Companies adjust their office footprint to working from home.

By Wolf Richter for WOLF STREET.

Houston’s office market got into trouble back in 2015 when an office construction boom collided with the oil bust that forced the whole industry to cut spending via downsizing and layoffs. Office vacancy rates began to explode. And then the pandemic’s working-from-home made it even worse. Now, over 30% of the total office space is on the market for lease.

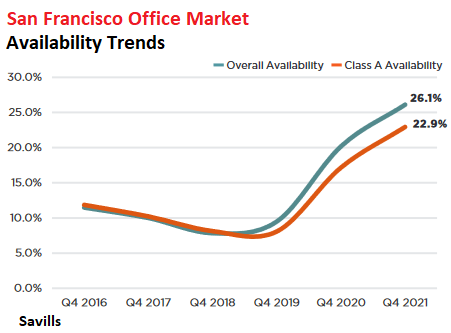

San Francisco’s office market, back in 2018, was the tightest in the US, amid ceaseless hype of an office shortage, despite the construction boom that had been throwing new office space on the market for years. But in late 2019, a lot of vacant office space started showing up on the market, with overall availability jumping from 7.3% in Q3 2019 to 9.6% in Q4 2019. Then came the pandemic and working from home. Now, total availability exceeds 26%.

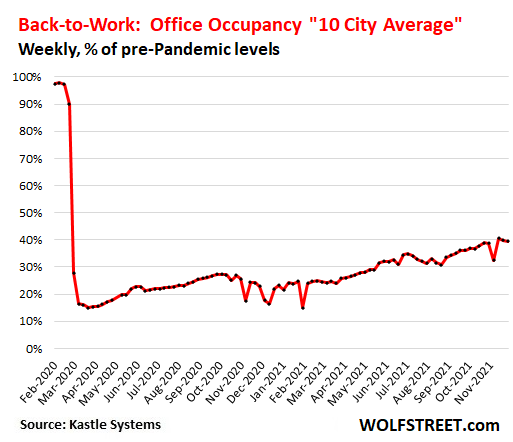

In mid-December, nearly two years into the shift to working from home, office attendance across the biggest office markets, as measured by Kastle’s data from its entry systems, was still down 60% on average from pre-pandemic February 2020, ranging from -72% in San Francisco to -42% in Austin.

At some point, more workers will return to the office. But working from home for at least part of the week has become a sought-after benefit for employees, and for companies an opportunity to cut costs – less office space.

This has long-term implications for the office market that was based on the theory of endless sharp growth in demand. Companies are already sitting on large unused office space, some of which they have now put on the sublease markets, and some of which they hope they will eventually fill with employees. One thing they’re doing a lot less is trying to find additional office space.

Here are the major trends in seven office markets – Houston, San Francisco, Manhattan, Los Angeles, Chicago, Washington DC, and Seattle – in Q4 2021, based on data from real estate services provider Savills.

Houston, the sickest major office market in the US.

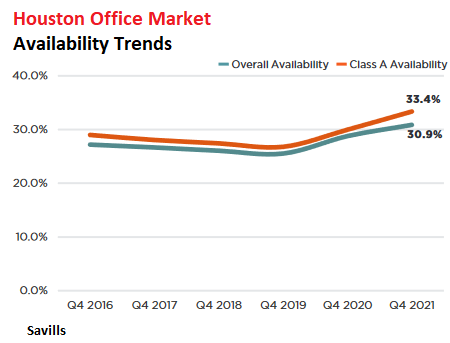

Availability of Class A office space, at 33.4%, was roughly flat with the record worst in Q3: About one-third of all Class A office space is on the market for lease. Overall availability “has leveled off” at 30.9%, Savills said.

Availability ranged from 8.8% in Medical Center/South Houston – the “life sciences” sector in real estate is booming everywhere as healthcare is gobbling up the US economy – to 51.7% in N. Belt/Greenspoint. In the Central Business District, availability rose to 34.1% (chart via Savills).

Average asking rents have been hovering for years at around $29 per square foot (psf) per year. Actual deals differ, often with lower rents and aggressive concessions.

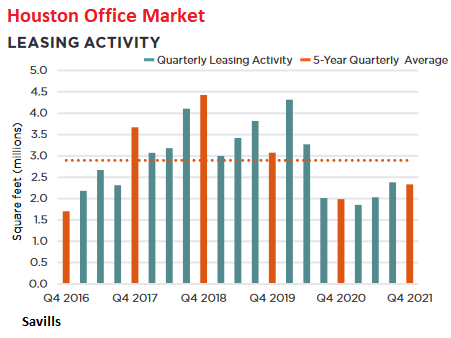

Leasing activity remains well below the five-year average and is back where it had been during the oil bust, with 55% being renewals (chart via Savills):

San Francisco, from office shortage to office glut.

After having stood out with its endlessly hyped office shortage, the San Francisco market has made one of the most breath-taking commercial-real-estate U-turns, and it started before the pandemic.

Of the total office space in the City, 26.1% were on the market for lease, up from 7.3% in Q3 2019, ranging from 21.7% in the Financial District South to 36.7% in Yerba Buena (chart via Savills):

Overall asking rents ticked down further, to $72.54 psf per year, down 13% from before the pandemic ($83.50 psf).

“There is an ample amount of price discovery still happening as landlords are willing to make exceptionally tenant-favorable agreements in order to secure new tenants and retain their current clientele,” Savills said.

“In addition to reduced rental rates, landlords are offering generous concession packages and increasingly flexible terms,” Savills said.

Leasing activity, though up from lockdown lows, remains well below the five-year average, and was down about 30% from Q4 2019. About 45% of the leases were renewals:

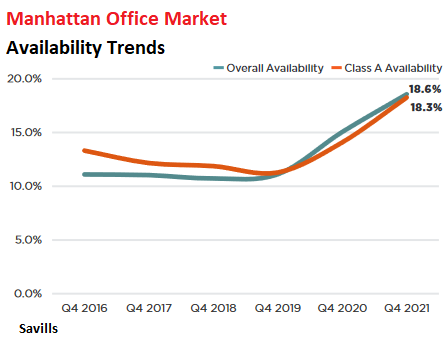

Manhattan, new projects drive up availability.

Overall availability rose to 18.6% as new office towers, approaching completion, were added. “This trend of new premium space additions forcing the availability rate higher is likely to continue in the quarters ahead as major blocks at 345 Hudson Street and 919 Third Avenue, among others, come to market,” Savills said.

Average asking rents rose for the first time in eight quarters, by 1.3% to $76.03 psf per year – “on the strength of premium space additions,” Savills said – but were still down 9.4% from pre-pandemic levels.

Leasing activity rose above the five-year average for the first time since 2019, but that wasn’t enough to absorb the new additions, and availability continued to increase.

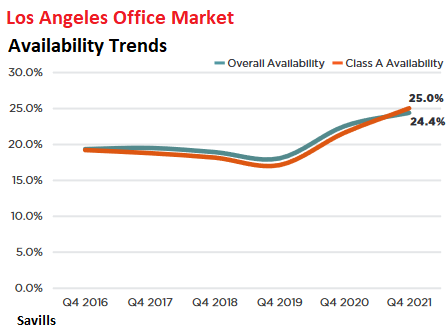

Los Angeles

Overall availability, at 24.4%, was flat with Q3. Class availability ticked up to 25.0%. Sublease availability eased to 8.6 msf (from 8.8 msf in Q3) “as space becomes leased, is pulled off the market, or master lease terms expire and the space becomes directly available,” Savills said.

Asking rents ticked up to $3.88 psf per month ($46.56 per year). But “concessions such as rental abatement and tenant improvement allowances remain at an all-time high as landlords aggressively compete for occupancy,” Savills said.

Leasing activity, at 3.6 msf, while way up from pandemic lows, remained below Q4 in 2019 and 2018.

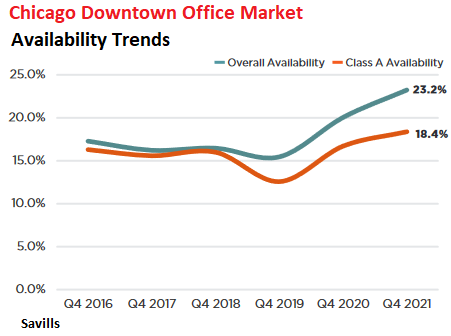

Chicago Downtown.

Overall availability jumped to 23.2% in Q4. The market is “increasingly bifurcated,” Savills reported, amid a flight for quality and therefore more demand for Class A office space:

Asking rents dipped to $40.47 psf per year. Sublease supply “remains elevated and will continue to exert downward pressure on asking rents,” Savills said. “Rental abatement and tenant improvement allowances remain at all-time highs as landlords are forced to aggressively compete for occupancy.”

Leasing activity, at 2.7 msf, was roughly flat with Q4 2019 but about 25% below Q4 2018.

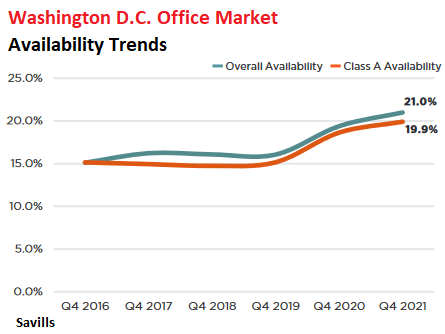

Washington D.C.: Government is the “driving force.”

Overall availability has remained at the record level of 21% for three quarters in a row:

Asking rents remained roughly flat, at $55.19 psf per year. But… “The real story has been the rise in concession packages which continues to validate underlying tenant-favorable conditions,” Savills said.

“Total concessions for D.C. prior to the pandemic historically only increased approximately 5.5% per year. However, in 2020 concessions went up a significant 21.0%, and this past year concessions rose 11.0%. New long-term Class A leases now receive an average of $148.00 psf in tenant improvement allowances and 23 months on average of free rent, totaling $280.00 psf in total value.”

Leasing activity surged 52% year-over-year to 3.0 msf, the highest since 2018, and the highest fourth quarter in years.

“The government sector was the driving force behind demand, accounting for 67.0% of activity by square footage, and sizable leases were signed by both local and federal government agencies,” Savills said.

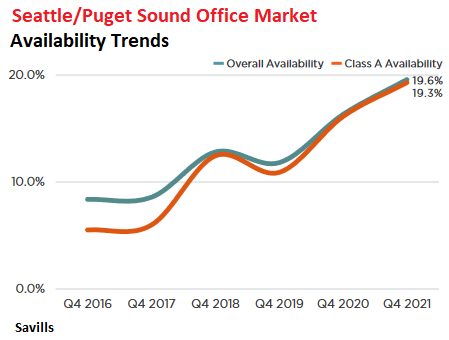

Seattle/Puget Sound: Meta did it.

Asking rents, in Q4 at $39.70 psf per year, have wobbled along just below $40 for years. Leasing activity, at 1.8 msf was back at the five-year average, with Meta signing the largest deal, and it and its Oculus division signing two additional leases. All three combined accounted for over 17% of total leasing activity.

Overall availability ticked up to 19.6% in Q4, having more than doubled since 2017:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If this is the case, why are CBRE & JLL stocks at new records, and doubled from pre-coronavirus levels?

Jackson Y,

Because nearly everything is at record highs (=asset price inflation)? Thank the Fed.

But wait… CBRE is not on the hook for the properties. It just gets fees. Landlords are on the hook. And every single office REIT is sharply down from pre-pandemic levels.

Wolf. Insurance companies are reporting the death rate among working age Americans is up 40% since Covid. Maybe corporations need fewer offices?

“The head of Indianapolis-based insurance company OneAmerica [with $100 billion in assets] said the death rate is up a stunning 40% from pre-pandemic levels among working-age people.

“We are seeing, right now, the highest death rates we have seen in the history of this business – not just at OneAmerica,” the company’s CEO Scott Davison said during an online news conference this week. “The data is consistent across every player in that business.”…

Davison said the increase in deaths represents “huge, huge numbers,” and that’s it’s not elderly people who are dying, but “primarily working-age people 18 to 64” who are the employees of companies that have group life insurance plans through OneAmerica…”

masked ghost,

Wait a minute… Let’s do some math. This 40% increase of the death rate is a “rate of a rate.”

As tragic as this increase is, its impact on a company’s office footprint is nil. I’ll do the math for you:

The death rate of working age people in 2018 ranged from 38 per 100,000 working 15-to-24-year-old women (lowest death rate) to 1,119 for 100,000 working 55-to-64-year-old men (highest death rate). I just looked it up. So let’s ballpark it as an average death rate of 500 deaths per 100,000 workers in 2018.

So an employer with 10,000 workers in one big office complex in 2018 could expect 50 of those employees to die over the course of the year, for a variety of reasons, ranging from illness to accidents and suicides.

So every year, 50 people of 10,000 employees die in that one big office complex.

A 40% increase of that 50 deaths among 10,000 workers means that now an additional 20 people among the 10,000 die per year. For a total of 70 per year.

The numbers – as tragic as they are, and as expensive as they may be for life insurers – are way too small (an additional 20 deaths per year among 10,000 workers in a big office complex) to impact that company’s office footprint.

Also, the company would just hire 20 new people to fill the newly vacant 20 jobs. Regular churn among employees, with employees quitting and having to be replaced is far, far higher.

So let’s not go overboard with “rates of a rate.”

masked ghost, you should of posted your comments in wolf’s next article. It would account for a wider spread, instead of the silly number of office workers.

Wolf, I am curious whether if there is a divergence in office building lease trends between Seattle and Bellevue. I know your data merges the two, but I am somewhat sure that there are two different tales between those two cities. Pretty sure Seattle is on a decline while Bellevue commercial RE is exploding.

There’s definitely some nuance lost in merging those two markets together

It goes by area. CBD = Central Business District:

Not a single Seattle market under 20%. Everywhere outside that overpriced overrated liberal urine-infested place doing better. Love it. Those scumbags that run this place and the wealthy tech liberals that support them will get what they deserve.

Seattle is my hometown and as much as I used to have fond memories of that place, it is now a total dumpster fire. And the business climate is so anti-business (including the entire state of WA, to be honest).

What is a bust for Seattle is turning out to be a boon for Bellevue.

As much as I appreciate the schadenfreude, Bellevue and most of the Eastside is pretty lame and incredibly sterile. I prefer Seattle despite all the problems the city is facing right now. It’s much more organic, interesting and varied. The Eastside is like one giant strip mall with a bigger mall in the middle. If the Eastside is the Pinnacle, beam me up Scotty!!

In the long run I think Seattle will recover just fine.

Very interesting, thank you!

As suspected, downtown Seattle / South Lake Union in Seattle are getting decimated while Bellevue space is in demand and tight!

good observation. Multiple new high-rises are being built in the Bellevue downtown, and not only commercial; and you can see a lot of residential buildings along the new light rail on the Eastside.

Along with the office space $/sqft massacre we have the bad juju being being telegraphed by the 2.3% drop of pending home sales. Are pending home sales more like deer tracks?Good for getting you excited but you can’t hang them in the barn. 60 billion decrease of the 120billion monthly Fed juice has gotta have an impact somewhere. That pile has a direct connection to the economy. Stimulus is gone. $300 /child benefit went to heaven via West Virginia and is also gone. Inflation is still roaring. This shit is starting add up.

Deflation great reset?

A 2.3% YoY drop in the traditional off-season after setting a record jump last year (up 16.4% YoY in Nov 2020 vs 2019) is hardly an indicator of anything… yet.

Heard a guy out of New Orleans on a podcast mention that after every benefit cut the crime there went up. Up when the stimulus ended, up when the extended unemployment ended, up when the child credit ended, and now the extra EBT is ending too. They ended the year with very high crime rate and the new year is already on the way to top it.

I was just in NYC.

So many empty prime retail spaces. Every block all up and down Manhattan and Brooklyn.

The retail stores that are still open are fairly quiet.

I was also in Maimi. Saw a few empty places but not much. Folks everywhere shopping and going out.

These trends will continue.

2banana, you have a valid point here.

The environments, political, safety, taxes and regulations, of these places has turned toxic in many ways other than simply vacancies versus rents.

Failed local government policies are now seeing the bills come due on their dreadful decisions, and they don’t have what it takes to cover the AP checks. Rule#6: Never let your mouth write a check your fists can’t cash.

“Work from home” is just a stop gap measure until firms find a better place, economically, safer, and with a more attractive living area, for their employees to come back to.

Moving to greener pastures is a basic market force that can’t be stopped.

SF & NYC will look like flyover down towns, destroyed in the late 70’s,

never recovered for 50 years.

Thanks for letting us know you’ve never been to SF or NYC.

Housing Crisis = not enough good houses on market. Commercial Real Estate = no tenants. I see commercial real estate to luxury large residential in the near future. Isn’t that what happened in urban revitalization of the 80’s and 90’s? Green energy of community living? As soon as COVID leaves the news thanks to Pfizer’s pill – the democrats will save the economy from inflation. They need the votes.

Sorry, the people are either awol or doa.

Are there enough very rich people around to buy into the luxury commercial conversions? Or maybe the Blackrocks of this world may be doing the converting, but then again, will there be enough tenants willing to rent at what will have to be expensive leases.

It seems to me that in the States, there is an undersupply of single family resi in good locations. Same as here in U.K., there is a dire shortage of good homes in good areas.

Cost to run plumbing and the likes to convert a commercial building into housing is prohibitive.

Building codes should change, why not run insulated water and sewer pipes up the outside of buildings and put in modular kitchens and bathrooms? Any building with windows that don’t open is a bad investment.

In Orange County, Ca, vacancy was 13.5% ( 3rd Q, 2021 ). The historical average is 12.1%. The suburban nature of OC keeps the offices vacancy rate reasonable.

Why are my comments moderated?

I don’t see any reason on my side why your first comment went into moderation. Possibly the doings of the spam filter.

When AAPL ShiexO saw those honest RE charts she lost her contact lenses

cell phone.

How does Boston rank? Being located in the business district, it appears dead! Sales are still down 60% from 2019.

Boston’s report isn’t available yet. In Q3, overall availability was at 16.5%. It has been high for years.

For all readers here: Please don’t ask me about other cities. Reports are released on different dates, this is what I have today, and only the major markets get reports at all. Boston and some other cities will be released later in the month.

Historically, Boston ran at 8% … now it is double. All the finance guys are working from home.

Even if there is a return to the office, WFH has been running long enough to solidify worker demands to keep it. I think it’s unlikely to ever go back to 5 days/week for most people. Companies can now consolidate to much smaller spaces and/or move outside of city limits.

I can’t see the financial district ever looking the same as 2019 at this point. Perhaps in a couple years, the condo conversions will start.

I wonder where Kastle get its occupancy stats from. It is after all a facilities management company. Do they count the number of people entering en leaving the building and somehow convert this to square feet? Without knowing their methodology I am skeptical about their data.

Kastle sells and services electronic office entry systems (electronic key fob systems, app-based entry systems, and card-based entry systems.) So if an employee enters an office via his card, the entry is tracked and becomes part of the data that Kastle reports. So they count attendance of employees. And office “occupancy” is measured in the number of people that are in these offices today, compared to February 2020. Nothing to do with square feet.

This is a measure to track the “return to the office” from “working from home.”

America will follow China way overbuilt real estate not enough businesses to occupy now automation taking over factories checkout no jobs no money on society sad

My son started work at a big online gaming and e-sports company in LA. They will be fully back in the offices by next month. A large residential, commercial and office complex started construction on the site of the old Olympic drive-in across the street. The company he works for just leased all 200,000 square feet of office space in the development.

I also agree that LA will continue to attract silicon valley companies, and will continue to stay popular with young office workers.

At one point in the earlier years of my career I interviewed at many companies in the LA / southern Cal area. I was shocked to see that so much of their industry was entertainment and gaming. At least in my field of work in tech at that time.

When will all these gaming dollars / capital go to something of real value to the economy?

Video games = opium for the mind.

PG-check out ‘Peoples’ Republic of Desire’ on PBS’ ‘Independent Lens’.

Interesting view of another form of mind opium in a different land (…2018 story, things may have changed under CCP repositioning since then…).

may we all find a better day.

In my old hometown, Detroit, 5000 on up sq ft empty former tool and die shops are being converted to pot growing farms for the recently legal cannabus industry General commercial retailing still in the dumps.

Overbuilding in office real estate is another result of cheap money. Carrying costs are also a lot lower with low rates.

I expect more working from home when companies have to cut costs further for a real recession that isn’t papered over by fake prosperity.

I agree. WFH has challenges, but it is a huge cost saving for everyone involved. This cannot be ignored in a competitive market. Even if nobody liked it (which isn’t even the case), the businesses that can make it work will be able to undercut their competitors big time.

As a small manufacturer, when the internet destroyed the traditional distribution models ten years ago, I didn’t like it, because I had to develop my own global retail face to the business. Before I just threw the product at distributors who sorted this all out for me. But I was forced to adapt because if i didn’t my competitors would have undercut me.

So now all the players in my market are all doing direct sales for similar margins as before. We all ship roughly the same amount of product as before, we make roughly the same net margins as before, but the customers get significantly cheaper product, the dealers are out of business, and our business had do to a lot of extra work.

The same will happen with WFH. Companies, landlords etc won’t want to do it, but if it reduces prices for customers then it will happen.

Jon W,

Interesting comments. I hadn’t thought of what you’re describing. Winners and losers of the WFH phenomenon.

But all these properties are levered. And now the revenues stop. And this is major coinage. At some point doesn’t this portend defaults? Then cascading defaults? What’s holding it up? Wondering how this plays out. Cascading job losses to follow? Maybe a few 2nd and 3rd homes suddenly come on the market?

Does anyone have comparable data for Portlandia? Would be interesting to see how they fare after the last 2 years and effects of the experiment that they have become.

I think the death of the office has been overstated. There is no substitute for face to face interaction and collaboration. Managers also like the assurance their staff are working, rather than doing other things. People will work from home occasionally and firms might utilize hotdesking to reduce their office footprint. However, I think a more likely scenario is companies make the office more enticing for employees, giving them more communal space and facilities, and probably increasing the size of workspaces. This will result in more demand for office space, not less.

Years ago Yahoo trialed work from home and it didn’t work. In 2013, the CEO asked all staff to go into the office.

And if staff could permanently work from home, they could be replaced by people working in other countries with much lower wages – think India and other emerging countries with good English proficiency. It may happen at the margin, but it’s not a good long-term solution.

it didn’t work based on what? based on actual productivity, or mid level managers who got their jollies on bossing people around couldn’t do it anymore?

You are correct about the office enticements. My son started a new job in the video gaming industry. His employer offers free food ( breakfast, lunch, dinner) plus free beer ( after 5) in the company tap room. My son , who is very frugal, plans to spend all of his working hours in the office to take advantage of this perk. He has calculated that it offsets the extra cost of rent in LA.

The free food and beer eventually gets old and delays people in their 20s from creating personal lives outside of the office. It also plays a major factor in their not creating “homes” in the places that they live. Probably also prevents household formation.

Although I partook of it in the very beginning stages of all those kinds of amenities, in the end, I think it is bad for society.

My employer would have to offer free MadDog 20-20 in the office, as I’d have to be crocked to give up WFH and set foot in the crime-ridden City of Chicago ever again.

A good manager does not need to measure performance of skilled, educated workers by seeing bodies in seats doing work.

I manage a team of software developers that have been remote since the start of the pandemic. I set proper performance goals, we use JIRA to track deliverables and velocity, and many other KPIs. When you create an environment that motivates employees, you can monitor their work output and performance without being in an office. Our output has arguably increased, since people don’t mind a few extra minutes around the margins to finish things up, and aren’t drained from an hour commute the minute they walk in the door.

At least in tech, your theory about making the office “more enticing” isn’t going to happen. Skilled technical staff realize they don’t need to work in an office, and more and more employers are recognizing it. They’ll choose that benefit over a “communal space” or foozeball table/beer fridge any day of the week.

The world and the technology to enable remote work are worlds different than 2013, and Yahoo was a failing, poorly managed company back then. That’s why they’re worth nothing today.

Overseas outsourcing does not work for a number of reasons. We’ve used it before, between communication barriers, questionable credentials, time zone issues and a multitude of other problems, the determents outweigh any cost savings, which usually disappear from re-work and lost time, anyway.

When the virus subsides, there will be one last attempt to control employee’s lives and get them back to the office while the remaining boomers in leadership try to keep their last grasp before GenX and GenY leaders take over.

I personally agree with your point of view, and I think what you just described accurately portrays a very large group of people’s perspectives (perhaps maybe even the majority?) but to be totally clear and fair, there are many many people who prefer to be in the office. And yes, many of them are younger workers who don’t have a lot going on in their personal lives outside of work, and their primary source of social interaction is at the office. I would say this group of people is probably at or around 20% or less, but it’s still a non-trivial number of workers who like being in the office.

>Years ago Yahoo trialed work from home and it didn’t work. In 2013, the CEO asked all staff to go into the office.

You forgot to tell us how that ended up.

I’ll fix that for you: making people go into the office didn’t work either. Yahoo!’s problems weren’t caused by people were working from home. They were caused by spending billions on acquisitions with no integration plan, no synergies, and no product vision. Turns out when people returned to the office (the ones that didn’t quit), Yahoo! still didn’t have any of that. Yahoo! sold out to Verizon and that division is currently languishing because VZ doesn’t have any better idea what to do with it. VZ does have ridiculous cash flow though, so all that gets swept under the rug.

About 80% of all bank lending is property based. At some point, all this ‘backwash’ hits the banking sector. Are we going to bail them all out? Again. If the Feds step in again, I hope it’s after the washout is over and the prices are sane.

perpetual perp,

A considerable part of this office debt has been securitized into CMBS which are held by investors, such as bond funds. So that’s were some of the bleeding will take place.

That said, some smaller regional banks that are heavily concentrated on commercial real estate lending are at risk, and the former Boston Fed governor Rosengren, now sacked, has pointed that out.

Evergrande have ten days to destroy 39 high rise buildings in China,

the grande relics of the past.

That way bankrupt real estate investors will not be able to jump from the upper floors.

Wolf, one of the other area I haven’t seen discussed here, but it may be in one of your articles, is the so called, “Paperless Office”. The last company I worked for went Paperless just before I retired. We were bought out by a company who was already Paperless (you can print something out, but by the end of the day you shred it), and they brought in a consultant who estimated that some 20% of our office space was taken up by paper records (ie filing cabinets, storage rooms (lots of old junk about), boxes of records in people’s office). So they started to simply move to getting rid of records and reducing office space (besides laying off lots of people). My point here is that Working From Home will accelerate this trend, since to work everything has to be on line. Also, one of the reasons to get rid of office space is linked to becoming more efficient that is working in the new paperless world. Once management starts walking around empty floors occupied by useless records they get the point they don’t need all this office space-just better electronic record keeping. They were right…when I cleaned out my office, I still had files from when I first joined the company in the filing cabinet some 12 years earlier, which I hadn’t look at since the day I joined.

Augusto,

I agree but I’m flabbergasted. Are people STILL talking about a “paperless office?” I thought that was a big topic in the 1980s and 1990s that went away, along with paper, in the 2000s. I’ve been paperless for 25 years. Are there STILL companies out there with file cabinets, and parts inventory on index cards, and payroll ledgers on paper, etc.? I’m just stunned.

OK, I’m sure there is a small company out there that’s still doing everything on paper, and mailing stuff, and filling file cabinets, and their one piece of high-tech equipment is a fax machine, but that’s got to be just a minuscule small number of companies that are still doing it that way.

Old habits die hard lol

Wolf, I think there are still a lot of companies using paper or too much paper. We had over 7000 employees. Yes we did a lot electronically, but people still hung onto the paper and there were still lots of old files around and lots of people creating new paper ones as well. A lot of the older employees and managers wanted the paper, and remember a lot of old guys still rule in the corporate world. They are the same ones who want to “see” their employees back in the office, because they kept working on the Executive floor (with secretaries and IT people right there with them because they can’t operate without them), none of this work from home stuff for them. I remember the new owners of our company had to literally mandate/physically remove filing cabinets from offices and seal storage rooms, to get people to destroy the paper

The younger employees don’t like paper and they will rule soon, so its going to happen…eventually…., but I think there is still lots of paper out there eating up rent, property taxes and heating costs……

I have a county zoning office that changes the color of their permit application forms each year. No shortage of paper work in the

permitting offices I deal with.

Wolf,

I live in the Houston and I would definitely agree with your article and the metrics you have shown here, there is tons of office space available driving around the city and in fact I’m currently working from home outside of a class a office. Office availability definitely looks like 2015 all over again.

I’m in The Woodlands on the north side and there is ample office space for rent. Also, there are a bunch of small strip centers with less that 50% occupied.