No one wants consumers to pay off their high-interest credit cards, least of all banks, and consumers had threatened to do just that.

By Wolf Richter for WOLF STREET.

The last round of stimulus checks started going out in March, and people continued to receive them in waves, and used them to drive retail sales to fabulous records in March and April. But in May, the magic was starting to fade. And May is when consumers dipped into their credit cards again.

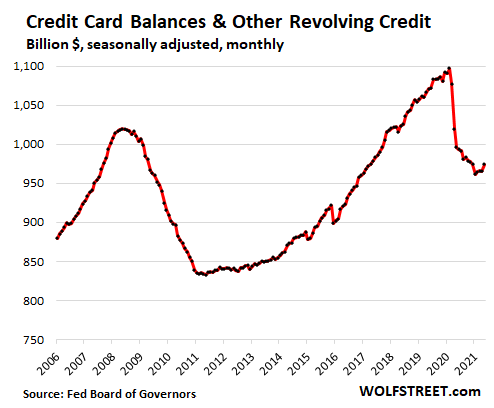

Credit card debt and other revolving credit, such as personal lines of credit, ticked up by $9 billion, or by 1.0% in May from April, seasonally adjusted, according to the Federal Reserve this afternoon. As measly as this uptick was, it was the first major increase since February 2020, and the largest percentage increase since December 2019. This followed many months during which consumers had paid down their credit cards.

The balance rose to $975 billion (seasonally adjusted), still down by nearly 11% from the peak in December 2019, and down by 2.3% from a year ago. Can you see that little relief-uptick that the financial media made such a big deal out of?

This 1% month-to-month uptick triggered phenomenal excitement in the media about renewed borrowing by consumers, and not just any old borrowing but the most expensive form of borrowing for consumers, and the most profitable for banks, at usurious interest rates often over 20%, and sometimes over 30%, charged by the same banks that pay near-0% on savings accounts.

This uptick caused a lot of relief, especially at the Federal Reserve, because no one wants consumers to pay down their high-interest-rate credit cards, and consumers had threatened to do just that.

It’s clear that this one small step for consumers was a giant leap for mankind, the way it sounded in the financial media, because American debt-slaves must forever shoulder usurious interest rates to fund the all-important American consumer spending and to fatten up the banks – according to the consensus opinion of economists polled by Reuters, or whatever.

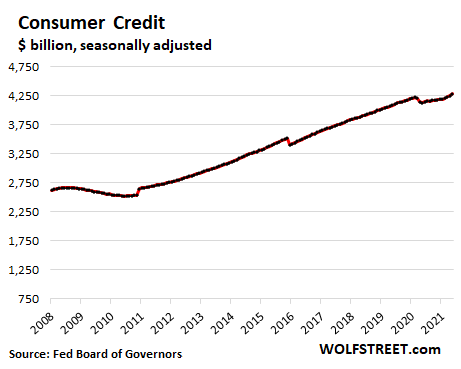

Total consumer Credit – what consumers owe on their credit cards, auto loans, student loans, but not mortgages – rose by $35 billion in May from June, or by 0.8%, seasonally adjusted, the largest month-to-month increase since March 2016, to $4.28 trillion.

March, April, and May each had set a new record on a seasonally adjusted basis. Year-over-year, consumer credit was up 1.1% in May, after having pulled even in April.

The heavy lifting here was done by auto loans and student loans that totally overpower credit cards and other revolving credit. Student loans alone now amount to nearly twice the balance of credit cards and other revolving credit.

The exciting things about this chart are the three jags: In 2010 and 2015 due to the five-year adjustments by the Census Bureau of the underlying population data used by the Federal Reserve; and in early 2020 due to the plunge in credit card balances as consumers paid them down with their stimulus money (see above chart):

The Federal Reserve releases the details of auto loans and student loans on a quarterly basis, and so we have to be patient for another month.

But both auto loans and student loans combined form the vast majority of the “nonrevolving credit” portion of consumer credit. This nonrevolving credit increased by 0.8% in May from April, seasonally adjusted, the largest increase since, well January, and was up by 5.6% year-over-year, the largest increase since August 2017, to a new record of $3.3 trillion.

Back in Q1, student loans amounted to $1.73 trillion and auto loans to $1.24 trillion. According to reports by Equifax, auto loans have jumped in Q2, and we know student loans always jump, particularly now because people are still taking out student loans, but no one is paying them down anymore because they have all been enrolled in forbearance. So when the detailed data for Q2 emerges we should see a satisfying jump.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The customers of Wells Fargo may have to start doing more than dipping since WF just announced all personal credit lines ,including home equity,are kaput. They are being funneled into a credit card high interest credit kill zone. Is this the start of “risk off” behavior hmmmmmmm……I wonder.

WFC has been constrained by the punishments inflicted on it by the Fed for past sins. They can’t expand their balance sheet until they’re no longer in time out. They have abandoned car loans, HELOCs, and credit lines.

The lines of credit were no bargain. They had variable rates up to 21%.

I thought the exact same thing last night when I read the Wells Fargo announcement of closing all consumer credit lines.

Passengers should take note;

When the pilots and crew all get up to pee then comeback and put their seatbelts on…

“we have a problem”

Dominick,

In terms of the Wells Fargo decision to close all “personal lines of credit,” here is what I said yesterday a couple of times, and I’ll say it again:

Why would anyone today still even use a personal line of credit? Credit cards have long ago obviated that old system. It’s just a small left-over business for Wells Fargo. Makes sense to shut it down.

WFC kept their personal loans, though, which are a bigger part of the business.

Last year, they shut down their home equity lines of credit. In the US, use of HELOCs has plunged since 2009 and continues to drop every year. People do a refi if they need cash from their house.

Things change.

The reason Wells Fargo is pulling back from these marginal loan businesses is that the Fed put a cap on Wells Fargo’s assets (such as loans) to punish it for compliance problems. The bank keeps bouncing into that cap. So it’s focusing on the big profitable types of lending and is shedding the others.

This was also a problem with the PPP loans. WFC couldn’t do PPP loans until the Fed agreed to buy its PPP loans. This was a big problem in California because WFC is such a huge bank here with lots of small business customers, who got shafted by not being able to get PPP loans quickly.

“People do a refi if they need cash from their house.” Yes, over the past decade that’s been the easy route with continuous dropping rates and increased equity. In the coming months refi’s for that crowd will have the sticker shock of higher rates and payments. Is it possible banks don’t want a run on cash from those who will buy a second property and walk away from the first?

Bank of America is offering HELOC loans. Reverse mortgages were used by seniors to fund retirement. 10 year cash out refi loans are popular due to the lower than credit card interest rates. Some people gambled with HELOC money and lost their homes.

U.S. homeowners have seen their net worth rising as home prices appreciate. Renters missed out.

DH, yeah, but the renters will be laughing all the way to the bank, if it is still solvent with a bulging portfolio of mortgages, commercial loans, personal loans, and credit card debt; spending based on such a metric is an exercise of playing on the railroad tracks. Net worths are a fiction until one turns the bloated financial portfolio or teetering home into good old hard cash. Tough times ahead, keep months of expenses in currency buried in a clandestine place. I would become a renter myself right now if now for the inconvenience. Have already moved 28 times in my life, and not my favorite activity.

“U.S. homeowners have seen their net worth rising as home prices appreciate. Renters missed out.” Not necessarily David. In personal finance, just like business, it’s all about cash flow. Those rising home values have come at a cost in terms of inflated home maintenance and operational costs like property taxes. Those are real-time cash flow hits as opposed to the unrealized gains or losses reflected in home values. Sure, you may be able to borrow against higher home values, or you can choose to sell your home. But unless you choose such options, along with the consequences of them, the cash flow advantages of home ownership versus renting is not so clear cut.

I have seen my real estate appreciate fast enough to pay for property taxes, repairs, utilities, HOA fees etc.

Someone renting paid for the repairs, flooring, appliances, roof, insurance, paint, property taxes etc. with the rent money. If a family stays three years in an apartment, the carpet is probably ruined and needs replacement, or they might dye it brown to hide the stains. Then they raised the rent again.

I used to live in the DC suburbs. Now I have a home in a retirement community with palm trees and low taxes.

Happy it worked out for you David. Re-read that last sentence in my post.

My friends unemployed for last 18 months.. paid minimum rent and the staye helped them pay the remaining

I think landlord took a haircut of some percentage

I explicitly told my friends not to pay any rent as I knew state would pay if you don’t pay

If you have already paid.. you are out in the water

This is in San Diego

reverse mortgages .. many seniors in Australia gamble & have lost their homes

I know how it works .. but to gamble the money instead of utilising it to more productive purposes is what ??

Insanity ??

It’s throwing away the house in the first place ..

We always ‘dip’ into credit cards. Paying them off monthly, or with stimmies, or not paying on them at all is business as usual.

With a good card that pays points why not charge everything you can and pay off the balance every month? Free points.

Because you’re still supporting the crooked banks, that’s why.

If you always pay off your credit cards… You hurt them far more if you get good at credit card hacking. I make thousands a year off churning cards for their points and perks.

It is a hilarious game of chicken. They keep raising their incentives for me to spend thousands on their cards by X date… Hoping that I will be unable to pay it back and have to start paying usery level %… Never has happened in. 20 years I have never played a dollar of interest.

If you have good credit and credit card debt free… Hacking and churning credit card offers is easy money. Use the banks own greed against them.

Do not forget to churn banks as well… I have not paid an ATM fee in 15 years. Last year BofA paid me $1200 to move my accounts to them took me 2 hours… Kept all my perks from my last bank and added a free safe Deposit box.

Just like Wells Fargo… These banks want to show wall st that they are growing their credit card and consumer products segments especially among certain demographics… So they let me keep playing them, accepting the losses… So they can account for potential future gains from my business.

Cash is a pain in the ass liability.

Not necessarily. I get 2.25% back on everything I buy. The merchant gets charged around 1.98%, so the bank is losing money on my purchases. They only make money from people not paying their balances on time.

That said, I still pay with cash for all purchases from small businesses, whether goods or services.

Actually I’m profiting from them.

re: “… I get 2.25% back on everything I buy …”

Who’s doing this?

I have the Chase Sapphire Reserve, which multiplies all points by 1.5X when used for travel. I also have the Ink Unlimited which gives me 1.5%, so together, it’s 2.25%

Never thought about that before. Is that legal to get 10 credit cards and pay each one off successively with the last one from a debit card? Seems like a good way to end up with an extra grand or two at the end of the year. I pay for everything off my 1.5% rewards card. Might be worth scamming the credit card companies if this is legal.

Aaaaaaaand cabal gets more $ from you as it collects even more data in a more granular level.Do the thought experiment of paying for some gas station purchases,car repairs,and some grocery purchases online or not viacompared credit c. Compared to buying magazine/newspaper subscriptions,website subscriptions,wine of the month xlub,shavers club,vet bills,all gas station purchases,all convenience store purchases,all insurance policy premiums and copays,all pharmacy purchases,allretail purchases,all charity contributions or political contributions.Lots of data,mmmmmmm???

So .. at any given moment .. you say / write something online that the government deems to be inappropriate & instead of .. or as well as being shut down online you bank account is closed & your life saving .. all $50 of it is confiscated ??

Because they add the fees to the price of everything they sell. Pay cash and get a discount or better service. I pay cash for everything that involves personal contact.

I always pay cash to independent vendors in order to increase their profits, which may or may not keep prices down. Regardless, if I respect and value a vendor I pay cash with a smile and thank you. Judging by their response they seem to appreciate it.

Another thing customers can do is write a positive Google review for favourite vendors. Many people only write one when they are mad, but a computer store owner I know said a decent review is the equivalent of spending $1500 on advertising. Besides, everyone likes and deserves a ‘good job well done’ once in a while.

I’m probably reading “I pay cash for everything that involves personal contact” too literally…

Hey Swamp, do those “entertainers” take credit cards now?

Nice catch HollywoodDog ;)

Credit cards bring value to a business. If you don’t accept them you lose customers. Simple fact of life. The seller pays the credit card company for access to people who like to use credit cards.

Check out the Wolfstreet donation page. If you donate $100 you get a mug. Theres a yellow donate button that takes you to PayPal. You can also pay “cash” by sending a check. I didn’t see where you get a mug if you send $97 cash.

Now why would Wolf accept PayPal? Because he’ll collect more money. Compare the piddly 3% fee he loses to a credit card vs 100% of a lost donation because someone didn’t feel like writing a check. One lost donation = 33 credit card fees.

These are businesses, not charities. I don’t owe them financial support. I do what’s best for me. They’re doing what’s best for them. Are they working feverishly to offer me the lowest possible price? No. They might work feverishly to offer me the lowest COMPETITIVE price but they’re not thinking about my welfare, they’re thinking about the best price point.

It’s called “business”. When I ran a business I accepted credit cards. I didn’t like it, but it saved a lot of hassles.

If I could haggle prices I’d do that too, but in the US that’s mostly reserved for houses, cars, and flea markets.

If you have a dispute with a vendor you have a lot more leverage since you can dispute the charge on the credit card.

I have found few opportunities in my area to get a discount for cash. In those few instances the cash price is pretty much the credit card price minus the value of the points and it’s usually a gas station. I’m not going to walk over to the cashier for a breakeven deal.

The only consistent cash discounts I’ve seen are for gun sales. If I were buying a gun I’d probably pay cash anyway. And that’s for in-store purchases. You can save more online using a credit card but you leave a brighter paper trail.

I have NEVER seen better service for cash. Maybe your lap dances are better. I wouldn’t know. At Home Depot, Sonic, the pharmacy, or the supermarket, it doesn’t seem to make a difference. At restaurants your behavior towards the server and your history of tipping well gets you farther than cash. I can’t imagine sitting down in a restaurant and saying, “By the way, I’m paying cash [wink wink]”.

Michael, I agree with 99% of your points. Just a few things. Where I live, people actually pay MORE for guns in cash, as a lot of people pay a premium to avoid the 4473.

Regarding better treatment for cash, you’re not going to get that at a chain or a restaurant. But if you’re hiring a wedding photographer, electrician, non-chain jewelry store and so forth, you can often get a better deal if you tell them up front you’re paying with cash. For example, my jewelry store and electrician don’t collect sales taxes if I pay with cash.

In case you are interested when I was in the Navy overseas and single I did plenty of that cash for entertainment.

Mr. Gorback,

This suggestion comes up frequently. My expenses are such that I could charge at most $1000/mo. — $12k/yr. Three percent of that is $360. That sum is a lot of money to me, but it feels as though I have to work all year to get it by earning credit card points. It doesn’t seem worth the trouble. I think there are easier, higher-return possibilities for reducing costs that I should work on first. Privacy is a consideration, too. I don’t want the big chain stores to know what I eat, drink, wear, etc. Maybe I’m putting too high a value on that. If you think maximizing credit card points is a good deal, have at ’em!

I put a significantly higher amount of purchases on my credit card than you do. The card I have is definitely worth it to me.

Check out a site like Nerdwallet to find what’s best for you. Look at what the premium cards like Amex Platinum or Chase Sapphire Reserve offer. Note that the annual fees are more than you currently get in points.

Those cards are not designef for your lifestyle. There are, however, rewards cards that would pay you well without the barrier to entry of an annual fee. Just not as well as the premium cards.

I fail to see how using a rewards card is a hassle. Please explain the onerous burdens of using a credit card. You have to “work all year” to earn points? BS. What work? You just buy stuff with it. Is it harder to slip a credit card in the pump reader or to walk back and forth to the cashier? Do you have to make periodic trips to the bank/ATM to refill your credit card? You can arrange auto deduction for your credit card payments every month. That’s not just convenient, it adds some discipline.

My dining habits, lawn fertilzer use, and gas purchases are not state secrets. If I don’t want something known, I can make it so on a case by case basis.

BTW you live in a world where you can be located at any time by your cell phone. Not only that but they can figure out who you might be with using cell tower data to see which numbers are nearby. They know when you saw your doctor and who it was. They know if you went to a restaurant and how long you were there. Get Google Maps and check your timeline. The government and who knows who else can do that 24/7.

Your bank spies on your transaction activity for the government.

If you’re worried about anyone knowing what you eat, where you get gas, or whatever, I’d certainly buy my tin foil hat precursors and burner phone using cash.

Those nefarious big chain stores are going to track what you are wearing so it will be easier for the NSA to monitor where you are at all times…because you are that important!

I understand privacy, but you are worrying about the wrong things. More important to try to be invisible on the net than invisible to credit cards purchases. Unless you are buying alot of ammo, fertilizer or whatever the drugs they boil down to create crack. Dont use Google, I use duckduckgo. I might spend some time to try to figure out how to use a proxy, so i really cant be tracked online. I have noticed that duckduckgo doesnt censor results, so you can actually see stuff, like sites that dont agree the COVID vaccine is a good idea, whereas it is impossible to find any dissenting opinions on certain subjects on Google. Be wary of Google.

“With stimmies fading….”

What cracks me up are all the people who are waiting until the last of their UE checks come to start looking for a job – as if they’re all going to be hired at the same time the cheese runs out. The smart thing is to look for a job right now when they are plentiful. But instead, we’ve got a bunch of lazy slobs.

“Lazy slobs” – Great title of future book cataloguing the decline of the US Empire starting from around the time Nixon went off the gold standard. But a better title would be “Lazy cunning bastards ran out of road so ate their children.”

Have you seen the tatted up, face full of metal, high fructose corn syrup laden, iPhone in the face 24/7, couch sitting, pot smoking youth of today? It’s unbelievable.

They didn’t raise themselves.

DC, these youngin’s blame us older folks for a lot of stuff we had nothing to do with, but the lower standard of living they are going to be stuck with, in some respects, couldn’t happen to a better bunch of disrespectful, know-it-all entitled rascals with posteriors that are their favorite work tools.

Ergo, the military can’t find enough young people fit enough to be recruits. Guess they’ll have to lower the bar.

Have you seen the lazy, tatted up, full of drugs, phone in the face, complain online, couch sitting, pot smoking 45+ yr olds of today? It’s unbelievable.

Government caused this 2 working parents changed economy from industrial to high tech kids were never taught anything but what they learned on there own

I know quite a few professors at a certain Ivy League university who have gone into retirement early because they no longer knew how to teach this new generation of Internet-reared student. They are very fragile emotionally. This, and the fact that the admissions standards had been lowered significantly to meet certain metrics, made for a chaotic and disconcerting classroom experience — not the intellectually rigorous experience of decades past. I don’t have much hope for the future.

And I shudder to think that these coddled, indoctrinated, and entitled young people (not all of our young adults, but a good percentage) that are entering low-mid-income labor pool today are:

… preparing and serving fast food/dining food, repairing your cars and houses, manufacturing goods we consume, teaching our children, and otherwise impacting economic daily life for millions of people.

Actually DC,,, I have seen some of them with all the embellishments you mention,,, and a ton more with just some of those decorations, ”statements/etc.”

Many of them are just waiting eagerly until the Marine Corps decides to let them join in spite of the tats,,, and have told me many times how eager they are… others, not so fast or far or any other metric except how much dope they can consume and how fast, etc…

Kinda/sorta helpful to remember who first said, ”This younger generation is going to the dogs.” EH???

Hint, try Socrates!!!

They’re busy getting rich on their Only Fans accounts and streaming video games on Twitch?

Thank goodness for immigrants. We’re doing a full renovation of my mother’s house before we move in; the plumber is on the job every morning by 6am–it’s 100deg+ by early afternoon–and works until 3 or 4 in the afternoon. He’s a Russian (Ukrainian?) immigrant and is methodical and meticulous, and insists on showing me all the cracked sewer pipe he’s removing so I don’t think he’s padding the job (I’ve told him he doesn’t need to, but he insists). He has more work than he can handle, and seems genuinely glad to be in the USA.

It’s like a Hollywood horror movie. Apocalyptic. Dystopia is here now.

Aouch. I might qualify for only one of those 5 features and yet I still somehow feel personally depreciated.

“Ok boomer”, says the boomer

If I got a resume from one of these lazy slobs I would shred is so fast your head would spin.

They’d argue you’d be lucky to read it… Let alone delete it… Unless a millennial helped you, lol.

Swamp Creature,

“resume”? and “shredding”?

Is anyone still mailing resumes? or even doing resumes? Especially young people?

I thought all recruiting of young people and not so young people is done via online platforms, no?

But what do I know. Haven’t looked for a job in a while. Too busy around the shop :-]

No they still ask for resumes and cover letters too. I would avoid the platforms.

My husband recently had to submit a Curriculum Vitae for one position and a resume for another.

Wolf

How’s your supply chain holding up with your mugs and shipping boxes? Got my stimmie check finally and wanted to order another mug.

Swamp Creature,

I think the company’s owner got cold feet about talking to this media mogul empire. I only have part of the story (from the middleman, hear-say). I lack the original. If and when I get the original info, I’ll post it. I’d love to know the whole story.

This is addressed to several commenters:1)d.d.go does and has been documented censoring,it sucks.Qwant is less censorious,Brave,Startpage,Tor,Dissenter. I have worked alongside and for many immigrants,legally here and not.Ive supervised their work at parents house.Chicagoland area has a plethora of them.Same experience with Polish or Ukrainians,good attitude,work habits,integrity. 3)Wells Fargo and others should have been much more harshly dealt with by Injustice Dept. And SEC,FED,FDIC,Commerce Dept. They are legacy $launderers who project their Amoral behaviour onto blockchain supporters.Safe deposit guy,Not Safe in the bank.Learn the law,beware.6)Humans are educated and parented,rewarded by other humans yet at some point they are responsible for looking in the mirror and challenging themselves to be better.Homeschooled kids tend to be less offensive and self-absorbed. Not brought up is the reason for increased charges,opening up=vacations,haircuts,dining out,festivals,summer parties,etc.

“Lazy slobs”

Nature follows the path of least resistence. If you create an incentive to do something (or nothing), you can’t be surprised people take advantage.

EXACTLY A:

Some folks seem baffled by the young folks, mostly in my limited experience the brighter ones, taking all the ”freebies” offered and just ”doing their thing” with that support…

Just wish I had had that support 60 years ago when my GI Bill $90/month ran out and I had to work 3 part time jobs instead of just the two that I had been working to pay my way through Cal…

IMHO, THE very best money spent by our lords and masters would be to support our young and younger, ”like totally dude” for a clearly specified length of time, say 4 years,,,

At which time, the full support could be continued with some demonstration of clear results,,,

ALA ”McArthur Grants, etc.”

Sorry you had to work so hard to better yourself and contribute more to America.Father,uncle,friends,friends of son,cousin all military with some firemen and cops in the mix.You should have had a full ride through gradschool at a decent state u.!!! :-) :-) :-)

Aside from the principle that one person is entitled to live at another’s expense simply for existing, my other objection to the additional stimulus is the lack of accountability. A “shotgun” approach whether the recipient needs it or not.

There is an article on CNBC (again) where some economist once again claims that paying people more not to work doesn’t motivate many people not to work or look for a job. Presumably, a noticeable or majority of these people have jobs this economist would never accept but it’s not keeping others from working.

The only thing clear to me, is that without stimmie help, the USA (like many countries) can’t pay down it’s credit cards and the only way is up and away………..

If I am not mistaken consumer debt is still trending down once you include mortgages. It got too high by the time the 2006 housing bubble was fully inflated. One consequence for 3% mortgages is the principal gets paid down at a quicker rate. The debt problem this time is corporate and sovereign.

Yeah, but those are tied together. Without all of the zombie companies being able to stay alive based on low interest rates and high debt, many more people would become unemployed (at least in the short term).

Credit growth means optimistic consumer with an sanguine view of future income and low rates.

Or it can mean people refuse to adjust to having less purchasing power and cover the gap with borrowing.

At some point they still have inadequate purchasing power plus double-digit interest on their debts.

Debts that cannot be paid won’t be paid. The debt laden US economy cannot pay off all the debt it owes. Unless incomes rise. But that isn’t going to happen. Who is going to keep expanding the wealth of the One Percent?

3rd time I have asked this Q?

What is stopping US Congress from designating an occupation of “Consumer” for tax purposes ?

Though choosing to live in bottom percentile of “earnings,” a Consumer’s FT occupation would be to spend the $2000 / Mo allotted to them (adjusted annually for COLA).

We (USA) have proven we can create spendable currency at will and the majority of the ROTW (rest of the world) will accept it as a financial boon to their economy(ies).

We have pretty much been doing a version of this for over a decade. Why can’t we just formalize it in our social customs and tax codes?

Don’t worry, it’s coming in the form of UBI. It make take another decade to fully roll out, but it’s inevitable.

I work in healthcare. You wouldn’t believe the number of healthcare workers angered by the sums of stimulus checks given to ppl to do nothing? UBI sounds excellent in theory! However, if the masses are receiving UBI to do absolutely nothing, then where are you doctors, nurses, teachers, firemen, plumbers, electricians, etc, going to come from?

What incentive does anyone have to get up each day and work in a society full of entitled UBI recipients?

And these aren’t jobs likely you can outsourced or computerized. Imagine heading to the operating room where a “Dr. Bot” plans to perform your child’s emergency surgery?!

Good Luck with that!

Not surprised at all by the anger you are seeing among those working so hard, and not exactly getting a lot of leisure time or great creature comforts, as their reward for it. You are spot on – UBI can only exacerbate societal conflict. Another mini civil war, neighbor against neighbor, ensues – the freeloaders vs. the hardworkers. Related to Ds vs Rs. – almost all UBI folk will be Ds.

Andrew Yang may be a very intelligent guy who might even rival Wolf as a top data analyst/nerd. But, for psychological reasons alone, there isn’t just a good outcome with UBI in the future – at least not under the current financial apparatus.

UBI will allow someone to barely survive. No luxury beyond the basic necessities. Certainly no social status. There will always be plenty of people who desire more and they will continue to work as they do now.

UBI will replace the massively inefficient (and frequently corrupt) social welfare system. But at something around $1000 a month, that’s still only $12k a year. Hardly big bucks.

Can you survive on it? yes, But barely.

It’s coming. Within a decade the entire social welfare system as we know it today will be completely abolished and replaced with a simple UBI to all.

UBI makes very good sense if the amount is set to a maximum it would take to live in an area. Enough to cover rent, utilities, food, some for gas. Health insurance would need to be provided.

What ends is food stamps, vouchers for rent or discounted utilities, no phone payments, no emergency help, no Sec 8 housing. None of the cost which the Fed/State/County now pays for with our tax dollars.

It also puts an end to tens of thousands of jobs to administer all the current social programs.

I think we could save some money.

Mankind is so stupid. It’s hard to believe that there was such a long time between the invention of the printing press and figuring out that prosperity could be created by printing money. Five hundred wasted years living in poverty.

Funny and sad at the same time and so true.

B

There is often an insurmountable barrier between perception and reality.

It can be happening, but if it isn’t deemed to be happening, it isn’t happening.

It speaks volumes about the state of western society that the media cheer when consumer debt rises and freak out when it falls.

That’s either because they are evil and want people to become debt slaves or so economically illiterate they actually believe modern economic drivel.

Like most of the public they mislead, they act like they don’t know that bubble inflated “wealth” is fake, debt doesn’t equal wealth, and most or all economic “growth” since 2008 is the result of increased government deficit spending. They don’t seem to understand the broken window fallacy either.

JMG

The beneficiaries of debt spending pay the MSM’s bills.

Customers v Merchants, they’re with the Merchants.

Who owns most of the media=your answer.Not about society,but about certain groups within society who benefit from financial enslavement and insatiable zombie hordes of consumers.

If we thought the end of last year would end rough, THIS Fall could be a doozy. People catching up on rent and mortgage payments, the ending of enhanced unemployment, perhaps another surge of covid, to add to crippling auto payments, etc.

The next stimulus would need to be about $5000 to keep people afloat, but the Fed is busy now figuring out how to deal with inflation, keep interest rates at zero and prop the stock market. I think we Peons are on our own now.

Don’t forget student loan repayments. I saw an article the other day about some rumblings to extend the deferment.

Federal student loan interest rates also went up July 1st for all new loans.

1) My direct saving account in the Fed : ZNT3893JP.

2) When JP is gone, because he is republican, a socialist Fed chair will recharge my saving account.

3) When the short duration rise sharply banks go bk.

4) Banks lend for 12 months, 5y, 7y…30y, buying low o/n lending high in the long duration.

5) When EFFR is greater, or near banks loans, u get the saving & loans

crisis, and the great recession crisis.

6) Since Feb 1998 3M moved sharply up from 5.70% to 9% in

Mar 1989. Papa Bush was gone.

7) Between May 2004 and Aug 2006 the 3M rose from 0.9 to 5%. Bush Jr

became toxic.

8) China export inflation to contaminate US economy.

1) In 2003 the RE collapse was light, the stock market plunge was not

deep enough. Some people expected SPX to reach 750-780.

2) The got their wishes in Mar 2009, with less zombies.

3) The pandemic crisis cleansed the elderly within a week, but wall street

zombies are still sailing.

4) JP clicked hot steam into their head and they are still flying.

5) Inflation reduce the real value debt at the expense of low wages

employees and blue collars contractors who recharge their beloved

pickup trucks and big tummy with expensive energy.

6) When people spend less on mattresses, implants, new paint…the economy will tank.

I’m not trying to be cruel here, but your comments under every post are super annoying to read. You have this same numbered list style of reply that is frequently incoherent and unrelated to the actual topic. You should really try to tone it down and make a more coherent point.

Sorry if that’s harsh, but this kind of inconsiderate verbal diarrhoea list thing you do is very irritating.

I just ignore them. I think Michael is legitimately a smart guy, and has insightful points to make, but for some reason he refuses to write them in a way that is coherent and understandable.

I don’t know if it’s a schtick or trolling, but I stopped long ago trying to make sense of them.

“I don’t know if it’s a schtick or trolling, but I stopped long ago trying to make sense of them.”

I don’t even read them anymore. Too hard to figure out what his points are, and if they actually apply to the thread topic. Kitten’s stuff is much more entertaining!

For me the issue is when people do not respond to any replies to their comments. Paulo is like this too. It’s like they post their stuff but don’t ever expect to engage in any dialogue. In which case, I just stop reading their stuff, because if it’s just mana from on high with no possibility of discussion, then I really don’t even want to know.

Of course it doesn’t help that the comments system here makes it very, very difficult to find discussions or to know when there have been replies to your comments.

@Zan, I suspect that I may come across as you describe, but my excuse is that I am half a day ahead of America. Wolf often posts in the evening Australian time and I have wrote a comment, then gone to bed, then gone to work, so that’s 2/3’s of the day where I am unavailable to reply. Then a new article is posted around the time I get home from work. At some point in that cycle (possibly 12 hours later, but maybe 8 hours later? I am not good enough with timezones to know for sure.) you guys will go to bed and then go to work. It is easier on the weekend as it’s only the 8 hours when I am asleep that I am unavailable, but this is also the peak time for comments with articles often getting over 300 comments, with new comments being buried deep in the threads of previous comments. I don’t get enough free time to spend it constantly reading comments I have previously read. It annoys me that I fail to reply too, but that is the vagaries of international timezones.

ZAN

Use Ctrl F on your browser then type search term, it transforms the site.

W told me that when I had the same problem at first.

Hey, leave Micheal Engel alone. He is a very smart guy and knows something about almost any topic you can think of. He is kind of like jack-of-all trades. I read all of his comments and sometimes you can find gold mines in them. i.e. he said watch 20yr and 30 yr bonds they might invert soon. He is one my favorite commenters.

Another one is Swamp Creature. He chronicles his life in the swamp as if he is a different creature[literally]. Another one is Michael Gorback. He is a doctor, financial analyst, militia man,poet…you name it. My favorite is last sentence punchline. These 3 always have something interesting.

Fat Chewer, not thinking of you in particular. There are some people who *never* respond to comments on their posts, which suggests that they never come back to them at all once having posted them. When I make a post, I try to check back at least once or twice in the following couple of days to make sure replies are read.

Auldyin, yes I know how to search a web page for text. But it has to be the most inconvenient way known to mankind to track replies to your post. You have to go into multiple articles per day manually and do it (if you post alot, which I used to), and you have to remember which articles you posted in, and you have to remember which comments you have read and skim them over and over looking for new ones. Perhaps the worst user experience possible.

JMG – What about Ron? Do you like Ron’s comments?

I personally like Ron’s comments and style; short and to the point, although I have to add my own punctuation.

Zan,

I said/say what I want to say, then let it go. It’s not my blog to hog and monopolise. Furthermore, Wolf discourages it as far as I know.

The other thing is that I only pop in once in a while and don’t look usually for replies. In this case I am on a tea break from work, started at the bottom of the comments, and worked my way up.

Most people post their thoughts and do not reply to responses. At least I don’t see the engagement if it does happens.

I do not troll or lob bombs, and sorry if it strikes you as such. I think I made a comment above about paying cash for stuff. I know when I comment about wages, unions, and health care, plus my country called home, it can be irritating for sure.

I wish I did not live so far away and could one day put faces and personalities to comments and replies like the past SF meet up, but I do really appreciate what people post here. Plus, when I do piss people off I always feel bad about it, a natural reaction I suppose. I absolutely hate arguing in person, don’t argue with others and/or don’t try and persuade that my point of view is the right one. It is futile. This comes from years of working in both management and as a union rep. Today I read this post around 5:00am my time, and have been working since 6:00am. Probably won’t look at WS again for this day.

regards

I know a Ron IRL who is a lot like this Ron. Aging curmudgeon type of guy. Cynical but generally accurate. He doesn’t annoy me. Too much of the IRL Ron does annoy me a bit – but we are still friends.

Forgive me, but I’m not familiar with Ron. I’m relatively new around here. But if Ron is anything Mr. Engel I predict I won’t be a fan ;)

U wrong dude,,, U not reading deeply enough into the poetry/rythmns, etc., of MEs ”stuff”

Sometimes he goes WAY out there to be sure,,,

Most of the time it’s either a ”koan” or some similar hibachi, etc.

Wolf has explained he is not a ”bot”,,, so the rest is up to us..

Not saying I too sometimes read it and weep/sweep it under the next rug, etc., etc.

I don’t have the time or patience to try to interpret posts. If I can’t skim it and immediately understand, I move on.

IAmaBOT : skip my punch lines !

Someone finally cracked. Yes, ME’s style is definitely out there, and many of us have shot a comment at him, but he persists. I honestly find him interesting but yeah, a bit strange. Such is life. I don’t even understand the “technical analysis” he employs, but then I don’t really understand the “technical analysis” that astrologers use either. ie What is “the cloud”?

After saying this, I note he is using more plain English after some earlier criticism and I appreciate that he is willing to adjust his style to make his comments more interpretable. Sometimes, he is more right about things than many realize. Maybe even more than HE realizes. Just like an astrologer. He is our resident financial astrologer and through persistence and through occasionally being VERY right, and because he is as addicted to and loves Wolf St as much as many of us here, he has carved himself a place here. It was obvious around January this year when he went silent. It just wasn’t the same without him.

That goes for unamused too. I hope unamused is doing alright and will come back to WS one day, as do many others here.

We are a bit like a bunch of friends here. We put with other’s foibles because they put up with ours. We can strongly disagree with someone and even bite their head off, but not with malice, just a strong need to state an opposing opinion. Just like you did here with ME. So no, not harsh by WS standards, especially because it’s water off a duck’s back for Mr Engle.

It is more just you venting as many of us do here occasionally. If I was not able to vent here at WS, I would have gone crazy years ago. I very much appreciate Wolf for providing a safe space for us and himself to vent. I also appreciate the readers who put up with my venting and sometimes even slapping me out of my stupor.

In my case, the stupor arises when the tsunami of news analyzing the most insane economic period in modern world history happens to coincide with my life. The old Chinese proverb “May you live in interesting times” is indeed a curse. Again, such is life, and I am thankful that I have Wolf Street to keep me sane.

Fat & all here -good on ya’, mate.

and, may we all find that better day…

ME, I think the bloom is already off the rose with both stock market and economy slowly rolling over into an eventual abyss. Your writing is similar to FEDspeak; reader has to parse the words, but there is a clear message in their once one has had his or her 3rd cup of coffee. Also agree that Powell is probably toast, even if Janet is jumping up and down as his cheerleader. What would be 3 qualifications or policy goals for a Socialist Fed Chair??

The continual staving off of a necessary recession has been disgusting. It’s been going on for years.

Easily more than half of investment vehicles should be illegal.

Now the hole is so deep that we are looking at the demise of the current currency system overall. Buy guns and grow food.

The monetary and fiscal steps taken to avoid recession is either hubris or an acknowledgment that society is so fragile it cannot handle it. An example is proposing additional open ended entitlements using ridiculously low cost projections when the country is broke.

I think it is a combination of both.

Beans, bourbon, and bullets might compose the basis for the forthcoming doomer ETF . . .

Can’t grow food, we live in a townhouse. But we can walk to three different grocers. And if there is money there are several good restaurants.

We have one car as we live on a great transit line. If need be, we can keep the car parked or sell it off.

Being retired, we have no debt and F&C home.

The primary reason I use a credit card is to receive cash back rewards…in essence, FREE MONEY.

Every year, I open several new cards that offer a cash bonus if I would use their card and $500 or $1000 in the first 90 days. Then I throw the card in a drawer and never use it again. I Never carry a balance or pay an annual fee. Back when banks actually paid interest on your savings, it would also allow me to float my money and earn additional savings as well. When I live in Mexico or China, cash is king and credit cards are shunned.

DD

I use a credit card when I could pay cash because in the UK we get free buyer insurance against any non-performance by a merchant. I’ve had failed holidays and broken items, etc covered over the years. I always pay off the balance in full every month and I get a nicely typed up list of all my spending to file, at no cost to me.

I’ve done this ever since I got one of the very first UK credit cards in 1968.

One somewhat positive effect of having multiple CCs is that it lowers your ‘debt-to-credit’ ratio; which usually positively affects your credit (‘FICO’) score. Which, of course, helps you get more credit cards, at more favorable rates.

I have over $125K of ‘credit’ from several cards. For decades, I’ve only used a small portion of this, on one card, and paid it off every month. Now that I’ve been forced to remodel and relocate my card balance–still paid off every month–increased significantly, and it knocked some of my credit scores down 50 points or more.

How long before student loans pass car loans?

One last comment: Interesting that Credit Card/ Revolving Credit is below the levels of 2008 – 2009. Whether or not it stays there in the months ahead is the Million Dollar Question. Probably not.

Americans are probably tired of getting raped by the usurious annual rates that credit card balances carry. An outright personal loan is always much cheaper assuming you have a decent credit rating, but no-debt right now is not a bad goal either since you can become a leveraged vulture in the quarters ahead when many defaulted upon or cratered assets are available and some lenders will be begging you to take out a loan.

Patience and frugality are tough virtues in an America spending at 90 mph. But consumers and the Government are quickly running out of firepower without creating an even bigger mess than we are already in.

I got it wrong. I’ve been cheering those who climbed out of their debt pit, paid off their loans/credit cards and could breathe free again. After reading this I’m not so sure since they seem to be diving back into the pit again. Maybe they like the security of knowing they’re owned by the banks 24 hours a day and when they go to sleep at night have to worry about making their next 30% interest payment on a cash advance. Plastic junk isn’t that important to us anymore, we’re trying to jettison it in the final stages of life. Dishes, clothing. We have a small, ancient second house on our property filled with xmas decs, discarded furniture, old fotos, clothing, dishes and medical supplies, enough to almost furnish a second home. Why do I need POINTS? How about something I can use at the grocery store and to pay the utilities, like INTEREST on savings? I’ve

dumped half my savings into the stock market and the other half lies fallow in the bank, drawing ZERO interest. This is a sin against the American people who worked all their lives to amass a retirement fund.

There WERE no 401k’s when I worked, we could put exactly 2K/yr in an IRA, while paying 13% on a home mortgage. Different strokes for different generations. Oh, and everyone back then was skinny and not by choice.

You either have high return on assets or low interest on loans. You can’t have both.

If you get higher interest at the bank, you will get lower returns on your stocks. Congratulations on owning stocks, BTW. Many people don’t.

Given your “When I was young” rant, we’re probably of a similar vintage although obviously different grapes. I hold a lot of cash and gold. Most of the time they sit there being boring and unproductive.

I don’t mind because at my age losing half my wealth in a bear market would be hard to make up now. If you’re half stocks and half cash you’re losing to inflation on the cash but the stocks are compensating. If there’s a severe prolonged bear market that cuts stocks 50% you’ll only be down 25% vs a 100% stock portfolio.

The people being screwed by low savings account rates are the ones with no assets like stocks, bonds, or real estate that do well in low rate environments.

This is almost half of the country. But they get what they Fed calls “trickle down wealth effects” which is a fancy way of saying they’re getting pissed on.

I fail to comprehend why accumulating free money (points) by using credit cards and paying off the balance every month is anathema to people.

We all just have to figure out a financial survival method that we can be happy with based our needs and abilities. I know even if I was mega wealthy I wouldn’t be happy with all the trappings of wealth as that’s to far from how I grew up.

The mob is very angry:

The banks are now loan sharking.

Pimping is downhill since friends with benefits showed up.

Gambling is now Indian run everywhere

Dope is being legalized in many states

You see……the white guys win again……they were jealous of the mob and wanted those jobs and revenue so suddenly all those illegal activities are legal. Amazing how the greasy mob becomes the clean cut white boy. Very similar to the land tricks they pulled on the Indians.

White man only lies when his lips move.

Just think of Jay P as a button man working for Don Corleone.

7) In real terms, credit cards balance is below 2011 level, and HELOC are below 2000 low, the lowest on the chart.

8) Socialist Fed will declare a limited students loans jubilee to cleanse debt.

9) WTI neckline with Oct 2018 will send it down until the inverse H&S

will be completed, years from now.

10) When WTI jump > the neckline to the neutral zone, the real inflation will

destroy the US dollar.

Yep, oil is a wild card for the Inflation Genie already miles from the bottle and partying on 5th Avenue. When things really go into the toilet again, and the flush has already occurred, just swirling around the bowl right now, the old geezers in Washington will start another shooting war in the Middle East and then watch crude go to $120 and beyond.

Wars take the publics’ attention away from some of the meals that they are missing and the leaky cardboard box that they are sheltering in. And payments for petro will not be predominantly in Dollars, but baskets of allied countries’ currencies, some of which we do not get along with.

To paraphrase Mark Twain, “The rumors of peak oil’s demise have been greatly exaggerated.” We won’t “run out,” but fracking chews up capital and tends to spit up negative returns. I think we might see a shadow/stealth nationalization of petroleum production in the next several years, if things got bad. Solar and wind are just not going to cut it in the short or medium term. Only issue is that when oil hit 147 in Summer of ’08, that pricked the US housing bubble economy (helped along by the Fed jacking up rates). If we get over 80 or 100 for WTI, I wouldn’t be shocked for some similar action to occur.

If this G nationalizes the oil industry, the rest of the world’s crude producers would have us by our short hairs. You can bet on that.

As far as I understand it the $1.6 Trillion is the largest asset the federal government has. If it’s forgiven I assume that’s $1.6 T that will be added on for government to roll over in perpetuity. More Zirp and QE and longer treasuries will have negative real yield.

11) Construction workers in the “healthcare sector” are building roads

and bridges far away from home, making good money in over time,

paid by the pandemic budget.

I’m still laughing at “When the cheese runs out”

???

They will be crying out: “Who moved my cheese!”

— Dated reference to famous book of same title which tells a parable about how humans count on their ‘cheese supply’ to be constant,

Better than who cut the cheese! Me bad.

Don’t worry, the stock market is recovering yesterday’s losses.

Construction workers working for the health sector ==> that’s why

the Fed is buying MBS, to finance gov debt in other sectors, or to

support favorite politicians, cities & states and for the invisible hand.

JMG – I think this was for you.

“I was born one mornin’ when the Sun didn’t shine

I picked up my Shovel and I walked to the Mine

I loaded 16 tons of Number Nine Coal

And the Straw Boss said, “Well, a-bless my Soul”

You load 16 tons, what do you get?

Another day older and deeper in Debt

St. Peter, don’t you call me ’cause I can’t go

I owe my Soul to the Company Store”

(Tennessee Ernie Ford,1955 hit)

Well,the only difference between THEN and NOW-BACK THEN people actually tried to pay off their debts.And being debt-free was a badge of distinction.And paying off mortgage usually ended in a block party.

Nowadays debt just balloons w/o the slightest prospect of being repaid.

Debt-free people are regarded with deep suspicion.Bank of America girl stares at me in wild wonder: “How come you dont have a credit card ? Without credit card you cant have credit history and,ipso facto,high credit score.(You should be ashamed of yourself !)”

Next time BofA will make the scene complete with George Thorogood music:

Branch Manager spoke up-

Said “Leave him alone.

I can tell right away-

He is b-b-bad to the b-b-bone “

BofA? I suppose Springsteen can work with those guys, and come up with another song for the struggling little Tom Joad guy. A pretty tall order having been locked in with the super elite rich for so many decades now, to actually try to relate to someone struggling hard on the lower rung of society whose getting kind of screwed over, by exactly the likes of BofA. But I still like the Boss.

BofA is not beyond redemption.

After failing to coerce me into applying for CC or taking $30K personal loan they sent me Birthday Greetings email with flickering candles…

B

In the UK consumer credit started very late 50’s, it was called ‘Hire Purchase’. The nickname everybody used was ‘live now, pay later’

Who would have thought that later never ever came!

I think consumer/business credit is as old as Ancient Babylon,before credit cards the name was “installment plan” etc…

When I was young I countered CC card offers by the bank employees with exuberant “Yeah ! I would prefer BofA EEC-PL credit card !!!” then explained that EEC-PL means Extortionist Extension of Credit-Predatory Lending.

With years my exuberance somehow abated and nowadays I mumble politely “I am old school.I dont believe in spending money which I dont have.Debit card suits me just fine.” and they let me go…

Brent-the ol’ pea-picker gave the definitive performance, but to give him his due it was written by the great Merle Travis.

may we all find a better day.

The Fed and government run things to continue putting money into the pockets of bankers and the ultra-rich in the areas of finance, healthcare, real estate, higher education and every other speculative business.

There is no interest in creating an environment where creators of real goods and services are rewarded, because those are not areas where billionaires can dominate markets with legal, political and financial tricks.

Can you imagine an economy that was built to reward companies for building manufacturing plants here in the US, for export to the world? Can you imagine an economy that tried to actually reduce the cost of living a decent lifestyle with low housing costs, low insurance rates, low healthcare costs, low cost and high quality higher education and continued education. The things that would benefit real people.

– Limit interest rates on credit cards to a percentage above the cost of capital for the banks

– Limit all mortgage to 15 years max. That means housing prices would be much cheaper and people would be able to pay off their homes and that would give them stability for retirement

– Force every medical provider to quote and post price lists for all medical procedures and visits. Focus healthcare resources on prevention, nutrition and lifestyle factors, that can reduce the most costly healthcare. Have the FDA increase the amount it charges drug companies and use that money to fund research on healthcare interventions that involve nutrition and lifestyle. Reduce the number of years drug companies have for patent protection. Pay doctors based on outcomes, not on just visits and procedures.

– Have national building code rules and regulations that help to pave the way for new building techniques and reduce local bureaucratic controls that prevent development

– Create a corporate tax code that heavily favors both job creation and production activities in the United States. Trump’s increased tariffs on China simply pushed production to countries like Vietnam.

– Reform government pension plans across national, state and local agencies to ensure stability of those pensions, but also eliminate the over-compensation of government employees that are no longer productive.

I could come up with a list of 100 more changes that if appropriately applied would create a country that encouraged self-sufficiency and productive output and decreased the enormous wealth gap. But Washington DC is a vile pit of snakes that would never allow any positive changes.

Its called a client state.Easier to please a handful of Veey Rich and powerful than a mob of Millions with vastly differing needs and opinions,eants and experiences.Vietnam,Bangladesh,Mexico,Cambodia,and Turkey have been doing superlow wage jobs formerly done in China,for Years.This is old news and one reason theres inflation in China. Outcome-based medicine has become more predominant in tandem with more preventative practices.China can have the toxic,polluting jobs,more cancers we do not need.

They pretend to lend to us, we pretend to borrow from them. Our family mottoes:

“You will owE nothing and be happy!”

“Pay cash for everything bought from people we know in the community. Expect a modest discount.”

“Accept only cash for work done, offering a modest discount.”

“Take whatever the government gives you and withdraw it as cash immediately, like those prepaid stimmie cards.”

“It’s ok to cheat, steal and treat corporate strangers like a lending library, i.e. Target, Home Depot, CVS etc.”

“Share everything durable with neighbors so they don’t have to buy so much and neither do we.”

“Make sure your very oldest relatives, have as many credit cards as possible, charged to their credit limits, making, or not making, minimum payments.”

What a lovely family.

Rip off “corporate strangers”.

Run up debt for the elderly relatives hoping they’ll die before starving to death paying the minimum usurious rate, so you can borrow money you don’t intend to repay.

“Expect a modest discount” paying cash to people you know. EXPECT? You must be Mr Popularity.

I wouldn’t be surprised if your neighbors don’t want to lend you their lawnmower or share other durable goods.

Knowing what I know about you now I wouldn’t let you near anything not nailed down.

The can gets bigger, you need a bigger leg.

1) Those who hate JP today might miss him tomorrow.

2) If a stock fall from 100 to 80 and rise back to 100, in half of the

time, ROC on the right will be higher than the one on the left.

3) Chartists pay little attention to low ROC.

4) High ROC catch their eyes, because they expect highers highs. They

build a positive feedback loop, because they are trend followers.

When they see a breakout, they salivate, constructing a bubble.

5) For the value investors, trend followers are construction workers.

6) They distribute stocks at high levels, bringing it back to value, crush the farmers.

7) The high inflation ROC build expectations for high inflation.

8) JP don’t care !

9) JP might be RIP. He has the budget ceiling in front of him, rent eviction,

unemployment expiration, anarchist teachers…

10) JP will not taper.

I blew most of my stimmies on a root canal and a proctology exam, the rest I just wasted.

I just got my stimulus- plan to blow it all on coke and hookers.

We’re boring, we bought a new stove that we really needed.

We aren’t totally boring, we went to Cancun for a week.

Spent mine on the balance after insurance of a crown for a dental implant. $1,400 was almost the same a the bill owed.

When Wolf ROC is high, with 300-500 comments, u will not see ME.

When Wolf blog is low, I jolt volatility.

Nothing personal.

LOL!

Never change, Michael- I love all your comments.

The timing of all this is very interesting in relation to the path of current inflation.

Rising car credit obviously helped to boost car prices to where they are now, so unless that credit keeps rising, we will probably see car prices steady going forward although there is always a lag effect.

The credit cards were deflationary when the balances were going down but if they have started going up again, that is inflationary and will add to the ‘fire’ but again with time lags.

I can’t figure student loans, my recollection is they would only lead to higher beer prices?

Sometimes a car loan is a student loan. I taught at a community college in rural Colorado where it wasn’t unusual for a farm boy to take out a student loan so he could buy a pickup truck.

There seemed to be very little oversight – a student could not show up most of the time and get straight Fs for a few semesters, no problem. I remember one occasion when two guys, sitting in the back of the classroom, were totally ignoring everything and spent most of the 50 minutes flexing their cool tats at each other.

Hey Wolf,

What do you see here?

Do you know if this happened any time in 2008?

Wells Fargo & Co is shutting down all existing personal lines of credit and is not offering the consumer lending product anymore, CNBC reported on Thursday, citing letters from the bank.

Mateo,

In terms of the Wells Fargo decision to close all “personal lines of credit,” here is what I said a couple of times here already, and I’ll say it again:

Why would anyone today still even use a personal line of credit? Credit cards have long ago obviated that old system. It’s just a small left-over business for Wells Fargo. Makes sense to shut it down.

WFC kept their personal loans, though, which are a bigger part of the business.

Last year, they shut down their home equity lines of credit. In the US, use of HELOCs has plunged since 2009 and continues to drop every year. People do a refi if they need cash from their house.

Things change.

The reason Wells Fargo is pulling back from these marginal loan businesses is that the Fed put a cap on Wells Fargo’s assets (such as loans) to punish it for compliance problems. The bank keeps bouncing into that cap. So it’s focusing on the big profitable types of lending and is shedding the others.

This was also a problem with the PPP loans. WFC couldn’t do PPP loans until the Fed agreed to buy its PPP loans. This was a big problem in California because WFC is such a huge bank here with lots of small business customers, who got shafted by not being able to get PPP loans quickly.

I was in my local ACE hardware store to stock up on some food for my bird and squerrel feeders. I went to isle where the food was located and there were practically no prices on the items. This is the same problem I noticed in the produce section of my local grocery store. I’ve made complaints before at both places, and nothing has changed. This time I called the manager and told him flat out that they didn’t know how to manage a hardware store period and this was a blatant example. They had 20 employees running around like chickens with their heads cut off and they had no one to do a simple task of putting prices on the merchandise.

Swamp-the magic of barcodes and their newer variants-the cashier need only swipe to make the charge, why burn valuable employee-time pricing items? (and you aren’t cluttering up the aisles ‘shopping’…). Again, a case making the tools and gear to aid the mission more important THAN the mission…

may we all find a better day.