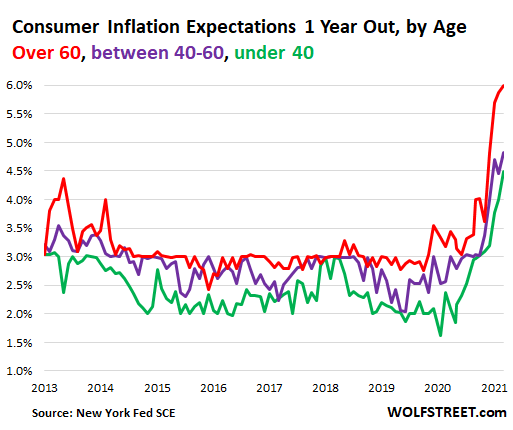

And those who experienced the 1970s & 1980s inflation as adults expect 6.0% inflation a year from now.

By Wolf Richter for WOLF STREET.

The Fed keeps discussing consumer inflation expectations as one of the key metrics in assessing the path of inflation in the coming years. Inflation expectations suggest to what extent consumers might be willing to accept price increases, thereby enabling inflation. Consumer price inflation is thought to be in part a psychological phenomenon, similar to market prices. When the inflationary mindset takes over, consumers accept higher prices instead of going on buyers’ strike as they infamously did with new cars in 2008 through 2013, when demand collapsed and stayed down for years.

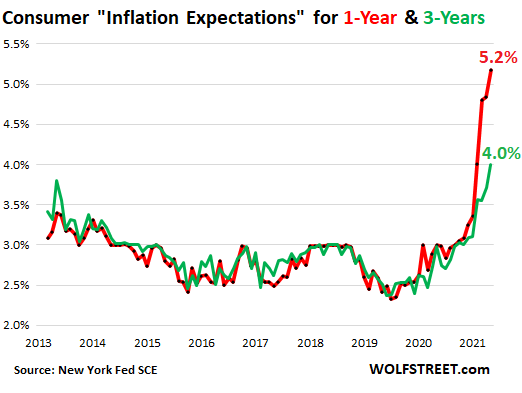

Consumers’ median inflation expectations for one year from now jumped to 5.2% in August (red line), the highest in the survey data going back to 2013, and the 10th monthly increase in a row, according to the New York Fed’s Survey of Consumer Expectations today. The survey also tracks consumers’ expectations of their earnings growth. And that combo became a hoot (more on that in a moment).

Inflation expectations for three years from now jumped to 4.0% (green line), the highest in the survey data. People are starting to blow off the Fed’s endless sermons about this inflation being “temporary” or “transitory.”

People who saw the 1970s & 1980s inflation as adults expect 6.0%.

The people who went through the last bout of massive inflation as adults in the 1970s and early 1980s, the people who have actual experience with large-scale inflation and remember what it was like – the over 60 crowd – they expect inflation to hit 6.0% a year from now (red line in the chart below).

The 40-60-year-olds expect inflation to be 4.8% a year from now (purple line). And the under-40-year-olds expect 4.5% inflation (green line).

The inflation expectation are actually worse.

Interestingly, consumers expect much higher inflation rates in the items where they spend most of their money – housing, food, gasoline, healthcare, and education – than what they expect for the overall inflation rate.

Just looking at these categories, and given their dominant weight in the CPI basket (housing costs alone, not including utilities, are one-third), it would seem that consumers expect inflation one year from now to be over 7% based on these categories, not 5.2%:

- Home prices: dipped for third month in a row to +5.9%

- Rent: +10.0% (new record)

- Food prices: +7.9%

- Gasoline prices: +9.2%

- Healthcare costs: +9.7%

- College education: +7.0%.

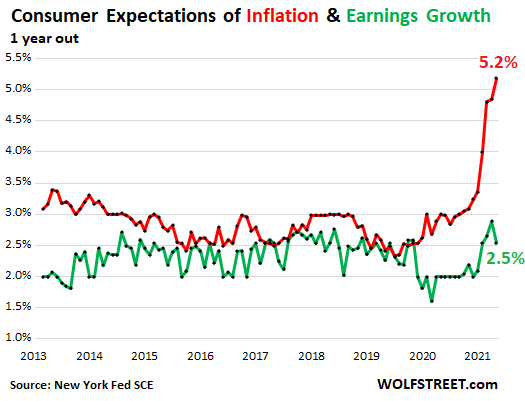

Inflation is expected to whack earnings.

Consumers expect their earnings in a year from now to be only 2.5% higher than today (purple line), down from 2.9% a month ago; But they expect overall prices to be 5.2% higher (red line). In other words, consumers expect inflation to increase at over the double the rate as their earnings. And that’s not fun.

Now compare that expectation of 2.5% earnings growth to their expectations of home price inflation of 5.9%, rent inflation of 10%, food inflation of 7.9%, gasoline inflation of 9.2%, healthcare inflation of 9.7%, and college education inflation of 7.0%.

If these expectations of big price increases and small income increases pan out, it’s going to be miserable for consumers at the bottom half of the income scale who spend all of the little money they make. But wealthy consumers, topped off by the coddled billionaire class, will be fine.

These inflation dynamics are taking place even as the Fed is still stimulating the economy with its 0% interest rate policy and $120 billion a month in QE, on top of the stimulative effects of the massive deficit spending by the government.

The Fed is approaching the point where it will dial back QE, but the balance sheet will remain bloated for a while, short-term rates are going to remain at near 0% for a while, and the government continues massive deficit spending for a while. So stimulus will continue, though at a slightly less massive blowout historic extravagant pace than today.

It’s totally unclear to me, and increasingly to consumers as a whole, why this inflation should be “temporary,” given that the factors that produced it – the most monstrously overstimulated economy ever – are still fully in effect and will remain so for a while.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Get ready for all those unintended second and third order effects of cratering the economy and filling the hole with money.

This money hole is an attempted whitewash of mistakes made by our fearful leaders over decades. Funds were distributed in a terribly inefficient way.

Why didn’t they use those funds to restructure our absurd finance run medical system during a global health threat where the US is way behind on public health care vs every other modern nation? >> Crickets… .

Remember the rule of 72 works in reverse too. 6% inflation means a doubling in 12 years (72/6=12). In other words, half your savings will be evaporated by 2033 at this rate. May seem far away to some and the young. Twelve years go by in a blink of an eye on this mortal plain.

I know this is a survey but I think we can all agree that there is a lot more inflation that 6% bubbling up in the system.

Except this is one of the most overly indebted economies in history. As inflation eats at real disposable incomes, it will also eat at earnings.

This is looking like Stagflation coming sooner than most think. As the real economy slows, as the earnings deflate, there will then come layoffs and defaults. It appears inevitable.

I agree that we are in for a stagflation 1970s redux style. I also think it will be shorter than that was, only to be replaced by viscous asset deflation.

My reason is that there is no other solution, barring societal collapse, than asset price destruction and those at the top of the parasite pyramid will plan to benefit; they don’t care about you or me, or our collective health.

Let’s see how many of the millions of recently off unemployment people get jobs in the next few months. I see societal decay everywhere… but I live in kooky PDX where everyone who doesn’t look like me is an automatic victim, and probably because of ancestors they assume are mine. Pure insanity here. Division in the name of diversity.

Unrelated to the topic but Just googlag at this:

Peter Boghossian

“My University Sacrificed Ideas for Ideology. So Today I Quit. The more I spoke out against the illiberalism that has swallowed Portland State University, the more retaliation I faced.”

I see crazy things like I’ve never seen before. Like naked women walking around on the street in mid-day on the way to the grocery. Twice in the last three weeks. Surreal. As are the compounding number of brazen homeless surviving on nothing and not caring about the wealth of old people renting their basements… talking to the angels, spray painting their stoops.

This is not a good setup for prosperity. Given, Portland is a petri dish of viral discontent. However, I suspect there are hints of this everywhere.

How much unaffordable can life be without society bursting at the seams?

Otis – I’d like to concur with you that viral discontent is everywhere. Unfortunately I can’t. Portland appears to have a franchise on abhorrent behavior. The rest of the U.S. watches this stuff and just shakes our collective heads. Can’t think of any city that spent an entire summer burning itself down.

Satya, check the comical link i referenced as a search term. Unfortunately this is everywhere, sorry to say, and most prominent in higher education.

I’ve said it before. Don’t hire recent grads. They are time bombs of learned grievances.

At some point you are going to hit peak multiplier such as price to sales and then even if you keep it pegged there you are going to be limited to about 2% inflation adjusted sales growth max therefore about 2% real stock growth max. But things will not stay at peak price to sales ratio because someone is going to head for the door.

In actuality stocks have got four government head winds:

1. Inflation.

2. Increased corporate rate

3. Increased capital gains tax

4. Congress has incentivized people to consume without working

Otis, Portland is just ahead of the curve. We were the first to embrace recycling, and microbrew beer in a big way, and now we are the first to adopt the distopian blade-runner aesthetic. I guarantee others will be following along soon, as they always do.

Otis – when my folks used to drive up to Seattle every year or so in the 1950s, Portland seemed like an industrial town. We sometimes stayed at an alcoholic merchant marine uncle’s house, which seemed a bit scary to me as a kid (low income working class area). Recently, I stayed in Portland a while at a cousin’s house when unemployed between foreign jobs (no unemployment insurance).

While your description seems mostly hyperbole, I can relate to it through various experiences I’ve had — not only in the United States. About five years ago, between overseas jobs, I went up the British Columbia (to avoid spending 35 days in the U.S. that triggers requirement to pay U.S. taxes). I stayed in various low-price hostels, bed and breakfasts, etc., at one of which I met a “first people’s” young woman. Over breakfast, she lectured me (in loud emotional voice) about how being white, I was basically a participant in evil violent racist genocidal culture that subjugated and raped women (she would not answer questions about male-female relations in her traditions “first peoples” culture).

She was on her way to Vancouver, to enroll for a university education that was 100% paid by the government. There seemed no doubt in her mind that her whole life, almost anything she desired, should be fully paid for by the government as a kind of reparation for the past.

But, regarding Portland, for me the entitled victim people aren’t the major reason to avoid. I’ve retired here in Thailand because America’s angry, in-your-face, divisive, simmering violent culture is too stressful for me.

Well, seems a growing number of women are choosing not to work full-time, some choosing not to work at all and stay home with children.

I’ve even noticed this in the healthcare industry where there are extreme shortages of (senior residential facilities) Home Health Aides… They were tired of excess workload due to staffing shortages so they stopped working… contributing to greater shortages. Sigh…

https://pewrsr.ch/3DJdIj0

Stagflation sucks.

I think it’s already here.

Stagflation? Sounds like fun. Your bonds and CDs lose 20% to inflation in two years, plus your stocks drop 50% or so. No sweat.

Will Powell send us a free copy of his book?

but now that you have CHEAPER(devalued) $$$

it will still cost more $$ to buy same

you just won’t have more wages

savings been getting smashed for over 10 years

over 1/2 retirees have less than $10k in savings and only ssi for income

personally have lost over $100k in interest from govt stealing(ie NIRP)

Stocks are ultimately destined to lose a lot more than 50%. Most overvalued market in history, by far. US market is an outlier in deep outer space versus other countries. P/E high even with inflated earnings from a fake economy.

The Dow lost 89% from September 3, 1929 to July 8, 1932. This mania is much bigger and the loss should be greater, measured by constant prices.

It took about one once of gold to buy the Dow in 1980. It took almost 40 in late 1999. It now takes slightly less than 20. At the bottom of the bear market, it should be below 1 again, from lower stock prices and higher gold prices.

Fiat money allows economic imbalances to just get kicked and kicked and to grow and grow until the house of card collapses. At least with gold when your gold started all flowing to your trading partners you had to address the reason why.

but gold isn’t money /s

Except inflation is a tailwind for fixed rate mortgages. Imagine the 1970s without the housing bubble (and there was no access to your home equity.) Course this will kill the REFI market and a lot of old people have even longer mortgages than lifelines. Lenders have all sorts of provisions to get you out of their low rate loan, and maybe there will be more liquidation than in 2008, at least in the lending business. What am I saying, you have a 3% loan your lender hits the skids, and sells to lender B, and he calls your paper. Now you’re back in the market for a mortgage and you have very little equity because you traded it for time and low rate, and the rate is gone. I could never understand that consumer decision. Now that CPI actually dropped or the rate of increase, yields are rising. If I don’t miss my guess this will fuel an even bigger frenzy in home buying which has been slowed by supply. There is no shortage of money and never will be. Just who gets it. Whats happening in China right now is instructive. A whole new bevy of FHA programs in the US probably and plenty of USDA cookie cutter ECO shacks for the nouveau homeless.

Ambrose,

This statement is interesting. Can you elaborate?

“What am I saying, you have a 3% loan your lender hits the skids, and sells to lender B, and he calls your paper.”

I believe that my current mortgage in the US is a contract for the term of the loan. ie 3% for 30 years. I don’t think it can be called without breaking a legal contract. Can you elaborate on this? Given that rental contract law has been ignored during the pandemic with eviction bans, I suspect that given enough banks and mortgage lenders (too big to fail) putting enough pressure on government, that these current low rate mortgage contracts could be in danger of being reset to a higher rate or called.

In the 70’s, my parents had a 6% mortgage while making 15% in government insured CDs. There was no motivation for them to pay off their mortgage with these conditions. There wasn’t any talk at that time about resetting or calling mortgages. However the pressure of mortgage lender lobbyists was likely not as strong.

Given that, as a consumer homeowner, I’d benefit greatly if savings rates were 15% and my mortgage was 3%. However, MBS’s and Fannie and Freddie would have to be bailed out.

Bob, post GFC the Fed bailed out the TBTF banks, and the process of liquidation was averted. In a free market, strong banks buy up the paper from weak banks which go under. That’s capitalism. That doesn’t mean the rules were abolished. The Fed has unlimited taxpayer reserves to accomplish their goals, and obviously they don’t want to see homeowners go through an industry wide mortgage reset but they encouraged homeowners of ample means to continue using the mortgage market for tax purposes. Now many of them are sitting a lot of equity, and in a reset the hunt for equity will become acute. So if you are in a REFI you should have the cash or assets handy to buy out your mortgage or face the consequences. Relative took out a loan to fix the house he inherited free and clear from his parents, from Countrywide. They went under and he couldn’t find another lender, and the house was sold at foreclosure. He works for the government. He still rents

Never heard of mortgage lien holder being able to accelerate the balance outside of default.

Thank you, Ambrose.

I also held a mortgage with Countrywide when they went under. Fortunately for me, my loan was sold off and I had to send my payment to a new lender who acquired my mortgage. My mortgage contract did not allow it to be arbitrarily called unless I:

1) Sold the house

2) Was in default in payments(pre-foreclosure) or default in taxes.

My current mortgage has the same conditions. It is currently owned by Freddie Mac. The loan contract explicitly states that the loan does not have a demand feature.

Demand Feature

Your loan

has a demand feature, which permits your lender to require

early repayment of the loan. You should review your note

for details.

X does not have a demand feature.

This was a line item buried among thousands and truthfully, I may never have considered this without your comment.

I will check any new refi for the fine print on this.

If I was a lender loaning at sub-3%, I may include a demand feature in contracts to avoid holding a 3% loan in a 15% environment.

I suppose if enough lenders and Fanny and Freddie were underwater, Government could call or reset the mortgages but that would be a major violation of contract law.

In 2009, the way the worst banksters implemented “demand feature”, despite contract language to the contrary, was to transfer the mortgage loan-servicing arrangements, doing the paperwork so badly that everything was hopelessly screwed up.

Banksters claimed to hold mortgages on property that wasn’t rightfully theirs, got robosigners to fraudulently rubber-stamp the erroneous paperwork, then claimed that owners weren’t paying and foreclosed on them – with prejudice.

“Rocket Docket” courts then rubber-stamped the banks’ claims without due process, and many homeowners were denied (or could not afford) to appeal. This was quite well documented among the non-mainstream media, and remains one of the greatest injustices in history, driving much of todays animosity.

If banks start to go belly-up again, pay very close attention to your mortgage and demand to “show me the note” before accepting anyone’s claim to hold your loan note.

The key to preserving wealth is placing it into vehicles that appreciate in value in conjunction with inflation or ahead of it. Such as real estate, gold, silver, etc. The dilemmas are finding vehicles that allow you to avoid tax penalties while owning them, such as real estate. For example, gold in the last 50 years has fluctuated from $32\oz, in 1971, to $2,000/oz in 2021. But, relevant to these times, one ounce of gold would buy a really nice mens suit, or a really nice dinner and perhaps an evening in an extremely nice hotel. The same value value realized by the same slug of metal, only the price point of the gold changes. But this is also an indicator of the decrease of value the dollar as a measure and store of wealth. Just like the Russian people discovered in the early 90s after the destruction of the Soviet Union as the ruble plunged in value so as to become almost worthless. The US is on the same path.

When you get down to it and inflation gets serious companies have to raise prices. The relative winners will be the companies that can do that, the others are going to have a tough time.

and who OWNS companies – 1%

called TRICKLE UP economy

reagan had it wrong

I’ll add that inflation harms almost every person who works for a wage. The main benefit goes to those who own long-term debt at a fixed rate or countries that have high debt to GDP ratios… like the US. In this case, cheaper dollars pay off the debt. hmmm, I think the Fed kniws exactly what it is doing.

Other than, ”The main benefit goes to those who own long-term debt at a fixed rate…” which is exactly opposite and I am thinking your ”typo,” I agree with you SG:

Inflation is only good for those of us who OWE debts with long terms…

For those of us with NO debt at all, it sucks,,, as the Fed knows full well, and it is a surprise to many to see them doing their best to degrade the USD again and again and almost always since 1913 when they were allowed to take over USA…and since when the USD has lost 99%, possibly more, of it’s ”value”…

Only when we consider the fact that oligarchy IN USA and global have most of their investments in ”non dollar denominated” assets can we realize what the oligarchs have known very clearly ”for eva”,,, and that is that they can manipulate EVERY ”currency” to their clear advantage and to the very very clear DIS-advantage of WE the PEONS,,,

Just exactly as has been done since at least the Magna Carta…

Pretty sure Steve meant “owe long-term debt”, not “own long-term debt”

Werd!

The government will never say when conditions are hyperinflationary. It just happens. The hyperinflation game appears to be in the second inning right now.

When our biggest assets, housing and automobiles, rise 15-20% in one year across the country, we are clearly heading down a hyperinflationary path. There has been no Federal Reserve counteraction to date, just more fuel on the fire, so expect hyperinflation to continue.

Don’t listen to what the Federal Reserve says. Look at the facts on the ground. 15-20% inflation in key asset classes. Food inflation running at 10%. Service inflation running at 10%. That is all you need to know. The middle class is under attack.

Like two weeks to break the curve?

Well, at least we are all in this together.

“It’s totally unclear to me, and increasingly to consumers as a whole, why this inflation should be “temporary,” given that the factors that produced it – the most monstrously overstimulated economy ever – are still fully in effect and will remain so for a while.”

When things get serious you have to lie. (John Law, Ben Bernanke, Janet Yellen, Jay Powell, Super Mario.)

First….there is no inflation

Second…there is but it is only transitory and is explained away

Finally, acknowledgement and meaningless 1/4pt increases, well behind the curve

Hold the Fed to their mandates.

Wolf… it’s interesting what you indicate about age and expectations. It’s almost as is the youngest generation seem to have more hope for the future. I wonder if Millennials and Gen Z are going to get the rudest awakening of a life time that will forever scar their economic psyche in a few years

60 year-olds remember the 20% inflation days of the 1970s.

No one under 50 has ever really experienced that kind of real inflation.

2banana,

Yup I remember those days when people were excited to get a 16% interest rate on a house, credit cards were 22% on average. Today, I would be thrilled with 4-6% inflationary rate on anything. Shadow Stats site indicates a true 10 to 12% inflationary rate. And hyperinflation is just around the proverbial corner with the money printers going BRRRRR!

I paid 9% ish on an FHA loan in 1997. I thought 7% was a screaming deal when my boss told me that was his rate. Then my house went up in value to 600% in 2005 when I sold it only to drop by 2/3 and end up in a short sale in 2009. Huge learning experience. At least I was the seller and not the buyer in that case.

I still remember the buyer at the closing table smiling like a Cheshire Cat when he heard my payout. His short sale was less than my payout. Pulled up in a convertible white 3 series BMW with a bleach blonde probable fourth wife first time he saw the place. Plastic breastopods. I liked them at first sight.

Hubris kills. Not that I ever meant them any harm but just goes to show you young punks to be careful. Timing is everything and it plays out over years. One wrong mistake and you are screwed for life.

My place was on an island with a salt water canal in the backyard and no bridges top the bay. Inland, property prices dropped by 80%, for cinder-block houses with pools in the Florid-Duh.

Deflation happens.

“The struggle against power is the strugle of memory against forgetting”

~otishertz 2009

Awesome

MCH,

“It’s almost as is the youngest generation seem to have more hope for the future.”

They should since they’re going to be around longer. But it may also be lack of understanding of how an inflation spiral works, not having been exposed to one yet.

Funny how opposites happen. Friends in college in the early 90’s said we’d never have the opportunities of our parents, so why try. Yet, as we saw, they had incredible opportunities. As did I.

People decry the dearth of marriage and child spawning, yet that will yield unforeseen opportunities for those rare progeny that survive. Funny how it works out that way.

And thus the pendulum swings.

I wonder if the implication here is that once they get a real dose of pain, not the minor kerfuffle that was 2008 or last year, whether they’ll become even more cynical about things in the future. The younger generation is getting set up for some serious nastiness in the next decade. And the more the government tries to “help,” the worse things are going to get. Worst of all, most of them will have no idea what’s coming, and they aren’t going to understand when the sky comes crashing down.

It’s funny how you’re writing about inflation, commenting about an inflationary spiral, and have said repeatedly deflation is and has been rare.

Yet all the comments are prognosticating a deflationary spiral and crash. It is like they don’t even read what you write.

It’s unknown how it’s going to play out other than not good. Possible scenario is inflation runs hot forcing Fed to tighten immediately crashing stock market and then real economy. Fed goes back to even larger stimulus to juice market and economy. Rinse and repeat.

Up from 0%. In California it’s over 8% now.

Americans don’t even yet have a full range of products. The most popular vehicles in the US are pickup trucks, and they’re just now coming out in EV versions.

Effectively, in terms of large numbers, there was only one EV brand you could buy in the US. All other brands had very small-scale experimental efforts, including GM’s Bolt, to test the waters and gain experience (expensive experience, it turns out).

The growth rates of EV sales are huge though. It’s the only thing that is growing in the auto industry. And that will continue. It’s where all the growth is. The ICE segment is in decline. That’s why EVs are doing “great.”

They’ve grown up during the biggest inflation in history, stocks and real estate, bitcoin, something from nothing, what they won’t like is deflation.

They have no frame of reference, and no direct experience with blow torch type inflation, so ya.

The young generation have zero hope for the future. All blame goes to old people or as they say boomers. The dont see themselves owning a car or needing a drivers license. Owning a house thats funny to them as if. Think of it this way, all the old people scewed the earth and all the ceos took the money and full time minimum pay wont rent you a apt. Honestly might as well couch surf never going to get ahead at this point. Aka Portland might as well burn everything down the rude awakening will be on the Boomers. FYI im 46.

This is not my personal view but what I have heard. I work with under 20 year olds. Also none of them can use cursive and almost all could not figure out how to write a check. I told one of them just sign your signature with a X if you cant use cursive almost as a joke. Yep she signed it with a X.

Glad to see our education system is preparing the young people so well for the future…. “Here is who you go to blame.”

Geez, can’t figure out how to write a check, I’m going to guess you’re actually trolling here… because I just can’t imagine that level of unpreparedness.

Not trolling at all, a class does not exist anymore that teaches kids any of the finances of how to balance a checkbook, maybe a college class but definitely not high school or under. But in reality kids don’t need to balance a checkbook they use debit cards nobody and I mean nobody uses checks the last time I ever used to check was to set up my direct deposit my father who’s in his 80s uses checks but he also is the mentality of taking out $100 bills from the bank and trying to get them broken into smaller amounts he is the bain of cashiers and whenever he tries to cash a check at Safeway he holds up the line, it is the worst thing. I cannot get him to get with the times at all in fact my wife a teacher had to explain to a kid greater than and less than by saying it was like Pac-Man kid said what was Pac-Man.

If that’s bad here’s worse. I went to am I’ve cream shop in Asheville and handed the recent HS grad cash. She looked at it like she’d never seen it. Then struggled to give correct change even after the cash register did the math. Help us!

I can’t write cursive and I don’t see this as a big deal

I am 50 year old

@Red

Sorry, didn’t mean to disparage. I just can’t fathom such a poor level of education. And although I agree on not needing to balance a checkbook, the minimum one needs is still to try to understand their own finances.

I can agree the cursive is no big deal. But, the math example you cited sounds just incredible, I’m going to assume that these are may be 3rd or 4th graders that your wife is explaining math to who doesn’t get the concept of > or <.

This is just sad.

On your comment about the bane of cashiers… I think I wonder if the reason there are signs everywhere not taking cash or asking for exact change… there isn't a coin shortage, there is a shortage of qualified people who can sort change and add it up in their heads.

There is no coin shortage. It’s just more malarleysalami. It’s not possible. Only something like 3% of coins in circulation are minted each year. Coins didn’t just vanish from existence. Banks are pretending. It’s an effort to get people away from cash, yet again. Pretty obvious… .

otishertz,

“There is no coin shortage.”

There actually was a coin shortage during and after the lockdowns because coins stopped circulating as people stopped using vending machines in public buildings and they used laundromats less often, and many retail stores and restaurants were closed, and some bank branches were closed, and because even many of the holdouts that still paid cash until then started switching to contactless payments, etc.

This was well documented, and even the Fed, which is in charge of making sure there is enough currency out there, wrote a series of articles about it, convened meetings to address it, etc. You can see some of this here:

https://www.federalreserve.gov/faqs/why-do-us-coins-seem-to-be-in-short-supply-coin-shortage.htm

It’s not that there weren’t enough coins per se, but they weren’t circulating, and people sat on them, and companies that needed then to return change couldn’t get them. For them, it was a real shortage (something you cannot get).

My 18 yo son wrote a check on my account and signed it “ my dad”

Unbelievable

Learning to balance a checkbook is not outdated. It’s basic personal finance. Most of us still have bank accounts. The same principles apply whether or not you use paper checks or reveal the bar code on your wrist and make a touchless (recorded forever) transaction.

Might be location dependent. I know a lot of people in their 30s and 40s that are doing better than I did. I am in central NC.

Most I know are doing it the way I did slogging it out day by day in a corporation. They have the house, the nice car, the six figure 401K.

There’s a shirt that says “I’m a millennial and my retirement plan is societal collapse.” Seems accurate.

Same age as my older one, who with spouse also a professional teacher, both with MAs, for HS and middle school have gone from CA to HI and are both loving it to the nines…

Younger one, totally great carpenter/GC, equally working along side spouse, loving the ”project focus” and making even more ”net” than the teachers..

Clearly, some on here focus only on the negatives for their generation,,, which I will be happy to say I did the same about 50 years ago,,, only to find that IF and only IF in those days, I got my ”act” together and worked hard ,,,, literally ”can to can’t” I could also at least pretend to join the ”slouchers” of my generation…

Unfortunately, when I ”retired” a couple of times,,, it was SO damn boring I was climbing the walls after a few months, and found a lot to do,,, and during the down times upgraded my digital skills and then found that companies really and truly valued my skills and experience in the field, etc., etc…

IOWs, get over yourself,,, study UP if you are not up to speed in your industry,,, etc., etc., and you will find you are, in fact, valued for both long term experience and current skills.

After LBJ’s election in 1964, the country faced the choice of “Guns” (the war in Vietnam) or “Butter” (LBJ’s Great Society Programs). LBJ decided to pursue both goals at the same time, which caused inflation to get out of control. Americans don’t read much history, and they have short memories concerning financial matters anyway. So the younger generations should prepare to get kicked in the teeth if the politicians don’t clip the Fed’s wings. Of course, the politicians are unlikely to do that because the Fed is making the politicians richer.

LBJ also moved Social Security (which was off budget, had its own accounts and had a surplus) into the general Federal Treasury to hide the real depth of the massive deficits of the war/butter thingy.

I should have added that the inflation of the LBJ years led to the formation of OPEC and rising oil prices.

Which led President Carter in 1977 to form the Dept of Energy to make us energy independent (from OPEC). We finally achieved that goal two years ago under Trump.

Today we’re once again relying on OPEC+1. WTF

Nope. US imports from OPEC are minuscule. They’ve plunged from nearly 200 million barrels per month in 2008 to about 35 million barrels in June (a little over 1 million barrels per day).

US exports of crude oil and petroleum products hit a new record in June, over 9 million barrels per day. This trend started with the shale oil boom in 2009. The US has roughly a balanced trade in crude oil and petroleum products.

The US has been a natural gas net exporter for years and the trend continues.

Dang it, I thought we were already at peak oil decades ago. This dinosaur juice sure is plentiful. Good for me in my old 350 V8.

GOOD POINT 2b:

Up to the point LBJ managed, somehow, to raid the SS ”Trust Fund” to augment the general ledger,,, SS had always been on a sound short and long term basis due to SO many folks paying into it and dying before they collected any or much…

So, possibly, with the absolute focus on truth on Wolfstreet,,, we may possibly have an actual ”reckoning” of the truth of the SS situation, we can , at least, hope, eh?

As I read they, the corrupt they, are arguing once again to try to reduce the pay outs to the young boomers and other similar youngsters…

Please, asking to you folks on this wonderful site, similar to MG, and way beyond me at this pint,,,

IF you have the skills to be able to discern what might be the case today if the GUF MINT in the clear control of the oligarchy did NOT degrade the SS program then and since,,, what would be the health of that program today…

Thank you all.

“One of the delightful things about Americans is that they have absolutely no historical memory.” – Zhou Enlai

It is temporary inflation, it will be long forgotten well before the heat death of the Universe.

On a long enough timeline the rate of survival is zero….

Except in the 70’s and 80′ we still had a functioning economy where people went to work and made things, grew things etc. so we could consider this kind of inflation temporary and we could work our way out of it. Now we have an economy based on stimmies, pot shops, youtube advertisements and entertainment. When printing money is your main productive activity inflation is baked in the cake.

in the 70s and 80s

WE HAD A FED THAT FOUGHT INFLATION…

now we have a FED THAT PROMOTES INFLATION..

what changed?

Politics.

Marching orders from the invisible shot caller.

Probably from the same confederacy of dudeness that’s whispering in Fire Marshall Biden’s earpiece telling him which “reporters” to call on next, according to the list he was given, like he said on teevee.

But the Fed is apolitical and independent, right?/s

What changed is we have a new ilk of central banker that serves different masters.

> in the 70s and 80s

WE HAD A FED THAT FOUGHT INFLATION…

Apparently you never heard of Arthur Burns, the Nixon-appointed Fed chair who Nixon arm-twisted into an increased money supply to win the election of ’72. Along with LBJ’s two wars (in ‘Nam and on poverty) financed without sufficient tax raising (i.e., with a form of invented-printed money-credit), that’s where the 70s inflation came from. Oh, and 60s consumers’ dollars going offshore for consumer stuff before that. OPEC’s price hikes were a knock-on effect of all that. It was a big party ending in a bad punchbowl. Only at the desperate end of that ordeal did (Carter appointee) Volcker appear as the first guy with any backbone to fight inflation.

My brother in law is a typical elite coastal white collar liberal. I have tried to explain to him numerous times that negative real rates crush the middle class but he insists despite me even sending him here that printed money is necessary to fund endless need to combat the Covid and Climate crises.

He finally relented when he went to buy a home a few months ago. He is still a proponent of demand side economics and MMT but he realizes now he is no longer middle class if owning a home is middle class despite making nearly 300k a year.

That is so typical of the Champagne Liberal

For the common man…who is getting slaughtered with negative real rates and every day inflation….

But, against fighting inflation for it might harm the “portfolio”

300k a year in Boston is not buying you much within 15 miles of actual civilization.

I feel bad for him. He will never get ahead and will be working until he is 75.

The northeast is filled with this mentality. That money should have no value. It seems to permeate western society at this point.

I just sold everything and moved out of the Northeast. I am done with it.

You can get a decent/okay home within 15 miles of Boston making $300k a year. It will just be very modest in size and yard

Depends how important the location is versus the swaths of 4k 90s/00s McMansions you can buy for 1/3 to 1/2 the price in the southeast or southwest.

Being rich is making $300k and renting.

The money crater I reference will lead to inevitable deflation. It is the only remedy our controllers have left to mitigate the mess they created. If you are old enough you have seen how this plays out.

Inflation has been caused by the extreme money printing, credit creation, and manipulation of the risk/interest rate curve. Plus the artificial demand manufactured by pulling demand forward with health care stimulus.

It will reverse. Deflation nowadays has usually been brief, due to the implicit and expected Fed Put, but there have been times outside of most of our lifetimes where it lasted for decades. Times like the end of the roaring twenties where the same problems of today were manifest and laws were thereafter created to prevent a recurrence. They were largely later repealed by you-know-who. see: Glass-Steagall.

Except the dot com implosion of the nasdaq. That was recent. People probably remember that. Took a long time for people who bought stocks in 2000-2001 to get their money back.

Those austere folks who create credit at will will be the first to benefit. How could anyone not make millions knowing for certain what the FedHeads will do in advance. Maybe that’s why congress members are immune from insider trading laws.

Any simple redditor could retire on options if they knew what the private kleptocrats know in advance. Don’t be fooled by their bluster and please don’t call them “elite.” They are parasitic plutocrats.

Has anybody been able to pin down what the Fed considers a “temporary” length of time? Because the double digit inflation of the 70’s was temporary; it only lasted 10-12 years.

Powell was asked about that. And obviously, he dodged it. But he and others did say some things over time that I interpret to mean that mid-2022 might be about the end of “temporary,” maybe even early 2022, depending on inflation expectations and other factors. The Fed IS getting nervous. This is far more far faster than they ever expected.

It is about time that they got nervous. As professional economists, a restoration of inflation on their watch after 40 years without would be written on their tombstones.

“When the inflationary mindset takes over, consumers accept higher prices instead of going on buyers’ strike as they infamously did with new cars in 2008 through 2013, when demand collapsed and stayed down for years.”

My question is sort of related to the article, but do readers think that people are willing to support high prices for new automobiles because they despair of buying a home? “If I can’t afford even a basic house, I might as well indulge on a bright new shiny vehicle?”

Maybe someone should tell people the worst investment is a new car instant depreciation then continues until it’s worthless scrap simple really

Agreed in normal times, but depreciation has been nil in my vehicles lately. I write off about $500 every month, and check KBB and listings a few times a year to recalibrate. Depreciation has been near zero for a year or two. Weird stuff.

Depreciation on my mint condition 2005 Mustang convertible with 64,500 miles on it has flat-lined. It’s stuck at around $5000. I only drive it a few thousand miles per year now that I am retired. Looks like it’s here for the long run, probably longer than I am here for.

Not true in my case. Purchased a 2019 Jeep Wrangler Unlimited Sport for $40, 250 out the door. Two years and 25,000 miles later my Jeep is worth $45,000+.

@MiT:

You can live in your car, but you can’t drive your house.

That’s one way of looking at it. But it’s not just about high ticket items. Its about everything. For some people it will be about doing their grocery shopping at the beginning of their pay period instead of the end when prices have been increased. Every little bit helps when they’re trying to make ends meet.

July CPI in the U.S. was up 5.4% YOY.

Gasoline costs $3.165 (EIA).

A one pound loaf of white bread costs $1.49 (St. Louis Fed).

The cumulative effects of price surges add up. The minimum wage is no longer $2.10/hr like in 1975 when I got my first summer job.

The Fed says they want a strong dollar and stable inflation., just ..,, lies, lies, lies

They are the worst type of politician. All they care about is trying to cover their constant regular mistakes. Bubble after bubble until they have socio-economically changed Society how they want it to look. A globalist hell-hole with the Elites in charge

in the 70s and 80s

WE HAD A FED THAT FOUGHT INFLATION…

now we have a FED THAT PROMOTES INFLATION..

what changed?

about a thousand basis points

“and stable inflation”

they are mandated to “stable prices”…ie FIXED.

There is no such thing as a moving inflation being stable…

> they are mandated to “stable prices”…ie FIXED.

There is no such thing as a moving inflation being stable…

Well, yeah, that’s what regulating is. Like your heart rate or blood pressure (or the temp of the climate), regulating mechanisms nudge these values to keep them within limits. These values fluctuate and a proper regulator keeps them in ranges, i.e., “stable.” So yes, regulating prices is to some extent “fixing” them. But here maybe you are borrowing terminology from antitrust law to describe a private combination or conspiracy. The Fed may be off track now, but has supported the values of my assets, except now not cash so much. There it flexed toward its mandate of full employment. The latter was an add-on by Congress in a time of radical government hubris in the USA — post WW2.

If natgas stays at these levels, the next round of regulatory price increases for utilities are gonna hurt.

Inflation is really not that bad yet. Hasn’t affected my lifestyle yet. Those days may be numbered. The worst is yet to come.

Home prices: + 5.9%, who cares, don;t plan on moving anytime soon

Real Estate taxes – neglegable increase

Rent: not affected

Food prices: +7.9%, Don’t eat that much anymore. Buy mostly produce and fish which haven’t increased much. Don;t eat much red meat.

Gasoline prices: +9.2% don;t drive more than 5K miles/yr, deduct work related business use off my taxes.

Healthcare costs: +9.7%, BC/BS premiums went 9%.. big impact

College education: +7.0%., done with that and my kids. No loans

Fed Pension and SS income – adjusted for inflation every year.

Golf green fees – little change

So other than home maintenance most of which I do myself the only item going up with this Inflation that is really affecting me in the cost of medical care and med insurance. I’ve created a medical savings account to cover unexpected expenses.

Things are going to get much worse with these incompetent morons running the Fed, Executive branch and Congress. Nothing good will happen with them in power. I see a Stagflation economy worse than the Carter days and inflation at 12% or more by the end of the year followed by a Real Estate crash when interest rates start to normalize, with or without Fed action. You can take this prediction and put it in the bank.

Make sure you don’t go car shopping.

My dream car. 1955 Buick Road Master. Not sure it will fit in my garage.

@ Jed:

If it doesn’t fit, just press the gas a little harder.

I’m hanging on with my fingernails to my 2000 Toyota and 2003 Subaru. Registering with the DMV as historical vehicles. Won’t have to get emissions testing as a result.

You got to be careful that you don;t get into some minor fender bender with your old junker car. Ins companies don;t like to fix any car below 2K. They want it totaled. Went through this several times with my Nissan Sentra. Had to go through some adversary ins company who didn’t give a S$it about me or my car.

They want to pay you off and then you are stuck going out and paying top dollar for some used piece of S$it used car, or a new car at $40K. Its lose , lose, lose. Ins company doesn;t lose anything. They just raise the rates on the dude that caused the accident.

You overlook that as home prices increase, real estate taxes also rise. My annual tax assessment went up 18% last year, the 8th year in a row for double digit tax increases. And those are taxes increased without a corresponding increase in my personal wealth, even though the property is worth more.

When this happens it’s an increase in the cost of living that directly impacts the homeowner, and the heaviest impact is on those with fixed incomes.

KGC

Mine did not go up much

“Bottom is when you decide to stop digging your own hole.”

Funny how the bottom can seem so much like the top, like freedom, like a joy ride even to people who are addicts, delusional, in denial, etc.

With inflation raging at such a high rate, why do mortgage lenders continue to loan money at ridiculously low rates when the inflationary rates for virtually everything are in the WTF category?

Because the government buys most of the mortgages and investors buy the rest. And MBS issued by the government entities yield just a little more than 10-year Treasuries. And the Fed buys both at a rate of $120 billion a month.

Does anyone have an idea as to why the Fed would buy so many billions in MBS, monthly, in the most historic property bubble ever, ostensibly to prevent a collapse of the same bubble?

I’m confused. Someone help me/.

Where does this need to buy garbage realtor excrement originate?

Powell says it doesn’t matter much whether they buy treasuries or mbs since they are similar products to investors the Fed buying either bring down the cost of borrowing for a house.

Now at this point why they think mortgage rates (and therefore savings rates) should be lower I don’t know. I think it is because the sophisticated model they use to make decisions tells them that is what they should do. But Larry Summers tells them they are screwing up big time facilitating Congress spending like drunken sailor.

Inflation of gas stopped me from looking at and buying a cheap used SUV today. Gas is up 66% since Biden took over. I was weighing the pro’s and con’s for so long—gas prices are what set my nerves free. I will drive my loathsome old clanking clunker until it falls apart on the road. I’d like a $17k Korean crossover but suspect the “chip shortage” will continue to keep them off dealer lots for another year.

Hey—I didn’t type the current guy’s name. Maybe you’ll do that for all other descriptors used for the previous guy also?? le sigh

Biden is Biden. Trump is Trump. Obama is Obama. For extra credit, write: “President Trump.”

My default reaction to pejoratives, made-up names, or descriptors for political figures is to delete the entire comment. If it’s easy to fix, and if I’m in the mood of fixing it, I’ll fix it.

I don’t catch them all, but I catch many of them. Been doing that for years. You should have seen the descriptors for the previous guy, from the presumed size of his genitals to the color of his skin to comparisons with Hitler. I was very busy deleting stuff.

See commenting guideline #7:

https://wolfstreet.com/2017/10/07/finally-my-guidelines-for-commenting/

Thank you for doing that! Politicians do stupid enough stuff that we can criticize without resorting to childish namecalling. To me it just undermines the argument of whoever posted it.

If you have a family and are lower middle class inflation is really stressful because you start getting price increases on everything from utilities, groceries, gasoline to haircuts to repairman. It all feels out of your control.

You start adjusting thermostat, buying cheaper cuts of meat, driving less, stretching out haircuts and try fixing stuff yourself. Makes for an unhappy wife and life.

At Costco this morning, I was looking for Kirkland almonds and there were none in the usual aisle spot, where they had been for years. I asked a worker nearby and he said the last plastic almond bag had been grabbed earlier, an hour ago. Two weeks ago, there were four stacked open boxes filled with almonds, maybe 400 bags. I went across the store to get a box of 1,000 T-shirt bags and the price had gone from $15.99 a box to $18.99 a box. Even so, there were only 3 layers of stocked boxes, not the about 7 layers I had seen on my previous visit. My Westbury Costco had for the first time Kirkland 80/20 grass fed frozen beef patties (15 in a package) about 6 weeks ago. Two weeks ago, I had got some more packages at their new location in the freezer aisle. Today, there were no packages and the sign for these beef patties was removed. In the vegetable area, I went looking for a bag of onions. There were only two types, yellow onions and New York onions. No Oso sweet onions from Peru, which were always around. If giant Costco is getting jammed by supply chain interruptions, that is a bad signal for the economy.

Grocery Stores are running out of Deer Park Water. Had to climb on a ladder myself to get the last bottles that were stacked in the back of the shelves where no one can reach them. Safeway is the only chain that carries them. The next crisis in this country will be clean water.

Nobody can afford spring water anymore. Now it’s all the store brand water which is just tap water filtered slightly better than usual but packed in the thinnest possible bottle.

The Fed is nervous that inflation will be … too low ;)

You can tell politically inflation is getting politicians nervous. They start trying bandaids to try to convince people they care.

After 18 month rent moratorium that probably will take a lot of rental property off the market white house announced they are going have program to build 100,000 lower priced homes. If Feds are involved the price will probably be twice as high to tax payer when all is said and done.

Is there anymore proof of government inefficiency that we can’t seem to have a trial for KSM after 15 years. Maybe they just want the guy to die of old age.

I suspect the chip shortage may never be over, or if it does end it it will be replaced by something else that makes auto’s unaffordable or unavailable to the masses. I used to think happy motoring would come to an end due to fuel prices and availability. But now I realize it will be the supply of cars that ordinary people can afford to buy and maintain that will put an end to happy motoring.

I remember the inflation of the 1970’s in NYC quite well. My biggest takeaway was the collapse of marginal neighborhoods all over the city. This is the period when landlords walked away from properties in poor and working class neighborhoods. My parents were living in a rent controlled apt, the building was abandoned by the owner, and nobody was providing heat or hot water to the tenants. This was going on all over the city. Entire neighborhoods were burned to the ground becoming urban blight.

I remember the Time magazine cover (c. 1970) showing rent controlled, abandoned slum property in Brooklyn.

Wolf– Inflation “expectations” means what’s going to happen in the future. Those have a GREAT deal to do with what people on the internet are yelling about.

You are one of the highest purveyors of panic of “inflation” “inflation” on the web that I’ve experienced. That has a lot to do with “expectations” people will have– so I believe you are one of those responsible for these”expectations.”

All that talk, especially by the right (not saying you are!) about “inflation horrible” MUST have something to do with those “expectations.”

Many wholesalers find it easy to raise their prices now because “everyone else is, and people on the internet are saying it, so we won’t be blamed.”

I still think that COVID has a lot to do with higher prices, just by the super obvious cause of reduced supply for some things. We have lots of evidence for that. The Fed may be wrong, but they are not completely stupid.

You may have noticed that Covid panic has gone up a lot in the last few months. I don’t claim to know the exact causes of higher prices, but it has to be at least partially responsible. So my advice is to have a little more humility about what you know the future will hold.

Inflation is one of the shittiest most insidious things a government/central bank can do to working people — other than government employees who get regular COLAs — and to many other groups. I don’t emphasize the insidiousness of inflation nearly enough.

I don’t disagree with you about the badness of inflation. Just questioning exactly what’s causing it.

For ten years the Fed has been dumping huge money in the economy, with amazingly little inflation. I’m just saying that it’s when Covid came along is when all the price rise action actually happened.

And don’t deny you could be right about future inflation. But it will take some good rise in incomes in the bottom 70%. Right now seems to me vast numbers of people don’t have enough money to maintain it.

The prior QE ended in 2014. Even when it existed it was a lot smaller and slower ($3.4 trillion spread over 6 years) than the $4.2 trillion printed in 18 months now. In late 2015, the Fed started raising its policy rates. In late 2017, the Fed started shedding its QE assets. At the time, fiscal stimulus was relatively small by today’s standards.

Also, in 2008, demand collapsed and stayed low for a long time. This time around, the demand collapse was very brief. And then it surged. These two periods are very different.

Inflation occurs when the supply of goods doesn’t keep up with the amount of money in circulation.

From the mid 1980s to just a few years ago a lot of money was put into circulation but little to no inflation occurred because we were getting massive amounts of cheap goods from China.

When that started to dry up (starting with Trump’s trade war with China followed by Covid) then inflation increased. So inflation will continue to be a problem until the supply chain becomes unplugged.

I’m not a wholesaler but did have to raise rents on my tenants (and it wasn’t easy or something I wanted to do). I also had to raise the rates I charge to my customers because I had no choice but to raise the amount I pay my employees. None of that was remotely easy. Again, none of this was wholesale, but all of what I did is because I had to because inflation is already here, despite any expectation of future inflation, which, by the way, is well on its way and will be continuing for a while. I tend to agree with Wolf below. This is insidious and folks who aren’t paying attention will get nailed, but the working class, regardless of whether they’re paying attention, are gonna get nailed the hardest. They should be hearing how bad this is and how bad it’ll get daily, but our wonderful media is more concerned in protecting its own so doesn’t tell the folks what’s going on. It’ll come as a shock to most.

Ralph,

If you put up a sign in your front yard saying it’s ok for everybodys dog to crap in your yard, would a reasonable person have an expectation of an increase in the population of flies?

Different yard, different dogs, same flies…

Jus’ sayin’

They can’t very well unprint the money, now can they? There’s nothing transitory or temporary about this. Inflation is way over what they’re stating and we all know it because we pay attention. The only reason they get away with this garbage is because most people don’t.

I don’t see why the Fed can’t “unprint” the money by taxing it back where it lands.

Property taxes on second homes, corporate profits, .01% tax on equities trades, raise capital gains.

Sure, but capital destruction makes credit magically vanish and in our world credit = money. With asset classes priced at the margin there is tremendous capacity in today’s economy for big piles of assets to be marked down by a few new incremental transactions. Like when your neighbor sells her comparable house for 30% less than you thought yours was worth.

That is a fine point. Inflation lingers.

There are exceptions. Gas prices go up and down based on what the King of Saudi Arabia wants them to do. Car prices are likely to go down after the chip shortage abates. Wood prices have already dropped.

But for the most part, a Central Bank that doesn’t control the money supply is totally responsible for the inflation that occurs. And it is VERY hard to get THAT genie back in the bottle. I was looking at steak prices at the grocery store this weekend and asked myself, “WTH? Did Texans stop growing cows?”

A beef shortage is in the offing because of Global Warming causing drought in many areas of the country where cattle are raised. Same with anything grown in California for the same reason. Grain prices will also increase because of unstable growing weather in the Midwest. All food will be subject to inflation because of decreased production while demand increases.

@ TBwcW

The Fed unprints money by selling stuff.

Every night they unprint more than a trillion at the last count I saw for RR’s. If they sold off their whole balance sheet we’d all have to barter like I did when I was a Kid.

No kiddin’

The Fed is getting nervous,…haha.. you are misreading the Fed dear friend and have been so for many years.

This is only the beginning and “temporary” will take us mid 2022.

By that time, expect a media blitz against the greedy landlords and businesses that cause inflation by increasing prices.

That should take us beyond mid 2023.

Also any slowdown on the rate of increase will be interpreted as imminent deflationary collapse and will prolong the pain.

When people will be marching in front of the Fed by 100k, then the party in power will nominate Volcker2 to (maybe by 2026)-8, but by that time CPI will be running in the 12 to 16% range and your money will be devalued in half.

Fed is not there to fight inflation or act in consumers interest, it is to finance the government. Buy real estate if you still can.

“Fed is not there to fight inflation or act in consumers interest, it is to finance the government.”

I’ve been reading a detailed history (Gods of Money) of how American oligarchs instigated and controlled the Fed from the beginning. They did it to consolidate their own financial power. The main goal was NOT to finance the government, unless doing that extended their domestic and global financial power.

As Historicus continually points out: According to Congressional legislation, in modern times (since 1977) the Fed is mandated “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

But obviously, like always, the Fed’s primary unspoken directive is the stability and profit of member banks (and the oligarchs that directly profit from that). For example, promoting maximum employment says nothing about livable wages.

The dual mandate game……but what of the third mandate…”promote moderate long term interest rates…”?

This mandate might be the most important, and the most abused…and is continually carved out with the “dual mandate” game (max employment, stable prices)

Moderate means not extreme. Moderate long term interest rates PREVENT the irresponsible creation of long term debt which draws wealth from future generations forward to fluff the present. Instead we get 4000 year lows, and Trillion dollar ideas from politicians flow like water.

Moderate keeps a balance between lender and borrower.

The Fed has been in “emergency” mode for 12 years….and $21 Trillion in new debt.

I don’t think people should buy real estate at this point unless you think government will let you keep it during next recession. Real estate is too illiquid in bad times and we have already had a big run up.

My wife and I live here in Canada and inflation has impacted much more this year than last year. Our total cost of inflation in 2020 was $950. The total cost to me and my wife with our higher property taxes, food, gas, heating, electricity, water bills, insurance and some other expenses is $1,600 more in 2021.

We are still doing great because we were proactive in the 38 years of working full time. We started with saving 13% of of our net income the first 12 years as we paid off our mortgage too.

We then we aggressively started saving 30% to 35% of our net income for the next 26 years into our savings accounts, term deposits, GIC’s, RRSP’s, TFSA’s which are equivalent to your CD’s, IRA’s, Roth IRA’s in the US.

We have no workplace pensions but have $1.35 million in the investments above and no debts, no mortgage now for 26 years. We have a modest house and that keeps expenses, property taxes more modest too. We did manage to lock in at higher rates, GIC’s back in 2019, 3.2% to 3.6% and this is allowing us to generate decent amount of $46,000 a year interest income a year.

Our CPP, OAS like your social security in the US has given us a $700 increase for 2021 so that helped. It covers all our expenses of $2,100 a month and after income taxes we still have an extra $300 a month from our CPP, OAS that we just bank it.

We are very concerned about inflation in our much better, prepared financial situation than most so it must be really concerning, scary for many with lower to modest income earners, unemployed etc.

You should be fine if assets get marked down by 53%. Just plant a garden!

You did everything thing right, but you will probably have to contribute more to the government through inflation and taxes in the future because you are able to. The government can’t get resources from those that have none.

You only live once, go on a holiday; you can afford it.

That’s the way to do it. Save a lot in the early years so you have plenty for retirement. You can quit working when it feels right, without worries about financial security.

Unfortunately, given today’s sky high asset values and central bank efforts to keep asset prices high, I don’t think younger generations will have much opportunity to follow that plan. The way it looks now, their savings will likely yield a loss after inflation. Their stock investments may yield a bigger loss. When older generations lose political power in a decade or so, hopefully the framework will change and asset values will be allowed to adjust to realistic sustainable levels, so everybody can invest with a reasonable degree of confidence and plan for the future.

I don’t know how many people are in this boat but all the younger generation of my daughter’s friends in the 22 to 25 years range started saving 10% to 15% of their gross income putting it in roth ira’s and ira’s. I am surprised too that they are very conservative with paying down their mortgages with accelerated payments and buying 5 to 10 year cd’s in ira, roth ira’s. They also have 1 year emergency or liquid money in callable cd’s.

If they don’t own a house they are renting and saving the difference. They do a little crypto trading but with only 10% of the 10% to 15% saved.

Because I remember last year — I do think it is temporary. Supply chains are wrecked. Workers are sitting at home, yet still consuming like fully paid employees (or even more). You can’t expect a constrained supply with normal demand and not get price increases.

You can thank your gov’t — both parties — for taking the worst possible options for combating a pandemic. Options which wreck jobs and businesses. I knew this year was going to be a mess. How could it not be.

What are you talking about? Polls in Russia, Belarus and Somalia show the US stimulus programs were pretty effective.

Mark: “Workers are sitting at home, yet still consuming like fully paid employees (or even more).”

One would need to provide some data supporting that assertion. According to BLS:

“Total nonfarm payroll employment rose by 235,000 in August, and the unemployment rate declined by 0.2 percentage point to 5.2 percent…” From what I can remember over decades, 5.2 percent unemployment is not an outlier.

Okay, those unemployment stats may be massaged somewhat. But how about giving some evidence to the generalization that the relatively small fraction of unemployed “workers are sitting at home, yet still consuming like fully paid employees”?

It could just as well be that employed people are the main cause of the increase in consumption, and those remaining unemployed are insignificant.

I feel like my business is doing better than ever. I do manual labor. Nobody wants to or can do any real work now. I can’t count how many calls this week from people who threw out there backs shoveling mulch, pushing there lawn mowers etc. As a result I charge more, as I can’t even keep up with the volume!

Thats why we reduced our hours, increased our rates, and don’t bother looking for employees.

They either have zero muscle tone & allergic to everything, or gym fit and can handle about 2hrs of work.

Routinely working up a sweat is essential to optimal health and longevity.

A wise old Eastern European visiting America for the first time was surprised that we go to gyms when we could be growing food on the acre around our house instead of grass.

Some jackass was on the financial news network this morning saying inflation is a good thing. Shows we are coming out of the pandemic recession. Another moron then chimed in and said the greatest threat to the recovery was wages going up.

Inflation is a good thing? Well J Powell has said that, and Yellen and Bernanke….but did Greenspan ever say that, or Volcker or Burns? No.

It is a direct violation of “stable prices”. What changed?

The WSJ ran an article in which the author, in an attempt to downplay inflation, said the past 25 years inflation only averaged 1.8% a year.

Well, that seemingly harmless rate took 56% off the value of the dollar.

Compounding, accumulated…..damaging..

It is UNAMERICAN to punish people who save so as to have a cushion and not be forced to the government teet.

But maybe that’s the game….they want people to be two paychecks away from leaning on the government.

In the mean time, if you are fully invested and the Fed sits on their hands with this 5+% inflation, you are killing it.

Just STOP saving !

No more punishment !

You’re welcome

Nope.

Article on CBC website this morning about how Canada’s next move will be to raise interest rates, sooner rather than later. This is to attempt to control housing costs. At least the purchase price. Here is the kicker though. They number crunched the higher prices with lower interest payments vrs higher interest costs and lower initial prices. The assumption was having the down payment and qualifying for a 20 year mortgage. With today’s lower rates the buyer will actually pay less over the duration as opposed to a lower purchase price so often touted as affordable. This also assumes people actually pay off their homes and stop trading up whenever they build equity.

Regardless, in our house we have saved, continue to save, and will buy more property as it comes available. The raw land I bought in 2009 has gone up 800%. My home has increased the same, but I did do many renos along the way. I don’t care whether the value drops or not because it is about owning a home and having land. The saving mindset doesn’t mean we scrimp, we just don’t piss it away on new cars and air travel, etc. Our lifestyle is what Twink wrote about breakfast. In fact, I had the same breaky he did but with our own eggs. My dog and I just came in from fishing where we released a 15 lbs spring. You don’t have to pay to have fun. My buddy travels to kayak in the Indian Ocean. I kayak here, for free. You can go hiking, anywhere. Always neat stuff to see. I know birdwatchers that do so on business trips to cities. There’s no limit on things to do, anywhere.

After going through the 70s inflation and early 80s downturn (job loss, etc) I vowed to never ever be in a similar position. That is why we always save. Screw them all, I have cash in my wallet and no debts.

Won’t be able to respond to any reply as I will be outside working all day. That is usually the case. Have a good one, all.

I’ve just got back from a dog walk and once a week I stop at a country pub for ham egg and chips @£6.95 pre pandemic price. It’s now…. £14.50. I just came home and managed to find someone selling eggs from their garden so got half a dozen (£1) and had lunch at home which cost about £1 in ingredients. I’m predicting a boom in picnic baskets!!

Lets front run and financialize the trend. We can call it the PIC6 basket fund!

Ok tough to blog the headline inflation story then have the print come in soft and the media jump all over ‘the FED is right’ meme. Transitoriness. One caveat is that RE inflation is building in the pipeline, but CPI drops and yields rise? The Fed will raise their rates first and Taper later, or never. Or open the endless REPO window (to everyone) If you want the cash (liquidity) first you need to own the treasuries. Convenient. Will be one of the most impressive monetary pivots in history of financial repression, but who is to say RRPO and RPO are not commensurable? QE provides cash reserves to the banks. Fed swaps paper for cash, banks use the reserves to buy more paper. Everybody gets monetized.

Interesting idea , if I understand your post, to get everyone to load up their 401K with Treasuries in order to borrow at RPO window. And all the earlier scare stories had the government forcing people to do that.

I remember my father chuckling about his 15% bonds back during the last inflationary cycle. To avoid that this time the Fed will have to keep money borrowing way negative in reality,

So much so that everyone will arbitrage. Not like the carry trade but in time. Borrow $1M at 1.5%. Invest in a basket that tracks inflation. Wait 1 year for inflation to raise your basket value by by 10%. Sell the commodities. Pay loan back and make $100K – 15K interest. 10% cheaper dollars but free.

Let’s see, if the yearly interest on the debt is about $500B now at say 1.5%, at 15% it would be 10 times as much or $5 trillion. Around twice current tax revenue and more than Biden’s current proposed budget.

It’s going to be interesting

I remember the 70’s. Some of it. (I went to college in the ’70’s.) We will not have a repeat of the ’70’s. In the ’70’s we had a real economy. Today’s economy is an empty shell of what it used to be. We have been in a depression for 21 years. Depressions are deflationary. That’s why they can get away with more extreme currency expansion then we had in the ’70’s. I’m glad that I’m retiring soon.

I want to thank California for sending all their polluted air to the east coast. The best Weather gal in town, Sue Palka said today that the temperature here was two degrees cooler due to the haze from the California fires which blocked some of the sunlight. Keep it up. I changed my mind. I like it.

We do our best!!! Wait till we’ve burned everything out West, and then everyone will realize they can neither eat haze nor money!!!

I need to dust off my WIN button.