What the Fed did in details and charts.

By Wolf Richter for WOLF STREET.

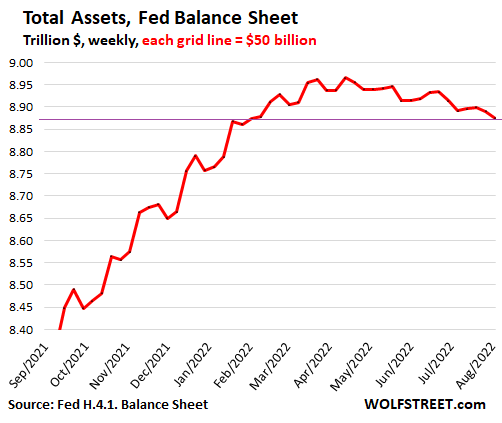

The Federal Reserve’s quantitative tightening (QT) finished its second month of the three-month phase-in period. Total assets on the Fed’s weekly balance sheet as of August 3, released this afternoon, fell by $17 billion from the prior week, and by $91 billion from the peak in April, to $8.87 trillion, the lowest since February 2.

QE created money that the Fed pumped into the financial markets via its primary dealers, from where it began circulating and chasing assets, including in non-financial markets such as housing and commercial real estate. The purpose and effect were to repress yields and create asset price inflation. And it finally also helped create raging consumer price inflation.

QT does the opposite: It destroys money and has all the opposite effects – not for day-traders but over the longer term. QT is one of the tools the Fed is using to crack down on this now raging consumer price inflation.

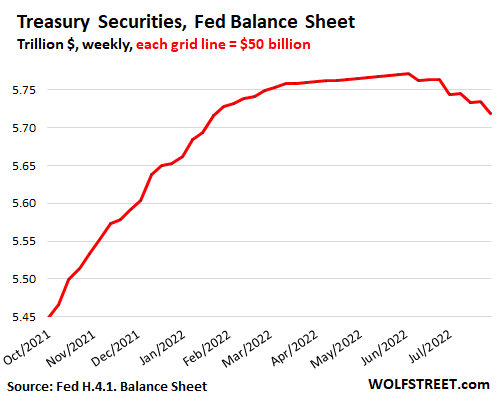

Treasury securities: -$52 billion from peak.

July: -$30 billion roll-off +$4.6 billion in TIPS Inflation Compensation.

Treasury notes and bonds roll off mid-month and at the end of the month, when they mature. Today’s balance sheet includes the roll-off at the end of July.

Treasury Inflation-Protected Securities (TIPS) pay inflation compensation that is added to the principal value of the TIPS. When TIPS mature, holders receive the amount of original face value plus the accumulated inflation compensation that was added to the principal.

The Fed currently hold $374 billion in TIPS. The amount of inflation compensation amounts to about $1 billion to $1.5 billion per balance-sheet week, or about $4 billion to $5 billion per calendar month, which adds to the balance of Treasury securities.

The QT phase-in plan (from June through August) calls for the Fed to let $30 billion in Treasury securities roll off per calendar month, as they mature. And the Fed did exactly that in July.

So why did Treasury securities decline by only $25.2 billion, and not $30 billion that rolled off? TIPS inflation compensation!

- The Fed let $30 billion in Treasuries roll off without replacement, which reduced the balance by $30 billion.

- The Fed received from the government $4.6 billion in inflation compensation, which increased the balance by $4.6 billion

- Net effect: the total balance fell by $25.2 billion.

Inflation compensation being added to the balance of Treasury securities every week is why the reduction in the balance will be less every month than the actual roll-off.

In the chart below, note the steady increase of around $1-1.5 billion a week after QE had ended from mid-March through June 6, which is the inflation compensation from TIPS.

The amount of Treasury securities has now fallen by $52 billion from the peak on June 6, to $5.72 trillion, the lowest since January 26:

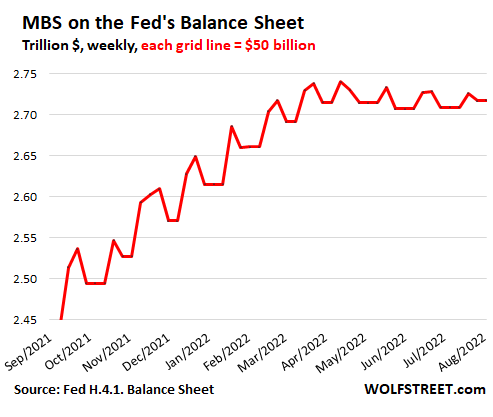

MBS, the peculiar creatures with the big delay.

How MBS can come off the balance sheet:

- Pass-through principal payments – the primary way

- When issuers “call” MBS

- When MBS mature, but they’re usually “called” before they mature

- When the Fed sells them, which it has said it might do some day in the future.

Pass-through principal payments: When the underlying mortgages get paid off (due to a sale or refi of the property) or when regular mortgage payments are made, the mortgage servicer (the company you send the mortgage payments to) forwards the principal payments to the entity that securitized the mortgages into MBS (such as Fannie Mae), which then forwards those principal payments to the holders of the MBS (such as the Fed).

The book value of the MBS shrinks with each pass-through principal payment. This reduces the amount of MBS on the Fed’s balance sheet. These pass-through principal payments are uneven and unpredictable.

The issuer “calls” the MBS. After a good number of years of pass-through principal payments, the remaining book value of the MBS may have declined so much that its not worth servicing the MBS any longer, and the issuer, such as Fannie Mae, decides to “call” the MBS to repackage the remaining mortgage debt into new MBS together with other mortgages. When Fannie Mae “calls” the MBS, they come off the Fed’s balance sheet.

When MBS mature. MBS have 15-year or 30-year maturities. But this is largely irrelevant because the average lifespan of mortgages in the US is less than 10 years because they get paid off due to a sale or a refi. And when the remaining book value of the MBS falls below a certain level, the issuer calls them, and gets them off the books.

How MBS get on the balance sheet.

The Fed purchased MBS in the “To Be Announced” (TBA) market during QE, and to a lesser extent during the Taper, and to a minuscule extent in June and July. The June and July purchases are designed to replace pass-through principal payments of June and July that exceeded the monthly cap of $17.5 billion.

But purchases in the TBA market take one to three months to settle. The Fed books its trades after they settle.

So the influx of MBS onto the balance sheet over the past few weeks are from trades that were executed a few months ago, before QT. What we’re now seeing are the purchases made during the Taper.

These purchases are not aligned with the pass-through principal payments that the Fed receives. This misalignment, and the three-month lag, creates the ups and downs of the MBS balance, that is then also visible in the overall balance sheet.

MBS: -$23 billion from peak to $2.72 trillion:

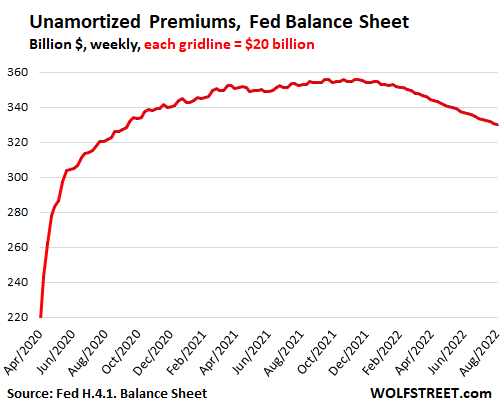

Unamortized Premiums: steady decline.

All buyers pay a “premium” to buy bonds if the coupon interest rate of that bond exceeds the market yield at the time of purchase.

The Fed books securities at face value in the regular accounts and it books the “premiums” in a special account, “unamortized premiums.” The Fed then amortizes the premium to zero over the remaining maturity of the bond, while it receives over the same time the higher coupon interest payments. By the time the bond matures, the premium has been fully amortized, and the Fed receives face value, and the bond comes off the balance sheet.

The “unamortized premiums” peaked with the beginning of the taper in November 2021 at $356 billion and have now declined in a steady process by $26 billion to $330 billion:

The other QE and bailout assets are largely gone.

- Special Purpose Vehicles (SPVs) through which the Fed bought bonds, loans, and ETFs: $38 billion

- Central bank liquidity swaps: $0.2 billion.

- Repos: $0

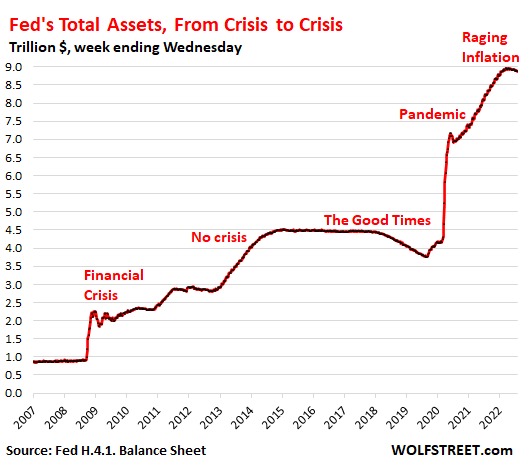

Money-printing comes home to roost:

In the 15 years of this chart, there are three crises: The Financial Crisis, the Pandemic, and now Raging Inflation. Today’s inflation crisis pulls into the opposite direction of the prior two crises, and dealing with it will require the application of the tools in the opposite direction:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Congress will have to inflate double time now. Good thing it’s added directly to GDP.

Look at the long term trend on the last chart! The tightening shows only through a lens. No wonder everyone is already betting that Fed will reverse soon.

No wonder, most people are working only half time in name of WFH causing huge Service inflation!

Economy becomes strong only through higher Production of goods and services.

Higher consumption through money printing only makes dollar based GDP look good as Economy keeps declining as Production reduces and inflation picks up.

A lip service of Fed tightening will not get us out of this loop. It will require steep correction in Asset prices that makes productive work feasible again!

SS,

That little bitty QT the Fed did in 2018, which was so slow in ramping up that you couldn’t really see it at all at first, took a couple of years to remove about $450 billion. But with just $200 billion removed by Sep 2018, it blew up the stock market, and housing started to get a hit, and the whole thing came apart.

A market that is totally addicted to QE cannot breathe under QT. Just give it a few months.

And in late 2018/early 2019, inflation was below the Fed’s target. Now inflation is multiples of the Fed’s target. This time, the Fed isn’t going to pivot because inflation is tearing up the economy.

“A market that is totally addicted to QE cannot breathe under QT. Just give it a few months.”

Looking at your chart, did anybody ever bother to ask anybody at the FED why they were just holding their balance sheet at more than $4 trillion for almost 5 years, and why 1 year of QE turned into 10 before they finally started tightening in 2018? We’ve been had.

@Depth Charge. Because there was no wage inflation until now. It’s a sad fact of how the Fed has always worked. Asset inflation, no problem. Wage inflation, form a Maginot line.

Hence, the Feds emergency “Standing Repo Facility”.

528K new jobs in July. Raging inflation. Measly 2.5% FFR. Stock market & services fighting the Fed. There’s zero reasons for the Fed to pivot. It’s hilarious that anyone with a reasonable understanding of economy to suggest we’re in a recession. To do so is just click bait.

Looks like the jobs report confirms Wolf’s thesis that the markets are fighting the Fed. I see interest rates going up because there is no other option. Just got back to work, after spending 2 months fixing my sewer lines to the street. Condos are still selling in the DC Swamp. They are still affordable and appreciating over last year even with the higher interest rates, People are moving back to the city because of the high gas prices. Properties in good locations are selling without any problem. Properties in bad locations and far out suburbs are not. The Fed is going to have to jack up interest rates a lot more than they have done so far to date if they want to cool demand.

So Wolf, are you saying the Fed will have to have a ‘Volcker Moment’? I mean, could we go into a pretty deep decline (recession?) due to QT and still have raging inflation?

I guess that is the Catch-22 (ca 1970) we might find ourselves in, but what would drive that? Oil doesn’t appear to be that driver.

Collapse of the dollar? Don’t see that on the horizon with interest rates headed up.

What’s your crystal ball say for 2-3 years out? Uncharted times?

My el-cheapo plastic crystal ball from Walmart doesn’t go that far.

“A market that is totally addicted to QE cannot breathe under QT. Just give it a few months.”

Pure wisdom dispensed daily. Concise and eloquent.

Wolf,

Have you done a blog on the 10 year yield and its effect on the markets? Also, what are your thoughts on the ECBs “unlimited bond buying”???

TIA

Michael

Michael,

What the ECB is doing is shedding bonds from Germany, the Netherlands, France, and some other countries, and it’s buying bonds from weaker countries, such as Italy, which allows them to do QT (reducing overall bonds) without blowing out Italian yields and causing another debt crisis. It’s working for now.

QE is OVER, even for the ECB. Get used to it.

“A market that is totally addicted to QE cannot breathe under QT. Just give it a few months. ”

This is the most prophetic quote I have heard this year.

Stand by for a rough year for stocks and assets.

The Fed is working on the supply side for all of the excess money sloshing around.

Wage increases provide more cash for the masses which stimulates spending and demand for stuff which drives up inflation.

The Fed doesn’t want this.

Ben W.

Let’s say what we have keeps going with real GDP and real wages shrinking for two years. If it’s not technically a recession it’s certainly isn’t desirable.

Nominal growth measured in dollars, but recession when measured adjusting for dollar debasement.

You can always run an economy hot with easy money, but history shows that permanent easy money always fails.

Wolf–your analysis and wisdom are probably the best out there on this entire range of topics. I am curious though–you point out how little QT it took in 2018, with half the Fed balance sheet of today, to cause everything to blow up. By mid-2019 the balance sheet was going up, and still in Sept 2019 we had the not so subtle flare up in the REPO market. The Fed was saved by the pandemic, got to go wild with QE, and then blatantly over-did QE, maybe in large part to avoid having near-term liquidity issues like 9/2019. So it isn’t that any of us are QT deniers, you factually chart that we’re in it, but the elephant in the room is how far will the Fed allow the financial system to collapse? The repo/reverse repo trends are showing that there’s plenty of liquidity out there for now, do you foresee that the Fed really will stick to its tightening path in the face of imminent fireworks?

Back then, inflation was below the Fed’s target. Now inflation is 9%. Huge difference. Back then, the Fed didn’t want to crack down on inflation, it just wanted to normalize monetary policy. Now it has to crack down on inflation.

Hello, Wolf,

The points you made here would make an interesting column of their own. From what I have read in your columns, you’re not a fan of QE. Neither am I. You seem perturbed, however, when some of us complain that QT is moving too slowly. Because QE was traveling at $120 billion per month before it ended, I think QT should travel at least as fast. However, I’m open to arguments to the contrary. For example, you cited the stock market “blow up” in 2018. Yes, stock prices and house prices declined, but that’s supposed to happen when interest rates rise. The biggest anomaly I recall was the problem with the repo market, when hedge funds that had borrowed short term to invest long term (a stupid practice) got into trouble because no one wanted to lend them virtually free money. Of course, I don’t have your financial database, and my memory isn’t all that great anymore. Thanks.

Confused,

Look, I would like for rates to be higher and QT to be bigger. QE should have never been used in the first place. And rates were kept way too low for way too long. And everyone here is welcome to say what the Fed should have done or shouldn’t have done, and that’s not going to get my dander up.

What gets my dander up is when people say that the Fed isn’t doing QT at all, or isn’t doing it to the extent it said it would, because that’s not true — but this is precisely what the tightening deniers that have fanned out across the internet are trying to post everywhere. That stuff I blow out of the sky with my old 10-gauge double-barrel goose gun.

QT $47.5 Billion a month? Two months of QT $95 Billion?

I don’t think it was the “little bitty QT the Fed did in 2018” that “blew up the stock market, and housing started to get a hit”… it was that the Fed was trying to SIMULTANEOULSLY raise interest rates. They SHOULD have just done one or the other. My choice would have been to clean up the Balance Sheet since there was no market pressure on interest rates at the time.

The markets understood the QT process… it had been telegraphed for almost a year prior to starting it. Those same markets had no idea what the interest rate increases were all about. “When are they happening”… “how much”… etc. THAT is what caused the markets to throw a fit.

I agree. The last chart tells the story.

“Quantitative Tightening”? The Fed expanded 9X in the time period.

Reversing this trend would cause financial chaos. Moderating it will cause much pain. The question is: how much pain can the Fed withstand?

We’ll see.

B

It took 14 years to get there, and you want to reverse that in a few months or a couple of years? You gotta be kidding.

Even at the pace they will be going following the three-month ramp-up (June-August), it will, as you say, “cause much pain.” You can rely on that. Markets that are totally addicted to QE suffocate under QT.

That last graph does show it pretty clearly.. the Fed eats and eats and eats, and then occasionally farts in an attempt to lose some weight. The thoroughly financialized dollar has no more calories left in it, and it no longer satisfies any appetites. Even when the long awaited time comes and the Fed craps a few major dumps, the markets will be left with nothing but steaming piles.

Wolf

Mkt is fighting back b/c it doesn’t trust Fed. Unless Fed takes a bold step in raising the rate (action and NOT jaw boning) nothing will change. No message transmitted to the mkt.

Mkts will remain trading zone. The word ‘neutral’ rate uttered by Mr. Powell in the last press conf, didn’t help. He is unable shed his ‘dovish’ image, itched strongly in investors’ mind since 2018. Who would blame them?

Inflation ‘expectation’ is growing strong roots in the consumers’ mind. No let up in increasing housing prices, rents, medical costs, food and energy. Energy has come down, but NOT consistently, b/c of lack of production in the short term.

‘NOT shocking the mkt’ should be put aside and take immediate, needed steps to contain inflation. But he won’t.

Bay steps in increasing rates and snail pace in QT, won’t help.

Next 2 months inflation numbers will interesting.

Seems to me you will not be able to run a slow multi year unwind. Whose going to hold a financial asset to see it decline for a decade. At some point people are going to run for the door and try not to be a bag holder.

It was easy to run policy when you are making people”rich”. Going the other way, not so much.

Congress is going to spend additional $736 billion,

so called “Inflation reduction”

How ironic, the FED tightened even less than planned because of inflation “income”…why wouldn’t they INCREASE the rolloff by a similar amount?!

It’s all way too little, way too late…it will take 150 months (12.5 years) to reduce assets by 50% at a 30 Billion per month run rate…that would get us back to where total assets were pre-covid … its all a bad joke….that’s why the markets are soaring…the FED isn’t serious regardless of what they say….

“How ironic, the FED tightened even less than planned because of inflation “income”…

What the effing ignorant &^%$#@ are you talking about????

RTGDFA

After multiple reversals, everyone is waiting for a reversal. As you say, this time is different… they can’t.

Until they have to, but that’s a housing collapse away.

I’m going to get you a blood pressure monitor for Christmas.

:-)

I get the sense Wolf responds to comments as needed with perfect tranquility.

bucket of ice will do, need to have that handy

To stick my head in, between comments.

Wold says the Fed isn’t trapped. A lot of people say it is.

I guess we’ll find out.

Wolf had an entire article about that recently, it’s worth looking up.

“Trapped” means higher rates and slower economy, which the Fed wants. There is no trap, only the desired outcome of higher rates. Don’t fight the Fed unless congress fights the Fed.

I would bet on Wolf being right.

I know they’re moving in the right direction, but if they could just sober up and eclipse the speed of a pregnant yak, that would be great.

A pregnant yak probably moves fairly swiftly as compared to the FED, which is moving at the rate of a sloth.

The FED has lost all credibility. I don’t think they will ever regain it.

Loss of faith in institutions of all sorts in recent years. Adding onto what was lost in 2008. It’s going to be a real shit show this decade. The Roe repeal might have shocked people into seeing what’s coming and put things off for a bit, but we’ll see in 2022.

I believe in the institutions when they are staffed by competent people and functioning right. That ain’t happening.

Institutions can function despite incompetent political appointees as long as the people at the lower levels know what they’re doing. That’s what kept the federal government (sort of) functional during the Trump years.

The long-term problem is when smart young people don’t want to go work for the public sector because the leaders are idiots.

We saw the playbook with Greenspan. When things blow up Congress will blame it all on the Fed chairman’s believe in markets, borrowing $30 T and making unfunded promises has nothing to do with it.

In essence what the FED is trying to do is reduce inflation via wage suppression which represents about half of consumer spending while leaving asset inflation based spending alone.

They are trying to engineer a soft landing for inflation while still maintaining elevated asset prices which only leads to reduced living standards for workers while asset holders continue to spend freely with the capital gains from elevated asset prices. One of these days the younger people will figure out the system is rigged against them.

What? Wage suppression? That makes no sense.

It’s not the Fed that is suppressing wages, it’s people all too willing to live by the monthly payment systems instead of saving for their purchases. They have built their own rent-seeking prison and the Fed is stuck with the liquidity problem. This western behavior drives too much investment into flipping assets and importing rather than producing the goods needed domestically

I think the inflationary cost of production still has a long way to go to catch up to asset prices. My factory generates a profit of about 30% from total revenues, but at the end of the year the money is just script in comparison to the inflation of assets and the burn, and the incentive to expand is removed. This is a structural problem that is causing more production to drop off the market for those who refuse to add production through financialization/increasing debt when many business owners can easily afford to pack it in and retire.

Higher borrowing rates is only going to inflate the cost of production and this may be the intended purpose…..to inflate production and deflate the price of bloated assets classes. Think of it as a re-balancing of necessities and regional supply chains.

The real pain is yet to come……

VERY good comment IMHO, MS:

Time and enough to ”help” ALL of our actual ”producers of wealth”,,, formerly known as ”creators” make and continue to make their folks, no matter if ”employee” or ”contractor” or any other such ”description ”

The point is to get ALL manufacturing BACK TO USA,,,, AND not only ASAP,

But, especially back ASAP to where the various and sundry ”challenges” of 21st era make better balance.

@Mark Stoneweapon – 100% correct.

many of those with real assets and savings are now in capital preservation mode. they’re taking the ball and going home.

the fed can move the cards around the table as much as they want but it’s just a financializaton game that can’t actually create wealth.

Mark Stoneweapon

All the easy-peasy’ of Trillions went into financializing the economy but little into ‘productive’ economy like manufacturing and living wage jobs. Fed has relied on ‘wealth effect’ which is NOT working but in fact has increased inequality in wealth and income, which Mr. Powell denies consistently.

Who cares about ‘earnings’ when ‘buy-back’ shares program using ZRP pads the options and again borrow ZRP and issue corporate bonds. Fed has actively involved in the distorting economy and assisting asset inflation.

Asset inflation is not in their equation.

Mkts and mkt expectation remain disconnected. They don’t trust Mr. Powell and his taking hesitatingly baby steps, won’t send any message. More volatility and churning remains.

I don’t think they are trying to keep asset prices up…I think JP has pretty much stated that asset prices will come down. He told Millenials to reconsider if they were planning to purchase a house soon, and as the market was selling off, I believe he and other FRB members stated that the market seemed to be getting the message. I think JP actually intends to drive asset prices down. How successful they are? We shall see in time.

Bit confused about TIPS. Since Fed creates money out out of thin air when it buys something (like treasuries), it would mean it destroys money when it sells something (i.e. Fed gets paid).

So it would seem if TIPS mature and they get paid the face value + interest, this would have the effect of extra money buying burned.

Codedude,

“So it would seem if TIPS mature and they get paid the face value + interest, this would have the effect of extra money buying burned.”

Yes, it does when TIPS mature and come off the balance sheet. And that happened on July 15, when $9.6 billion in TIPS matured and rolled off, along with $2.5 billion in inflation protection, for a total = $12.15 that rolled off and vanished. That roll-off alone destroyed $12.15 billion.

Ok, I got it it, I think. The compensation is not cash. You wrote:

“Treasury Inflation-Protected Securities (TIPS) pay inflation compensation that is added to the principal value of the TIPS. When TIPS mature, holders receive the amount of original face value plus the accumulated inflation compensation that was added to the principal.”

Thank you.

Doesn’t FED send the income from interest to the Treasury Department? If so the interest income does not disappear.

The Federal Reserve ANNUALLY REBATES 94% OF ITS PROFITS to the US Treasury which includes profits from both US Treasuries and MBS instruments, but that does not directly send interest from US Treasuries to the US Treasury.

I am puzzled by the fact that they did not immediately start with 100 billion a month QT back in June. This three month transition period of 47 billion a month seems to be deliberately designed to appease the stock market. It is kind of ridiculous imo.

Last time (2018), the phase in was much longer and much slower. It was like a snail, and it still ripped up the markets about 9 months into it. Markets that are addicted to QE suffocate under QT.

When someone was addicted to heroin in the good old days, the treatment was to have them kick the habit “cold turkey.” At this point, the markets, and the overpaid Wall Street casino hustlers, have been given sufficient notice that the era of risk-free betting is coming to an end. Rather than worry about their suffering, the Fed should focus on ending the suffering that inflation causes for most Americans.

The stock market was declared a bear market on June 13.

Rising employment does not seem like a recession.

Yes, it’s seems very unlikely that we’re in an official recession with this kind of labor market, that kind of job growth.

Wolf

Baby steps in raising the rates and snail pace in QT, actually sends the WRONG message that Fed is really NOT serious about and is afraid of hard landing and inducing recession!

The attitude of NOT shocking the mkt, adopted by Mr. Powell is again the wrong message. No wonder Mkt doesn’t trust him to administer strong medicine. Why should they? They are even NOT afraid of QT b/c of it’s slow and impractical pace, so far.

When does the Mkt really get the message? I am still waiting!

Just my humble opinion…but it seems like they are trying to walk things down slowly. They want to remove the excess money, but don’t want panic, or a market crash in stocks and real estate. Moving assets lower slowly is waaaayyyyy different than a crash and panic.

100 billion a month is a TON. Things will start breaking, especially if the economy is bumpy when they start. The ramp up makes sense and $47b is not nothing, but they should have started it sooner than June. Everything made sense when the SPY was at 375. But now, they should probably exceed their caps in August given how much the market has gone up. Instead of just jawboning, they could let an extra $10 billion roll off and issue a press release – “the market is so strong that we can be more aggressive.”. That would change the narrative.

Supposedly each month they are fully running off balance sheet is roughly equal to a 1% addition to whatever the Fed rate is. So things are tightening pretty fast, but it hasn’t really affected people’s behaviour to much yet except housing. That is going to be what gets hit hard by monetary policy first.

Greg

Unless one breaks ‘eggs’ there is NO omelet.

it is the price for their’ ill thought out’ monetary policies of over two decades! Using debt on debt by creating insane credit creation has serious consequences. I say ‘ rip the band aid’ NOW!

After three months it doubles as I recall.

That means the cap will be 90 billion (?) starting in Sept….a month that historically is a down month for stocks.

Should be interesting.

QE =Bitcoin

QT =Bitcoin falling

High risk markets already started to roll over after fed wire in 2021 — even while fed was loading up on MBS and UST…

Just more open throught operations…

Private money supply destruction >>>>> pittance created/destroyed by “central” banks who spend far more effort on DSE models than managing risk…

Looking at the last chart where the scale starts at 0, how can you seriously consider that the Fed is fighting inflation? QT so far took a teeny tiny drop from the enormous ocean that was QE. It will likely stop at the first clear signs of recession. Look at how much Fed ate into its balance sheet during the “good times”. It was less than 20% from peak to trough. Fed ultimately wants inflation to clear old debts and fund the massive Federal government deficit, which is going nowhere.

Konstantin,

Assets CANNOT go back to where the were in 2007 because of “currency in circulation” (paper dollars). This is how that works:

1. Assets on the balance sheet = liabilities + capital (minimal). Any balance sheet anywhere.

2. The Fed’s assets will have to be more than the liabilities. So you have to look at biggest liabilities to see how far assets can drop.

The biggest liabilities:

1. Reserves can down a lot maybe by -$2 trillion;

2. RRPs (reverse repos) can and will go to $0 as QT grows, so -$2.2 trillion.

3. “Currency in circulation” (paper dollars) is driven by global demand for paper dollars. And that has been growing over the decades. It’s $2.27 trillion now and will keep growing. As long as people globally want to hold paper dollars, the Fed must provide them. The Fed does this via the US banking system. Foreign banks get their paper dollars through relationships with US banks. And as long as customers globally walk into a bank to buy paper dollars, the Fed must provide them.

US banks get paper dollars from the Fed in exchange for collateral, things like Treasury securities. This collateral goes to the asset side of the Fed’s balance sheet. It’s a trade with the banks. So assets will always be higher than currency in circulation.

Add that up: paper dollars and some reserves, you’ll get to about $4 trillion in liabilities at a minimum. So the Fed’s MUST have at least $4 trillion in assets.

So it’s impossible to go back to $800 billion or whatever. Before QE, the Fed’s balance sheet – assets and liabilities — has always grown with currency in circulation and with the economy. So it’s silly to think that the Fed can go back there. Right now, the lower limit is around $4 trillion, and that grows over time, as I just said.

Thank makes a lot of sense Wolf around my comments on Dollar strength. Thanks for that explanation!

Wolf,

Thx much for the reply/comment explanation on how much the FED at max can reduce its balance sheet and the article explaining the how QT and the reduction of the balance sheet has reduced the balance sheet of the FED.

It helped this reader very much.

Total assets down $91B, or about 1% from the peak. RRP is down $139B from the peak, down about 6%. JP valve released liquidity.

What will happen to UST10Y & UST30Y if Fed Total Assets reach $15T.

The more realistic question is: What will happen to UST10Y when Fed Total Assets reach $5T or $6T?

Q1 2023 – BOA is forecasting 2% for the UST10Y on Bloomberg today….. I assume stocks will be much lower if the UST10Y is 2% or less with QT.

AAPL, GOOGL, BRK/A, Big$Mike… have more cash than the gov have. Best friends helping hands. Best friends enrich themselves when our gov in need. Are u one of them.

Thanks Michael E I was thinking the same thing. Unfortunately the big tech are supported and rewarded with the Wallstreet casino as you frequently point out. I wish I had your experiences and wisdom for the details behind this travesty. As Wolf points out the timing is a minimum of 9 months for the effects of QT and Fed Funds Rate increases to meaningfully impact the markets and economy and we are just starting the process.

The private sector is not cooperating and I read that margin purchases of equity was increasing again but have not seen any charts.

The number of companies raising guidance or reaffirming guidance far out number the companies cutting forward guidance. The economy is bubbling along and it will take much higher rates for longer to quash inflation! Of course, banana-republic Jerome is continuing to slow-walk hikes and QT allowing inflation to run redhot for almost 2 years while the FFR sits at 2.25% and a measly few billion of $$$ destroyed!

The western economists are laughing at Turkey’s Erdogan who is keeping interest rates below the rate of inflation. It’s risibly called Erdo-omics. I guess Banana-republic jerome and other western central banks are acolytes of Erdo-omics!

At the Fed is hiking rates, and quite fast (though way too late), not cutting them, unlike Erdo-omics :-]

But the FFR was at effectively zero(ZIRP so basically nowhere to cut) while inflATION was growing hotter and hotter for over a year! So, your point is Erdogan is an idiot and Jerome and the western central bankers are volker-like genius’! OK, got it!

YOU made the point. I just shot it down with my double-barrel goose gun.

In your mind!

I have heard from several people specially from turkey that erdo-omics is really great ,etc…. But they have not been able to provide any rational explanation.

I guess Erdo-omics means ~70% inflation and currency deprecation ~500% in last years :)

Once CPI prints lower, the FED, media, and politicians will declare victory “inflation has peaked!, blah-blah” Then The FED will have the cover they need to pause their hikes by the Fall (right before the midterms). They are 100% not serious about truly fighting inflation. In real life, everyone knows inflation is 15-20%, and the FED is at 2.25%! LOL! This is still highly accommodative/negative real rates. The QT and MBS sales are pathetic and will also not go very far. “Inflate or die”

I’ve read a few books and papers on inflation/deflation.

I’m not an expert but the explanation below makes sense to me.

Since the mass exodus of manufacturing to cheaper countries, the Fed has been battling deflation. Electronics, clothing, household goods, etc that are manufactured overseas and sold in the US cheaply, is a severe deflationary trend.

The Fed has not been trying to keep the inflation rate down to 2%, they have been trying to keep the inflation rate up to 2% to battle deflation.

The pandemic changed all of that. Cheap manufacturing was shut down due to draconian Covid lockdowns. Ships and trucks and all transport soared in costs. This eliminated any deflationary pressure. Formerly cheap plentiful goods became scarce and expensive.

Meanwhile, the Fed was still lowering rates and printing money forming a positive feedback loop on rising prices.

The Fed was half-correct when they blamed supply chain issues for higher prices and inflation on the supply side. They are now working on the demand side and relieving people of excess cash that they handed out during the pandemic which as Wolf pointed out, people are gleefully spending to go on expensive trips and buy expensive stuff at any price.

Eventually, inflation and the Fed will take back all of the free money and cheap manufacturing will be operating at full-speed and ships will be unloaded.

We will be back to normal. Less money and cheaper stuff.

The Fed will then resume its fight against deflation.

Good synopsis Bob, but you left out the impact of asset prices. As people had all that extra cash much of it went into asset purchases. Homes and stocks shot higher. Now stocks have pulled back, but with the exception of tech stocks, not that much. And homes are still sky-high.

High home values are the ultimate stimulator to the economy, as the average person feels rich, so they spend more.

Bank balances will drop and credit card payments will rise to their pre-pandemic levels and then go even further. Once the economy loses steam and inflation is still high, then we have home prices start to really crack (over the next 6 months). But home prices will need to drop for 3-5 years and will cause massive debt problems and insolvency of the quasi-government entities that have absorbed all that toxic exposure.

This is a long term huge problem.

The fear of deflation is crazy. Tech companies deal with an inflationary environment all the time. It benefits consumers leadint to better products for lower prices. It rewards savers and leads to a more stable economy, with much less concentration of wealth.

All debt has to be supported by real income. Asset prices and debt levels can only go to the moon if interest rates are zero to negative in real terms.

We will find out within the next few months or years how high real yields can go before the weakest go under.

gametv

‘The fear of deflation is crazy’

NOT crazy, when the debts of all and kind are at record levels unlike any time before in human history! How is the required interests payments serviced? With more debts, like they have down for over a decade. Where does this end? Assets are built foundation of ZRP + SWAPS+CDOs wtc

Debt to GDP of USA is at ‘least’ over 130% – Total debt 31 Trillions

Global wise Debt to GDP over 200%. Total debt from 5.1 Trillions in ’08 to 303 Trillions now!

Guess just print more right?

“High home values are the ultimate stimulator to the economy, as the average person feels rich, so they spend more.”

I agree, if home prices in today’s dollars become underwater, then people will spend less and possibly panic sell and cause an oversupply and crash in house prices.

The trick is to let inflation continue to whittle away at the real value of the house. The current dollar value of the house can stay constant.

If interest rates go up, then the demand for a house should flatten at some optimal price. It may stay flat for years while inflation eats away at the real value of the house.

If you bought your house for $1M and have a job to pay the mortgage, you will not panic if your house price is flat. In real inflated dollars, the value of your house becomes cheaper deflating any bubble.

ie you would have made 9.6% more money if you hadn’t purchased the house and bought 9.6% Ibonds with the $1M.

A soft landing is possible with assets such as houses. The Fed can control the demand and prices with interest rates. House prices will not be inflation protected but will also not drop significantly to cause a massive oversupply and sell-off like in 2008.

JG, You are extremely optimistic.

Things take a long time in this large of an economy and the fed might be neutral by fall of 2023 maybe. There is a lot of slush money in the system. It isn’t just going to go away like magic. IF it did, we’d be in a Depression overnight.

For instance housing, it takes a year of bad times to get foreclosures up to a point that they actually start affecting prices. The banks can prolong that downturn by not actually foreclosing, like they did after 2008/9. People caught at the top can’t just sell at a 20% discount without extreme pain.

Mortgage rates have doubled just because the largest purchaser of MBSs started to not buy. House sales haven’t stopped and prices have continued to rise or not go down much YET.. When the fed really gets going and stops repurchasing and allow QT of the MBS market, things will get really interesting but that doesn’t mean prices will immediately collapse. They never have before. It is a slow process to bring housing prices down, if it is even possible.

I don’t see much of anything happening before the mid terms. It is possible that the real collapse of the markets doesn’t happen until around the elections in 2024. If the politicians are lucky or their handlers, it won’t actually happen until after the next presidential election. Then the next President can be a hero as the economy recovers during their term.

“They never have before.” Say what?

Very good article.

“The Fed then amortizes the premium to zero over the remaining maturity of the bond, while it receives over the same time the higher coupon interest payments”

Higher coupon? When were treasuries issued with higher coupons than today…..decades ago? Would that be a correct understanding? Just asking.

As for the TIPS credit adding to the balance sheet, Bull and Bear asked does this not then go to the Treasury, which would then drop the balance sheet tally?

Thanks

Yes, much higher coupons than in the QE period between March 2020 and Dec 2021.

For example, in the five years between 2014 and 2018, the 10-year yield was between 1.5% and 3%, mostly around 2% to 3%.

So if the Fed bought in May 2020 a 10-year note issued in 2018 with a coupon of 2.8%, it gets that 2.8% coupon interest payment until maturity (2028). But in May 2020, the market yield for an 8-year yield (remaining maturity of the 10-year note) was maybe 0.6%.

So the Fed (and everyone else) had to pay a huge premium to get an 8-year maturity with a coupon of 2.8% when the equivalent market yields was 0.6%.

“Markets that are addicted to QE suffocate under QT.”

And suffocate they will, under QT, rising interest rates, or inflation.

With QE and NIRP/ZIRP, The Fed had several years where it could have resolved the causes of the 2008 debacle, but it didn’t, and now it can’t. The FIC didn’t want to fuck around with a DJIA under 10k forever, for example, and instead wanted to ignore the problems, hide them under trillions in debt, return to business as usual, and pretend the hot mess wouldn’t worsen and blow up a few years later. But in doing so the FIC robbed its own future, and once Mister Market has to stare reality in the face it’s going to panic and send the world into a nastier version of 2008. And this time QE and NIRP/ZIRP won’t be saving anybody.

Meanwhile, the planet is burning.

Ticktickticktick . . .

NOT with the glacial pace. Too late and Too little. NOT with the fear of hard landing and inducing the recession.

Mkts don’t trust him. He has lost his credibility and Jawboning won’t help this time.

Why would The Fed need ‘credibility’? For YOUR benefit? I don’t think so.

You guys really need to get off this credibility thing. It’s not helping you.

And what about the strength of the dollar? The dollar index is at 106, the highest it’s been since Oct 2001. Through Financial Collapses & Pandemics it has done nothing but go up.

Yes, we’ve printed a ton of money that everyone now uses around the world, but the value of it hasn’t collapsed. And with interest rates doing nothing but going up, the value of the Dollar will follow accordingly, especially with QT absorbing more of those dollars.

So strength of the Dollar means we lose exports to cheaper options, but it also means we can continue to buy unlimited cheap goods. Yeah! And yes, unemployment will be the key!

Until we see job growth contract meaningfully… the Fed will implement the one mandate it is focused on… reducing inflation! And when the labor market contracts, if it hasn’t slayed inflation, it will have some decisions to make.

But as Wolf said, don’t fight the Fed!

Me? I lost a bit on my Bond Shorting strategy over the last week or so, but that chicken is coming home to roost! I’m confident of that!

Oops, meant Oct 2002 for the Dollar Index level!

With STRONG US$, we are exporting inflation to other countries, where they don’t have ‘trustable’ global currency of their own!

All EM Countries, with loans designated in US $ + China which continues boasts a lot but pegs the Yuan to $ in a trading range.

Can We “Export Inflation?” Yes We Can, Yes We Are

August 1, 2022 ( h/t CH Smith)

The USD is not strong, just less weak than others. There is one objective meter for the strength and stability of your money and that’s how much gold it buys.

Wolf, could you clarify/confirm one thing regarding the MBS purchases:

As you’ve made clear a number of times before, the reduction in MBS purchases that are part of the MBS QT plan don’t show up on the Fed’s balance sheet until the purchases settle 1-3 months after purchases are agreed to in the TBA market. However (and this is the part I would like you to confirm), the impact on the market – the impact on mortgage rates via supply and demand for MBSs – occurs when the purchase is made in the TBA market, correct? So, while the impact to the Fed’s balance sheet from July’s reduced MBS purchases in the TBA market won’t be seen for another 1-3 months, the impact to mortgage rates in July from these reduced MBS purchases should have already been transmitted, correct?

curious how the Fed has no problem buying MBSs 40,000 million a month (40 billion) ….but seems to only rely on attrition, principle paydown, etc.. to reduce that which they bought with both hands.

that is why the market does not believe the Fed at all.

Didn’t the fed buy most of the MBSs from GSEs?

So selling them into the market would be looking for institutional buyers, right?

Who are now having to buy the newly created MBSs and that is why mortgage rates have doubled?

If I’m correct, then selling MBSs would drive a wooden stake into the heart of that Vampire and there would be virtually no new sales of homes as interest rates would be? A lot higher!

Wolf

Could we say that first QE’s are directing to the assets and created asset inflation but last QE is directing to people and created real inflation.

Thank you

What time does the inter-meeting rate hike of 2% come from the banana-republic fed!??? Anyone believe they are serious about quashing inflation left?????

still at near record disparity Fed Funds to CPI

but we are assured they are “keeping a close eye” on it.

1) Gringo, both Erdogan and JP keep rates below the inflation rate.

Erdogan deflated labor, JP deflate gov debt.

2) Nerd #1 and China’s drill is a knock knock missile. No harm is done.

3) The Fed raise rates, trim Total Assets and release RRP liquidity in a

balancing act.

4) If China harm NDX, RRP deflate and the Fed Total Assets might reach $15T.

Doesn’t really matter who owns the Fed’s assets, unless these assets are retired, which is inflationary. After you monetize spending, then cancel the bond you posted as collateral, you have the money but not the obligation. Then you reverse the policy of forty years of deficit spending.

Ambrose Bierce

Fed is behind the curve from the very start and then hesitatingly too little and too late. See the demographics in the last 10 yrs, below. Labor shortages will persist.

Fed ignoring asset inflation but focusing labor with out understanding the demographic changes right under their nose!

Not impossible to grow the economy while the money supply contracts, but it does seem like it will be highly inflationary, for a long time.

This is about QE and QT. It’s not the assets that matter but the money to buy assets with that matters. When the Fed sheds assets, it destroys money and there is less money then to chase assets and asset prices come down. Opposite of QE.

NOT disagreeing with you.

But I am still waiting!

Interesting how many Calvinism adherence bound people want a crash.

In reality, this is, as Wolf says, going to be a very long process to tame inflation. One of the hardest things for people to understand is that most of the Feds balance sheet is gone overseas into the world banking system and has no effect on the domestic economy. This trade America money is sent for huge imports of cheap goods to keep America humming along. QT is just a blip designed to soak up the drop in dollar demand from sanctions. The soft nature of the dollar is not coming out during a crisis, but with long term decline of the international trading system.

Now China cutting off trade with us would have a huge impact on the value of the dollar. That is a shock. But not yet…. so the value of the dollar goes up with QT

Someday this war’s gonna end…

I’m now thoroughly confused about everything. Today the internet is saying there was a surprisingly strong jobs report, and yet also reports that mortgage rates are still dropping today. Just a newbie here trying to understand all this, but I had thought that would mean the opposite!

Oops. My husband and I are under contract for a house (felt we had to buy because of job loss, relocation, rent going wayyy up, plus a 12 yr old boy in the upstairs apartment doing karate jumps and waking up our 2 yr old from her naps *all the time.*) So we locked in at 4.875 earlier this week thinking it was some kind of dip. But now the rates just keep dropping, so maybe we should have waited.

Nope…..in a year from now I think you will be glad you locked in. In Canada half the mortgage market is floating on variable rates…..they are not paying any principle right now and will have to reset soon. I think it was Q4 2020/Q1 2021 our 10 year bond was trading at a higher yield than mortgage rates. People has 6 months to lock in at 1-5-1.7% for 4-5 year term. It was a no brainer.

You’re not confused. THE MARKETS ARE CONFUSED, and the action in the markets is BEYOND LAUGHABLE TODAY as the whole scam and false bogus ‘beliefs’ in the Federal Reserve come crashing down in a heap of hopium smoke, the likes of which have never been seen before!

No shame in being a newbie… we all are at one moment or another. You are doing well tuning into Wolf… he knows of what he speaks and as a statistician extraordinaire he’s pretty balanced…. although a little disappointed in the most reckless Fed of all time!

Now, to your question, the reason Mortgages having been going down over the last couple weeks, is that the 30yr. Bond has been skyrocketing (yield has moved down) from about 3.43% to around 2.9% at points. This has a direct effect on mortgage rates.

The reason for this is that there is some delusion the markets are in about what the Fed is doing, but they are tightening and the 30yr yield will head higher. Don’t fight the Fed!

So, bottom-line, you were wise to lock in at these lower rates. You will see mortgages head back up towards the 6-7% range, no doubt IMHO!

Yes, I’m learning so much from the Wolfstreet articles and comments!

Now, not to make you nervous, but just because you got a low interest rate, doesn’t mean your buying a house worth it’s value.

Many here will tell you that housing prices are way too inflated and that the value will crash. Could be, we’ll see. You could end up ‘under water’, meaning the mortgage you have is above the value of your house.

If you are buying the house to be in for the long haul, probably not to worry. However, if you plan to move again in the next, say, 5 years? Well, you may end up losing some money!

Good points WolfGoat, it’s a lousy market for investors / short term holders, but bear in mind that RE is ultimately local. There are pockets where value exists. The biggest risk I see is forced relocation. Job loss is the same either way, and a landlord is less likely to work with you than a bank. A landlord wants their rent, a bank generally would rather not own another foreclosure.

The future value of residential real estate is very unclear IMO. So many factors affect it. Seems to me the risk is heavily to the down side of price for most places.

If you own in an area where there are new and expanding jobs or that is valued as Boomers retire and relocate, prices should be much more stable than if you own in an area where there are business closings, new dangers from floods, wildfires or even drought. Things like Work from Home brought high values to the Burbs but high energy costs may reverse that.

Add in interest rates rising or inflation leading to demand destruction leading to the most severe recession in our time.. Not good for housing.

Both corporations and the government need the high valuation of assets as the lending on such is what creates money. Lower valuations actually means less money creation and that means less profits and less taxes collected and less available to buy both corporate and government bonds.

The fed is walking a tight rope over a very deep chasm. Tighten too fast and the liquidity dries up and collapse happens very fast. Go to slow and inflation destroys demand and earnings collapse and layoffs destroy demand.

I say this is a very risky time to purchase any asset. Good Luck.

Mortgage interest rates are all based on the 10 year US Treasury yield (interest rate) and not on the 30 year US Treasury yield.

Thanks… got it! 10’s have been following 30’s down as well, but up 16 basis points today. As Wolf commented, mortgages jumped with this bump.

So PonderingPA, rest assured there’s no where to go but up with rates at this point… and also rest assured, ‘nothing goes to heck in a straight line’!

WolfGoat – Noone is wise to buy an inflated home price in order to lock in a current rate. You dont understand economics.

A home with a home loan is a leveraged asset, and the most highly leveraged investment anyone will make (even with a 20% down payment).

The future value of homes over the course of the next 5 years will be dependent upon the monthly payment of the home. The pool of potential buyers falls as monthly payments increase. So while home prices flew higher but low interest rates kept monthly payments low, there was sufficient buyer demand. But once interest rates increase, the monthly payments explode higher and the demand dries up.

Over a period of time, the balance between buyers and sellers tips toward buyers. Inventories rise and sales stagnate. Then prices start to fall. But it will take a good solid year of falling prices before the market understands that home prices are 50% overpriced in many places.

The future home price is totally dependent upon monthly payments. If you believe inflation is transitory, then you can wait it out until interest rates drop again, but if you believe the Fed will have to push them much higher to stop inflation, then a home is a terrible investment right now.

Stop giving bad advice.

Yep, I am worried about all this!

PonderingPA, a house is not an investment. It’s a place to live.

Also, in most markets, you won’t see anything like a 50% drop. Housing prices are stickier than that.

If you can sleep at night with your mortgage payments, relax. It’ll all work out.

WolfGoat was not giving you bad advice.

I don’t know if I was giving good advise or bad advise… but consider this GameTV… she, her husband and 2yr. child need to live ‘somewhere’.

Paying rent in a rising inflationary period, with no chance of any equity being built up is certainly less desirable than paying a fix mortgage that you can budget around.

What happens in 1 year, 2 years… who knows, she may lose some equity, maybe not. My advise was to get locked in and live in the house for 15-20 even 30 years and pay off the mortgage.

If that is her headset, the value of the house will ultimately be realized in that when she does pay it off, she owns it and never has to worry about the value again!

I think that’s called planning for retirement!

One tip and from a more recent comment it seems you may already bring so this, read the article, then read all of Wolfs comments (and their context) I usually search the page for Wolf Richter so I can just jump right to them, and then reread the article.

Correction: change already bring this, to already doing this

Forget the interest rates, the key problem is that you are buying a leverage asset that is going to fall in value. Your whole down payment will be wiped out with a mere 10-20% decline in the asset price.

If you are fine with losing that capital, go ahead.

If you believe anything Wolf writes about the stickiness of inflation and how the Fed will be forced to fight it, you need to not buy a home right now (unless you are getting a great deal or buying in a market that has not appreciated recently)

PonderingPA,

I hope you locked in your mortgage rate because the 30-year fixed jumped today. Back to 5.45%, upon the jobs report.

https://wolfstreet.com/2022/08/05/recession-mongers-shocked-horrified-by-this-surge-in-employment/

Mortgage rates have been bouncing around like a pinball caught between bumpers.

I see both sides of this discussion.

Interest rates have in the past gone down in a recession but will they this time? Or will they continue to go up as 30+ years of risk denial is coming to fruition.

Bouncing around like a pinball off the bumpers is good.

Banks have to lend money to exist. Can they if the economy goes to hell in a handbag? They have not relied upon deposits for a long while as they have been able to pkg and pass along the loans to others but I wonder if the others, like PE and Pension funds will have the capital to buy them as re-balancing risk occurs. Blackrock already had a really bad qtr.

1) The Fed is a bank, the bank of the last resort. In the next downturn

the Fed will select who live, who die.

2) COLA is baked in. Rent is baked in, until it stop. If after a knock knock

warning shot come the thing ==> shortages are baked in.

3) RE deflate/CPI rise. RE might deflated until it stop, but in real terms inflation accumulation might shave assets for another decade

or two.

4) The Fed cannot fight exogenous causes. The virus is the cause, the

printing to keep the comatose economy are the symptoms.

5) Blame the Fed always work. They never answer back.

It’s great to get the money printer bandits out of the TIPS market, finally we can hedge for inflation a bit. I bet they think there won’t be any inflation in the future.

The level of criminality has subsided a few %.

Today’s strong report is a shocker to the mkt, expecting a Fed pivot late this year. Establishment blew the (528K )number of Household (174 K) survey over 340, 000! Big disconnect!

As I wrote several days ago demographics favor labor shortage b/c for the past 10 (2010-2011) 55y or below increased just 1.2 Millions but 55Y or above went up 21.1 Millions, most the bump is at 65-75y!

MSM is clueless! A lot of work cut out for this ultra dovish Fed. QT is at a slow pace NOT facing the reality. But, of course, Fed doesn’t want to shock the mkts, right?

It will be green by the close.

Butters

Unlikely, but you could be right!

B/c the power of perception remains strong, against the reality and the fundamentals.

Hence my ‘swing’ trading (major indexes by leveraged ETFs – long/short )cuts all the volatility and holds my portfolio close to neutral, if not very slightly at the end of day. For the last 3 weeks!

But long term remains bearish.

We desperately need a housing collapse to prevent America becoming a third world country.

I came from a third world country and in the last 20 years I see America slowly converting into one.

So sad to see this.

Rip.

Exactly where it is headed. US is new Brazil.

Only rip roaring inflation, beyond the control of Fed like in late 70s, with rates increasing continuously, may (?) bring some sanity.

Unfortunately Mr. Powell is NOT MR. Volcker as I witnessed action.

It will get WORSE before it gets better!

Your writing technique, as again evidenced in this article, explains much even within the parentheticals.

Not that my opinion amounts to anything, but I continue to be truly impressed by your style, skill, knowledge, dedication and deftness of communication.

Wolf…

We all learn about the workings of the Fed from you and I suspect that is why many are on this site.

Thanks.

Could you explain this…

“The Fed received from the government $4.6 billion in inflation compensation, which increased the balance by $4.6 billion”

If Federal Reserve notes are liabilities on the balance sheet, and the Fed receives this 4.6 billion dollars in this inflation compensation, why wouldnt that money be an offset to those note liabilities, ie create a reduction in the Fed’s liabilities, thus a reduction in the balance sheet? I know it doesnt work this way, but wouldnt that make sense? Is there a choice on how they treat this?

In terms of the inflation protection, the key is that there is no cash involved until the bonds mature and is paid off. During the life of the bond, the inflation protection is added to the principal, and not paid in cash.

TIPS and i-bonds work the same way in that the holders gets the inflation protection amount added to the principal, instead of paid in cash. So the value of the bond increases as the inflation protection is added to the principal. When the $1,000 bond matures after 10 years, the holder might then get $1,500 in cash from the Treasury Dept, which covers the original $1,000 in face value plus the $500 in inflation protection over the 10 years.

I hope that answers your question.

thanks

Wolf – You are being too kind to the Fed in regards to the pace of QT. 50 billion in sales with almost no sales of MBS is a JOKE. Your chart also does not go back far enough. If the chart was pulled back further, it would be even more evident that the Fed piled on the QE, but has not sold hardly any off.

With the price of homes skyrocketing over such a short time period, why would the Fed not have been selling MBS very rapidly to drive interest rates much higher? Increased home prices are probably the number factor in pushing inflation higher right now. People think they are rich and go out and buy more stuff. Higher home prices also ignite higher rent, as people are priced out of buying a home.

My view also…they are not serious at all. With one 50bps raise this weekend…the FED will be taken seriously…until then, not so much.

This is like watching paint dry, except it is much more interesting since the psychological effects on the financial markets are like yelling fire in a crowded theater (which may be a felony!). Now, if the Fed thinks that the Band of Monetarists can shrink their balance sheet to $5 Trillion or whatever number one expostulates, then even a $150 Billion reduction via Runoff, Outright Sales, or Revaluations will take what ineffective (vis a vis Inflation Containment) time period to lope off $3.9 Trillion: Drumroll or eggroll please: The answer is 26 months while the Inflation Genie eats everyone’s lunch, literally.

Now we choose $5 Trillion based upon what Wolfmeister says above about normal growth in the money supply/monetary base and then add in a cool $1 Trillion to build in a buffer, since $5 Trillion of residual Fed balance sheet is possibly threatening to collapse a financial system, economy, and Government addicted to and constructed with Cheap Money that flows like water across the land forever and ever, World without end.

Now since we know that a $150 Billion monthly BS reduction by whatever alchemist’s method the Fed employs is higher than stated amounts to date, we will used a 30 months window for this eye-opener. I use the royal reference of WE since “we” are all stuck in this mess together, sort of jointed at the hips as victims of overzealous agencies.

2.5 years to normalize or even pretend to normalize the level of liquidity and the cost of money in the American economy and financial system. The front-loading of interest rate hikes, affecting the short end of the Yield Curve primarily, is going to get us to north of 4% for Fed Funds by December 31, I bet Wolf’s next royalty check on it! Since this is the most visible sign of Fed tightening activity to the average American, we can expect the Fed to stop stealing the limelight by mid-2023 with a Funds Rate around 6% to 7%, still probably 100 to 300 basis points below the then-current inflation rate for us suffering Americans. No Paul Volcker starch in the shorts there! Inflation is going to punch the American economy and global economies like a George Foreman haymaker!!

So the Fed is going to pivot, and a raucous cheer goes up from the speculating crowd on Wall & Broad with just a whisper of that word, but the so-called “pivot” will be to utilize QT until the cows come home or a very hard collapse of the economy and/or financial system happens first.

There will be no soft-landing in this whole exercise, the rubber band of valuations, debt accumulation, and consumer mindsets have been stretched way too far out of normal parameters to allow this monetary C-10 to land “softly” without any tested landing gear. The Fed took 14 years to put us in this perilous state ( of course, “we” drank the Kool-Aid! ), so the ship will not be put back on a steady, sustainable course in less than 3 years time. Ain’t going to happen.

Any who, I am having more fun watching what Mr. Market is saying about stock prices and bond yields. Really very tired of hearing the pablum coming from the grossly conflicted members of the Federal Reserve Board which seems to often change with the wind and the wind currents are going to be very strong and very variable going forward. The markets are where price discovery should have been located since 2007, and manipulating the markets for over 14 years in unprecedented fashion will have unprecedented effects.

Yep. There is a political element to it as always. Right now politicians are worried most about inflation. Once the layoffs hit big, then people will be screaming about unemployment. Powell will have to tap dance at the press conferences then.

You cannot have the CAKE and eat it too!

David W young

Couldn’t said it better. Same thoughts here.

14 yrs of ill thought out monetary policies, insane credit creation, everything bubble.

Inflation erupting after 41 years of deflation, NOT that easy to contain, especially this ‘ dovish but wearing hawkish’ skin pontificating that they are really serious containing the inflation. OMG!

Statically glitch between Establishment vs Household survey, making employment number higher than it is actually!? Is it intentional? Politics?

The number of multiple jobholders whose primary and secondary jobs are both as ‘full-time’ just hit a record high, and apparently recorded as FULL TIME JOBS!

So what’s going on here? The simple answer: Fewer people working, but more people working more than one job, a rotation which picked up in earnest some time in March and which has only been captured by the Household survey.[..]

‘surprised to learn that something appears to have snapped a few months ago, around March, when the Establishment Survey kept on rising unperturbed, while the Household Survey hit some unexplained brick wall, and hasn’t moved at all. In fact, since March, the Establishment Survey shows a gain of 1.680 million jobs while the Household Survey shows an employment loss of 168K!

(h/t ZH)

Since this from. I am waiting for confirmation from other source.

Hello Wolf,

Will this QT even in when they go up to the 95 billion per month, be done so only through maturity rolloff without replacement. Or will those same primary dealers that the Fed purchased those bonds through, be forced to buy back those from the Fed at value it determines? Have not seen many discuss this matter.

At this point, QT will be from maturing securities getting paid off. As you can imaging, with a $8.7 trillion portfolio, there is a lot of stuff maturing all the time.

Thank you for easy to read charts that quickly reveal Fed policy.

No one else does that.

I watch real estate listings fairly closely in a few mid-to-large size popular cities. The market seems to be cooling pretty fast. Closing price data doesn’t reflect the current listing reality due to the 1-3 month lag time.

Automated valuations on sites like Zillow and Redfin are already down from April/May peaks just in the past few weeks. I see updated, well priced, well presented homes still going under contract. But sellers of anything less are having to cut prices.

IMO there will be no coasting at flat values. They’re down already, and we’re only getting started.

Yes, from what I’ve read and heard, for every 1% increase in the 30 year mortgage rate, there is a 10% drop in price.

The Fed Funds rate sits around 2.5% and from what I’ve observed, the 30 year mortgage rate historically is about 2% greater than the Fed Funds rate. It peaked between 2009 to 2022 to about 2.75% back in 2018.

The mortgage rate spiked for various reasons such as mortgage demand, etc.

The Federal Reserve likely wants to continue to increase the Fed Funds rate to at least 5% in order to generate enough margin to lower the rate when necessary, without going back to zero interest rate policy (ZIRP) like 2009 to 2016.

I just hope they can pull that off without the economy crashing and I hope the economy cannot sustain itself without ZIRP and quantitative easing. If that is the case, then I have some serious reservations about the quality of the economy.

The real crash starts in November 2022. Been sayin’ it since 2019 and wasn’t sure I believed it myself after the intervention of Covid, but mathematical models predict it based on data going back over 100 years.

Alcoholics get DT, alqeholics get QT

Running off the balance sheet doesn’t sap liquidity unless the government has to go out and issue new debt to replace it. It’s only starting in the last several weeks with publicly held debt increasing and expected to continue for the rest of the year according to Treasury.

The Atlanta Fed released a report mid July implying the effect of the $95 billion/month QT over three years is likely to have an economic impact equivalent somewhere between a 0.25% and 0.50% hit on the ten year yield for the duration of the QT. In other words, assuming 0.35-0.4% on average, closer to chump change than crisis.

I’m not sure how TIPS work. The principal is added to the bond every six months according to an increase in CPI. Suppose the CPI rose to 10% and held constant for the bond’s duration. Then the Principal addition would only occur once.

Investors actually get PAID the inflation compensation when TIPS mature and are paid off by the government. So yes, investors get PAID for the principal and the inflation compensation only once.

But the inflation compensation represents (taxable) income every year. If you own a 10-year TIPS, you have to pay taxes on the inflation compensation every year, though you’re not paid for it until the TIPS mature. In other words, you have to pay taxes on income that you do not get paid until much later. This makes TIPS kind of a complex thing to hold, unless they’re in your tax-deferred account (IRA, etc.).

The Fed shows the increase due to the inflation compensation on its balance sheet. On July 15, an issue of TIPS rolled off. And that’s when the Fed actually got paid for the principal and the inflation compensation for that issue, and both were removed from the assets, as described in the article.