Buy-Now-Pay-Later (BNPL) Lenders Face Tougher Reality.

By Wolf Richter for WOLF STREET.

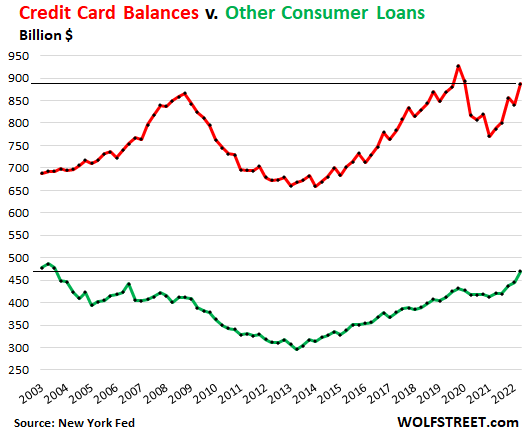

Credit card balances jumped by $46 billion to $887 billion in the second quarter, which was still down by 4.3% from the peak in Q4 2019 and was just a hair above where they had been in 2008, despite 14 years of population growth and inflation. Raging inflation is responsible for much of the increase in Q2, according to the New York Fed’s Household Debt and Credit Report.

Credit card balances also include balances that are paid off at due date the next month, every month, so that no interest accrues. Many Americans use credit cards purely as a payment method (and to collect the 1.5% cash-back or whatever), and not as a borrowing method.

A report from Fitch estimated that the total amount paid with credit cards for goods and services – in the US reached $4.6 trillion in 2021, which would be an average of $1.15 trillion in purchases via credit cards per quarter.

Yet the total credit card balances outstanding in Q2 only grew by $46 billion, which shows to what massive extent credit cards are used as payment method, and to what small extent they’re used as borrowing method, which makes sense, given the usurious interest rates.

The credit card balances of $887 billion in Q2 include transactions incurred roughly in June but paid off in July that are not accruing interest. And this was boosted by the surge in traveling, much of which is paid for with credit cards.

Other consumer loans, such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, all combined, rose to $470 billion in Q2, below where they’d been 20 years ago, despite 20 years of inflation and population growth.

Trying to dodge rip-off usurious interest rates: Dwindling importance of credit card debt.

People are borrowing lots of money to finance home purchases and auto purchases where loan balances have shot higher compared to 2008; and they’re taking out lots of student loans, whose balances have spiked since 2008.

But in order to dodge getting ripped off by usurious interest rates, people are practically restrained when it comes to carrying interest-bearing debt on credit cards – shown by the huge amounts that are getting spent via credit cards, nearly all of which get paid in full every month and never accrue interest: Last year, $4.6 trillion was spent on credit cards, and yet, credit card balances only grew by $40 billion over the same period.

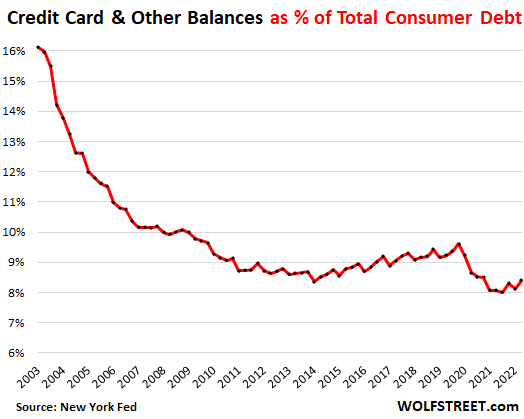

In 2003, credit card balances and other loans combined amounted to over 16% of total consumer debt (including mortgages, auto loans, student loans). During the pandemic, this dropped to the 8% range for the first time and ticked up to 8.4% of total debt in Q2:

A word about Buy Now Pay Later (BNPL)

The New York Fed’s data does not break BNPL loans out. But Fitch estimates that in 2021, $43 billion (with a B) in purchases were made using BNPL loans – compared to $4.6 trillion (with a T) in US credit card purchases. So BNPL loans are minuscule, but growing rapidly.

BNPL loans, which often cater to subprime-rated customers, are short-term installment loans, such as one payment down, three more to go, typically spread over six to eight weeks. These loans are often issued at the point of purchase. They typically carry 0% interest, and are subsidized by the retailer to encourage larger average tickets and fewer cart abandonments. Retailers may partner with a BNPL lender.

If this sounds like the installment plans from decades ago, it’s because that’s what it is, but now imbued with the infallible aura of FinTech and AI.

One of the most hyped specialized BNPL lenders in the US is Affirm Holdings [AFRM], a startup with less than $1 billion in revenue in 2021. It went public in January 2021 amid immense hoopla. In October, its shares hit $176.65 after which they plunged through the IPO price of $49 a share, and today closed at $31.55 a share, down by 82% from the high.

The company has lost oodles of money every quarter, including $55 million in Q1, and $430 million last year.

According to Fitch, the BNPL lenders “have seen delinquency rates more than double over the past few quarters,” while credit card delinquency rates have barely ticked up, as the subprime rated customers that take out BNPL loans are most impacted by the raging inflation.

And as so many times with infallible FinTech and AI, the credit checks are only as good as the folks that wrote the code, and apparently, the code was designed to maximize revenues and not to control risks. Thankfully, this is just a tiny portion of the consumer credit scenario.

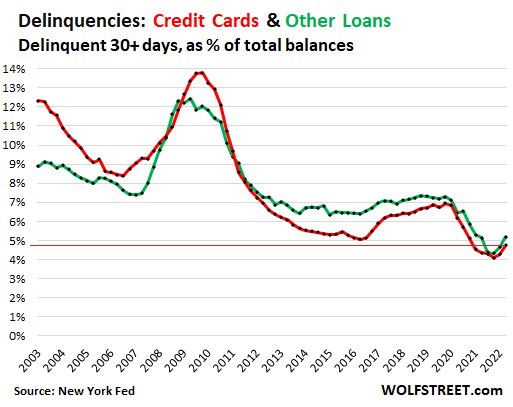

Credit card delinquencies rise from record lows, remain low.

There is still lots of cash floating around, but some people are starting to run low. In 2020 and 2021, people used their stimulus checks and PPP loans, and the extra unemployment benefits plus some of the cash left over from not having to make rent or mortgage payments, to get current on their credit cards. And delinquency rates across the board dropped to record lows. For credit card delinquencies, that record low was in Q3 2021, when balances that were 30 days or more delinquent fell to 4.1% of total credit card balances. Then they started rising.

In Q2, credit card delinquencies of 30+ days rose to 4.8% of total credit card balances, which was still lower than any pre-pandemic low point.

For “other loans,” the 30+ day delinquency rate In Q2 rose to 5.2% of total “other” balances (the record low was in Q4 2021, at 4.3%).

In both categories, delinquency rates are rising but are still below the Good-Times normal. Credit card delinquencies are rising faster and may soon reach the Good-Times normal, and then the not-so-good-times normal. A major employment crisis, such as during the Great Recession, will entail a large increase.

Note how the pandemic stimulus payments of all kinds, and the ability to skip rent and mortgage payments, have pushed down the delinquency rates through mid-2021. But that game is now over, and there’s a trip back to reality. This is a very similar trajectory to auto loan delinquency rates:

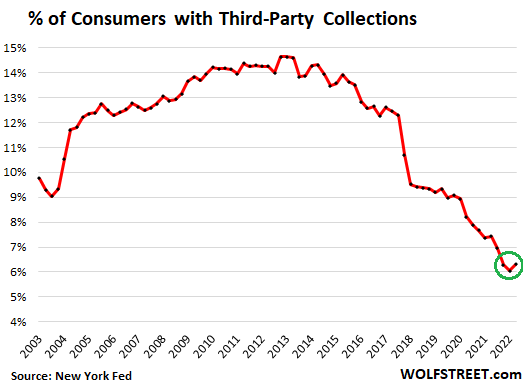

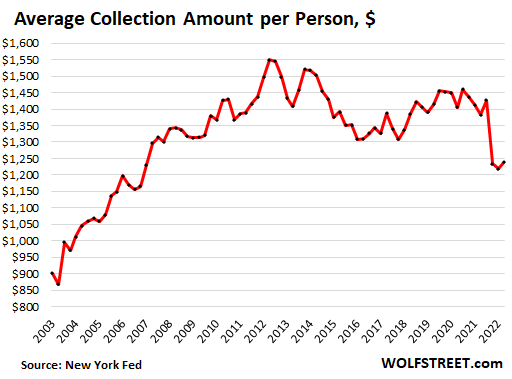

And the first uptick in third-party collections.

The percentage of consumers with third-party collections rose to 6.3% in Q2, less than half of where it had been in 2013 (14.6%). So far, so good:

The average amount of collections per person remained roughly stable at around $1,230 for the past three quarters, after the decline during the stimulus era:

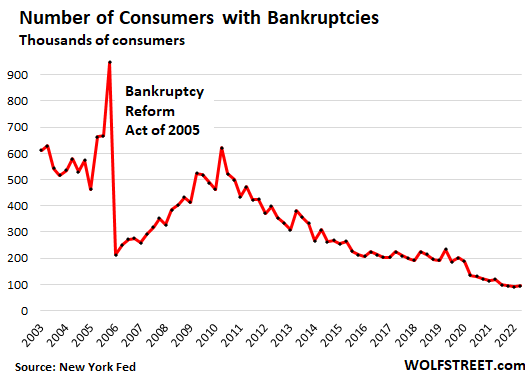

Bankruptcies

The number of consumers with new bankruptcy filings in Q2 ticked up a hair to 95,200 but remains at historic lows, after the long down-trend that started in 2010 when bankruptcies peaked during the Great Recession. Also note that the number of people filing for bankruptcy in Q2 was less than half the number filing in 2006, the low point just ahead of the Great Recession.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The hiatus in student loan payments and interest is probably an even larger factor than the mortgage and rent deferrals during the pandemic because it still ongoing.

Just out from Cox Automotive, owner of Manheim auto auctions:

“Auto Loan Defaults Are Increasing, But We Are Not Heading Into A Repo Crisis”: With annual data on repos

https://www.coxautoinc.com/market-insights/auto-loan-defaults-are-increasing-but-we-are-not-heading-into-a-repo-crisis/

Which confirms my article:

https://wolfstreet.com/2022/08/02/auto-loan-delinquencies-and-repos-are-not-exploding-they-rose-from-record-lows-and-are-still-historically-low/

It’s hard work, being right all the time. I share your pain.

Wolf. I just watched inside job on Netflix – about the cause and actors in the GFC (it’s quite good) and it’s particularly interesting to recap on where we were in terms of financialisation in the economy of the US- and the role it played as it wove itself into the psychology of consumers, borrowers, speculators and their lenders through a low interest environment – with a huge and growing wealth effect. And also how the illusion in society and the financial press, regulators and rating agencies that this huge and fast growing stock of debt was all fine and that there were no deep problems.

I wondered, if we fast forward to now, if feel like everything, house prices, debt, speculation have only grown since then, but we also have inflation and an increasing imbalance between where the wealth is held.

I wondered – is their a useful measure of the shares of financialisation, debt, financial profits and debt payment streams now represent when measured then and now as shares the US economy?

And, I guess, to follow that – do you have a view as to whether these obligations can be met by all the net borrowers in the face of persistent inflation, as remortgages require refinancing,, as assets are sold to meet cash flow requirements and if/when a recession brings job losses into the economy and/or interest rates continue to increase to – say – 5pc.

It’s not cheap to file bankruptcy.

Interesting to see the graphs during the Trump years and compare to other years under other administrations. #themoreyouknow!

It wasn’t intended to be. Nobody should ever file for bankruptcy protection from creditors. Debtors prisons should be enacted in federal law with mandatory prison sentences for debtors who default.

The US Constitution gave Congress the power “to establish… uniform laws on the subject of bankruptcies throughout the United States.” (Article 1, Section 8, Clause 4.)

No.

Shit happens. That hardline stance reflects how you *feel* about deadbeats, not how the business world treats credit or utilizes the credit scoring system.

If I owe the bank $1000, I have a problem. If I owe the bank a million, they have a problem.

Hahaha, don’t take SoCalBeachDude’s comments seriously.

I’ll make a deal with you: We can bring back debtor’s prison if we also bring back (and enforce) laws against usury.

Let me give you an example: Someone I know borrowed $1,100 on a credit card. Made $800 in payments toward the debt. By the time the debt was discharged in a bankruptcy five years later, the creditor claimed that they were owed over $5,000. It wasn’t just the 29.99% “penalty interest rate”, but also the $50/month in fees they loaded into the debt.

If you’re going to use debtor’s prison, you also need to structure debts such that it is possible to repay them if you go through a hard patch and need to catch up. Most current credit card terms make this nearly impossible.

Seems strange that BNPL is not thriving. Traditionally, installment financing was so profitable that it sometimes became the company’s main business. At one point GMAC was most of GM’s profits. Same thing happened with GE’s internal bank.

GM has a new credit card called My GM Rewards Card™ and its rating on Credit Karma is 2 out of 5 with 222 review!!!

It’s happened even in housing. At one point in 2004, we were visiting model homes in the Virginia DC suburbs. We were considering selling our existing home and buying new with cash. The sales rep immediately discouraged that, saying oh no, keep your current home and rent it out. It quickly became clear that the real product he was selling was financing. These beautiful new homes were little more than an inducement to take out a mortgage.

Of course we now know where all that was headed…

1) There is nothing wrong in the charts above. Consumers spending

reached an all time high. Household debt in the last 9 quarters is vertically up, but lately it’s losing it’s thrust. Total household debt, in real terms, deflate. Nothing wrong with that.

2) Population is growing, but the labor force participation rate is trending down. Labor productivity is sharply down. Business capex, down. CEO don’t know what’s coming next.

3) Household spending is up, but the stock market is sharply down.

The stock market casino comprise 36% of US household total assets, the highest in the world. In China, only 11%, because they are smarter. They trust real stuff, they invested in vacant apartments and houses. RE comprise 62% of Chinese household assets. It’s their pension.

4) After bubbles burst they create a glut. Shanghai composite had two. SSEC is “safe & sound”. It osc between two backbones from 2007. It might form an Anti bubble along with RE.

6) U cannot glue a broken mug, after a bar fight.

What about the real estate crisis in China? People are losing everything because they thought real estate is safe.

No they are not. Only a tiny fraction of Chinese real estate is involved in the things you read about in the American media. So far, the government has stepped in protected the homeowners. The latest round of people who are refusing to pay their mortgage because the builder shut down will also be rescued.

“In China, only 11%, because they are smarter.”

Wow. Generalize much? The U.S. Stock/Debt market are indeed a house of cards, nurtured by the Politburo of the Fed.

But China mirrored the fractional reserve/money-conjuring/infinite debt financing of the USA to create their own growth. Neither the U.S. nor China are adequately anchored.

“Smarter” ? A larger pool of gamblers and smokers, I have never seen.

I think the US mix of assets such as stock, bond, real estate is more balanced than most countries.

How so?

P/E ratios are absurd. Interest rates are absurdly low. Capital accumulation is entirely a function of money/credit conjuring.

The U.S. is a sheet of plywood sitting on marbles on a slate floor.

I agree with you that assets appear to be inflated. Iam just saying that assets in USA are roughly equally split between stock, bond and real estate assets. Many nations are over weight real estate market.

None of the power structure’s actions matter – all short-term props targeted to political objectives.

They have no energy transition plan. They cannot wish away the pervasive and damaging impacts of existing energy policies.

We are all eff’d until policy changes. The lament “it coulda been worse” will wring hollow.

Chinese real estate is so so bubliciois and only time would tell if it burst.

Either it hurts and homes become affordable or people come out in the streets.. oh I forgot China has dictatorial regime

China has always had dictatorial regimes trying to control everything, and despite that a long history of big swings from left to right and back again, and huge violent social movements.

The CCP is historically well aware of how explosive their population can get, and their control fetish doesn’t allow much in the way of smaller-scale social pressure relief.

Great stuff. I find it interesting that you leave the reader to draw their own conclusions from the data that you present.

Brian-as it should be (thank you Wolf, as always), but thinking and analysis for oneself even in the best of circumstances can be a truly difficult endeavor for many, very often leading to less-than-thoughtful deference to another’s opinion as to what to conclude…

may we all find a better day.

The upward pressure of inflation might be mitigated a bit by the ‘inflation-adjustment’ checks planned by some states. Of course, that weakens the demand destruction necessary for reduced inflation, but the checks are for political rather than economic purposes.

States don’t print money. If the states are borrowing to write these checks, it still doesn’t affect money supply, at worst it adds to default risk, but that’s on the bondholders, assuming the gov’t doesn’t start bailing out states. The states could either put that money in a bank account or spend it. The latter would have the exact same effect. CO is sending out $750 checks under TABOR, are we against tax refunds now because it “weakens demand destruction”? I agree, TABOR was also done for “political rather than economic purposes” and it really grinds my gears when there’s a hard winter and the state runs out of money for snowplows because they aren’t allowed to have a rainy day fund (or a snowy winter fund). That’s what happens when you let Californians influence your politics.

Some of this may be states using Federal Stimmie money to fund tax cuts?

……or, in other words, just another method of pushing money into the hands of corps and the 1%.

Actually California does have a rainy day fund, one of the highest

The Fed game is has started the demise of traditional banks. When the traditional banks see the light there will be some major league crying.

Banks have made a lot of money because retail customers tend to not be very aggressive about pulling out funds when bank is screwing them over on interest rates. They are getting to be dinosaurs and the cost of having brick and mortar offices is making them uncompetitive.

Not comforting that market fixing banks like JPM/Citi will then hold total control.

Compared to what? Radically insecure, unreliable and rickety DEFI structures? Where is your cash — all in bankruptcy proceedings and absconded with some brilliant crypto scheme, or just radical runs and capital losses? If so, your are touting dreams, like flying cars, so, talking your book. Banks are cumbersome, slow-moving, thoroughly regulated and therefore usefully predictable targets with responsibility. Yes, they get bailed out, meaning WE depositors get bailed out.

I guess the current crop of superficial dreamers haven’t been punished enough by reality yet. Yeah, someday, but the DEFI collapses are everyday, hacks, etc. My credit card works first time, every time, all over the world.

Phleep

Hmmm…..you know… there might be a middle ground between the highly corrupted N.Y. banks and gambling your money away on the Crypto carney.

If it were possible to have a good feeling during the darkest days of the pandemic, that feeling was no debt. For those just a bit prudent, it was a time to shore up the finances and also finding out you can do with a bit less.

I think at this point, most customers of banks with high-interest, high-balance credit cards are those who don’t care and never plan to pay off the card anyway. The banks deserve it with their predatory methods.

Banks are not budging from ultra-low paying savings accounts even now. Let them do business with the backstreet Pay Day Loans and pawn shop customers, it’s their class of people.

All insurance has costs, with no visible rewards except in avoiding losses. Low interest is part of passing on eh costs of this whole thing, deposit insurance, the bailout regimes. These had their downsides but were not without benefits to me.

“Many Americans use credit cards purely as a payment method (and to collect the 1.5% cash-back or whatever), and not as a borrowing method.”

That’s what we do… Costco, Discover and the occasional miles on the American Citi card…. works for me. Glad to be part of the stats!

But what sucks is that retailers (many) add a 2% credit card fee to credit card purchases. Kinda defeats the incentive of the credit card. I try to pay cash at those retail locations.

Yeah that’s what I hear, kind of a zero-sum deal to get people to pay with credit cards or else pay more. As long as you don’t carry a balance, I still think cards are worth it just because they’re faster, you can keep track of what you spent, and you don’t have to touch the keypad like with a debit card.

You also have the safety of fraud protection with credit cards. There have been so many stories of people getting bank accounts cleaned out due to gas pump skimmers that I just assume that they’re all compromised. I wouldn’t dare stick my bank debit card into a gas pump card reader.

I use my credit card for all my purchases but pay it off when due.

Convenience has a fee, yeah. No surprise there. just handling cash eats so much time and attention. That is a “fee” too. And it means the retailer has to pay staff for the aggregate time spent, handling physical cash, etc. , added back into cost of goods and services for everyone.

Visa spent a lot of money on commercials through the years training us on the habit of using cards. Just swipe! Mission accomplished.

Collecting 2-3% on CPI is a hell of a lot of money.

The retailer pays the merchant fee to the credit card company or they pay their staff to deal with cash, or both. The customer will necessarily pay transaction costs in the final price.

If the published price is the same for both forms of payment, one is subsidizing the other to the extent of real cost differential between payment methods.

I only spend eating out money at local fresh seafood restaurants, if offered a significant cash discount I would pay cash. But this is a tourist destination so cards have to work everywhere. Some friends own a local chicken place that’s cash only with a privately owned ATM on the premises. It’s always busy. And anything you buy from fishermen is cash or they just give away, always have a cooler along. I always tip cash regardless, that percentage of the bill function on the receipt is irritating and presumptuous. Why can’t people do math? Tips aren’t anybody’s business except the customer and the server. And are always appropriate unless you’re dealing with the owner. They’re not tracking your tipping habits somewhere with the rest of us and selling that information to someone, no way. There’s some takeout that includes a tip on the keypad for doing nothing but handing you a bag of food? That’s rude.

Like most, I pay off the cards every month. Three percent back on gas adds up with a 3/4ton van and a 36 gallon tank. Never use debit for anything at all. The credit union would give me several bucks to use it each month, for no benefit and considerable risk. It’s around here somewhere.

Illegal for us in Massachusetts. We may offer discounts for cash, but no penalty for credit/debit cards. And yes, the fees we incur are about 4%, in my case. And yes, that is factored into the retail sales price. So…you are paying the 2%! No free lunch, just a question who pays?

“We may offer discounts for cash, but no penalty for credit/debit cards”

That seems contradictory. If you can offer a discount for cash, is that not a lower price than paying with credit? So, paying with credit costs more, you’re being penalized for using credit.

Cookd-but the merchant keeps himself legal vis-state law in offsetting percentage the CC company is charging him for CC systems use…remember, the merchant is getting socked with 4% charge on EACH transaction-NO% loss from one in cash!

may we all find a better day.

Ditto on the payment method use only. No debt, and use the CC for on line payments, and purchases, paid off every month.

The Cox report comments conjure up an image that Captain Smith of the Titanic also must have thought the collision wasn’t showing much real threat……at least for a little while.

Inflation is not hitting fixed debt such as mortgages or car loans as they don’t increase in their monthly outlays. However the energy and food costs have now claimed such large portions of the low to mid incomers, that the squeeze is on for both car and home payments. Literally getting to the point where food is competing with the car for available payment.

Don’t see this getting better with each passing day. Doesn’t matter how “recession” is defined, the budget reality is what it is.

Agreed I let them pay me, not me pay them.

“Delinquencies are rising and may soon reach the good times normal”

Take away the ‘strictly political’ student loan forbearance and we are already there. This party is just getting started.

Another observation…. Interesting to know that the pandemic years the credit cards were paid down because if the free money given out. Seems we are paying for it today with the government report spending that went on and still going today – under our tax payer dollar.

People using a freebie to fix their credit condition seems good, versus spending it on say, partying. I think it speaks well for people, that they thought first of their own responsibilities.

I’m carrying the largest credit balance ever on my cards in my 42 years of cardholding (back in the good old days, when Sears called my MOTHER to ask whether I’d be a good credit risk!) , but only because Amex has given me a 6-month 0% plan. Taking full advantage! The stats will plummet once that 6-months is over ;)

Just be careful. Those are sometimes worded in such a way that if you screw up even once, and in a minor way, interest kicks back in and is retroactive to when you made the charges or balance transfer, NOT from when you screwed up.

Amex, oh boy!. Never, ever, carry any debt you can’t pay off 100% when they hit you with “pay this or else”…. Watch your back friend.

Yeah, what is truly free? NOTHING. There is a risk transfer to the debtor.

“Watch your back friend.”

Yeah, our guvment ain’t. Banks are too big to regulate.

I can picture grinning Jamie Dimon sitting behind a desk at a Payday Loan or pawnshop.

Yes, careful. These things are set up as traps. Read all the small print. To avoid problems, make sure to pay this off well ahead of due date, and pay it off via electronic fund transfer, not by check, because that check might get “lost in the mail,” or whatever, and they will hit you over the head with the interest. This stuff is notorious.

I’ve noticed that mailed checks to one CC are always delayed days, up to a week after other payments mailed same day have been cashed.

IF I carried a big balance on that CC, I wonder what the interest would be on that week or so delay?

That times how many millions of payments delayed?

Get the feeling it is carefully engineered “mail delays” that boost interest on those with outstanding balances.

In the glory days of 16% CDs, one often mailed their CC payment to somewhere off the pavement in North Dakota. Then, some flyboys started twice daily flights from the nearby dirt field airports to SFO with courrier service to the Federal Reserve Bank. Multi millions in interest made on the quick deposit of said checks after the late fees and interest charged because the mail was late.

Yeah, I get balance transfer offers all the time, the going rate right now is 4% which seems low, but I’m sure the real game is to either not get paid off in a year and you swing to the real (usurious) interest rate, or to screw up and get nailed with interest and fees.

You can setup automatic payment with your credit card bank. Every month on the due date they take the balance out of my checking account. No hassle with remembering bills or worrying about checks in the mail.

as I posted before our neighbor a female attorney in 2008 headed up a 32 attorney bankruptcy practice at a major law firm- they did work all over the country but primarily the southeast – by 2015 she was the last one and in 2016 they closed the bankruptcy practice down ( this was corporate work not individual bankruptcy) virtually no business bankrupt anymore too much easy money out there – will that change? ahh that is the question

Wow – that is an astonishing contraction !! Is it possible your daughter’s firm simply allowed BK bases to runoff and not take on new BK cases because they (as a firm) did not want to be in that line of biz anymore?

Commercial bankruptcy filings (all chapters) totally collapsed when QE and interest rate repression took effect on corporate credit. The yield chasers started lending to anything, and they bought bonds of anything, no matter what, and even the junkiest bonds got refinanced, no problem. That’s why there are so many “zombie” companies now out there.

That’s why we need high interest rates and a wave of bankruptcies to restructure this mess and clear it up at investors expense hopefully, and not at taxpayers’ expense.

“at investors expense hopefully, and not at taxpayers’ expense.”

Haha, oh my. Wolfstreet is at the top of my list when it comes to compelling data-driven coverage of financial news. I had no idea I could come here for the comedy too! This site just gets better and better!

The same thing happened to all corporate restructuring and turnaround work. With few exceptions, it just disappeared.

My son’s in-laws also ran a BK practice, same scenario, once a thriving business, then dried up. He left the BJ practice for criminal defense.

Bankruptcy, the result of spending more than you are earning, has been passed from the individual to the collective.

Government is spending your money, your children’s future earnings and whatever your diminishing supply of grandchildren can produce.

Yep,

It’s sad to say, but if you don’t borrow the government is going to borrow on your behalf.

“ According to Fitch, the BNPL lenders “have seen delinquency rates more than double over the past few quarters,”

Doesn’t take long for people to figure out that you’re not going to repo a blender…

in the early 1980’s I borrowed about 20k at about 8 percent to start a silver fox ranch. the fox ranch was a disaster and I soon owed 30k. interest rates rose slightly to 22 percent and it took decades to recover. I paid it all off and currently am debt free, have my bills paid in advance, own my own home and business, and have yet to forget the lessons I learned.

Amen. I started adult life off with debt because even a small wedding costs money and we needed a bed. The credit card became our enemy. We resolved to simply not buy something if we don’t have the cash for it because the debt was a major stress.

There is so much to be said for living below your means and owning your home free and clear, saving for things in advance rather than buying on credit. We’re saving for things 10 and 15 years out like an A/C, roof, car, etc. It’s psychologically liberating.

It’s not popular because “now” and “more”. But boy is it a better life. Kudos to you, motive unclear.

Popular thought was “debt is good” and living on huge debt was the thing to do. Vacations, toys, couples with 8 big screen TVs in a house taking 50% of their income. The house they only sleep in because they dine out mostly, and of course any kids need the best of everything, cars, college to “find themselves” and of course world travel also to “find themselves”..

Who gets all the interest from a life of debt?

Sadly, you need some credit history in order to qualify for things like mortgages, car loans, etc.. Responsible use of a credit card is one of the few ways to do so. That’s how the system is designed.

Years ago, I had my wife get her own credit card in order to establish her personal credit as opposed to having it tied to my record as joint account holder. I encouraged that in the event that something were to happen to me and she was on her own.

Credit is like any other tool. Used responsibly, it won’t hurt you. Wrecklessly? All bets are off.

PS: We’re our own “bank” for lending. Started that back in the 1980’s once we had a nest egg. We’d “lend” ourselves money for a major purchase and then pay the amount back with interest (whatever the prevailing rate was). You’d be amazed at how much you can bank by doing that simple thing. It just takes discipline to make sure you pay yourself first.

Reminds me… credit ratings are funny.

Over two decades ago, when I got married, I gave my wife an American Express card linked to my account. I had opened that account in 1984. So my wife gets this AX card in her name, “Member since 1984.” The card is billed to my account. She’s from Japan and had been in the US for only a couple of years at the time. A year earlier, I urged her to get a US visa card, which she did, and it had a $500 limit, given that she had no credit history in the US. So maybe a year after she got the AX card, we checked her FICO score, and it was over 800, and credit established since 1984. And that’s still the case today…

This AI shit is nuts. But sometimes it does work for you.

FFR has to to 4% before a serious message is transmitted to the Mkts. Of course, Fed doesn’t want to shock the mkt but at the same time, keep jaw boning, how they are determined to contain inflation.

Mkts appear remain in trading range until either the inflation shoots up or the (less probability) rates.

Am I the only one that chuckles (and wonders what the heck is going on in the world) when checking out at Amazon and they want to know if I’d like to make six easy payments of $11.12 for a $64.23 radio. Or if I want to buy $6.27 of insurance for an $89 inkjet printer?

Turtle

Consumption mania fed by the Corporates’ spin, all the time. kool aid dispensed in various outlets and sheeple keep drinking. BNPL

Majority can longer discern between NEED vs WANT. There is ENOUGH for those realize in late in life!

It’s all an intelligence test, starting with the garish packaging on empty-calorie unhealthy foods. It is in layers. Each level of bait captures a certain level of consumer intelligence. The algorithms have us pretty well cataloged too.

You’re onto something, phleep. You’re right – buying a pitifully stupid product, or electing a malignant narcissist, is effectively an intelligence test. JHGAY? = Just How Gullible Are You? You get a score and, if your score is exceptionally low, it’s tattooed on your forehead. Bill Engels might make signs for those folks, too.

And if the tattoo is cruel and unusual and not allowed, then stockades could be employed. They were used for deadbeats during the early colonial period in the 1700s.

Not sure there is any other way to interpret this information that doesn’t suggest a damn healthy consumer. We may be past the inflection point of minimum debt but we’ll need a sustained vertical rise in debt accrual for several quarters to catch up to historical norms. Ending the student loan pause might accelerate this process but in the relative short term I think consumers remain in good shape inflation or not. This is all the lingering effect of dropping atom bombs of cash on American consumers during the pandemic.

“Not sure there is any other way to interpret this information that doesn’t suggest a damn healthy consumer. ”

How ‘healthy’ can The Consumer be with over half a million medical bankruptcies every year? That number would be higher except for those who passed on overpriced medical procedure because they would rather die than leave their family destitute.

Medical Industrial Complex: “Your money or your life. Choose one.”

MIC – not unlike banks: the last place you want to leave your money.

I recall folks in 2006 pulling out credit cards to buy $4 coffees, while the savings rate was below zero. The faith apparently was that the home line of credit ATM was inexhaustible. Consumer balance sheets were super-unhealthy while on the outside, the people looked and talked rich. (That was like a skinny smoker or muscly steroid abuser with systems inwardly already breaking.) It was all headed for the big crash.

Behaviors seem healthier now. That doesn’t mean everybody is just fine, but at least their are not aggressively borrowing themselves into a hole for discretionary stuff. Some few, of course, are, but in a free country, I can’t help it if someone does a self-destructive act with any tool at hand.

I feel for those at the bottom, but they are always one paycheck away from distress. Some (though not all) of it relates to mismanagement of their lives: poor risk management. Catastrophic uninsured losses happen, yeah, every day, everywhere on this planet, for every second of history, from the very start. We can’t afford to insure everyone from consequences. I don’t see how virtue-signalling here has any effect on that.

Excellent article. Thanks.

One probably shouldn’t expect these numbers to turn south until the massive economic overstimulation gets reined in. That’s going to take a while because The Fed is going way easy on the interest rate hikes.

After having botched it with the overstimulation they don’t want to compound their mistake by crashing the economy too soon. That can wait until they’re closer to the ends of their terms and they’re better-prepared to defect to a country where they can live out their humiliation in peaceful anonymity.

Yes, and there will be crying dogs, children, old folks, weeping and gnashing of teeth. There will be righteous pointing fingers of blame, much intellectual hand-wringing about this or that bad guy. I don’t see how any of that will be avoided, absent some deus ex machina that flies down and reverses entropy.

Will your hyperwealthy corporate masters be merciful?

Or is that a bad question?

A “Financial Garden of Earthly Delights” anyone?

Bad news for the “FED is gonna pivot” crowd. Raging inflation continues, unabated, and all of the data point to more of the same. Like some FED talking head said in the past few days “inflation is not coming down,” meaning their actions have so far done nothing. So, more big rate hikes on the way as the American “consumer” spends everything they have and more.

Jobless claims are also up, which supports my conjecture that the ‘labor shortage’ is self-inflicted to a meaningful degree.

It’s estimated The Fed kept interest rates too low every day for over ten years. Does that mean they made 4,000 mistakes or one mistake repeated 4,000 times?

Isn’t all of this just a matter of the American consumer shifting where they keep their debt? Why put it on a credit card when borrowing against a house at a much lower interest rate has been such a bulletproof option throughout the era of QE and ever-ascending house prices? That being said, the rate of climbing CC debt is about the steepest its been in the last couple decades… Only maybe another quarter away from matching the pre-pandemic peak. The CC debt chart could look pretty ugly in another year or two at this rate.

“ Isn’t all of this just a matter of the American consumer shifting where they keep their debt?”

Frequent commenter Augustus Frost opines all the time about how many people are destined to become poorer and poorer…

This kind of stuff illuminates the path and is merely a way station on that journey….

Most of these people are already poor by definition, by not having enough to maintain the lifestyle they desire or feel entitled without increasing debt to maintain it…

So rather than admit they are “poor”, they try to maintain an illusion of “not poor” by kicking the can down the road with unsustainable and expensive debt to keep the illusion alive…

The consumer game, I think, will be over soon…

Lower standard of living, divorce, and bankruptcy on the horizon…

This may be controversial. I don’t believe poor people load up on shitty debt because they are fucking brain dead zombies that can’t do basic math and are mind controlled by commercials.

Instead, poor people load up on shitty debt because they have no reserves and a lack of options. Volatility does the rest. People learn real quick how much double-digit debt sucks in a minimal wage inflation regime.

There are definitely some brain dead zombies. Plenty of people think trying out crack/meth/heroin is a reasonable choice or casino gambling is an excellent pastime. But you can find those type all over the wealth spectrum. There are, after all, “whales.”

Kinda makes you wonder about the all the gutting of usury laws, tightening Chapter 7, and “reforms” focusing on disclosures/consumer education initiatives that do jack shit in the real world.

Don’t forget about negative real wages.

Okay points, Nate, with one exception: they actually “can’t do basic math”. Not all of them. But those that do understand fractions, percentages, interest/dividends are the exceptions.

No evidence; just a retired school teacher’s opinion.

Poor people DO NOT LOAD UP ON DEBT at all. They’re too POOR to qualify for mortgages, and too poor to qualify for credit cards of any size. They can’t even get a decent car loan.

The amount of debt that poor people owe is MINUSCULE.

It’s RICH PEOPLE THAT LOAD UP ON DEBTS because they can get this debt. It’s the subprime-rated dentist that has $2 million in debts (home, cars, practice, credit card debt out the wazoo, etc). The subprime-rated poor person has $2,000 in debt, maybe.

Too wolf how about articles on farmland ,biggest bubble out there

Thank you Wolf for touching on the BNPL space! Your words reflect many of my thoughts. Jees it’s like I read articles just to reinforce what I already think. Sounds dangerous!

1) China RE stalled. RE land sales drained municipalities and localities cash flow. China is dehydrated. People are out of control.

2) If China aggression towards Taiwan & US cont, unemployment will rise both sides.

3) The Chinese gov is so angry, they might impose a severe embargo, hurting themselves, because it’s all about power…

4) Fri data is looking back at the mirror.

5) This bull run might be a crap.

6) PnF indicate that SSEC might breach BB #1 and reach 2,400, taking down SPX with it, in a seat belt position.

> The Chinese gov is so angry, they might impose a severe embargo, hurting themselves, because it’s all about power…

Look at the embargo they are putting on their own people, with zero COVID lockdowns, and refusal to accept a functioning vaccine, out of national pride and xenophobia. They are getting pretty unhinged.

I don’t underestimate snowballing national mania. I think of 1914, 1933 ….

Those ships are sitting targets. The Chinese navy can sink 10,000 feet.

China is so angry the live fire drill will end on Mon instead of Sun.