Investors may still be doing a lot of heavy breathing.

By Wolf Richter for WOLF STREET.

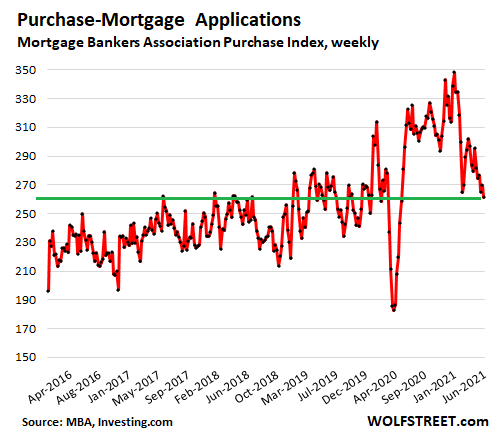

Whatever demand there may be from investors, demand from buyers needing a regular mortgage in order to buy a home continues to decline, and in the week ended May 28 fell 4.0% from the prior week, to the lowest level since May 2020 (when mortgage applications were coming out of the collapse of the prior weeks), according to the Mortgage Bankers Association today.

This put applications for mortgages to purchase a home roughly in the middle of the range of 2019, having worked off the entire Pandemic boom (the big drop and bounce-back in February was the result of snowmageddon; data via Investing.com):

Out of homes to buy? Wait… inventories available for sale of existing homes, while still low, have been rising for months and in April reached the highest level since November, and supply rose to the highest since October, according to the National Association of Realtors two weeks ago.

The NAR also confirmed the decline in sales volume: sales of existing homes have been falling for months and in April hit their lowest level since July 2020, having worked off most of the Pandemic spike.

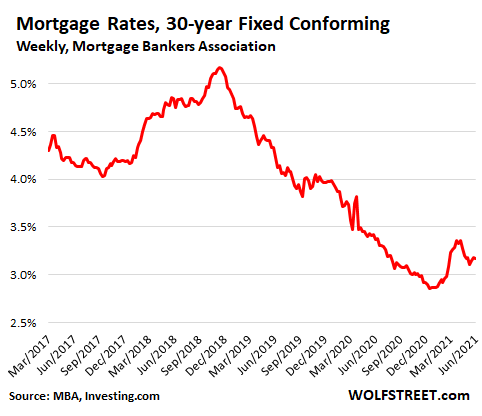

This comes as mortgage rates have ticked up a little from their record lows late last year, but remain near historic lows, with the average interest rate on 30-year fixed rate mortgages with conforming balances and a 20%-down-payment at 3.17%, according to the MBA this morning:

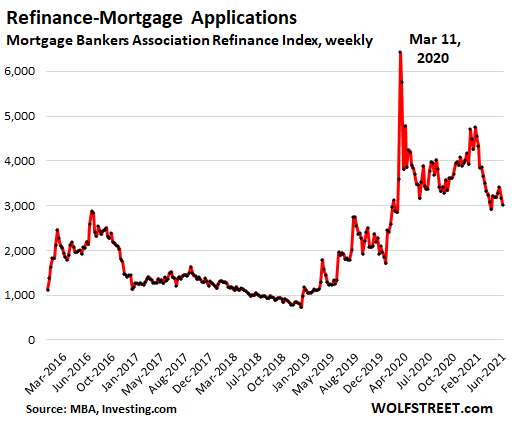

Mortgage applications to refinance existing mortgages have also worked off the Pandemic spike and have fallen below the year-ago-level.

But these refi applications remain over twice as high as in early 2019, when the average 30-year fixed rate mortgage carried an interest rate of a now unthinkably high 4.2%, though they’d been over an even more unthinkably high 5% in late 2018.

What would the housing market look like with mortgage rates at 5% and today’s sky-high prices? That was a rhetorical question. Back then, among the effects it had was that it calmed down refi activity by a lot:

There are now a number of “obstacles,” as the MBA calls it, to home sales, the primary obstacle being sky-high prices, and by extension the affordable supply that has moved out of the affordability range of many potential buyers.

Then there is the possibility that the explosion in volume over the past 12 months, a form of panic buying, is now showing signs of getting exhausted, as many people who really wanted to buy bought, and enough potential buyers that are looking for a home to live in – rather than investors – took a deep breath and stepped back from the “raging mania” and the crazy bidding wars.

Investors are still reported to be out there in large numbers, and worrying even Fed officials. But enough regular home buyers may be staying away from the raging mania to where it has started to show up in the numbers.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Why would a potential buyer apply for a mortgage if there is nothing decent to buy? That is the story.

Men lose their minds in herds; only to regain them one by one.

SocalJim,

These is more to buy now than there was in prior months. Inventories are rising. See paragraph 3, and for further detail:

and new listings:

Meanwhile, the house price average has hit a record high, and the higher end house sales are screaming hot!

Wow, that inventory build is massive, Wolf. Looks like the “SHORTAGE!!!” narrative is quickly eroding.

It gets massiver by the day :-]

Hey DC, you need to shut up and buy….well at least that is what the realtor clowns and speculative investors are saying. All trends are finally pointing (hopefully) to a cool off. This market has been made so dang predictable at this point. The Feds comical fiscal responses and speculative investors have backed themselves into a corner. You’ve pushed homes to all time highs with near all time lows with rates….what did you expect? And now they can’t get out of the snake pit for the hole they dug themselves.

DC

All that shadow inventory will appear as if by magic. I may add that so far we’ve received no pressure from lenders to jack up appraisal prices. I believe the lenders are glad to have an excuse not to make a loan on an overpriced property, unlike 2006/2007

Factors:

1. Mtg Forbearance is ending.

2. Empty second homes are no longer a good investment.

3. Prices are reaching a point where the properties are unaffordable.

4. Mtg interest rates are rising make house payments larger for the same loan.

5. Banks don’t want a repeat of 2006/2007 and are being more careful about making loans.

We’re back to work after a month off to get vaccinated and all gross side effects. Will keep you posted on the Swamp RE trends.

People are taking a wait and see approach because the prices are insane?

This is usually what happens right before a crash. Sellers won’t drop prices, because they know that they could have gotten more a few months ago, but buyers won’t buy.

It stays like that for a while until a few sellers realize the prices aren’t coming back.

Where I’m looking I see a lot of homes that are income properties and home based businesses being listed. Very few homes that are actually nice, good quality family homes in good neighbourhoods. I haven’t booked a showing in at least a month. Am prepared to wait it out in definitely.

Yep! We are taking a wait and see approach. We are in the of the hottest markets in Northern California and we tapped out about 1.5 months ago following poor advice by our realtor and buyers who think they can have whatever they want. No thanks! We are stacking our cash and patiently waiting.

Hopefully more and more buyers will join me on the sidelines! -BABS

Just because there is a quantity of inventory does not mean the inventory is high quality. In my area, I’m seeing a lot of beat up ex rentals hitting the market, or fix and flip junkers whose paint will soon be falling off (again). I’m not inspired by the inventory I’m seeing in Oregon.

I live across the river in WA, and I am amazed at the bidding wars, and the number of CA plates I see now, every day. We have only slightly more inventory, on the market only slightly longer, most are gone in a week. People are waiving inspections, and paying part of seller’s closing costs for really desirable properties.

In the bottom graph i see the leg up of the normal yearly pattern. Only April 2020 distorted the yearly pattern for 2020. We will have to see how this pattern will evolve. The top graph is more telling. There is a long term (multi year) trend towards a shrinking supply. If that trend is holding house prices will go up, because demand is chasing an ever lower inventory.

I completely agree. There’s too little inventory, which is driving down the loan apps and new mortgages.

New home construction ticked up.

hope prices collapse – with home builders paying obscene lumber and other prices

we decided to put on hold for 2 years(or longer)

we’ll see were 20% INFLATION IN EVERYTHING goes

not going anywhere

and will not be buying like 2020 anymore

time to raise more cash

Buyers whose employers or businesses are failing might not be excited to sign up for inflated mortgage payments as things worsen, particularly now with adjustable rate mortgages. The retailers are in dire straights, reportedly.

I wonder how we could quantify how many small and medium size businesses in the US will fail and are failing, since not all file for bankruptcy and many were left with huge rent arrearages? Some lessors may patiently await payment but not all will or can be reasonable.

> if there is nothing decent to buy?

Homes from the elderly who died and had a reverse mortgage are coming to the market. Bought one myself for a super decent price.

Higher mortality is the key to normalizing the housing market given NIMBYsm.

After looking for a home the past 3 months, outside of Seattle, the wife and I have finally decided to step back from the mania. We’ve seen too much of the insanity and would rather move than play along.

Move out of the area? If so, why? It’s the same story everywhere. Just renew the lease and revisit the situation next year, though I don’t anticipate any “deals” for 3 years minimum.

The Midwest is super cheap, remote work is here to stay.

It’s a massive geographical arbitrage that the young don’t need to wait until retirement to exploit.

Let the NIMBYs in HCOL carry the country on their shoulders while relaxing in a LCOL area.

The issue is inventory. Everything else is noise.

Unearned currency will keep chasing hard assets until nothing left and shortages develop.

Most of the remaining listings are homes with incurable defects. For the first time in many many years, those are moving. Dumb.

In NJ even those incurable defectives have been sold, but for a few.

Memento mori,

See the two charts above I just posted in reply to SocalJim. Inventories have been rising and are the highest levels since Nov 2020 and supply is at the highest level in Oct 2020.

So rising inventories and declining sales.

Wolf, in the zip codes I watch, nearly everything left is a defective property … busy streets, tiny lot, next to apartment, …

In fact, it seems that people with defective properties that have incurable defects are taking this opportunity to list them … there is a flood of junk hitting the market.

A cherry picker says what?

I have the opposite experience. My wife and I were in the thick of the craziness a couple of months ago before deciding to take a breather from this market, but I have to say Solano County and Contra Costa County listings have definitely increased and with some nice homes…only problem is they are even more expensive than 2 months ago. Fingers crossed ever increasing inventories and sluggish sales with put some much needed downward pressure on these crazy ass prices.

Same behavior that existed just before the drop off in 2008. Dont get me wrong, dont think it will be the same situation but could have the same effects in longer terms.

Memento mori,

was it you yeterday that commented this on the ft site?

Réne Descartes: I think therefore I am

JPOW: I am not even thinking about thinking.

HAHAHA. This is a brilliant one.

You blew my cover ?. It’s a small world.

Give me back my anonymity, I need to change my handle now.

it’s a small world indeed.

Isn’t the ‘unearned money’ the issue then and inventory actually the noise?

We also were gung-ho on buying a few months ago and have slowed down. I have seen that the houses I am following on Zillow are dropping their prices. One today dropped $65K from the initial listing 1 month ago! If they come down more, we will rethink.

Same here. Was looking for over a year and stopped watching all the prices climb. Now the prices are finally falling. But they were overpriced to begin with.

I am seeing the same in San Diego

Although inventory is low but lot of homes coming back to market and price reduction as well

My friends who were looking to buy decided to wait and would leave CA if needed

> would leave CA if needed

Even if not needed, it’s the financially savvy move.

Outrageous!!!!!!! I won’t have any of this!!!! Expect further rate cuts from me as soon as possible!!!! I will be buying more MBS and treasuries!!!!!! I will be doing the short/long treasury switcharoo!!! No one can stop me!!!!!! THIS IS NOT A BUBBLE!!!!!

Your CAPS LOCK did it!!!

If you truly meant it, and were truly frantic, you’d get a few 1’s in amongst the !!!

!!1!!!11!

1) Inflation usually change people behavior : buy now, because tomorrow prices will be higher.

2) The charts above indicate that buyers don’t believe in the inflation story.

3) Plenty inventory in the flyover country. Plenty inventory in NYC.

4) For sale signs for more than half a year.

5) The expensive apartments list is getting longer.

6) Mortgage application decline for 20 weeks.

Fed policies are a lagging system. Not only in terms of implemention, but also in terms of structure.

Pre-information age, flooding liquidity into the banking system could drive growth.

Now, all local data is international. This includes data and information regarding housing. Why would we assume money will work it’s way to benefit a mythical “middle class?”

Isn’t it easier for it to flow into a real estate ETF, housing related spac, or someone else wanting to start a “venture?”

Why take the time for due diligence, validating that mythical John and Jane doe work where they do, and have viable credit ratings.

It wouldn’t actually, make sense.

Spigot turned on, and there is no locality to real estate anymore.

Working, I won’t even say families, since those are now pretty much outliers, folk who want a place to call their own are having to make purchasing decisions on the hand-me-downed, fronted, exorbitant price levels created to profit people other than themselves.

The system is severely flawed and inequitable.

So now, people rationally wait until the money that wants to suck out their blood by being spewed out before them, drys up.

And thus, defeating the entire “purpose” of the policies to begin with.

Guess what, there’s no maligned actor here. The fed is doing what it can do, the bankers are doing what they can do, the speculators are doing what they can do.

There needs to be systematic change to account for the technological ones that have occurred over the past 30 yrs, otherwise, we are just all living within the stagnant and immortal beast from Jekyll island.

7) People who want to escape the virus are not looking for something

nice to buy. They will buy now, anything offered to them.

8) The vaccine change everything. This fad is over.

If one rushed out to get vaccinated, one was probably scared enough of the virus to move and buy a new house. If one was more cautious and investigated Ivermectic and such, one probably didn’t rush to buy a house. The fog is beginning to clear, no matter what the government is promoting.

I have a good friend who is a very good mortgage broker (Texas location). He told me this last week that mortgage refi’s have come from a deluge last year to a trickle now. And he said that new financing on homes (not refi) have all but stopped in May. He is laying off a few of his associate brokers.

This is Texas near Houston, which is not the center of the RE Universe like Ca, Or or Wa.

What? How come the stimmies aren’t propping up this market too?

Everyone needs a good scapegoat!

Stimmies of $100s of thousands are in order now to correct this problem. Forget these stimmies in the thousands….lol. Just ask J-Pow, he can’t seem to figure out how to unplug the money making machine.

“But enough regular home buyers may be staying away from the raging mania to where it has started to show up in the numbers.” …….. think of it this way: when no one is buying homes to live in them because they can’t afford them and only investors are buying, the Fed will have “solved” the housing affordability problem.

What I notice that is odd is that closing times are now averaging between 12 and 16 weeks. It appears if a buyer doesn’t qualify that shows up in about a week, cause if houses go back on the market they do so within a week or less of the contract.

A couple of people have told me the mortgage companies have “lost” their applications a couple of times during the process.

It seems mortgage companies are reluctant to lend.

OE, getting a mortgage these days requires good credit, 20% down payment (unless VA), good job, and some time. It’s not like the good old subprime days!

Absolute nonsense, Anthony A. I’m sick of these lies. If you don’t know the truth, then don’t spout off.

“In his corner of American finance, where hard selling meets hard luck, Angelo Christian is a star, and he looks the part. He’s wearing black caiman shoes and a Bordeaux-red silk shirt, tight and open wide at the chest. His dark widow’s peak is slicked high with gel. He has 180,000 Facebook followers and a budding YouTube network, where he shares original videos such as “How to Master Your Mind” and “How to Manage a $50 Million Pipeline.”

Many of Christian’s customers have no savings, poor credit, or low income—sometimes all three. Some are like Joseph Taylor, a corrections officer who saw Christian’s roadside billboard touting zero-down mortgages. Taylor had recently filed for bankruptcy because of his $25,000 in credit card debt. But he just bought his first home for $120,000 with a zero-down loan from Christian’s company. Monthly debt payments now eat up half his take-home pay. “If he can help me, he can help anyone,” Taylor says. “My credit history was just horrible.”

Depth Charge

Ha, I thought Anthony A was being sarcastic. That’s how I read it. Maybe I goofed. Maybe he was serious :-]

If he was joking, Wolf, he has my most sincere apology. I have just grown so tired of people spouting narratives and memes irrespective of the truth. This is why I love your site so much. You offer cold, hard, irrefutable facts supported by the evidence.

Wow, are we back to 2005/2006 time frames. Except now the action is on social media.

I wonder if these are getting packaged into AAA bonds again. ha ha,that would be hilarious.

Subprime never went away, contrary to all of the lies people are being fed. It’s the only way prices can become so detached from reality. No-doc loans are still around – everything from last bubble. By the way, the article I quoted is more than 3 years old. Google it. Subprime is everywhere – mortgages, auto loans, credit cards, RVs, boats. How do you think all of those people are driving new cars?

I was joking…..

My bum of a stepson, who is a felon with no job, but SS disability income (only), and lives with his Dad, bought a new VW Jetta with $2000.00 down earlier this year (stimmi money). He was financed @15%.

I would have figured no one would finance him as he had a car repossessed a few years ago.

Exactly. Reminds me countless senseless approvals in 2007/2008 when hearing stories like bus drivers getting approved for million dollar loans.

That is a frightening quotation Depth Charge. It really does make one wonder if another 2007 – 2008 scenario is coming.

The Fed is never going to let the mortgage market crash the system again. The implications of quasi-MMT (forbearance as far as the eye can see) is lower mortgage rates and easy consumer access to loans. It’s their right baby, and the shadow banks are going to do the work, and the charters are going to bail out the shadows, which is why Warren B owns all of them, although he did sell his stake in WF. History repeats itself as farce. Better to be invested in the “bailed out” institution.

DC

Speaking of facts, because of the lack of inflation in grocery prices over the past 2 years I have started upgrading the food choices I make and am starting to buy gourmet food products more often like German cheezes, Crab claws, Rockfish which I used to pass up because of price. I’m living it up. I want to thank J Powel for keeping this part of my budget under control. As far as housing costs, that ain’t my problem as I have my mortgage paid off, and these Montgomery County politicians wouldn’t dare raise property taxes or they would be thrown out of office.

My biggest problem is getting a tee time at my local golf course. The courses are packed.

Yeah SC, everyone is plain stinkin’ rich around here, too. Can hardly even find any caiman loafers to buy.

“It appears if a buyer doesn’t qualify that shows up in about a week, cause if houses go back on the market they do so within a week or less of the contract.”

That has not been my observation with properties I follow on Zillow. Often properties that go back on market (after change to Pending status) do so with a lag of 3-4 weeks, sometimes more.

Reason given in new listing for property being relisted is “Through no fault of seller” or “Financing Fell Through”.

Yea right. I made an offer a year ago on a vacation home subject to inspection, because the previous 3 offers backed out. Sure enough, the west wall had to be completely replaced, studs and all, due to rot. Seller wouldn’t even give me a price reduction. I have made 15 offers in the last 3.5 years and found other defects where the seller wouldn’t budge. Insanity ! I give up. There will be a lot of remorseful buyers out there.

This is a ticking time bomb. Most are focused on meeting minimum payment, unfortunately, not upkeep and maintenance. I’m certain there is gonna be more of this to come with hidden, costly expenses for homes that at some point will flood the market.

I watch what comes on Zillow in three different locations in the Portland Metro area on a daily basis. So my gage for inventory is how many new houses come on the market in these places on any given day. The number of homes coming on the market each day has been steadily growing from its bottom in the depth of the pandemic. It is not back to where it was in the summer of 2019, but on the way back up. I think the thing hurting sales ( and thus mortgage applications) is prices. Maybe prices can keep going up in Miami due to drug money, or SoCal due to Pyramid scheme entrepreneurs and reality tv stars but in most of the country people have to get a mortgage which is based on their actual income and savings. The price run up has hit the wall and something will have to change or there it will stay.

I would love to be excited about this data but the other half of me knows that the supply shortage narrative is strong with this one and all lemmings will plow right in if there’s a 5% dip in price…this herd is insistent on going off the cliff, any buyer strike is probably pure wishful thinking at least not until we turn FOMO into FOOP. Wilmar Powell won’t let that happen, better turn that $40B MBS purchase into $100B soon to get it goosed.

Just saw a sold listing on Refin on a 1900sq ft house in Placentia, listed $850k, sold for $1M…yup no buyer strike in that area apparently..

I don’t think there’s any doubt in anyone’s mind that a lot of the famous “sideline money” will jump in at the slightest dip.

The question is what happens after that.

This is where being young (b 1981) and not having gone through any of these cycles (not as a buyer / potential buyer) is a disadvantage… so grain of salt with what I’m about to say, etc.

But I am really looking forward to observing and learning how the psychological element plays out in a falling price environment where it appears so much of the market has been captured by speculators. Isn’t the phrase “dead cat bounce” one of the possible outcomes of “all that” sideline money from us little guys hitting there market and making a mere blip? Then what?

Wonder how much buyer’s remorse there will end up being among the cohort of people whose primary reason for moving to the ‘burbs was escaping the pandemic. Living in the suburbs is a whole different kettle of fish from living in a major city. Plusses and minuses to both. It’ll be interesting to see how it all shakes out.

I am going to assume a lot, neighbor of mine upstairs bought the place for $450K, wouldn’t pay half of that in “normal” time. Young couples probably first time buyer, think they are already regretting it. Moment they moved in, discovered there’s water leak in the bathroom and couldn’t use one of the bathroom already. HOA is worthless here, charge $400 for basically nothing, last HOA embezzled money, this new one also suck. Would be surprise if they are not regretting it now.

Last owner went small time investor and flipper, probably also stupid, bought the place for $400K ish, paid to put in hardwood floor and freshen up the place and basically sold it for a loss after renovating in matter of a little over a year.

Not so sure that premise that living in suburbia or exurbs makes you more safe against pandemics holds much water. Sure the houses might be a scooch farther apart but not by much. Big deal.

You still have to encounter people at close range go shopping, get gas, and run other errands no matter where you live.

Unless you live in your basement and won’t come out for any reason.

It makes you safer from crime ridden cities who think defund the police is good policy.

You are 100% correct. My wife and I are leaving our home in Portland after 10 years for exactly the reasons you address. A homeless camp at the end of the block has 4 stolen cars. This is the new normal. Drove 10 miles into the suburbs across the river, not a homeless person in sight. Parks were clean and dozens of families playing together happily in the parks without a mask in sight.

Living in a single family home in the suburbs, makes living through lockdowns much easier. First, even a small house has more space than most apartments. Second, you don’t have to deal with common halls, staircases, or elevators. Third, you have your own private yard for access to the outdoors – extremely valuable with children.

As for shopping, suburban stores tend to be larger than city ones allowing for easier social distancing, and travel to and from them is in your private car.

But with a yard comes either maintenance ($$$). And the benefit of a complex is somebody is paid to care and clean that pool, spa, gym. All things balance out and have their ups/downs

It’s more a psychological thing. More yard, more space, pedestrian traffic is controlled, quite possibly 100% less rioting nearby. If they WFH and want to raise kids, well, FOMO before it’s all gone. Rent versus mortgage probably not a huge difference.

Just get the vaccine and a lot of the risk goes away.

Someone help me understand.

Okay so investors are flooding the market and paying way over asking for virtually anything in sight. Often without on site inspection. Of course driving prices past what is reasonably affordable (or what they are worth)

Then they bundle these mortgages into a marketable asset and sell them to various investors in the form of REITs? Which promises great ROI. And they are back stopped by the treasury? So no matter how much they pay for the property they make money at the point of sale to these REITs?

Then when housing prices collapse the REITs are bailed out by tax payers? Who can’t afford housing?

And if the treasury stops backing these everything goes into free fall and totally screws everyone who has been competing against these titans over the last 2,3,8 years?

And something else. If 50% of homes are all cash buys doesn’t that indicate that there are no bank loans on these properties so if they tank the sole loss is with the buyer and not the bank but by the taxpayer?

And people post that we need less government intervention. Seems to me the opposite is true.

Where am I wrong on this?

You have it pretty much nailed. Wall street will now lose and the MBS owner will not lose. The home owner will if the price drops.

You will not have to worry about the MBS not being backed. The GSEs back the MBS and the FED will bail out the GSE like they did in HB1.

Wall Street will raise more money and buy up more homes if their are foreclosures.

In reality, since the GSEs back or bought most home loans they are probably the biggest landlord of all. I would not be surprised if there is a housing crash that the GSEs will just rent to the foreclosed owners. Some Wall Street company will form to be the front end servicers of the rentals. LOL

Now some of the cash buyers are mom and pop people who probably took out loans against their 401ks. They could be stung a bit but luckily, houses do not go to zero like a bankrupt company.

Chicken dinner for you!

Here is the one I worry about … a new and much more deadly Covid virus shows up … imagine the panic. People would run from the cities and house prices triple crash. Very unlikely, but possible.

6 homes for sale in few blocks of each other in Livermore Ca, still on the market after 2 weeks. 45 minutes from Silicon Valley. Getting back to normal?

Hmm, It looks like all the ducks that were going to fly the coupe from S.F, did.

Nah, if they drop price back to asking or 1-3% less, the frenzy will be back on..

Most homes for sale intentionaly leave the listing active to allow the most amount of potential buyers to see it and fully engage FOMO. listings quite often state “offers accepted on certain date”

Taking the first, or more often pre-empivte offers likely results in leaving momey on the table.

I’ve seen this practice too.

A listing will go under contract but pending property listing will now state “Accepting Backups” (additional offers accepted in case current pending one falls through for any reason).

Personally I am hoping for one of those UAP sighting released by Pentagon means an alien invasion is on the horizon. Independence Day style, that should help reset the market nicely.

Then again aliens probably came to take a quick look and headed right back out in a hurry, taking over this flaming s*** show of a planet? No thanks..

Aliens probably took one look at the outlandish house prices and said to each other– we can’t afford to live on this planet.

Less mortgage apps due to cash buying investor mega corporations?

Possibly.

RE investors, as Wolf points out, are still in the market (and I would add are still an obstacle to freeing up more precious inventory for buyers who want a home for shelter).

Wolf mentioned at one time that there are people buying new houses that do not sell their previous ones– they are engaging in a form of arbitrage to ride housing bubble up and sell old house later for a handsome profit.

I’ve heard that other ‘investors’ are simply buying up houses as speculative investments or use them as cash cows to rent them out for a reliable cash flow when other forms of income are so dodgy now.

And still worse, I’ve heard that big corporations like Blackstone are making deals with home builders and are buying up whole brand new subdivisions of homes before even first bulldozer scrapes the earth.

If all this crazy stuff is really happening and the authorities don’t intervene it is entirely plausible that average people will no longer be homeowners— and we become a nation of renters.

“You will own nothing and be happy”.

Toll Brothers CEO said owning a home will be a luxury in the future.

I am in fly-over so houses are still reasonable. Sure they are up 30% over the past 3 years but they are still cheaper than building.

I read only 15% of homes are considered starter homes. You know the small 2 and 3 bedroom homes.

I looked in my 2 million person metro area. Right now there are only 71 4 bedroom single detached homes for sale that are 4 bedroom or larger. All new 4 bedroom homes in my area start out at $400k.

My 4 bedroom home price has risen from $250k to $350k in 3 years.

I am not worried about it dropping in price because there is no way they can build a 4 bedroom house for what it would cost to buy mine.

Lots to build new houses are all over $100k too . Sure land could go down some but not much. Maybe $10k to $15k. Labor will not go down. Lumber might drop some but not much. I am guessing if there is a downturn, housing my area at the most will drop $30k as that is about the most the input prices can drop.

FYI. During HB1, housing in my area dropped on the average of 10% as it did not have a huge bubble. Same thing will happen this time.

So much is geographically dependent.

“I am not worried about it dropping in price because there is no way they can build a 4 bedroom house for what it would cost to buy mine.”

With smaller households these days (2.53 persons in 2020) just why would 4 bedroom houses be in demand?

I know some people with either lots of money or easy access to credit want and buy fancy schmancy big houses (and expensive to heat and cool, not to mention higher cleaning and maintenance expenses) for prestige and to look wealthy to family and friends, but in today’s economy that would be foolish for most of us.

The argument that older houses are worth more simply based on replacement cost alone sounds a bit shaky. There is a lot more to housing market than current (and always subject to change) prices for raw materials like lumber.

The only people dying now are the unvaccinated.

I believe a big part of the rise in prices/rents is from people/investors buying in order rent on Airbnb, VRBO, etc. and taking houses off the market that would normally be owner-occupied or rented long term. Our quiet, off the beaten path “street” is dusting off our HOA charter and meeting to vote on changing the CCRs so people can only rent their house or guest cottage for 30 days or more. A small corp bought the 5000sf home up the street for $2.2M, put in a lot of money to fix it up, and now advertises it on those sites for $1500/night with “capacity up to 65” and “can sleep 21.” Why would someone think neighbors are going to sit idly while someone runs a hotel in the neighborhood? Because so many people are now doing short term rentals, prices will drop, people won’t make what they thought, and will sell, I predict, within a year or so. We shall see.

Airbnb lawyered up early on to fight all of this illegal hotel business they’re engaged in. I would NEVER buy a house if I knew the neighboring one was an Airbnb. This garbage should have been shut down YEARS ago. Same as UBER. They’re illegal.

Our “good” Governor Ducey executive ordered AirBnB and VRBOs as legal across the state several years ago. These stupid rentals have ruined quality of life for so many neighborhoods and turned them into rotating hotels. I personally refuse to rent them. I know it costs me more money to stay at nice hotels but I also recognize that new daily AirBnB and VRBOs neighbors showing up are not desirable for anyone that lives in those neighborhoods long term. Everyone owns an AirBnB these days. If I rent homes out, I do them long term to folks that can make an investment in that community.

Airbnb and other short term rentals still have to go through the city planning and zoning process to get approved.

If a neighborhood’s residents care about their community’s character and livability it is time they packed city hall chambers to express their views to politicians when these greedy rental parasites show up to pitch their proposals.

Not true in general H,,, at least not yet in many many areas.

Maybe becoming more and more true as states and municipalities realize the tax implications of allowing the airy bnb model to continue to exist ”unregulated”…

FL tried to mandate ”state” control, but last I saw, was totally shot down by the local municipalities, as it should be.

IMHO, just another fad that will fade, as have SO many.

Not true? Then tell me what cities have no regulation of Airbnb-type short term rental businesses and let them operate without the permit approval process.

Thx.

@Heinz Not here in AZ on these. They are trying go that route now but ita been state mandated and overrode since Ducey put it in place back in 2016.

https://www.azmirror.com/blog/short-term-rental-regulation-bill-returns/

Arizona is one of only six states that have enacted local bans on short-term rental regulations. The other states are along with Florida, Idaho, Indiana, Tennessee and Wisconsin.

I’m north of the border. Where rural property is still relatively cheap, compared to what is being sold in the big cities, the real estate market is still manic for new properties. However, the inventory of new properties is almost gone. I have contacts in 4 other Provinces who tell me the same story, that what is causing the drop in sales is that most of the houses now in the inventory require some kind of work, and you simply can’t get the contractors. The ones I know are already booked up for over a year.”If I get any more orders, I’ll have to start lying” one told me last week. That’s in addition to the lack of materials. An apartment block near here was completed last month, but 70% of the units have no/limited appliances. You can’t buy a new freezer for love nor money; ovens? forget it. Some contractors put in used appliances they bought locally and promised to upgrade to new for free ASAP. Those units sold, but now the used appliance inventory is gone too.

Several more conservative media outlets (e.g. Washington Times) reckon this is not real estate investment or a remote-working effect, but a flight from the cities similar to that following the disturbances of the late 1960s. A look at the city crime rates seems to confirm that.

That is so true. Talking to a rental management company in the midwest. They will have a contractor come to inspect a home to provide some maintenance work and the contract will leave and not even call back if the work did not result in a big bid.

In most places, most, everything will eventually make sense again. Apex margin buyers will suffer swift buyer’s remorse before they even close escrow and lingering embarrassment as a member of the subdivision’s “Greatest Fool Club”. Bidding war “losers” will exhale a sigh of relief and rationalize “maybe it was for the best”, “maybe we dodged a bullet”. I know more than a few people on both sides of the equation in ’05-’06.

No way. “Cash Guy” said so.

People are taking a wait and see approach because the prices are insane?

1) New Listings : the trend was up : x4 higher highs and x3 higher lows since 2016, until : Xmas massacre 2019.

2) Xmas Dec 2019 sent the New Listings to a lower low, a spring.

3) 2020 was election year, cv max, Antifa & BLM and media bs . That led to a change the character. A trading range.

4) Instead of peaking in June/ July, as New Listings does every year, new listing turned down in March. June/ July were lower highs. New Listings peaked in Mar 2020 with little recovery : Accumulation !!

5) Since Dec 2020, under a new president, the New listing started to accelerated again. Apr is the last reading.

6) 2021 peak might be reached Sept/ Oct 2021, well beyond June/ July. After a minor correction, the uptrend will resume. The peak might be in 2023/ 2024.

7) A New Listing bubble cause by ====> a new recession.

There is still a dearth of new homes coming on the market due to COVID. Sellers are just waiting until all the restrictions are gone. By July we start to see investories really rebound. The imbalance in supply/demand really flips by late this year – watch out below!

The big issue is all that investor money, which is a result of Fed and government money pumped into the market.

I met a realtor who just bought 2 homes because she thinks the stock market is too expensive. Hmm, homes are a leveraged investment and you cant sell them fast. Sure, she is making great commissions right now with sales booming, but she is doubling down on real estate, both her income and her assets are now relying on this bubble market.

That is what happens at a peak. Let’s check back on the market with 4% interest rates and normal supply/demand metrics. Those buyers who are buying at 20% premium to last year are going to feel alot of pain soon.

Many investors make the false assumption that they can rent it and will hold for the long term, but they dont realize that real estate prices in some places will fall or stagnate for a decade to come, as stagflation destroys incomes at the same time it forces interest rates much higher.

Smart investors buy when there is blood on the streets.

A 20% premium from last year is small potato’s. Today, even JT acknowledged that the market has gone up 41.9% and the majority of that was within a 6 month time frame. As sales happen, I keep wondering if that will the markets greatest fool and if the deal will actually close. Some deals have long closes of up to 6 months and at prices that there is no way the property would appraise for right now. If/when the markets drop, I’m thinking there will be a lot more than regret and the lawyers are going to be very busy. I’m also thinking there is going to be significant knock on contagion particularly with how over leveraged Cdn households already were.

It is actually quite simple.

If you believe that mtg rates will remain well below the inflation rate for at least 2.5 to 3 years, then you need to buy a home as soon as you can get a decent property.

But, if you think the mtg rates will approach or rise above inflation, then you can wait this out.

“If you believe that mtg rates will remain well below the inflation rate for at least 2.5 to 3 years, then you need to buy a home as soon as you can get a decent property.”

This is the most irresponsible, BS advice I’ve ever heard in my life. If you are a young person, do not listen to this guy or you’ll make the worst financial decision of your life, and your future will be severely affected.

Actually, it is good advice. If inflation rates are quite a bit higher than mtg rates, then most homes will appreciate. This is what we are seeing now.

If that conditions holds for at least 2.5 years, then you should have a large enough gain that makes the purchase wise.

That’s a lot of “ifs”. Just sayin’.

But if mortgage rates rise then people’s ability to purchase an expensive home with a mortgage is going to get destroyed. And I imagine house prices would thus go down?

All I’m saying is “Inflation” is not uniform across asset classes. I

And I say this not knowing what asset classes are the “good ones” to own right now

home prices are dependent upon supply and demand and we are seeing an imbalance with limited supply, that is all. yes, the interest rates were pushed down to rates never before seen and that also helped affordability based on lower monthly payments.

but you basically are making a classic mistake. you think that inflation rates reflect home prices. they dont. that is not how inflation is measured. and home prices are pushed up and down by the interest rates, not inflation rates. higher inflation rates will lead to Fed tightening and that will result in higher interest rates, which will depress home prices.

the issue here is that homes are the most leveraged investment the average person will ever make. with a 10% down payment, the principle investment is wiped out with a 10% decline. this is also the only investment where investors can simply walk away from the mortgage and give the keys to the bank, who is then forced to liquidate it at a loss. that magnifies the downside potential.

during the last housing crisis the Fed was able to lower interest rates massively. but they have no room to lower rates now. and if inflation is spiking higher, they will have to sacrifice the home prices to keep inflation under control.

higher inflation will kill home prices, so you better hope there is not higher inflation.

There is also the affordability wall which we appear to have run into. It’s not likely that there will be a sufficient increase in wages to fix this problem particularly considering that wages aren’t rising enough to allow for inflation. Having RE prices continue to climb under these circumstances is highly unlikely and extremely dangerous for the entire system.

Then there is the assumption that interest rates wouldn’t climb from unprecedented historical lows for at least 2-3 years. The Feds are trapped. They can’ raise them due to debt levels, however, they can’t afford not to given rising inflation. Assuming that they wouldn’t rise for at least 2-3 yrs seems highly unlikely. Furthermore, many mortgage brokers are saying that they don’t need to rise to traditional levels. Anything more than a slight rise in rates and they are expecting a tsunami of defaults.

Additionally, while in certain states they are Non recourse mortgages that allow an owner to simply walk away, many states and ALL of Canada are recourse mortgages which means the owners are legally on the hook for any loses. Given the recent run up in prices creating clear overvaluations and the # of households that over leveraged and stretched, it’s reasonable to assume that it wouldn’t take much of a correction to wipe out many households capital, put them underwater and yet leave them on the hook for the original funds. That’s quite the risk and painful consequences for both the owners and the entire system if your “ifs” don’t pan out. At best it should be considered a high risk choice.

DC

He’s joined at the hip with Lawrence Yun of the NAR. Pedaling Bull s$it is their stock & trade.

SocalJim – Are you a realtor or invested in real estate? because that logic is not good. As we all know, the inflation rate is not necessarily reflecting home prices, it reflects rent equivalents. If inflation kicks up, then the Fed must allow interest rates and mortgage rates to move higher. Even if inflation is running high, home prices will melt down with higher interest rates because the rent equivalent is much lower and households simply cannot afford the higher monthly payment.

The real problem is that home buyers have not been intelligent enough to realize that they were vastly overpaying for homes due to low interest rates and when rates rise again, the demand for homes will be reset at a much lower home price. Add to that the fact that upside down home owners often turn into distressed homes that are sold at a discount and you will have alot of negative pressure on the real estate markets. Once the markets turn, investor money will also dry up rapidly.

The only thing that keeps real estate markets up is if the Fed continues to keep rates low and that only happens if they are willing to stoke massive inflation. The Fed will be forced to back off from low interest rates this year and that is the death knell for home prices.

Oh, and I have not thrown in the fact that remote work allows workers to move to less dense areas, which will actually reduce home prices because there are more opportunities to build a home where land is plentiful.

And with labor market participation at a low, once the free money from the government dries up, we will have higher unemployment and lower incomes.

All of this is a formula for higher home prices?

It is important to recognize the really big turning points and ride on the wave when it is moving in a direction. Sometimes those waves can last for decades, such as the constantly lower interest rates that have happened for decades. But that wave is now moving in the other direction, albeit, slowly.

If inflation is running hot, odds are your home price is increasing, even if interest rates are rising. Why? Because if inflation is running hot, odds are salaries are also rising, so they can afford the higher payment from higher interest rates.

Today is a unique situation. You can actually lock in a super low mtg rate because many speculate inflation is temporary. If it turns out inflation is permanent, then home prices will continue to rise, and you will be kicking yourself for not locking in that low fixed mtg rate.

You have absolutely no idea what you’re talking about. In times of high inflation, mortgage rates rocket up, and house prices crater because it’s about the monthly payment. Wake up.

@gametv,

#1 “inflation reflects rent equivalents.”

#2 “Even if inflation is running high, home prices will melt down with higher interest rates because the rent equivalent is much lower”

Can you explain the conflict here?

@gametv,

So if inflation is temporary ( 1y or 2y or whatever Fed believes), then RE price can cruise along? Hyper-inflation is possible but unlikely with over-capacity and de-leveraging in China.

I dropped by my credit union this morning and had a chance to speak to the manager for a few minutes.

She’s been there close to three decades and she’s been making Real Estate loans from the beginning.

I mentioned that I thought this Month would be the top for Real Estate prices and she replied “I think so too, and we know what comes next”

I’ll add that I looked at a property at the request of two friends, an Appraiser and a Broker looking for their final home.

A little less than 8 acres with several more or less level benches mostly hilly and about 60% meadow/40% trees and a seasonal creek.

A very nice piece of land with an 1100 Sq Ft 2/1 that had a nicely renovated kitchen and bathroom, a freshly painted exterior and a roof that looked recent.

Three parcels, the main parcel zoned AR 10 with two residences allowed

$950K asking.

The house has serious structural issues as well as flooding issues and more importantly it is not properly placed on the lot.

It’s nice this time of year, but it’s in a hole and it is going to be dark for months out of the year.

End of the road privacy and end of the road fire danger.

Someone will buy the shiny and an education.

Sounds like a $75,000 property.

Tom Stone,

I always wondered about that: why would you want to live in a 1,100sf house on a big property? 1,100sf is smaller than a decent classic 2BR apartment in San Francisco. 1,100 sf is really small for a house. OK, if the lot is small, but out in the sticks?

Okay, we are buying a larger house, but still it is a manufactured . I have crazy amounts of unharnessed energy so I just want to build trails and pull weeds, fix stuff, build stuff, and grow stuff. Some folks need wide open spaces more than a house or community.

Here are the features that I like:

1. low draw well all the water under the sun. For free

2. Propane – 3 years worth about 1,500 dollars

3. Septic.

4. Land acreage with coastal oaks ferns and vines. (think northern Cali on the central coast)

5. wildlife of all sorts.

6. Favorite part: Close to our favorite beach town near where my wife grew up.

7. kids get to have dogs and pets and explore all kinds of crazy wildlife.

8. I can’t list all but they are there.

Wife: she love the idea of living in the house until we build a permanent home somewhere on the property. The place we will be renting recently rented for about 3 grand – build and rent out.

Sounds great! Good luck!

As someone who does live like that.

1. It’s great if you spend a lot of time on your property, including decks, rather than in the house.

2. Goes well with a big barn/workshop. Mine is 2,500 sf

3. The combination means lower property taxes. If you go ask the county exactly how they assess property taxes (and I have), the small house / big barn approach is way cheaper.

4. Nothing in the barn counts as residential, avoiding many permits, inspections, etc. However, you can use barn space as a bunkie if your main groups of visitors come for summer holidays.

5. Much cheaper to heat the main house in winter/cool it in summer.

6. Often much lower purchase price on an old, small house on a big lot, because most people’s first reaction is the same as yours.

Tom’s points about major problems like flooding, structure, and fire risk are very important, and in my searching a majority of rural properties do have at least one and often several of these problems. So, you have to look carefully and thoroughly. My only problem is big snowdrifts occasionally in winter, but I can handle that.

Could you elaborate on the barn space…. what are the ins-and-outs?

I still believe it depends on what you are buying. There are two condos in town going for a little over 400. They are 2 bedroom near downtown 2 miles from one of the best colleges in CA. they are about 7 miles from the choicest beaches.

20% is 80 grand down 320 mortgage with a few hundred HOA at 3% APR more or less.

With a small dog or cat allowed they’d garner 3g per month.

That is a good investment. Better than gold, better than Tesla, better than bite-me-coin.

You are certainly correct about location mattering but if my map-guess is accurate, then I’m a little skeptical about a SmalLish twO bedroom pulling $3k/month as a long-term rental.

My sister and her husband are in the market to buy a home in the San Francisco area. They sold both their home and their farm in the Carolinas over the last two years and are hoping to catch the sweet spot of inventory, price, and interest rates.

I tell her to watch Wolfstreet.com for articles just like this one. If only Wolf were a Realtor…

Tell them to buy in Marin County, across the Golden Gate from San Francisco. Excellent to very good schools, clean, safe, cool breezes in summer, unpolluted, highly educated population, healthy recreation opportunities everywhere, varied neighborhoods, architecture, geography, right next to the city for whatever they might want there. Lots of progressive varnish on a very conservative family oriented place.

When the economic collapse inevitably comes, living in San Francisco or most of the east bay will equal crime and uncertainty.

Maximillian,

Economically, Marin is nothing without San Francisco. It’s a bedroom community of SF. If SF goes down the tubes, so will Marin.

Yeah, economically it will go down the tubes, but the rioting demographic is severely limited in Marin because of “demographics.”

1) The eviction moratorium was extended again until June 30.

2) Normally New Listing peak in June/July.

3) Millions owed an est $57B in back rent in Jan. Currently, there are about 10-12 millions renters who were somehow behind on rent, in mid Mar.

4) The current pool of qualified renters is trending down.

There are less qualified people and there will be more available homes and apartment for rent in the market

5) Eviction and repairs take time. The damage to landlords was done. Some liberal courts will rule against evictions. BLM will demand rent jubilee, or else. 2021 New Listings high will probably be in the third quarter. The upthrust, the largest number, in 2023/24.

6) RE recession are more painful than a stock market plunge.

7) The new stimulus will sooth the pain, if it pass.

Nice writing, hope they are not extending it further beyond June 30. We are looking to afford a home. Cant wait for ever.

I seem to recall that the housing market showing signs of struggle in 2019 before COVID gave it a magical boost. Well, I shouldn’t blame COVID.

What’s the current state of forbearance at this moment? It’s been forever.

“If the Fed be printing, you be sprinting.”

You be sprinting to buy quality real estate, S&P500 index, Gold, and other quality assets. Or, you’ll be sorry, if not already.

About all-cash offer:

“HomeLight, a real estate technology firm and lender, underwrites and approves the buyer, confirming they will be able to qualify for a loan. It has an in-house valuation team that evaluates the home they are seeking to buy. The company then makes an all-cash offer on the buyer’s behalf. If it’s accepted, the company buys it and can close in as few as eight days and holds the home and its title while the buyer secures traditional financing.

For buyers who use HomeLight as a lender, there is a fee of 1% of the purchase price for the service. If another lender is used, the fee is 3%. Currently, the program is only available in California and Texas, with the company saying it is working to expand to new markets across the country.”

https://www.cnn.com/2021/06/02/homes/all-cash-home-buyers-feseries/index.html

Wolf,

Assuming RE downturn will trigger another recession, with the current recession (doesn’t feel like one) is not done yet, how likely another recession can happen?

It took over two years for the last housing bust & mortgage crisis to trigger a recession. And that bust was a biggie.

Thus the Economic Kamalatastrophe will be in full flower in 2024.

Doesn’t look good for the party in power.

Slow down. You’re skipping a step. We’re still in the Trump recession that started in March 2020 and that Biden & Kamala inherited in Jan 2021. First we need to get out of this Trump recession before we’re ready to get into anything else.

We just went thru a pandemic and the housing market sky rocketed up. I’m not convinced they’ll let the housing market drop. Like nearly everything else now due to having low rates for too long, I think the housing market is too big to fail. The Fed is trapped.

They’ve opened the door to mortgage forbearance now so who’s today that’s not a new tool they’ll use in future recessions?

“I think the housing market is too big to fail.”

By my definition of ‘fail’ housing market is failing badly now right before our very lives.

When a market becomes over leveraged, distorted, highly speculative with liquid big time investors rushing in to pick the bones, and prices become unaffordable for average market buyers I would say it has failed big time.

Nearly time to stick a fork in it and call it done.

– Falling amount of mortgage applications = falling growth of mortgage debt = Recession.

(Source: Steve Keen)

1) Since 1967 the Suez canal was closed for a decade. // Since 1974 there

were two oil embargo.

2) Commodities jumped and RE slumped.

3) Union declare strikes and and got higher wages.

4) The 60’s/ 70’s inflation destroyed stocks and RE. To reverse wealth destruction ==> people saved. The saving rate in 1975 was : 17% !!

5) Last Apr saving rate was fake. The source was gov stimulus, not

wages.

6) Today the equivalent to the closure of the Suez canal and the oil embargo will be economic war with China. That didn’t happen even after the pandemic.

7) There are four types of deflation. One is bad : a real war !

8) A war with China will destroy our (both sides) mega population, mega armies, mega cities, mega infrastructure, mega industries, mega mega mega…

There’s no buyers on a strike, there’s only buyers who couldn’t offer high enough to buy.

In a conversation with my daughter, she told me tales of people who were working from home and, thinking that it would be a permanent change, moved away from the city center and into the cheap seats of the Bay Area.

Lo, and behold, the employer (who is located on Market St. in SFO city) put out a notice that WFH is being phased out and their butts are to be in their seats at the office per the schedule that was attached to the email.

Some of the people she spoke to are in a panic as they bought out there and the commute is going to kill them – especially as traffic increases as other organizations tighten up on WFH.

Anecdotal, yes. But this will be interesting to watch.

Yes, there is going to be a backlash. But companies have to watch out. They could lose a lot of good employees if they’re not “flexible.” Working from home has seriously caught on with lots of people.

This spring virtually all homes in my zip code have gone under contract within no more than a week after listing and the only reason it’s taken that long has been bidding wars which have taken the prices sometimes hundreds of thousands over list. That’s been the spring selling season.

Now we are seeing a few homes still on the market a week after being listed, and a few homes with big price reductions where the list price was over the top ambitious. Does this represent the early stages of things turning? I don’t know. I’ll be watching.

Data has been posted re local sales indicating that about 50% of recent sales closed over list. I thought this was interesting as I believe I once saw data that about 50% of Ebay auctions end with the “winner” paying more than the Buy It Now price. Auction Mentality at work.

It is impossible to keep a “boom” market going for any sustained period because eventually, the rising price of housing outpaces rising income.

The result is that at some point, the prices begin exceed what people can qualify to borrow. At that point purchasing slows but supply continues to expand. That is when boom turns to bust…

Just did a property in the heart of the Swamp where the owner illegally installed an accessory unit in his garage. This was not disclosed on the VA loan application and is an abuse of the whole VA loan program. This is going on all over the place. I wonder what the insurance company will say when one of the units has a fire and was not on the policy. This whole VA loan program is being abused left & right and is no longer fulfilling its original purpose.

But as long as the music keeps playin we”ll keep dancin, as Chuck Price once said.