Credit-score algos got fooled by forbearance. Weirdest economy ever where no one knows what’s going on anymore.

By Wolf Richter for WOLF STREET.

So what happens to debt when borrowers stop making payments on their mortgage, credit card debt, auto loan, or student loan, and the lender puts the delinquent loan into forbearance or into a deferral program, and notes the loan as “current,” despite past-due payments, because there is no payment due this month since the loan is now in forbearance? Well, the algo of credit bureaus, such as Equifax, sees that the borrower who was delinquent has “cured” the delinquency and has become “current,” and it then raises the borrower’s credit score. A brave new world, but here we are.

Delinquent loan balances have plunged across all loan types, as these delinquent loans have been moved into forbearance or deferral programs, according to data from the New York Fed’s household credit report for the third quarter.

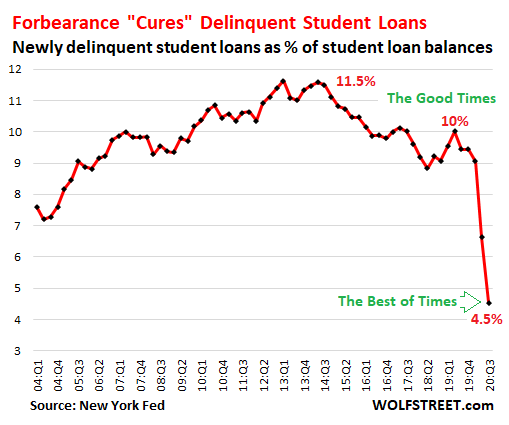

No Payment, no Problem for Student Loans.

The percentage of student loans that are 90 days past due plunged from 11% of total loan balances before the Pandemic to 6.5% in Q3 2020. And the percentage of newly delinquent student loans plunged from 9.4% of total loan balances before the Pandemic to 4.5%, by far the lowest in the data going back to 2004:

Student loan forbearance – the program also included 0% interest on outstanding balances and cessation of collection efforts – was originally scheduled to end on September 30 but has been extended through December 31. Now among student loan borrowers, the hope of student-loan forgiveness has turned into a feeling of near-certainty, and to heck with the idea of making payments even after the forbearance programs ends.

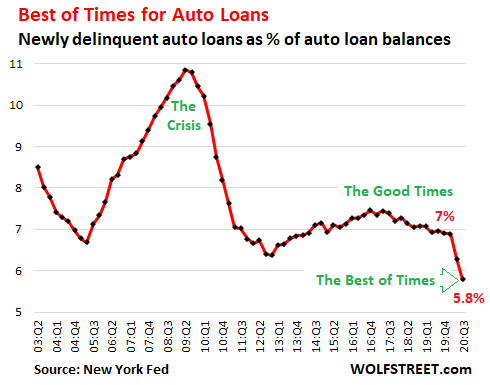

Best of Times for auto loans delinquencies.

Auto loans are not backed by the government, and the deferral and forbearance programs have been implemented by private-sector lenders and loan servicers. Newly delinquent auto loan balances dropped to 5.8% of total auto loan balances, the lowest in the data going back to 2003. Note the delinquencies of auto loans during the prior crisis, when they exploded into the double digits. But this crisis now is the Best of Times:

With auto loans there are two factors: Voluntary loan deferral programs by private-sector lenders and government cash sent to households.

In terms of lenders, for example, Ally Financial reported last summer that in its second quarter about 21% of its auto-loan customers were enrolled in its deferral programs where they would not have to make payments for 120 days. The programs ended on September 30. For its third quarter, Ally reported that 8% of the borrowers exiting its deferral programs were 30 days or more delinquent.

In terms of the government cash sent to households, this included the $1,200 per adult and $500 per child in stimulus checks, plus the extra unemployment benefits sent under federal programs, including the extra $600 a week through July, then the extra $300 a week starting in late August, plus the other special federal programs established under the CARES Act, including the Pandemic Unemployment Assistance (PUA) program that has been surrounded by fraud allegations. This government money helped many households keep their auto loans current.

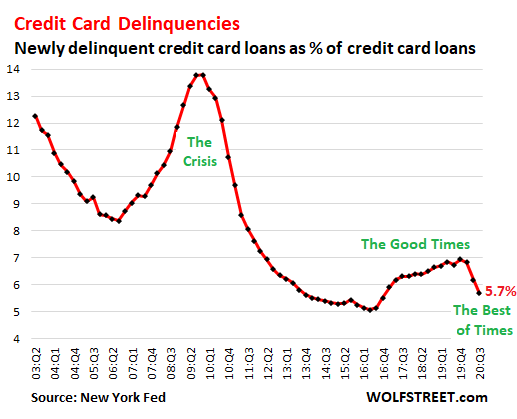

Credit card delinquencies also plunge.

In this era of deferral programs and government cash sent to households, newly delinquent credit card balances also dropped during the crisis, instead of surging, as they did during the last crisis. Credit card delinquencies had been on the rise since 2016, during the Good Times. Then the Pandemic and the unemployment crisis hit, and surprise, instead of spiking, newly delinquent credit card balances fell to 5.7% of total credit card balances, the lowest since 2016:

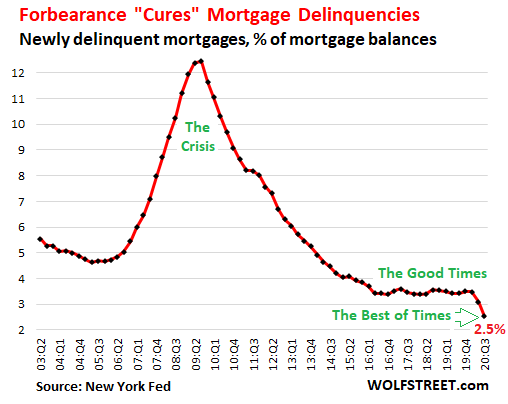

Forbearance pushes mortgage delinquencies to record low.

The government guarantees or insures the vast majority of residential mortgages issued in the US, and these mortgages became eligible for forbearance programs under government rules, which provide forbearance for six months, extendable for another six months, so in total for a year. These borrowers can live in their homes without making a payment for one year. When borrowers who have fallen behind on their mortgage enter forbearance, the lender can choose to mark the loan as “current.” This “cures” the delinquency though no catch-up mortgage payments have been made. Newly delinquent mortgages therefore dropped to a record low of 2.5%, despite the crisis:

Who are the borrowers seeking forbearance?

The New York Fed looked into which borrowers relied on forbearance to deal with their mortgages and auto loans and found that borrowers that are now in forbearance had lower credit scores and higher outstanding balances in March before forbearance, than had non-forbearance borrowers:

- Auto-loan borrowers now in forbearance had an average credit score of 652 in March, compared to 693 of the non-forbearance borrowers.

- Mortgage borrowers now in forbearance had an average score of 708 in March, compared to 754 of non-forbearance borrowers.

- Forbearance participants had outstanding balances that were about 30% higher for both types of loans in March than those not participating in forbearance.

Confused algos raise credit score of borrowers with delinquent loans in forbearance.

The New York Fed found that for both types of loans, “troubled borrowers were far more likely to opt in to forbearances as evidenced by the higher delinquency rates of participants three months prior to the first forbearance month.”

But then, once the delinquent loans are in forbearance, lenders mark them as “current,” and the delinquency is “cured,” as seen in the charts above, which the New York Fed also noted.

And this curing of the delinquent balances by moving the loans into forbearance has a salubrious effect on the delinquent-but-not-delinquent borrowers’ credit scores.

The New York Fed found that, “On average, delinquent borrowers whose loans were converted to ‘current’ upon entry into forbearance saw an average 48-point increase in their credit scores (here, Equifax Risk Score 3.0).”

But for borrowers who were not delinquent when they entered forbearance, their credit score was unchanged.

Yup, the algos that Equifax and others use to arrive at their credit scores, and that lenders rely on when they extend new loans, got fooled, and these algos improved the credit scores of borrowers whose delinquent loans moved into forbearance while they did not change the credit scores of borrowers who were not delinquent. Just another distortion in the Weirdest Economy Ever, powered by government-sponsored loan deferments and government stimulus payments, where in the end no one really knows what’s going on anymore.

My 13 whiplash-charts on retail sales by retailer category. Read… Stimulus Fatigue? Retail Sales Wane at Many Brick & Mortar Stores. Department Stores Progress to Zombiehood. But Online Sales Surge to Record

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The banks will not get fooled though. Presumably they have a better picture of what’s going on. The question is more whether they will relax their lending standards and use the “improved” score as a convenient excuse.

don’t forget all those FHA loans in forbearance

around 17% of all mortgages currently in forbearance

and

FHA PROHIBITS THEM FROM SELLING – don’t want to flood market with NO EQUITY SELLERS

What kind of MBS has the “Federal” Reserve bought at way above FMV prices to bail out their bank owners – -$892 billion reportedly this year out of about $2 TRILLION total? FHA loans?

I think that foolishness will delay federal until our legitimate, medium and smaller businesses have failed. Prepare for an avoidable economic, self-inflicted, economic disaster!

I meant federal aid, since only banks and some, few cronies have gotten aid.

So what happens on January 1st!? Everyone becomes delinquent again??

Dear Christopher Spisak,

I try not to think about what happens when (as appears inevitable) the evictions can resume again, no federal aid is forthcoming, the health provider financial trends and other expected, foreseeable catastrophes occur. I recommend that and wine.

Lots of good wine. If you do that, weed is now legal in California. That might also help as will watching those online comedians smart enough to do gallows humor.

I handled evictions for a few months long ago, when I represented huge corporations for many years, before my strict, religious upbringing, fear of hell, and sense of guilt prevented me. I am now considering handling business evictions and collection work — no hungry widows, children, or families to make homeless. However, I doubt that I can.

The business will be booming for most lawyers. I fear that I am now too sentimental to profit off of my countries’ oncoming catastrophe with the other lawyer-vultures. Despite my children’s foreseeable college extortion-tuition payments, I sure hope that the majority of business owners realize that filing a bankruptcy case can help them restart.

That way, I can say to myself that I am effectively a fireman. We will need lots and lots of firemen.

Joe, I specialize in foreclosures and can tell you unequivocally, it’s going to make 2008 look like a walk in the park.

This time there will be a huge commercial component coupled with the residential aspect.

Remote working is here to stay and all that empty space in the cities will trickle down to local businesses (if they even manage to stay alive). So no more foot traffic for bars, gyms, hair/nail salons, restaurants because no one will be going into an office any more. The flight from the cities has begun and will continue.

Realestatepup:

So what advice do you have for us?

“Creative truth telling” [intelligence community trademark] in play amidst the smoke & mirrors of accounting transparency.

Also under MMT, everyone is always credit worthy. We are rapidly approaching the MMT Inflection Point!!!

Like the true inflation or unemployment rates?

Wolf,

You have to get use to the new economy where we build back better. The old system of debts and credits are obsolete and an affront to human dignity, everyone should have good credit scores, everyone should be able to afford food, housing, and other stuff at reasonable pricing. We should no longer be beholden to banks and their corporate interests. They have robbed society for far too long. It’s time for a societal change, a permanent shift in our economics. We will start by building back better.

With that, I believe we must introduce perpetual moratorium and put in permanent injunction against evictions. After all, human dignity is more important than dollars. Out with the old, in with the new.

Hehe, I think this could be a start of a manifesto or something, can someone who isn’t as lazy as I am write it up?

https://en.wikipedia.org/wiki/Building_Back_Better

The concept came from …. Japan. The US has officially run out of ideas, we now have to steal taglines from other countries.

I am looking for the AAA plan… you know… Assholes Act Alone…

I know, it doesn’t even make sense, but I am too lazy to think of anything more intelligent.

LOL, nice. You had me going for the first paragraph.

The manifesto on perpetual moratorium and a permanent injunction against evictions was written in 1987. It’s called “The Art of the Deal”.

And that was one wonderful book, made the best sellers list somewhere too, I heard.

It is so good that it might become a seminal text like Art of War, where it is referenced centuries from now.

Sound like socialism.

It’s called EQUALITY. Say it with me… EQUALITY. This is not socialism… don’t confuse EQUALITY with socialism.

Wait, are you against equality? Are you against justice? Are you against build back better? What are you? A [insert your favorite current political insult here]…

?

Good point.

Equality, equality equality…. repeating ?

I will call Mariam-Webster dictionary to change the word to Equality

First thing First,

Immediately, we must correct the credit scores of those NOT in forbearance. Their scores must be raised to the equivalent, OR higher, of the borrowers, who are in forbearance.

It’s time to stop holding anyone to a higher standard. All men must rise together, despite their labor of sacrifice!

Re “we must correct the credit scores of those NOT in forbearance” does anyone seriously believe the banks have no way to separate the wheat from the delinquent chaff? (though it does raise the question as to whether enormous crony loans are being forgiven with a wink and a nod.- incidentally, is forgiven loan not regarded as income by the IRS?

Minimum wage needs to be raised to $50/hr.

And bread should $ 45.00. The Weimar Republik started that way.

A man went to buy a loaf of bread with a wheelbarrow full of Money. While in the store somebody stole the Wheelbarrow and left the money.

Man had a very nice expensive dinner, asking for the check when he gave the waiter his order. Took his time. When he finished he sold his empty wine bottle to the waiter for the price of the dinner.

We were first told that government debt didn’t matter, then corporate debt, and now private debt is being deferred or in forbearance.

As a prudent person, I have been made to feel quite the fool. I never believed extend and pretend could become permanent policy. Debt is the new wealth! I should have been indulging myself for the past 30 years.

You coulda been President!

“President of what?” –Snake Plishkin

Actually…

“President of what?” –Lillian Carter to her son, 1974

Rumpled Bemused,

I would be pretty mad as well, if I were to remain financially responsible and all debts were suddenly wiped away/eroded/not enforceable. I need a warning first, and then I’ll get a loan for an expensive car.

What’s the use of credit if you can’t use it?

If one doesn’t own a house, or have money in the bank, charge everything to the hilt. Assume the debt will be forgiven. When they demand their money, ask for ongoing forebearance, or offer them a dollar a month.

It’s a civil debt, as long as the credit is in your name with no funny business, there’s nothing they can do but seize your used beater and your stuff, which ain’t gonna happen.

Your credit score will go down? The HORROR!

Wolf:

I want to know is what happens when the music stops. If all of that debt is just being deferred, and we stop deferring it on January 1, what happens with the debt overhang? Will all these borrowers suddenly fall into default on massive number of mortgages and car loans and credit cards and how will that impact the debt holders. Is it possible to extend the delay and pretend strategy for another year until conditions improve?

Anton,

“I want to know is what happens when the music stops.”

Yes, everyone wants to know :-]

Wolf,

Excellent, excellent distillation of the “forbearance fraud” problem.

Some thoughts on where/how to get out front (if only slightly) of the revelation of the true delinquency/ultimate default numbers.

1) Declines in creditor cash flows.

Banks and other creditors can play classification games (abetted by “regulators”) but they can’t hide (I think) the fall in inflowing cash due to delinquent/forborne/whatever “walking dead” loans.

The FDIC has fairly granular aggregate level metrics (and at the individual bank level too).

So aggregate cash-flow-from-loans drops yr over yr may reveal something closer to the truth.

And since the Big 4 banks dominate the industry so much at this benighted point, taking a look at Wells and BoA’s specific financials and FDIC filings may turn up the truth (Citi is more of a bank for intl loan f*ckups and JPM is more of a front operation for the G to fix/hide f*ckups).

2) Certain classes of creditors might be more incentivized/obligated to report more accurate numbers in real time, rather than gaming the classification system. For tax write off purposes for example, taking the loss today vs. tomorrow is usually more valuable. So I wonder if “family offices” might be first to honestly recognize losses…but their info isn’t public generally.

Maybe ETFs/closed end funds holding loan portfolios, might have to be more truthfully mark to market because of fiduciary liability (and no FDIC wink-and-nod) and tax write off benefits.

Maybe others can think of institutional investors with publicly disclosed data that have less reason to hide their true current state.

> 1) Declines in creditor cash flows.

Yup, that’s all that matters. You can see it in eurodollar futures OI… down by like 20% y/y… and you can smell it in china with “AAA” rated corp $ denom bonds going into default overnight… like you said, they can play classification games… but nothing smells like insolvency more like overnight “AAA” defaults lol

I think we all know deep down that the music can not stop, and so it will play on.

Just another movement in the symphony that began with perpetually low interest rates and infinite C.B. bond purchases.

Don’t worry, it’s only money.

The one thing I don’t expect is that most of the “forborne” debt will ever be collected. Including back rent.

You didn’t discuss, but also in forbearance are 6 months worth of Social Security contributions that are supposed to come due in January. IMHO that money is unlikely to ever be collected either.

That only effected government workers, I suppose if they all retire in the middle of December, they might be able to escape the catch up payment.

Old Engineer,

Probably true, but, it vary by type of debt, I myself will push off paying taxes until the mid April date approaches, because, I expect that by that time, if not earlier, they will eliminate those back social security payments; and possibly have other tax benefits. Unless, there is a early cutoff date for tax relief, even if you have the money, it might pay to wait.

Right now social security payments are supposed to be paid in January, but, at the minimum, i’d expect they would let you wait until you file taxes. Waiting could be the right move.

Most unpaid rent is definitely not getting paid.

The Party os over!

My guess it starts 2H21, plenty of dry powder ready for REOs in my zip code.

It only depends on if you have a chair or not when the music stops. But not to worry, we just need to hold out until January 20th, build back better will save us.

And also, I have a bridge to sell too.

Does that bridge happen to cross the East River in New York? I’ve been looking for a bridge like that for a while.

Even better, across the bay between SF and Marin County. The traffic volume is great even today.

I would prefer an escape boat than a chair. Remember Jack and Rose?

Got to have cash when the music stops or you will be trying find a friend to loan you some.

Physical cash?

Perhaps… but at the rate our currency is devaluing.

Klaus Schwab, Great Reset

We are witnessing a World Bank coup of all classes except Big Tech Big $$

I understand it is starting in NYC. De Blasio is clearing out all the riffraff through bankruptcies and mob violence; and Cuomo is bringing in Schmidt and crew to start the rebuilding and rewiring – for the selected.

WorldEconomicForum,I believe has a whitepaper on its site recently published by Global Research.In the paper various hopes,dreams,ideals,goals,projections are laid bare including the percent of online workers,unemployed,nononline jobs,etc. Scary to me given what I Know,see,hear in today”s Insanity.

1)permanent growing underclass/serfs.Many rich get richer especially Goalongs and Getalongs.2)More of the concentration of $/power.3)More widespread,invasive Nannystate/supersurveilance,a.k.a HART-U.S.HomelandSecurity.Trackable,never anonymous digi$,5)Less human rights,6)Green NewDeal/forced austerity/less meat/eat bugs-labmeat.Canada has docs online saying debtforgiveness+take tracking dangerous vacc.+healthpass=sort off more freedom,but surrendering of all “assets”,whatever may be deemed as such.Not making this up!

sounds interesting – could you point to this paper?

If Biden actually takes the white house and the dems win the senate in January then you can expect 2021 to be the year of extend and pretend. Many, if not all debts will be paid off by the US Treasury. So, borrowers and lenders will both be made whole.

If Trump should keep the white house or republicans stalemate the senate and congress, then you can expect little, if nothing to be paid off. I’m really not sure what Biden can offer a Republican senate, since Biden supposedly wants to do something and the Republicans will want to do nothing.

Note my use of the word ‘supposedly’. The Biden/ Obama White House did a whole lot of nothing for 8 years and managed to actually shrink federal spending between 2010-2015. They could have past progressive programs, but the truth is they’re almost identical to the republican party. So, I expect Biden to be much more happy with doing nothing, rather than have to pay off the debts of his indebted voters.

The sad fact is that you would have gotten instant stimulus if Trump had been re-elected.

All politicians are selling the same products, but each is using a different sales pitch. You buy the story you prefer.

Biden will reestablish the Seniors’ Catfood Commission and will slash social security and medicare payments for austerity, because after all, someone has to pay for the bailouts.

https://www.laprogressive.com/catfood-commission/

Kitty tuna is almost as good as people tuna, and is a lot cheaper. It’s amazing what one can do with a fifty pound sack of dog chow. Pro tip, big warehouse chains have damaged packaging blowouts where one can load up on months of food cheap, as long as you can fight off the animal rescue nuts.

I don’t really think you want to know……

If investors are prepared to accept zero real interest rates then there is no problem. If I have a magic rock and sell it to you for $1m, but the interest rate is zero then there is no issue as long as we are all happy to keep rolling over the debt forever. In fact, you just have a stupid rock now and I can prance around saying I’m a millionaire and pretty much nothing else has changed.

Unfortunately, as much as I’d like to believe there will be a day of reckoning, the real impact of these stupid financial policies is the slow decline of the real economy. Look at where all the top graduates go every year – finance and ponzi tech firms. When your system is deploying its best and brightest into the real economy you get the golden years of economic development after the war. When they are deployed into casino economy jobs, you get stagnant wages, rising cost of living and infrastructure that is falling apart.

There is no risks, the tulip prices will go up much higher, because there are more rubes willing to pay

Four words to strike fear in heartbeat of Democracy:

Klaus Schwab: Great Reset

How about

Chastisement: Second phase

Martha C,

“because there are more rubes willing to pay…”

Yup, Robinhood…best app ever!

/S

On the surface buying a house now is a good way to catch a knife that’s just about to get dropped. Then again, if they print money like it’s literally going out of style to fill in the default black hole, inflation could make the true carry cost of a note evaporate.

I am a renter with little debt, a stable career, and a sizeable down payment ready to go, and this quandary keeps me up at night. :|

Spend it before your sizable down payment becomes worthless.

or exchange it for bitcoin

Don’t worry, most of house buying is with debt/credit… you’ll have plenty of time to watch all the leveraged home “owners” get washed out…

Death contracts gonna be worth more than house values… again… lol

Being a homeowner is good if married with a family. Probably better to rent if single, just because of the flexibility it gives as life gives you challenges and opportunities.

This is where im at with my life. Recently single, good job, money in the bank. I actually got my realtors license with the intent to purchase my first home, but now im renting still and going to wait and see how this all plays out. House prices are ridiculous in Idaho right now.

The Covid shutdowns have and are eviscerating the entrepreneurial middle class. The Forbearance Programs documented above mollify the non-entrepreneurial under and unemployed, keeping them, I assume, from acting out (i.e. Obama’s pitchfork fears) There’s no happy ending here.

Bitcoin is Not the Answer to Everything.Las I heard,there were many Bitcoin holders left unhappy after the last halving.Additionally,did anyone hear about fairly recent restriction placed on Chinese in Chinaby the gov. Whereby they could Not Access their$$?Could happen elsewhere.Then there are the powerouttages as an issue.Then there is the everyday reality of using Bitcoin.Stuff goes down fast tomorrow.You want to get some food,coffee,gas for car,whatever.Not fetting that in n. Illinois with Bitcoin.How are you going to pay for a hotel room,propane,firewood, out in the sticks with Bitcoin?

The Fed is ready to hit the ‘QE’ button at the first sign of trouble caused by any covid ‘wave 2’ correction in the markets . Their ‘lower interest rate’ dial is already turned down all the way. The question is, do you pile in when it happens?

When did QE end?

From another website with regards to QE:

“I keep an eye on assets at the Fed, ECB, BoJ and BoE, and here are the monthly movements (in USD bn) in 2020:

Jan -36bn

Feb +49bn

Mar +1,420bn

Apr +2,232bn

May +1,025bn

Jun +884bn

Jul +805bn

Aug +410bn

Sep +37bn

Oct +576bn

This totals $7.4 trillion over ten months.”

When people start realizing this is too good to be true.

When confidence fades, then what?

GL

As Ambrose Bierce sarcastically alluded to – it might be BitCoin. The underclasses are the proverbial frog in lukewarm water, beholden to banks and the gubment. It may be years before the frogs get boiled, but Paypal / Venmo and others are in the game of BitCoin now, legitimizing it as a currency with no middlemen get to take a cut.

Wolf has never (in my recollection) done an article on the relatively current state of BitCoin which has tripled since the Fed turned on the future inflation spigot. I would love to see an article on the short and mid-term viability of BitCoin as a currency (vs a commodity).

I’d be interested in hearing more about bitcoin/stablecoin.

At some pt, USD alternatives will become the absolute friggin enemy of the DC Way (currency debasement) and war on them will commence.

I wonder if bitcoin/stablecoin developers have thought about somehow tying the dying USD in to the rising non-dilutional currencies so that DC can’t attempt to destroy them without harming themselves.

Perhaps that is what “stablecoin” is really about…I know little about its construction dynamics.

(I have to admit that DC at least publicly seems blase about the non-dilutional alternatives to the USD…which look like Liar Killers to me, and so bad for the DC Way. Perhaps DC intends some Bitcoin bastardization that achieves USD dematerialization while allowing 100% pushbutton dilution/timer based USD self destruction in the name of “full employment/utilization”)

Beardawg,

Here is my article (it’s a bit short, but it’s enough):

It doesn’t matter what bitcoin trades for. The “value” is in people’s imagination. It conveys nothing to no one. No ownership of anything. It’s not money. You can barter it for fiat currency or stuff if you find people willing to believe in it. IF you can’t find people that believe in it, you can’t even throw it away. I’m tired of writing about it. I used to a few years ago. And I’m tired of the twisted gobbledygook with which people hype it. Like any good scam, it can make some people a lot of money.

+1. Prosecution futures, Yves from NakedCapitalism calls it and she is right. Even the underlying tech, the so called blockchain is more a solution looking for a problem.

Granted it’s not tangible as gold, they number of “people who believe in it” is growing by the day. I think it’s got some decent qualities. What its future is, only time will tell. In the short term, it’s a tradeable asset.

Wolf,

If you think of “bitcoin” as really meaning “any alternative currency substituting for dilutional USD” then it is really a topic perpetually worth talking about, with Fed debt at 100%+ GDP and the nightmare phase of entitlements just beginning.

As for “value only being in people’s belief/imagination” that is true of *any* unanchored fiat money, from Confederate Dollars to Weimar Reichmarks to “Quantitatively Eased, Linguistically Sodomized” USD.

The dollar is an official medium of exchange and a global accounting entity (such as GDP or exports expressed in dollars). Bitcoin is neither. Bitcoin is a bad joke gone haywire.

In order to be a credible currency, Bitcoin better have an army behind it, and not the speculative kind, the real kind.

It all comes down to it in the end.

So there we have it. Wanna raise your credit score? Come ‘ere kid. I’ll show you what you need to do!

The prudent get penalized and scoflaws benefit. Think of the long-term implications.

Based on what happened in 2008, its means the stock market will soar and the wealthy will get wealthier.

We are witnessing moral hazard on a biblical scale.

Moral Hazard, definition-

The risk that an individual or organization will behave recklessly or immorally when protected from the consequences.

How wonderful! Credit scores have improved across the board due to loan forbearance. If the Biden Administration Dept. of Education decides to reduce school loan balances by $50,000 or so per loan, everyone will have a credit score of 800. Happy days are truly here again!

“Weirdest economy ever” ©

There, Wolf, fixed it.

:)

MiTurn,

Thanks ?

Since I’ve been using that term for a few month, it’s time to set up a category for it — thanks for prodding me: https://wolfstreet.com/category/weirdest-economy-ever/

Fed can handle it. Need capital because of bad loans? We will make a data entry and the Magic Money Tree will blossom, same way it does in every other nation.

Many of these bills will eventually be transferred to taxpayers. We’ve learned that ~25T of debt has no consequences, so why not a few trillion more?

It’s sort of like smoking. Have a pack a day, year after year, and where’s the problem on any particular day? Certainly nothing will go wrong at some point…

Who’s paying taxes if they’re not working or out of business?

The taxpayer is only on the hook in a technical sense– hence the exploding debt that is the result of perpetually unbalanced budgets. I wouldn’t expect an actual bill in the mail, ever.

Instead, my bet is on monetization, which has already begun if you believe that the Fed will never reverse its positions.

And yet consumers have never had so much cash

stashed away. The water is still high.

Do you really believe, with 10 million added to the unemployment rolls the past 1 1/2 years, and the army of government employees dependent on taxes extracted from everyone else for their incomes that the American consumer is flush with cash as never before? It makes no sense, and I for one do not believe it.

My friend who works for a regional bank that has a huge hotel portfolio says that most of these hotels are about to go on their third 90 day deferral.

3rd 90 day deferral… lol… this will end well… hahahaha

Ironically, hotel to apt conversion is probably one of the least expensive redevelopment types.

Given the absurd hikes in apt rents over the last 10-20 yrs (product of ZIRP, as landlords attempt to recoup idiotic sales valuations given stagnant incomes), making housing much more affordable via such conversions would benefit 10s of millions.

(Hotel owners are already toast, so conversion to apts can’t increase their existent 100% losses).

They’re now starting to do “student housing” to apartment conversions. Which is interesting on many levels.

Yeah… all this massive supply just waiting to be unlocked in the search for cashflows…

What is really needed to convert a hotel room into an apt?

Bathroom…check.

Kitchen…not so much check, except for extended stay…which is doing well under C19 anyway.

Market opening up…for small, portable Pullman kitchen type setups. = Instant apt.

Or, even simpler, small cubic refrigerators and microwaves…far from fancy…but almost immediate conversion.

(Are kitchen sinks an absolute necessity?)

I’m sure some here will be aghast, but maybe less so at 75% of current mkt rents.

The model for conversion from hotels to apartments might be those buildings where the foreign guest workers are housed in in the Middle East and Southeast Asia. When traveling abroad last year I tried to get inside one to see what they were like, but could not. My foreign guest worker contact said it was 4 guys to a small two-bedroom apt. with one shower, and one hot plate to heat up water for tea. Eating cheapo street food was the preferred option. And had he tried to sneak my past security, he would have been shipped back to his home country (India) and blacklisted from ever again working abroad.

Sometimes think the monied elites in this country look with envy at how elites in other countries have organized things.

Claus Schwab 2030 ” you’ll own nothing and you’ll be happy about it”. You have any outstanding open credit? Run it up!

I suspect that a new below-the-radar system of determining credit worthiness, outside of our current credit scores, will ultimately emerge from all this ,based on the simple premise of whether or not one pays one’s debts. It might be a rather small select group for a while, but it will come to pass. In the interim, watch out below!

Dargg! I should’ve sent my daughter to the 75k a year school instead of being responsible and saving her from a lifetime of debt.

Thelma and Louise. Went to college, bought a car, bought a house, took vacations, ate out…..oops

Equifax, Banks, FRBNY, FDIC and BLS have adapted the CCP gongfei style of data analysis for their reports… the level of intellectual dishonesty stands in stark contrast with the levels of desperation exhibited… FUBAR lol

No worries we have a self sustaining service economy.

As the lights continue too turn off, it is just a matter of time before

the demand for services forces the lights back on.

I called my utility company and demanded they put my electric bill into forbearance. Netflix told me they don’t even offer forbearance, unbelievable.

I am moving to the country and I am going to eat a lot of peaches.

Wow, a Presidents of the United States reference. Strange days.

That was funny.

“Netflix forbearance”

Nice.

The new Fed gov nominee was rejected today, says that the national debt is a public asset. Machevelli said “private debt equals public good..” Accept the symmetry, and government is in some trouble. We can solve the problem by building a more direct democracy; public spending initiatives, MMT, etc. Equifax is now a branch of the Federal Reserve, a free bump in your credit rating is the first stimulus deposit.

Great piece of work. I love the way it you used to be realistic about the good times and the current crisis. The new best of times caught me off guard. But honestly what the heck. OK so the US government pushed a lot of cash out the door. How are we at ATH in so many places (market, housing, digital currencies)? Does the music stop…for somebody, anybody,… Feels like the person who pays on time and is not delinquent is somehow missing the boat

Everything is fine under the cloak of ‘extend & pretend’!

Then Why do need 2nd stimulus? It is not coming until early next year, latest. Even then with GOP most likely controlling the senate, it would be a small one. Mkts gone up like crazy on vaccine news although none will be available for average Joe/Jane until middle of next year, ASSUMING they do work!?

60 days before Prez takes office! Will the Mkts be patient? A lot selling could happen in December if the tax rates of uncle Joe come into effect next year!

I saw if price to sales of sp500 fell to long average the value would be about a 75% wipeout for s&p. Fed’s gonna print more on next pullback.

Top Federal Tax Rate History:

1963 – 91%

1980 – 70%

1986 – 50%

1988 – 28%

1991 – 31%

1992 to 2020 – 30% range

Wolf – Trickle down tax reductions for the uber wealthy started in the 1980s. Is it coincidence that the financial sanity and equality has fallen apart over the last 40 years, from 1980 to 2020? For all the data at Wolf Street on how weird the economy behaves in the present, how did we get here? Study prior cultures and empires, and there is a pattern of fiscal, political, and social decay once a small sub-group of individuals are allowed to become obscenely wealthy. A possible simple solution? Move the top tax rate back to 70%, increase the death tax from 45% to 90% for transfers above 100 million, and take all the increases of such taxes and buy stocks for the bottom 99%. Make the stock transfers yearly from birth to death, never allow any stock sales but people can borrow against the portfolio and spend the dividends as they please. Perhaps over 50 years, wealth inequality would decrease back to 1980s levels and the rich would become less powerful politically, and companies would place employee goodwill above shareholder profits as when you limit the amount of chips the top 1% can skim and take home, you change the nature of the game. The current rich still get to live out their uber wealthy existance, yet their offspring would have reduced inheritance. Yes Bill and Melinda get to live in their 66,000 square foot house and fly around in their private jet collection in their fantastic attempt to “solve global warming”, yet their kids will have to suffice with a 20,000 square foot house, and their kids kids only a 8,000 square foot home, etc. This is going to take a very long time to reverse, generations perhaps. Else we let it get out of hand and it will reverse in a few short years, in ways that will be much more destructive…

“Top Federal Tax Rate History:”

You left out the *huge* array of politician brokered exemptions/credits that made the *effective* rates far lower than the statutory rates you quoted.

The 1986 tax reforms wiped out a lot of the convoluted, deceptive insanity. The deal was lower, truthful tax rates in exchange for a broader, more truthfully comprehensive tax base.

The 1986 reforms were fairly revenue neutral on that basis.

America’s fiscal nightmare does not come from insufficient revenues but from DC’s pathological imperative to purchase political support via almost unconstrained (and unpoliced) spending.

Take a look at US gvt expenditure growth per year, for decades.

Compare it to almost any private sector business growth metric.

The former far exceeds the latter.

The parasite has killed the host.

The future I am planning for will involve significantly increased tax rates on the working class and retired since it’s pretty clear there isn’t any political will for increasing taxes on anyone else. Even with the current rates, many continue to grumble that the top rates are still way too high. Beginning in January, the very same people will soon be screaming from the rooftops about the national debt.

“Beginning in January, the very same people will soon be screaming from the rooftops about the national debt.”

Depends on their portfolio. If they are down 20 to 30%, they’ll pull an Avenger’s like “Whatever It Takes”. Otherwise you are right.

Doesn’t matter. This country is done.

“This country is done.”

Hmm. Nations tend to endure, political structures tend to fall.

So it may be more that, “This government is done”…too many decades of promises they never had any real way to keep (entitlements likely the death blow).

The real discussion very much worth having is what comes next and how the transitional ruin can be handled so as to minimize mass loss of life.

Cas127: The discussion of “what comes next and how the transitional ruin can be handled” is one I have been eager to engage in.

Who is having that discussion?

How did we get here?

By electing people who where selected.

Freaking 66,000s.ft. And That a.h… Is Trying to implant rfidnanochips in dangerous b.s. Vacc. So like 10,000 satanists can own the planet?They need to go 1st-maybe austere,supersurveilance Hardlabor can get them in touch with their souls if they have any! Some inequality could be remedied if co.s would pay decent wages to more than the ceo and tech. Staff.Taxrates should roll back to what Wolf cited.Like to see luxury taxes on certain things like fancy private planes,yachts,pricey sailboats,certain cars,overly. Huge,polluting homes.Americans are too complacent and should take a page from the French and Spanish Occupy protestors.Not thieving,looting,and assaulting like socalled antifa bastards,but Peaceful protests/massive workstops like the truckers workstop on Veterans Day,just longer and more widespread!!

30% range? This should be corrected to 40% range, we haven’t had a top bracket at 30% since the 80s.

What makes you think you or anyone else has the right to the fruits of another person’s labor?

Best Economy Ever (for top 1%)!!! J-Pow will not rest until his very own Fed inequality chart (link below) finally hits 100%! Praise be Jay…creating a couple minimum wage jobs utilizing only $1 Trillion QE per year, soon to be $2.5 trillion!?!?

“QE for the poor” Fed chart:

https://fred.stlouisfed.org/series/WFRBST01122

The $US is needed as legal tender for the masses (you and me) to use to pay taxes. Movement away from fiat using phys pm and crypto has to be a nightmare scenario for the DC people. The rapid debasement of the $US is obvious now to everyone. That problem got a lot of attention in the recent presidential election, right?? hahahaha. The debasing will accelerate. Does anyone wonder what Milton Freidman would have to say about MMT?

Since we are supposed to be in a negative interest rate environment, where everything is upside down, it seems only fitting that lenders should now be paying interest to borrowers for the privilege of creating debt assets out of thin air!

Lots of moving parts here. First, everyone is still operating under the Dalio Great Reset scenario. That ain’t happening folks. Instead, anyone who was championing China replacing the US and the world adopting globalism picked wrong.

Say goodbye to Amazon, Google, Mainstream media, Microsoft, Tesla, SpaceX, HomeDepot, CostCo and Walmart. Say hello to main street USA and the great small business revival. Decentralization is coming folks.

Central banks are all disposable. All debts will be consolidated into instruments that the CBs will be forced to buy before they’re written off. People who were responsible and are debt-free will be rewarded with cash to start companies if they invest it in rebuilding destroyed neighborhoods. Trade schools are going to be HOT. Universities will be hiring to replace fired leftists at all levels.

Manditory military or peace Corp ala Israel is coming.

Look at 1950 America. Factoryjobs, Andy Mayberry on TV, stores closed on Sundays, high church attendance. That’s where were heading. Position your portfolio accordingly.

Don’t bogart whatever it is your smoking. Pass it this way.

You shouldn’t smoke so much of the stuff at one time. Listen to music. Munch on something.

I’d like to un-dismiss your core assertion that “decentralization is coming”. I think decentralization is coming, but not for the reasons you cited.

Some of your corollary assertions, like China won’t replace the U.S. as the world’s major econ player, and that we should all go to church, I don’t agree with at all.

About re-distributing that productive capacity (that’s what “decentralization” implies):

Decentralization will entail massive reduction in std of living until local production becomes as efficient as global (comparative advantage) production is. So that limits decentralization’s “take rate”.

Centralized production is about to become vastly more efficient as the juggernaut of automation accelerates its wrecking-ball effect. This automation game is waaayy far from over. And for many years to come the prime movers and major beneficiaries of automation are high-scale (centralized) producers. Concentration of wealth will continue.

While I am a big believer in the possible advantages of local production, I see the transition to local prod as very difficult, and requiring major tech and personal evolution to achieve. That’s going to take a long while, even if calamity provides lots of incentive. And it may.

And given the massive effort required, why do you propose allocating resources (“mandatory military service”) to the military? That seems to be quite a stark and obvious mis-allocation of resources. Militaries destroy things. A good portion of the world’s productive capacity is nearing the end of its lifecycle, and needs to be replaced. We need to build things, not destroy them.

This part: “All debts will be consolidated into instruments that the CBs will be forced to buy before they’re written off” is occurring right now – no crystal ball required.

The “write off” has just been euphemistically re-labelled as “balance sheet growth”.

In most fiction I’ve read, the problem with Time Machine travel to the past is that the machine tend to malfunction. One glitch on the gears could get you back in the Great Depression/WWI or WWII bloodletting. And the Make America Great Again time travel will need a far more stable pilot, I’m afraid.

I gave a keynote presentation at a Chengdu conference in late October. The topic initially planned was model-risk management, but it had expanded to include shock events prior to Covid-19, which was a significant focus when finally presented. Credit providers responded by looking for other data sources, including normal banking transaction data, amongst others.

The link includes the presentation script, the slides, plus a link to the film presentation.

Or, bands of roaming Vikings raping, pillaging, slaughtering and all the usual things Vikings get up to.

I think the only thing I did right in life is to maintain a ZERO debt posture.

In a more sane world this would be true, especially if you held assets that were off the grid and could be used to buy or else barter/sell. But note all these events which close the door to transactions that can’t be traced. Everything you hold could become levied against for current debts, and all that you obtain after could be taxed away for future debts. These new proposals to wipe out the obligations of current debtors are capable of putting them on equal footing with you solely to be able to run up more future debt against their names…it is a case of bankruptcy en masse far different and greater than the normal manner of debt relief from which you can climb back up from through hard work. (The founders had foresight, but they weren’t crazy.) Right now, targetable assets are still somewhat protected by the filthy greed mongers who hold sway over the political class. But politicians will do whatever it takes to survive. If that means siding with a growing debtor class against asset holders with fewer votes, you know who will become the target. Only the richest will get out asset intact as long as they pledge monetary support for the false leaders. All these wonderful gadgets and proposed policies that are presented in living technicolor on your screen are in reality a dressed up set of chains to bind you to the control economy. Debt free is becoming a dirty phrase step by step.

Debt avoidance was a virtue back in the day, and so were prudent savings habits.

In today’s topsy turvy world, debt is virtuous and savings are spit on.

The forthcoming ‘Reset’ is likely to combine radical reconfiguration of existing currency units (e.g. US $) with a form of ‘stealth’ Debt Jubilee ( low-key debt forgiveness for selected segments of indebted individuals and businesses).

Wiping out a portion of student loan balances would be a trial case to test the waters.

Debt Jubilees date back to antiquity but contemporary DJ enthusiasts are not whispering anymore– there is serious discussion about it afoot.

Oh, and by the way, debt destruction is inherently deflationary, at least in a sane economic world. We don’t live in one of those.

Time for the 1,000 year credit card. Just pay the interest. /s

BWAHAHAHA!!! These greedy bastards and fools in the banking system have dug their own grave and are now ready to step into it!!!

Hehehehe!! I just LOOOOVE it to death! Here they thought that they could “get over” on the rest of society by creating their fake money out of thin air to rip people off, and now their “success” in that is their own undoing!! The minute they began to use unjust weights and measures to steal, is when they also took aim at their own feet, and pretty soon now, they will pull that trigger!!

Once a lie is told, more and more lies are needed to either cover it up or to reinforce it, and before too long, there are too many lies to keep track of all of them, and then the truth starts to leak out. When enough truth has leaked out, the entire banking system scam is exposed. You get hyperinflation and the system implodes. Only those who were smart enough to think in a straight line longer than just to the end of their own nose, saw these days coming and prepared for them. The rest will suffer a very painful and slow death.

Man, that’s quite a narrative. Could you give one concrete example, how it affects normal people, with numbers, to illustrate it?

Some of you will be in SHOCK when it does happen. YOU will pay for all the rents and mortgages and student loans via Taxpayer money!

You’ve already seen what they’ve done, you better believe what’s coming is the mother of all free monies to a lot of people at the expense of all of us.

That’s the ONLY way out. The system is too BIG to Fail. lots of Care programs for needy people who are in debt, loans that they won’t have to pay back. Financial Assistance to all in trouble.

Wolf- thank you for doing what you do!!!

Sounds logical to me, get everybody’s credit score up so they can borrow more to keep this fake economy nice and rosy looking. The dollar is on a death spiral. You see the euro had more transactions on Swift than the dollar last month. The dollar has lost 11% of its purchasing power against the basket of currencies since March. But the dollar won’t collapse, yea right. It’s collapsing before your very eyes. But they won’t let it totally collapse before there’s a currency reset. All debt will be wiped clean. It’s the only possible solution. There’s to much debt and it can never be paid off. They can’t inflate there way out of this mess without causing more damage. The Fed is stuck they can’t raise rates without popping the bubble and that can’t cut rates without more bad debt.