My Big-Four Bank Index already got crushed back to 2004 level.

By Wolf Richter for WOLF STREET.

After the stock market closed today, the Federal Reserve announced that “in light of the economic uncertainty,” and to provide “a cushion against loan losses,” and to support lending, it would extend for another quarter, so through December 31, the blanket prohibition on share buybacks by large banks (banks with over $100 billion in assets). For the same reasons, it would also cap dividend payments tied to a formula based on recent income.

The Fed said that according to a stress test and additional analysis, whose results were released in June, “all large banks were sufficiently capitalized” to deal with the fallout from the Pandemic.

But it appears that the Fed now thinks the banks need to be even more sufficiently capitalized, so to speak, to deal with whatever may be coming at them. And the Fed will conduct another stress test later this year.

Many banks had voluntarily halted share buybacks in March as all heck was breaking loose. In June, following the release of the stress test results, the Fed imposed the buyback prohibition for the third quarter, now extended through the fourth quarter.

So, let’s put it this way: As far as the Fed is concerned, this crisis is not a blip, and banks need to be prepared for what’s coming at them. The large banks have already set aside billions of dollars each to deal with the fallout on their loan books. But apparently, the Fed thinks there’s more to come.

The thing is what’s coming at the banks has been largely put on ice, but that’s just temporary ice, not permanent ice: Credit-card loans, auto loans, mortgage loans, commercial real estate loans, and other loans have been moved into deferral or forbearance programs, often after they were already delinquent, where the borrower doesn’t make payments for the term of the program, and the bank can still book the loan as “performing.”

These loans on ice are now everywhere. Many of them have been securitized and the problem has been moved on to servicers and investors. Many of the residential mortgage-backed securities with mortgages on ice have been placed into the government’s lap. So those are not for banks to worry about.

But banks still hold a considerable portion of loans on their books, and some of those loans are now in deferral and forbearance programs, and banks will have to deal with them eventually.

There has been a spectacular number of bankruptcies among brick-and-mortar retailers and in the oil & gas sector. Other sectors saw some bankruptcies too, but not to that extent. Overall, consumer and business bankruptcies have not spiked as they would have given the magnitude of this crisis because of the enormous amount of stimulus money, unemployment benefits, small business support programs (PPP loans), and large business support programs, including for the airlines.

Then there were the Fed’s asset purchases and direct lending programs that whipped the credit markets into frenzy, and nearly all companies were able to borrow in the market, even airlines, cruise lines, and move theater chains whose businesses got totally crushed. By being able to borrow in this frenetic market, they averted near-certain bankruptcies.

But these support programs have already ended or will soon end. Even the mortgage forbearance programs, though extendible, are on a timer. And the Fed only dabbled in the corporate bond market, buying only about $12 billion in bonds and bond ETFs, but stopped buying bond ETFs in July and bought almost no bonds in August, and likely wound down that program entirely in September.

Credit markets are still in a state of frenzy, and issuance of investment-grade and junk bonds has hit all time highs under insatiable investor demand, who are frantically chasing yield.

But the Fed is telling banks, get ready, you’re going to have to face the loans that are now on ice, and your borrowers are going to come under more pressure, and this is going to drag out.

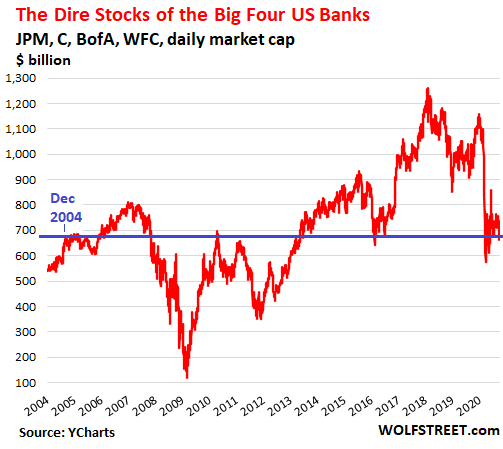

The stocks of US banks have already been getting battered. The KBW Bank Index is down 36% year-to-date.

The Big Four bank stocks.

JPMorgan Chase [JPM] is down 32% ytd. At $96.27 today, it’s back where it first was in October 2017. Having about doubled since the peak before the Financial Crisis, it’s the least-dirty shirt of the batch.

Bank of America [BAC] is down 33% ytd. At $24.09, shares are down 56% from the peak before the Financial Crisis, and are back where they’d first been in December 1996, well, 24 years ago.

Wells Fargo [WFC] is down 56% ytd. At $23.53, shares are down 61% from December 2017 and are back where they’d first been in October 2000.

Citigroup [C] is down 46% ytd. At $43.11, shares – adjusted for its infamous 1-for-10 reverse stock split in March 2011 – are back where they’d first been in 1993.

My Big Four Bank Index, based on market capitalization, closed today at $685 billion (yup, $60 billion below Facebook’s market cap). That’s down 46% from its peak ($1,258 billion) on January 26, 2018. You see, banks got hit two years before the Pandemic. And the index is now back where it had first been on December 28, 2004, nearly 16 years ago (data from YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My only hope is that when the rubble stops bouncing on this upcoming banking meltdown that some of the bankers will be put in jail. One of the biggest problems with the crash of 2008 is no-one was held accountable. In a truly just world the prisons would still be stuffed to the gills with bankers from the last crisis.

Seneca, sadly we do not live in a truly just world. Those responsible for reckless and fraudulent behaviour are seldom punished. The banks’ customers, share holders and taxpayers bear the brunt.

Seneca’s Cliff…… In my world they would have the lobbyists to play cards with in their cells. Oh dear, I left out the politicians that they both paid for as well…. hmmmm, what to do?

The ugly truth is that banksters truly are doing God’s Work, and we didn’t privatize our prison system for white collar crime.

Watching the debate the other night when the phrase “Law and Order” was repeated, and I thought, hmm?? Isn’t there a snappy comeback in here someplace?

Being rich and paying less in taxes than a working class grunt with bad knees and a stomach full of rotten mickyD’s may be the law, but it’s not a recipe for order. The American people are all farting large clouds of smoke, especially the ones who actually like DT. The atmosphere can’t handle anymore pollution of this sort as we head over the cliff into the valley of smog.

So what makes you think the banksters or politicians are going to be held accountable this time round?

The fact that most folks are willing, and continue, to pay taxes to feed this system of fraud and support the fat pigs (of Animal Farm), simply means everyone still supports the current system, implicitly or otherwise.

And oh…not even get me started on the futility of your sacrosanct democratic vote (to effect political change). Remember all the teary-eyed and hopeful wonderment of the American electorate when the first Black man proclaimed his “Change we can believe in!” Kool-aid from the pulpit of 2008? Look at the state of where BLM is today. Change we can believe in? lol.

Kevin,

Does your comment mean that you no longer pay taxes?

I for one do not want to have the full weight of the IRS bear down upon me.

Prez T didn’t pay taxes for 10 yrs out of the last 15 yrs!

‘Only little people pay taxes’

-Leona Helmsley ( billionaire New York City hotel operator and real estate investor)

Jeff, I’m not an American citizen so don’t worry about IRS on my behalf. I feel sorry for Americans who CAN be chased down GLOBALLY by the IRS though. I guess that’s the “privilege” of being a part of American exceptionalism. ;-)

In any case, you either learn accounting 101 – on how to expense your profits, use off-shore tax havens, transfer-pricing, own everything under a corporate entity (LLC equivalent in the States), while drawing a low base salary which makes you pay near zero taxes etc., while controlling the equity of the entity.

Sunny below is correct, the rich don’t pay taxes. Neither do the biggest corporations who can hire an army of tax advisors and savvy accountants to help them do Tax Avoidance…ahem… the polite phrase is “Tax Planning”. Even Trump organization does it, as do the largest listed companies of the world. As usual, its always the “little people” who are “law-abiding good citizenry” gets screwed.

Where I come from, its all perfectly legal if you know how to do it right, but best for you to check your local tax laws because each country/counties may have very different tax regimes.

Generally, if you’re an 9-to-5 employee, its rather difficult to workaround (income) tax laws, but if you can make arrangements to become a “consultant” to your current employer under a separate legal entity, then you can do many wonderful things – all the while performing the same “job”. Of course, you’d have to be really savvy with your approach.

I guess the current pandemic may allow more opportunities for such arrangements since almost everyone is working from home anyways, so I see lots of possibilities now to cut the corporate umbilical and attachments to the office cubicle. Good Luck.

If the bankers should be in prison, so should all the people who took out “liar loans”, the housing crash took dishonest behavior and greed from more than just the bankers.

Who created “Liar Loans”?

Better yet,who allowed them to exist legally? I believe we have a well paid regulatory system where nobody lost their job,despite massive failure.

You didn’t have to lie, they issued no income stated loans for an extra quarter point.

‘Fiduciary Duty and Due diligence’ belongs to Banks(Lenders) and NOT the borrowers!

Who created ‘ interest only, stated income and various LIAR loans? TBTF- TBTP aka Banksters!

Bank: How much to you make?

Borrower: How much do I need to make for this loan?

Bank: $150,000/yr

Borrower: $150,000/yr

Bank: Approved!

They are approving loans for furloughed workers they know might not have a job after closing. There is also talk that refi’s are being counted as home sales.

Petunia: If you have links on REFIs as home sales. In CA homeowners take REFIs, Rev Mos, all sorts of equity draw downs, without disturbing their Prop13 tax limits, even while there is no reassessment, they keep their 2% cap in place. I decided against any of them for that reason, although the agent assured me there would be no reassessment, (or rather their own private assessment) The possibility looms, tax collection goes back on these people, with retro tax bills. Should Prop13 be repealed – values would collapse, but they would start to rise more quickly without the 2% cap. In a period of asset hyperinflation the tax assessor might see this as a stop loss measure. They might take a tax revenue hit up front, but recover quickly when the cap is off. To me it’s just a matter of time before they start to shake the tree. Rent control is a bit scary topic, as it puts power in the hands of non-homeowners, who imagine that lovely estate takes of itself.

True that others misbehaved and some punishment might be appropriate.

Think about the first-time home buyer, though. He has no idea what the process entails. The mortgage originator tells him to sign here, here, here, . . . ad nauseam. That buyer will suspect that the mortgage originator is doing wrong but the banker and mortgage originator KNOW. I think there’s a difference, a big one, in what sort of punishment is appropriate.

‘Fiduciary Duty and Due diligence’ belongs to Banks(Lenders) and NOT the borrowers!

For that malfeasence they got BAILED out!

Seneca’s Cliff, agreed. The fallout from lack of prosecution hasn’t helped us.

I how the original enabling legislation for the Federal Reserve prohibited corporate bond purchases, but through the so called Section13-3 provisions Powell talks about the Fed can make these purchases now. As you point out, they have not made aggressive use of this authority. Is there a “sunset provision” that will expire on this authority before they decide to go all in on this authority?

‘the so called Section13-3 provisions’

A fig leaf for their their ‘extra constitutional’ act!

No one in Congress/ regulators questioned it b/c they ALL are complicit.

John Hussman PhD has pointed this one in his recent blog article!

The big banks are a cancer, I’d rather do business with the Fed directly and that says a lot! Why not just nationalize them and get rid of TBTF? They are just as atrocious, inefficient, and corrupt as the government, so they’d fit right in!

Why not indeed bancster. Why not have only the Fed. Why not let the Fed handle every payment we make, why not have a centralized Fed bank with small little branches all over the US. Why stop there why not have the Fed open their banks in foreign countries as well. Why not let a semi political obscure group unaccountable to anyone in charge of all the money and all of the people’s wealth.

Isn’t that too much power for such a group of people to have? What is it they said about absolute power?

You need some semblance of decentralization in order to serve your cronies

You could look at it another way.

And say that we need more but smaller banks. So that they can truly compete with the bad ones failing.

Bring back capitalism.

A few big banks don’t work, a lot of small banks don’t work. Regulation dont work, de-regulation don’t work. You know why? Because the banking industry is inherently corrupt. Absolute power corrupts absolutely.

The Fed already has too much power with no accountability (other than to the cabal of banks

There was a briefest moment that TBTF was going to go away in 2009. Then all of the finger pointing began and TBTF became even bigger than TBTF, thanks Tim, thanks Paul, thanks Ben, and thanks Barack… good job guys.

The biggest TBTF is the economy and in 09 it was going to fail. The banks weren’t lending to each other let alone business. Biggest historical of the Fed is the Depression, when it sat on the sidelines.

Let’s get some names right too. It was George Bush who got the FED bankers together and warned: ‘this sucker could go down’

He also signed the first bailout of GM in the last days of his term ‘because I didn’t want Obama to have a crisis on his first day’

Outside of Roosevelt, no incoming President has been handed such a can of worms as was Obama.

Typo: Should be ‘biggest historical criticism of the Fed’

Thanks George, but… BTW… still, thanks Barack, cause he didn’t do jack about it afterwards and pretty much maintained the course. Subsequently TBTF became NPTF… as in Not Possible To Fail.

Obama’s crime was failing to push for prosecution of individuals. That’s a mortal failing in the U.S. regulatory arena.

In his defense, the whole of Wall Street was claiming the system was too fragile for such legal action. Baloney. But it’s true that’s the advice one read in the WSJ, from the Fed, etc.

The Financial crisis of 2007–2008 led to many bank failures in the United States. The Federal Deposit Insurance Corporation (FDIC) closed 465 failed banks from 2008 to 2012. In contrast, in the five years prior to 2008, only 10 banks failed.

There, I fixed your assertion.

TBTF is a complex topic. They all have a chance to fail simply because they constantly need fat profits that are acquired by exploiting the naive to the bone. What keeps the ones who don’t fail operating is political protection provided by the swamp scum. Just like the Renaissance bankers. And don’t think it’s one side or the other doing it. Both sides have their favorites that they protect for their own benefit.

Now you’re going to tell me that Barack destroyed the banking industry when a regulatory arm of the gov shut the 465 banks down after the biggest crash yet. As if Barack personally directed it.

Will the realization that Dubya did NOT shut many banks down make you realise the true nature of the problem? In not shutting failing banks down, Dubya created TBTF.

Sub-Capitalization of Banks! Fed is hood winking again!

A big joke!

https://www.nakedcapitalism.com/2020/09/how-bankers-hide-losses.html

So two of the big four are back in the 90s? I heard this Internet thing is gonna be big.

Wolf,

Thanks for highlighting how accounting, regulatory, and internal corporate rules tend to be designed to spread the impact of likely/highly likely loan losses over several quarters.

That fact tends to be obscured by the “I don’t see any problems”/”don’t worry” crowd…who are often trying to offload their own positions before the full scope of the catastrophe is made clear.

Next goal – getting an accurate read on the non-performing loan mkt.

But there are so many definitional games played to avoid non-performing status (mortgage forbearance v. Mortgage deferral, etc.) maybe the best stat to research is amount/percentage of loans *performing*.

I wonder if any entities report loans in that seemingly harder to “game” way.

I get the impression that banks no longer have a grip on what is going on in their loan book. They have entered these loans into deferral and forbearance programs, and they know some/many of them are going to be nonperforming when the period ends, but I doubt they know how many, and the deferral period will end for these loans at the same time. So suddenly, they’re going to have to get their customers to make payments again, when their customers have gotten used to spending this money on other things.

Banks have set aside quite a bit to cover some of it. But if they have trouble getting their borrowers to make payments again, it’s going to get very messy.

To which we can say, thanks Nancy, thanks Donald, thanks Jerome, and let’s not forget Steve…. good job, guys. Setting up an unimaginably dependent structure that is even more addictive than cocaine.

Thanks for all the work wolf, I always check out your posts. I have the same feeling now that I had when I first started reading the housing blog sites back in 2005……..that hinky feeling that something is just not right.

Yes. But what to do? I tried a short I still believe in a month or so back and learned a lesson. ;-)

I think things are RICKETY.

The problem is valuing the derivatives, mortgage, credit card and auto loans. These products are valued based on income streams and default rates. Right now the default rates are technically zero. The default rate might stay at zero in the future, or it may break through up the wazoo.

It is now impossible to price these products based on default rates or income expectations. The models have all broken down because nothing can be predicted based on income or defaults. If you can’t price it, you can’t buy it or sell it.

Why doesn’t the Fed buy back those bank shares? They can certainly buy the ETF. They nationalized the “economy” but they can’t bail out their own charters? Bnaks balance sheet is small potatoes, their stock price is the meat. The only thing wrong with banks is that they can’t make money, other than front running shares from their trading desks (using inside info). Banks are the heart of the capital formation process, or used to be. What is going on with Palantir?

Since the banks own the fed, with every share the fed would purchase, they would be buying back their own shares. It’s self dealing, insider trading, and a bunch of other unethical practices as well.

“Accountants portray themselves as truth-tellers, but especially when they work for a dangerously undercapitalized bank, their jobs are far more complicated than that. In INET Working Paper 136, I compare skilled bank accountants to master illusionists such as Siegfried and Roy. Much as these famed magicians made audiences think that they could make large wild animals disappear, some bank accountants enhance their income by convincing client banks that they have the power to make losses disappear. But in both kinds of illusion, items we no longer see have not actually vanished. They have been moved surreptitiously to places for which outsiders have no sightline….’

h/t Naked capitalism

Accountants interpret and follow accounting rules. It’s not their fault. It’s the accounting rules that are the problem. The accounting rules are laid out in GAAP.

Beyond that, it’s the regulators that are the problem, and Congress for allowing banks and hedge funds and investment banks to be fused into one, as they are today. Separate deposit-taking banks from everything else, and regulate them with an iron fist, and let hedge funds blow up and fail, and it’ll work just fine.

Mr. Richter, maybe the banks will just go to off balance sheet accounting…

If I remember correctly, these big banks got some Stella quarterly reports not too long ago… Do their share prices impact them much at all? Do they even care, especially with Fed in their back pocket?

Stacey and Max Kaiser quoted your bank statistics on the Kaiser Report. Good on ya’.

WOW Wolf is gone mainstream for sure Love those lunatics, especially Stacey

I know the enabling legislation for the Federal Reserve prohibited the purchasing of corporate loans, but the so-called “13-3” authority Powell talks about now permits these purchases. You point out that the Fed has not exercised this authority aggressively to date. Is there a “sunset” provision that will expire for this authority before the Fed might decide to go all in and expand their purchases?

Joseph A Vignone,

Yes, these programs expire. The original expiration was in Sept., and they extended it through the rest of the year (Dec 31). Unless something blows up until then, it looks like they’re going to let it expire this time.

Each of these programs has a term sheet that explains the details. Here is the one for the secondary market bond purchase program we’re talking about here:

https://www.federalreserve.gov/newsevents/pressreleases/files/monetary20200728a1.pdf

Remember when 0% interest rates were supposed to be temporary?

They were only needed until unemployment got down to 6.5%.

Extremely low interest rates mean interest margins are very low,

Sounds like death for banks and insurance companies.

They’ll just create more ‘fees.’

Banks and insurance companies can and do put their assets in a plethora of investment vehicles.

When I was in college years ago, my finance professor told me every building with more than 5 stories west of the Mississippi was owned by an insurance company.

And savers. And retirees and pension funds. No safe investments means withering away or taking on too much risk and blowing up.

I don’t think Powell sees anything, it’s just public relations, it sounds and looks good , but it has absolutely no real impact or effect.

Tens of thousands of layoffs were announced just today.

If you want a real horror show look at the prices of UK bank shares. Lloyds were £6.30 at their peak now all yours for 26p, Natwest Group £60 now on sale at £1.06 etc.

Stick a fork in them, they’re done.

“Let them eat stimulus.”

I don’t think the peasants are going to remain happily numb forever, though. Eventually a real economy will be necessary to feed and clothe and house people. Accounting fantasies dreamed up by the nobility only last so long as they keep their heads.

We haven’t had a real economy that wasn’t based on the petro dollar scam since the 70s. It’s all extend and pretend that the ‘loans’ will ever be repaid.

i think it was citi that recently spent their entire

years profit on stock buybacks. Some thing like 20 billion.

Still trying to figure out the why.

It’s not complicated: C-suite bonuses.

Come on, you guys are being so unfair. I really like my bank and banker. Oh, wait a minute, my bank is a credit union with local ownership that provides me with a detailed statement of assets and liabilities every year. Oh yeah, I get to vote who is on their Board of Directors. When I need to present my number for a particular request they give a low whistle and call me Mr. _______, and add, “My goodness, you have such a low membership number you must have been one of our members for a long long time. Come on right in”. And, their account guarantees by Government mandate is 2.5X higher than a charter bank.

Why on earth do people use a bank, anyway? It can’t be convenience in these days of internet access and online services. Habit? Sloth? Resistance to change?

It takes an hour or two to close your accounts and switch over, and it can be done right at the Credit Union. This hour includes the time to drive there and find parking. In many business environments customer complaining falls on deaf ears. Money that walks carries a big stick.

One more thing. We just spent some time with our Credit Union investor representative (who works on salary and not product commission) and put a bunch of cash in various term deposits etc. In this time of Covid, we met in a sterilised office separated by plexi, and came to an agreement and plan. All paperwork was then forwarded by email and all signing was electronic as we live 50 miles away. Pretty convenient for us.

All banks are inherently bankrupt by their very own nature. It’s only the implicit Fed and government guarantee that keeps them in business as well as their size that makes them efficient hostage takers a little bit similar to a man named Kim in the North Korean Peninsula.

I bank with big banks for the simple reason that they have this implicit government guarantee and hope to get my money back in a crisis.

With incoming and outgoing automated payments it takes way more than an hour these days to switch banks.

Some accounts at big banks are very old but they started at smaller banks and got gobbled up over the decades.

I’ve been with my (previously company-sponsored) CU for over 35 years. I put a low 6-figure dollar amount on deposit with them after I sold my house a couple years ago, and they assigned a personal ‘consultant’ to me who does my bidding with an email or phone call (and free checks!). The only fees I’ve paid in all those years was for a couple wire transfers. Like banks, though, they aren’t paying squat in interest and, when they did, it was a few basis pts below the banks’.

Fed and the banks have really gone their own ways. Fed head is under secretary to the Treasury. Now a conduit for Congressional stimulus. The banks are where the auto industry was fifty years ago, never far from the next bailout. Every bank creates the same product, credit, and it all pretty much looks the same, spreads narrow, and none of its profitable, which begs the question, why forex? How do you register an unregistered derivative? Sell it to another bank! Why we don’t follow the spirit of the law when it comes to money laundering has never been answered. Apparently only physical cash deserves the opprobrium of blood money. Hence the Fed will digitalise your next stimulus payment. Bank payment flow on Main St loans is non sequitur.

If you want to see where the market capitalization of US bank stocks is headed, look at the market capitalizations of European stocks. Interest rate suppression kills the banks, and the US just reduced the 10- year rate from over 3% to .7% in one year. The European banks saw their market caps plummet when rates went to zero.

Tons of pain lay ahead for US banks.

The blueprint was already established with Japanese Banks (Mitsubishi UFJ, Sumitomo Mitsui, Mizuho Financial). Banking will eventually be a quasi-nationalized industry.

Bankers rule the world by making government in debt to them. It is really about that simple. The government does not control the Fed, the Fed control’s the government and in so doing, controls you, and your life. Life as you know it, can change with a single keystroke.

Wolf:

Any idea why Canadian banks are so secure and still seem solid?

Thank you.

At least the giant banks know if anyone gets bailed out, it’s them. Also, if cash is needed, they have the power to freeze anyone’s accounts and limit transfers and withdrawals.

So, we can all sleep well.

I’m in complete agreement with Paulo and California Bob above, re Credit Unions. But my household has accounts with banks as well, for the usual reasons.

From this post, and your latest podcast, Wolf, it looks like the Fed has taken to running about and screaming, “the sky is falling”…..well, yeah, guys at the Fed, that has been obvious for some time now, and you’ve been a big part of the problem. I’m not letting you off the hook; and BTW, your instant digital $$$ stimulus idea, as Wolf outlined in the podcast, just sounds to me like one more invasion of my privacy. And has someone explained how the “couple in a tent” who I’m guessing don’t own digital devices get their $$$ from their Fed account ?

I hope to see better ideas for reversing the concentration of wealth in the few wealthiest, and re-creating a prosperous American middle class.

I’m with you, Wolf, on the cease and desist of ZIRPs,and NIRPs, and Fed purchasing of assets; but I don’t see making the Fed the administrator and guardian of every adult? American’s stimulus payouts as a good answer.

Thx, Wolf

Any private sector business that engages in stock buy backs or massive bonuses to their partners and executives should be placed in a different category regarding federal bailouts. ie, not eligible.

They goose the stock to kick in their options….or they disperse the firms capital so as to remove it from exposure, like a reserve fund for bad times and unexpected events.