But on the surface, stocks still look hunky-dory.

By Wolf Richter for WOLF STREET.

It’s amazing how individual stocks, at the tippy-top of the biggest stock market bubble in modern times, are getting taken out the back one by one to be crushed, but without denting the overall indices all that much.

The stock market bubble was driven by $4.5 trillion in QE in the US alone, along with many more trillions by other central banks, and it was driven by interest rate repression, even has inflation has been surging to multi-decade highs, not just in the US but globally, and not just in goods, but now also in services, particularly housing, such as rents.

After a decade of QE being relatively benign on the inflation front, giving central bankers a false sense of confidence, it has finally broken the dam, and inflation is now surging everywhere, and it’s spreading across the economy.

Central banks are now no longer denying it, and some have raised rates, and others have ended QE.

Even the Fed, which engineered this money-printing orgy and is very slow in ending it, is now ending it, and it will be raising rates, and everything is moving faster than expected, and suddenly the orgy is over.

Each stock that crashes has its own story for the crash. What they have in common is that they were all ridiculously overvalued, and investors knew it, and they kept hanging on till the last moment to ride them up all the way, but they were sitting all bunched up near the exits, and when the signal came, they all rushed out together, causing those shares to collapse. But even at those much lower valuations, those stocks are still ridiculously overvalued.

DocuSign, a company that still had a market cap of $46 billion on Thursday at the close of regular trading, valuing the company at 20 times its 12-months trailing revenues, despite having lost money every year of its existence, plunged 42% on Friday during regular trading, after it had announced that its revenue and billings growth would slow as “the environment shifted more quickly than we anticipated.” Shares are down 57% since September 3rd. Yet, shares are still ridiculous overvalued, trading at 14 times revenues.

Housing-sales-related stocks got crushed.

Zillow had some good news, well sorta, on Friday by promising a big share buyback as it is unwinding its house-flipping business and selling the thousands of houses it got stuck with largely to institutional buyers. Upon the announcement, Zillow’s shares [ZG] jumped 10% on Friday, which whittled down their collapse since February to 71%.

Opendoor [OPEN], another algo-powered house-flipper, has collapsed by 61% since the peak in February this year, only months after its IPO via merger with a SPAC in December 2020.

Compass, which bills itself as a tech company but is a real estate brokerage, went public in April 2021. Over the eight months since then, its shares [COMP] have collapsed by 53%. Hapless dip buyers got steamrollered. It lost money every year under GAAP. If a brokerage cannot make money in the hottest real estate market ever, when can it make money? It still has a market cap of nearly $4 billion.

Redfin [RDFN], another real estate brokerage that cannot figure out how to make money in the hottest housing market ever, experienced a crazy 730% spike in share prices from March 2020 to February 2021. Much of that spike has now been unwound, with shares down 60% from the peak. Easy come, easy go.

IPO stocks are getting crushed.

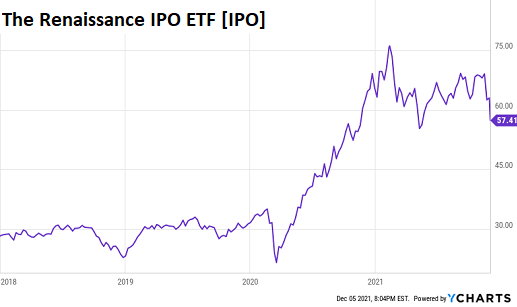

The Renaissance IPO ETF [IPO], which tracks the largest and most liquid newly-listed stocks of US companies and whose biggest holdings are Moderna, Snowflake, Uber, Cloudflare, and Zoom Video, has plunged 24% since the peak in February. But some of its biggest holdings have gotten totally crushed.

Moderna [MRNA] has plunged 38% since the peak in August 2021, including a 31% two-day collapse in early November.

Snowflake [SNOW] is trading at an absurd valuation of 125 times revenues, despite huge massive and increasing net losses every year. It’s down only 16% since mid-November, after having bounced back partially from the 14% plunge on December 1. This is a prime candidate for a massive one-day plunge, followed by dip-buying, followed by dip buyers getting taken out the back and crushed.

Uber [Uber] has plunged 48% since April, which reduced its market capitalization to $70 billion. This is a still ridiculously overvalued global taxi enterprise that is now 13 years old and has lost $36 billion since 2016 under GAAP.

Cloudflare [NET] plunged 28% from the peak three weeks ago. With a market cap of $51 billion, the stock trades at a ridiculous 88 times revenues though the company has lost money every year. So now, shareholders get to look forward to that whiff of disappointment that crushed DocuSign on Friday.

When shares of companies that have been around for years and that have never made money are trading at ridiculous valuations of 88 times revenues, well anything can crush them.

Zoom Video [ZM] has plunged 67% from the peak of $568 on October 19, 2020 to $183.92 on Friday. The descent included a 16% plunge on August 31, followed by a little dip-buying, followed by massive drops. Despite this massive haircut, the stock still trades at a ridiculous 15 times revenues.

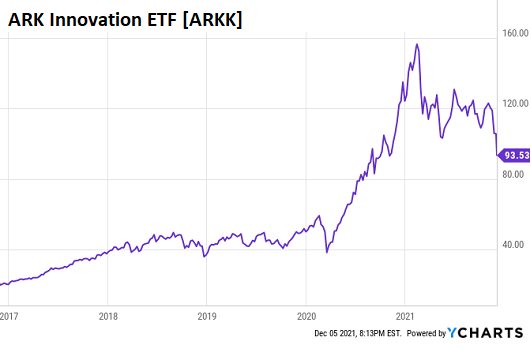

The ARK Innovation ETF [ARKK], that chases the latest and greatest high-flyers from online shopping to crypto exchanges, has plunged 41% since the peak in February.

The entire complex of US-listed Chinese companies has cratered.

The structure of how these Chinese companies issue shares in the US has come under attack by regulators in China because it attempts to dodge Chinese laws against foreign ownership. These companies have created separate off-shore mailbox companies in the Cayman Islands or other tax havens, with a contract with the Chinese company. And those mailbox companies issue American Depositary Receipts (ADR) in the US, and holders of these ADRs own the mailbox company, not the company in China.

From Alibaba on down, they have all done this to get around Chinese regulations. And investors have been bamboozled into buying ADRs of mailbox companies.

During the Trump administration and now during the Biden administration, these listings have come under attack from US regulators as well, including because companies fail to conform to US disclosure rules.

These companies are now pressured from both sides to delist the ADRs. And prices have collapsed.

Alibaba issued shares in Hong Kong in 2019 via an IPO, and when it gets delisted in the US, it can continue to trade in Hong Kong. It’s Hong Kong shares dropped to a record low of HK$ 119.40 on Friday. In the US, the ADR plunged 8% on Friday to $111.96, the lowest since April 2017, and is down 65% from the peak in October 28, 2020.

All of them got further crushed on Friday: Pinduoduo (-8.2%), Baidu (-7.8%), JD.com (-7.7%), Nio (-11%), and then there’s Didi (-22%).

Didi, the Chinese version of Uber, listed its ADR in the US via an IPO in June this year at the IPO price of $14 a share. After briefly reaching $18 a share, the ADR has since collapsed to $6.07, down 66% from the post IPO peak. Didi is now trying to figure out how to delist the ADR in the US.

Investors who’ve been trying to out-hold these collapses, or who’ve tried to “buy the dip,” have gotten screwed over and over again.

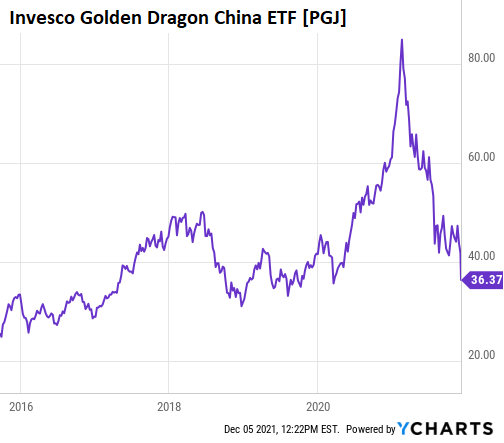

The price of the Invesco Golden Dragon China ETF [PGJ], which tracks these Chinese ADRs listed in the US – it’s largest five holdings are Baidu, Nio, JD.com, Alibaba, and Pinduoduo – plunged 9.3% on Friday and has collapsed by 75% since the peak in February 2021.

PGJ shows what kind of bubble-nonsense these ADRs were and still are, how they’ve been hyped by Wall Street, and how people who believed that stuff got fleeced, despite some of the head-fake bounces and dip-buying on the way down:

These were a few examples.

The amount of crushing going on beneath the surface has been phenomenal. After the one-day or two-day plunges, there was dip buying, but these dip buyers had to unload quickly, or else they got crushed, and so, if they could, they unloaded to the slower dip buyers, and they got crushed.

Tesla, which dropped 6.4% on Friday, is down nearly 19% from its 52-week high in early November, as Elon Musk has unloaded over $10 billion of his shares over the past few weeks.

The Russell 2000, which tracks small stocks, has dropped 12% from its peak.

Most of this mayhem playing out among these individual stocks and some of the ETFs is band-aided over by some of the biggest stocks that have held up better. For example, Microsoft is down only 6% since mid-November. Apple barely dipped after hitting a new high on December 1. Google is down only 4.9% from its 52-week high in mid-November. And the Nasdaq has only dropped 6%, including the 1.9% drop on Friday. And so on the surface, it still looks hunky-dory.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Stonks and crap coins are plunging. Those who listened to the media are the bag holders while a few got rich.

Buy now or forever be priced out!

That is what people said just before the 1929 crash and as to real estate, they said the same before the 2008 real estate market crash. Good luck with that. The only way that the oncoming hypeinflation can be fought is Volker’s way: to raise interest rates until it dies with legal changes so the ultrarich finally are required to pay taxes, or as to those few who have not been engaged in massive tax avoidance, pay a fair share of taxes, so the future costs of the government (hundreds of TRILLIONS per estimates) are covered without printing more US dollars each year.

I am afraid that the Fed is between a rock and a hard place with regard to the raising of interest rates. Back in 1980 Volker could do it as the system had much more flexibility than it has now. Now any significant sustained interst rate increase will crush the the U.S. as well as the world economies. These are crazy economic times. Keep fingers crossed.

Sad!y, we are like passengers on the Titanic after it hit the iceberg so crossing our fingers will not help. If interest rates rise like Volker raised them, our government may have to make major cuts like eliminating the US air force and army or social security, OR (horrors) force the rich to pay taxes.

Good bye army; good bye air force. Welcome, CCP overlords! Please do not kill us all this month. LOL.

“force the rich to pay taxes”. They pay the bulk of the taxes. The ones not paying taxes are the middle class and below with children. Not only do they not pay income tax, they make bank off ever expanding child tax credits.

Bitcorn is down a LOT. And it’s going down more this month. A lot more.

Watch the S&P 500, drop down to at least 4000, and more likely 3800.

The complacency is remarkable.

Bitcoin down:

Bitcoin is not down, it is still up fromit’s real value, somewhere around 0.

What fascinates me is all discussions about printing money, monitizing debt and that fiat money , USD or Euro, is not backed sufficiently with real value, “in god we trust”

But bitcoin and other crypto’s, it is totally OK that they are only backed by the good faith we have in the pimpers of bitcoin and those early to the crypto ponzi scheme that they will also hold and never sell.

Are so many people that gullible and financially dumb?

Yes

Yes

Yes

BitCON is over $50,000, up $9,000 since the so-called “crash” a few days ago. Every dip is bought heavily, likely by whales who crashed it intentionally so they could quickly buy at a much lower price, then they run it back up immediately. It’s a pump and dump scheme.

The whole thing is then celebrated by a bunch of loudmouths online, like the El Salvador President. The “crash” hasn’t even begun. I can’t wait until it has dropped below $10,000 and this clown is hauled off to prison – or chased out of the country by an angry mob with machetes.

Yes to the million degree. Speaking as someone who didn’t have any of this click until my 30s.

I’m cracking open a book on Truth Default Theory and the study of deception. I figure I’m going to find some parallels to our current reality.

depth charge, is that any different than the stock market these days? there are no valuations, no research. it’s all a pump and dump scheme.

The central bankers (Fed) have magically created wealth.

Magic is illusionary.

The dystopia is set, IMO.

Stocks appreciations (and perhaps decline) will NOT cover the inflation rate.

Cash, with the meager 1/4 pt raises (if we get them) will not cover the inflation rate.

But, this time it is different.

The past was Beannie Babies, Pet Rocks, Tulips, and Cabbage Patch Dolls.

Today, Bitcoins are where it’s at.

It is different this time.

You forgot to mention NFTs.

Long T .

O, and MLPs.

I feel as though crypto for people aged 15-30 is full of as many greedy get-rich types as the stock market. The number of (Bitcoin/Ethereum/insert coin here) millionaires that I personally know has grown to 5. They are all in their early 20s and typically have 2-5 million each. Funny thing is, not one of them knows a thing about economics or wants to learn because trigger words like “scarce” are all they care about. None of them have jobs and they all pretend to be boy geniuses. I can only imagine the look on their faces if BTC/ETH fell 60%+. Honestly, I already know what they’d do. They’d probably buy more.

Let’s not end this yet. We need to borrow more money from future generations so I can continue to enjoy my free ride! The grandkids can work for $34k a year while housing costs $380k. Nothing to see here..

Canadians get paid C$30,000 a year in Toronto, while a condo is over C$800,000 these days.

They’re living off of their houses. What could go wrong?

It worked for the Chinese. 🙄.

The Chinese are money laundering in Canada via the real estate market … been going on for some time.

Trade imbalances do have a negative effect.

Why are foreigners allowed to own land in another country?

Land, (the Country itself), should only be owned by the Citizens of that Country.

Absurd, cruel, and just plain wrong.

In the 1970s-80s it was drug money through the Caribbean, banks – no questions asked. And money from Hong Kong. And Taiwan. Then there was the big Japanese property buying boom, then there was … etc etc and now it’s China. The sources change, but the practice never does. And if the buyers often use their purchases as anchors to enable residency or citizenship, what’s wrong with that? At least they’re coming with money, are self-sufficient, and enterprising.

Actually, foreign buyers buying property can be quite beneficial to the local economy, providing liquidity to local markets, and it’s hard money coming home (if home is a hard-money country – rare) – most of the world’s currencies are worthless outside the home country so have to be converted before buying in the foreign country. If you’re not a hard money target country then it’s even more beneficial if the purchase is in hard money.

A closed economy is instantly recognized by its poverty level.

“At least they’re coming with money, are self-sufficient, and enterprising.”

Or … corrupt as can be. You don’t get rich in China by being law abiding.

Chinese money has now made the town where I grew up totally unaffordable. So … yeah, that worked out great.

Boise is the hottest US housing market and median salaries are 1/10 of median home prices. That is still less than CA, and many of those home buyers are cash, and many have WFH jobs which pay more than the local wages.

wait till they see that most employers still want their employees back in a day or two a week.

Fact checking here: Isn’t median salary of Boise around 30K?

And aren’t their median home prices there in that metro area about $500K?

Wake Up! It’s 2021!

“so I can continue to enjoy my free ride”

Don’t pretend you have any actual control of what has happened and what will happen.

Yes Winston, its not as if baby boomers or those previous were in charge this whole way/ sarc off

Abolish residential zoning and redraw all building codes everywhere.

The only other stock mania that might be bigger than the current US one is Japan on December 31, 1989.

But even here, it wasn’t as dependent upon a fake economy based upon QE and government deficit spending; both came later.

While P/E ratios were higher or much higher (on average), I’d rate the current US mania as comparable if not worse. The P/E ratio isn’t a good indicator of relative value anyway, since the only reason it has any correlation to stock prices is because the “P” IS the market.

There is absolutely no comparison between the current US stock mania and any other period in the history of this country. The 2000 dot.com bubble is the same mania we are in now, as it never ended. Valuations at the 1929 peak were also noticeably lower plus with no QE, much smaller government, much lower leverage, and the country mostly produced real “stuff” as opposed to much of the hot air currently composing GDP. All other supposed US stock bubbles (such as 1968 and 1973) were nothing compared to this one.

So, what we have now is an absurdly overpriced market supported by the weakest long term fundamentals in the history of the country.

‘much lower leverage’

Especially middle class household debt, that didn’t exist. No credit cards.

Virtually no auto debt. No seven year auto loans.

There was credit then, for mortgages and cars, just not credit cards. Even the local stores let you run a ‘tab’ and settle it periodically.

And according to one version of the 1929 crash I read, it happened when the markets realized that people were over extended on credit and the small stores etc. stopped letting them run up the tabs any further, and earnings started dropping because people could no longer buy. No electronic money / credit cards to keep spending going. Also no electronic food stamps, which kept the soup kitchen lines from forming as in the 1930s and kept the public plight in the headlines.

‘General Motors invented the credit system by loaning consumers the money they needed. They required a 35 percent down payment, with the rest of the cost being paid over a 12 month period. Henry Ford opposed this and offered the layaway plan. ‘

Ford did not offer actual car loans until the year before the Crash. Outstanding auto credit and consumer credit was negligible by today’s standard.

Re: mortgage credit. This is always separated from consumer credit.

Mention of the grocery store ‘tab’ usually settled monthly actually illustrates the rarity of consumer credit. Another illustration is that in this era and for decades after, the pawn shop was the lead source of consumer credit for cash, as distinct from goods.

Having had a front-end seat at the Japanese bubble, I must opine it was perhaps even more dependent on a fake economy, but one more in the character of America’s 2008 real estate bubble on a several-times more absurd scale.

Note that it began rapidly and inexorably to disintegrate from the first trading day of 1990. Will we see the same here after New Year’s day 2022?

Front-row, not front-end. Damn autocorrect

And for those who think real estate in the US is impervious, the Tokyo real estate market dropped 90% from highest to lowest. In 2007-2009 US market only dropped 30%. That time.

I find this fascinating. I pointed out some of these facts to a group of co-workers last year. They didn’t believe me. When I shared links to the information they were surprised and then said “Well the U.S. is a much bigger market, that will never happen here.” I let it go at that point but have been wondering if we are following Japan down the same path.

As silly as their real estate bubble was, the exports from this ‘fake economy’ would extinguish the US consumer electronics industry and more slowly, thanks to protective quotas and tariffs, most of its auto industry.

The Japanese real estate bubble was worse than either pre-GFC or the one now in the US. Other than that, I don’t see how Japan’s economy could be more fake than the US is now.

Reduce US deficits to even the 2000-2007 levels/trend and “growth” since 2008 is close to zero or negative. Normalize the FRB balance sheet and interest rates to pre-GFC levels and credit conditions are noticeably tighter.

The other primary difference with Japan is that their mania was “normal”. It moon rocketed from a normal base in 1982 and flamed out in seven or eight years. That’s the prior pattern for all real manias I know.

This one in the US is like the Energizer Bunny, it just keeps going and going….

Its end will be truly calamitous.

It would a good idea to stop using Japan as a comparable. The cultural divide makes this a different planet. In the US we see smash and grab thefts. In Japan you can leave yr wallet in Mc D

and an hour later it will still be there. There are no mainstream cultural, religious or ethnic divisions. One Western expert, asked about religion in Japan, replied: ‘the religion of Japan is Japan’

Far better to use Germany, to my mind the most successful economy in the world. Pre: Covid it was running a 2% budget SURPLUS!

Prices drop harder when there are fewer people willing to buy what is being sold.

Surely there are more global investors willing to pick up US equities, RE, etc now than there were investors willing to buy Japanese assets when their bubble started deflating.

It was before my time so happy to be told I’m wrong, but the fact that we’re talking about the US market makes a bigger cushion and therefore a softer drop.

Fundamentals do NOT matter. Where can the money go, now that it has to get out of Govt.Bonds??? IT has no place to park…so equities and Florida real estate it is. (Investors don’t understand or know, how to invest in commodities.) The Govt bond market is 10x the size of the equity market – just a shift in assent allocation and the market explodes to the upside.

Fundamental/Earnings/ etc etc DO NOT MATTER. It is the flow of capital that counts.

Prices are set on the margin. Which means your thing can drop tremendously if somebody else’s thing loses a bid. Your money then has been destroyed. It is not a zero sum game unless you go by cash accounting purchase price vs sales price and forget about all the ledger vapor.

After that, whatever capital that is left can flow around to the least frightened destination.

i use the analogy of a suburban development to discredit the ridiculous “tons of cash on the sidelines” or “money will flow in or out of a certain asset” nonsense. suppose the development has 1,000 houses. in a normal market, 20 are on the market at any given time, and the average price is $500,000. suddenly, take the current market, and only 5 are on the market. since there are so few available, as no one wants to move out and have to pay an obscene amount for another house, the 5 who are selling can sell for an average price of $650,000, and there are plenty of investors looking to buy.

now, let’s suppose that it’s discovered that there is a serious contamination problem under the development, and it’s hazardous for anyone to be living in any of the houses. assuming no insurance or tort claim availability, the value of all of these houses has just dropped to 0. no money has “flowed” out of these assets. in fact, no asset and no money has changed hands at all! all that has happened is that the “value” of the development has changed, from $650 million, to $0, overnight.

that’s what can happen with any asset when the mood changes. that seller of a house, bitcoin, msft stock, a pickup truck, or anything else can suddenly find no interested buyer, at anywhere near the prices that were common a week before.

all of that “wealth” has just evaporated.

MooMoo that’s a flawed analysis. There are no sidelines, and money doesn’t park itself in an asset, because in every transaction there’s a seller as well as a buyer.

If you have more money than you can handle, and you buy something, you get the something (but someone else has to sell it to you), and that person gets your money. Your money isn’t destroyed and doesn’t go anywhere except to a different bank account (or mattress…).

Similarly, stocks don’t “go” anywhere. They just change owners until the stock is bought back or retired in a merger.

And Bonds don’t “go” anywhere. Once issued, they always have an owner until maturity.

At the system level there’s no such thing as a “shift in asset allocation”. There just are bonds, and stocks, and cash, and so on. Their relative values are set by the preferences of the people who hold them, and by the willingness of companies and borrowers issue more stocks or bonds.

Also the govt’ bond market is not 10x the size of the equity market. The equity market is currently larger. The US stock market is 2x GDP and the Treasury bond market is only 1.25x GDP. Both are outrageously record huge numbers. As recently as 1981 US debt/GDP was only 0.3x. Historically stock market / GDP over 1x was a huge bubble; now we’re in double-bubble territory.

There is a grave yard universe of bonds that never reached maturity but no longer exist, via bankruptcy or restructuring of debt, forcing bond holders to take equity and cancelling the bonds.

I can’t help adding: another large galaxy of sovereign bonds that exist but have been repudiated. Among the usual SA players, Mississippi. There is a society of UK bond holders still insisting the state make good but no luck under US law.

You have to determine how you account for wealth. Is wealth market value? Yes but that can disappear in a flash such as Mississippi bubble or Enron. You have to know when to sell

Or is wealth summation of real future income.

It makes a difference mentally how you account for wealth. Take US stock market. Market Cap is $60 plus trillion, but dividend income is only roughly $1 billion. Which one represents the value more correctly?

It’s psychology that matters which drives the flow of “capital” which is predominantly credit.

Don’t think you are right on the 10X. US equities are 60 plus trillion market cap. Isn’t that in the ballpark of US bond market.

This is the correct comparison. There may not have been QE or deficit spending but the colossal C/A surpluses produced the same effects domestically – liquidity far beyond the capacity of the real economy to contain, plus the magic of zaitech.

Other parallels: domination by the big banks; regulatory negligence; accounting abuse; ‘new economic paradigm’; property as speculation; blue-sky technologies; hubris in government and boardrooms and plenty more.

It was called the Bubble Economy at the time, just as we now call the Everything Bubble by its name. There were just as many justifications for how the infallible potentates at the centre of the system would keep it going indefinitely. But a bubble is a bubble.

AF,

Do you think the intro of 401k , Gov’t plans, etc and the internet has had a hand in this?

Every week money automatically rolling in whereas before , the financial crowd actually had to work for people to invest their money with them…

Yes, but it’s still psychologically driven.

401k and mutual funds is a form of financial intermediation. The public years ago turned its savings over to money managers who takes risks most individuals would never take directly.

Just look at so much of the garbage being bought.

It will be interesting to see if the Markets head down hard before the end of December. Most Insiders seem to have moved to the exists already, may be the professionals as well with the usual retail investors left holding the baby ?

“…with the usual retail investors left holding the baby?”

You mean Rosemary’s Baby?

Haha. Love it. Great movie, btw.

@ M

Indeed it will.

In UK one of the 2 MPC hawks who pushed for a Dec rate hike said in interview he was not so sure now as a result of Omcom. He wants to wait and see , surprise, surprise, there’s always something crops up to delay an actual rate rise. It seems to have worked to some extent because UK stabilised and slightly rose today.

In spite of all the hype I still say I’ll believe a rate rise when I see it. Maybe they are using scare tactics to pull in a higher peak?

Is not it amazing – everything is soaring and skyrocketing but actually goes nowhere ?

The closest analogy I can think of is:

“A strange loop is a cyclic structure that goes through several levels in a hierarchical system. It arises when, by moving only upwards or downwards through the system, one finds oneself back where one started.”

In the book “Gödel,Esher,Bach:The Eternal Golden Braid” (1979) there are many pictures of such structures-staircases,triangles,waterfalls…

Well,what was optical illusion in 1979 became reality in 2020 and beyond,thanks to Fed Almighty.

That 1.38% 10yr rate is moving oh so fast (in the wrong direction)!

😀

Direction can be both right & wrong simultaneously when one masters the fine art of Doublethink: the acceptance of or mental capacity to accept contrary opinions or beliefs at the same time.

Pull that casually inserted $4 Trillion back, and lets see what real rates are.

Yep, it is.

With all the talk of the greatness of this bubble, do you all think it will end by the FED raising rates and crashing it after propping it u p.o. for 10 years?

Not me!!!

Probably not the FEDs doing. More likely due to some consequence of what the FED did. Like the supply chain debacle severely affecting revenues and profits enough to cause some overly leveraged entities to fail. Could be something else.

The entire system is propped up on sentiment and nothing more. Something will cause the BTFD mentality to change to Sell, sell, SELL at whatever you can get.

US I-bond interest rate went to 5.3% from 3.4% on Nov 1. That is more than most mutual funds and even hedge funds (who are supposed to know how to make money both short and long, but most don’t). Next hike in May could put it over 7.00%. They are talking about taking off the $10,000 yearly cap for purchases.

Akakai Akakaikovitch,

I like I-Bonds too and the ones issued Nov 2021 thru Apr 2022 are paying 7.12%.

There will be 2 rate adjustments in 2022.

From the treasurydirect.gov website:

“The initial interest rate on new Series I savings bonds is 7.12 percent. You can buy I bonds at that rate through April 2022.”

I haven’t heard of them raising the 10k cap for individuals, but if you Google this below as-is without quotes, there is a possible way to put 65k in it.

Google this below as-is without quotes:

How to Buy I Bonds (Series I Savings Bonds): Soup to Nuts

Akakai, November 1, 2021 I-Bond COMPOSITE rate is currently 7.12% thru April, 2022. The semi-annual rate for that period is 3.56%.

The fixed rate still remains at 0.0%

Impressive article. You rattle off stock stats like you have a full research team, or a bloomberg terminal in your head.

That’s why I come here.

Chip implant in the brain :-]

Just kidding. I do have this stuff all over my screen.

If I remember correctly the money in SOFR doubled on Friday the 26th of November. Capital moving into to cash?

MOVE index, ie the VIX for bonds is rumbling.

SPACs make me particularly nervous. It seems like they soften a fair amount of the financial disclosure typically required of a traditional IPO. Perhaps we’ll see large cap over perform for the next few years.

– The weekly Advance-Decline line also gave a warning that “all was not well”. That line remained flat since early june of this year while S&P 500, Dow Jones and Nasdaq kept rising.

All the RE companies you listed very much wanted to mimic the technology companies by taking some risk while losing some. However, RE is a different ball game where even 1% loss on the portfolio can translate to millions of dollar of losses. I believe the valuation of all these RE companies will go down until they fix the underlying issue.

DOCU was purely an over-reaction from the market. The business model and adoption of their product is pretty solid and growing. I see the stock going back to around $75 in next couple of months (Note: I own no stocks/options).

Lastly, we all know that there will a market correction in the near future all this fancy companies with extremely high valuation will suffer a lot while companies with strong fundamentals (AMZN, MSFT, AAPL, NVDIA) will maintain its dominance.

At this point, I guess the safest bet is to hold real estate which hopefully won’t go down 40% in a day!

Would you postulate to say that P/E is not a valid function to value companies at this time or in this environment? Bonus question, should we ignore fundamentals and just raise stock prices by 15-50% annually for the ones in favor?

Look at the historical correlation between earnings and stock prices. I have seen a chart recently (not for recent years of this mania) but in the past, it would fluctuate wildly. The primary or even only reason there is noticeable correlation is because the “P” in the ratio is the market.

Based upon what I know, revenue has been a much better indicator using historical data. Yes, the current ratio is also in nose bleed territory.

The trouble with inflation is that the “E” comes unanchored and you have no idea what P will be appropriate, other than in a relative way…

The institutional money runners, AND most importantly, the big banks, have much of their trading done by their robots, which are designed to front in Nano seconds the other robots.

Wonderful on the way up so lets see how it works on a correction to the downside.

Given what you have just said, I would imagine that the last thing an algo would do is dump huge numbers of shares at once. The clever thing to do would be to dump less than 0.5% of the shares in many intervals. Sort of like feeding the seagulls. In fact, doing it right may in fact make it look like a stonk is being BOUGHT, not sold! The “I see value there!” type day trader says “Wow! I made the price go up just by buying them! Bingo! Reddit will love this!” Like seagulls, you’ll soon attract a crowd begging for your stocks! Fighting over them even. Having greater fools like retail traders is an excellent price support.

Oh, wait, that’s what the instos HAVE been doing for years. Sorry to let the cat out of the proverbial bag, lads.

Sayonara, bag holders.

The algos aren’t any smarter than the one who programs it. Just look at LTCM in 1997 or Archegos earlier this year.

Agreed. I don’t really think having stronger, faster computers really gives the advantage that people think it does.

At the end of the day it’s all about understanding the value or worth of something, isn’t it? Why is it advantageous to get to an uncertain number faster than others? It’s still uncertain.

We were due for a recession and covid was going to be the catalyst but money printers saved the day. Now we’re either going to have to fire up the money printers once more and (cut rates?) Or weather a much more violent storm as the high is so much higher now.

The question is, how long can they keep the disco ball turning and shining? Powell and co. Have all had their positions secured so politics aren’t quite as relevant. They might try and hold off for the midterms but I think everyone with half a brain that pays attention knows the bad times are coming and the good times are withering.

It will last as long as the collective optimism lasts, not a day more. When that turns, whatever the FRB or any other central bank tries will fail. It’s inevitable when it’s only smoke and mirrors with so much underlying decay.

Had to laugh at the prodigious use of the word “crushed”. Deja vu all over again. Eerily similar to the Dot-com crash.

Wolf should have added in profitable, dividend paying, long established, gold mining companies to his list of crushed stocks. Easily down 50%!

The problem with the mining stocks is they are making money. In the new economy you need to lose billions in order for the stock to soar. Actually making money is so out of favor!

Yes. And there are lots of stocks — an astounding number of stocks actually — that are down 50%. I focused on the high-flying “tech” space this time.

It’s the word that described best at the time how I felt day after day during the dotcom bust. Stuck in my mind. And today, I let it out a little.

2016-2021.

Disrupting the market.

2022.

Do you make any money?

So, what you are saying is, the fed is allowing the rats to leave the sinking ship?

The Fed *knows* that everything is in a bubble and that the government is bankrupt. They are looking for the smoothest way to deflate that won’t disrupt the status quo. Just like any other Central Planning political institution.

Completely agree. But what to do? TINA (there is no alternative in the face of so much inflation) still prevents me from moving from significantly from equities to cash. I am currently about 60/20/20 (equities/gold/cash). The equities are mostly not the high-fliers.

Prices are rising and at the same time corporate profits are rising to all time highs. So clearly we don´t have inflation , we have monopolistic price setting.

no, it’s just that the sellers are able to raise prices more than their inputs. let’s see if that lasts after the money dries up.

“it’s just that the sellers are able to raise prices more than their inputs”

Isn’t that what I said?

I see your reasoning. I am heavier cash. Why?

There are many dynamics that, when a drop spreads across the market, cause all sorts of risk assets to correlate and fall together. This is especially true of equities, with the “easy in, easy out” trading tech everyone has.

There are index funds that span across lots of equities, now very widely held. (Even the S&P 500 is now very heavy in big tech.) There are new sellers dragged in, who are levered, or who must go to cash to meet other obligations or maintain reserves.

True, the dotcom crash was pretty confined to tech stocks. But this time, the nosebleed P/E ratios and asset prices are seen across the board. Hence the nickname some use, “the everything bubble.” If it all goes badly enough, money (issued as debt) is destroyed (defaulted debt) and cash becomes at least temporarily scarce, and desirable again. Credit too becomes more scarce as every defaulter scrambles for it, and burned banks pull in their horns. Even if the printers restart, those caught sufficiently wrong-footed have been cleaned out. It is hard to start over from a cardboard fortress.

There are still plenty of novice “traders” lured by the prospects of easy money. My relatives, at Thanksgiving, bragged as heros. We all know how this ends. But there will be downs, then hope, more buying, bigger downs, then people get really humble. The dot com era is similar. But I don’t yet understand how the fed might prop up equities. They have no tricks left. Could they start buying equities in a new QE ? Bad for reality but no one cares about reality.

I think they will just let the markets settle lower and lower. I’ll bet that every politician and banker in the know has been deleveraging and going to cash for a while now.

In Australia I haven’t seen any politicians selling real estate. I think they own 4 houses each on average. But little Aussie battles might be out of the loop

Those 4 houses are just their personal holdings. In their family trusts, they own entire suburbs.

My guess is that the pain of the large correction that deserves to happen — pain both for retail investors and for Main St. — will become so great that it will be politically impossible for politicians and the Fed not to step in and support the market. This is especially true with a midterm election now less than one year out. On the other hand, Powell just having been reappointed takes a lot of short-term political pressure off him.

If I had to pick a number (a WAG), I’d say that the Fed will go back to madly printing (including QE to support assets that are held by entities that are deemed too-big-to-fail) if there is approaching a 20% correction. In round numbers, that guess can be converted to a “Fed put” at around Dow 30,000.

Those are wild guesses of course, but I have to invest based on likelihoods, and not be overly driven by worst-case scenarios. The worst-case scenario for equities holders is that the Fed is more hawkish than I am guessing and there is no Fed put at around 30,000. The same scenario that is the worst-case for equities holders is the best case for cash and gold holders.

In one of Wolf’s other comments, he says “this White House doesn’t give a crap about the Dow,” so he is saying that it isn’t wise for me to be counting on a Fed put at 30,000.

Maybe, but it’s also possible social mood will make the “price keeping operations” you infer politically intolerable.

It’s not possible to help the little guy without bailing out the crony capitalists at the same time.

Most people don’t own much in the stock market.

I expect the government to impose another mortgage moratorium to try to prevent another GFC type real estate crash. A lot more public support for that and temporarily feasible @ 3% rates.

Probably also more “stimulus” cash in one form or another to the masses.

except for the people in their 20s and 30s who would see such “support” to mean that they’d never own a home.

The FED could not under current laws buy equities.

A real downturn would require Congress to do a new round of stimulus. To do that they’d have to sell bonds as neither they nor the FED can just print money under current laws. I don’t see that changing either.. It would destroy the US as the world would soon require something other than US$s in compensation for all the goods we buy (and we buy a lot, that’s why the ports are in such chaos).

Could Congress actually do this if interest rates are already effectively negative? You want to lend money to the government and get less back than you gave them?

Looks like the gov and fed are somewhere between a class 5 hurricane and an F5 tornado on a broken down bus.

Good point that the Fed can’t directly buy equities. I had to go back to see how they actually supported the market. These were some of the programs introduced in the Fed’s March 23, 2020 press release:

* Support for critical market functioning. The Federal Open Market Committee (FOMC) will purchase Treasury securities and agency mortgage-backed securities in the amounts needed to support smooth market functioning and effective transmission of monetary policy to broader financial conditions and the economy. The FOMC had previously announced it would purchase at least $500 billion of Treasury securities and at least $200 billion of mortgage-backed securities. In addition, the FOMC will include purchases of agency commercial mortgage-backed securities in its agency mortgage-backed security purchases.

* Supporting the flow of credit to employers, consumers, and businesses by establishing new programs that, taken together, will provide up to $300 billion in new financing. The Department of the Treasury, using the Exchange Stabilization Fund (ESF), will provide $30 billion in equity to these facilities.

* Establishment of two facilities to support credit to large employers – the Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance and the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds.

Also, good point that Augustus Frost made that these programs are seen as supporting “crony capitalists,” even though they help everyone who gambled on equities, and Main St. too, when an equities bust finally reaches there.

It’s been more than 30 years and Japan is not back to stock market peak. If you eyeball current trend that it looks like it might take another 20 years. Fifty years is long time to wait.

Tried to look back at market cap to GDP and it looks like Japan got to ratio of 3.5. USA currently is at 2.0. I think 100 year average is in the 0.7 range for USA.

It’s all relative.

If you bought the Nikkei in 2011, you’d be up all most 400%.

I have seen all kinds of number for market cap/GDP ratio, more recently a lot higher (for the same time period) than before.

For example, years ago the 1929 peak was supposedly 80% of GDP only matched by the 1968 peak, until the late 1990’s.

The more typical rate was below 60% and cheap was around 40%, like 1982.

From what I have seen we are now higher than great depression bubble, and tech bubble on most measures. Not sure there is much logic once you have Zirp and 6% inflation. Own real stuff I guess.

I’ve recently waken up to the fact that QE doesn’t seem to correlate as strongly with interest rates as most believe. Why is it that rates decline when QE stops and tend to increase during QE? Quite interesting.

Anyways, my portfolio is just fine. I’ve been buying undervalued companies and holding, and while I am down, I’m glad it’s not like buying into any over valued stocks. With a healthy allocation to cash and a growing cash machine, I deploy slowly.

“I’ve been buying undervalued companies”

What – both of them?

My thoughts exactly!

Those two companies must be the ones that have not gotten caught fudging their numbers yet.

Funny but true. But then to most people, these stocks are “undervalued” due to the relative valuation.

Greed allowed China to build a huge economy in 50 years most of world gave away manufacturing to them ,lent money thru bond purchases ,probably won’t get much of it back bankruptcy or nationalization fools born every day

In the 21st century it’s China getting the rave reviews. In the 1980s it was Japan getting the rave reviews. China will probably go the way of Japan. Meanwhile, nary a mention of the greatest story of the last 500 years – the USA.

I’m still scared really bad – 98% cash.

The US of today isn’t even close to the US of 1999. It’s far worse. If it was, your point would have some merit.

the u.s. in the 1990s still somewhat resembled a traditional western society. the nightmare combination of wokeness, deviance, third worldism, and cultural and moral rot of today does not

I read this last week from MarketWatch, – here is the title:

“In his final warning, this stock trading wizard — who made big money in bear markets and crashes — called this market a bubble like no other”

I also believe this too and think that the “screwball” Crypto, NFT, SPAC markets, plus record margin will accelerate this process in a unseen epic way.

I believe that in the USA we have become accustomed to the insanity of high asset prices. It seems inconceivable that we can have an asset collapse like Japan.

Ours is different, but US banks were in big trouble like in Japan at the bust. The US went all in and reflated housing and bailed out banks with customers 0% deposits. Eventually assets have to be supported by income and not fantasy and when that happens things reset to about the fundamental level.

When this is over I don’t think we are going to be saying that our government officials and Fed chairman did a good job.

Watching over priced Stock Queens lose their crown might be bad news. Small caps are saying a shit storm may be coming. I see chart heads on you tube with their multi screen led screens in the background yelling buy,buy while yelling about zones and support, head and shoulder patterns or my favorite the inverse Bart Simpson spike bull hair flag buy pattern. It’s all good going up. I could smear peanut butter on my key board and let my Springer Spainel lick the keys and trigger buys that couldn’t miss on the way up in this Fed QE fueled market. Valuations will matter if the Fed does more than jawbone about inflation. The market and the dollar has priced in the Fed jawboning 10x. The market has also priced in curing c19 5x. We have no cure but what the hell, buy. Lose jobs ,market rallies. Gain jobs

,market rallies. 600 year moon eclipse , SELL. I have a white squirrel that only appears before the market crashes. It can’t be the same squirrel because I have seen “it” off and on for 30 years. A white squirrel was in one of my walnut trees today. I have ended the Spainels market analyst position and have replaced him with the squirrel. Neither give a shit about my move. Peanut butter and walnuts are in their contracts. I really don’t have a clue what’s coming. We will know when we start hearing about something called market fundamentals. I will have to google that.

Oh, I have a clue what’s coming. Fundamentals in all aspects of life are in decline. Lunch today in a mediocre restaurant was $50 for two .No drinks or dessert. Food was subpar, and skimpy, service was poor as the other places we have enjoyed over the years. We are 73 and happy we are headed out vs coming in.

“We are 73 and happy we are headed out vs coming in.”

I feel the same way, though I’m a quarter century younger than you. That’s what the FED and politicians have created – a mostly miserable country. Extreme asset prices benefit precious few, and ratchet up the misery index.

While I’m a saver and doing better than I’d imagine a lot of people, which I am thankful for, the relentless assault by the FED to eat away at – STEAL – my savings via inflation while rewarding disgustingly greedy, fraudulent gamblers has chipped away at my general happiness as I look around in horror at the current system.

There is a special place in hell for the people who have conspired to do this. The homelessness and general decay that are a direct result of these policies is much worse than I ever imagined it would get, and now see an entire country that is on the precipice of failure. In fact, the social fabric is already torn apart.

I don’t know where we go from here, but I don’t think it’s anywhere good. I think it’s a place where these disgustingly wealthy pukes who are running things take a little bit more for themselves, then a little bit more, then a little bit more, all the while smiling and telling us how much they’re helping everybody else – you know, kind of like the FED frontrunning the markets by daytrading their upcoming policies.

Depth

“There is a special place in hell for the people who have conspired to do this.”

Why is the Fed not held to its mandates? I am stunned that for decades yes, then since 2009 no.

Powell says he worries about the “tent people”, but turns a blind eye to the fact there are record job openings, and that the workers/earners/savers of this country are getting slaughtered by his policies. (inflation)

Stable seems now to mean a stable increase in inflation. What?

Stable means “fixed”. 2% rips 22% off the dollar in ten years. 2.5% rips 28%. These are the self authored parameters of the Fed. How can this be, how can it not be questioned?

And moderate long term interest rates…(3rd mandate) moderate meaning “not extreme”, either way, in order to keep a positive yield curve, prevent burdening future generations with massive low cost debt, and maintain a balance between lender and borrower.

But that third mandate is carved from discussion due to the pushing forward of the “dual mandate” mantra.

The great flaw in our system is that the Politicians LOVE the free money, and it is they in Washington who are supposed to be the oversight of the Fed, keep the Fed between the lines. But they enjoy just the opposite.

To know the Fed would not do their duties was to know to be fully invested for the past decade.

To expect the Fed to operate historically, to obey the mandates/agreements/instructions that ALLOW their existence was folly.

Who hijacked the Fed? Cui Bono? Follow the money

The new BBB bill now in work has as its purpose to rip families apart and put everyone on welfare. A Single parent with kids will make more than a nuclear family who plays by the rules. America as we know it will be history.

Swamp Creature:

“A Single parent with kids will make more than a nuclear family who plays by the rules. ”

I did social work in SE Alaska in the early 1990s. A single mom with two kids would get $35K in welfare if she were unmarried. Of course, boyfriends didn’t count.. That was more money than I made then and with a wife and three kids.

I don’t bother eating out anymore. Oatmeal and fruit for breakfast. Omelette for brunch and then my friend and I fire up the grill at night, dine with a glass of wine and watch some Netflix.

I will give you a real example of how asset prices drive spending. My friend who is 75 has a pretty good teacher’s pension and social security. She reason’s that since she has secure income she should her IRA stay fully invested in the stock market no matter what.

That has resulted in her having a 7 figure IRA from which she basically spends the required distribution each year. That means her spending from her IRA has been growing at the rate of stock market returns plus the life expectancy kicker of about 6%. Once the stock market unwinds a lot of income is going to go poof and I think that is what the Fed is afraid of.

The Fed lit the fuse when they started down the wealth affect path.

As grotesquely overvalued as the stock market is, it pales in comparison to e-tulips – “crypto” as they like to call it. What an absolute joke of a scam that whole space is.

Crypto IS a bad joke of a scam space. But people sometimes get what they deserve and the outcomes can be harsh. Like people who sell their physical assets, (maybe gold and silver being the first to go) and buy crypto with it.

Aaaaand who is buying gold at the moment? Why the Central Banks, (aka .gov treasury depts not just US, but Poland, Singapore etc.) Govs won’t necessarily outlaw crypto, but can make life very difficult for it. Meaning they will let the crypto scam space slowly fizzle out due to unpopularity. Then .Govs will adopt it for themselves.

“But people sometimes get what they deserve and the outcomes can be harsh.”

True. And sorry to say some of those people don’t just deserve it – they NEED a cold shower of reality. And I’ll have zero pity at the time that shower arrives.

“they NEED a cold shower of reality.”

Agreed, and avoiding the lesson now only makes the final outcome worse.

Saaaay….

Where are all of the crypto queens from the last few of weeks…

Probably out in the driveway trying to figure out why the tire is only flat on the bottom…

My friend told me that she talked to her sister who is 71 or 72. She was talking about crypto coins and how much money she had made based on her son’s recommendation. Sad. They probably don’t have the money to lose.

Some of the smartest old timers are calling out this bubble (Munger, Grantham, Larry Summers, Gunlach, Jim Grant, Michael Berry). The dumb money is enjoying the blow off top most not smart enough to know their way around the casino.

I have been reading on the Japanese bubble and it seems like a lot of it was driven by fiscal, monetary and international trade policy mistakes that sound so much like USA today.

Pension funds were conceived to be supported by secure income, not asset values. A Japanese style crash would put SP500 values in the 1000 – 1500 range and that would blow up many, many pensions.

Toonces has been driving for awhile. So many of the hottie small craps have been getting haircuts for weeks. Up next on the chopping block are the chips. The last 52 week high biggies left are HD COST LEN AAPl. There are few soldiers left to hold this up for much longer. Also keep in mind the leveraging of portfolios to buy crypto or houses also crypto has been leveraged. To buy more stocks and crypto ! What can possibly go wrong. Can we say Tether?

Hussman’s last article was another good one. He uses multiple indicators to determine level of market risk sentiment. It hit one of the highest levels ever about two weeks ago.

He is a smart guy, but has been wrong. His model says a 10 year treasury could outperform stock market by 8% per year over a 10 year period. Who would buy treasuries at 1.4%? Some smart money needing a place to survive what is coming. Of course we can’t know what is coming for sure, but we can’t get caught with a high risk position at the wrong time.

Having made every financial bad decision a man can make – I was supposed to be retired with a house paid off. Ex-wife has a paid-off house and I work as a mortgage broker (20+ years).

We are the “”canary in the coal mine”” and we are seeing Layoffs and loan volumes drying up by the week (regardless of a falling 10-year yield).

My only hope of salvaging a bad situation is to short the QQQ (Nasdaq) on margin. I do not have to be right this week… just right next year some time.

Thank you Wolf for confirming what I already see in the Real Estate and Mortgage Stocks (Quicken and U.W.M all down 50% from IPO’s this year).

As boys we are trained not to beat up girls. Doesn’t help us in divorce.

Oh boy, sounds kind of risky given your age. Are you sure that’s what you want to do?

Why not sell the house in Seattle and ride off into the sunset somewhere else?

1) The Trout quintet – US, Japan, Australia, India and Russia – will diminish

China’s rising threat.

2) A bilateral trade deal might happen between Putin and Biden.

3) US will not disintegrate due to it’s high debt, inequality and negative interest rates.

4) US might decay but not fall apart. No Anti bubble and no Seneca charts.

5) US debt, in real terms, is falling due to negative interest rates.

6) Q4 2020 @$28.74T // a small increase in Q3 2021 @$28.43T // but

in real terms , with negative rates : 0.95 x $28.34T = $27.00T.

7) Fed gross assets minus RRP = Fed net assets. // RRP to protect us after

Xmas bull run.

My question….

For those inner loop few who aren’t going to lose, where are they putting all these trillions of dollars they siphoned off the bubble??

If they know when & what’s coming and are cashing out before the crash, it has to go somewhere safe…

India rip Russia and China apart as it did during Mao

and USSR. China’s silk road diminished Putin power. China’s GDP left Russia behind. China is Russia biggest military threat, not US. Russia is sandwiched east and west economically and military.

A bilateral trade deal to invite Putin to the Trout quintet might happen

in the kitchen cabinet.

Putin pipelines are China’s arteries to the heart.

A Crab choke hold is good enough.

What goes up must come down including the American Empire, and very likely the Chinese, built on the sand of borrowing, Empire. One small example, the Chinese high speed rail network loses $24,000,000 a day, every day, now add in all the Evergrand, China Steel, China ship building, and all the SOEs plus everything else we don’t hear about and I estimate China is going broke at about a billion a day. Funny how alike China and America both look from a distance, broke military superpowers both, with shafted citizens on the verge of revolution, they cannot afford a fight over Taiwan, Northrop, Hughes et al would never get paid, nor the Chinese equivalents.

Read Michael Pettis on “The Bezzle”.

Take note:

The cable financial network talking heads will begin the “Santa Claus” rally BS this week….

They have their orders.

If you look beyond the shores of the USA, you will see an interesting phenomena – while American shares have gone up something like 400% in the past 10-12 years…Europe (DAX and CAC) has done zilch. The money is still in the USA and European capital is running out of the EU as fast as it can.

Moreover – the stock market may retrace in the USA, but it is STILL going higher over the next 5-10 years. The reason is simple – EU governments are getting ready to default on sovereign debt – and that means capiltal will run to the USA. Forget picking stocks…follow the indexes – that’s what gives the big picture…

ANd in case you haven’t figured it out – this is a commodity cycle now… food and energy. Investment in energy has been destroyed by the Greens, and that means oil (up 3%) this morning… is going to double. Especially when war kicks off. Then the Greens will have what they always wanted. A world where everyone is freezing to death and no one can afford to drive or get on a plane.

Success!!! (as they say in Amsterdam)

MooMoo you speak Troo!

EU sovereign default on any meaningful scale would almost certainly coincide with a global credit contraction.

In such a scenario, there won’t be any shifting to US markets, it will simply vanish into thin air where it came from to start.

The rally against China isn’t bs. Mad man Xi accumulated the most

powerful nations as his enemies.

Just read a good article on globalization and China. Western world middle class was already fed up with offshoring to China and now they rightly or wrongly blame China for screwing up their life with the virus. Politically it’s an untenable position to defend China.

That’s Funny…Half (or more) of US Congress and the Senate has been making a fortune by investing in the place!

Happy you are going to die soon because you paid $50 for a mediocre meal!??

What the hell is wrong with you people?

Quit mainlining doomster porn and get out there and enjoy life.

Find something captivating to do that doesn’t require money in any fashion, and then when money isn’t worth anything, it won’t matter.

My covid fix is riding a 50 cc scooter which is basically a 200 lb 2.4 HP motorcycle. It’s a hoot if you pick where and when you ride. I like rural farm settings on back roads and will do a 50 – 75 mile loop.

I can entertain myself all afternoon for about $1.25 in fuel. Plus 30 mph is a perfect speed for sight seeing.

“Quit mainlining doomster porn and get out there and enjoy life.”

Yup, keep your head in the sand. These problems will solve themselves or our leaders will fix everything. They’re the adults.

Just say no to doomster porn. Go for a hike instead. Do cardio. Ditch the processed foods. Become a vegetarian. Enjoy life.

“Become a vegetarian. Enjoy life.”

Oxymoron? How to enjoy life without eating meat? lol jk

Crush the Peasants!

I love your dry sense of humor:

“Go for a hike instead.”

Yes, a RATE hike. And not just one. Those hikes were discussed near the top of this very article.

But no hike today. Starting next spring, when the weather is nicer, and there will be quite a few of those hikes, so enjoy, hahahahaha

I have little optimism for the future of humanity, but intend to enjoy this beautiful planet as long as it and/or I am here. Simple pleasures that are low-cost or free, and use minimal resources – ride a bike, teach a child, build something out of salvaged materials, observe Nature, grow a garden, make home made meals and foodstuffs, etc.

I’ve eaten a primarily plant-based diet for over 40 years, and enjoy not only the food but excellent health. While most Americans think the standard American diet tastes good, being meat, sugar, and processed food heavy, it is not healthy and what they will NOT enjoy is the coronary artery disease, diabetes, and colon cancer that goes along with it.

Governments like to monetize and regulate everything to buy votes and get revenue. In 50 years you will have to pay your wife to fix you a sandwich and she will have to pay you to take out the garbage. Politicians will tell each of you they are working for you, but send in the 1099 so they can get their cut anyway.

Crush the Peasants!

“…and get out there and enjoy life.”

Hahahahaha… being on Wolf Street = enjoying life! Why else would YOU be here???

“ Happy you are going to die soon because you paid $50 for a mediocre meal!??”

Dude,

It was Hooters and they had…. Well, you know…

The old marxist jingo seems to still apply

They know they are lying,

We know they are lying,

They know we know they are lying

But they still keep on lying.

The old adage that,

People prefer to believe in lies and can’t face the truth seems to be as popular as ever…

There is nothing new under the sun, that’s why they lie and cheat because they know (for the few) that it works everytime….until, of course, it doesn’t but by then they are in such a great position as to not care…

If you can accept that everybody is lying, then you will make a great trader…..especially if you don’t mind making a profit when the Fed (and other central banks) cheat the poor to feed the rich.

Applies to capitalists just as clearly. Lying has no favorites. The truth lies somewhere in between. Socialism isn’t the world wide evil. Neither is capitalism. It is the extremes of both that cause problems.

“Even the Fed, which engineered this money-printing orgy and is very slow in ending it, is now ending it, and it will be raising rates,”

Unlike Wolf I remain skeptical and will be amazed if the Fed balance sheet is appreciably reduced, and even more amazed if they raise interest rates above 1 or 2 percent.

They are trapped in a hole that they have dug with hubris, smoke and mirrors.

Gilbert

I don’t agree

Rates are going up no matter what the Fed does. Inflation is built into the rate structure. More printing and QE will just make the rates go up faster as the inflation premium soars. No one in their right mind will buy any bond will a maturity of more than 2 years.

right, that’s what people mean when they say that the fed can lose control of interest rates

I don’t know about that. I am not betting either way. Some make the argument that government debt doesn’t generate positive cash flows so the debt just becomes a weight to pull rates lower. Example #1 Japan, Example #2 Eurozone.

Policy makers have the power to change the monetary system so I don’t think it’s prudent to bet too big one way or the other.

So then why is yield so low right now? There’s plenty of demand for UST all along the yield curve.

Remember that other countries are in significantly more severe economic turmoil than the US. Brazil, Turkey, etc.

They are happy to receive mediocre risk free returns on UST?

peanut gallery,

“So then why is yield so low right now? There’s plenty of demand for UST all along the yield curve.”

Haven’t you heard? The Fed is still buying and will be adding $105 billion to its pile between mid-Nov and mid-Dec. It already owns 25% of all publicly traded USTs. Demand is coming from the Fed. Unlike traders that buy and sell, the Fed doesn’t trade. It only buys, which has a huge impact on demand.

But that buying is coming to an end.

We shall see ….

Gilbert,

The Fed is not “trapped.” It can do whatever it wants to until the President tramples on it. Now the President is trampling on it to get inflation knuckled under. This White House doesn’t own the Dow. Trump took possession of the Dow and ran with it. This White House doesn’t give a crap about the Dow. People still haven’t figured this out, it seems.

“The Fed is not “trapped.””

An important point, Wolf. Most people assume that the extreme distortions, bubbles and resultant inflation would force the FED’s hand. Not so. They have shown that they will happily destroy the country while front-running the markets and day-trading on insider information to amass fantastic personal wealth – pigs in charge of their own slop lever – while they create tens of millions of homeless people with their policies, having absolutely zero regard for the public good and ignoring all deleterious effects.

We shall see what we shall see.

“they were all ridiculously overvalued, and investors knew it, and they kept hanging on till the last moment to ride them up all the way, but they were sitting all bunched up near the exits, and when the signal came, they all rushed out together, causing those shares to collapse”

Sounds like cryptocurrencies, aka digital tulip bulbs.

To make that more accurate, I should have removed the “and investors knew it” part.

The Fed has conducted a “cattle drive” to stocks and real estate.

But we know how cattle drives end…..

Drunk Cowboys and steak dinners.

Wolf had done all of the heavy lifting documenting the truth in Fed overstimulation and subsequent inflation.

His website is a beacon of truth.

Sell.

Stock prices are driven by EPS growth and other factors. S&P 500 double digit earnings growth continued through Q3.

The 10 year interest rate is about 1.385%. The S&P 500 dividend yield is 1.31%.

If I had to absolutely have the money to eat over next 10 years I would probably take a 10 year treasury. Nominal income is guaranteed and you would know the nominal amount you were going to get back.

Stock market dividends do grow over time, but they decline during recessions usually, and with stock market at all time high you don’t know what value will be in 10 years. It’s a tough call. Maybe that’s why people are looking other places.

If you have very low risk tolerance and you are on a short time line then yes I agree with you.

But if you are young(er) and have (some) appetite for risk, there are so many ways to skin a cat.

Option value of cash will grow over time in the next year or so?

I think option value of cash is good, but I went to short term treasury fund about 6 years ago with duration roughly 2.5 years thinking surely top couldn’t go past 2018.

I have messed around with some single stock picks and got mid single digit returns last six years on portfolio. I am OK with it as I have lower risk tolerance now, but the last 6 years have been like nothing I have experienced before.

Some of the stronger but clearly overpriced stocks will start dropping more significantly next. TSLA. NVDA. BIG TECH. Then all hell breaks loose.

Screw the corporations!

Signed, your valued (cough, hack, choke) customer.

Wow. Thank you Mr. Richter for this. I search the internet and get bits and pieces of what you have masterfully put together here in one post.

The nifty thirty……..back in the 70’s were considered infallible. Led by IBM. Like most narrow markets it fell apart eventually.

All narrow markets in my lifetime have eventually collapsed. Its one of the signs of the end of a bull. Advance declines have been scary lately. Fewer and fewer stocks have been participating in the up days and more and more have been getting creamed.

Its simple economics…..how can Amazon do well if the other 500 S&P companies are not doing well. Their customers work for the 500.

I suspect the year end will be ok……but maybe sometime in the first or second quarter…….another of those generational lessons will be taught………some will learn……others will be dinner.

We have been operating in a don’t fight the fed decade…….the trouble for most investors is that they might have a hard time understanding that if the fed goes hard money…….don’t fight the fed.

Inflation is chewing up disposable income.

Leverage and margin are great things on the way up……and killers on the way down.

Eventually……S&P 1500 will be retested. Let us hope it holds.

Of course this mess could just keep on sailing until the water comes over the deck…….that would be worse.

right. no one has been able to explain to me who will fill the coffers of amzn, msft, fb, goog, and the others if the rest of the economy is bankrupt. who will pay for their products and services?

Fred. I am certain it was the nifty fifty, not the “nifty thirty”. And I remember them well.

It’s hard to stay on top. I remember reading a book and the number one performing stock over so many decades was Phillip Morris. They used to say that if the smoker had spent his cigarette money on the stock he would have been a millionaire.

Entire US markets are a hoax.

Thanks Fed for for destroying it

I read a few books on Buffet. He closed his original investment group when inflation got high (and if I am not mistaken the investors were placed in Sequah mutual fund ran by Bill Ruan.). Buffet owned no stocks for a while. Prospects for stocks were so bad as inflation took hold and PEs eventually dropped to 7. Why own stocks when you can get 18% on government guaranteed bond?

I find Wolf’s observation that individual (non SP500?) stocks are separately getting crushed. This has to mean that stocks outside of passive investing are getting killed.

Does this mean that passive investing is what is keeping the rest of the market afloat?

And if some estimated 70-80% of the total equities market is driven by large institutional investors, does that mean that those large institutions also invest via passive means?

I find it interesting how passive investing has changed the stock market – perhaps it increases volatility because larger chunks of the market go up faster (and go down faster?) when these large players all decide to go one way or the other.

Wait till the passive investors have had enough and head for the exits jointly and severally, hahahaha.

Can’t wait! Got my cash ready.

Now wait a minute… You’re contradicting your prior comments.

Yes, I, me, and moi, we got our cash ready because I’m negative on this market, and because I’m sitting on a bunch of cash.

But you’re bullish and invested. So what cash do you have ready? And if your stocks that you do have swoon, are you then going to be willing to throw more cash at the falling market after being down a whole bunch on your current portfolio?

Not contradictory at all. Cash came from recent sale of a house on the west coast ;)

Haven’t touched my equity positions in a long term 401k in probably ten years.

Aha! You dumped real estate holdings to cash out on that bubble!!!

What are you going to dump next?

The wife. Haha just kidding. Sort of…

I am not really that sophisticated of an investor. I have contemplated setting aside some play money to try and make some bets here and there, but the wife won’t let me.

I basically hold RE and SP500 long and only sell at pre-determined times to support life events and family needs.

The sale of the house was not for monetary gain (although it coincidentally ended up being so, at least in some small part) but was to support a move to a different part of the country for the sake of the family.

I learn a lot about the markets and various different aspects of money and finance here on this website (which I greatly appreciate and am indebted to both you and all the readers/commenters here), but I can’t say I am comfortable enough (or have built up enough expertise) to really do much more than buy long on SP500 and RE in the most basic way.

I found fascinating the latest OECD economic outlook report, and how there is such a vast difference in monetary policy between different central banks across the world. I initially thought that the Fed’s influence spanned the entire globe (and I think it does, perhaps to a certain degree).

But I wonder if there are any arbitrage opportunities converting USD to different fx across the world where yield is higher? Understood that fx risk is introduced, but there has to be some inefficiency somewhere in the world with all this movement?

Investing is a lifelong learning experience. Financial industry tries to complicate it. The free lunch with computers is cheap diversification. Your biggest enemy is usually yourself. Try to pick a style and stick with it.

Mike Green of Simplify Asset Management makes that point, which I’ll repeat here. Only about 1% of passive investors (at Vanguard? I forget) withdrew money in March 2020. If an even larger number sell their stocks, declines could be unreal, because now that active managers manage less of the market, there is less liquidity. In other words, active managers buy when P/E declines, whereas passive vehicles simply buy/sell to match customer deposits/withdrawals.

I think passive investors stuck it out pretty good in GFC as well I think most realize 50% loss is possible, but this one in theory could be bigger and I think that would feed on itself. If we really take out the trash, we could go down sub 1000 on SP500.

I’m a VG investor and I bought equities in March 2020. I remember being giddy each day watching huge declines in the market. Sadly, the Fed stepped in and ended my fun. I would have bought a lot more if it continued going down. Right now my buy targets are staggered between 20-75% lower than today’s prices. That’s not a typo.

The trouble with passive investing is that you can’t just sell one company. If you sell SPY you’re selling the entire S&P 500, the good along with the bad. That’s a massive asset dump.

Also everyone is trying to get through that same exit at the same time.

Bond funds have a particularly difficult time because they have to decide how much of their crap to dump vs how much of their good inventory in order to meet redemptions.

I read where 40-50% of 401k money was in passive mutual/index funds… several trillion…

Median balances are pretty skimpy ( across all age groups) if forced to liquidate….

I could easily see a scenario of a 40% or more loss ( equity and penalty) if you can’t get to the exit first…

Yes but something like 80% of all new money is going into passive and that flow vs stock is important too

It used to be $3/1 active to passive, and now it is projected to be $1/1 nowadays. If 80% of all new money is passive, then we are probably at or near the point where passive investing has surpassed active managed assets.

And like Wolf said, the herds will stampede harder and faster with this much passive money in either direction

PG – According to Mike Green of Simplify, ~50% of assets are currently passively managed.