They’re not the same consumers.

By Wolf Richter for WOLF STREET.

There is no monolithic American consumer. Each does their own thing. And the folks with credit card debts and other revolving credit such as personal loans – all of it high-interest rate debt – paid them down by record amounts in January, possibly using their stimulus money to do so.

And in the opposite direction, the folks who own homes have been extracting cash from their homes via cash-out refinancing their mortgages at a clip in Q4 not seen since the peak of the good old days before the housing bust in 2005 and 2006, and at record low mortgage rates while they lasted. But those two groups may not be the same people.

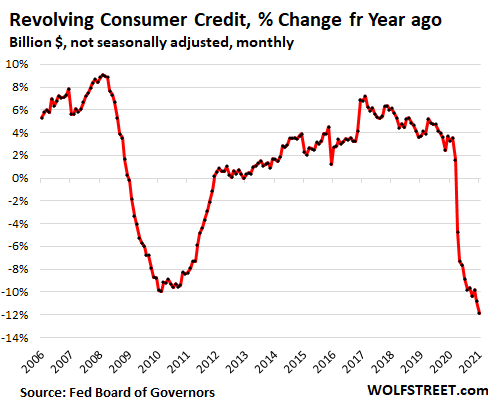

Paying down credit cards and other revolving credit. In January, consumers paid down their credit card balances by 3.6% from December and by 11.9% year-over-year, not seasonally adjusted, to $940 billion, according to the Federal Reserve Friday afternoon. It was the biggest year-over-year decline in the history of credit card data going back to the 1970s and blew by the year-over-year declines during the Financial Crisis:

There were only two periods in credit card history when balances dropped on a year-over-year basis, and for two very different reasons: First, during the Financial Crisis when consumers defaulted on their credit cards; and second, during the Pandemic when the government sent hundreds of billions of dollars in waves of stimulus payments to consumers, and some of this money was used to pay down credit card debts.

January is the hangover month after the holiday binge-spending-and-borrowing, and credit card balances (not seasonally adjusted) tend to drop from December as people are beginning to grapple with the consequences of their binge. Between 2013 and 2020, the decline in credit card balances from December to January averaged 2.4%. This year in January, credit card balances dropped by 3.6% from the already lowest December levels since 2016.

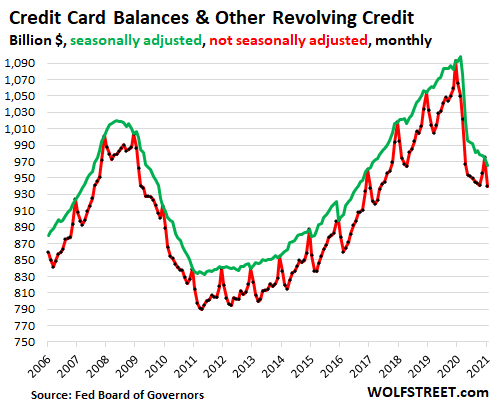

In dollar terms, credit card balances fell by $35 billion in January, not seasonally adjusted (red line), to $940 billion, having plunged by $153 billion from the peak in December 2019; and seasonally adjusted (green line) they fell by $10 billion in January, to $965 billion, having plunged by $128 billion from the peak in December 2019.

The cumulative two-year plunge during the Financial Crisis was larger than the drop during the first 10 months of the Pandemic. But the next stimulus packages is being put together in Congress, likely producing further drops in the future:

In the opposite direction: Cash-out Refis.

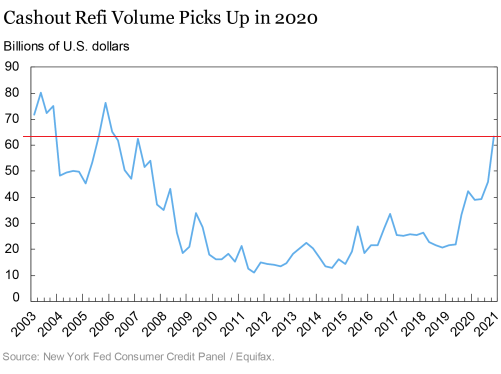

Historically low mortgages in the fourth quarter triggered a historic mortgage refi boom that exceeded the peaks before the housing bust. Amid this historic refi boom was a near-historic cash-out refi boom. According to a New York Fed report two weeks ago, the amount that homeowners extracted from their homes in Q4 spiked to $63 billion, with borrowers on average extracting $27,000 from their homes (chart via New York Fed):

Homeowners used the proceeds from the cash-out refis to fund consumption and “investment opportunities, including home improvements,” as the New York Fed said.

So on one hand, consumers are paying down their expensive credit cards and other revolving credit; and on the other hand, consumers are borrowing a lot more against their homes.

It is possible that some folks with cash-out refis also have credit card debt and are using the proceeds from the cash-out refis to pay down their credit card debts, using historically cheap mortgage debt to pay down expensive revolving debt, and that would make a lot of sense.

But it is also possible that there is little overlap between these two groups – between those who paid down their credit cards, and those who increased their mortgage debts via cash-out refis.

In other words, it’s possible that people with credit card debts paid them down with their stimulus checks, but they may not own a home, or cannot do a cash-out refi because their credit score is too low, or because they don’t have enough equity in their home, or because their mortgage is in forbearance and/or delinquent – over 17% of FHA mortgages are delinquent, including those that were delinquent before they entered into forbearance.

So the theory that most of the cash-out refis were used to pay down expensive credit card debts doesn’t hold water. These are different consumers. As the New York Fed pointed out, the cash-out refis were mostly used to fund consumption or home improvements, such as a new deck and hot tub, which has been back-ordered because of the surge in demand, or speculative investments in what were then seemingly forever booming financial markets.

Suddenly rising mortgage rates to tango with refi boom.

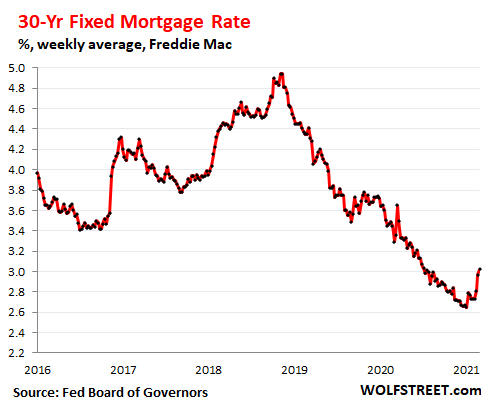

Mortgage rates bottomed out in early January and have risen since then. The average 30-year fixed mortgage rate, according to the Freddy Mac benchmark index, increased from 2.65% in early January to 3.02% on average during the week ended Wednesday. Since then, mortgage rates have further risen, which is not reflected in the data yet:

Mortgage rates remain ultra-low by historical standards, but they’re a little higher than they were two months ago – and there has now been a lot of hand-wringing in the financial markets about them, and folks have been clamoring for the Fed to do something to push down those mortgage rates, which has not been forthcoming at all.

But the more mortgage rates rise, the harder it is to make cash-out refis work. So while some consumers are creating a little extra room on their credit card for future consumption, other consumers will find cash-out refis to fund consumption more expensive and difficult to do.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Don’t jack rates, Jerome! Let that 10T bad boy keep on rising! You gotta get your inflation on! And I gotta get me a cheap house!

Well, that is the $64 question.

Yield Curve Control or Operation Twist or let the market decide.

The irony is the Fed wants at least 2% inflation which means 10 year Treasuries should be at 3% minimum.

Mortgage rates should be at 3% but they ain’t at 3%. The first operation twist happened in 1961. Operation twist #2 happened in 2011. Powell needs to start up operation twist #3 so that he can keep the 30 year mortgage at 2.65% while real inflation is cooking at 5%-6%. If we’re going to live in a mystical la la land then don’t cut any corners.

Real estate rising 10% a year. Cars & healthcare, more or at least the same. Assets rising double digits (and they absolutely must be considered inflation too). 5 to 6 % inflation…best guess that’s a big underestimate.

Let’s do short cut math. You have $1.1 million home you put $100,000 down payment on. Your mortgage is 3%. Interest cost roughly $30,000. Home appreciates 10% in 2020. That’s $110,000 leaving $80,000 increase in equity. Subtract off just under 3% for maintenance tax ins and that’s another $30,000 of cost. That leaves a $50,000 net gain on $100,000 investment. Good Job Powell.

Run the numbers for 10% decline. $30,000 interest, $30,000 cost and $110,000 house value lost. That’s a $170,000 loss on $100,000 investment. Bad job Powell.

Leverage works both ways.

Old School,

That $50,000 gain in just one year looks “free”, but that would be magic. And there is no magic. So where did it come from?

That gain comes from thousands of working people who can no longer afford shelter, due to the price increases. But those costs are widespread and diffuse and can’t be pinned on any particular individual homeowner. That allows the smug homeowner to congratulate themselves on being smart enough to make money while they sleep.

Too bad about the folks sleeping in their cars. They just didn’t work hard enough / weren’t smart enough. Good thing there is pie in the sky when they die.

The gain, as noted by OldSchool, only comes if you can sell it for a value that captures that run up. Until the sale is made any gain/loss is all smoke and mirrors.

I keep pointing that out to my investment advisor(s), but they don’t get it. It’s like all the letters flooding my mailbox telling me I should do a cash out refinance in order to “put that money to work” or “buy something you deserve”. (Like I need stocks or a new car right now…)

Yep Trash, the class warfare in this country is extremely vicious, especially considering all the wealth here. $100T net household wealth, was the last Fed number I heard, and that doesn’t count all the hidden $$s, of course.

Someone set fire to one of those unsightly stupid homeless losers here recently, but since, as you noted, we practice “pious class warfare”, it gave him immediate access to his eternal heavenly reward. So they really did him a favor…..once he finally died…..I guess….

Guess I should just glad we are all “free” here.

Buy up all the UST will leave the markets that are dependent on collateral even more leveraged/reyhpothicated and exposed to greater tail risk…

Buy up all the corp bonds will make them even less attractive (hedged), faster, on a spread basis to UST… game will be up when avg IG yield after fees/tax is less than UST hedged… 27.4 bps asof EOD friday… not even considering duration/convexity…

Offshore banks dont have access to either of these compared to the frbny’s brokest dealers at the teat of frbny daily… Offshore banks also have the most eurodollar exposure…

Best frbny can wish for is at this point they remain relevant when all is said an done as they like their peers rush to instill CONfidence in their CBDC’s… the CB monetary fonzian shark jump… lol

Saw her last night, and she had modest goals for inflation, normal, she said, or 2%. They are downplaying the GDP overshoot. [10Y at 3% and positive real rates they won’t have any problem financing the deficit (at shorter maturities)] Should the dollar firm imports will continue (and those manufacturing jobs will not return) Fed’s job now is selling this paper, not suppressing rates for subprime corporate borrowers. Wolf noted this cuts off high end REFI spenders. They already have YCC, but they won’t go full Japan on this. There are easy paths and hard ones, they choose a policy, and then let the market decide. The political litmus plays a big part.

I try to listen to a lot of people. You can never be sure how it will turn out, but I am starting to believe Harry Dent explanation is going to be correct. He says in financial crisis 9 times out of 10 it’s going to be Asset collapse.

He is saying the play is holding 30 year treasuries because they are going to head to 1/2% and you will make 40%. I am not that brave, but I could see it happening.

Old school,

That has been Gary A. Shilling’s play since 1982 (and he has done very well for his clients!)

:)

House won’t be cheap…sellers will just hike price so your monthly stays constant.

Same house…same monthly…doubled debt.

Story of last 20 years.

The endless column of supplicants in the comments imploring Saint Jerome of the Holy FED are not unlike medieval peasants roughing the long roads to Padua to ask Saint Anthony to intervene on their behalf.

Nothing new here, we saw exactly this same behavior in the early 2000’s leading up to the 2008 crash.

People using inflated home equity to pay down credit card payments they can not afford. We have seen this movie before, and we know how it ends.

Except they used their home equity to pay down credit cards….

Only to run up the credit card balances again.

Rinse. Repeat.

Until the music stopped.

I have noticed a large increase in new cars with temp registration tags on them in the Houston area since the first of the year. It’s my guess some of that “cash out refi” money is going into new cars.

More likely to be insurance money from the hurricane last year. I drove through Houston, TX and Lake Charles, LA last month. The blue tarps and boarded up buildings are still all over Lake Charles. Houston looks like it is booming.

Hurricane Laura hit Lake Charles, Louisiana in August 2020.

We didn’t have a hurricane last year in Houston and really didn’t get much rain from Laura at all, and it did no appreciable damage around Houston. (lucky that time)

Storm Harvey (hit landfall as a Cat 4) was in September 2019 at Rockport, TX then moseyed up the coast to Houston where it dropped 53″ of rain over 4 days. Sure was wet here!

Those new cars around HOUSTON are Texas buyers and it’s all about PPP loans, Stim checks, UI payments, buying Tesla stock!

I forgot to mention Refi’s cash too!

Without going into detail, I have a rental house in Lake Charles that was slightly damaged by the hurricane. Got a new roof on it and fixed a broken window and fortunately made out okay.

People are refinancing to pay off their big credit card balances, stripping most of the equity out of their homes. After they pay the credit cards off they then start using them again and running up the balances to even higher levels. This was what “The Miestro “Greenspan” said was needed to keep the economy running. Same thing is happening with Powel who is copying the same playbook by keeping interest rates artificially low.

Banks are constantly bombarding homeowners with an advertising campaign about how it is financially prudent to refi your home or take out a HELOC to pay off high-interest credit card debt.

Not to mention that now intolerable Tom Selleck ad that runs forever (actual commercial time and also frequency, so it must work) for Reverse Mortgages. I figure it is targeted at older widows with homes. Like the old(er) lady here in my apt complex who immediately put a Ben Carson sticker on her car, “Because he is such a nice man”.

Several differences this time however, lenders are not offering NINJA loans and scrutinize income to debt ratio and credit scores. Also, these low interest loans are fixed, unlike the adjustables which offered low interest tickler rates that doubled in short order, making them unaffordable for most upon adjustment. With today’s low fixed rates, mortgages are less than rent in many jurisdictions. Home equity is irrelevant if you can afford the mortgage and ride the wave until it crests once again.

Not exactly. There is a limit to conforming loans in each county. In the county I live it is 701,000 dollars. After that you either have to get a jumbo loan about 1/2 – 1 % higher; so the rate would be 3.5% or more on the loan.

To fix this all the lenders I have worked with want a borrower to either make up the difference or get an interest only adjustable 30 year HELOC (after 10 years) at 5.5% or roughly 500 dollars interest for every 100,000 dollars borrowed above the non conforming rate.

I’m willing to goof around with the HELOC a little; but I was surprised when one lender knew I had the money to cover the difference but still wanted me to get the 50,000 dollar HELOC?

Top it off, closing cost are somewhere between 20-30 thousand on a million dollar home- which is surprising too.

There is your adjustable rate mortgage hunting middle class buyers. You think you have the money then pow- closing cost gets you and HELOC becomes an attractive option – even at 5.5%

I would be careful with the HELOC. If I remember correctly, there are fees involved in opening the account, even if you never use it.

Also, I remember stories in Florida about HELOCs being called in during the GFC even if the homeowners were paying. I think some of these products actually put some people into foreclosure.

What happens to your future buyer pool if rates

1) rise 2% to the “historical” lows of 2009-2016, or

2) by 5% to 90’s normal, or

3) by 14% to 70’s stressed (when national debt levels were 50%+ lower?).

Paying top dollar with 2.5% mortgages means absolutely no profitable buyers if rates reach 5%…which would have been a historic low pre 2003.

Rates are not going to normal, yet. I don’t see it. The Fed can do a technical adjustment to exert more influence. If that is not enough, they can increase QE. I am not saying its right but inflating the debt away is important ultimately to the US government. The Fed dual mandates certainly continue to give them a reason to keep easy money policy.

Wealth inequality may not necessarily be resolved by a huge crash in asset values. It may be solved by devaluation of the currency (that those heavily in cash or bonds don’t seem to understand – makes the rich less rich in real terms) and an infrastructure bill that also requires a lot of new employment and possible reducation programs and such.

Just taking some realistic guesses… post WW2 monetary and fiscal policy had very similar goals to today. As every day passes, that thesis continues to be proven out by the Fed actions.

This is 100% correct.

Also, everyone needs to understand that the maximum loan to value on conventional and FHA loans is 80%. So, that’s leaving a lot of equity left over.

500k appraised value

400k Max loan amount

Most Helocs won’t go above 80-85%

There are a couple banks that will allow90%, but, not the norm.

I live in NC and spent last week at beach close to NC and SC border. A lot of new construction on the island roughly $600,000 plus and off the island in retirement communities for $200,000 less due to cheaper lots.

Bumped into a building contractor who works for a housing construction company. He had just closed on a nice home in one of the nicer retirement communities. He was tired of renting just to be close to work. Might be a sign of the top when the real estate sector creates its own demand.

If true – very poor decision making and will end in disaster.

Risking your home for a hot tub or some Tesla stock…

“As the New York Fed pointed out, the cash-out refis were mostly used to fund consumption or home improvements, such as a new deck and hot tub, which has been back-ordered because of the surge in demand, or speculative investments in what were then seemingly forever booming financial markets.”

I was just exactly how many of these cash out refis are to buy DogeCoin or Gamestop.

I don’t know (but can make a good guess at the PR agenda) where these, “everyone else is frivolously stupid” assumptions come from.

When I saw $27K, I figured, OK, a new roof, paint job, dual glazed windows, fences, replaced appliances, or maybe a deck. In fact, if hot tubs really are on back order, I’m pretty certain we are talking about yet a 3rd group of people, i.e., the ones $2K+ mattress ads, Pelotrons, etc, are aimed at. And I doubt any of them are cash re-fi money.

I love charging everything on CC, paying it all off, and then getting 3% back! Better than a Treasury! Charge/Rinse/Repeat. Even regarding home equity, people will find a way to get the best bang for the buck. Not everyone is a loser.

Credit card companies play plenty of games to trip up even the most dedicated card holders.

Taking a week to cash a check.

Sending out bills late.

Reducing the bill cycle.

Give you some cheap and easy money that isn’t.

Etc.

You definitely have to be on the ball, an d KNOW what you are doing.

Checks have nothing to do with it.

Know your closing date.

It’s illegal you change the cycle without telling you on the current monthly statement.

Knowing what you can afford is definitely the key, pay the card before you charge it, if that makes you happy :)

Not sure what CC you’re talking about. Not sayin’ it ain’t true for some, but I’ve been using my Chase UA card as a convenience card for over 30 years. Pay it off every month and use the points to fly to Hawaii every few years. I have NEVER had an issue with them “tripping” me up or trying to change terms.

What is this “check” thing you speak of? Pay your bills online. Use automatic bill pay. If you don’t have enough money to keep in the bill paying accounts, you need to cut up your credit cards.

You forgot to add, the prices on everything you buy with your credit card are inflated by the 3% or more to cover this rebate, so you still are a loser.

Where do you get a cash discount?

Nearly every gas station offers cash discounts.

Lots of places, if you ask.

Not in my area. How about your grocery store and department stores? Get any cash discount on your online purchases?

No, but my favorite Indian restaurant likes cash, and they always throw in a few free items, like a few samosa’s for free because I always pay cash. I also get a free Bud Light at my Irish Pub whenever I pay cash which is all the time. My lawn man gets paid in cash and he gives me a great deal on the lawn service.

Don’t know about recently osp, but several decades ago I usually had a couple thousand dollars in pocket ready to pay cash for building materials, tools, etc., and would routinely get at least 20% off the prices at almost every location all over NorCal. ( I could also run really fast if needed!!)

Of course, some places would not negotiate one bit, but there were few of them, mostly bigger places where the owners were not on the floor or in the yard, etc.

And don’t even think or blink about the ”deals” at the ”flea” market, usually formerly known as the thieves market most places.

This was before wide spread of major credit cards, so either had a gas card, or a ”store” account — with 2% 10th prox — or check or cash.

Many smaller/older motels across USA, with owners in office, are still willing to negotiate for cash versus CC recently.

Paying cash means the tradesman makes approximately 50% more on the job.

Paying by check or credit cards mean federal, state and local taxes, unemployment insurance, social security come out of your payment to him.

At best, you save 15% on capital gains if you sell the property and write off his bill.

Cash means 100% goes in his pocket. That’s why he’ll be happy to give you a 25% discount, you both come out 25% ahead, and if forgo the reciept and write off against capital gains, you still come out 10% ahead.

If you are buying any expensive power tools or building material, have a contractor buy them for you. He gets the ~50%tax write off and will often split that with you, he gets a lower contractor price and he will usually deliver.

Winwinwin all around. Cash is king.

There might be stores that charge extra for using a credit card, but at supermarkets, restaurants, gas stations, and plenty of other retail outlets (including airlines) you can use a credit card that awards you points but no added fee for using the card.

A Chase Sapphire Reserve card pays 3x points on purchases for travel, dining and groceries. Each point is worth about 1.5 cents when spent using Chase UltimateRewards travel portal, so for each dollar you spend its potentially 4.5 cents back. Lyft is 10x points Most other purchases are 1 point. You can cash in your points for 1 cent each so those 3x point deals kick back 3 cents on the dollar.

Points are transferable between numerous other programs. 1.5 cents per point when transferring to SWA or Hyatt. Some swaps suck, like 0.8 cents with Amazon.

Free Doordash membership with all the perks.

This particular card is aimed at travelers. It has a hefty fee of $550, but you get $300 back on your travel expenses, a free Global Entry or TSA Pre card ($100), free entry to certain airline lounges at airports (I love this feature – free booze and food, quiet comfortable seating).

Similar benefits with Sapphire Preferred which is only $75/yr but the 3x points drop to 2x points and you lose the travel perks.

I don’t play any of those credit card games. To me it’s like going to an orgy at an AIDS clinic and believing that you won’t get infected. I have a M/C and an Amex and I pay them off when they post the transaction. And no, this does not affect your credit rating. We have $35,000 credit limit between the two cards. This is consistent with my policy of being debt-free. We bought cars cash and saved ten years and bought a home cash. Now retired, we don’t have money worries.

“I don’t play any of those credit card games. To me it’s like going to an orgy at an AIDS clinic”

This.

The CC companies aren’t charities…all those convoluted bonuses/reward structures are very carefully designed to maximize borrowing and/or late pmt…at least in aggregate/statistically.

(What do you think CC company employees *do*?)

You can play Indiana Jones with their rules or you can just Google for lower prices to begin with.

As a business owner, I pay for those “rewards” they do not come from the credit card companies. The merchant pays higher fees on reward cards than other credit cards. With Square processing, it is a blended percentage, so you don’t see the reward cards pulled out at a different rate.

Prove it.

And another 3% inflate to cover the transaction fee.

Yes, you would be ignorant not to take advantage of a cash discount, and I do, when available. Don’t forget many gas stations charge high prices, regardless of cash or CC. (don’t forget that free car wash!) ?

2% cash-back is the best I could get. Where did you find 3%?

Sam’s Club MC offers 5% on fuel, and now 3% on most everything else. Capital One just offered me an upgrade to their 3% no fee CC. I have been receiving several offers lately for upgraded cashback. Is there something going on that is provoking these latest offers?

Discover offers 5% cash back on items in certain categories. They change the categories from time to time.

I’m getting 5% on specific deals or retailers, on a sporadic basis, but not across the board. As a loss leader, I can see that. But fees collected from the merchants don’t cover those kinds of cash-backs.

The best I can do is 2% cash back on a PenFed VISA. I’ve had it for a few years now. I don’t do points, just cash back.

I think Fidelity also has a 2% cash back VISA

BofA has a 3% option on their Cash Rewards Visa where you select which category to apply, such as restaurants or home furnishings or whatever they allow. You can change monthly if you anticipate some larger purchases.

I have a Fidelity Visa that pays 2% on everything…. Went from a traditionally cash paying customer (debit or check) to one that charges just about everything possible and pays it off monthly.

I hate those credit cards that play games with categories / percentages and change them on a whim. 3% on restaurants but 1% on groceries? Forget it. I’ll take my 2% on everything. Works out better for me.

I have lived about a year without a credit card. I do use a debit since covid, but I was all cash before and plan to return to reduce big brother tracking.

Living without a credit card makes you a more conservative consumer I think as you have to keep bigger emergency fund and you do a double clutch on some items because it’s coming right out of your cash account now.

Costco Citi Bank- I have a 500 dollar check I have to get cash for that I received last week. REI also has large dividends; I have 175 dollars I just received to buy goods from them since they are not giving out cash this year.

We shop at BJ’s club in Utica… I have a MasterCard through them, and we stock up on groceries. The premium card costs $75 a year, but we get a discount of 5 % on groceries, 10 cents off a gallon of gas at their station, 2% off gas and groceries at other stores, and 1% on general purchases in other stores. In the past year, I have gotten over $600 on savings, so the CC cost is more than offset. Also, I pay it off every month.

The banks suck!!!

Cheating us from normal 5-7% interest rate because they can.

Hi to ceicius for 10%

F… The bank!!!

When is Jerome/Janet gonna let us buy homes with credit cards? That will address their worries of declining consumer debt and allow us to get 2% back.

Refinancing on empty homes may be one of the hidden dangers out there that no one is aware of or talking about. I’ve had to take notice of the unusually large number of houses that we’ve inspected for cash out refinances, or sale in the last 2 months that are vacant. I would say 50% or more. Is this a shadow inventory waiting to be dumped on the market just like in 2006? Why is anyone refinancing on an empty unoccupied investment property just before selling it? If so this could be a signal that the housing price spike is nearing an ugly end. The game is Just to grab as much cash out of the property and then let it default, and hand the keys to the lender and walk away with the loot.

Units for sale could be small investors selling the rental house while the market is hot. Cash our refi on a vacant unit is weird.

In the Eighties speculators bought condos with almost zero down. Prices were going up very fast. You sold or refinanced to take profits, tenant or not. When it all crashed, the banks took them all back. No problem, your primary residence was all cash and all the appreciation was already in the bank. We had a local medical student who dropped out of medical school to make a lot of money doing this. He got very rich and went back to school about 1990 when it all fell down.

This can be done in any up cycle of the Boom or Bust real estate market that afflicts America now.

As a real estate Broker in SoCal, in 2007-2008 I saw owners take huge re-fis and then walk away and then buy a similar house at a lower price in 2009-2012 using that cash. Some didn’t walk away but did a short-sale. Great strategy and I think it applies right now.

That’s exactly what’s going down now I suspect.

When criminal behaviour is considered a great strategy for increasing wealth the end is nigh.

Dine and dash is a great way to eat out in restaurants, too.

I like Roddy667’s comment about debt and CC (above). I have always worked and operated under ‘Live within your means…live below your means…thrive and prosper.’ Thank God my wife is of the same mindset.

My dad would have disowned me, and/or rolled over in his grave if I had ever refied and walked away with the cash. It’s easy to see stealing from your immediate neighbour is wrong, but the refi walk game is simply stealing from all your neighbours, or the system, or everyone is doing it, etc. Wrong is wrong, imho. And debt is debt, none of it is good, even when it is necessary to get started.

Excellent point, Swamp Creature: this was THE game in San Diego in the early 2000’s before it all went to heck kinda in a straight line. I forgot that part though again this time it’s not one hundred percent financing with lier loans and on dome dreadful adjustable rate mortgage.

@Swamp Creature-

>Refinancing on empty homes may be one of the hidden dangers

>out there that no one is aware of or talking about.

Oh, they’re talking about it…behind closed doors.

Swamp Creature,

Good observation.

What I have seen in a few instances is that people moved out of the city to some other area without even trying to sell their old home, and bought a new home somewhere else. They’re expecting to make more money off the old home the longer they wait. This would account in part for the shortage of inventory (people buying but not selling when they move). If this is broader, as maybe you’re also alluding to, then the shadow inventory might be huge.

I am getting tired of offers from flippers, for my single family houses, in different suburbs! Please, everyone move back to the big cities!

Upon further investigation, with Ms Swamp Creature, I believe the data supports Wolf’s analysis, that the Vets being mostly older Vets, not first time home buyers, are refinancing to get the cash out of their home in the city, and are using the money to either fix up the home while it is vacant, and they are living somewhere else, maybe overseas, or in the suburbs. Or they are permanently living somewhere else and using their city home as an income providing investment by renting it out. So they are owning two homes, or owning the one home and renting somewhere else. The theory that they are just trying to milk the home for all the cash they can get and walk away is probably not the case or only a very small minority. Vets are are very conscious of their credit ratings and which can affect their performance evaluations if they are on active duty.

If you live in Ca you can buy a second house in Ohio out of petty cash. Coming back the other way the comparisons are tougher. Would like to see a regional breakdown of REFI and CC debt.

If you sell your major urban house in Ca and move away for about 5-7 years, more likely than not, you can’t afford to get back into the same area, It is a one way ticket out. Many take that one way ticket out and live happily ever after.

On an entirely different issue: There seems to be a younger generation locked in bidding wars … this is new. Remember? The younger generation was not interested in owning … they did not want to be tied down in a location. They hated suburban. That has changed. Now, they are interested in buying everything, suburban and all. And they have money.

I’m trying to understand this. The only way that makes sense is if the home has no equity to lose if the borrower defaults. If that is the case who is going to loan to that borrower with no equity in the home?

If you get a cash-out refi you would have to have enough collateral in the home to secure the loan would you not? And if you had equity enough to get that loan then why would you walk away and risk all that that entails?

Do banks still ignore loan-to-value like they did when they were packaging loans to resell?

What am I missing?

In the mortgage debacle, loans were made on the fake and the bulk of them really stinky adjustable rate mortgages. This time around, getting a mortgage nearly requires giving blood and my hunch is most of the new loans are lovely fixed rates and at gorgeous percentages. So, while this cash out refi boom does give me the chills, with underwriting standards so rough and rates set, it is at least a bitsy bit different this time. This time, maybe folks can weather any big decrease in their home’s value in practical terms and maybe in emotional terms to ride out the cycle versus needing to bail. Okay current realtor and former loan officer here, starting in 1986. I have seen a lot.

Liar loans were only a small part of the problem in 2008. The vast majority of the people who lost their homes, were telling the truth about their income, and most probably could have gone on making the payments, but when the values dropped far below what they owed, they walked, and the same thing can easily happen now…

When you are mortgaged to the hilt, and then the value drops 100K or 200K the smart move is to let the bank take the hit…

Jdog

I agree with your assessment. Isn’t it funny how most of us were in shock when co-workers / friends with plenty of $$$ who put down miniscule amounts to buy their homes dropped key on their lenders instead of honoring the contract they signed?

It used to be called “moral hazard.” Though it was indeed a multitude of factors which caused the housing crisis, we have collectively concluded the banks and Loan Originators were the scum bags. Hence, NOW dropping key after a cashout Refi followed by a significant price correction is seen as a smart move – contract be damned.

I read an article around 2012-2013 which broke down who defaulted en masse. I wish I could find the article, as I do remember it being well written and researched and a legitimate source….hence why it caught my eye in the 1st place.

The charts and stats in the article clearly showed that the highest default rates/jingle mail among homeowners were people who had 2nd properties/investment properties/vacation homes. These people had better then average incomes/cash flow. They could walk away easily for the simple reason that they have a home they can afford to live in if they lost the investment/vacation/2nd homes.

The other stat which caught my attention were the default rates among the people who had tight budgets or stretched to get that new home(usually lower to mid income people). These people defaulted at a much lower rate than the aforementioned people. The why made sense to me….. it was their only home and if they lost it they were out and would have to find somewhere else to rest their heads at night and damn quickly too. So they kept struggling to make that monthly nut.

Of course there were exceptions to the stats in both groups but the overall trend clearly displayed the trends above

I read the same article as Dave, below. Makes sense to me. I would not be surprised if it happens again along the same lines. Especially seeing techs moving from the city and buying structurally unsound houses for well over worth/asking prices.

“Dave

I read an article around 2012-2013 which broke down who defaulted en masse.

The charts and stats in the article clearly showed that the highest default rates/jingle mail among homeowners were people who had 2nd properties/investment properties/vacation homes. These people had better then average incomes/cash flow. “

I can’t tell you how many people I thought to be ethical that did this during the late 2000s. I suspect the same nonsense going down again with high home prices. Most could make payments but chose to short sale ot foreclose after the had already bought another home.

Can’t the lenders chase them?

I think the ethics comment is in need of further inquiry.

People see corporations and wealthy people default all the time to cut their losses and yet they preach from their high castle how immoral and unethical it is if regular people use the same methods as they do.

Ethically speaking, I agree with the regular peoples take on the double standard.

Shiloh1,

I’m with you…many/most states have “deficiency judgment” rules that apply to the defaulting borrowers…so borrowers don’t get off Scott free…they can and are hunted, hounded, and sued for years following their default.

While a few states don’t allow deficiency judgments…it is a safe bet that lenders hike rates/fees up front to try and offset the increased risk they face because lenders can only go after the falling-value house collateral in those states.

I really don’t get why these “deficiency judgment” rules aren’t better known after 1.5 housing implosions…

Dave,

Yeah, kinda like a “regular person” who somehow developed the “business acumen” of a “C suite person”……or at least a middle manager.

Aren’t there a lot of FHA loans being done with very little money down?

Old School

3% required for FHA down payment. The VA loans are the ones being made with no money down. Leveraged to the hilt. What is not being reported is the massive abuse of the VA loan program. Instead of being used by the Vet to buy their 1st home, as the program was intended, the VA loan program is now being used for real estate speculation, investment property management, renting out illegal accessory units, home flipping, and numerous other abuses of the program. The loans are all guaranteed by the taxpayer. With Covid-19, we cannot even get into the property to see what the collateral for the loan looks like inside, and have to rely on the pictures supplied by the person getting the loan, a clear conflict of interest. Everyone is cashing in on the scam, including ourselves, unfortunately. When we told one of the underwriters about some of these abuses, we were told to shut up and do our jobs, and if we didn’t like it they would get someone else.

I am suspicious that the long term plan is to just back and eventually transfer nearly all bad loans to Fed government because government gets paid to borrow money now in real terms. Student loans why pay 6% when government will absorb it for 1%. Housing why pay 4% when government can borrow for 1%.

It would be interesting to compare the default rate on FHA, VA, and conventional loans in the 4th quarter 2020 vs the 3rd quarter. A continued negative trend would be a signal that we’re heading for another 2008.

Default rates distorted by extend and pretend mortgage forbearance.

FHA delinquencies, including mortgages that were delinquent when they entered forbearance, have been roughly stable at just over 17% since summer. Not getting worse. New delinquencies are lower than a few months ago.

Once this starts to trend up, I suspect the siren sounding will already be too late. 17% is no small amount either though.

The current 17% delinquency rate of FHA mortgages is catastrophic — the worst ever. Without the forbearance programs, all heck would have broken loose.

But the 17% is concentrated in lower income areas. High end areas don’t seem to have a problem. So, the gap will widen between the rich and poor. These things happen when you outsource high paying blue collar jobs …

I get worried when I hear the word “stable”. It avoids making a judgement about being good, bad, or terrible. Dead people are stable.

SocalJim

Higher income people don’t go FHA. Lower and lower middle class people do. That’s who are targeted for foreclosure and repossession. Also, upfront fees on FHA are huge.

It would be interesting to know if the amount owed among that 17% have risen significantly since summer….

con$umer con$umer con$umer con$umer con$umer ….

but never a “CITIZEN” mentioned!

Says it all, doesn’t it. I wouldn’t weep a single tear if this Econoworld of ours sidled over the event horizon of a depressingly black hole of deb … taking Jerome and his ilk, Wall$treet and the rest of the so–called ‘markets’, and assorted Billionairians like Cardigan Billy, Krampus Claus with it!

‘depressionary’ black hole of ‘debt’ …

Hey, use both words and make it “depressingly depressionary”!

And keep “deb”. After all, it is just maintenance of the dutante class and “Rich Wives Matter”.

polecat,

Haven’t you figured out that your sole function and job is to “consume?” If you can’t or don’t want to consume, they’ll throw you out :-]

How we are raised by our parents plays into that thesis. My sister and I were taught that the way you ‘win the game,’ was to consume as efficiently as possible.

Spending money is OK, but one must get the most return for every dollar spent. Kids from the pre-WW II depression were almost all raised that way, and Mom used that lesson to teach us. Thanks mom!

I have more than I will ever spend now that I’m retired and set up fairly well, but I am still as thrifty as I was decades ago. I see the same traits in my nieces and it makes me happy knowing that they’re wise about spending.

What’s missing from your story was most of your big returns were driven by people raised the other way. The stock and the bond market didn’t start jumping until people lost their money sense.

In order for there to be winners, there will have to be losers. Make sure to thank the later as well.

There’s a point to be made there. However, we work to produce. If what is produced is not consumed then why do we work? Do you dig holes for fun? If everyone was utterly frugal and never spent, inventories would pile up, services would go unused, and the companies the same frugal people work for would go bankrupt or suppress wages. Then everything would slowly go into a deflationary collapse.

In reality most of what is produced is ultimately consumed by someone. If, sooner or later, you do not consume the fruits of your own labor then that means someone else did it for you.

Today, I did spend, although my purchase is on order from the manufacturer and the check’s not been written yet.

Just over four grand on a pair of home audio sub-woofers. And from a brick and mortar retail house – not from the internet. Could have spent much, much more, but I believe got the best quality for cost with the choice I made.

Engineered and assembled in the USA!

Last comment, I promise, but I should have written: Engineered and manufactured in the USA. All parts designed and built in-house (Florida).

Rhodium,

How is someone never going to spend? They suddenly are able to produce natural resources for themselves to make everything they want? Plus they have all the time in the world to farm their own food?

Never gonna happen and nothing wrong with being frugal. The economy will shift towards the needs of the frugal and commerce will go on. As opposed to the current wasteful lifestyles promoted by hucksters (aka influencers), marketers and the government with free money. Things will eventually stabilize to where they should be based on real demand.

Thank you SO much for posting that Wolf!

Been trying to get my overly thrifty spouse to understand that for eva, and due to her respect for your economic wisdom, maybe, just maybe, we, ( that’s the you and me ‘we’,) will now be able to carry the day!!

Polecat,

According to Paulson the former Treasury Secretary from Goldman Sucks, you are nothing but a “Taxable Unit”.

Enjoy

Yes Wolf, it’s as old as the Ages. If ol’ L. DaVinci were kicking it today … he’d be describing us all as tubeworms, as he curmudgeonly did of those within his social sphere – the King’s court @ Versailles!

Cheers .. I guess

Yep, and the homeless are there to show you what happens to those who “can’t consume”.

But they are still “citizens”.

You know, free and have rights and all that good stuff.

Maybe because we are the reserve currency and consumers for the world we have raised a lot of financially illiterate people. I was broken down physically and mentally from working at age 48. I did a little part for two years after, but no work after that. I lived the next 14 years on a next egg that has doubled since then and I really lowered portfolio risk four years ago as things started getting pricey.

How did a do it? I knew my max draw down rate and cut and cut and cut til I got there. That means living in places 98% of Americans wouldn’t choose to live in. But you can clean it up and put a fresh coat of paint on it all. Too many Americans don’t understand the power of investing or the trap of consumer debt. It bothers me that government gives carrots and sticks for the wrong behaviour.

@OS – what sticks? I haven’t seen any government sticks lately. Just carrots and more carrots and even more carrots followed by carrots and free carrots.

We stopped being Citizens when we became derelict in our duties as such.

Being a Citizen requires certain duties and responsibilities that the American public reneged on decades ago… We just witnessed the most dishonest election in history and yet where is the outrage? There is none. Just peasants with their hands out for another government free lunch.. Placated by bread and circuses….

Yeah, I miss the circus, too. The real thing was much funnier than the comedians who tried to duplicate it.

Other than that, I just try to forget almost half of us derelict citizens want a 4th Reich.

It was a very wise move for the govt to give trillions to the voters, who could then give trillions immediately to the banks. Much better optics than sending trillions directly to banks like the last recession. I thought I took a risk buying multiple banking stocks last year thinking they would come back in two to three years. But thanks to govt stimmi checks (which get sent directly to the banks), they are up between 40-73% each. We all “win” I guess, even if we don’t get free stimmi, the fiat paper gets passed around and most likely ends up in the hands of the top 10% of society. Now if that was true, that would be bad optics…but lucky for govt, current American life is so distracting, complex, and overwhelming with too many unnecessary choices…few have the time to research, study, learn, and understand the mechanics of how govt and Wall Street really work.

Concerning houses, CNBC had an article, showing an all-time high of $347,475 for newly listed homes. Wow, $350,000 use to be a lot of money just a few years ago. It would seem that $350,000 is chump change for Inflation Nation USA.

I just checked and Zillow showed my own house value went up 4.25% in the last month alone, which would be 51% on an annual basis. My neighbors are selling for 40-50% over list right now, my area has entered bizzaro land. The irony is the Fed has created a zero sum game of hot potato asset inflation, as where are you going to move to find that “cheaper” house when if you sell your inflated you are in right now? Perhaps that is a big reason why the inventory of available houses across America is at record after record after record lows???

I feel for those who do not own, and the younger generations who will have to get 50 year mortages to buy houses in the future if this grand Fed inflation experiment works, and by working I mean screws everyone except the top 1% of asset owners. I don’t think it will work long term as voters will only take so much inflation pain before they revolt at the polls (already has been happening these last two elections), and make changes to our society in the near future that would be unthinkable today. Push the majority too far and too long like a gigantic pendulum, and the majority will ultimately push back, most likely quickly and too far in the opposite direction. So enjoy it while it lasts, for last it can not…

Per CNBC today:

The tight supply has only made sellers more bullish on their potential gains. Asking prices of newly listed homes hit an all-time high of $347,475 in February, according to Redfin.

Sellers have plenty of reason to feel confident. Redfin also found that just over half (55%) of homes that went under contract in February did so within their first two weeks on the market.

Great observation.

Gov sends out checks, citizens pay down CC-debt and currency ends up at the banks.

Politicians scream it is all for the ones who need it. Following the money, we see who apparently really needs it. The banks. The risk of the loans is transferred from the people and the banks to the Gov and now every tax-payer has to pay for the burden of the debt. That’s very social(ism) of the Gov. I wonder if all tax-payers agree with their participation in this scheme.

The consumers are simply the middle men between the government and the corporations and banks.

They got some crap in the last crisis for giving the money directly to them, so now they give it to the consumers knowing in a matter of days it will end up in the accounts of the corporations and banks anyway. The consumers will end up with nothing of any real value in return. They will however at some point in the future have to shoulder higher taxes to service the ever growing debt.

If voting changed anything, it would’ve been stopped a long time ago. Team A and Team B work together to make sure no Team C can ever take hold. Democrat lawsuits all across the country to keep Ralph Nader off the ballot come to mind.

Armed rebellion inevitably ends in mass death and suffering with little or no improvements in living conditions for serfs. Unfortunately dear leaders are working overtime to wreck the lives of people involved with the January “invasion” of Congress, thus guaranteeing the creation of guerrilla fighters. That seems to be the intent, to justify more repression. When people are treated like “terrorists”, they will become “terrorists” as a matter of survival.

At this point the best strategy for working people is to help each other weather the storm and prepare to build a better society after dear leaders finish burning this one. Of course that means consciously working to overcome the divide-and-conquer strategy known as “identity politics”.

So far people prefer to push to the front of the queue and shout “I’m the biggest victim – *I* should be in charge”. That attitude won’t get us very far, and I’m not optimistic it will change anytime soon. It is already a very rough ride, and likely to get much rougher, I am sorry to predict.

Actually, the American Revolution resulted in a huge improvement in both living conditions and the upward mobility of the average person.

At least until 1913 when the Monarchy was reinstated….

Really?

Why isn’t Tom Paine considered a founding father? He did more to drive the actual peasant combat in the revolution than Georgie ever did. Most read USA author per capita EVER, as in EVER.

No statues nowhere. No quotes, no nothing.

Must not have fit well in our new master’s agenda, eh?

History is written by the victors, ya know?

“So far people prefer to push to the front of the queue and shout “I’m the biggest victim – *I* should be in charge”. That attitude won’t get us very far, and I’m not optimistic it will change anytime soon.”

That sentiment has been manufactured as well to the detriment of us all. Divided. They are very very good at that, and manufactured division will increase as the fear of pitchforks increases.

Realistically on this reactionary level of division the only thing that can manifest is mob mentality.

– Perhaps people see that rates are rising and decide to refi before rates go higher ???

Yes, same with purchase mortgages. At first there is a burst of activity “before rates go even higher” and then there’s the slowdown.

None of this ends well for the banks. What am I missing with this story?!

The banks are similar to “made man” status w/always being protected [@ any co$t].

Re “it’s good to be a gangster” [Ghetto boys video of decades ago].

The Have and Have Nots…Madame Defarge is knitting away!

This is a question of how far the balloon can expand pay attention most stimulus money is pork very little to people who really need it most people’s problems they buy at top of market follow warrens advice u will do well of course this will end badly then when it crashes rich swoop in buy for.50 cents on 1$ always rinse and repeat except interst rates crashing party

As a consumer bankruptcy attorney, I wonder if consumers are really paying down credit cards, or if the balances are not “written off” by the credit card issuers. Generally this means balances with 90 day delinquencies are sold off for pennies on the dollar to debt buyers. This could show up as a reduction of outstanding revolving credit. It is hard to believe that the 70% living paycheck to paycheck are paying down anything.

Delinquency rates on credit cards have plunged during the pandemic (as well on other types of credit). It seems many people who were late used a stimulus payment to get current.

Housing is being bought as an inflation hedge.

Unless our “right thinking people “ get credible about not letting inflation get out of control instead of promoting it every time they get a chance, housing and other assets will continue to appreciate.

The only thin more hateful than Trump telling me for 4 years how great he was, nowadays it’s Powell with his almost daily appearances telling how concerned he is for my welfare while keeping interest rates below inflation on my meager savings and at the same time trying to gaslight me about how more inflation is for my welfare .

Those planning to just “walk away” might want to review that pile of papers they signed at closing. Unless you live in a “non recourse“ state it might not be that simple. I’m thinking they addressed “strategic” defaults after the last market meltdown extravaganza. Judgements may follow you home especially if you have the means to pay.

Looser rates can help build ships,

And looser lips can sink ’em,

But all we fear is wasted beer,

So c’mon y’all and drink ’em!

J. Edgar could only have dreamed of great source like Wolfstreet. One rolodex card for each article that spills the beans.??????

Am I the only person who actively wants America to collapse at this point? I figure let’s get it over with while I’m still young enough to help rebuild.

Look at photos of the desperate refugees at the Mexico – US border, or the refugee camp on Lesbos, or any refugee camp anywhere. That is what our future looks like, maybe for a very long time.

Is that really something to cheer for?

One man’s vision of collapse is another’s projection of an opportunity to right some wrongs. He says he wants to rebuild. Is it any worse that what is being set up on the path we’ve been on. If the road you followed brought you here, of what use was it?

Correct. I feel like it’s more selfish to put us on a road to hell and to expect one’s children and grandchildren to clean up the mess.

I do not think anyone really wants to see America collapse, it is just that some of us have realized it will not get any better until it does…..

Yep. We won’t make hard decisions until we have to.

“We” (as in US peons) don’t get to make policy decisions. Our superiors know what’s best, according to them. And they like things the way they are (more or less), so there will be no decision to change course. It will be straight into the wall at full speed.

I am sorry that people my age were not able to stop the insane policies of people my parent’s age who refuse retire from the ranks of active Dear Leaders.

The former USSR and East Germany had the same problem with decrepit leaders who were advised and deceived by dishonest butt kissers. We all know how that ended.

It won’t end well for us, either.

I want the top half to collapse. The rest of the economy already has. If the top half follows suit we have less homeless people and more first time home buyers.

If the top half follows suit we MAY have less homeless people

I remember reading an article circa 2007 that Californians bought new cars with HELOC funds @ 3x the rate of other states, so we know the drill, borrowing from the first national bank of your home.

Consumers are paying down their credit cards so they can qualify for a larger mortgage. Real estate is smoking hot … hotter than it has ever been at the beach in SoCal. In Ca, the only real estate that you don’t want is in the SF bay area … especially in SF county. Everywhere else in Ca is hot.

Dude! You’re insufferable!

polecat, I am just telling you what I am seeing. It is very hot. The risk is an overheat … This is just crazy.

Vacant lots still aren’t worth spit. Not that I get out much but I don’t see any projects, notification of intent, except for commercial. City puts it money into improving busy secondary roads, the franchises follow, ca ching.

Ok, thanks for replying. Took your comment as a kind of schoolyard taunt. My apologies – and yes, it always seems .. hottest before the ice storm approacheth ..

There is not a commission he does not like.

America has slowly become a moral cesspool over the last 35 years or so. Just look at pop culture. Now it’s in finance. Anything you do is alright as long as you “win”. Corruption at the top filters down. The crooks at the top never go to jail so I guess I’ll be corrupt too!

That’s the best explanation of how this mess has progressed. Should be on a billboard, exactly as written, at the highway’s edge of every town…right next to the one that reads “We’re all in this together!”, just above “Re-finance now. Low Rates.”

Everybody is Michael Burry nowadays.

Burry had solid data in front of him. Mortgage Bonds. MBS.

Hands up, who looked into those Bonds here? Who knows Delinquencies rate on them?

Las time Adjustable Rates triggered sell-off. And Burry new that. What exactly gonna trigger sell-off now?

Last time banks been exposed deeply.

Last time we had Liquidity Crisis.

Now we swimming in the Ocean of Cash.

Just like generals, who always prepare for the Last War, you guys expecting exactly the same Crisis.

Exactly the same !

The first chart is the percentage change in the average(?) balance but not the change in billion$, yeah?

I was in debt for 30 years and finally had enough…been debt free for the past 7 years.

When you refuse to carry debt for any purchase you begin to realize how hard it is to spend cash as opposed to just signing yet another loan document.

Spending hard earned cash is truly painful unless it really adds value. I used to borrow money impulsively like so many people I know. Good to see others pay down debt and build a better life for themselves.

I used a similar tactic to train my children when they were young adults. They both had a “debit card addiction problem” and would buy the most ridiculous things on impulse. Then they’d complain they were “broke” and demand more allowance (they were in college).

So, I asked them to carry cash for a month… and buy nothing with a debit card. Their attitude towards what they bought changed when they had to crack a $20 bill for the latest beannie baby. They thought better of the purchase and passed. Later in life, it became more meaningful as they earned the $20… not mooched it.

The lesson stuck with one of them. The other? He has to live on an “allowance”…. otherwise there’d be a smoking hole where his bank account used to be.

I recall the quite successful entrepreneur father of a friend. He had no problem with taxes set by his representatives. However, he wanted, every payday, a row of tables in the cafeteria. At the first table everyone would be paid their wages in cash folding money. Then they would work their way down the row, paying each tax in cash. He felt it would change workers’ attitudes about taxation.

I know several people that cashed out refinanced in Q4 and put all of that money in the stock market. Borrow at 2.5% and make TSLA/BTC bank!

YOLO!

Heard that on the local Radio station here in the Swamp. WMAL, on Sat 1PM, Network Capitol Funding based in Irving CA, pushing cash out refi’s to speculate in the stock market. Their phone’s are ringing off the hook.

By the way, we did an appraisal for them about a year ago, and they took over 6 months to pay the bill. Total crooks.

I wonder how much of this debt payoff is small companies getting government loans in the last year, and using that money to pay off business credit card balances? It feels a lot better to owe for a Small Business Loan, than for credit cards. I did this, and I know someone else who did also. That would skew a lot of numbers. You still owe the money, but it was just shifted to another type of debt. So the economy is not better off, it just looks that way.

I am a dinosaur. In preparing for retirement, I paid off my home, put cash in the bank, use only 2 cards sparingly where I can pay them off completely every month. Not beholding to banks or CC firms. Like I said, I’m a dinosaur.

Now that I am retired I can see the wisdom of throwing excess stuff overboard. Government has set tax policy up where with social security plus $1000 or $2000 investment income a month the tax burden is very low but if you need social security plus $5000 to keep it all afloat it’s going to cost you in taxes.

You’re giving me visions of a horse trader who packed the herd on the ferry at Cash Point, only to discover midway in the river that the next landing is at Digital Cove. The G-man is waiting and hungry as his watch nears dinnertime hour. So much for the Ponderosa. Maybe keep enough good stock for small healthy ranch. Toss the rest in the water and pray that distracts the Indians, miners, and highwaymen long enough for you to get away.

Except for the IRA/401k Required Minimum Distribution that kicks up your taxes. In my case the IRS takes the entire RMD and more. I never see any of the $$ from the retirement account. The 2019 tax changes increased my tax 200%.

Purveyors of debt are legalised drug dealers.

They sell a quick fix in exchange for long-term pain.

Don’t do it if you can avoid it.

It’s not rocket science. 2 people with identical lifetime earnings. Borrower is minus all interest paid. Saver is plus all interest received. A no-brainer. Exactly.

– Consumers paying down debt ? This is called DEFLATION !!!! And people are still believing the future will be Inflationary ????????????

Max K calls it ” Interest Rate Apartheid ” which, I think, is a very neat description of the phenomenon.

Carry on the good work