But condo prices in the San Francisco Bay Area fell year-over-year again, and in New York City have been flat for years.

By Wolf Richter for WOLF STREET.

The national average doesn’t do justice to the craziness in specific housing markets, but it’s crazy enough: House prices soared by 13.2% from a year ago, the biggest increase since December 2005, on the eve before it all came unglued starting in 2006. The National Case-Shiller Home Price Index today is based on a three-month average of sales recorded in public records in January, February, and March. That’s the timing we’re looking at.

“House-price inflation.”

The Case-Shiller Index is based on the “sales pairs method,” comparing the sales price of a house in the current month to the price of the same house when it sold previously. Home improvements are taken into account. The index tracks the amount of dollars it takes to buy the same house over time. This makes the index a measure of house price inflation. And that’s what we’re looking at, not a miracle of some sort, but house price inflation.

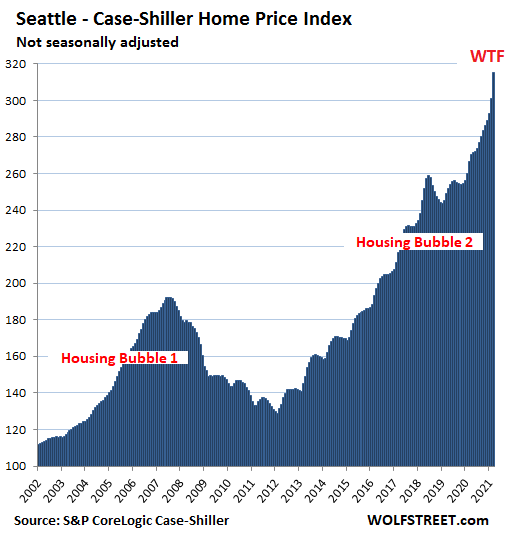

The March Queen of House Price Inflation: Seattle.

House prices in the Seattle metro spiked by 4.7% in March from February, the largest month-to-month spike of house price inflation in the data going back to 1990, after having spiked 2.8% in February from January, to create a new WTF moment. Year-over-year, the index has spiked by 18.3%, the third-hottest annual house price inflation on this list, after Phoenix (+20.0%) and San Diego (+19.1%). House prices have more than tripled (+215%) since January 2000:

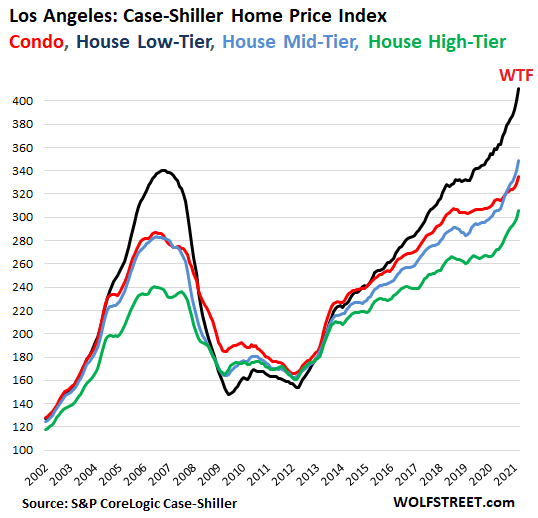

The long-term Queen of House Price Inflation: Los Angeles:

Prices of single-family houses in the Los Angeles metro jumped by 2.3% in March from February and by 13.4% year-over-year. The overall index value for Los Angeles of 333 indicates that house prices skyrocketed by 233% since January 2000, despite the collapse in the middle, which makes Los Angeles the most splendid housing bubble on this list.

There has been a big divergence in recent years, following the same formula during Housing Bubble 1 before it imploded:

- Low-tier house prices (black line) skyrocketed faster than the others and quintupled since January 2000, for another WTF moment. During Housing Bubble 1, they also collapsed the fastest and the most.

- High-tier house prices (green line) show slower price movements, up and down, though they too have spiked recently.

- Condo prices (red line) have risen “only” 6.6% year-over-year, less than half the rate of house prices:

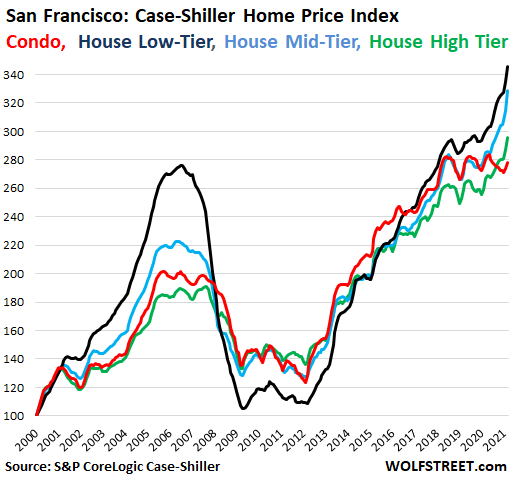

San Francisco Bay Area: everything surges but condos.

The Case-Shiller Index covers five of the Bay Area’s counties: San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay).

House prices spiked by 3.2% in March from February and by 12.2% year-over-year. They have more than tripled since 2000 (+207%).

- Low-tier and mid-tier house prices (black and blue lines in the chart below) spiked by over 15%.

- High-tier prices (green line) rose by 11.0%.

- But condo prices (red line) fell year-over-year and are below April 2018. And there is no shortage of condos for sale. Condo prices have gone nowhere for three years:

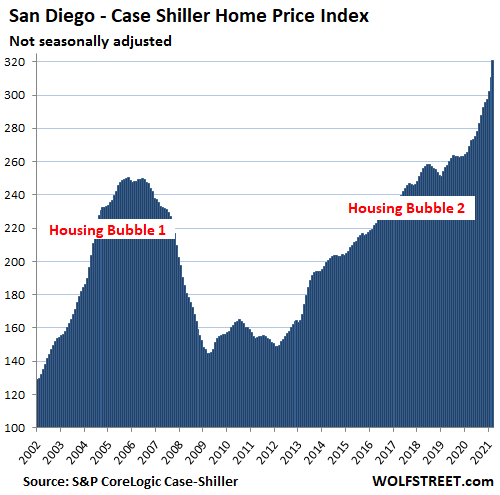

San Diego metro:

House prices spiked by 3.2% in March from February, by 19.1% year-over-year, the second-hottest annual house price inflation on today’s list of the Most Splendid Housing Bubbles, behind Phoenix. Prices have more than tripled (+220%) since 2000:

The charts below are on the same scale as San Diego to show the relative magnitude of house price inflation over the past two decades in each market.

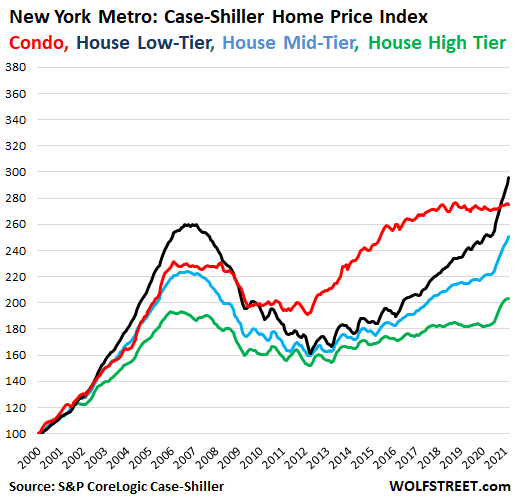

New York City metro: low-tier house prices spike, condos flat since 2017.

For the Case-Shiller Index, the vast and diverse New York City metro includes New York City plus numerous counties in the states of New York, New Jersey, and Connecticut.

House prices overall rose 0.6% in March from February and are up 12.3% year-over-year. But by price tiers, a massive divergence emerges:

- Low-tier house prices (black line) jumped 17.3% year-over-year.

- High-tier house prices (green line) spiked recently, after not moving all that much for nearly a decade, and have only recently risen above their 2006 peak.

- Condo prices (red line) ticked down for the month and are on the same level as in July 2017. Condos are concentrated in Manhattan and some other markets near Manhattan.

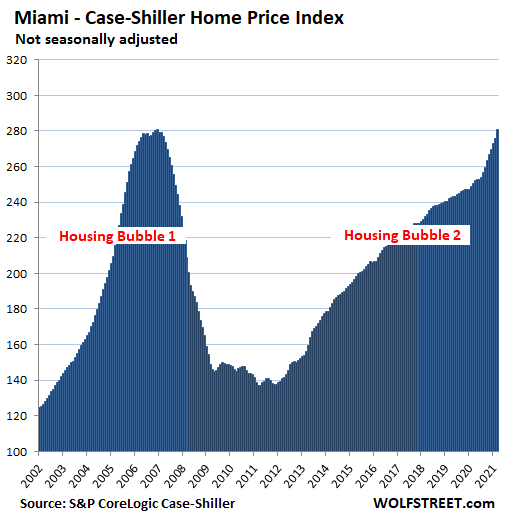

Miami metro:

House prices jumped 1.8% for the month and 12.2% year-over-year. They have nearly tripled (+181%) since 2000, and now match the crazy peak of Housing Bubble 1:

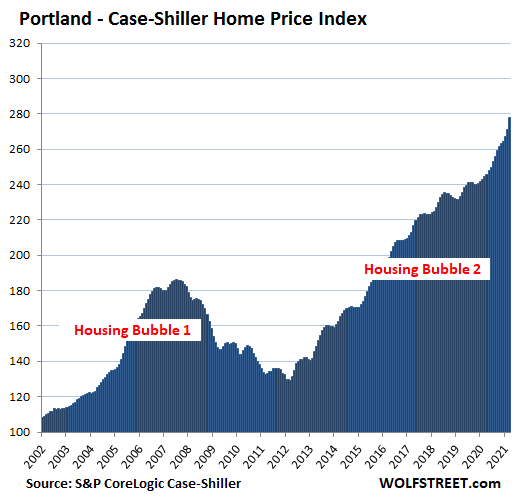

Portland metro:

House prices jumped 2.5% for the month and by 13.5% year-over-year:

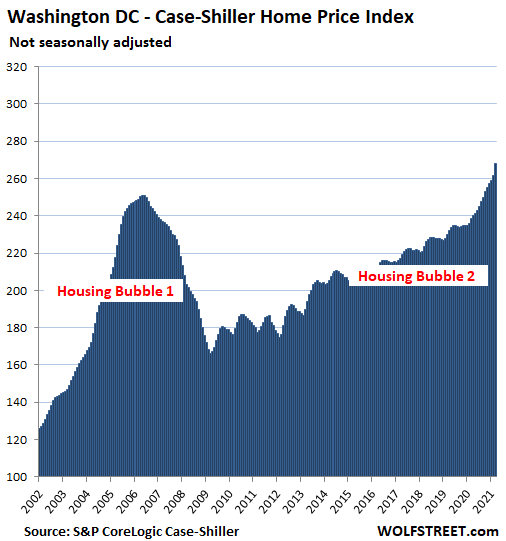

Washington D.C. metro:

House prices jumped 2.4% in March and by 12.2% year-over-year:

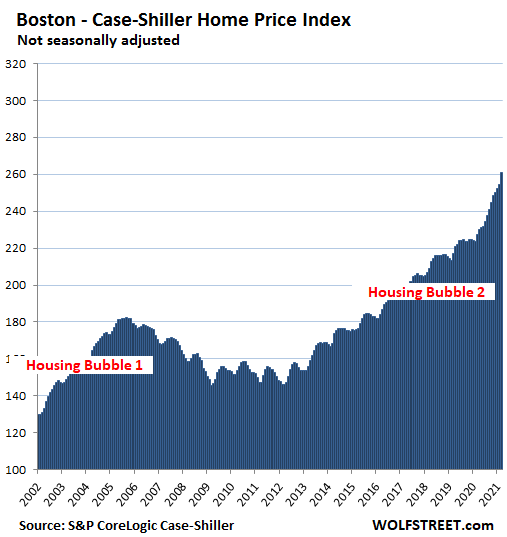

Boston metro:

House prices jumped 2.6% for the month and 14.9% year-over-year. Not shown in the chart here, but similar to New York City and San Francisco, condo prices haven’t budged much over the past eight month.

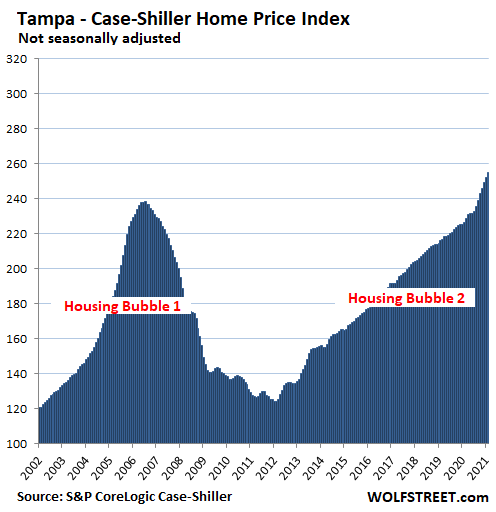

Tampa metro:

House prices rose 1.9% for the month and 13.7% year-over-year:

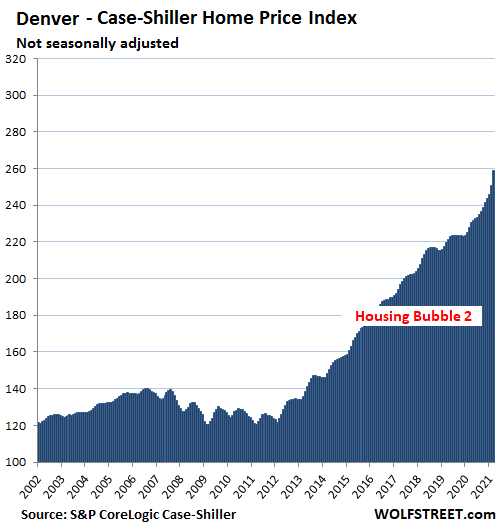

Denver metro:

House prices spiked 3.3% for the month and are up 13.4% year-over-year:

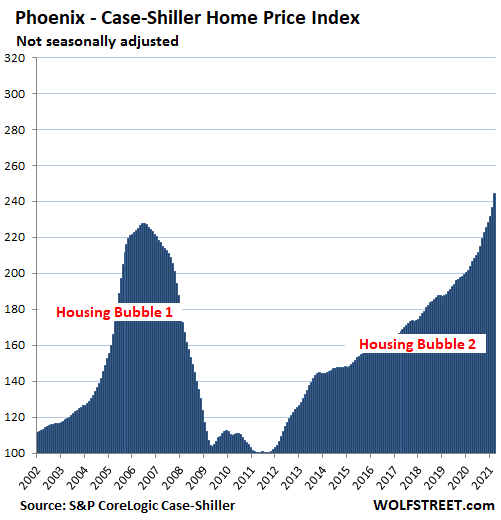

Phoenix metro:

House prices spiked 3.3% for the month and a holy-moly 20.0% year-over-year, the hottest annual house price inflation among the Most Splendid Housing Bubbles here, ahead of San Diego and Seattle:

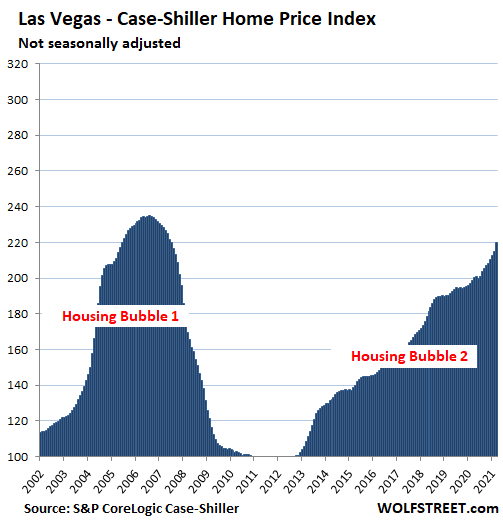

Las Vegas metro:

House prices jumped 2.3% for the month and 10.6% year-over-year:

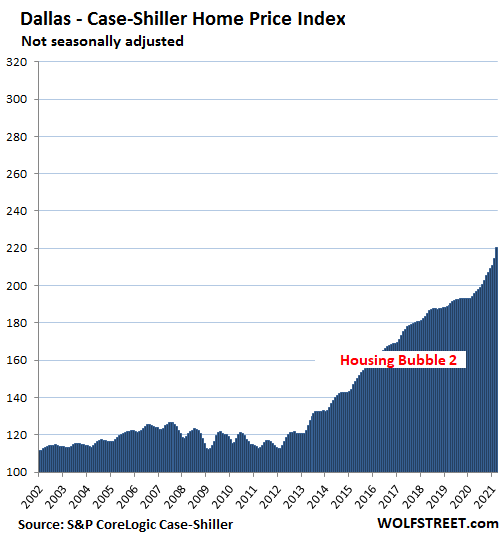

Dallas metro:

House prices jumped 1.7% for the month and 13.4% year-over-year. The index is up 120% since 2000. In the remaining cities in the 20-city Case-Shiller Index, the two-decade house price inflation is less than 120% — for example, Minneapolis is at 101% and Chicago at 56%. This makes Dallas the last entry on this list of the most Splendid House Price Inflation in America:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In a weird change of responses. The Fed instead of buying MBS after the GFC – they have been buying MBS during this, or inside the “bubble”?

Uncertain times we live in.

Great article as always Wolf.

In the minutes of its latest policy meeting, the central bank acknowledged that “if the economy continued to make rapid progress toward the Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.”

I count 6 qualifiers, including the last two: ‘begin’ and ‘discussing’. And even after all that timorous preamble to ‘adjusting the pace’, it doesn’t actually say in which direction. One assumes they mean tapering asset purchases, not increasing them, but perhaps the ‘T’ word cannot be spoken, or is now ‘inoperative’.

Just watched economist Steve Hanke on Kitco explaining how he came up with a sentiment dashboard for gold. It makes you realize how computers can be used to determine where markets are going in the short term in his case to read all news articles. Fed will have to say everything is ok until after the next crisis or rats will flee the ship in advance.

Probabilities .. type a bunch of facts into a computer & ask “What are the odds.” If you have reasonably reliable facts .. you have reliable odds.

Can we predict the future ??

Yes .. there is future based on the memory & churning of the facts of the conscious intelligence of the universe .. Physics holds that the universe never forgets therefore the most reliable source of probabilities is the memory of the universe .. all man needs is the intellectual capacity to tap into that memory bank.

Nikola Tesla said listen carefully

Look at those charts. The Fed’s primary job is price stability. A first grader could understand that the Fed is not doing its job. Either the mandate is phony or they have lost control.

Incorrect.

The Fed’s only job is increasing the wealth of it’s shareholders.

You forgot the method to achieve this, steal from everyone else in the country.

Wolf,

“House prices have more than tripled (+215%) since January 2000”

A useful stat…but unless similar charts for total employed, median household income, and Employed-to-population 25-54 ratio are placed nearby, it is difficult to appreciate the madness of that appreciation (approx 8%-10%+ per yr for 20 yrs during one of the worst 20 yrs in American labor mkt history? “Hanging by a thread” doesn’t do it justice…).

CPI has gone up 58% since Jan 2000.

Yeah, but that metric at that (cooked) level is viewed as benign.

Ditto one way of viewing housing inflation (as an asset for 65% of people vs. as expense for 35%).

The metrics I mentioned get at the public’s ability to truly afford homes (shorn of the Gvt’s zero interest rate games).

Having stagnant or vanishing incomes is not consistent with booming home prices…that is the main pt.

“as an asset for 65% of people vs. as expense for 35%”

The Share of Never Married Americans has reached a new high.

In the US marriages are more stable due to the steady decline of divorce since 1980’s.

In 2018 a record of 35% of Americans aged 25-50 .. or 39 million had never married.

Marriage rates tend to fall during a recession ..

Covid-19 stay at home order & the financial fallout from the pandemic & we are most likely to see never married numbers break new records.

ifstudies.org

Q. Who are the players in the housing market .. ??

A. Not many .. !!

In Australia I suspect .. perhaps a select few working the federal governments .. New Home Buyer Scheme .. to their advantage under false pretences even !!

PM Scott Morrison has offered almost total financial support for a third child .. go have a first child in this financial chaos .. let alone a third.

The BLS should publish CPI statistics with and without “hedonic quality adjustments” in the interest of fair disclosure. Let the consumers decide which inflation statistics are more applicable to their individual situations.

Yes, but earning your money in America doesn’t mean you have to live there, that income can still buy nice housing outside the US.

I decided five years ago expenses in America were too high and the living standard too low. I moved to Spain and I don’t regret it. I earn all of my income in the US but I spend and invest all of my money outside the US so I get something for my wages. My home purchase was very reasonable, I live in a beautiful area and the purchase gave me legal residency for life.

I understand most of you have houses already, but for those who don’t, you should not overlook greener pastures. As things stand now there are many greener pastures, find one that suites you.

Let Americans enjoy their enormous home equity but don’t be the one who fund their lifestyle. Spend your wages on you and vote with your feet.

What area of Spain do you live in?

Pontevedra (Galicia). It’s beautiful, the climate is amazing and I get around mostly by bike. It was a good fit for me, probably not for everyone but there is a place out there for almost everyone. An important consideration is to live and rent in a place before you buy to avoid making a mistake.

I have so many wonderful memories of the US but I realize the place I remember is gone now. As the saying goes, you can’t go home again, because home no longer exists.

MyLadyLumps, can I ask how old you are? I feel that I don’t recognize the America of my youth, and I’m only 38.

> I moved to Spain and I don’t regret it.

Brilliant! I stayed in the US so far, but I live and budget as Italians do. Very easy for me.

So killed housing costs completely by buying a REO and fixing it, leanFIRE is possible for me before 45. I’m not spending on healthcare being super healthy. If that changes, I just stop working and sign up for Medicaid. I pay for it with taxes, so why not use it?

The other key cost to kill was car: 2-year-old Honda Civic, nicer looking than all Teslas for a song: $12k cash. That’s how Italians live: they kill housing, car, and healthcare expenses and achieve a higher household net worth than Americans that way.

> Let Americans enjoy their enormous home equity but don’t be the one who fund their lifestyle. Spend your wages on you and vote with your feet.

EXACTLY!!! The last thing I would do with my time would be to fund the healthcare issues of NIMBYs that turn decent areas into HCOL ones. I turned the tables on them so that they pay for my healthcare instead if the need arises.

Not wasting $ on US healthcare is how I compensate for artificially inflated housing costs.

Do you have healthcare? Never in my life did I think I’d want to leave the US, but what Weimar Boy Powell and Co. are doing is something I cannot live with anymore. I’m looking to retire elsewhere.

“Do you have healthcare?”

That’s a question you should someone living in the US, not Spain.

America has the undisputed worst healthcare SYSTEM in the world.

Pro Democracy movements are all over the globe. Places like Myanmar and Belarus will good places to live in ten years.

We are currently looking for a place in France. Health care costs roughly $1500/yr per person for foreigners, and the actual costs are a tiny fraction of US costs. I’m hoping we can make the transition before something here snaps.

If you want to see house price levels on a relative level, I can recommend calculatedrisk’s charts with CPI adjusted prices and price to rent ratios. Those show that we are again in 2005-2006 territory. It will be interesting to see if it will crash in the next 2 years like back then. That would require big rate hikes like back then. But it’s also possible that this time is a little different and nominal prices fall less. Instead CPI could pick up a lot to get ratios back into historical norm. This stagflation scenario looks more likely to me as this is what the FED prefers and has already signaled with inflation being ‘transitory’ and just pandemic supply chain related. Using these excuses they can probably keep the CPI smoke and mirrors up for a couple of year.

Same in New Zealand. House prices are in “WTF” territory.

Same in Sweden. My apartment in central Stockholm is up 1000% (yes, a thousand percent) since I bought it in 1993.

Housing is going the way of stocks: Time in the market is more important than timing the market.

Magnificent bubbles. History in the making before our eyes.

I predict tears, soon, in some of them. Especially those of the FOMO types.

Doubtful. Banks books are solid. No shadow inventory lurking unless all the hedge funds unloaded at once, which would be stupid. Harder than ever to get a loan. This might be inflationary rises in pricing but the supply and demand economics of this market are evident. In the USA we only completed 5.8 million homes 2009-2019. Almost 1/3 the necessary amount needed to keep up with population growth.

No shadow inventory? Pffft. I see houses that have been vacant over 10 years since the last bust.

Ok got it, so good time to buy then and this is not a bubble in way shape whatsoever..loving this new normal for sure

The pro-housing contingent (and they are legion) are firmly entrenched in recency bias and readily overlook historic cycles and trends. As usual, this time is always different for these believers.

Actually this gives me a bit of hope. Denver, Phoenix, and Vegas all collapsed incredibly or had little interest after the cycle but places like DC and Boston never dipped super hard and maintained solidly. Probably because those are places with actual bustle and meat to them. Denver sucks, Phoenix is 11 billion degrees with bad traffic that has swollen beyond what the infrastructure can handle and Vegas sucks to live in. Seems like the trendy hot spots eat it the hardest in the crashes.

I hope that is the case for North Idaho/Spokane. I saw a nice property today. A metal warehouse type deal that is half living space half garage clearly built for a man as the interior was about as lifeless and cheap as you could imagine but nice for a guy like me. 5 acres and a fortnight from civilization by most standards but with power and a well. In 2015 it appraised for 73000. It was listed yesterday for 350000. And just like that it is pending sale.

And I suppose I understand it to a degree. That would be the ideal set up for myself and I’d even be will to go in 200000 on it with rock bottom interest rates and that is pretty overpriced for what would cost 70-80 to build tops and near worthless polluted mountain land in the backwoods of snow country 10 miles from a paved and maintained road. But I don’t have all cash and I’m not getting into bidding wars or paying above sticker price for anything.

Either way hopefully the trendy area of North Idaho will have interest evaporate and the bottom will fall out and I can swoop in like a hawk. I know Boise is the hot button place to be if you’re fleeing California and you’re house poor, but I suspect that place will get a swift kick in the teeth if the burst comes. Boise sucks and is in the part of Idaho that also sucks.

Scratch that, they pulled the listing and relisted for 425000 from 350000 for yesterday morning. Wish I knew how to make 75000 dollars in less than a day.

My own private Idaho would be nice.

B-52s R A W K !

“Boise sucks and is in the part of Idaho that also sucks.”

Actually Boise is kinda quaint and civilized. They have a Trader Joes and Whole Foods, which is what I assume is drawing in all the Californians.

You can get your unwanted Cali population to flee within 3 months if you close down those two stores. It’s really that easy.

While your Cali-prevention methods may be legit, what Boise really needs is a way to get rid of Blackrock & Friends.

It’s hilarious that San Diego has three Whole Foods stores while Dallas-Fort Worth has like 13. It was all BBQ when I moved to TX but now it’s like freaking San Francisco when it comes to health food stores. My parents can’t get Whole Foods delivered in SD because the store’s too far and here I am in a small town in Texas where there’s cattle across the street from city hall and I get my Whole Foods delivered just fine.

It’s mega LOL.

Most people in Texas prefer the BBQ over Whole Foods (aka, WholePaycheck.)

See my post below about why Phoenix prices may not drop this time. Also, “billion degrees” it is not. 100F here, with humidity of 3% (which is common in May and June) is like mid 70s in the coastal area. Do not let “accuweather” and such fool you with their ‘real feel’. Real feel is what you feel on the ground, and nothing else.

Although, to be fair, the heat in summer (june to some extent, because it is super dry, and july and august mostly) is something you have to get used to. When temps hit 115F, it’s something no one can prepare for, if you’ve never experienced it. It is otherwordly, just like the plants here that seem to enjoy it.

However, after a while, a “wall of heat” just goes by. Surely better than bitter cold. You don’t have to shovel sunshine…

Yes, things are overvalued, but many people (including perhaps Wolf?) have been saying that since 2014. Well, prices have gone up 55% since then (in LA anyway). One day, of course, the bubble WILL pop and all the bears will be right, but when it does, how much will it drop and to what year will the prices reset? They’re unlikely to drop 55%. People paid with real money. There’s no jingle mail this time. You can lose by betting, but you can also lose by being a Permabear.

At today’s interest rates, if you’re going to stay in your house for long enough, you will probably do fine even if you are paying too much.

And what else is there to put your money in? Stocks? Bonds? Dogecoin? Bank account at .0003% with inflation looming? Out of all of these, housing is probably the best of the worst.

Seriously, what DO you do with your money?

The Fed should have let this bubble pop a long time ago when it was manageable. Instead they have prevented the rock star from detoxing and now we are in for the mother of all detoxes if they allow it, but I don’t think they will. They’ll just extend and pretend and since we are still the world’s reserve currency everyone gets paid back in our fake, worthless dollars. We are not Wiemar republic Germany who had to pay war reparations in foreign currency.

“saying that since 2014”

And 5 of the 6 chambers are empty in Russian Roulette.

May the Odds Be Forever in Your Favor.

The Fed wont be able to stop it this time because they simply cannot deal with the 3 headed monster to come. US Treasury rates cannot stay down because there is not enough demand for US Treasuries to finance the deficit. Wolf showed us that they have been using previously borrowed money at the Treasury to finance the debt until June, when they are forced to borrow from markets and there will be few buyers of Treasuries, so the prices will spike higher. The Fed cant go in and buy all this crap up, with the dollar dropping and prices spiking.

The Fed is caged now by inflationary forces an an obvious bubble, so they need to allow interest rates to spike higher, which is good for cooling the housing market and also good for bank profitability.

As this bubble starts to burst it is going to get ugly. Bonds, stocks and real estate collapsing in short order, with unemployment skyrocketing and massive stagflation occurring. The American public that has been binging on free money will get a rude awakening.

I see this starting as a typical correction/bear market, but then the bear will get worse and worse as time goes by.

Gold and silver.

The opportunity of a lifetime is in front of you, but you have to open your eyes to see it. This may be the best investment climate you’ll every find as a prudent investor. One simple look at the S&P 500 chart tells you everything you need to know.

Mark

I agree. If you bought in 2014 and you’re up 60% and RE drops 50% in the next 3 years and your loan is 3% – you have still gained.

If you buy today and it drops 50% in the next 3 years and you either have a tenant paying your 3% mortgage or you are living there yourself – what have you lost? You’ve lost nothing – and you might even be making positive cashflow if you have a tenant.

I sold all my rentals last year and I am carrying the loans on them, so I don’t have an “equity appreciation” dog in the fight. If the market crashes and my borrowers jingle mail, I own rentals (cashflow) again.

RE is not a zero sum game – it has nice tax advantages with the current rules in place, and when it crashes, the value is meaningless if you can cover your nut (with rentals).

Most Buyers are using high leverage, especially at the lower tiers. Its an inverse relationship: lower tier = more leverage, higher tier = less leverage. The more leveraged, the greater the tendency to focus on the affordability of the payments, and less on the price. Given the decline in rates, availability of interest-only loans, and increase in dual income households, it would be interesting to see the data for housing payments undertaken as a percentage of household income over the same period.

Like I continue to say, it is one thing to buy something on credit, but it is another all together to pay for it.

That’s the thing – all of these people with FOMO, signing up for big loans, then have to pay that money back. It’s not happenin’. All one has to do is look to the past to see the future. People are borrowing mountains of money they’ll never dream of paying back.

The Fed will inflate the debt away!

Exactly, who takes possession of all these assets that can’t be paid off. The central bank … “you will own nothing and you will be happy” …. get it?

Above is a very sobering WS article on results to-date of housing bubblenomics redux. It is deja vu, recalling 2008 (not subprime this time around, but a whole set of different circumstances).

If you look around there are serious potential headwinds to deflate much of the ponzi exuberance and animal spirits we see (both greed and fear are so evident right now).

And now it seems a cagey player in former subprime debacle is back and ready to bet against housing again. Back in mid-2000s Dave Burt convinced his investors to short subprime era MBS and they made billions off the trade (remember book and movie ‘The Big Short’?).

He is ready to short mortgage bonds again and this time for climate change and pandemic-response risks

His analysis shows that climate change factors (no, not Greta’s fears of earth burning to a crisp) of increased floods, fires, and winds will cause increased property insurance costs and losses. Also in the that mix are future higher taxes and foreclosure/delinquency risks (pandemic forbearance outcomes causing devaluations).

These risks/losses will increase costs of owning a home, and when that happens housing values will go down. His estimate is that about 1/3 of homeowners are at risk from such big losses.

That means rents will go up, too. And people will pay it. Being homeless is not an option for the vast majority of people.

Rents may go up but people have a limit to what they can pay. This fact seems to be lost on most real estate investors. I can tell you, from my own experience, that landlords will not get any rent they ask for.

Here is how it will go based on the average requirement that renters earn 3x the rent. First renters with income and good credit get chosen first, then renters with income and bad credit get chosen second, and then some get chosen at whatever they can afford, and the rest move to other rental markets. At each level renters pay less and less and eventually fall off the scale in the location.

Take a good look at NYC and SF if you think it won’t happen in your market. Rentals will become a Dutch auction where landlords fill units at lower and lower rents.

Petunia

You are correct in your analysis of the rental market. I would add in your 3rd & 4th category that government will step in and play a larger role (Section 8 on steroids or something) in coming years as incomes cannot meet market rental rates. It has already started when govt banned evictions but then realized that not all landlords are Blackrock. As such, they now have “temporary” rental assistance programs to try to fix their initial failed initiative. My bet is these programs will become permanent as political mantras will be “housing is a right” combined with “we can’t make Mom n Pop landlords homeless.”

Bear,

I do agree that the govt will have to step in to support the housing market for low income people. I have seen it coming since 2008 and expected it to lead to some form of rent control. Now I think rent control won’t be enough to stabilize the issue.

In Germany there have been demonstrations where renters are advocating for confiscation of properties from landlords. The dislocation of people from homes will come to a head and it will be everywhere and ugly.

Good comment Pet and BD,,,

Been there, done that,,, on both sides of what you have made clear:

”Back in the day ”squatting” in a ”flat” and then,,, much later, several decades, having some folks ”squat” in a house owned with the bank who would do nothing at all to help get them out.

Going to be very very interesting to see how this obviously unique, so far in her and history situation of ”fore bear ances” and moratoria play out in the next few years.

Very glad to have gotten rid of all rental property, in spite of the very good ”cash flow” and triple net,,, mostly glad because of the triple head aches due to folks who have NO idea what the papers they sign mean, etc., etc.

It won’t take anything exotic.

Mortgage rates going to 5% from 3.5% might be enough. (This in a country that thrived with 8% to 9% rates in the 80’s and 90’s, when Gvt debt – and thereby effective default risk – was a small fraction of today.)

And when capital holders get disgusted enough and shift away from 20 yrs of dollar debasement, rates/Fed inflation will have to rise,

Do you have a plausible mechanism by which they would rise even that much in the near future, with so much active intervention to suppress rates?

I’ve asked similar questions many times, but never got an answer.

Kevin Paffrath recently suggested that higher than expected inflation, if it occurs (which he doesn’t think is likely), could cause interest rates to spike and real estate to crash. I made the same comment.

It seems to me that it just boils down to morality: It’s so unfair that the government can spend money so recklessly, yet the credit risk goes down rather than up. There’s a desire to see the government punished the same way you or I would be punished for borrowing too much money: with higher interest rates due to the higher risk of default.

I’m convinced that the right way to express one’s anger is not to short treasuries like Michael Burry is doing, but to make a leveraged bet against him by going long the 30 year treasury bond.

That is exactly why I stepped down 6 years ago to a relatively small 650sqft home that I can maintain myself. I think homeowners are going to get kicked in the teeth before long due to the environmental collapse you describe above.

The worst financial decision of my life was selling my home in a trendy Seattle neighborhood 6 years ago. I went sailing for a year in the carib instead…

We bought a small townhouse for retirement. Much smaller than the house on the cul de sac lot we had. We have the amenities we want for a low fee and no daily work on our part. The big expenses are covered with a large HOA reserve account.

After 11 yrs we are still happy with our decision.

We aren’t moving – ever. Whoever is left in very old age can sell to cover assisted living.

I’m glad that you are satisfied with your situation. However, I see nothing good in you spending your entire life building assets, that over time, get depleted by the money cult and the healthcare industry, as if by right. It’s really a disgusting commentary on our society.

Sorry, but it’s not OK for you to die broke after a lifetime of work. Going along with it, is why they get away with it.

Gotta DIS agree with Pet on this one:

BEST deal of all is to slide sideways into the grave, or now a days the place they do the burner part to consider thereafter only the ashes,,,

with many many ”scars” from trying too hard, or too ambitiously, or trying to abscond or ridicule the so called Laws of Physics,,, etc., etc.

If you don’t have any scars, you likely have not taken any ”real” chances,, and similarly, are likely just a donut or some other kind of politically correct ”NUT” of the worst kind,,

And,,, IMH and very well considered opinion, the best thing for anyone without any scars, SO FAR,,, is just bend over and accept what is coming from the oligarchy,,, or whatever you want to call our current ”owners of the world”

( Clearly not much different than a 1000 years ago, except for some of the names, etc. )

VAST improvement in the fact that “”THEY”” no longer can rape our brides on our wedding night, EH???

There is a lot of luck in how one does in housing and financial markets, but over a very long period the person who manages risk and reward well usually ends up in a satisfactory situation. Being too risk adverse ensures you are not reaping the rewards of the economic system and taking excessive risk means you probably will get wiped out eventually. I like the basics 1) make sure you have adequate cash 2) don’t use margin to buy stocks 3) don’t short 4) don’t buy too much house

The big short only works when you have a functioning market in a functioning world where there are functioning FED officials who are willing to back stop the whole thing with printed cash. Betting against climate change i.e. shorting nature is just really really stupid. When nature informs us that many of our towns and cities are no longer inhabitable because we have put too much C02 into the atmosphere, then getting the FED to call nature on the red phone is not an option.

Man oh man.

When will people learn that we are all in this together. Everything is viewed as a money making oportuninty even the end of the world.

“When nature informs us that many of our towns and cities are no longer inhabitable because we have put too much C02 …”

It is not man-made CO2 that is going to wreak considerable havoc on human activities. There is undeniable climate change in motion but has nothing to do with human-caused global warming.

The real cause is solar cycles that ebb and flow through the ages and right now earth is going through such a difficult period. There is actual science and research to support that premise– not silly junk ‘settled’ science that is behind beliefs in global warming, green deals, and carbon tax ideas.

“The real cause is solar cycles that ebb and flow through the ages and right now earth is going through such a difficult period…”

No, wrong.

Don’t you think that the extremely large numbers of scientists who are looking at the data would have noticed? Or do you have some magical source of information that is not available to the rest of humanity?

Not sure if that is true. As of three years ago according to Buffet there had been no increase in policy claims due to weather related events. However insurance rates may be going up because of Zirp policy. Insurers count on being able to get a return on the “float” while waiting to pay out the money.

No condo data for Seattle? Based upon a recent uptick in my Zillow feeds, there are tons of ugly and over-priced condos and townhomes on the market in the pro-crime Emerald City. And when did we cease calling these tenement housing?

Western WA state offers very poor bang-for-the-buck relative to other areas in the USA, and so if you dont have to live there for your job, and do not prefer to breathe wildfire smoke during the summer, or be subject to a recently legislated 7% state capital gains tax, there are greener pastures elsewhere.

Case Shiller doesn’t offer condo data for Seattle.

The WA capital gains tax has no teeth. The WA state capital gains tax exempts all RE, as well as any gains less than $250k. Even if you have big stock market gains, you can entirely avoid the tax by staggering them over time.

The only people paying this tax will be people with passive income so high they surpass the $250k gain limit each and every year. I think that’s the top .5%.

Consider that having a few million in the equities and bonds does not put one in the top 0.5%. $4 million (top 2-3% depending on the source) at an average of 8%/year gains over time. Now you want to relocate your investments, selling some and buying others – WHACK! You should now have to time this out over several years to fly under the $250,000 capital gains limit radar? Plenty of greener pastures elsewhere with better leadership, as well as natural beauty.

I forgot where Wolf posted data on Adjustable rate mortgages. If this next bubble were to pop, what would the fed have to set that rate to?

The main mechanics for 2008 bubble were

1. low interest rates

2. giving relatively unqualified people loans (majority adjustable rate)

3. property value sky rocketing (people willing to buy at insane prices)

4. Fed increasing interest rate ever so slightly (unsure on the exact numbers)

5. Adjustable rate goes up, people can’t afford their payment

6. Mass sell-off

In terms of present parallels were are at number 3.

My question is, at what point does the interest rate go up to cause this repeat? What catalyst must occur for that rate to go up. Essentially the fed raises that because it thinks the economy can handle it. By not they signal it cannot handle it…ever?

Thanks for the comments Wolf community!

I don’t think we’ll see real estate in the US decline again on a nationwide basis. From 1945 to 2008, real estate prices never declined on a nationwide basis, as Bernanke famously proclaimed. Expect the next housing crash to occur in about another 50 years. I’ve mentioned before that I think real estate is the new cash in an era where people no longer want to hold cash because cash is trash, and RightNYer found this laughable. But I’m serious, if you sell your house watcha gonna do with the money? The trend towards greater income inequality is still ongoing, so if homes become unaffordable to buy, you’ll just have to rent it from Amazon. Homeownership is around 51% in Germany and we can get there, too.

The only way I see real estate crashing is if we have a financial reset of a magnitude that is 10 times greater than the GFC. Something like a currency reset. Who knows. But what I think I do know is what triggers this reset. The only thing that can trigger a major crisis is a major shift in the willingness to work. The logical reason to stop working is to boycott the wealth inequality, but we’re very far away from such a boycott. Florida just became the 23rd state to announce an early end to the $300 unemployment bonus. The pendulum is swinging the wrong way at the moment. Watch the 30 year yield drop back below 1% over the next 3-5 years tops. If we wait for a crisis and market crash, we may wait forever. The way to make money is to buy 30 year treasuries using leverage. Or maybe I’ll go broke doing this and then RightNYer will have the last laugh.

I agree with you that the Fed has created a situation where no one wants to hold cash. But that’s fair different from saying that the status quoa can continue for 30 years. There’s a huge segment of the population that would rather collect unemployment than work. But there’s a much larger segment, one with a lot more political power and more training, that will revolt if their labor can no longer buy anything.

There’s not a chance that 60-70% of America is prevented from ever owning a home and just sits down and takes it.

Americans will quite literally fight and die for the rights of their overlords to exploit them. Muh freedom!

Orthodox Investor

I would go with Michaels Burry’s bet that interest rates will go up and long term bonds will crash. To buy 30 year bonds with leverage is like going to the racetrack and betting on a 50 to one long shot horse. I don’t gamble with my life savings.

Wish you luck with that bet.

Anyone looking at those charts should understand two things:

1. Housing since the tech bust is now a very volatile asset.

2. Trend of price increases accelerated during Covid.

“I don’t think we’ll see real estate in the US decline again on a nationwide basis. From 1945 to 2008, real estate prices never declined on a nationwide basis …”

I wouldn’t be so sure about that.

Historically, real estate markets have been cyclical, with highs and lows.

I might add that it was Bernanke who infamously stated in 2007 that subprime mess was ‘contained’– just before the housing collapse and and Financial Crisis in 2008-09.

The other difference is that from 1945-2008, the U.S. economy was growing. It makes sense that housing prices will increase as the population doubles, along with massive economic growth.

Since 2008, we’ve had very little growth. Just printing, debt, and trade deficits.

Wolf, curious why you omit Santa Clara county when you offer housing facts. Not as glamerous as the northern counties but it is where everyone that cannot afod the north end up and the moves there are crazy of lat

I’ve lived in Santa Clara County most of my life (with a little spurt of Santa Cruz county here and there). It is absolutely insane what has happened here. People fleeing to the south: Gilroy, Morgan Hill etc(and homes there are now just as expensive as San Jose, if not more), and now Watsonville is posting very basic, unatractive single family homes for upwards of $700,000. That may seem like a bargain in the bay area, but understand, it is NOT the bay area, it’s a long, long drive from any Tech job, and it’s historically been a very poor, one horse town to live in. With quite a bit of crime and gang violence fueled by neighboring Salinas.

Neither I nor myself nor moi “omitted” Santa Clara. This is the “20-city” Case-Shiller Index. It’s coverage of the Bay Area is the 5 counties I named. The other four counties are not covered, including Santa Clara. The index famously doesn’t cover the Houston metro either, the 5th largest metro in the US, and that’s a whole story of its own.

I wish someone expanded the CS to the top 50 metros in the US. But that hasn’t happened and won’t happen.

Google has this thing called “Google Trends” where you can search a word and it will show you the interest history of that topic. If you enter “Inflation”, you will see two weeks ago was the highest ever interest in that topic. That was when the inflation data was released. It has since abated. The next data will come on June 10. It will be interesting to see how that trend will turn out in the next few months.

Amazing to think that there are people out there who have to Google “inflation.” But that’s the times we live in.

Wolf,

Good point, and IMHO, the reason folks have to research inflation on the internet is because people, including this old guy, frequently pay no attention to their receipts, if they bother to get one in the first place.

OTOH, some people, including some close to me, ogle every receipt twice, cross file them against the outrageous delta(s) now growing for every item, and go on and on and on about every extra dime…

One friend and her sister have a competition to see who can find the most thrifty clothes, furniture, etc., at the thrifty stores, and buy same for all in the family when they do find the true bargains that are still out there and possibly increasing as people downsize their housing, etc.

Wolf,

An ignorant populace is a politicians best friend. (I kinda stole that from the old SYMS ad campaign). Seriously though, we are not all impacted by inflation the same way. If your not in the market for a home, current prices don’t hurt you and if you own and are not remodeling, lumber doesn’t matter. Gas prices, still not driving much and a dozen grade A large eggs stuck at $1.79. Inflation is there but not impacting me all that much.

Dave Rosenberg was just on the Macrovoices podcast. He makes a pretty compelling argument that inflation is transitory. Gundlach disagrees. A few months ago, Cathie Wood said their will be around $500 in treasury issuance that will need to be absorbed outside the fed so that should be interesting.

Egg prices where I shop are in long term decline. Right now they are 68¢ per dozen. Hard to believe you can convert corn to an egg at that price.

There was a good article by the seasoned economist Stephen Roach. I always found him credible.

He told of being a young guy at the Fed getting mistreated by Author Burns. He kept denying inflation and kept insisting that they drop categories from the inflation bucket. He was the guy that started core PCI. I believe he said when he was though only 38% of the inflation index was left.

Anyway, said A. Burns denied inflation until it was too late. He is concerned Fed is making same mistake.

Charts look like Tesla stock. But like the mountain climber it just kept going UP! Split and kept defying gravity. Rate increase is going to limit the ability to support these values

$300k @ 3% = $1,264

$300k @ 6% = $1,798

When rates go up the affordability is going to cause a reckoning

Six percent is an unthinkable rate today.

True to an extent…but even the fact that more and more people are getting to learn how home price dynamics work and learning to ask questions…means that the ranks of sucker buyers will thin.

Not seeing much evidence of that, outside the comments sections of blogs like this one.

Sooner or later, savers/capital holders will get terminally sick of the interest rate suppression/Fed led inflation of the USD.

(The widespread interest in crypto is, at bottom, a reflection of post 2000 disgust with the untrustworthiness of the USD).

And there are over 100 other fiat currencies.

And dozen of commodities.

All of which may be better stores of value.

And every alternate store of value draws capital away from the dollar…triggering a rise in rates or requiring the Fed to step into failed auctions with printed money.

But, by all means, they should keep on courting economic ruin (capital flight away from dollar) in order to cover up policy failures and thereby preserve their worthless careers.

I was with you all the way up to “triggering a rise in rates.”

Pea Sea,

When savers/lenders get sufficiently sick of being paid just 1% to 4% to lend to risky borrowers in USD…they will go on strike and shift that capital away from USD invts to something/anything with more return and less risk.

The hunt for that something has grown more energetic by the yr.

Boy how times change.

The LOWEST mortgage rate I ever had was 61/4 % (refied down from 8%) around 10 years ago. The HIGHEST was 18 1/4 % in California when we moved there in 1981. (yes, that’s EIGHTEEN and One Quarter)

No mortgage now and never going to have another.

mortage rates in Europe at 1% and below. My mortgae is now 0,75%

This may look like the top of every Boom to Bust cycle in California History, But THIS TIME IT”S DIFFERENT!

Ask SoCal Jim if you don’t believe me…

if you can’t trust a Realtor, who can you trust?

More seriously, you can find SFR in places like Lake County that genuinely cash flow.

Not many, but they are there.

In most places if you bought now you’d be likely to break even in nominal dollars eventually.

Likely, not certain and it could take a decade.

You can’t dismiss the wildfire threat in Lake County and others like Shasta, Butte, etc. Better pay cash to avoid the staggering insurance premiums. An old High School buddy burned out of both Paradise and Lake Port.

> Better pay cash to avoid the staggering insurance premiums.

I’m paying GEICO under $1k to insure my home, if it gets destroyed I receive 1.5 times what I paid for it to rebuild.

I would call that a good deal, not staggering.

Do a piece about NZ property prices.

The real bidding wars starts after the bidding deadline. The max bid becomes the new base for the cash bids. First time buyers with conventional loans got no skin in this game…but, they sure can shill it up. What they got to loose..they’re never going to win anyways.

Redfin CEO just did a long Twitter thread on current market. A c&p of one of his tweets:

“But in two of America’s largest cities, inventory has increased, in New York by 28%, in San Francisco by 77%. San Francisco hasn’t had an inventory increase this large since 2008. And still in both markets, prices are increasing.”

So, inventory increases & prices not reflecting increased supply? Speculation is a powerful drug. Too bad we let it ruin housing.

GirlInOC,

I stopped citing the Redfin data because it doesn’t distinguish between condos and houses.

The below is based on MLS median price data, not Case-Shiller, because the CS doesn’t cover the city of San Francisco and Manhattan by themselves.

In the City of San Francisco, condo prices are down around 10% yoy, and in Manhattan they’re down too. There is a condo glut in SF and Manhattan.

In SF, the condo glut is historic. The condo market is larger than the single-family house market in SF. So this is what you’re seeing in SF: condos (larger part of the market): lots of supply and falling prices; houses (smaller part of market): tight supply and rising prices.

I bought repos in SoCal in 2008, been collecting rent ever since without missing a months payment. I have one in escrow now and the return on investment exceeds 500%, not including all the rent I collected. Mind you, I bought these SFR’s below $100K and am selling them in the mid 6 figures. I will sell the remainder of my rentals before August, sit back and wait for the next crash before I jump back in. I don’t understand why so many on this site are sour on RE, if you buy low, rent them and sell high, you cannot beat this type of investment.

I can tell you one reason, it’s that in 2008 I was 20, broke and had no cash for buying anything. I’ve fought hard to pull myself out of low income despite being literally less educated then the average felon. As much as I learned to make more and save more housing just quickly soared right past what I was able to afford. Now, here I am watching the biggest bubble and tranfser of wealth in history. I’m sitting on cash that I have no idea what to do with, as I am just old to remember how so many I knew back in 08-09′ lost nearly everything. I know that markets cycle and I have no desire to be a rube to dogecoin or to try and play in this massively inflated real estate market. The real problem that no one wants to talk about I when it comes to this whole mess is that people are no afraid. We know our leaders have lost the ability to affect stable markets, price stability, and dependable currency. It’s disgusting that we don’t trust our dollar. That’s what all the alt coins and cryptos are really about. Americans have lost faith in the thing that we fought a war to produce. Makes me sad and sick. I can’t trust Jay Pow, Janet Felon etc, every time I turn around they’re printing more money, buying more MBS and destroying what I’ve worked so hard to save.

In 2008 every single one of my friends that were ready to buy were outbid by investors. The “easy investment” game that is housing has made it exponentially harder for people like us (I’m a first generation college graduate). I’m not even anywhere near the bottom of an income bracket & we are priced out. The next generation will want for revolution if they keep getting told “my investments come before your ability to live”

> The next generation will want for revolution if they keep getting told “my investments come before your ability to live”

The boomers will be gone soon, their homes will solve the lack of housing supply.

When it comes to housing scarcity, the lower longevity gets, the faster it’s solved in NIMBY areas. The supply is not allowed to come from new construction, but it’s coming from the mortality of homeowners.

Yes, LFQ, …..”The boomers will be gone soon, their homes will solve the lack of housing supply.”

Very true around where we are as the old crowd moves on. And as the saying goes, “the one fact about old age is that it doesn’t last very long”.

“The boomers will be gone soon, their homes will solve the lack of housing supply.”

Makes some sense but then why haven’t 500k+ Covid deaths really increased the supply of homes?

>The boomers will be gone soon, their homes will solve the lack of housing supply.<

Sigh. I'm 63 and hear this all the time. It's like younger generations can't wait to get rid of us. I've spent the last twenty years as a full-time caregiver for aging parents in ill-health who had/have nothing to leave monetarily. It's been a thankless endeavor, but there was no one else, and I saw it as my duty. Please don't write me off the planet before I get a chance to live. I'm hoping that when my mother finally passes I get at least a few years to take part in society. The Boomer generation was twenty years long. I'm definitely not ready for a nursing home.

Buy gold and silver.

Jay Pow is in bed with the rest of the world central banks and the IMF to inflate the dollar away to zero values. It is not money, it is currency and backed up by nothing. It use to be backed up by Gold. Gold has been accumulated extensively by Russia, China and horded by central banks. They are acting hypocritical about Gold. Gold is real money and was specified in the US Constitution that money be made of Gold and Silver; of course, the Constitution is being violated more and more. I would suggest you accumulated Gold/Silver before you can’t; not for gains, but to preserve your excess labor efforts. All other assets are in a bubble of large magnitude. Soon Gold/Silver will be recognized as the only safe haven left, get there before the crowd.

Gold is not real money. Gold is worth the same as any other item you can barter with another and exchange goods. Have you ever in real life bought something with gold? The metal has value and use but for purchasing it is much easier to convert pesos to USD

Not everyone wants to make their money by being a parasite rentier. I prefer to make an honest living

HAHAHAHAHAHA!!!!! I AM DOING THIS ALL FOR MY OWN ENTERTAINMENT!!!! AND TO FATTEN MY WALLET!!!! I AM NOT SO DUMB AS TO THINK I CAN STOP THE CRASH!!!! I AM CREATING THE CRASH!!!!! DAMN COVID RUSHED MY BUBBLE SCHEDULE THOUGH!!!!! THIS WAS ALL SUPPOSED TO PLAY OUT OVER YEARS BUT MY VIRUS PROVIDED A GOOD COVER!!!! YES…MY VIRUS!!! I CREATED IT BY RUBBING TOGETHER TWO TWO DOLLAR BILLS AND DANCING IN MY SPEEDO!!! BUY HOUSES NOW FOOLS!!!! PRICES ARE RISING BECAUSE INVENTORY IS HISTORICALLY LOW!!!!! DON’T GET LEFT BEHIND!!!!! BUY NOW WHILE YOU CAN STILL AFFORD A HOUSE IN YAKIMA, WASHINGTON!!!! THE PALM SPRINGS OF WASHINGTON STATE!!!! HAHAHAHAHAHAHAHAHA!!!!!!!!!

Dear Mr. Chair J-Pow Sir, given the power you have at the Fed, and all the underlings shuffling around you all day, please have one of those underlings help you locate the CapsLock key on your keyboard (usually somewhere on the left). Future all-caps comments will go into the money shredder.

He probably confused the cap lock key with the print key.

I think J-Pow!!! is a Bot. (not humanoid) LOL!

LOL!!!!!!!!

Blahaha!

Comment of the month.

I doubt the real J-Pow has a computer or even knows how to type. Modern US Presidents are generally famous for not knowing how to use a computer. I don’t think it would be different for any Fed chief.

BUT I HAVE … oh wait there it is … the caps lock button!!!! I always wondered what that white dot was?????? Thank you for helping me find that Wolf Richter!!!! None of my underlings could find it!!!! I will reverse repo half a trillion dollars tomorrow!!!! Just watch me! I can’t wait!!! I am so excited to do this!!!! No one can stop me!!!! The end is coming people!!!! I am finally blowing everything up!!!!!!!

Vindication, finally! My life-long dislike of $2 bills has finally found a logical basis. Thanks, J-Pow!

Please, all that shouting hurts my ears …

These comments are always gold.

Mission accomplished!!!

– Jay Powell

That phrase and red trucker hats are permanently ruined.

New housing starts have surged again. The profits from these homes, if any, might be used to expand more new home building.

More people are added to the Texas population each year than any other state.

“More people are added to the Texas population each year than any other state.”

They will love our weather, rattle snakes, scorpions, floods, gas prices, BIG pickups, ice storms, and Texas BBQ. All, I can say is “here comes a state income tax”….

Lived in Tx for 20 plus years and then I escaped. I had all of the above on my farm. As for no income tax, the gods of TX made up for it in other ways, taxed about everything but the air I breathed. I miss my farm and all the stingy critters ( and the bbq) but not the rest. Texas going to get californirized and turn purple.

Mexico has entered the chat!!!

MB, yes!

And there will be a new language spoken here soon!

And lots of Tacos, Burritos, enchiladas, etc to be had. This should make the new “visitors” from the West feel at home.

Born and raised in California. Lived in TX for college. Back in California. I will die in California. Nowhere, absolutely nowhere, is better than California. Nowhere.

Nowhere, absolutely nowhere, is better than California. “Nowhere.”

For some people. But for those of us who don’t like left wing politics, high taxes, dry air, or Mexican culture, anyplace is better than California.

Best thing about California? The weather if you live along the coast.

San Diego weather for example is pretty much perfect all year round.

We get San Diego weather in Texas for about one week each year, then it’s back to the usual.

Same here Hernando. I grew up in Santa Clara when the walk home from school was along apricot orchards. I lived in Boston and Madison Wisconsin for awhile and couldn’t wait to get back home. I too will die here, i hope not before my new rug arrives.

It’s so great that people who don’t like progressive politics or Mexican culture live elsewhere. Keep that up!

Despite the talk of buyers in trendy cities paying infinite amounts for houses with all cash purchases, the bulk of Americans can only afford houses with conventional mortgages ( fha etc.) The upper limits for conventional mortgages are being overshot by housing price inflation in most areas. In the near future we will see these limits increased ( they vary by location) or the the ongoing bubble will grind to a halt ( thankfully).

The limits will be increased. It can be done, and will be done, with the stroke of a pen.

The objective is “keep all bubbles going forever” and policy will continue to reflect that. This will work very well, until it doesn’t.

The migration from blue to red states will have a great effect on the housing prices, even during a correction.

In my little part of flyover, two builders I work with

were contacted by there suppliers to expect another 25%

increase in lumber prices over the next 2 weeks.

Will soon need security guards on home builds.

One poor fellow deposited his lumber on his land to build a wood fence. The next morning all of the lumber was stolen! The RCMP invested the crime scene and discovered the local beavers were hoarding all of the fence lumber and had no intentions of returning any of it! The RCMP said they didn’t have the authority to arrest the beavers!

My friend had a problem with beavers killing trees in his yard. He found out that if you want to trap a beaver there is a lot of red tape. Shooting a beaver, no problem.

Wholesale lumber prices peaked about the middle of may and are on the way back down. Tell your friend to hold tight and builder prices should start going down. My wife is in negotiations to buy a lumber mill that sits in the path of a dam upgrade by the public agency she manages. The owner has told her he wants to keep it running till august as he is coining money, but after that he expects lumber prices to be way down and he will happily take his money and move on.

This place is going to have to be renamed WTFstreet.com pretty soon.

What blows my mind is how is seems everyone on main street is just accepting that this is normal. Maybe we are at a “permanently high plateau” and maybe this time is different, but I’ve heard it before and I’m trying not to get fooled this time.

I am struggling with the same problem. I feel like this is absolutely bonkers insanity going on with stocks, crypto, RE. I even heard from a friend that works in Commercial Real Estate, that it’s not even declining in value. How is that possible with so many vacant spaces?

Everything about the last year defies reality and economic “laws” – which apparently don’t mean anything now. I just scratch my head ever day and my anxiety grows worse.

With the current Fed rate / Inflation /all the chart’s standings today price increases Etc: The whole ball of wax- – – – –

Assuming the entire government controlled current economy ( CCE ) is Crooked / all wrong rather than Not , just an assumption, exactly ” who stands to gain from it ” ?

Stands to Gain :

Can someone provide a List ? Say 1 to 20 or ?

> ” who stands to gain from it ” ?

Commodity producers/extractors from farmers to miners will be sitting pretty.

Everybody who doesn’t need the money benefits. The poor, retirees on fixed income, and the working class get destroyed. Powell should have his head on a spit.

Of course : Humm Raw material or Primary Agricultural & increased Real Estate Commissions well be Huge That could be an incentive

I am getting it . How about foreign Incentive ? wops that sound scary

At this point, Lawrence Yun should introduce the Yun Coin. It’s crypto backed by mortgages. If that doesn’t go gangbusters, I don’t know what will.

Nah, think he got bigger ambition, I can picture him as the next FED chairman, he can gaslight like nobody’s business, been perfecting it way before 2008.

You certainly are a character J-Pow!, way more so than the actual elite robot in charge hitting that print key nonstop. That guy has as much personality as a door knob, you would think a guy that’s literally robbing the American middle class by terrible monetary policies can at least smile once in a while from the giddy of knowing his own portfolio just got more excess along the way but nooooo…

What I find interesting is that at this stage of the bubble, you find people that have been holding out for a while now all of a sudden want to jump right in at possibly the peak of insanity. The justification is often filmsy reasoning such as this time is different especially since 08 was all about subprime that caused the crash (which was not true if you dig deep into the data as proven by an MIT economist looking at credit score related to default on the last crisis). Tons of mental gymnastic to arrive at their justification to reassure they are doing the right thing. A friend of mine just bid and got accepted on a house in San Diego close 100k shy of $1M, a place that sold for mid $400k in 2013, a house that in “normal” time would be consider expensive at $400k. Funny thing is that he is a smart guy but yet ate up the narrative the RE agents and mortgage guys are selling. Interest rate is all time low, it will go up soon, so buy now. Oh and last crisis, good areas were not impacted and it only F up lower middle class and lower class..etc..etc. Another friend are now looking but can’t find anything in West LA area for less than $1.5M, owns a condo now but somehow also think the market will just level out and for some reason even if there’s a downturn the volatilities won’t affect condos and townhouses but only on single family homes will be impacted. Honestly can’t roll my eyes hard enough when I hear their reasoning depsite my failed effort in getting them to look at the actual data, look at historical context more and even have them read through some of Wolf’s articles in the past…Sure I am the odd one holding out even now…who knows if either they or I will get the last laugh. If the market turned out the way they predicted I guess I will then truly suffer the MO from FOMO but at least I know I did my part on going on buyer’s strike and refuse to overpay for some s*** box. Anything is possible so maybe this time is different but is it probable? That’s the part I can’t convince myself no matter how I slice it in my head. Surely a frustrating and depressing time for a contrarian to live in.

I think if your roots are not too deep and you are in an area that average home is a million dollars it’s smart to consider cashing out as there are plenty of places to shop for average homes in the $200K to $400K with property taxes $1K to $3K.

Paragraphs would help t be able to read this without quitting in the middle somewhere. Please?

We are closing this weekend on our house. The owners dropped the price by 10%. Our hand was somewhat forced. We have been shopping since January and nearly gave up for renting but our rental was bug infested so we decided to move… again.

So, we made an offer on 5 acres with a well that pours out clean water for hours with very low draw. A perfect septic and a full propane tank. 2000 square feet of a newer prefab home. Oaks everywhere and 2.5 miles from the beach. I have never been so happy.

I could spend 72,000 dollars the next two years on rent… or pay 36,000 dollars the next two years on principal. I can also own a dog, some chickens, and a goat.

Frankly, I don’t care anymore. Atlas shrugged.

congrats. You have detailed your long search. Sounds like you found a nice place.

Wonderful! Congrats!

In 1999 and 2006, CPI was running near (actually lower) this current rate.

30yr mortgages 6%.

Now, the Fed has them at 3% … as they buy MBSs…

and with the inflation in building materials, house replacement costs increased 35% or so….

Buyers have money too cheap…

Sellers must raise their prices to compensate for the replacement costs…

Central Planners at work….

Free markets gone, the Fed manipulates like a Central Planner/Socialist entity.

One comment keeps running through my head. What if they did drop 30 year mtg rates to 1%? Would we see a huge rush to refi again?

$300,000 @ 1% = $964/month.

If the gov’t is backstopping all the loans why not see…How low CAN we go?

How can the Fed basically and continually lend money to the govt and the mortgage industry BELOW the inflation rate? This has NEVER happened before.

Last time inflation ran near these levels (actually less) was in 1999 and 2006. Both time the 30yr mortgages were 6%. Now 3%.

The Fed has changed everything…….and their friends were the first to know…and the “bravest” to act.

“When central planners act, they intentionally aid one group at the expense of another.” F A Hayek.

Free markets? Nope.

Stage one – The markets are rising.

Look at all that wealth we are creating.

Stage two – It’s a bubble.

That wealth is going to disappear.

Stage three – Oh cor blimey! I remember now, this is what happened last time

At the end of the 1920s, the US was a ponzi scheme of inflated asset prices.

The use of neoclassical economics, and the belief in free markets, made them think that inflated asset prices represented real wealth.

1929 – Wakey, wakey time

The use of neoclassical economics, and the belief in free markets, made them think that inflated asset prices represented real wealth, but it didn’t.

It didn’t then, and it doesn’t now.

Asset prices go up.

Asset prices go down.

Don’t mistake this for a store of wealth.

A whole new generation are going to have to learn the hard way.

Real estate – the wealth is there and then it’s gone.

1990s – UK, US (S&L), Canada (Toronto), Scandinavia, Japan, Philippines, Thailand

2000s – Iceland, Dubai, US (2008), Vietnam

2010s – Ireland, Spain, Greece, India

Get ready to put Australia, Canada, Norway, Sweden and Hong Kong on the list.

It wasn’t real wealth, just a ponzi scheme of inflated asset prices.

Will they ever learn?

It doesn’t look like it, does it?

We haven’t been able to get past stage two.

Stage three is when it dawns on you what is really going on.

Where is the real wealth in an economy?

It took them a long time to disentangle the hopelessly confused thinking of neoclassical economics in the 1930s.

This is the second time around and it has already been done.

The real wealth creation in the economy is measured by GDP.

Real wealth creation involves real work, producing new goods and services in the economy.

That’s where the real wealth in the economy lies.

Exactly, what good is a pile of money on a desert island?

Or for that matter in an integrated global economy? A traditional pension probably replaced more income in retirement for workers than most 401(K)s but a pension doesn’t count as wealth.

Anyone that knows finances knows that government pensions are running fraud on the general taxpayer. Virtually all pensions used to be backed by conservative fixed income investments. Now they are backed primarily with equity like investments with the whole industry built on a 7% assumed return Hussman does a pretty good job showing that even if the Price to sales ratio stays at this record level you can’t really get beyond about 5% future returns and they are probably going to be a lot less. Pension system design is basically can kicking problems to next politicians.

Implicit in the “Washington Consensus” (i.e. neoliberalism) is that financial markets are the most efficient allocation of economic resources. Market liberalization has allowed the West to hoover up assets all over the world.

China is trying to upend that order, basically “if we control the beginning and endpoints of products, why do we need your financial markets?”

Bingo! “Real wealth creation involves real work, producing new goods and services in the economy”

Why should dollars earned & saved from goods & services produced ,say, 20 years ago have the same purchasing power today when those goods and services originally produced are subject to depreciation, obsolescence, and lower reproduction cost because of technology?

Low end housing (however defined) is the place to be. Trend will be the creation of multifamily homes on what used to be single family lots as local zoning rules will be modified to meet demand.

Because savings equal investment equal productivity gains equal higher standard of living. At least that was the way it worked before Fed begin printing savings. But Fed pulled asset values too far from the future that returns are now zero in real terms.

It’s the vaccines fault. That’s why Wolf will never get invited as a journalist to ask questions at a Fed event.

As somebody who’s planning on moving (to East Idaho) for work, part of me really hopes the bubble pops in the next few months. At least apartment rents out there are still cheaper than what I’m paying right now in New York.

Good luck. Im probably going to move back to the midwest after renting in Boise the last 5 years.

“Leave your housing inflation worries behind and move to beautiful, inexpensive Punxsutawney, PA! We have a wide selection of single family homes for well under $100,000.”

Quality of the homes not guaranteed. Finding employment might be an issue.

(No, I don’t live there)

Richmond Hill in Ontario, Canada will always hold the record as single detached home prices have gone fifty fold in the last 37 years. 1984 to 2021. From $30,000 to 1.5 million. It would be much more than 50 fold as the bungalows that were new in 1984 are the exact same ones going for 1.5 million 37 years later meaning all of them are resale not new ones.

FWI, USA has lots of bio weapons laboratories mostly encircling Rus/Chi.

Suggestions that do not account for this – which pretty clearly show who is the aggressor – are not providing an accurate account.

The cost of such lab is cheaper in China. To shift the risk

and cut cost it made sense to transfer risk to our good and

trusted friends in China. On top of cost and risk, there might have been a political pressure to do so.

“China Halts Banks From Selling Commodity-Linked Investment Products To Retail Traders”

Terminating financialization.

Are we learning, USA?

Seriously CLIPs?

The day we start comparing USA’s policy towards its citizens to that of China, is the day I’ll want to leave that place.

Based

I’m beginning to believe the Fed is now creating new ways to keep the liquidity hose on high permanently. Maybe home prices will never correct again?

I Just read an article on how the Fed is going to cut the primary Treasury dealers out of the Fed’s ecosystem. My understanding is that the primary dealers buy or sell treasuries at the whim of the Fed. When the Fed tells them to ‘sell’ Treasuries, the banks get cash which I assume they’re supposed to use for productive loans. This stimulates the economy. Apparently the primary dealer’s haven’t been cooperating, so the Fed is going to take on that role themselves.

I’m not sure how much of a change this will be but it sounds ominous. Wouldn’t be surprised if the Fed also kills off interest on excess reserves.

Is the Fed going to dial liquidity up to 11?

Stockman had that right ten years ago. Fed policy just begets more and more extreme policy.

How can a Fed Chairman get before a group and say

“we are promoting inflation.” ???

The agreement that allows the Fed to exist is “stable prices”.

Those mandates are also the instructions for the Fed.

INFLATION STEALS past labors (savings) and current wage earnings.

To promote inflation is to prearrange a THEFT from a group of people who are unrepresented, innocent, They are victims of an unelected group (the Fed) who is violating the rules, violating the instructions, violating the idea behind the Federal Reserve.

This is an outrage. Powell should be arrested. Fed Funds have NEVER been 4% below the inflation rate. This is the stealing gap…and it widens.

No talk of increasing wages but we just might see that. BOA has announced their minimum wage will be $25/hr by 2025. In markets where the lower end can afford homes this is significant. Even Florida voted for a relatively high minimum wage ($16?) Hearing stories of professional type well paid jobs in such demand too that folks are getting large pay increases. Is this part of the weird jumps in demand right now or a longer trend.

I think they are central planning too much. We will see what the outcome is. No price discovery for interest.rates. No price discovery for labor. Paying people not to work. All made possible by stealing from the the prudent. Where can this go except more crony capitalism and long term decline of USA

Do Boise! Do Boise!

Wolf – Are you able to chart Bend, OR? Over the past 20 years housing here has been ridiculous.

How long can this go on?

I’d like to see that along with Reno and Couer d’Alene, in addition to Boise and Bend. There must be a dozen smallish areas in the West that have gone totally bonkers thanks to the influx of Californians. Boise price gains exceed 30% year over year!

Got crypto? 235% per year for 11 years. R.E. ,Bonds ,Gold, Equities and Sovereign Funds of varying amounts will head for the only safe refuge. It’s a 500 Trillion TAM and Bitcoin is the Amazon and Google of the space. Check out the adoption rate of the cellphone, and internet . It took 15 years to hit +80% of U.S. households.

I say when asset bubble pops and people panic, Bitcoin will lead the race toward the bottom.

Here is Phoenix, it’s different this time. Last time (circa 2009), they said the economy was “construction workers building homes for construction workers”.

This time, there’s so many high-value businesses moving in, it’s mind-boggling. Companies from California, Washington state and elsewhere are leaving inhospitable business climate and coming here.

As an example, there’s 4 new chip-producing factories to be built here. The first one, which has already started is Samsung one, with $15 billion investment.

Along 202 there’s about 14 new huge warehouses (each at least 1 million square feet) built in just the past few years. All huge brand names.

A mystery IT business (name not announced) broke ground on a new 1.5 billion data center near Eastmark in Mesa. Probably 6th or 7th in the area.

In Buckeye, new manufacturing is popping up like mushrooms after the rain. Lots of it transplants from elsewhere.

So housing pricing going up here reminds me of Southern California in the late 1990s and early 2000s. House prices doubled and then trippled in about 6-8 years time, and never looked back. The reason was that good paying jobs arrived.

The same is happening now in Phoenix. Good paying jobs, and diversified, galore, everywhere.

For those who think that this time, like in 2009, Phoenix house prices will drop back, well, it may never happen…

You are correct. I am a native and moved back here for family reasons (and to escape CA). The place is booming and jobs everywhere. There may be some issues long term with water and such, but for now it’s tremendous. It’s not the city of the 2006. Doesn’t mean there won’t be a correction, who knows.

In the past I argued that the DFW Dallas-Ft-Worth housing market was not in a bubble and I was correct. Now I agree it is in a strong bubble that is driven by speculation and the FOMO on top of low interest rates. While not as crazy as Austin and driven by economic growth, it is exceeding the rise of income levels. In the past housing was so far behind the rest of the United States the rapid rise was justified to make it on par with other large US cities. So it now is on par which means it is just as crazily overpriced as the rest. Time for everyone to take a profit while they can if they can find a replacement home. Prices will keep going up, but you risk missing the top if you wait too long.