TO ALBERTA

The good news is that the buyers purchased these homes with ‘loonies’, which, to me, sounds like cartoon money. Unfortunately, for those that purchased with real fiat currency, top-ticking this bubble-like RE market is going to be painful…

My goodness: are you silly enough to think it’s called loony because it’s, like, a cool name? Google the Canadian 1 dollar coin and look at the picture. It’s got a loon on it. Go figure.

Just going to say… the common loon is my favorite bird. We only rarely see them in NC in the winter. I believe they come south with the Canadians for the nicer weather :)

Since 1961, the Gavia immer has been Minnesota’s state bird. They have incredible swimming and diving abilities, and can go over 25 meters deep under water when fishing. Wing span is a meter and a half. Our pro soccer team, the Minnesota United FC, is called The Loons.

But as much as I like them, both to watch and to listen to, my favorite is the Geococcyx californianis. Yes, they do belong to the cuckoo family.

“real fiat currency”

Now THAT is funny!

“Real fiat currency” hah that’s a good one. No such thing. Cleanest shirt in the dirty hamper etc.. the outrage coming when printing returns to save the treasury market from China/Japan dumping will be epic. And that’s nothing to say of the US debt rolling over in 2 years at these rates causing the debt interest payments to be larger than the already bloated military budget. USA looking like FTX but with a military (one that couldn’t beat Afghanistan no less).

Wow, nice example of U.S.-centric thinking. I love the loonie and better yet, the toonie. At least Canuck money has color and style (and birds!).

“real fiat currency” – thanks for my laugh of the day. All fiat is toilet paper, or soon will be. U.S. dollar is just temporarily the cleanest dirty shirt in the laundry.

It gets ugly when reality and perception diverge, especially when that perception is purchased with hundreds of thousands of dollars of borrowed money…..

I like this, in a twisted way you can see this as bringing some level of fairness to future prospective buyers and force some level of turn in the market. Definitely way fairer than California with prop 13 and people that locked in ultra low rates last 2 years. Good for you if you got in at the right time and can squat on either low tax or low interest rate mortgage provided you still have a job to pay for it.

“Canada’s house prices reacted faster to rising interest rates than US house prices – though they’re now reacting too – largely because in Canada, most mortgages are either variable-rate with all kinds of guardrails or fixed-rate for terms such as two years or five years.”

What it tells me there are a few cities that are not in as much trouble as others. The others, followed the greater fool theory and are out of luck..

What it suggests to me is that the pandemic drove regional population shifts and some markets were hotter than others. I don’t believe that people are regionally irrational. Rather I think some areas saw a sudden arrival of buyers that they weren’t prepared for. Many US markets saw the same.

A lot of people completely shut out of the housing market in Ontario moved to Halifax and Moncton. A lot of retirees from Ontario also moved there.

The temperature in Chicago is the same as it is in Moosejaw Saskatchewan at the moment.

Listened to a real estate show from Raleigh, NC yesterday. Inventory on the market has went from about 2 weeks to 7 weeks. I am still seeing a lot of infrastructure being put in for housing developments within one hour drive time. of city.

My brother lives near Halifax. It’s one of the nicest areas I have ever visited. Another 40% or so and I would consider using it as my home base in retirement.

Beautiful summers, Brutal winters, great people but in the middle of nowhere if you want to get “somewhere.”

I could never even think of living there. Why anyone moved to Halifax I’ll never know? Sometimes you can never figure out what the people from Ontario will do. I thought all of them would move to Alberta due to the much lower income taxes for upper middle class people and no provincial tax.

A bunch of them are.

My brother lives in Wolfville where there is even less to do.

One primary motive?

To escape the expanding barbarism infecting most (if not every) US metro area.

I’d have to find somewhere else to be in the winter. Never been there then but agree it’s not pleasant.

“To escape the expanding barbarism infecting most (if not every) US metro area.”

Stop reading the NY Post or watching cable news.

The same story is in every news outlet these days Cy; doesn’t really matter where ya get your current news IOW.

Too many guns and too many drugs in every major municipality as well as the meth epidemic continuing in the rural areas.

While the cities grab the headlines far shore,,, many rural areas now have higher crime PER CAPITA, also mostly similarly due to druggies fighting it out for territory when they are stoned, etc…

I don’t care what dumb news network you’re watching. The data is clear that while crime is elevated it’s not that bad. And it’s not everywhere, Boston is fine. And it has nothing to do with ‘too much drugs n’ guns’.

Oil towns know real booms and busts, so they aren’t impressed by a mere money-driven boom.

Alberta real estate always moves up and down with the price of oil. The price of oil is the only thing that matters especially in Fort McMurray.

You can add fires to the things that matter in Fort McMurray.

Bahahahahahaha.. I spit out my coffee 😂

In 2016 my wife and I bought our first house in Kitchener (a city about 2 hours from Toronto) for $365k with 20% down and a 35 year mortgage (a feature available at the time). I expected to be paying it off until my sixties.

Then early this year I saw the writing on the wall. We sold our house just after peak insanity – signed agreement in April, closed in June. We sold for $925k.

Since then we’ve been renting a small apartment and waiting for my immigration papers to clear so we can move to the US (my wife is American, so it’s not too difficult). In the meantime I’ve converted the proceeds from our house to USD.

After our mortgage and realtor were paid and the funds were converted we ended up with a hair under $500k USD, enough to buy a house just north of Dallas, bigger than we had, with no mortgage at all. At least that’s the plan.

I realize this could come off as bragging, but I don’t mean it that way. I just mean to say that Canada’s market went utterly mad during the pandemic, and I’m grateful to have gone from a 35 year mortgage in what was already an overinflated market to being mortgage free and not fearing the loss of my house anymore.

I’m practically economically illiterate, and it’s sites like this that helped me make good decisions. So thank you very much Wolf, and sorry for the novel.

Also, once I land in Dallas next year, I plan to buy two mugs. One for me and one for the wife.

250% appreciation in 6 years?! Mazel tov! For your buyer, not so much…

Resale detached homes spiked about 500 percent the last 6 years in Hamilton. The ones selling for $200,000 in 2016 spiked to more than a million in 2022. 2015 and 2016 were the years the rich Chinese came to Canada. The collateral damage has now spread to the entire country with the exception of Alberta.

You should be able to afford AC there…you’ll need lots of it. I’m sure you know about the summer there. This year worse than usual.

Per the Accu Weather website I believe it was Dallas (may have been Austin) that I counted 121 or so days with highs over 90. Fifty of these days were over 100.

Its a challenge. I lived near Dallas for 11 years.

Unlike you I lost $$ buying real estate there.

He might yet lose $$$ there!

Yes, Dallas is also in a bubble, just a smaller one.

DALLAS is a bigger housing bubble hyped up big time.

I live in Palm Springs, California, and keep the heat on in the winter on days when it’s down to 90 degrees. 110 is perfect.

I sure hope you are not a landlord!

Big difference between Dallas and Palm Springs. It’s called humidity.

Great story! It will be a good Thanksgiving.

People that come to this site are made more aware of likely probabilities regarding prominent historical trends as they relate to economic realities.

The variable rate Canadian mortgages accelerated the selling process creating more urgency comparted to most U.S sellers, they were willing to drop their prices.

Even now in Canada and the US many people that want to sell should lower their prices more that their neighbors, and they still would make a nice profit compared to what it will be like in a 6 mos., a year, 2years etc… They would be considered lucky and smart in 5 years.

Odd Captive

You ate not bragging, just sharing the truth. It may help others and that’s what the Wolf Pack does. Congrats on your windfall !

1) The housing market is breaking down, but TNX made a new all

time high last month.

2) The weekly Dow is 8% below the top. In the last 7 weeks it had only

one tiny red week. The Dow for fun and entertainment. Options.

3) Option #1 : the Dow stalled. It might turn lower to a higher low, before

making a new all time high. This nightmare is almost over.

4) Option #2 : The Dow weekly close is slight below Aug 8 close. The Dow,

in a sling shot, will lurch lower to close Nov 2/9 2020 open gap. With such down thrust the Dow momentum will take UNH and Goldman with it.

Are you some kind of AI-generated comment bot?

If so you fail the Turing Test. Please try again.

What? You don’t get the Engelese Newsletter?/s

If you have to ask, I think he did pass the Turing test.

I’ll take Option #3. Do nothing and be happy.

I am in the market up here in Ontario and so watching housing closely. The housing cult has not capitulated yet, only some of the desperate members. Sellers banking on a pivot soon, and a rapid bounce back still.

You see the same house listed and relisted at a lower price and then put up for rent … over and over again as inventories keep climbing. The few that actually sell are usually the very “clean” in ideal locations or the serious sellers willing to negotiate (seen houses sell for over 15% below asking). If you look at median house prices its falling much faster than HPI – it seems cheaper is still selling while pricier not as much. Vacant land just sits and has not adjusted much with investors out of the market.

Rental inventories and prices are now dropping and with the “standard” 25% down rentals are not covering the 75% mortgage anymore at current rates, so landlords are making a loss in hope of a price bounce and caught not being able to sell for the price they want or increase rent further. Blackstone is selling all the homes they bought in the area now and I see empty newly built houses for sale frequently – even homes partially built.

I think you are commenting in not only the wrong thread, but probably the wrong website, and very possibly the wrong universe.

Beam me up scotty!

– your loyal Nigerian Prince

In related news…

Blonde: Does anyone know what IDK means?

Brunette: I don’t know.

Blonde: OMG! No one does!

(in before the comment deletion :) )

Always a blonde woman ?….so passé. How about a 50 yr old white doode

He know what exactly he is doing. Stake out on economics blogs and report on popular opinions. He has assistance from local post office and Pythonscript. I have nothing against him as a person. His comments on the other hand…

Maybe I’m in the minority, but I find Michael Engel’s post’s interesting, perhaps more so than the constant whining of some of the other posters. Although many require codes to decipher the encrypted messages.

The teranet index is backwards looking in time. At the moment Edmonton condo prices are being crushed well below the 2007 peak down about 18 percent from the 2022 peak. Resale condos are still down fifty percent from the 2007 peak in Edmonton. The exact same ones that sold in 2007. Home prices are down about 11 percent from the 2022 peak in Edmonton.

Is that Dogecoin? Oh no wait…it’s the housing market.

Central bankers deserve a Nobel Prize for this.

I heard BernaQE is accepting one on their behalf.

Only catch, there is no Nobel Prize in economics. The Swedish Central banks prize in memmory of Alfred Nobel is the closest they come.

Home prices in the greater Toronto area peaked in mid February this year not using the teranet index. The greater Vancouver area peaked slightly later. The teranet index is backwards looking in time.

The Canadian press and the real estate community continue to position current house prices as greatly reduced. In fact, house prices in Ontario are barely changed from one year ago. At that time, one year ago, homes were already unaffordable for many, and that was at a time when variable rate mortgages could be found at well under 2 percent. With current interest rates, it’s hard to overstate how serious the affordability problem has become.

So headlines pointing out how much housing prices have fallen is not helping.

Im in the GTA, since 2H 2020. Before that Vancouver Island.

A month before the peak (April 2022) i was still treating my van as home. But because of Operation By-Law, was forced to wrecker. Its truly a shame if thats what happened to it, a finer art studio one couldnt hope.

“Calgary and Edmonton, whose housing markets had been asleep for 15 years.”

No, those markets are not ‘asleep’-there is lots of buying and selling going on. The difference is we have BUILDING so that we have supply, that all important aspect that is missing from so many housing markets, as I’ve repeatedly told you. Hopefully this is coming to Ontario soon thanks to Premier Ford’s reforms. He is starting to become awesome.

Alberta isn’t the only oilpatch place in Canada, Saskatchewan has lots of that going on. Pity that Saskatoon and Regina aren’t included in the list so we could compare oil-ish towns but I understand given how shockingly few people they have.

In an upwards housing market any supply that comes onstream is snatched up the Chinese in mere minutes when the sales offices open driving new home prices to the moon and skewing overall home prices a lot higher. Prices are irrelevant to the Chinese as long as the market is going higher not lower. So more supply in the greater Toronto area and the greater Vancouver area results in much higher prices. The opposite is true in America more supply means lower prices. It’s hard for an American to fathom but that’s the sad reality in two thirds of Canada. Basically what happens is all the Chinese buy at the exact same time and home prices go towards 86 times income like in China.

I don’t agree with this thesis but only time would tell.

Prices are absolutely not irrelevant to buyers be it Chinese or non Chinese.

Going by your logic, we should not see drop in places where Chinese buyers are present but the numbers tell us different stories.

Are you a land lord or realtor by any chance ?

Great Article / Post > more of the Developed results of the Governments actions leading directly into recession ‘ lower home values ‘ foreclosure ‘ foreclosure ‘ foreclosure ‘ foreclosure ‘

Etc.

Is this the modern 2022 2023 2024 2025 economy platform for the foreseeable future then ?

One can’t just pull out the rug and undo whats already been done or turn a blind eye and its gone.

Various Politicians stepping down Retiring with varying amounts of gathered ” booty ” seeking becoming quietly anonymous .

No wonder so many people don’t Evan Vote

As example :

2020 had a record Voter turnout but 80 Million Americans Didn’t Vote

its simply to see Why

Thinking back, do I recall that when the bottom fell out of the US mortgage mess of 2005 to around 2008, that the values in Canadian housing did not tank much if at all in that “great readjustment”? Perhaps there is a “great readjustment” coming then this time.

Maybe I’m confusing the mortgage mess with housing values but it seemed all related. One thing stuck me though, was how did Canada not have the same steep declines as the US at the time.

Help me out if I’m wrong.

the Canadian dollar was up and those snowbirds were buying 2-15 homes at a time in Arizona during that time

Who really knows where we will end up? There is a cycle. You have to measure from peak to peak and bottom to bottom. In US we peaked just before GFC and bottomed in GFC.

This time we peaked around end of 2021. It’s all going to be different until we bottom. If you are a buy and hold you just have to not panic at the bottom or be in such a precarious position to be a forced seller.

If you are on this site, you probably try to read the tea leaves and buy close to the bottom and sell before it implodes. Not an easy thing to do.

‘Vague humor wafts around these kinds of ridiculous price spikes that then unwind. This stuff make you wonder about the functioning of the human brain:’

It’s quite simple, really. Testosterone.

The output of a man’s dangleberries is far greater in effect than of logic.

As greed turns to fear, so too do dangleberries to dingleberries

I was at an open house yesterday on Eastern Long Island, in NY. The prices are only down now about 5% here. The sign up list showed 3 others showed up before me. It was a big home. The place empty, no furniture and had no heat on. While the realtor stood in the kitchen rubbing their hands to keep warm. I asked “are they negotiable’? Answer, “This is not selling below the asking price”

Whether this is a good or bad deal depends on how low the asking price is.

Asking price is meaningless. It’s a strategic fabrication by the seller. The asking price might be 30% below the market price in order to start a bidding war. It might be ridiculously high to test the market.

Wolf, thank you for the reply.

I thought the price was about 5% off of the recent summer high. I just asked to see what the reaction would be from the agent. In the agent’s mind, they probably felt, it was under priced, a.k.a. “priced to sell,” that’s why the response was immediate.

I am going to open houses to see places, thinking when they lower prices more I will be ready. Maybe I will be wrong. The NY area has so far been resilient, as far as where I have been looking.

I will post here again when the home sells as a point of interest.

Thank You for all the great content. I always enjoy your video presentations and interviews.

Are they on oil heat out there?

Eastern LI sellers in the off season sell only if they get their asking. Otherwise they will just vacation there next year. Owners fish for offers all the time.

There was an excellent article put out by the Bank of Canada a few years back called:

“The Rise of mortgage Finance

Companies in Canada:

Benefits and Vulnerabilities”

It’ll be interesting to see how these mortgage finance companies weather the slowdown in sales – the TLDR on how they operate is that they borrow money from the big 6 banks and use it to fund mortgages (generally) for people who were previously denied a mortgage by these same banks. They rely on a steady flow of mortgage originations to stay afloat and have very little cash reserves. They also make up a fairly significant portion of new mortgages (and they’ve been growing pretty steadily as the article name implies). Interesting times ahead!

Kind of getting the feeling that we might be in for the great washout like the tech bubble and GFC.

The most speculative asset crypto is in the middle of a crash with the dead bodies floating to the surface.

Pull up a Tesla long term chart. Very symmetrical blowoff top and downside. Looks like it could go all the way back to $20 – $40 to wash everyone out. The company was built on constantly expanding capital raises in stock market. Tesla and hundreds of other companies will not survive a tight money recession.

GM and Ford are going to be in a tough spot as well if we have a tight money recession during EV transition as you have got to have people buying autos to support the capital spend.

But housing industry is going to feel it the most. It’s just hard for me to believe Powell is really going to crush everything when the pain really gets here. It does seem to be a coordinated central bank effort to convince investors there is no Fed put til inflation is dead and buried.

So… when does it drop to the point that a significant number of mortgages are “under water” and people start simply walking away from homes for which they over-paid?

It’s happened before; people seem willing to live with it on the credit rating.

In Canada it’s not so easy, if you’re underwater on your mortgage and need to “walk away” from your house you have to declare personal bankruptcy. The other option is to negotiate with the bank for what they call a “proposal” where they effectively give you a loan for the difference in what you owe minus what the house sells for, so you walk away with no down payment, no house, and a bunch of debt (debt they can collect on through wage garnishment if necessary).

What would be the advantage to a borrower to do a proposal, versus just walking away and making the bank sue you for the deficiency? The latter would be a lot more work and I’d think that many lenders wouldn’t bother.

For any significant amount of money (in the 100s of thousands range) I think the lenders would definitely bother since it’s a slam dunk for them, and as a borrower you’ll also end up on the hook for your legal fees.

Thank you for this analysis.

Home price’s are still up +200% from “the financial crisis” of 2008, considering that the housing market was the catalyst.

For the last 12 years, real estate values went through the roof, whilst mortgage rates was close to zero.

My question, is the values still highly over inflated?

How does first time home owners even start thinking of affordable homes?

That is why there is a plan to maintain this bubble.

The government is planning to bring in 500,000 new rent and wage serfs a year, estimated to increasing to 750,000 in 2030 and eventually a million a year by 2035.