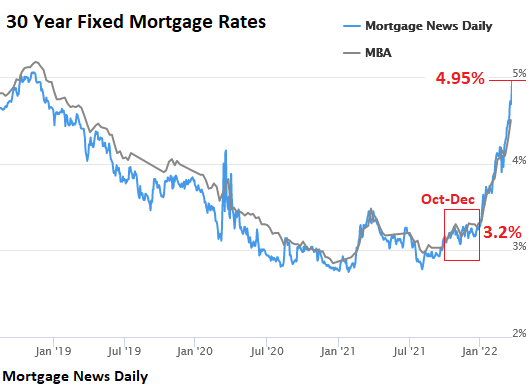

Raging mania to lock in mortgage rates when they were still at 3.2%. But now they’re near 5%.

By Wolf Richter for WOLF STREET.

So now we have a new snapshot of the incredibly spiking home prices, topping out at over 30% year-over-year in Phoenix and Tampa, according to the S&P CoreLogic Case-Shiller Home Price Index today. But these prices predate the Great American Mortgage Rate Spike.

What time span are we talking about?

The “January” home price data released today are a three-month moving average of closed sales that were entered into public records in November, December, and January, reflecting deals and mortgages that were agreed to roughly in October through December, when the average 30-year fixed mortgage rate was around 3.2%. Now, the average 30-year fixed mortgage rate is flirting with 5%, according to Mortgage News Daily, and today’s home price data is still untouched by that spike in mortgage rates:

There was a mad scramble to get the deals done late last year and earlier this year before mortgage rates would rise, and this mad scramble is reflected here.

The overall National Case-Shiller Home Price Index for “January” jumped 1.1% from December and 19.2% year-over-year. The Case-Shiller Home Price Indices were set at 100 for January 2000. This means that the overall index, with an index value of 282 for “January,” shot up by 182% since January 2000, more than four times the rate of CPI inflation.

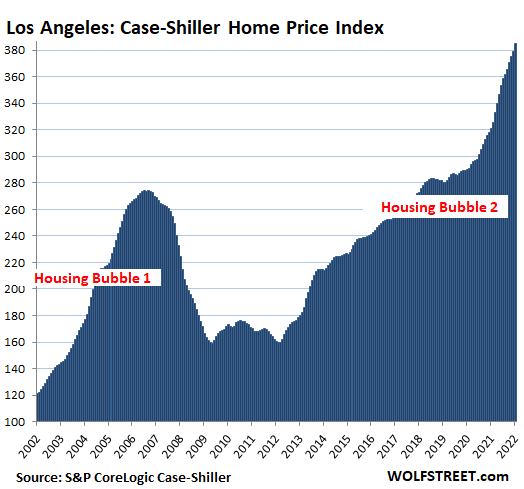

Los Angeles metro: Prices of single-family houses jumped 1.6% in January from December and 19.9% year-over-year. The index value of 385 means that home prices shot by 285% since January 2000, which crowns the Los Angeles metro as the Number 1 most splendid housing bubble on this list.

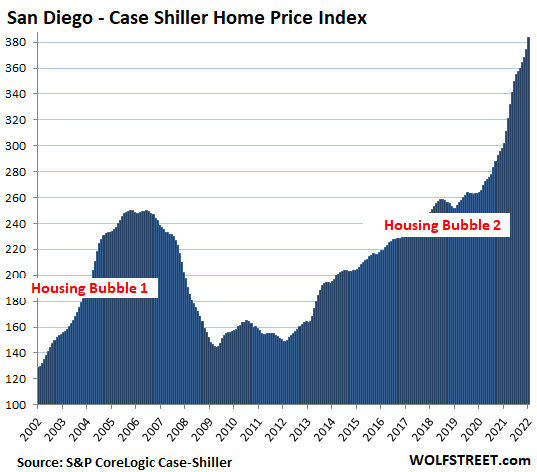

San Diego metro: Prices of single family houses spiked 2.5% for the month, and 27.1% year-over-year. Since 2000, house prices have ballooned by 284%:

This is house price inflation.

The Case-Shiller Index is based on the “sales pairs” method, comparing the sales price of a house when it sells in the current period to the price of the same house when it sold previously. The index includes adjustments for home improvements and the passage of time between sales. By tracking how many dollars it takes to buy the same house over time, the index measures house price inflation.

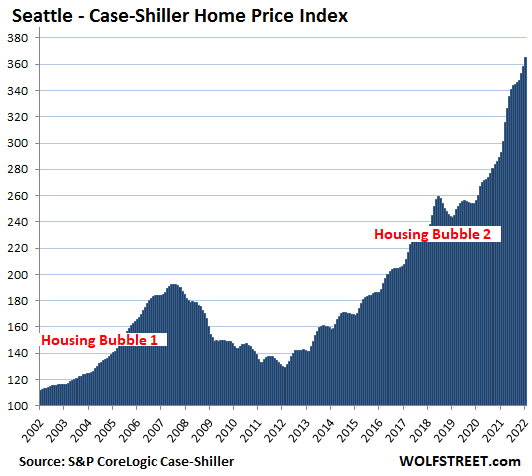

Seattle metro: The Case-Shiller Index spiked 2.0% for the month, and 24.7% year-over-year. Since January 2000, house price inflation in the Seattle metro has ballooned to 265%:

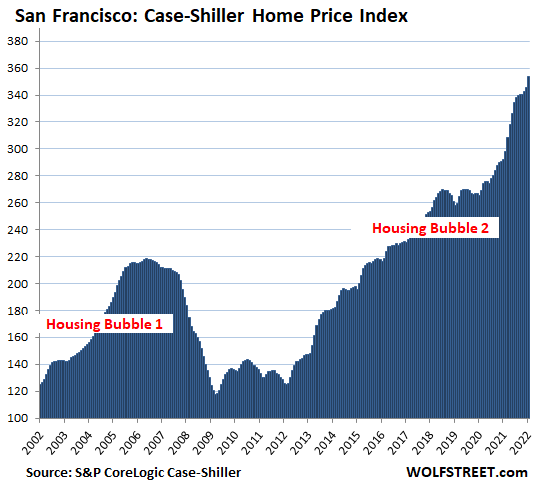

San Francisco Bay Area: House prices spiked 2.4% for the month, and by 20.9% year-over-year:

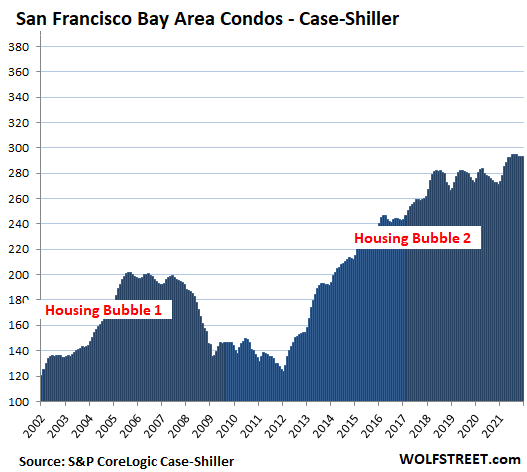

San Francisco Bay Area: Condo prices edged up 0.1% for the month, after having ticked down four months in a row. Since July last year, prices have remained roughly flat. Year-over-year, the index rose 8.3%. Since June 2018, condo prices have risen just 4.0%:

Miami metro: House prices spiked 1.8% for the month, and 28.1% year-over-year, the fastest since February 2006, on the eve of its epic Housing Bust:

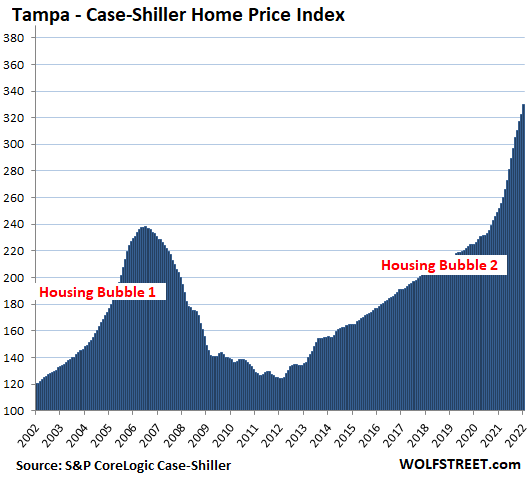

Tampa metro: House prices spiked by 2.3% for the month, and by 30.8% year-over-year, a record spike for the Tampa metro, out-spiking even the crazy spikes on the eve of the housing bust:

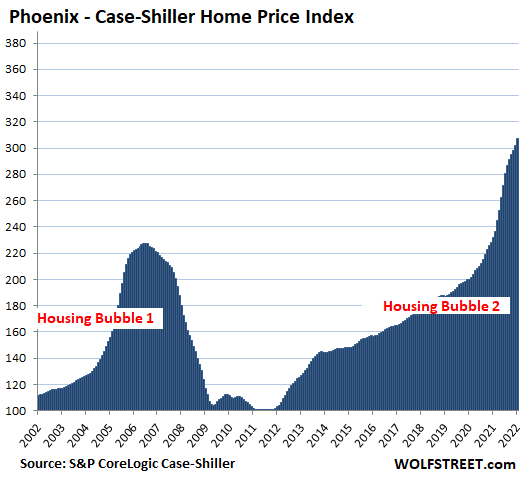

Phoenix metro: House prices spiked by 1.7% for the month, and by a record 32.6% year-over-year, out-spiking the craziness just before the housing bust. The year-over-year price spikes have been over 30% starting last July:

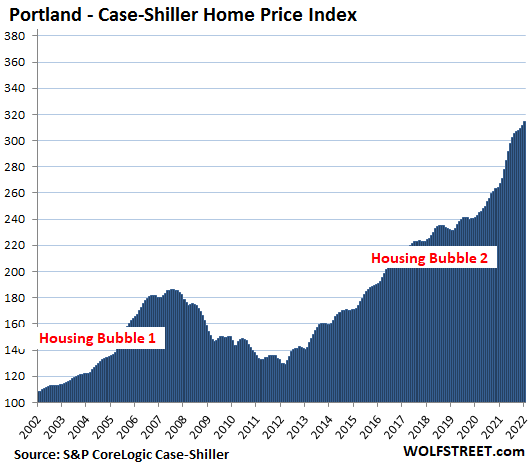

Portland metro: The Case-Shiller Index rose by 0.9% for the month, and 17.7% year-over-year:

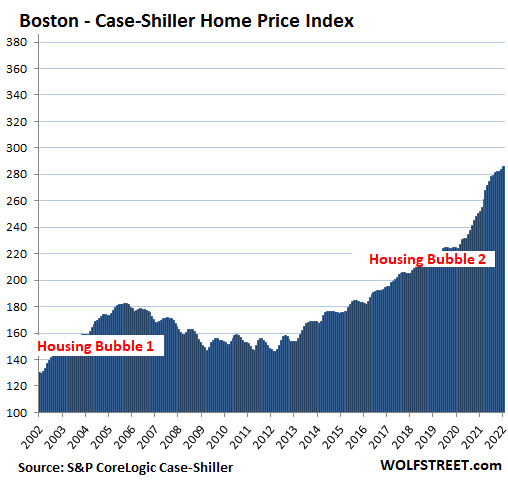

Boston metro: +0.7% for the month, and +13.3% year-over-year:

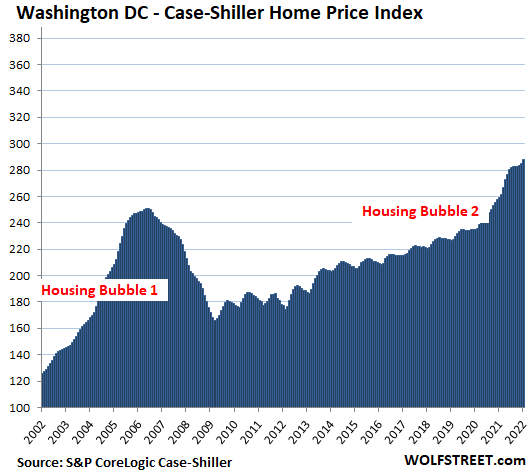

Washington D.C. metro: +1.1% for the month, and +11.2% year-over-year:

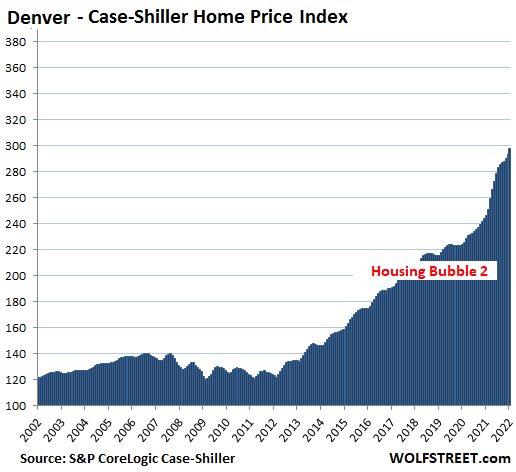

Denver metro: +1.6% for the month, and +20.8% year-over-year:

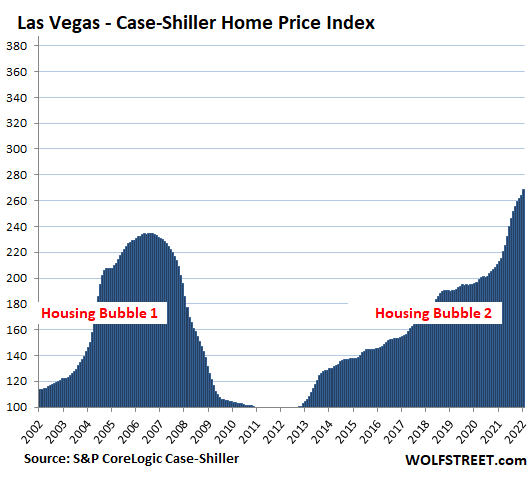

Las Vegas metro: +1.7% for the month, and +26.2% year-over-year:

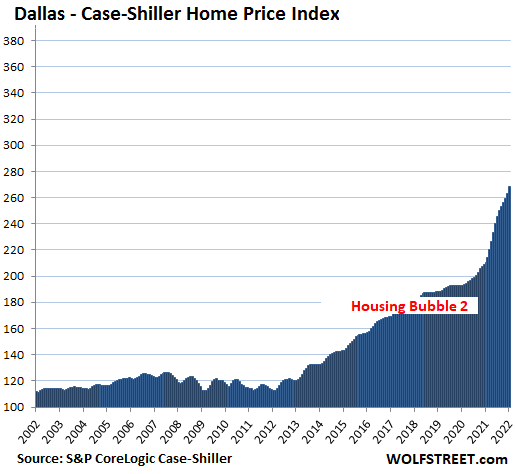

Dallas metro: +1.9% for the month, and a record +27.3% year-over-year:

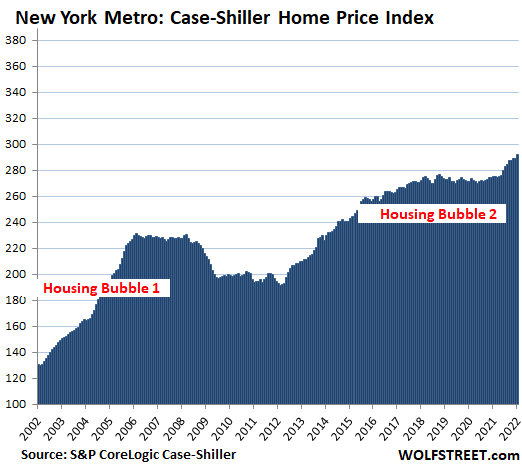

New York metro: +0.9% for the month, and +13.5% year-over-year. At an index value of 258, the metro has experienced 158% house price inflation since 2000.

The remaining metros in the 20-metro Case-Shiller Index – Atlanta, Charlotte, Chicago, Cleveland, Detroit, and Minneapolis – have house price inflation since 2000 of less than 150%, and while some of their price increases are still huge, they don’t qualify for this illustrious list of the most splendid housing bubbles.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The sheer arrogance & stupidity of creating a hyperbubble in property & stocks after 2000 & 2008, then destroying people through lies, manipulation & fraud in a desperate attempt to stop the collapse. The only way this ends is in collapse, whether they like it or not.

80% collapse coming, for both. That’s fair value, even after inflation.

US stocks will end up losing over 90% accounting for inflation when the bear market ends multiple decades from now.

1966-1982 saw a 75% decline adjusted for price changes.

1929-1932 saw an 89% nominal decline.

Valuations were lower or much lower then and the societal fundamentals were much better.

1929-1932 was a deflationnary crisis, leading to a huge nominal decrease

US stocks may lose 90% accounting for inflation, but what is the alternative that will preserve 100% of the buying power of your capital ?

Gold ? Commodities ?

Better have US stocks than cash in the bank

And even better to have a blend of stocks, gold and keep your cash in a currency less likely to depreciate

Hyp,

“US stocks may lose 90% accounting for inflation, but what is the alternative that will preserve 100% of the buying power of your capital”

The way you wrote that, you seem to be saying that it is better to maybe lose 90% of investment (in very overvalued stocks) than it is to lose a dime in savings due to grinding away of inflation.

That seems like a bad, bad tradeoff to me.

Equity collapse comes in an unpredictable blink of the eye – too fast for 95% of shareholders to respond to. And it takes years to crawl out of that blast crater. And the more the overvaluation, the bigger the blast crater.

Anything less than Weimar type inflation, is a much, much slower grinding away, leaving time to think, respond, adapt.

And there is sort of an attitude here, that *anything* is better than likely losing dimes, slowly. Even if it courts ruin.

This attitude seems to me to proceed from an absolute denial that DC has put the other 329 million of us (dollar holders, US citizens branch) in a very, very, very bad box – surely there is some DC “magic” immunizing equity holders, right?

Like in 2008? Or 1999. Or….

DC has created an ugly, ugly situation for savers, in order to save only itself.

There is no magic equity unicorn buried in the pile of its sh*t.

As much as I would love love love to see this and then some, I just can’t imagine what event would cause it to crash in such epic fashion. The almighty FED won’t let that happen and people that survived 08 are even more zealous in their religious belief that housing will never crash. Maybe as a collective effort, these and many others can keep this bubble going for another decade or two.

On the other hand, even at 80% down, it will probably just barely bring it in line to fair value for some of the crap shack in Socal

It’s not hard to figure this out. If a buyer can’t buy, then a seller can’t sell. Buyers won’t be able to buy unless Fed keeps printing. Fed can’t keep printing because of inflation. So, Fed stops printing. Only way buyer can buy is if prices come down. Only reason they ever went up is because of the Fed. The whole mechanism is now reversing.

This should be technically housing bubble three? The duration should extend, there should be a topping process and probably a minor pullback in yields. I sort of imagine lending institutions will try to soften the rate hikes, whatever they do, points, or whatever.

Bernanke called it “courage to act’. The demented Senate allowed this to go on.

Here .. let me do an hedonic adjustment of that statement for you..

I believe that to be: ‘the courage to put on an act!’

There. Isn’t that a more honest assessment of Big Bankster Thievery?

I am not so sure there is a bubble . Taking the base of 100 Jan 2000 and compounding at 8% ( that seems reasonable ) , property should have more than quadrupled in 22 years. Am i missing something?

Phillip Turner,

“Am i missing something?”

yes, everything.

The growth in house prices is a disgrace and based on easy cheap credit making one’s home an “investment” and “ATM” rather than a place to live. Due to labor shortages/material prices increases expect prices to go higher until they “dont”. May we get a reasonable reset soon as this is harming our future generations from whom we borrowed. the FED purchase of MBS was an outright crime not allowing for true “price discovery”. Of course writing this while listening to the “rocket mortgage” commercial telling me how I can get “cash” out of my home since prices are up almost 20% in the last year. FAKE money causing devaluation of “work”. Okay now back to my hard “work” trading crypto and “STONKS” (which always go up)! Haha and peace to all.

that’s the problem with money printing. it ultimately makes work pointless

Moreso *savings* (accumulated product of labor) rather than *current* labor (which at least in theory can try and demand upward adjusted pay).

The distinction matters because I think what is really going on is that DC (via planned/disregarded inflation) is trying to enact a vast reset…hugely diluting the burden of its enormously hopeless debt obligations (which by definition are all its counterparties *savings*) while not completely destroying the productive capacity of the US (since *current* labor can, in theory, adjust itself to any level of inflation).

(But not so much in practice…)

yeah the problem with that is that people were only willing to actually “save” because they had some faith that the government would actually try to preserve its value.

once they lose that trust, it’s very tough, if not impossible, to get it back.

Jake,

Agreed, that is why most people with a knowledge of economic history treat inflation with fear and respect – they know how many currencies and countries it has destroyed.

But the politically tainted Fed has spent 20 years operationalizing a “we are smarter” attitude in the service of ever more degenerate fiscal policies by Congress, the President, the whole of the unelected DC political class, etc.

And so we got endless speeches about the horrors of deflation (otherwise known as consumer savings) and the “magic” of 2%+ inflation and money (not politicians) dropped out of helicopters.

The lenders with the largest market share are above the 4.90% “average” from Mortgage News Daily today:

30 yr Fixed APR Fees and Points

Rocket Mortgage 4.99% 5.024% $1250

Quicken Loans 5.50% 5.535% $1250

Chase 5.125% 5.125% $237

Clearly, house prices are headed lower.

Wolf has given me permission to request an asking price for an authentic Wolfstreet beer mug to help make a market. My current bid is $200, but so far no interest.

HarryHoundstooth at yahoo dot com.

My WS mugs will NEVER,,, repeat Never be available HH,,, and my spouse has direct instructions,,, but that will only last as long as she/we do…

”get over it HH…”

OK, IF you bid $”A” million or so,,, might be able to convince the spouse to sell,,, otherwise NOT likely, in spite of my every day use,,, SO FAR!!

“My current bid is $200, but so far no interest.”

That’s not a bid, that’s an ask.

No, that’s a bid. A bid is the price offered by someone who doesn’t have an asset and wants to buy it. The ask is what someone who has an asset and wishes to sell it, is asking for.

Easy way to remember is that bid is always lower than ask because the buyer always wants a lower price than the seller.

I mean, DUH. I misunderstood Harry’s post as if he was selling his own mug.

Lune, interesting. thanks.

Lune,

Except in today’s housing market, where the ask is always under the bid!

I am seeing 4.625% for a 30-year fixed at Quicken Loans, 4.375 at Rocket, and 4.375% at Chase.

Not sure why your figures are so different. Nevertheless, this fast runup has to put the brakes on this market. They’re only headed higher from here within the next 12 months.

Because you’re looking at rates which include a large amount of discount points: 2pts on Quicken, 2 1/8 on Rocket etc.

They shouldn’t legally be allowed to call them “discount” points. You’re paying up-front for a lower long-term rate; there’s no “discount” involved except in some ancient banker jargon.

“You keep using that word. I do not think it means what you think it means.”

Inconceivable!

Sadly, the finance-media complex has horribly distorted the language in many, many other ways, and none of them to public benefit.

UrsaTaurus,

Thanks for pointing that out. When rates are low the front page has way less discount points. Very shady.

The CU I watch for mortgage rates just today dropped the 30 year fixed from 4.125 to 4.00.

I watched them raise rates over the last few weeks and kind of thought they were frontrunning FED actions and perhaps they did.

everyone did including traders, I doubt TNX holds above 27 if it gets there…

Harry,

Maybe the mugs are priceless?

I got mine

Just in time

For all of your invaluable information, Wolf, your mugs are priceless. Thank you!

I use mine daily. It was well-worth the deflated dollar cost when I invested in it.

Disgrace is the right word. It didn’t have to happen. And you can’t unring a bell either. The digestion or revulsion process out of this may last a decade imo. That much damage has been done.

Points buy down ?

To sc7….

That was it, it appears lenders cranked up the points on the front page offers compared to when rates are low. Then it was half a point or so, now it is 2 or more.

There will be a momentous policy choice to be made … “assignment of losses”.

In 2008 the financial elites were protected at the expense of the middle and lower class, many of whom were “legally robbed” by a broken system. Those crony elites still retain their power. But there is an election ahead.

The amount of times I hear co-workers discuss how their homes have quadrupled in value, or that a friend they know made C$250,000+ flipping homes in Toronto amazes me.

But the CRA will audit a minimum wage retail worker for receiving free lunches from their employer.

Just sold a house near Boston on Jan. 5th this year for 15% over asking. My parents hadn’t upgraded much since 1963. The latest figures from Redfin would price it 22-30% over my asking price of 3 months ago.

“A tendency to go to extremes is often observed at the highs and lows of a protracted market trend. At such times, precedent and overwhelming psychological expectations reinforce prevailing economic factors.”

Homer and Sylla – A History of Interest Rates

True for interest rates, and for home price indexes.

Unfortunately, the extent of extremes is not visible until after the fact…

That’s true except for the “Unfortunately, the extent of extremes is not visible until after the fact” This is extreme it’s flashing red & sirens blaring, only those greedy people taking part are blind & deaf.

Jack X-

I’m not saying the current situation is not extremely concerning and unprecedented (especially systemic debt levels), nor that it doesn’t deserve a significant correction.

My point is that it CAN get more extreme before the shyte hits the fan. You and I won’t recognize the top until we’re looking back at it.

Oh I forgot to mention a house in Beverly Hills probably never lived in, 7 year build advertised for $165 million sold for $51 million, near 70% collapse & probably didn’t cover building costs. 67 Beverly Park Ct, Beverly Hills, CA 90210.

The fish rots from the head.

What have ya got to say about that Wolf? Would be interesting to hear a comment from you.

67 Beverly Park Ct, Beverly Hills, CA 90210 Is in a wildfire burn pit with no escape. That could be one reason it’s so “cheap.”

Hi Wolf,

We are seeing an even larger RETRACTION of would-be home sellers here on the Monterey Peninsula. This is different than the entire county of Monterey, this is coastal California with many second homes. This is the most constricted market I can remember other than Summer 2020 and just about nothing is moving under $2mn for single family homes, forget about under a million right now, and there are many multiple offers. Lots of cash just waiting, truly cash, not portfolio loans cash. Many trades are happening off-MLS with agents acting as matchmakers. The pause button seemed to get hit soon after geopolitical events got super hot over in Ukraine. No idea what is behind all of this other than the possibility that “a confused mind says ‘no’ “. Would-be sellers of primary residences also have nowhere to go unless way out of area. We are an outlier here, not a standard market. This is choice real estate. Our sales numbers are down not due to lack of buyers but rather lack of inventory to sell. The listings that sit and sit are sellers waiting for the market to come to them and it just may soon enough. This is a stuck market here.

Oh my God, hurry up, BUY AAAANNNNYYYYTHIIIIIIIIIIIIING!!!

‘GIVE .E YOUR CASH BECAUSE IT’S WORTHLESS. ALL OF IT! NOW NOW NOW!!’

Watch out for the rugpull.

This post and others like it scream bubble. It is amazing how the psychology becomes so deeply entrenched. Professor Shiller must be fascinated by the situation today.

The two things I can recall more recently said by Robert Shiller…

One was on housing, and he said he could “imagine” prices could be lower in 2-3 years.

The other on the stock market, and he said he didn’t want to be an alarmist but current investor behavior is reminiscent of the 1920s… As far as people knowing the stock market is overvalued but buying anyway

The 1920’s aren’t even close to now. There is no comparison.

There is no precedent for 21st century financial experience.

Yup, he always understates the severity. He has actually sounded bigger alarms on housing. I wish he spoke out more. He’s one of the few economists that actually understands bubbles.

I would agree with you all. But I have been hearing how its “all about to crash any day” (housing, stocks, dollar, bonds) since 2013. It sure is taking a long time! 10 yrs is a long time to hear the chicken littles. And I am saying that being a chicken little myself. Scarred by dotcom and gfc I have been very conservative this run up and watched neighbors and friends scream past me in net worth. This run up NEVER seems to end!

Backroad,

Don’t worry about anyone else. It would be nice to make a bunch of free money riding this mania and get out with it but only a very low percentage will do that. Most either have no clue or else will ride it most or all of the way down after failing to sell at the peak.

As an individual (as opposed to institution), your goal should be to maintain or improve your living standard, not “beat the market” or outperform your peers.

Backroad,

Everything has been driven by the most insane monetary policy in our nation’s history. Been going on since 2008. Things are finally changing, not because inflation has finally arrived, but because now it is everywhere and the Fed can no longer hide behind manipulated metrics. They are trying to let inflation go, and so far they are getting away with that, but the clock is ticking…

“ As an individual (as opposed to institution), your goal should be to maintain or improve your living standard, not “beat the market” or outperform your peers”

Augustus,

This should be printed out and put on the refrigerator…

A gem…

“scream past me in net worth”

Just like those 2007 flipper millionaires, living in their car from 2009 thru 2016.

There are many reasons not to sell, including hassle, loss of low 3% mortgage, need to replace, and avoidance of tax gain.

But there is now a strong reason to sell. Rising interest rates and potentially falling prices. A lot of people think prices can’t fall after they rose 40% on the coasts in two years. Really? Is that a good assumption?

I know of a couple who tried to “Sell High, Buy Low again” during the last bubble.

They saw the bubble and got out with a huge gain.

Timing the market is hard to do in practice. They sold in 2005 before the bubble peak and rented until 2014, after the bottom. They still paid less for a comparable house in 2014 than they sold in 2005 but counting 9 years of rent, I doubt they even broke even. They did get a good rate in 2014 and refi’d a couple of times since.

They would have done much better if they sold in 2006 and re-purchased in 2012. Their Magic 8 Ball was off.

“…but counting 9 years if rent, I doubt they even broke even.”

This must be the most misleading argument in the Buy vs Rent analysis. It’s not as simple as “you’re wasting your money by renting”. With a mortgage, only rouhgly 20-30% of your mortgage payment is principal depending on what you put down, taxes, homeowner’s insurance, PMI, etc.

In your example, the amount of rent, location, what they did with the proceeds, etc. needs to be taken into account as a WHOLE in order to say “I doubt they even broke even” or the opposite “We made a killing!!”.

The principal percentage of a mortgage payment is dictated by the amortization schedule.

Nunya,

You have a good point. If they would have been able to keep the rent payments below their 2005 house payments, they may have made it through with a nice gain. However, they had purchased their house 5 years prior to the run up so their mortgage PI payments were lower than current comparable rent. Due to the 10M+ people losing their homes to foreclosure in 2008-2009, rent did not drop that much during those times.

They had put all of their house gains into stocks and bonds. In retrospect, they lost more when the stock market crashed in 2008. However, stocks recovered quicker than houses so they were able to get back into the housing market by 2014. At a lower cost than theysold in 2005. They have also refi’d since their 2014 purchase so I don’t think they will try to time the market again.

I just rode the roller coaster with both the house and stocks.

I had a relatively cheap place to live compared to renting and just mentally pushed out my retirement when my 401K dropped 30%.

I think I came out better in this situation.

The thought of cashing out now on my house is a consideration, but with rents much higher than my mortgage payment, I think that would not be a good financial move.

However, if I owned a second home or rental properties that I did not live in, I think I would seriously consider cashing out now at a “peak”. But what would I do with those gains in this everything bubble? Not stocks. Maybe bonds in a year or so.

I’d probably just suck it up and hold cash and lose 7% per year from inflation.

I bought in 2004 for $96k and sold a well taken care of, updated home in 2015 for $85k. Paid $400 at closing to get out.

First of all, man do I miss Michigan home prices…

Secondly, we essentially paid rent all those years except we replaced a furnace, and remodeled a few rooms including a kitchen. $$

If they put the extracted equity into stocks, they made a killing.

They did put their gains in the stock market in 2005 and lost 30%-50% in 2008. They jumped from one bubble to another bubble.

By 2014, they recovered enough stock equity to get back into the housing market below when they sold.

These prices might be stickier than you think. Still lots of buyers, inventory is low and new construction is cost prohibitive (even if you *could* get windows, doors or appliances).

Needed a new our microwave went too 3 stores 1 st had only expensive ones 2 ne was 80% out of stock 3 rd Best Buy had he I was looking for on sale 251$

I doubt there are lots of buyers at a 5% mortgage interest rate. Next month, we’ll see that home affordability has declined dramatically.

I not too sure about that, Bobber…

$400k at 3.5 vs 5 % is only about $350 per month P&I…

I don’t think that’s enough to roll it over yet… you?

Hal, I think you are right, I do not see prices falling much. Just not enough inventory. Too difficult to add more inventory.

And I say this as a renter hoping to buy at lower prices. I sold 3 rentals in CA in 2014, 2015 and 2020 (that I bought at the bottom in 2011 very cheap) – I’m shocked at how much higher they all are in 2022. I should have done a 1031X on one of those sales and then moved in a few years later after renting. Now I fear I’m priced out forever in any decent area (for what I want to pay….I’m cheap).

Regrettably I agree. I look at houses in the east Bay Area and Sacramento and they are currently becoming more scarce and more expensive. If inventory remains low until wages catch up, then it wasn’t a bubble after all. It was just wanton destruction of the dollar and the economic standing of some group of Americans.

I wonder if “e pluribus unum” will be sarcastically encoded somewhere in the Fed’s new digital dollar.

Y’all are assuming there will continue to be an ability to buy. There won’t be. Nothing else matters. If buyers can’t buy, sellers can’t sell. The monetary insanity is finally ending, albeit slowly. If the Fed changes course, everything will collapse due to hyperinflation, so i think they will finally be forced to end the insanity after 14 effing years.

plus 30% of stock is institutional now

cd, back in ’29, “institutional” investors held 90%. Retail investors held only about 10% of the stocks. By the depth of the melt-down, July ’32, about 30% of all Americans had lost virtually everything they owned.

I should’ve added: 40% of all Americans, today, own nothing.

Live in Tucson AZ. I would love to sell and take a profit and move to another part of town closer to work but right now there is nowhere to go. The inventory is at a record low. There is a massive affordable housing crisis like we’ve never seen here. People can’t find places to rent. We’ve been trying to upgrade our windows and we were told there are literally no more aluminum windows available. None. They stopped taking orders for them. Period. Vinyl yes, but vinyl sucks in the desert of AZ.

Agree. I used to think rates would flip this script, however all cash buyers and Airbnb/short term rentals are screwing normal people.

Big brother needs to tax ALL of the incentive out of these rentals and give the SFH back to working people.

It is tempting to sell now with a huge gain with an expectation that housing prices will fall shortly, but my wife won’t live in a tent to save money for the next 6-9 years so the gains would be wiped out by rent.

I don’t even think I could convince her to buy a post-pandemic cheap used RV and take 6-9 years to tour the country.

Yeah, it’s a known fact that women get spoiled pretty easily.

Mate, in Toronto, if you don’t own an entire condo tower, many Tinder prospects wouldn’t even want to be near you.

I would think there are an awful of of homeowners [boomers?] who will not need to sell even if house values drop 30%.

They can just ride it out. No need to move; enjoy the lower property taxes. Enjoy your house being paid off or your 30yr 3% mortgage.

Also, there has to be some point where the FED will just crank up the money printing machines to bailout the homeowners and banks.

I could be wrong but I just don’t see the big big drop the alarmists keep predicting. I wold bet that home prices in most areas will higher in ten years, even if it is small and it’s all just inflation.

We will see.

Enlightened,

That is exactly what I am going to do. Ride it out and enjoy my forever house.

That is what I did in 2008 and my forever house was underwater for awhile.

It may be underwater again in the next few years but eventually it will be paid off and will never be underwater again. At least I hope we don’t get to the point of having to pay someone to take my house.

Lower Property Taxes???!!! You must be joking!

Property value goes up, assessment goes up, taxes go up.

Property values goes down, assessment goes down (only for sales or if you contest valuation), Tax RATES go up, taxes go up.

The local government WILL get their money from you.

Kenn,

Unless you are lucky enough to live in CA where property tax increases are capped at 2% no matter how high appraisals or inflation. This is from Prop 13.

Grandma is safe paying her 2K/year property taxes after buying her 3 bedroom tract house in the 1970’s for 50K. True story for my mom and all of her friends who will leave their houses when they finally drive off into the great CA sunset in their Teslas. It just makes financial sense for them.

or FL, where the cap is 3% per constitutional amendment by the same person who worked a few years later to get it done in CA

God Bless him, eh?

And FL has a lot of municipalities that also reduce their ”fees” etc., for folks that are elderly, veterans, etc.

It is definitely ONE of the reasons folks move to FL,,, but ”tech” has found the positive environment for biz development good there too, in spite of the long long hot hot and hotter summer that starts in March and goes until November now a days.

Patience is a virtue…

There is no better proof than these charts that Jerome Powell and the entire FED board should be fired. These ass clowns have turned housing and the entire economy into a speculative casino. They were not only derelict in their duties, they were profiting off of their insane policies which have perhaps mortally wounded the country, and hurt the most vulnerable.

While admittedly unscientific the Zillow estimate on my house in SW FL :

Jan 2020 – $256 k

Today – $454 k

Pretty good place to live but it ain’t that special…

Value of 256k in 2020 dollars – 256k

Value of 454k in 2020 dollars – 256k

Join the club

Ouch, that hurt!

Hi Wolf,

I have been curious for a while now about the adjustments in the Case Schiller index. Do you know how the adjustments for home improvements are made? Is it proprietary?

This seems like it would require research into each individual home with a sales pair. Is the number of sales pairs in each period small enough that manual investigation and adjustment possible?

Thanks for the great work

It’s sales pairs so no adjustments are made like you’re talking about.

Imagine a house was purchased in December of ‘20 for $300k, then sold in December of ‘21 for $400k representating a 33% increase. That’s how this metric is established.

To put 20% down would increase from $60k to $80k and the payment would go from $1.3k to $1.7k. However what’s happened now using the same figures but shifting back to March to March the payment would go from $1.3k to $2k over a year due to interest rates rising. So a 50%+ increase in payment cost in one year. This is why you get young folks who might’ve just barely been able to afford a starter home a year ago are pissed.

I’ll check back in for the “f you I got mine stop crying crowd” comments.

> I’ll check back in for the “f you I got mine stop crying crowd” comments.

Not “f you,” but I bought mine and paid for it steadily through 27 years of all kinds of conditions, ups and downs. I took the very real risks that it wouldn’t pan out. I took extended “losses” in value for a long time post-2008. Now in perfect fairness and economic logic, I risked the full downside with real skin in the game, so now I get to keep the upside. I settled my divorce and cashed out the exiting wife, etc. For the moment, a transitory moment maybe, it seems way up. These moments come and go, if you’ve lived awhile. But all I want is my house.

So now I’m a bad guy? I owe somebody housing? I should join anyone not in the same situation in, myself, weeping? That is what, to my ears, you imply here. I was 37 when I bought my house. I rented before that. Worked every minute of the time I’m talking about. How old are you?

Oh c’mon phleep. You’re too old to still be living indoors! Give that house to some youngsters ;-)

I have no problem with anybody buying houses at any price to live in. What I have a problem with is speculators trading houses like stocks, running up the prices with no intention of living in them or renting them out for fair market value, and smug old “homeowners” gloating over their situation – posting the details here while virtue signaling – because they had the dumb luck to buy before the FED decided to destroy the young, the working class and the poor in the name of selfish, criminal greed.

There are these attractive human attributes called “class and decorum” where you just know not to rub things in the face of the underprivileged people who were not the beneficiaries of said policies, but instead are crumbling under the weight of a system so disgustingly twisted and perverted that it’s led to a record wealth gap which shows no signs of abating, and a homelessness epidemic that is truly jaw-dropping. Enjoy your house but STFU about it already. I think we’ve heard enough. Don’t you have some yard work or something to do?

DC.. you talking to me?

hal, no, I think he’s talking to people like phleep and cowg.

I missed the part where I said people who live in their home should give them to young people?

Is anyone my age mad at people like you? Nope. We would however like a fighting chance that doesn’t include playing at the high stakes table with every chip we have against groups who essentially own the casino. I thinks that’s a fair ask, why people you’re age can’t see that is quite sad. What’s even stranger is that “fight” is against those rigging the game, not you. So why are you so defensive?

But the cherry on top of your comment was still the fact that at its core it was “f you I got mine” how’s that for irony?

I’m 31 and work two jobs teaching coding as well as my day job in a Fortune 500 finance dept. Not sure how that should change your opinion of me.

Here is the methodology. It explains it all:

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

I don’t know if you’ve covered this related topic before but here is my question. In the Phoenix area we are deluged with TV ads from home buying outfits like ’72Sold’. What do they do with the homes that they buy?

These ads are still going strong despite the rise in mortgage rates. What’s going on?

They don’t buy the houses, they are a discount real estate broker.

It’s crazy how the manipulated growth in home equity can mess with your head. That wealth effect really makes you wander off into the abyss. My “never forget” moment was buying a home early 2007. It took a decade to dig out of and maybe the positive is I learned that lesson early in my life. I think many are underestimating how much effect this current wave of inflation is going to have. It seems many don’t understand what it really is.

they seem confident that the fed will never get inflation under control until we have a crack up boom. maybe they’re right.

Asset prices continue to shoot the moon because the FED told the world that they will not take inflation seriously. They announced that they will end the year with a Fed Funds Rate under 2%, which is still 6% under the current inflation.

What a responsible FED would have done is raised by 2% last meeting, and signaled rate hikes of 100 basis points at every meeting to catch up to inflation by early to mid next year. Instead, they told everybody to keep gambling because they would continue to throw gasoline on asset prices and debase the currency.

Bingo.

> keep gambling because they would continue to throw gasoline on asset prices …

They are still at it! Interest rates, mortgages included, are still in real terms below zero, below inflation generally.

But I worry for the youths if they lock in a high house price plus higher interest, fed hikes bite, and we get recession. Hard to refi without much equity and a job? That is not a pretty outlook either. Too little, too late, and now risks abound to all sides. So I hope the soft landing can happen. Yeah, sure.

Debasement of the currency is a Capital Offense.

For phleep. Hard to refi without equity or a job. Pretty hard to make current payments without a job. Refi? Good luck with that.

A responsible FED would never have dug this hole in the first place.

Why are you expecting the guy who dug the hole to go and fix it?

“Why are you expecting the guy who dug the hole to go and fix it?”

I’m not. I have been saying that the FED won’t do what it should the whole time, and calling for Jerome Powell to be shitcanned.

Someone on Reddit told me today the government was designed to prevent recessions.

I guess if you’re younger I could see how you’d have that belief. They’ve certainly behaved that way in the recent past. But they’re not omniscient or omnipotent and if inflation is thrown in the mix there’s only so much they can do.

“Someone on Reddit told me today the government was designed to prevent recessions.”

Sigh. What a shift a generation makes.

I remember an era of Constitutionalists. Those proving the FCC, FBI, and ATF didn’t have jurisdiction to go anywhere they wanted.

That the IRS Codes weren’t law which meant they applied as much as my made-up policy affects you. That war was a horrible and oppressive act. A population that would never accept a government handout.

Now government pays us and we defend anything it does.

Am I the only who believes we’re already deep into our crack up boom? The Fed creating trillions of dollars, insane asset valuations, endless WTF charts. Do we have to have hyperinflation at street level before you recognize it for what it is?

Doesn’t it depend on what type of inflation they are fighting?

The Fed raises rates 0.25% and mortgage rates jump up 2.0% from 3.0% to 5.0%?

Mission accomplished for housing.

I’ve got my popcorn to see how all this turns out for the rest.

Yup I like to watch this : Its like a Crime TV Series

Phoenix metro: House prices spiked by 1.7% for the month, and by a record 32.6% year-over-year Wow that’s Huge and Las Vegas

grab my Eye as they are the leaders in the western USA

to watch I think ” talking Bubble Burst ”

Just how far the FED Go ,Be allowed to go to continue to stagnate the overall economy by Inflating to value of everything resulting in Devaluing the Dollar leading toward the demise of economy overall ?

Huge Company’s some adding 800 Homes per month to use as rental property’s at Huge rental amounts now making it very costly and difficult to buy a home and creating a rental market rather like it or not .

So ? are these huge RE investment company’s also going to join Masses should the economy crash with foreclosure’s and bankruptcy’s joining the Stock market correction joining the Fed’s agenda resulting by their actions .

Will the Lenders be bailed out by more money printing again lessening

the Dollar Value ? and just how Low can the Dollar go perhaps to a Negative Dollar ? is that possible ? A dozen Eggs for say $50 Negative Dollars and Gas at $275.00 NEG a Gallon .

I am sure the Fed knows what they are doing look at all the money they are making ( for themselves )

Things are great in America immigrate the War torn right away since we don’t want to help them lets join them

The Federal Reserve annual rebates 94% of its profits to the US Treasury for the benefit of US taxpayers and citizens and has always done so throughout its entire 109 year history and is the only US government agency that actually turns a profit to benefit the US Treasury.

it’s easy to turn a profit when you can print money.

Do you actually think the Fed is the direct beneficiary of its’ shenanigans?

Mostly correct. The Federal Reserve keeps 6% interest for all of its work in taking over the Congress’ exclusive constitutional duty to print money. 94% goes to the US Treasury. However, the Fed is not a US government agency – I’m just baffled that you are unaware of that while reading the info that you are aware of

Hello everyone,

I’m sitting in the airport in Quito, Ecuador waiting for a flight to Houston,TX that leaves in 12 hours.

I’ve considered offering a historical perspective on S.F. Bay area real estate prices as I had lived there in the mid ’60s and again in the mid 70s. Today is our lucky day.

I went to high school in Pleasanton, CA from 1967 to 1971. In March 1968 my parents bought a home in Pleasanton Valley and paid $25k for it. Three years later my father was transferred back to Philadelphia, PA and the house was put on the market. The buyer paid $33k for our house but shortly after he made his offer, he was informed by his company that he was being transferred to Houston, TX instead of San Francisco. He told our R. E. agent to relist the house.

In mid June, just after I had graduated high school, there was a double closing at our dining room table. The second buyer paid $35k which covered all closing costs for our buyer. A fight ensued over the andirons and wood rack in our working fireplace. Both wanted those items.

Two years later, the sewer and water systems reached capacity and the town fathers put a building moratorium in place. Prices shot up to $50k for those houses.

In 1972, 3, 4 and ’75 prices of similar tract homes in Walnut Creek and Concord, CA -just to the north of Pleasanton – were rising by 2% per month. The homes that people had purchased in the ’60s for $20k were now selling for $40k. These people began borrowing against their equity to purchase “investment property” (or should I say “properties.”

By January of 1976, when I moved back to the Bay Area, those homes were now selling for $80k. A married man I worked with in San Francisco had bought one of those homes at $80k. Then, suddenly, 300 empty houses came on the market all at once.

The “investors” had not rented out the homes because they were afraid of what a renter might do to the property. Therefore there was no ready market of renters who might have become the buyers. As potential buyers were shown empty home after empty home the offers they made fell quickly. The couple I knew that had bought at the top of the market got divorced about a year to 18 months later…..And they sold their home for….. $40k.

You’ve got to know when to hold ’em

Know when to fold ’em

Know when to walk away

And know when to run

You never count your money

When you’re sittin’ at the “kitchen” table

There’ll be time enough for countin’

When the dealin’s done

Everything returns to the inflation mean eventually. In 2008, “Game Over” happened fast. In the late 1970’s and 1980’s , it was a slow playing game with the odds in favor of the house.

I wonder how much it is worth now ;)

If you think these are all bubbles…take a look at the greater Nashville area. Yikes!!

It’s hard to see the whole area while gridlocked dead still on I-65.

The morons otherwise known as the FOMC actually allowed the yield curve to invert today……..even a monkey knows that they should have been selling enough securities to ensure that the long rates go higher so the inversion was put off.

They are truly a pack of morons……but……maybe I’am being hard on morons.

Anything to keep the robbery going. In a replacement to “In God We Trust……the current fed should be printing……As God we steal.

The FOMC has no control whatsoever over the yields of US Treasuries.

Hahahahaha nieve

This is sarcasm, right? Or do you not understand their balance sheet?

SoCalBeachDude,

Are you being sarcastic? I can’t tell. Just in case you’re serious…

The FOMC locks down the front end of the yield curve — the short-term yields — with its policy rates, including federal funds, repo, reverse repo, and primary credit. And it’s $9 trillion pile of Treasuries and MBS weighs down the longer end of the curve. And the middle has a little bitty room to move. There is no free Treasury market. If there were, the 10-year yield would be 10% (above the rate of inflation).

I cannot believe that there are still people out there who preach that the Fed doesn’t control yields, when that’s all the Fed does and explicitly says it does it!!!

I don’t want to argue, but it’s my opinion the Fed is constrained in what they can do on the long end of the curve by economic reality. Economic reality is long term rates can only be so high before we are in severe recession. Fed knows it and market knows it and places their bets.

I am hardly a defender of the Fed, but here’s what I think is happening.

The Fed controls the short end of the yield curve with the Fed Funds Rate, and they control the long end of the yield curve with QE (buying long-dated bonds).

I’m thinking one of the reasons why they only raised the FFR by 0.25% this month was because they hadn’t planned on starting QT until later in the year. To raise the short term rates drastically while not starting QT to raise long term rates would cause a yield inversion. As it is, we’re seeing a mild yield inversion even with just the 0.25% increase. They’re not going to be able to raise interest rates much more until QT starts to kick in and the tail end of the yield curve starts to rise.

Why didn’t they start QT this month? Because one of the hallmarks of every Fed since Bernanke is that they want to telegraph their moves long in advance, so that everyone in the market can prepare for it and it doesn’t lead to sudden panics. Especially something like QT, which will start dumping hundreds of billions of dollars of bonds into the market, is not something you want to surprise people with.

As it is, they moved up the timetable for QT, to May. And I think they’re hoping that that’s enough to get long-term rates to start rising. The quicker they rise, the more leeway they have to raise short-term rates. The mortgage market is already moving fast, but that hasn’t caught up with the treasury market, probably due to flight-to-quality from the Ukraine war. But either way, it seems the Fed will be hamstrung on raising short term rates until QT starts raising long-term rates in earnest.

I do give leeway to the Fed that managing the yield curve is a tricky business. Of course, they shouldn’t be in it in the first place, but now that they are, managing it is tricky. That’s also why they have such a massive reverse repo facility, to drain liquidity on a daily basis as needed to calibrate the yield curve more quickly and finely than big QE/QT programs.

The dollar-denominated bond market is a big ship to turn around. They should have started at least a year ago if not earlier. They’re way behind the eight ball. But that doesn’t mean they can automatically catch up quickly without causing equally disastrous effects to the economy and the market.

if they shouldn’t have “surprised” the market by dumping hundreds of billions onto the market without warning, they shouldn’t have “surprised” the market by buying hundreds of billions without warning either.

what’s good for the goose is good for the gander.

Right on the mark, Lune, IMO.

We are where we are because the public has not yet become incensed enough to allow for the politics of canceling the Federal Reserve System and its failed purpose (stabilizing the economy) and/or its confusing and conflicting mandates.

Until that happens, we have to live with the existing institution, and the fact that it, the banking system, and the bond markets move in slow motion.

As Wolf has described, the inflation in real estate and commodities has caused a major shift in Fed-talk and Fed-think (we hope), and they are belatedly going through the motions used to telegraph what’s coming.

Probably not enough, but they are moving, and might even accelerate by summer, as they’ve accelerated since December.

I love your closing lines:

“ They’re way behind the eight ball. But that doesn’t mean they can automatically catch up quickly without causing equally disastrous effects to the economy and the market.”

Southwest Florida has them all beat, again. It was the epicenter of the last bubble and it’s even crazier this time thanks to Covid and DeSantis.

In Cape Coral, Fort Myers, Estero, Bonita Springs, Naples, many neighborhoods have nearly doubled in price since 2018 with much of the ridiculous run up coming in the past 2 years. It’s total madness. One house sells, the one just like it next door goes up 10-20% immediately, sells, rinse and repeat. Houses that comped for $250k 1-2 years ago are now selling for closer to $500k and people are practically fighting for them. I bought one in 2005 for $495,000 and sold it in 2015 for $277,000. But they all say it’s different this time. It’s different alright, it’s worse.

There are thousands of vacant lots for sale in the region of Lehigh Acres, Cape Coral, Port Charlotte and North Port. The area was subdivided decades ago and the lots were sold as investments. They are visible in the satellite photo map in the Google Earth app.

I bought a .28 acre lot with water, sewer and electric last year. It is across from a 2800 sq ft house on a half acre lot. The streets there are half empty. I bought another one in a low income area with water and electric for about $16,000. One on the same street sold for about $21,000 recently. I avoided flood zones and areas where there are no houses or electric lines nearby. Prices are so high I do not want to buy any more lots. There are tens of thousands of empty lots with street frontage. Hospitals are the main private employers in my county.

Two years ago, in my subdivision ( south Charlotte county), there were 1500 lots with 500 homes…

Lots were 8-9k…

Current estimate is the subdivision will be built out within 2 years…

Lots are now 50-60k….

Kinda sucks for me cause I am certainly not a people person… :)

Those lots you’re talking about have gone from $5,000 to $50,000 and back to $5,000. Nobody “wants” to live in Lehigh (or Cape Coral for that matter) but it’s the only place that working people can afford to live (barely). It’s not different this time, the crash will be epic.

Those DINK couples from the north were browsing Cape Coral listings and offering over US$100,000 over asking from their laptops. I saw everything from the person seated at my eye level in that plane. It was 2018.

Many seasonal people who have rented previously are buying to-be-built for next year…. Trying to lock in the prices now…

I guess if they decide they don’t want it, they can sell it for profit…

The medium family income in 2005 was $45k and now it is $75k. 66% increase.

Adjusted for inflation in todays dollars, the $45k in 2005 is the same as $68k now.

Thus we should expect some housing appreciation. At least 66% from 2005 prices.

What inflation rate did you used?

I pulled this from a graph on Doug Shorts site where he shows real and nominal income. I am guessing he uses the CPI.

Several very large corporations are buying up houses and renting them out.

Yes, if you want to buy my beaurtiful asset, you will need to pay moar and moar. (Snidely Whiplash laugh).

I am reluctant to trade away land for a (rapidly growing) pile of depreciating paper. And then what, throw it all away on stuff costing ever-more? So yeah, “moar” actually makes perfect sense.

Some extremely intelligent young relatives have just returned to Seattle after visiting us over here.

No worries at all! Their house will continue to rise in value because – “Don’t you know! It’s doubled in value since we bought it five years ago, so, in another five years it will double again.”

I’m sure they’re far smarter than me but I’d take the money and run.

The joy of inductive logic. The Sun has always appeared in the morning so it always will.

Then the Black Swan appears.

Except that NOW, depending on the geopolitics of the moment, we could witness several cans of mourning sunshine materialize all at once..

Mortgages, let alone rates .. would then vaporize to nothingness!

NOT true MG!

While it IS true that the sun ”rises” ,,, it does NOT always appear, especially as one goes north or to the fog zones.

Surely, some friends from Wish A Gin have told me they sometimes don’t see the sun for MONTHS on end, and that is well known re arctic etc.

Suggest you try another analogy, eh

The cynics say: housing prices didn’t go up, but the dollar lost value by that much.

I love to tell people that. It’s literally a measure of inflation. Your house didn’t get better; it’s probably more run down than ever. Your money sure buys less than ever.

Not cynics. This is reality, explicitly stated in the paragraph in the article under this heading: “This is house price inflation.”

Inflation means loss of purchasing power of the dollar. This is the dollar’s loss of purchasing power with regards to houses.

Maybe turn all your RE charts upside down so your readers can readily see the fiat frn dollar denominated in houses.

Ha! 🤣

There was a report on TV in the UK about this and it was something like if a chicken had gone up the same as house prices then a chicken would cost £40. A chicken actually costs £5.

I just went over to the MLS.

Listings in the Auburn, WA area (south suburbs of Seattle) are mostly around 6-8 days on the market. No sign of a slowdown.

I am unable to predict what is going to happen, but I’m pretty sure that the recent rise in interest rates has already scraped off the marginal First-Time Buyers. I expect that when a 30-year fixed mortgage gets to 8%, things will change.

The problem is that inflation expectations are quite high, and going higher. As long as you have Wall Street types who can borrow at 5% below the inflation rate, the normal rules of housing markets do not apply.

It will take some time for the market to internalize all these changes

Give it some time

Anecdotal evidence but interest is still low (3%) for jumbo mortgages in Bay Area for those with excellent credit.

Prices are still ridiculous but there is plenty of “easy money” that won’t be the case in 6 months.

I picture a speeding car, accelerating on the freeway, and then the driver shifts into reverse and lets the clutch out. There’s your soft landing!

If the Fed blinks, the prices lift off again from this crazy level. I will hunker down harder. But if the fed hits reverse, I expect to rely on my harness system — my balance sheet I have spent decades shoring up. I am not auditioning to be a crash test dummy. I can stand a reversal in real estate prices.

Don’t worry.

The American & Canadian governments will cut funding for social services to bail out the upper middle class real estate investors.

Don’t worry Gov Newsom and the Biden admin have both recently talked about increasing rent vouchers and subsidies for rentals.

The social programs themselves will be the bailout for upper middle class investors, and in turn create more inflation to drive more people into those programs and rentals. See it’s win-win for both parties…

Just an observation. My guess is many house shoppers are locked and loaded with a pre approved loan and rate from back in January and early February.

Most locks are good for 90 days and are valid up until the end of the 90 days and or once you commit to a contact in that period and into closing.

Rates have skyrocketed since that time. Will be interesting to see if we observe a significant and dramatic pullback 90 days from mid February.

If this observation is correct. That means we should see the brakes slam on come around the end of May. Or, earlier.

The loan application is good for 90 days from the time they pull your credit. But lenders don’t typically lock rates until after you have a signed purchase agreement.

So that means pending deals are the ones with fire under their them to close, not potential new deals.

I have taken a beating trying to call this housing top. Having been an investor and gone through dotcom and gfc, I got worried and sold my CA rental houses that I picked up cheap near the 2011 bottom in 2014, 2016 and 2020. I had no earthly idea how prices would keeping powering though the stratosphere. I left a lot of money on the table.

Calling the top of both stocks, bonds, and real estate has been a widow maker in this run up. I was bearish way too early after having experienced dotcom and gfc. It almost hurts as much losing out on big runs as it does losing money in crashes. I wonder if real estate is ever going taking a big price hit? There is very, very strong demand out there and WAY less inventory than there was pre gfc. It’s just not easy to add inventory with labor shortages, permitting red tape, materials costs.

I read a report that said we will not get back to pre-covid normal inventory for 2 years. Covid, Low interest rates, and WFH caused a lot of demand to be pulled forward.

There has been a big influx of immigrants. I have been reading thousands of Ukrainians have been flying into Mexico and then they had to the U.S. boarder. Once there they can ask for asylum. This gives them 1 year to live in the U.S. while their case is being evaluated. I read that close to 30k over the past month. Add in population growth and other immigrants, housing just cannot keep up because of the reasons you listed.

It will be hard for housing to drop much at all on low inventory and high demand. IMHO….there will be a lot of housing incentives given out the next couple of years.

I know these charts look like bubbles ready to be popped but the FED want those charts to just go sideways or slightly up. They will do whatever they can to keep them from dropping. Can they…who knows but they will react very quickly to stop any big drop. Just my humble opinion lol

rue82,

Immigrants coming across the Mexican border aren’t buying $500K homes. Or any homes.

Scapegoating is alive and well.

But they do move into those 500K houses and since crowding is acceptable, are more than willing to pay 2x rental compared to some Americano who wants a 2BR house for no more than five people.

Same with apartments.

Some of the most profitable rentals in the Bay Area are in Hispanic areas like Marin and the East Bay where this rent gouging takes place. i.e. 4 adults in what was once a kid’s bedroom, paying $600 each.

4 Roommates packing into 2 BR apartments is common in San Francisco. That might still amount to about $1,000 per person in rent.

Certainly have done in FL at least Wolf, and for a long time: place we lived in SWFL 04-06 had very hard working recent immigrants w purchased papers buy two houses across the street. Learned that when a party with many of my Hispanic coworkers happened and neighbors, invited, got to talking re immigrant status, etc.

It is a myth that folks coming across our southern border are always poor, etc.; these days, they are usually coming here that way to do so asap, rather than waiting 7 or 8 years to immigrate totally legally.

Last I heard, it cost approximately $500 USD to purchase papers in Tijuana good enough to pass E-Verify, though that was some years ago, and with the inflation, maybe double now.

Half the ”field workers” at my last big national corporate job had come in that way; all of them were excellent workers and valued by the company. About 25% were from various European nations, but came through Mexico with purchased papers too.

@VintageVN

You maybe be on to something. I went to a site that studies immigration. What I found odd was that illiegal immigrants after 1 year in the U.S. , only 11% were below poverty. 47% were over 200% above poverty level. No Poverty level is pretty low. $12k for a single person and about $24k for a family of 4. But 200% of $24k is $72k.

wow. you sound like a junkie.

How come when I imagine your voice making that statement, the “j” sounds like an “h”… :)

COWG,

Not sure Kitten speaks Spanish. She’s half German, half Puerto Rican Black.

She certainly doesn’t have a Hispanic accent when she speaks.

Kitten, you may want to chime in here, if I got this wrong.

don’t know either WR and cowg,,, but KL is helping me decide to add ”I GOTTA” get out to my beloved SF Bay Area at least once more to my bucket list…

Who knows, if HH will meet my ”ask” on the unique ”heritage” Wolfstreet mug, at least close to half way,,, LOL,,,

I might even be able to buy another house or three there right after the next crash, eh

‘How come when I imagine your voice making that statement, the “j” sounds like an “h”…’

–the same reason i read your name out as COWGIRL, i guess.

but you can listen for yourself if i say “hunky” or “junkie” after James and i record our first podcast this afternoon for Record Scratch Radio on substack because James IS a “hunky” so much so that people call him Hondo around here.

only kidding about the Hondo part. who doesn’t wanna be called Hondo? My first muse and his best friend told women in the 80s when they’d go to nightclubs that his Jewish dentist friend was “Hondo.”

the girls went for it.

x

dear VINTAGE VIET NAM VET:

no lie, when you DO decide to come out, you MUST MUST MUST co-ordinate with Wolf and me around a future WOLF MEET. he’s said nothing about it but i act like i’m his second wife when it comes to the Wolf Meets and insist they become a THING first moment possible because it’s all going down and whether or not the WEF is a “thing” we need our own parallel economy or world that actually tries to adhere to The Constitution or logic or enlightened self interest that isn’t about demolishing humanity for a dime.

it was RD Blakeslee who sent Wolf here a silver quarter to send on to me, and he told me the reason there’s a scalloped edge to coins is to prove it hasn’t been shaved off like they did during the Black Plague, when they first did the first Enclosure of the Commons.

now we’re onto the next Enclosure of the Human as another writer on JMG’s blog, “Murmuration”, calls it.

i’m not even talking conspiracy. i’m looking at HISTORY (in Barbara Tuchman’s book “A Distant Mirror: The Calamitous 14th Century”.

and we need ELDERS, THE ONLY PEOPLE LEFT WHO KNOW HOW TO ACTUALLY DO ANYTHING COME UP WITH ANYTHING COMPLETE ANYTHING now that results don’t matter; only image.

so DO plan a trip here but later. things are still flushing down the toilet and yes maybe you’ll be able to afford something. i’ve been thinking of consumer collectives (us all buying into a gym/cafe combo) or something when commercial rents plummet here.

San Francisco IS the place to be if you can sit tight for the inevitable downturns. if you’re a scrapper.

x

GREED.

Don’t call a top in housing yet. Agree that total inventory will remain tight in most NON fringe areas due to reduced new starts (red tape/permits/lack of labor) and the fact that anyone with moderate “money” is picky. I am confirming real estate is very “local” and “selective”. In my youth I bought the house I could afford with 8% rates (1998) and slowly fixed it up with my own labor and the help of a few local contractors. Now the millennials who have money ( I work with a few) WONT consider an “old” house that needs updating (at 350K) but keep placing offers at 500K and “losing out” to cash bidders at 550K here in the mid Atlantic. the contractors I used decades ago have cut back and “dont” need to work hard as they are close to retirement ( late 50’s/early 60’s). So the stock of “old” SFH around here just sits as it is overpriced (350K for 1800-2000 sqft of 1970’s love) and needs upgrades, YET the NEWER stock gets bid on like crazy. The really cheap stuff (townhomes sub 200-250K) gets snapped up in days by “investment types” who upgrade and rent it. No matter what anyone says I dont see the “mid Atlantic” going “down” in price anytime soon ( Philly/northern Virginia/ NJ). BUT BUT as for the Miami condo’s I watch, yup they are starting to drop, but ever so slowly. watch a couple buildings and it’s amazing the difference in price/SQFT. the SAME building I am watching in Miami Beach has some units owned by individuals dropping prices to $690 a SQFT yet the same exact building has the same UNupgraded units at $900 SQFT owned by a “investment” firm. Hope they get hosed as they aren’t able to rent and carrying costs are at 5-6% a year ( taxes/condo fees). Ah I hate the FED for this distortion!!!!

$900 per sq ft. I’m gonna have to slim down to live in what I can afford.

63% of Americans don’t even have $500 in savings for an emergency. They can’t even afford a coffin, much less a $900 per sq. ft. house.

I read 40% of the price of a home is in the land. It varies from place to place.

They are building 1800 sq ft homes homes in Charlotte County, FL in the $300’s with the lot included. There are more 55+ residents per capita here than most other counties in Florida. Land is dirt cheap.

In my area, last years $300s are this years pre- building price above $400k now…

And none being built are spec…

Most areas are also HOA restricted to minimum sq ft allowable…

Extended Zirp took us to a new place. I for the most eased out of stocks in 2014 and 2015. In 2014 stocks hit 2X their long term value on price to sales and 4X their all time lows on price to sales measure. It’s now about 3.5X and 7X due to Zirp. Probably not that different for housing as anything after 2014 is caused by Fed crack that will end up being a historical mistake

BackRoad,

I view real estate investments the same way I view stock investments.

I bought AAPL stock back in 2002 at the stock split equivalent of 30 cents per share. I sold it all around 2010 at $9 per share. It is now at $180 per share.

Did I take a beating? Not by any measure.

After investing the gains in stocks with far less returns, I decided to invest in a new Magic 8 Ball. It didn’t help. Nothing helps.

However, my glass has still been half-full since 2012 in everything I’ve invested in. I have always been moderately conservative.

As Wolf has pointed out, recent aggressive SPAC and ARKX type investors have taken a beating.

How long can this current runup in houses and stocks last for conservative investors like myself?

Why try and time the market? Just take what you need and live contently ;)

The following may be far fetched idea. I think the FED does not want house prices to go down. Housing prices dropping quickly causes all kinds of economic problems, jingle mail, foreclosures, bankruptcies. I think they would rather have home affordability go up.

After seeing California looking to give people $400 checks to combat rising gas prices (instead of conserving), I think we may see money given out to people so they can buy a house.

So I am guessing we will see a lot of incentive such as free down payments for new home buyers, etc.

I have already seen programs out there now where the government will give you $15k down payment and another will pay up to 5% of the down payment payment . The 5% works out better than the 15% on houses over $300k. Buy a $400k house and you could get $20k of you down payment paid.

Every sale requires a ready, willing, and ABLE Buyer. If they don’t have down payment and closing costs, and sufficient income, they may want it but they ain’t buying. The all cash buyers are right now re-thinking their second home, etc. The institutional buyers, investors, flippers should all be reassessing their “investment” knowing as interest rates rise, prices and rents will decline. Able buyers are the key to market prices.

If there is any large scale government housing buying assistance, it’s either going to be tax credits or loans.

No, leaders in government presumably don’t want housing prices to decline but it’s only one of many moving parts.

The cheapest option to mitigate another housing crash is probably a mortgage moratorium. At 3% or slightly higher rates which should be a noticeable percentage by now, it costs around $2.5B/month for every $1T in loan guarantees.

If supporting housing has to compete with something else which it undoubtedly will when this mania bursts, depends.

Contrary to any belief, the FRB is not going to trash the USD to save middle class home equity. It’s not going to happen to save the stock market or economy either.

The country is being asked to suck it up and make sacrifices due to the current geopolitical situation for a country most Americans can’t even find on a map and the US government is “all in” on it.

The only reason for it is to preserve the Empire and practically everything and everyone else will be thrown under the bus to preserve it.

The Fed completely threw a curve ball on more then one occasion and bailed so many investors out of the deep end. The other day I read a few investors purchased a ton of “walk away homes” in new subdivisions near me. They took out PPP loans to cover normal operating costs. Then they used normal operating costs to buy homes in 2020 when everything was flat. Now they are selling in some areas by us. They are getting out and making a 20%+ net gain from this little act. The question is if the others follow suit? If so, then inventory will increase and house prices will fall. As long as they break even – all is good. The other demographic we are reading is that Millennial generation is in the landlord game. They used the equity to buy the down payment to their second home, moved in, and now rent out the house. If it goes without a bid or if things crash, they sacrifice the old home and keep the one they wanted. Either way it is just two threatening pins to the bubble.

“ The other demographic we are reading is that Millennial generation is in the landlord game. They used the equity to buy the down payment to their second home, moved in, and now rent out the house”

Gabby,

Are you alluding that Millennials who were smart enough to see this coming and took advantage of it are now somehow to blame for screwing over the Millennials who weren’t…

I had not heard that before…

However, how novel….

I guess greed isn’t limited to the Boomers… /s

let’s get one thing straight. people who bought houses in, say, june of 2020, were arguably “smart enough to see this coming,” as interest rates had just cratered to around 3%.

people who bought houses in 2018 or 2019 were not “smart,” they were just lucky. no one could have known that the fed would print $5 trillion and suppress interest rates at that time, driving the prices of all assets through the stratosphere.

i bought a *lot* of assets (not going to say what kind) in 2019. i don’t consider myself smart for that at all.

some humility would do you well, cowg.

Apparently, you took offense to my comment thinking it was directed at you…

Good catch…

BTW, I reserve humility for those I think have earned and deserve it, not demanded by whiners on a public comment board…

Since the end of the gfc in 2009, this has been a absolute stunning run up in stocks and real estate that will just not die! Nothing can kill it! Covid couldn’t kill it, the highest inflation in 40 yrs can’t kill it, Russia invading Ukraine can’t kill it.

I think back to the dotcom run up, and really that was only maybe 1995-2000. GFC housing bubble was only 2003-2007. We are now at 2009-2022 in this one and still do not yet have anything close to a sustained downturn in stocks or real estate! This is a insane 13 yrs at this point. The power of this cycle has just astonished me. I think even the 1929 crash was only like a bull market from 1926-1929? Nowhere close to this monster!

is it that astonishing when you consider how much money has been printed?

if you see it as regular inflation, and not a “run up,” it makes a lot more sense.

exactly. Housing is not only up a lot in the U.S. but globally. The 3 central banks FED, ECB, BOJ increased their balances sheets from 3 Trillion in 2007 to 25 trillion now.

Everything should be going up on prices.

In addition, go look at the currency in circulation. Think cash in your wallet. It was 900 billion in 2020. Now it is 2. 3 trillion. Amost tripled in 10 years. If you go look back in time. In 1990 it was about 275 billion, in 2000 it was 520 billion (double), in 2020 it was 905 (almost double), 2021 it was 2.3 trillion (almost triple) .

Government plus Fed has brought forward our future into wealth affect. Flip it around and say what is our future on an asset bought at these prices?

Our local utility stock is Duke and price is so high that dividend is down to 3.5% nominal. I hear people are doing real estate with 4% cap rates. SP500 dividend income 1.3%. Ten year Treasury 2.5%. True value should be the income the asset will produce not in the bubble price unless you cash out at that price.

BackRoad-

“I think even the 1929 crash was only like a bull market from 1926-1929?”

While I agree that the 12 year market run-up that we’re looking back on is gargantuan and unsustainable, I think you’re misrepresenting the 1920’s cycle.

The 1930’s depression, when the stock market bottomed in 1932 and double-dipped later in the 1930’s, was a blow-off to the roaring 1920’s, BEGINNING in 1921. 1921 is the year of the “forgotten” post WWI depression when the adolescent FED was ineptly grappling the inflation that happens after world wars.

Presenting the 1920’s “bull market from 1926 – 1929” minimizes the effect of the Federal Reserve System as a major contributor to the Great Depression.

For background, try Friedman/Schwartz “Monetary History,” or even better Phillips/McManus/Nelson “Banking and the Business Cycle.” [ latter — https://mises.org/library/banking-and-business-cycle-0 ]

The dot/com bubble and stock advance during housing bubble 1 aren’t different events from the current one. It’s the same mania because the prior two events were never even close to being corrected.

Yes, we’re talking about a multi-decade mania.

It’s lasted a lot longer than I ever thought remotely possible too and I’ve been following it in real time the whole time.

All it means is that when it ends, the collapse is going to be far worse than any prior occurrence in history. Virtually no one believes it because it’s supposedly either “different this time” or the government/FRB won’t “let it” happen.

It’s never different because there is never something for nothing. As for government, “printing” and borrowing aren’t a new invention and that’s all that’s available to hold up this house of cards. There are no new “tools” or some deus ex machina hidden in a closet somewhere which will magically create or sustain permanent fake prosperity.

Wolf, do you really think SF single family home prices are heading down allot when prices in the South Bay are about the same, if not higher? That is unsustainable as jobs/workers return to SF, esp. if the stock market stays high. everyone would rather live in SF than in the bay area suburbs.

also, re “Every year, 2,000 to 4,500 housing units are completed in SF.”

that is not true post COVID crash. new SF building permits have plummented, and likely to stay in the toilet going forward for all the bearish reasons you say, including costs vs rents no longer pencil out. So, the lower rents will attract more people to live/work in SF. So, supply likely to stay flat while demand will soon be surging, if not already. That is not a good setup for lower prices, IMHO.

Not sure I know what you’re talking about. Seems you don’t know either what you’re talking about.

SF lost 6% of its population between mid-2020 and mid-2021, according to the latest Census data. Every year, SF builds between 2,500 and 4,500 housing units, In 2020, a total of 4,000 housing units were completed, after 4,500 being completed in 2019. An additional 5,800 units were under construction at the end of 2021, most of which will be completed in 2022. About 60,000 units are in various stages of the planning pipeline. This includes mega-projects on Treasure Island, the Naval Shipyards area, and the Bay View & Hunter’s Point area. There is construction going on everywhere, including fill-in projects everywhere, including in our neighborhood.

I understand that you live on the other side of the country, so you don’t know and don’t see what’s going on here.

SF home prices tanked twice over the past 30 years: From 1990-1996 (-11%) and from 2006-2012 (-40%).

Condo prices haven’t gone anywhere since 2018, despite the HUGE bubbles everywhere else. And condos are the biggest part of the market.

Rents are down 22% from July 2019. There are more apartments available for rent than I have ever seen before.

When the cause in a cause-and-effect relationship changes, the effect changes also. We are at the point in time where the cause of the current asset bubbles is changing. To all of you who think this won’t matter, good luck.

Eventually this market will have to nut. Stand Clear , it’ll be a mess.

Found the following at fred.stlouisfed.org. Released by US Federal Housing Financing Agency. “All Transactions House Price Index” is the name of the index for each state and D.C. It goes back further in time than does Case-Shiller and offers another perspective. Some general observations: Idaho is in a rip-your-face-off uptrend the past few years. Bubble 1 really did burst in Nevada. In other states, the previous bubble looks more like an oversold condition when looking from the perspective of the long-term trend.