The raging mania slows. But it’s still a raging mania.

By Wolf Richter for WOLF STREET.

House prices, instead of spiking by over 2% from one month to the next, and by over 20% year-over-year, spiked by “only” 0.8% for the month, the least explosive spike since January, and spiked by “only” 19.1% year-over-year, the least explosive spike since June, according to the S&P CoreLogic Case-Shiller National Home Price Index today. House prices rose in 18 of the 20 metro areas in the index – by just a tad in some; by a leap in others.

But prices stalled in the San Francisco Bay Area for the first time since June 2020, and in Boston for the first time since February 2020, something we haven’t seen in a while.

“The slowing of home prices is most notable in colder and more expensive areas, as well as middle-tier priced homes where homebuyers may have less wiggle room in their budgets,” said CoreLogic Deputy Chief Economist Selma Hepp today. “Low-tier priced homes are still in higher demand as entry-level buyers and investors continue to compete for the very limited supply.”

House prices have performed truly crazy feats, with prices in Phoenix being up 32% year-over-year, 28% in Tampa, 26% in Miami, 25% in Las Vegas, and 24% in San Diego. But even in those crazy markets, price increases have been slowing.

The charts below show the metropolitan areas with the most stunning price spikes, as tracked by the Case-Shiller Home Price Indices today. In terms of the time frame, note the lag: Today’s “October” data are a three-month moving average of closed sales that were entered into public records in August, September, and October.

It’s not a miracle of houses getting bigger; it’s that the dollar is losing purchasing power. The Case-Shiller Index, by using the “sales pairs method,” compares the sales price of a house when it sells in the current period to the price of the same house when it sold previously. It includes adjustments for home improvements and the passage of time since these sales pairs can be decades apart. By tracking the price of the same house over time, it is a measure of how many dollars it takes to buy the same house, and it’s therefore a measure of the loss of the purchasing power of the dollar with regards to houses, and therefore a measure of house price inflation.

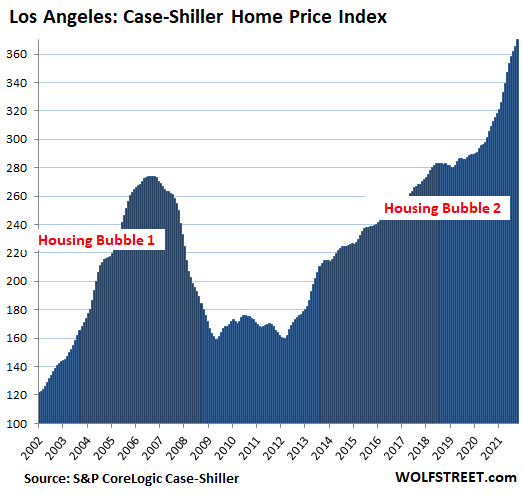

Los Angeles metro: Prices of single-family houses jumped 1.3% in October from September, and by 18.5% year-over-year.

This 270% price increase since January 2000 enshrines Los Angeles as the most splendid housing bubble on this list – the metro with the most house price inflation since January 2000. The charts below are on the same scale to show the relative house price inflation in each market.

The Case-Shiller Indices were set at 100 for January 2000. The index value of 370 for Los Angeles means that house prices have soared by 270% since January 2000, despite the Housing Bust in the middle. By comparison, since January 2000, the Consumer Price Index (CPI) rose by 65%.

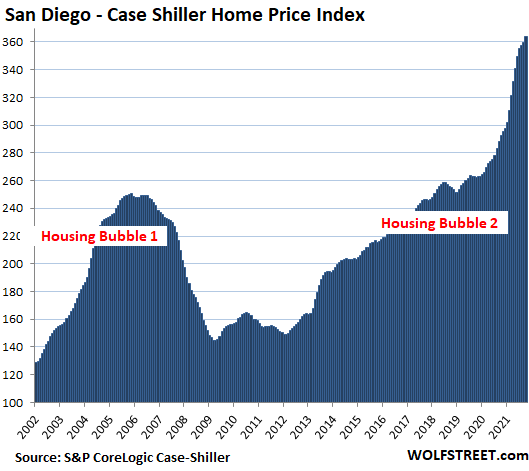

San Diego metro: Prices of single-family houses rose 1.1% for the month, still ridiculous but down from the peak-heat spike in March of 3.4%. This whittled down the year-over-year spike to 24.2%, from peak-heat in July of 27.8%. Since 2000, the index has ballooned by 264%:

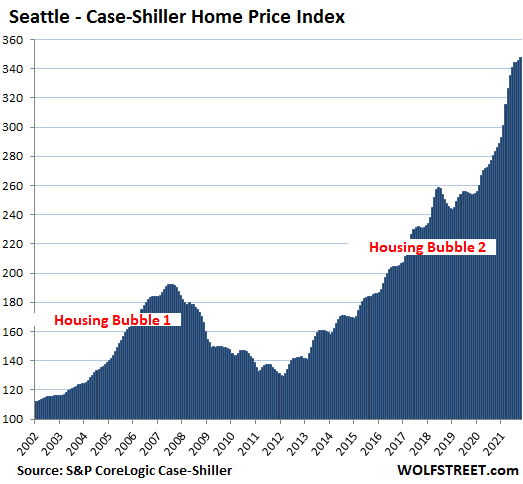

Seattle metro: House prices rose by 0.6% for the month, which whittled down the year-over-year spike to 22.7%, from peak-heat in July of 25.5%. Since January 2000, the index has soared 248%:

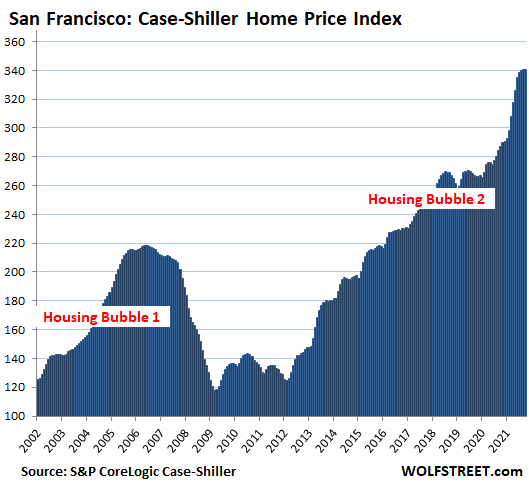

San Francisco Bay Area (counties of San Francisco, San Mateo, Alameda, Contra Costa, and Marin): House prices were flat in October with September, after having inched up just 0.1% in the prior month. October was the first month since June 2020 that prices didn’t move up. This whittled down the year-over-year spike to 18.5% from peak-heat of 21.9% in June and July.

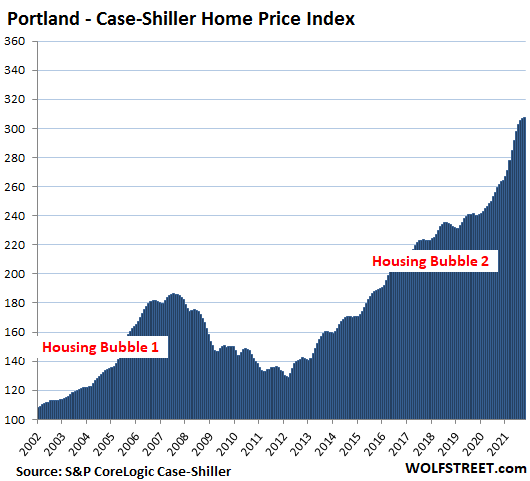

Portland metro: The Case-Shiller index rose by 0.3% for the month, the slowest month-to-month increase since December 2019, which whittled the year-over-year spike down to 17.7% from peak-heat in July of 19.5%:

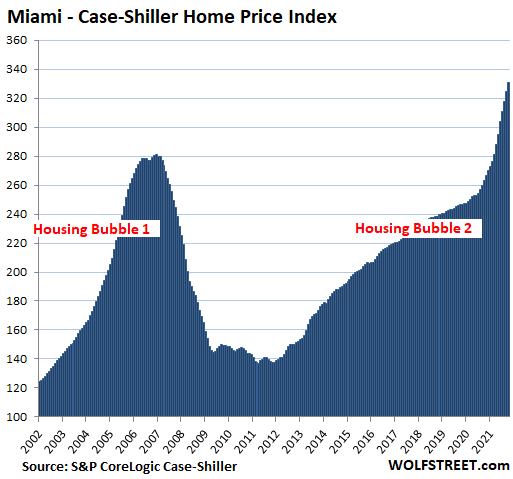

Miami metro: House prices spiked by 1.8% in October from September, just a tad less relentless than in prior months, with peak-heat of 3.1% in June. Year-over-year, prices spiked by 25.7%, the fastest since March 2006 during the peak of Housing Bubble 1, just before the onset of the Housing Bust:

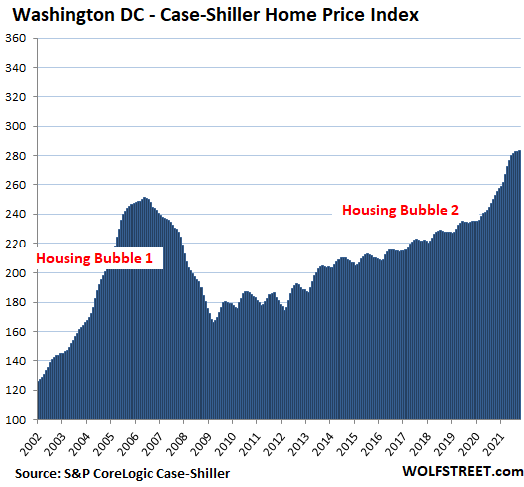

Washington D.C. metro: House prices +0.2% for the month, after stalling in the prior month, which is something that hasn’t happened since January 2020. This whittled down the year-over-year gain to 12.0%, down from peak-heat in June of 15.4%, and the lowest jump since December 2020:

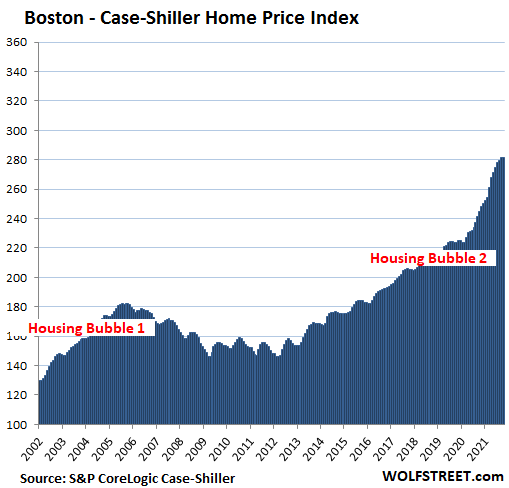

Boston metro: House prices were nearly flat for the month, after peak-heat in March with a 2.6% month-over-month gain. This was the first stall since the drop in February 2020, and it whittled down the year-over-year gain to 15.1%:

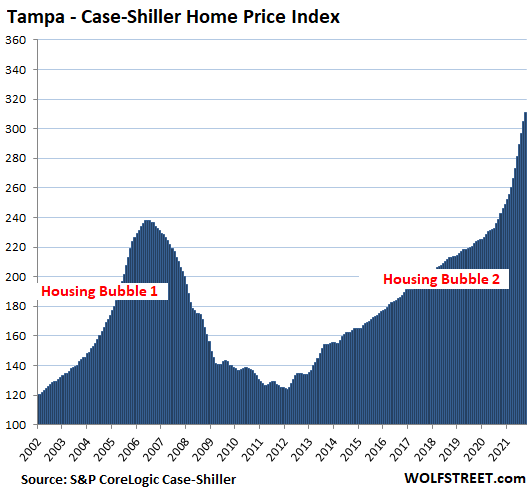

Tampa metro: +1.9% for the month, the slowest spike since February. This pushed the year-over-year spike to a new crazy record of 28.1%, out-spiking even the craziness during the peak of Housing Bubble 1:

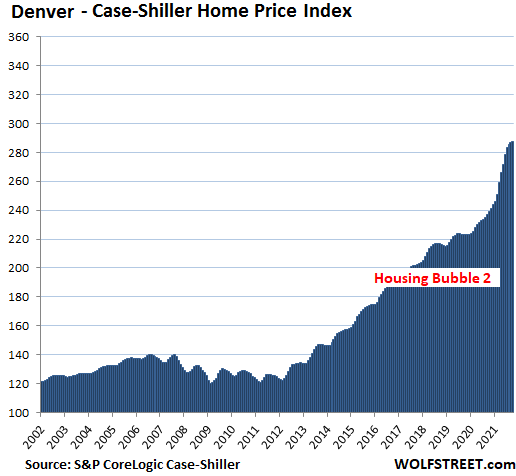

Denver metro: +0.2% for the month, the slowest since the drop in December 2019. This whittled the year-over-year spike down to 20.3%:

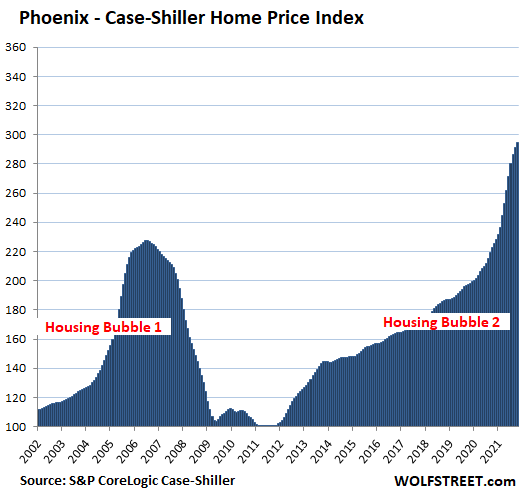

Phoenix metro: +1.1% for the month, the slowest month-to-month spike since July 2020. +32.1% year-over-year, down from over 33% in the prior two months, the red-hottest annual spikes in this line-up of the most splendid housing bubbles, out-spiking the spikes at the peak of Housing Bubble 1, but this time it’s different, no?

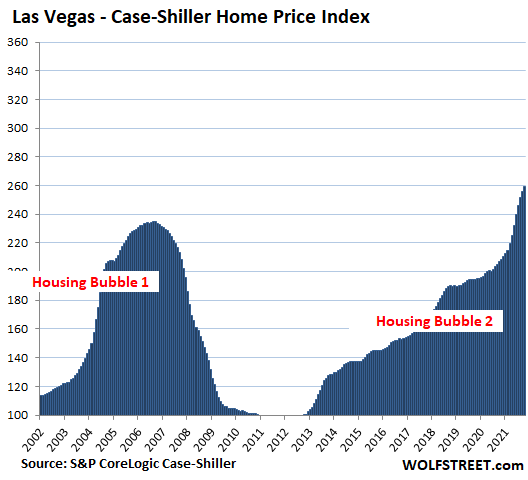

Las Vegas metro: +1.5% for the month, down from peak-heat in June of 3.4%. +25.5% year-over-year:

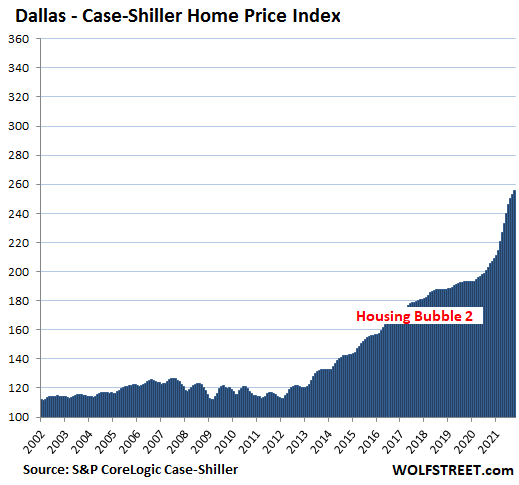

Dallas metro: +1.1% for the month, +24.6% year-over-year. The index is up 156% since 2000.

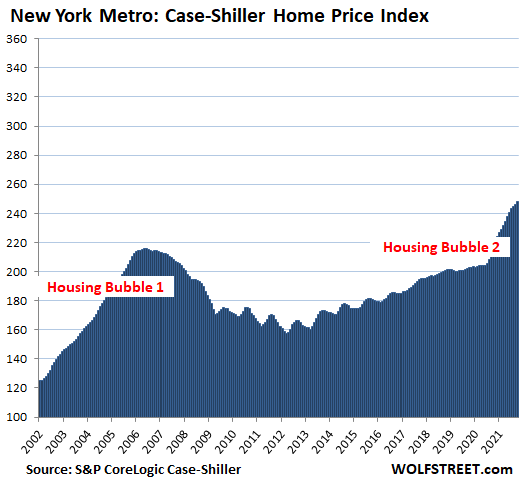

New York metro (New York City plus numerous counties in the states of New York, New Jersey, and Connecticut): House prices jumped 0.7% for the month. The last three months saw the least rapid gains since August 2020. This whittled down the year-over-year gain to 14.6%, the slowest since March. This is a huge diverse metro, that includes some of the most expensive real estate in the US, but also other areas in New Jersey and Connecticut, where house price inflation was a lot lower.

The remaining metros in the 20-metro Case-Shiller Index have house price inflation since 2000 of substantially less than 150% and thereby don’t yet qualify for this list of the most splendid housing bubbles.

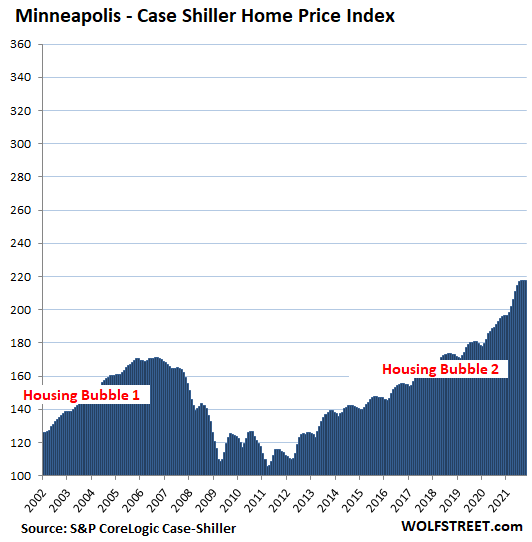

But wait… Minneapolis: This is where, back in April, house prices had jumped 2.3% from March. And now Minneapolis is the first metro where house prices dropped for the month, and stalled for three months in a row, followed by San Francisco, Boston, and Washington D.C. And even if it’s just a seasonal thingy, it would be the first seasonal thingy in two years:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Maybe the population losses at certain silly run cities and the movement to much less silly run cities is also having an effect.

Nah. Your (and maybe my) wishful thinking. House prices SPIKED in San Francisco, Boston, Minneapolis, and Washington DC earlier this year, when the supposed “exodus” was the most fierce. The “exodus” appears to have already ended now anyway.

Also you make it sound like the ridiculous prices in San Francisco, Boston, and Washington DC are a good thing. But they’re not. They drain the economic lifeblood out of the local economy. What these cities need are LOWER prices. And a decline from the current levels would be a good thing.

Over the years, there has been so much demand for housing in this “silly” run city of San Francisco, and so much money, and such high salaries, that house prices spiked to ridiculously high levels. Demand did that — because people wanted to live in San Francisco and they moved to San Francisco and the population exploded.

But if a market is allowed to exist and operate without Fed intervention, high prices are their own worst enemy. Some cities start the house price decline, others follow. During the Housing Bust, San Francisco was the last city on this list to go into bust mode. It may now be one of the first to see price declines.

Yes Wolf, lower house prices would be good, especially for the younger generation. But I fear the Fed will attempt to maintain the status quo, because once prices start to decline things could out of hand quickly.

Watched a good video on John Law. Same as today. Funny money games were conning people out of their hard money savings. Stock bubble blew real estate bubble then too. Before it was over you got the death penalty for doing a transaction in hard money.

Also they were so desperate to settle Mississippi region they would chain a prisoner to a prostitute, declare them married and ship them off to America. No morality for elites when it comes to keeping illusion going.

Let’s not forget the long-standing anti-growth policies in SF, going back to the 1800s to prevent encroachment on rich neighborhoods. This was documented in vivid detail by Fast Company in 2018.

For well over a century SF zoning has been abused in a way that limited population density. Some traditional opponents to multi-family dwellings are changing their minds as the consequences play out. This doesn’t apply only to SF, but SF has been baking this cake since before the Civil War. Other large cities such as those mentioned above have long been gerrymandering residential zoning to benefit the upper crust as well.

See also HuffPo article 2017 saying the same thing.

Michael Gorback,

Yes, yes, and yes, but…

SF has the second highest population density in the US, behind NY City. Multi-family, including lots of towers, is just about the only thing that got built over the past two decades. There is a lot of construction going on in SF. There are about 60,000 housing units in the pipeline. There are huge areas that are now being developed or re-developed, including Treasure Island and Yerba Buena Island, the old Naval Shipyards and Hunter’s Point.

In 2020, during the Pandemic, 4,040 new housing units were delivered, in a city of about 360,000 housing units.

What you cannot do in SF is put a tower no matter where. There are areas where you can put a tower, and there are areas where 4 or 5 or 6 floors might be the limit. You don’t want a tower to go up across the street from your own house, do you? Your neighborhood is not zoned for towers. But other areas are. Same in SF.

And there are high vacancy rates for apartments, rents are down about 25% since July 2019. Lots of condos that are kept as investment properties with no one living in them. Plenty of condos are on the market too. Condo prices have stalled for three years.

There is NO housing shortage in SF. But prices have to come down because this is ridiculous:

And rents:

Gee, that sounds like a subtle plug for Agenda 2030’s action point of abolishing SFH zoning in favor of mixed-use MFH apartments and townhouses and the like. That action point is being slowly introduced under the cover story that SFH is “racist” and “classist” so it needs to be abolished in favor of stack-n-pack rental junk instead.

pj,

Nah, not racist. Just economics. Money. SF is too expensive to build SFH. If you want a new detached SFH with yard, move inland, or maybe down the Peninsula. Or buy something old in SF, but make sure you have enough money. If you want to live near the center, it’s “stacked” apartments or condos, and they’re not cheap either, or if you want one of the few houses in the area, you better be rich.

PJ you are correct. Much of the zoning shenanigans, especially early on, were definitely racist (especially targetingChinese). Just read the history.

Nobody ever seems to mention how Prop 13 encouraged people to hang on to their real estate as long as possible.

And although SF may have a high population density now, city planners repeatedly failed to increase density in proportion to population growth. As Wolf says, multi-family and tower construction has increased but only for about 20 years after over 150 years of deliberate repression. This has been known for probably 50 years and estimated to have trailed projected needs by 3X.

The desirability of living in much of California does not derive from good management. Take away the blessings of its geography and climate and it would be West Oklahoma.

Right now the price of solar has dropped enough that CA no longer requires the level of subsidies it currently offers. As a result, non-solar households are are paying increasingly higher relative prices for electricity in the famously stable power grid known for its rolling blackouts. This inequality has become a political hotspot.

Zoning code has been changed in my town to now allow three-story triplexes on what was single-family areas. From the city’s words:

“Minneapolis 2040 went into effect on January 1, following over two years of engagement with the people of Minneapolis. The plan guides growth with change with fourteen goals in mind, including eliminating racial disparities, slowing climate change, and increasing access to jobs and housing.”

Only little glitch in this policy change, is that this has helped remove affordable starter homes from the market. Now developers come in and buy cheap shacks to do a tear-down & put up rental complexes.

Note the first point the City makes as to the motivation behind the change.

San Frandisco is just scary now. I was attacked by some crazy dude right next to the grocery store. Police showed up 3 hours later. Gave them the pic from my phone, never heard back. Saw bunch of dudes with ankle bracelets on the streets at the start of the pundemic. I think they cleared out the jail.

It’s not “silly” run, it’s criminally run.

andy,

I’ve gotten robbed, attacked, and burglarized in several cities, including Tulsa and Austin. We’ve lived in San Francisco for 15 years, and have had only 1 incident: a thief knocked out the window of our car ($90 to fix) in 2018 and made off with my wife’s lunch bag ($5 value, including lunch) she’d forgotten on the seat. So go live somewhere else for a while and find out what it’s like there.

America is a dangerous violent place. 20,000+ homicides or so a year (of which 50 in SF, one of the lowest big-city homicide rates in the US). Lots of shit happening all the time all over America.

If you want to live somewhere peaceful where practically no one is armed, go live in Japan. It will open your eyes on the violent nature of American society.

Wolf,

Fair enough. I suppose you could host another get together for the readers in SF (once the pundemic is over). I’ve attended the last one, many intersting people. Thank you.

I did hear/read violent crime is almost non-existent in Japan.

Do you speak Japanese? Otherwise, how does one live in Japan for extended period.

andy,

There are a bunch of reasons why I don’t want to live in Japan, and there are a bunch of reasons why I would like to live there. Here are some of the reasons why I would not want to live there:

1. My wife, who is Japanese, doesn’t want to live there. Many Japanese women who have tasted life outside Japan don’t want to live in Japan after that overseas experience. We have a bunch of friends like that. They have very good reasons.

2. At my peak, I was barely able to have a simple conversation in Japanese. Even if I try forever, I will never be able to read in the proper sense, and will always be helpless. I won’t be able to fill out forms, read contracts, etc. Being helpless is a real handicap. I don’t have this issue in countries where English, French, German, or Spanish are the official languages. Many foreigners in Japan are willing to deal with this handicap, and there are ways of dealing with it, and it’s OK, but it’s against my nature to always have to rely on other people (such as my wife) for basic stuff.

3. I love swimming in open water. I swim here in the Bay, and it’s wonderful, and I’m addicted to it, and I need it, and my swim club is just a few blocks away. But it’s something that is not easily and conveniently doable (including a swim club) in urban Japan, esp. now that many waters are contaminated. I mean, you can probably do it somewhere, but if you live in Tokyo, it’s not something that you can just mosey over there when you feel like it and do it.

They have some very nice lakes, for example around Fuji-san, beautiful lakes, but if I swam in them, I might get arrested. There are all kinds of unwritten rules about everything that you need to know somehow, and swimming in open water is something that breaks a bunch of those rules, I’ve already learned.

I live in a city that is considered one of the most violent and with a crime rating of “F.” I’ve been threatened by mentally ill homeless while out walking. SWAT came down our street in the middle of the night and asked for the keys to our backyard gate to search a suspect. Another night, a drunk rammed his car through the front of our neighbor’s house and then fled. We hit an annual record for homicides this August while other cities needed until November and December to make records of their own (I believe all of which were outside CA). I’m thinking if I moved to SF, which I could never afford to do, it would equal an upgrade over my city’s crime rate. But I am perfectly fine living where I am.

As Wolf said, this is life in the U.S. Watch some Japanese street videos some time. You’ll be shocked; people strolling around downtown Tokyo in the middle of the night with no worries at all.

Japan sounds wonderful. As of Dec 20th, my city of approx. 200k had 75 murders.

Wolf – you say you’ve lived in SF for 15 years, since 2006 or so. Are you familiar with what it was like back in the late 1980s and early 1990s? Because to me it seems grittier now, but the same can be said for any west coast city from the Mexican border all the way up to the Canadian border.

That being said, I’ll never forget sitting at a light on I think it was Geary Blvd one Saturday night in 1991 when I heard a man screaming, and I looked over to see him walking into oncoming traffic and towards our vehicle yelling and pointing at his leg. Cars were stopping as he was making quite a scene.

As we drove by after the light turned I could see he had an open, festering wound that was the most ghastly thing I think I’ve ever seen. He was clearly out of his mind on drugs or something, but it’s a memory I will never forget. It was like something out of a horror film.

Anyway, I don’t know what my point is. It’s a neat city but it’s always had some strange goings on. I heard they shut down The Cliff House restaurant which is a bummer. I used to take my mom there from time to time, as well as some old gfs. Great views, great vibe, and some walking on the beach after a meal. The times they are a changin’.

Depth Charge,

In 2019, the number of homicides in SF hit a six-decade low.

I came to SF in the late 1980s and early 1990s on business a few times. Let me tell you, South of Market was an unspeakable don’t-go-in-there place. Now there are towers. Back then, it was dilapidated warehouses. All kinds of stuff going on. On one of my runs, I ended up in there, and it was like, holy shit, I gotta get outa there.

Some old SF hands here will likely tell you that the 60s – 80s were probably the worst by far. The Dirty Harry times. There was a reason why a tough-cop movie was made in SF at the time.

I think the park sevices, or some such agency, refused to extend the lease on the Cliff House. So they closed.

Andy, the birds have finally come home to roost.

SF has had a crazy element pretty much forever. That was once part of the charm.

Visualize sitting in your car at a stop light. A taxi on a side street takes the turn too fast and bounces off the fire hydrant like nothing happened. The look on the old couple, probably tourists, in the back seat was priceless. The onlookers mostly shrugged, but a few of us watching up close got a good laugh!

Americas (North and South) are violent because consumerism and greed takes over everything, family and community values. I disagree with Wolf on Japan, in the sense is not just Japan but is Asia. You can walk through a slam in Jakarta with Rolex and miniskirt feeling totally safe as you can in many places in East Asia. We, westerners, could learn a lot from them if we were just a bit more humble. In the meantime we are paying the price, western middle class has been massacred, indebted and overworked. We could “observe a lot just by watching” as great philosopher Berra said.

Funny, when I was in San Fran for a few days on leave and on my way over to the West Pacific in July 1970 I spent some time in the financial district checking out the scene there and talked to some dudes in suits who were part of the establishment there. I told them how much I liked the place especially coming from a cesspool like NY at the time. They told me the city was not the same as it use to be. I wonder what they meant? What was it like in the 1950’s?

It many times depends where in the city. All cities have rough areas. I am guessing that grocery was in a rough area?

Some builder just leveled a rambler on my block. $675 was the price of the sale on MLS. That would be the land value. They are putting up a 1.7 million dollar home on the lot. This has been going on for the last 15 years. Non-stop construction.

Replying to Swamp Creature’s “What was it like in the 1950s”, I can relate the 1960s to you. Women wore white gloves to go downtown and got dressed up. There was little or no street crime downtown or north of California Street.

Burglaries were fodder for gossip they were so rare.

Local neighborhood men beat the crap out of a guy that attacked a woman on the street in front of Swensen’s Ice Cream. The attacker could barely stand when they got through with him. The word spreads about that kind of thing and people take their criminality elsewhere to bad neighborhoods, the only place that you got “jumped”.

It all began a slow sad decline after the Summer of Love, which attracted wonderful people along with every loser in America to the city. District elections sealed the fate of a civic unity. Then the outsiders began running for local office. Today the city is a dangerous sewer compared to what it was a generation ago. The people in local government are the problem, there is no leadership, no connection to previous values and decency. Today’s small children might see a return to normalcy decades from now, but we adults will never see it. 1/3 or storefronts are boarded up and there are more and more rules and hurdles, so the small businesses that made the city are gone forever.

Maybe the exodus from SF as ended.

It’s the end of december. Out here in flyover, my machinery should be parked, and maintenance and office cleanup should be started.

Outside of friends and family, the phones should be quite.

Not to be. Still digging were I can,

And the calls have not stopped.

The great divide continues.

What kind of business are you in?

Is it possible the “silly run up in” prices for the big coastal cities, and big sun belt cities, is just Boomers fleeing from their snowy residences in the Midwest ?

I grew up in SF and moved out this year. I’ve traveled the world, and I’ve concluded that SF is the most beautiful city with all the accouterments of civilized living.

Like Wolf says, there’s crime everywhere, and the mentally disturbed roaming around can be ignored and avoided.

However, as soon as you want to buy a house or have a gifted child enduring a slow and often hostile public school system, SF and its surrounds become a most frustrating place to live.

SF will always have a bid from the rich, the career oriented, and empty nesters.

The schools are THE problem. No parent who cares about his child long term will subject them to the ever changing experiments, failures and inadequacies of the School District. Private schools are hideously expensive and or full. The kind of people that use their children as props for their failed social ideologies are the exception. “How wonderful that little David learned how to count to ten in Mandarin! Oh, the diversity!

David will either be strung out on Heroin by high school or will have moved to Montana to be a cop. We’ve seen that happen dozens of times among friends kids. Our grand kids go to school in Larkspur across the bridge. Fine public schools in a completely different rational world just twelve miles away.

There is not much product for sale out there, at least what I call somewhat decent product. People are withdrawing from putting their house for sale, why sell an asset that can be bought with printed money, most people think Fed and government have gone berserk on the printing presses.

Its classic textbook, as printing continues, product is withdrawn from the market, prices go even higher, shortages develop, then price and wage controls and eventually black market takes over before we become officially banana republic.

Tinkering with honest money has consequences.

Absolute dereliction of duty from our elite.

Google the term “shadow rate” if you are not familiar with it. The shadow rate has has averaged being negative during the period shown covered by these charts. The shadow rate was minus 0.6 as of Oct 31 of this year.

The question to ask is why is the Fed running a negative 0.6% rate with inflation running at least 6% and leveraged assets like housing running up at a much higher rate? How do you invest in this environment? Why is 10 year treasury at 1.5%?

Also interesting gold has averaged highest price this year than any year in history in the USA at $1799. Last year average was $1774.

US stock market to size of economy is at off the chart record level.

There is discussion going around that because of what has happened in the last couple of years the USA is already at maximum employment and several million workers are not coming back into workforce.

At $1800 Gold is up about double its1980 high of $800. What else can you think of that has only doubled since 1980? Car prices? Housing, health care, energy, education? And consider since 1980 the Wall came down, China emerged, etc etal. That is, many many more people have gained access to global markets and become wealthy. And how much money has been printed since 1980? Yet the pile of physical gold has only risen at 2%-3%/ year. And its supposed value has only gone up from $800 to $1800? Hmmm.

Stockman said the truth around 2009. When you have Zirp you are paying people to speculate. That’s about all you need to know about how we got here.

If it’s all speculation then you must sit close to the exit door ready to head out.

People are fed up with crazy property taxes too many entitlements fire police utilities

It’s “doo, doo, doo lookin’ out my back door” to Indiana from Illinois Chicago metro and collar counties. Cutting the property taxes 80%.

True. Both supply and demand of housing is relatively inelastic. Thus a small change in the quantity demanded results in a larger change in price.

“population losses at certain silly run cities”

Yeah, this is a big myth by right wingers who have bad information and are priced out of California. Cali lost like a tenth of a percent of population this year, hardly a flight.

Of those people, lots move to Texas and then find out they didn’t save any money, and end up paying MORE to live in a flat, boring, uneducated pit of lacking culture.

Yeah, keep telling yourself it sucks here. I’ll take the good weather, jobs, education, and diversity. Who wants to be an isolated bigot?

Somebody is getting bad information for sure.

Just imagine Gomer Pyle U.S.M.C. using the word “Cali”, and you have an insight into the background of some commenters on the local scene.

Comparing recent sales in my neighborhood in Woodstock GA shows a 32% appreciation in one year. My home is a builder grade, 21-year old starter home in a planned community neighborhood with 1,100 – 1,300 SF. We have tiny lots (e.g., 600 SF back yard) and a $75 HOA to maintain 20 SF of bermuda & trim a few shrubs. They are now selling for $300K. My home has doubled in less than 4 years.

It’s beyond silly to say the least.

I live in the ATL metro. I periodically check listings in the heart of downtown Woodstock. The listings all claim it’s condos but the one time I drove there, some look like single detached.

It’s a nice area but I consider it really overpriced. It’s more expensive and in some instances a lot more expensive than more centrally located areas which have been considered desirable for a long time.

I am aware that the distance from the metro ATL core may be the actual reason for the recent price increase, but I can find other areas for more reasonable prices with enough separation.

I’m in Atlanta and flip homes for a living. All RE is local at the end of the day. I think people will pay a premium for nice homes in a nice neighborhood with good schools and good county government. For places like Woodstock, I don’t see a price collapse in the future since people want what you’ve referenced above (distance from the metro area, 1/4 acre of paradise etc). Moreover, specific to Atlanta, are the huge number of institutional investors hoovering up inventory every place they can find it. These people are not going away and not all of them operate like Zillow. Owner occupied housing might have been a historic anomaly since these folks seem bound and determined to buy everything they can buy.

We shall see. Good luck with flipping houses when the market turns. If Uncle Same actually allows foreclosures next time around, you should make a killing. IMO, institutional investors are the wildcard in all of this. They have a significant hand in driving up prices, and they can afford to ride out even a significant downturn.

Institutional investors are looking for returns- any returns. As interest rates tick up 2-3% returns may not be palatable and this money will properly flee. Historically they’re not long term investors especially when markets are or are choppy.

It’s next door to East Cobb & Roswell. In large part, this is what makes it so expensive along with a very good school district.

Be that as it may, it’s bonkers. People’s property taxes & hazard insurance are going up which are notable parts of home & rent inflation that the BLS underreports.

If we could define what makes a “very good school district”, then we can make all school district, very good, and therefore benefit everybody. This will benefit society, etc.

This would make a great Dissertation topic.

Golly, i oghta buy an old wood frame house before im priced out forever from owning a golden albatross craftsman kit.

Cant ever go down.

Amen Otis.

Perhaps what we need is an American Dream Price Index, one that captures the actual costs of Living the American Dream at any point in time. Most of the cost of the American Dream actually isn’t in consumption spending so the CPI is just wrong.

Start with median household income and then price out the Dream, maybe sorta like this:

Item 1) Down Payment (20%) savings required to purchase home “affordable” with payments (PITI) at 20% of median income.

Item 2) Medical insurance

Item 3) Retirement: cost of a lifetime annuity starting at age 67 which covers 50% of median income. (We assume lower expenses in retirement, with the difference covered by Soc. Sec. and Medicare.). Price index uses some suitable percentage of this cost based on assumption that Median Family is saving a little for retirement each year and then using it to buy their retirement income when the time comes.

Item 4) College – 20% of median in-state tuition at state university. Use 20% because median family (2 kids) works for ~40 years and pays tuition for 8 of those years, i.e. 1/5. Don’t include scholarships or loans, b/c the goal here is to measure the system-level cost, not the cost to any one individual.

Item 5) 20% of median price of new vehicle. Use 20% because median American Dream household has 2 vehicles, each of which lasts ~10 years, so payment is 1 vehicle per 5 years i.e. 20% of a vehicle per year.

Item 6) Income and Property Taxes

Item 7) Food, clothing, basic utilities, cell phone etc. This is about the only part of American Dream that’s properly captured by “CPI” (except maybe vehicles) and it’s a small fraction of the cost of the Dream!

They call it the American Dream because you have to be asleep to believe it.

Apologies to Carlin.

I can barely stand to click these articles any more. It’s so painful to watch future generations getting priced out of housing and stock markets, due to faulty decision-making by the Federal Reserve Board and legislators. It’s as if the so-called “leaders” want younger generations to suffer immensely so that older generations and speculators can benefit beyond their wildest dreams.

Here we are, after a 15-20% annual housing price increase for many years straight, and the Federal Reserve Board is STILL buying mortgage backed bonds to further juice housing prices. They are STILL repressing interest rates. Total policy disaster!!!

Yes

But they’re pouring slightly less gasoline on the fire now, so it’s OK.

With all the overpriced real estate, the fed may still be buying mbs because no one else will. I would be curious to see the real demand and the real rates required to sell into “free” markets.

By January, 1/2 of the MBS support from the FED will be gone and rates will have barely budged. We’ll have to wait until all of it’s gone to really get an idea. Based on the 30-year rates charts, it’s unlikely that the FED is suppressing rates more than about 60-70 basis points. Now, it we get the 10-year treasury up around 3.5%, then we may see 5% mortgage rates. However, this will take at least two years, if it happens at all.

disagree. nobody is buying these bonds based on them being a good investment. they just know they can flip them to the fed. i think rates will go up substantially once the “support” ends.

The only MBS buyers with any motive to hold to maturity are pension funds and insurance companies who have offsetting predictable liabilities.

Everyone else is a speculator, as buying 30 year paper of any kind at these rates is financially insane.

100%

RIP free markets…

Bobber: It’s intentional. World Economic Forum Great Reset slogan “By 2030 you will own nothing and you will be happy.” The pricing out of houses for younger folks is intentional to force them into living in stack-n-pack rental apartments and what detached houses they may still have access to will be rental only and owned by a mega-bank. The younger generations will never be able to buy a house with a yard.

Some kids are investing in crypto with the idea of hopefully tuning their backs on the USD. There is also an anti-work movement, if working for money doesn’t land you goods then why work? Figure out how to use the system or skate by. Eventually this will burden the productive people enough to cause collapse. And of course you have all the Fourth Turning theory, that we are close to the end of the 80 year cycle and everything is going to blow up. It sure feels like it.

Personally I want to get the idea of rent strikes going. Convince all the renters to just not pay their rents.

i’d rather just have a galt type strike. if all of the people who keep america running just refuse to show up, the whole country grinds to a halt, with no power, no running water, no food, or nothing else.

You just described Texas last February.

If one does not pay their rent,

they are stealing.

oh no! we know people who steal in this country always face consequences…

There are starter homes everywhere.

People just don’t seem to want to buy them, but notice people live in them right NOW…….confusing.

How are people getting priced out of the stock market?

And yes, the fed should have stopped buying mortgage bonds in September 2020 after it became clear the housing market was not only going to remain healthy, but see a major juice in demand.

Bobber

They are mentally deranged.

When you create a bunch of money out of thin air and put it into the economy by purchasing stocks/bonds/mortgages. The price of those assets goes up immediately. But since no value was created, you’re inflating the price without inflating the future cash flows.

Which assets are first order beneficiaries of this? The very assets the that are being purchased with the new money supply – mainly, mortgages (so housing prices) and treasury bonds.

Second order beneficiaries? Growth stocks because they are already built for high valuations on lower earnings. Once assets like bonds and mortgages are trending in that direction – companies that are literally built for speculation (TSLA to some extent, BTC, ARKK, etc.) skyrocket because they are purpose built to thrive on high P/E ratios.

Third order? Rising tide lifts all ships.

Then once there is an everything bubble and investment assets are maxed – inflation shows up because the economy has literally gotten to a point where a hammer or a loaf of bread or refinished basement or new car starts competing with the future cash flows of investment assets so suppliers rise their prices as demand increases.

^This is where we are now. Housing/Stocks/Bonds are so maxed out that there is little growth that’s left to be found. The earnings just can’t catch up when the value was created by money supply only. So they’re flatlining as traditional investments are competing with just buying things.

Eventually inflation will catch up and P/E and future cash flows will start to look attractive again if assets prices flatline for another few years as nominal prices (inflation) rages.

Higher asset prices go ,more tax revenue very simple ,people make things to complex .tomorrow I will short the nasdaq totally crazy

QQQ 600 EOY 2022

Hussman explains when the government runs a deficit it generates a surplus in the nongovernment sectors. The humongous deficit has to flow somewhere.

The thing that seems to be missing in modern economics is unwise spending of other people’s money is not the same as wise investment. Spending money on hookers and blow is not the same as spending money on improving efficiency in home construction.

You’re describing the broken window fallacy.

That’s why so “much” growth” today is economic waste and it’s not just government spending either.

In the backwards mirror of economic statistics, the country appears richer when it is almost certainly actually becoming poorer.

All these price increases raise the wage needed by the American worker to just get by. This makes manufacturing in America too expensive. The jobs are not coming back.

It is very easy for the jobs to come back.

If you want to sell a product in America, you must make the product in America.

Amazon, Walmart, incompetent small business managers, and weak local governance killed manufacturing. The labor and raw material increases are neutral for the remaining manufacturers because the reason they are still in business is lead time and know how. The price can go up as long as lead times and quality are better than imports. And, imported stuff is also going up in cost. Wages will go up for American manufacturing as making 12 bucks an hour near a big city is not a livable wage it’s poverty.

The Public killed manufacturing in America.

See that hammer for $4 made in America? Right beside it for $3.75 is the hammer from Indonesia, or Mexico.

Which did you buy?

Normal, natural, human behaviour will default you to buying the cheaper one, even if it looks and feels cheaper, since you will justify it.

So, how to prevent or reverse this? We must force each other to buy products made by each other in America knowing we are paying more. But, you have a job and I have a job, but of course we both own less stuff.

Directly, we are the cause.

Indirectly, we are also the cause since we won’t vote in protectionist, nationalist, leaders who put you, and your job, first.

For the last 300-400 years, our desire for Cheap Labor and Cheap Products has destroyed us. China and Japan and other countries have watched us and know what not to do.

I, too, have lived over-seas (I was born over-seas), and the decay and rot in America is so obvious. All for cheap stuff. We produce nothing but paper notes and sooner than latter the rest of the World will stop sending us their products and then we will have hell to pay.

Congratulations my fellow rentiers, we have scaled the ladder of success and pulled it up behind us! Time to light a cigar and watch the little people wail and gnash their teeth in anguish at their broken dreams.

Is this sarcasm, regret, or denial?

Sarcasm, regret, anger, dismay, shame.

It’s parody. He’s ridiculing all those suckers portraying themselves as financial geniuses for pledging to toil away 1/3 of their life for a shack they couldn’t afford, thinking they “made it” and were somehow part of an elite rentier class because of a debt noose they voluntarily slipped around their necks. That proverbial cigar they’re lighting is really a stick of financial dynamite which is going to blow up in their faces. Dirt cheap shacks – they’re coming.

If you deflate Case-Shiller data by a given metro area’s “Average Weekly Earnings of All Employees” then (over the last decade) house prices in Los Angeles have slightly underperformed those in San Fran, Seattle, Dallas and . . . Detroit.

https://fred.stlouisfed.org/graph/?g=KjOK

House prices in Chicago, when viewed in terms of average weekly earnings, are essentially flat over the last ten years.

Maybe workers should demand to be paid in crypto? Some sovereigns like China are beginning to reign in digital, if the Fed made a grand mistake it was allowing counterfeit money to gain acceptance. They liked the auxilary bubble effect, the one bubble they weren’t blowing. Crypto is honest money and dollar policy is a colonialist’s weapon, a liability to domestic users, which their government has to issue script (zero interest treasury bonds) in order to fulfill US trade deficit obligations. Who gets dollars and what they have to pay for them is a giant magic act. Stock market speculators get them free, less than wholesale, third world countries buy them retail to pay interest on their junky sovereign bonds. Then foreign buyers drive up home prices by repatrioting those dollars through the backdoor, and paying a premium to do so. Muni government and GCs smell the hot money and raise their permit frees and prices. Being in the west coast grift zone, I know what I can a build a house for, in dollars – and I know they will never let me do that. Mexican nationals are kidnapped and forced to grow pot in El Norte while the cartel holds the family hostage, but these same people can’t come here and build houses and make an honest wage, and I would gladly pay them in crypto.

Crypto is literally nothing. At least with fiat currency, it’s necessary for taxes and must be accepted for all local currency debts.

Yes, I know an individual “coin” such as Bitcoin is limited but there is no limit to the number of “coins” and no substantive difference between any of them.

The current cumulative value and its current perception is the ultimate sign of an asset mania.

Crypto is, in fact, something. The infrastructure being built on top of Layer 1s and using Layer 2s is exploding with real utility and function. To say it’s nothing is the equivalent of someone in 1995 saying the Internet is just a fun little distraction of no consequence.

Crypto is currently building up to the dot.com bubble stage. When that bubble bursts, a lot of people will have made money and many more will lose money, but the network and connections and redesign of international commerce, online security, data management, and communications will be changed forever. The projects with real value will crawl out of the crater left behind, growing in market share while the vast majority shrivel and die. New projects will come along, and after learning from the lessons of preceding failures, take off running.

I plan to always keep crypto assets because crypto is global. When the dollar loses hegemony, as it inevitably will, I suspect crypto will become a surprising safe haven for those with the foresight to DYOR and see its worth.

There’s a difference between Bitcoin and blockchain in terms of value. The former really has no value unlike the later. As for the rest of your points, there are a lot of what ifs that have to happen, and there won’t be one dominate blockchain based crypto. All the major countries will develop their own crypto. If I got into crypto, it would definitely be China’s. In 2030, the FED & Treasury Dept will probably still be evaluating it for use within the US financial system.

Crypto won’t ever be mainstream until the average person can use it effectively and in a SAFE manner. Right now it is for the tech heavy folks who have the means to protect it.

Comparing the internet to crypto is ridiculous.

Any future government crypto “coin” is fiat currency. It didn’t change.

Anyone can create a new “coin” any day of the week.

Bitcoin has name recognition and first mover advantage but that doesn’t make it worth $50K. Its value is due entirely to speculation, as in over 99% of it,

Blockchain is a terrible solution to the distributed transaction database problem. Inefficient, slow and non-scalable.

The problem with cryptos is they are benefiting a few who get in early.

I could get behind a crypto that was given out fairly but none of them are. You usually have the top 5% of the crypto owners owning 90% of the cryptos.

In my mind this is why most will fail. That being said, money talks an whatever crytpo conglomerate can pay congress via political campaigns may have a shot. I would not be surprised if congress member start getting early allocations of cryptos.

Wait until you find out about the market in fine art!

Really good fakes abound.

It is going to be interesting if there is a Cyber Attack and the internet is shut down for some time.

How much will Crypto be worth?

An EMP? How much will Crypto be worth?

A Carrington Solar Flare Event? How much is Crypto worth?

Crypto does not even exist. At least paper currency exists. Gold and Silver really exist. But Crypto?

When Texas has their next deep freeze and no electricity for a week, or more? how much is Crypto worth?

Brown-outs or Black outs coming to Green California? How much is Crypto worth?

In the event of an EMP or a solar flare, I think we’ll have a lot more to worry about than how to pay for things. I mean, that would be the apocalypse, right?

Here’s the thing about crypto, the ledger is global. If there’s a cyber attack or an EMP and the U.S. is suddenly sent back to the pre-electronic age your crypto will still exist in Europe or Asia or anywhere else you can find a way online. As long as you still have your wallet’s seed phrase safely stored in the real world on a piece of paper or engraved on a specialized steel blank or committed to memory. That phrase IS your crypto. You can hold it in your hand. It’s just not accessible unless you are online.

The real problem with an EMP would be getting out of the U.S. and back to civilization since almost nothing would be functioning. Your argument about digital money could equally apply to banks. I don’t think WF or BOA will be working any more than the localized Internet that would let your access your crypto. It’s not going to be like George Bailey with a stack of cash doling out whatever fractional reserve is in the vault.

You’re right, though. Perfectly sensible to have cash on hand in the event of a natural or manmade disaster. Cash would also probably be good for the first couple of days after an EMP until people finally figured out that the U.S. no longer existed in its previous form. After that, how much will a printed dollar be worth? Gold and silver are a whole other conversation.

The last thing I would do is abandon the U.S. dollar and switch to all crypto (least of all Bitcoin, since I’m not a Bitcoin maxi). Crypto has probably another decade of development to go before it functions and is adopted as a form of currency. The volatility will need to calm down significantly first.

I’m just saying I like having a reasonable percentage of my funds invested in it and the technology rapidly being built on top of it.

As a worker, I sure am peeved at the way inflation has caused the purchasing power of my earnings to go down by at least 7 percent in just a year. To escape this, I think I’ll demand that my boss pay me in a medium whose purchasing power, such as it is, can easily go and has recently gone down by well over 10 percent overnight.

Problem solved!

A one bedroom apartment rents for $1800/mo. My HOA fees are close to $300. It is nice to own my own home. Working for the landlord was not a good deal. It is a good time to have a home paid for and sell it not.

.8% per month inflation is 9.6% annualized inflation.

Over the last several years our HOA has increased rates at the maximum allowed by the bylaws. Currently what started in the $200/month range is now $474/month. So expect HOA fees to feel the squeeze of inflation as all the items that go into the monthly statement are increasing with WTF cadence.

Having worked in a public corporation I know that they tend to be brutal regarding managing costs. Consumers need to be tough too. Try not to be a price taker. As a consumer we have 50 states, each with many jurisdictions. If you are getting squeezed where you are at, do your research on a better economic situation to see if it is worth the hassle of moving.

Most people live where they must or are limited to a low number of options.

Still, there is a reason most places don’t attract more people. The place sucks.

I’d move to another country given the choice than live in most of the 50 states.

a lot of people live where they do simply because their family and friends are around, which i think is a poor reason to pick a place.

in my opinion, the northeast objectively sucks. bad traffic, bad weather, high taxes, crowded, high costs, but people still live there.

Technically, with compounding….it’s 10%

Don’t worry, the Americans just have to elect Justin Trudeau and that evil witch Chrystia Freeland, and they will bring in millions of money launderers to prop up the real estate bubble.

America should not tolerate money laundering plain and simple.

Gen Z, ever wondered why America is rated one of the most “effective” anti-money laundering regimes according to international “standards” but even the State Dept admits the reality, labeling the US a “major money laundering jurisdiction”?

https://www.state.gov/2021-international-narcotics-control-strategy-report/ (at Vol II, p14)

The global AML regime is designed so badly and is so ineffective that it has “less than 0.1% impact on criminal finances,…[with] banks, taxpayers and ordinary citizens penalized [vastly] more than criminal enterprises”.

https://doi.org/10.1080/25741292.2020.1725366

Despite constant “reviews” that never review anything meaningful, forever tinkering to be seen to do “something” while preserving ineffective status-quo in perpetuity [recent, upcoming: Canada, US, AU, NZ, UK], real estate remains a great way to launder criminal funds, in those countries and more – with US, UK, Canada leading enablers.

And with high prices, all the better to launder more. So, rampant Fed money printing helps another elite, boosting criminal enterprises’ 1990 (FATF) charter to print money. “Thanks Jerome,” say Criminals Inc, “rate repression and QE to infinity and beyond!”

Next book on my list is:

“American Kleptocracy: How the U.S. Created the World’s Greatest Money Laundering Scheme in History”

by Casey Michel

The pandora papers begin to explain how loose trust laws in some western states have created perfect opportunities for international robber barons and oligarchs to store their wealth in USD tax free. What a country.

Selling your home for the big profit and buying an RV on Roids is no better. Lot rent fees are expensive and so is gas / maintenance / insurance.

And construction quality on an RV is sketchy to begin with. Even with decent construction what do you think it does to your house if you drive it around at high speed?

Yeah, it would be tough to keep the turntables dead-level and stable I reckon.

I’ve seen pictures of turntables in 1950’s cars. 16RPM to play longer. Wonder what materials were used for the stylus and cantilever. Like the Elcassette, read about but never seen one in the flesh.

Rvs, unless you’re talking about high end Class A motorhomes build on a bus chassis, are overpriced garbage. They make single wide trailers look high quality by comparison. It’s not only the materials, but the execution. You’ve got minimum wage lackeys assembling balsa wood on wheels.

1. People are taking a breath before starting the next round of buying.

2. Families buy and move in on summer. Kids have schools on other times. Once the spring semester is over, time to buy and move in.

3. I am not doing technical analyses but these graphs looks like two mountains. The larger one near a smaller mountain. The larger mountain has more room to grow.

4. Something hasn’t happened in Washington DC area. Yeah, there is no more land to sell-buy. Everything is owned by the Feds. Most employees are in WFH until 2025. Feds will sell their buildings to ease the housing crises.

5. Most of the current generation will be renters. The current house-owners will end up owning 5+ homes.

6. Most houses are investment properties and second homes. So even if younger and working population moves out, investors from foreign countries will still buy homes and keep it their portfolio. Later when their kids come for the medical degree in a state university, they can save money on rent.

Applying technical analysis to residential housing makes absolutely no sense. It has no predictive merit whatsoever.

Most houses are not investments. That so many believe it is another sign of an asset mania, especially with the prior bust which was less than 15 years ago. The structure is a consumer good like a toothbrush, just with a much longer shelf life.

Apperantly you never owned rental property great investment do research u will understand

apartment buildings and commercial properties can be great investments. single family houses almost never are. if you buy a single family house as an investment, there’s a good chance you’ll lose in the end.

Every single landlord I have ever known who rented single family residences was losing money after figuring vacancies, non-payment, maintenance, repairs and all other expenses. The happiest days of their lives were when they sold them. Their stories made boats seem like a good investment. Most of these people are doing it to capture the appreciation, then bail.

A rental property is an investment. Read what I wrote.

augustus, yes, a rental property is an investment if you your rental income is covering your costs plus a return. but buying a rental property purely because you think it’ll appreciate in value is a greater fools investment.

Jake, I bought a SFH in 2010. 7 years later half of the purchase price was paid by rental income. Another quater has been paid in addition. I’m getting a free house. Not a bad investment.

Oh by the way, it also has quadrupled in value, no joke.

yes, you happened to buy at the very bottom. you are either very prescient or very lucky. but no one here has a time machine. the question is not whether buying a sfh in 2010 was a good choice in retrospect. it’s whether it makes sense to buy a sfh today.

I was addressing the statement that “if you buy a single family house as an investment, there’s a good chance you’ll lose in the end”. Simply not true for most people that do so. Why else would Blackrock, Invitation Homes, American Homes 4 Rent, Progress Residential, Tricon etc. be gobbling up homes?

Obviously timing and strategy are important and some make bad decisions. But overall, in the last 20 years It has been a great investment, and the last 10 have been incredible.

it simply is true. most people will never get enough from rents to make it worthwhile. the appreciation from the past 20 years is due to interest rate suppression. it can’t go any lower.

I remember 5 years I would tell people on housing forums I was investing in flyover real estate. It was clear as day to me that money would flow there next. I bought a SFH rental and all the housing perma bears gave me grief, claiming I was either a troll or a real estate agent. One pandemic and endless bailout later, and volla! The house is almost paid off and has gone up 30% in two years. Sold my big house and moved into the little rental, probably be paid off next year. Little town of 40k people, no mugging, no looting. Now I am out of everything and will stay this way until something changes.

… graphs looks like two mountains

How about the left shoulder and head of a head ‘n shoulders pattern. You have to have a cast iron stomach to buy now or in the near future.

Can bubbles really be considered bubbles after 20 years? Really??

Happy Home Owner,

LOOK AT THE CHARTS: Housing Bubble 1, Housing Bust 1, Housing Bubble 2, and…. ?

Wolf, time in markets beats timing the market. As a longer term holder of US assets for over 20 years my portfolio of equities and [SF Bay – Peninsula] real estate doesn’t see a bubble. If you go back far enough all charts move toward to the top right corner. Your charts do the same.

OK, we’ll have another discussion on that in a few years.

Its not a bubble until and unless it burst.

We’d see if it burst.

yes, over the long run, america’s economy was growing. now it’s not. so any future gains can only be from multiple expansion and inflation, not growth. not sure that counting on that is a winning investment strategy.

It’s a bubble because it’s based upon artificially cheap money and artificial demand. In a global economy, it can be argued that certain markets (such as SF and Manhattan) aren’t in a bubble because of increased mobility and capital movement, but this can’t apply to housing in most or all of an entire country.

People need somewhere to live. That’s what residential housing is to the homebuyer, not an “investment”.

In a non-distorted market, no product (housing) can be priced above its customers (house buyers) ability to pay indefinitely much less forever.

It’s only where government distorts a market that this seems reasonable. That’s what’s happened to medical care, higher “education”, and housing in the US.

It’s a scam, all of it, to make wealthy people even wealthier and keep us struggling.

I’m going to slack off at my job til they fire me then I’m out of the workforce and taking up cardboard signs. $1600/healthcare premium and $2200/month rent. I work for those 2 things. Can’t even save for a house. Why even try? It’s pointless. Save a couple hundred a month while prices go up a couple thousand a month. Fuck this.

Van life. We’re all going to die. Why struggle for these things. It’s sad isn’t it.

The Fed has done a wonderful job ensuring that younger generations will mostly spin their wheels in the mud trying to afford a piece of America. Even if you do the historically responsible thing and save, the cost of the assets you wish to purchase outpace any savings rate.

We’ll deserve it when they vote populists in in 15-20 years to redistribute wealth. That is if they don’t start blowing shit up first.

“Fuck this” is the correct sentiment

it won’t be 15-20 years. we’ve seen this sad, bizarre and predictable sequence play out throughout history. batista’s cuba was a hotbed of corruption and crony capitalism which ultimately led to castro.

the younger generation is going to want to just burn it all down. the elite are very myopic if they think their ill gotten gains are going to survive what’s coming.

You have every reason to be angry, SOL, and I feel for you and every other person in the situation. What they have done to you and all of the young people in this country is criminal. They are stealing your future to pad their bank accounts – rendering what would have been your future wealth into zeros on the end of their balances.

DC, the exact same thing has been done to you. Your future was stolen, but like the slow-boiled frog you never noticed it. Neither did I until I started reading about medieval and Renaissance trade, such as the invention of letters of credit, why they were such a great idea, and what structural changes were required. But the changes didn’t happen overnight.

This blog is constantly populated with short view comments that assert what’s going on is new. It isn’t. It’s simply another step in the evolution of the financial system. Maybe the steps are getting faster. Setting up letters of credit took a lot longer than today, where you wake up one day and wonder what the heck is an NFT?

As the unicorn beer mug says, nothing goes in a straight line. Along the way we have had Magna Carta, the birth of the USA, the South Sea Bubble, the French Revolution, the rise and fall of Communism, the breakup of Standard Oil and all sorts of blips but the main story thread is never broken The Rothschilds loaned money to both sides during the Napoleonic War and got rich whereas the Romanovs were exterminated.

I am still waiting for the big black box that says “This is not something recently cooked up in the past 10-20 years by evil idiot bankers. It’s been business as usual for millennia, sometimes by evil idiot bankers but usually evil intelligent bankers and financiers. The procedures have been refined but the core principle has never changed.”

“DC, the exact same thing has been done to you. Your future was stolen, but like the slow-boiled frog you never noticed it.”

That’s not true at all, Gorback. Why don’t you stick to things you know?

I’ve been talking about this since the 1990s. I cannot stand Paul Krugman, but back in 2002 he had a piece in the New York Times called “For Richer” that talked about how these modern-day robber barons were building more mansions than back in the days of slavery as they were feeding off the carcasses of the once middle class. This was of course after the dot com bubble had burst, but well before the insane housing and everything bubbles we have now.

The repeal of Glass-Steagall was what really threw kerosene on this inferno. Unless there are material changes to laws, and some reform of the FED and the political system (campaign finance in particular), nothing’s going to change.

The Fed DOES have three mandates…and the third is often not mentioned because it is just one more mandate ignored. From the official Federal Reserve site..

“The Federal Reserve Act states that the Board of Governors and the FOMC should conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.””

Moderate long rates. Moderate, in the Queen’s English means not extreme, neither too high nor too low.

Record low historical rates is therefore “extreme”.

This makes the Fed in constant violation of two of its three mandates. The other, Stable Prices, is in direct conflict with a 2% (or more) inflation goal, running near 7%. Maybe the Fed should get a dictionary. Moderate means “not extreme”. Stable means “firm, steady, unfluctuating”.

Depth….it is the 3rd mandate, now impossible to find on the Fed website or in any Fed publications…..moderate long rates……that was in place to PREVENT the pulling forward of future wealth via cheap longer maturity debt creation.

Remember all the talk about the flattening yield curve and how it predicted no inflation?

Remember people declaring the Fed couldnt control long rates?

Both proven false.

Former Fed Gov Fisher, in the PBS documentary “The Power of the Fed” admitted the Fed flattened the curve to FORCE (his word) investors to take more risk. That is a remarkable statement to me.

And part of the mechanism to do this was the $40 billion (40,000 million) a month of MBS purchases which still proceed yet at a lesser pace.

Historicus. You need to wake up (is that “wokism” ? ) and realize that the Federal Reserve’s “mandates” are just a bunch of meaningless arble-garble window dressing.

ghost

I am WIDE awake

and this is NOT how it used to be NOR as promised

What you’re saying is really the core of the problem.

The destruction of the working class. Slowly and surely.

By inflation stealth.

For the benefit of the banking class owners.

That was always the purpose of a central bank.

Feudalism.

We haven’t seriously looked at buying a house since the financial crisis. We actually love renting and pay a reasonable amount for a 4bdrm home. I did start looking at homes online in our area and was shocked to be priced out of the market. There are homes in the 200k’s, but they are either going in days or are dumps. There are homes $400k and up and even those are going fast. You almost have to pay more to escape the crime. I refuse to pay that much though. Apparently we are the capital of dreams. Seems more like the capital of screams.

Not sure what market you are looking in, but 400K for a home is considered extremely cheap by certain standards…

Early this month I made the drive ( in a uhaul) from PDX to LA on I5. I had not done that drive for 20 years. The big change that surprised me is that at every highway interchange in Southern Oregon and Northern California there were now huge RV Parks. These were not the KOA’s of my youth where people stopped in for the night in campers and 17 foot travel trailers. These were permanent communities of people in 40 foot fifth wheels, etc. My guess this the in-between for many retired folks who are priced out of a house and an apartment but can scrape together the 40 grand for a trailer and the few hundred bucks a month for a permanent campsite. The folks who had modest retirement savings chewed up by JPow and his buddies.

Watch “NomadLand”.

There are also a good number of those in WA state as well

Great article.

It is the same story across the entire developed and semi-developed world, from Australia to Europe to California.

Everyone has realized *leveraged property is an easy way to make money*.

Much easier than building a business.

Global culture has changed.

Borrow $500k. Stick it in a nice house. Refuse to sell. Sit on it for 5-10 years. Low risk. Put it on the market at 5-10% above current values. Sit tight and wait for the cash to roll in.

“Nothing can save a group of people determined to suddenly grow rich.”

Worst time in history to try to do that. People learned nothing last time. GREED will be their downfall.

Yep. Leverage cuts both ways. I guess people have forgotten the lessons of the GFC.

As long as the Fed pegs the mortgage rates at half of what they should be, and well below the inflation rate, real estate will draw speculation money.

Last time we had inflation even close to this level, acutally much lower

1999 and 2006, 30 year mortgage was 6%, now 3.1%…..

why is the Fed STILL BUYING MBSs at all? Who benefits?

“It’s not a miracle of houses getting bigger; it’s that the dollar is losing purchasing power.”

I measured my house last year with a cotton ruler. This year I washed and dried the ruler and presto my house was 27% bigger.

Thank you Wolf for this magnificent site.

I’m building a house on 10 Ac in rural NE Iowa- beautiful country, but a little chilly. I own a home in a quaint little town I bought two years ago for only 150k. Just got a CMA and it’s now worth 240k. Almost anything hitting the market is pending in under a week. I just hope it doesn’t roll over before I can get moved into the new house and sell the old one.

It is not worth $240,000.

The $1 bill in your pocket is worth 50 cents.

You sort of made the point why the house could be worth $240k. Lets say two years ago his $150k of dollars in his pocket is now only worth 75k. That means to buy the same physical asset like a house today would cost him twice as much. So a $150k house 2 years ago would cost $300k in todays dollars. The house assets appreciated against the dollar.

So if you look at Wolfs charts, what would they look like normalized? Maybe they would not look so dramatic? I am not sure if these charts are normalized against inflation.

Traders are going to give a big bite to the $3T bait, while the

whales are selling at peak.

Home buyers feast on Case / Shiller baits, stuck in their throats.

Fed is running extraordinary unconventional policy, so anyone with assets is flying blind on their future value as the future value is unknowable. Not a way to run a country.

Housing goes up over time because the dollars value goes down. It’s really simple. Was watching an old Bogart movie ” dead reckoning” last night. He mentioned a house that was 5K before the war was now 15K ( 1946). Our wages haven’t kept up hence our standard of living has declined.

‘

‘

I was watching a Chinese English language news program in 2020. They locked down cities. When they reopened, the price of everything had gone up.

There’s a little more to it than that.

Take Seattle or SFO for example: The topography limits the amount of buildable land available in those markets. Once the easy parcels are built upon, the difficult to develop parcels drive the cost of construction up. Those on the easier to develop properties benefit from the cost of construction increases of the newly developed properties. The limitations of buildable land, coupled with high income potential, drives the insanity. There’s also the NIMBY crowd that wants to protect their views and exclusivity that lobbies for zoning restrictions that make additional development financial suicide for the average Joe. Been that way forever.

However, if you have acres upon acres of farm land that can be plowed under and developed on the cheap, the costs don’t traditionally rise as quickly.

The Bogart movie you describe: What events could have created the environment for housing demand and prices to increase substantially at that point in time? Could it have be the soldiers returning home from war and wanting to start families? The fact that most other industrial countries were bombed back into the stone age and jobs were plentiful? That’s how developments like Levittown, PA came to be. Quick tract whacks to satisfy the seemingly insatiable demand for housing. Cheap land outside the urban core that could be quickly and inexpensively developed.

Omi is spreading in China. China is locking down, because ShiShi have zero tolerance.

Meanwhile US & British fleet sail in South China Sea. ShaSha ShiShi.

On a very related note, good news out of Wall St., Jimmy Cayne the former CEO of Bears Stearns is dead. His obit rehashes his behavior in the years before the demise of the firm, his being mostly absent, out playing cards, and his “reputed” use of weed.

I have a different take on his behavior. I think he knew back in the 1990’s, like I did, the firm was skating on thin ice. To me, he checked out early and waited for the ship to go down, it just took a lot longer than anyone anticipated. Even at the end, he couldn’t be bothered sticking around to negotiate the takeover. Good riddance to both.

The message in this story is, these guys are not looking out for the clients, they will ride the ship till it crashes, cashing out along the way. He left the firm with hundreds of millions, everybody else got screwed.

Professional management, huh? Yea, right! (sarcasm)

Honne y Tatemae

I just spoke with my sister and her husband last night about their experiences in the San Francisco housing market. They are both doctors and moved there in 2018 from Asheville, North Carolina. They love the city but cannot find a home to buy. I mentioned this earlier this year and Wolf told me to tell them to “just keep looking.”

After last night’s conversation it sounds like they haven’t figured out what they want from a home though. Do they want the “high density” experience where they can walk to their work, store, barbershop, etc. Or do they want the house with a lawn and garden experience.

Decisions… decisions. From the looks of these charts EITHER decision is going to be expensive in San Francisco.

The number of listings in higher end east and west coast markets that I watch continue to decline. Historically, there has never been so few listings, and they continue to drop.

Imagine the spring when buyers bid on the few listings left. This will be a shocking bidding war event. Buyers that decided to step back earlier this year really screwed up.

In SoCal, small old beach city homes in great locations jumped 1M dollars in less than 1 year. Laguna, Manhattan Beach, Malibu, Santa Monica, South Redondo, The Palisades, Newport, CdM … just impossible to find a good location with a yard for much less than 3M.

As far as Boston goes, it is the same story in the single family housing market. Crazy bidding wars on SFR during the holidays. Boston has a large number of condos, and those are slower … personally, I hate condos, and I just don’t know if condos will work … too often, buying a condo or townhome in a fast market is a disaster..

One more Boston comment … since 2008, snobby Boston realtors just trash talked high end Boston suburbs. They said dump those suburbs and buy an expensive condo in the city. And, like a bunch of lemmings, many did just that.

What a mistake that was. Those same snobby realtors are trying to reboot that dump the high end suburb story … screw them. This time, it will not work. They can eat those downtown condos. The smart money is back in the high end Boston suburbs.

Who listens to Realtors, much less quotes them? Realtors are LIARS, first and foremost. They make used car salesmen appear to be men of the cloth. They are like a bad odor that won’t go away – financial leeches who suck away a cut of every house sale while doing nothing for it. These people are useless. I have no idea why they’re even still around.

You really should cut down the visits to the Housing Bubble Blog.

DC

Agreed

I’ve uses Realtors a half a dozen times over my lifetime. 85% to 90% are liars and are lazy, dishonest and incompetent. Most of them I fired before we got to the settlement table. There are a few good ones’s out there. I haven’t found one unfortunately.

I spent a lot of time in New Hampshire back in the 1980’s. People were already leaving Boston back then and moving over the border. NH is really nice, a lot cheaper, and only 45 minutes from Logan Airport in Boston. NH must be a lot less rural these days.

I just read if the Ice Shelf in Antarctica breaking off could raise sea levels by 10 feet in a short time. (i do not know if this is a valid claim or not)

It will be interesting how beach front property gets affected.

Watching the frenzied bidding wars on SoCal stucco box tract houses this year has been incredible theatre. Auction events for even the most mundane items on Ebay or on cruise ships results in a highly charged emotional response where logic and rational thought take a back seat. Imagine the complete evaporation of logic and the recklessness involved where the item is not mundane but instead involves the most emotionally charged purchase regardless of whether a bidding war is underway – the purchase of a home. There is an entire sector of psychological study dedicated to the subject.

I’ve been on the fringe of bidding wars many times in my life, and never engaged. And never regretted not joining the fray. Never wished I would have outbid the high bidder. Some may have a different experience – congratulations to them.

The only thing more astounding than the ever-escalating sales prices we are seeing is the fact that anyone thinks this can possible end well.

There is market listing and private pools that that belong to certain

agents, specialized in certain areas or buildings, for qualified buyers only.

My prediction: shortly after the first we’ll see several houses come on the market starting in the “low 1’s” in central San Diego. They’ll get snatched up in a frenzy of panic buying by the FOMO crowd. This train ride is gonna go for a while, but we’re in a very unhealthy market that won’t end well.

Is there some significance to this being tagged as “Federal Reserve” and not “Housing Bubble 2” like the previous monthly updates or is it just a typo?

Yes, the significance is that I checked the wrong box :-]

I just got my tax assessment on my house. It went up 20% from the last assessment three years ago. I’m going to appeal it. They just want more money from me to waste on useless government programs in the county.

And of course the cost of those useless government programs has likely gone up by 20% over the last 3 years due to inflation, especially the cost of funding all those inflation-protected local government worker pensions in the era of financial repression.

Sounds like you lucked out since the market price of your home has likely gone up by a lot more than 20% over the last 3 years.

Due to WFH etc. where I live, most commercial property seems to be available for lease or sale so maybe the local government is no longer able to raise sufficient taxes from commercial property so needs to compensate by raising residential property taxes.

Dont look at Bubble 1 because it’s not really Bubble 1.