CMBS delinquency rates for retail properties spiked to 18% and for hotel properties to 24%.

By Wolf Richter for WOLF STREET.

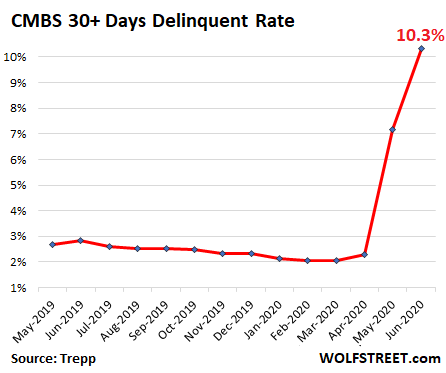

The delinquency rate for Commercial Mortgage Backed Securities (CMBS) spiked by 317 basis points to 10.3% in June, after having spiked by 481 basis points in May, which had been the largest month-to-month spike in the data going back to 2009, according to Trepp, which tracks securitized mortgages for institutional clients.

Another 4.1% of the underlying loans missed the June payment deadline. Because they’re not yet 30 days past-due – they’re marked in “grace” period or “beyond grace” period – they’re not yet included in the delinquent pile. A loan that is in the “grace” period or in the “beyond grace” period could revert to “current” in July without a payment being made, if the borrower enters into a forbearance agreement with the loan servicer. If the borrower fails to obtain a forbearance agreement, the loan will be added to the pile of 30-plus days delinquent loans:

Trepp suggested that this still might get a little worse, but more slowly, and not much worse. “So perhaps we have reached terminal delinquency velocity,” as the report put it, where “most of the borrowers that felt the need for debt service relief have requested it.”

In other words, borrowers that made it through April, May, and June without becoming delinquent have a good chance of being able to weather the storm, according to this theory.

But this theory will be challenged by the meltdown of retailers that continues despite the reopening of malls — more on that in a moment.

Commercial mortgages have a balloon payment at the end of the term, and when the loan matures, the balloon needs to be paid off or be refinanced. But when this becomes impossible, “maturity defaults could still be an issue,” Trepp said. “If that is the case, the expectation would be that the increases in the delinquency rate going forward should be smaller than what we saw in May and June.”

The percentage of loans that are “seriously delinquent” jumped by 408 basis points in June to 6.25%, larger reflecting May’s record surge in 30-day delinquencies that became seriously delinquent in June. These seriously delinquent loans are in these stages:

- 60-plus days delinquent: 3.22%

- 90-plus days delinquent: 0.29% – the low rate shows just how fast the crisis hit the commercial real estate market

- Non-performing balloon payment: 1.31%

- Already in foreclosure: 0.33%

- REO (“real estate owned” by lenders that already took possession): 1.1%

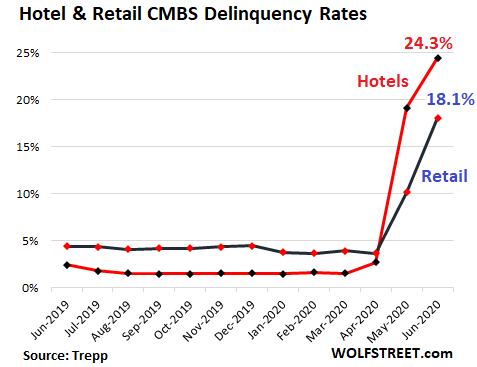

By property type: Retail and Lodging loans are getting crushed.

Industrial property loans, such as for warehouses, are the best-performing category with a delinquency rate of 1.57% in June. Ecommerce was one of the biggest beneficiaries of the pandemic and the lockdowns, as much of non-grocery brick-and-mortar retail sales, and even some grocery sales, shifted online. Retailers, such as Macy’s and Nordstrom, whose stores were closed, reported soaring ecommerce sales. And the brick-and-mortar part of ecommerce, the fulfillment centers, remain in high demand.

Office property loans are experiencing still low delinquency rates, though they ticked up in June to 2.66%, from 2.4% in May and 1.92% in April.

Multifamily loans (apartment buildings) are experiencing moderately rising delinquency rates, at 3.29% in June – up from 2.11% in June last year.

Retail property loans – this is the brick-and-mortar meltdown and includes many loans backed by malls and outlet properties – are getting crushed: 18.07% were delinquent in June.

Even though many malls have reopened, many stores in them remain closed, numerous large retailers filed for bankruptcy protection, and the whole industry, which saw much of its sales wander off to ecommerce, is in perma-decline. This has been going on for years, but the Pandemic compressed several future years of continued meltdown into half a year now.

Hotel property loans are the worst hit as much of the travel industry has shut down. The delinquency rate spiked to 24.3% in June, and the sector remains in turmoil, with many hotels still closed (delinquency rates by Trepp):

Many hotels that are now closed will eventually re-open, and those that are now open, will eventually see their occupancy rates rise from the current fiasco levels. But the glory days, especially for business travel – the most lucrative segment for hotels – may well be gone, and it will be a tough slog going forward.

But the brick-and-mortar retail business is in a different ballgame. There are now estimates that between 20,000 and 25,000 stores will be permanently closed this year, after nearly 10,000 stores were permanently closed last year, with department stores and apparel and fashion stores on top of the list.

Numerous retailers have filed for bankruptcy protection this year. Some of them will try to restructure their debts in bankruptcy court and continue operating, but with fewer stores. They use the bankruptcy proceedings to get out from leases or renegotiate more favorable lease terms at locations where they want to continue operating a store.

Some retailers are being liquidated and will close all their stores. This includes Pier 1. Many retailers that haven’t yet filed for bankruptcy have unilaterally declared that they will not pay rent while their stores are closed. This includes Gap. And then, without rent payments, there is no hurry to re-open stores even at malls that have reopened.

Other retailers, such as Nordstrom, told landlords that they would cut the amount in rent they’d pay. In Nordstrom’s case, it had told the landlords of its department stores and Rack stores that it would only pay half of the occupancy costs for the rest of the year, according to Retail Drive, which obtained a copy of the letter. Nordstrom had already announced the permanent closure of 16 stores, and those landlords are out of luck.

Department stores serve as anchors at the malls. With them gone, foot traffic at the mall declines further and causes other retailers to close their stores. And when retailers disappear or don’t pay rent, landlords eventually fall behind on servicing the mortgage.

In addition, many retail properties are so bogged down in shuttered stores and stores that stopped paying rent — amid retail property valuations that plunged in recent years — that when the loan matures, the landlord has trouble refinancing the property to pay off the balloon. This would trigger the above mentioned “maturity defaults.”

These mortgages are held by banks, insurance companies, and other institutional investors, and they’ll be busy sorting through this, foreclosing on properties, and tabulating losses. And some of these mortgages have been sliced and spread over many CMBS, and those slices are now defaulting in large numbers.

The problem with retailers is structural. The Pandemic compressed three future years of brick-and-mortar meltdown, that the industry could have dealt with more adequately, into just a few months. Unlike other industries, brick-and-mortar retailers – clothing stores, department stores, outlet stores, specialty stores, even shoe stores – will not recover to the already beaten-down levels before the Pandemic. During the Pandemic, another big chunk of their sales has permanently shifted to ecommerce, and there will be little relief for landlords, such as mall REITs, and for CMBS that contain these mortgages.

In the area of apartment rents, the impact of the Pandemic is already showing up. Read... Massive Shifts Underway, Rental Market Reacts in Near-Real Time: Rents Plunge in San Francisco & Oil Patch, Drop in Expensive Cities. But Long List of Double-Digit Gainers

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Can this come printed on a mug?

“we have reached terminal delinquency velocity”

This is nothing. You should have seen Argentina in the last default.

And this year another default is very likely.

I have no idea why folks keep buying Argentinian government bonds.

But they always do.

Because our exceptional US courts have ruled that debt owed to the 0.01% are sacrosanct and must be paid for by breaking non sacrosanct obligations owed to retirement funds of non 0.01%’ers.

Imagine you’re trying to set up an investment fund and you need clients. Your clients will likely want high yields and relative safety, and they won’t know much about finance.

You decide to offer an emerging markets government security fund. Play off the weakening dollar theme (which US-focused news watchers often fret about), along with government security and a juicy yield.

That’s good sales pure and simple. You give the clients a happy illusion, make a percentage while it works, and then it’s not your fault (or your money) when it blows up.

One needs volatility for diversification.

“Make the economy scream”!!

(A South American country back then)

Nixon to Kissinger…….LOL!

I avoid malls, corporate retailers and Amazon as much as possible.

Independent businesses, flea markets, garage / estate sales and Goodwill types work for me.

“Independent businesses, flea markets, garage / estate sales and Goodwill types work for me.”

Independent retailers: for those who love paying 50% more than Amazon. My wife is one of those people, unfortunately. I don’t know how many times I’ve had this conversation

Her: I bought XYZ at store ABC for $100

Me: You know Amazon has that exact item for $50

Her: Yeah but I want to support local business

Me: How about you support your personal net worth instead?

Her: Stomps off….

Me: Grabs a beer….

:)

In some industries, what Amazon is doing would be considered illegal. It has been demonstrated they are selling some products for less than what they cost to make. This is a strategic move to “corner” that market away from whoever else may be selling the product, including the manufacturer selling it directly. Sure, it is great for the consumer, until its not, then it can’t be easily changed back. Remember Walmart moving into small towns?

actually isn’t amazon middle man always getting VIG

in that way you don’t hold inventory and price risk is suppliers

That was old school Amazon.

Amazon is usually the higher cost retailer now. Usually not even close on larger ticket items.

But people are lazy, and they pay big bucks for convenience.

Due to Covid I am shopping almost 100% online.

It’s very easy to price compare by having a window open for each seller. I’ve found 30% differences in prices sometimes. Almost every national store has an online store.

There are way better deals online from independent merchants. I always look at the Amazon prices as the the ceiling and then go from there. It might take going to the second or third search page, but they exist.

This reminds me of wolf’s search for jeans article where if I remember correctly he shows it does take some experience and skills to find the best price. My son showed me the other day when he looked for a sixty inch TV based on a established account the best price he could find was 569.00 then he uses a ghost account with no history and finds the same TV for 269.00. This old timer is a slow learner but I’m getting there.

I’ve often found eBay to be a suitable alternative to Amazon. Many sellers are small ‘mom-and-pop’ businesses; (some sellers sell on both platforms, often with differing prices). Not something you’d likely see on Amazon, but I bought a magazine (‘clip’) for an old pistol on eBay, and with the magazine came a handwritten note; seller was an older man summering in the desert in Arizona. The note said my payment would almost cover his gas to drive back to his home in Minnesota. That felt good.

I’ve been routinely beating the Amazon price via other vendors for these past few months too. I’m getting decent-or-better deals on eBay.com and Etsy.com.

Maybe Amazon thinks they can still charge me more for some reason – and I’ve always wondered how much they’re charging others for the same stuff, there’s no price transparency – but the romance is over.

Whenever I do a search on Amazon, they never sort the products in the order I like, half the slots are “promoted” (ads) making me wade deeper to find what I want, and then half the remaining listings are not what I’m looking for, and among the rest, half of the remaining products are shoddily made overseas with gamed fake ratings.

Online stores with a curated product collection, where a thoughtful manager has already filtered out the crap and useless stuff that no one wants, will begin beating Amazon. Those will still be a national thing (economies of scale), but the competition will still be better for consumers.

There is a browser plugin called ‘Keepa’. It shows you the price history of most amazon items as a graph. Needless to say, all these reduced prices that show up on Amazon are complete fantasy. Even items where the price is higher by 50% over a year ago still show up as reduced.

You can buy whatever you want on Amazon, but now days, the chance of actually getting it are getting less and less. I have had 3 items ordered in May that still are not delivered. All you get are apologies, they just take your money and make excuses for not delivering. At least at a b&m store, if they do not have what you want, you walk out with your money…… I am getting real sick of Amazon.

JDog,

I’ve had a couple of items not turn up from Amazon recently; I marked them as no received and got the option of it being sent again, or refunded.

First time I asked for it to be resent, but the second time I just asked for a refund and got it the next day.

re: “There is a browser plugin called ‘Keepa’. ”

I’m very leery of browser plugins; I don’t believe they are being properly vetted (looking at you, Google). I’ve been out of the tech business for a couple years, but the plugin interfaces of most browsers were known for being insecure and poorly designed/written (maybe that’s improved, maybe not). FWIW, I use Firefox; maybe not the best security-wise, but not the worst either.

Me grabs a beer and make her return it and buy same thing on eBay for 25$

for the same reason.. I avoid Amazon if I can

I dont mind paying lil extra and this won’t make an impact on my personal wealth

Amazon is great for looking at pictures of merchandise, reading reviews, getting details, sometimes downloading manuals, instruction sheets etc.

THEN you look for the manufacturers website and can order it directly less in some cases, even with the cost of shipping.

Beware of price point B.S. We found a refrigerator we were researching online. Best Buy had it for X price. I called a local old time American run appliance store and they ordered it for me. Their price? One dollar higher, which makes me think that Best Buy lowered their posted one dollar cheaper price to harvest the online shoppers looking for price alone.

Your local Craigslist has a For Sale section, subdivided into categories such as appliances, building material, cars, computers etc. That is where you can buy bargains, or sell surplus or unwanted stuff. In addition, there’s a Free section which means people will come take things off your hands and will reuse them, or you can get needed things for nothing.

Lol!!!

Concur, but I do enjoy Ebay.

:)

Back in the bad old days of 13% mortgage interest rates and required 20% down-payments. I purchased my first home with a 7 year ballon mortgage at 9.5%.

Those years I worked like a dog to pay down that debt and to save as much as possible.

As I knew the ballon clock was ticking. And if interest rates shot up, I better be able to afford a new loan. And the only way to do that was to borrow less principal.

Somehow, I am guessing, statistically, no one currently in residential or commercial forbearance is doing that.

“Commercial mortgages have a balloon payment at the end of the term, and when the loan matures, the balloon needs to be paid off or be refinanced. But when this becomes impossible, “maturity defaults could still be an issue,”

Yep, me too, my interest rate on my first home back in 1983 was about 18% in the northeast. Imagine that today-paying 6X in interest!!

Many homeowners that could pay their mortgage, and probably many renters, mortgagees and leasers took advantage of the 3 month forbearance just because they could.

The premise being that money inones pocket, and /or invested, is better than paying rent on time. However, most, unfortunately, probably did it because of hardship.

Yes I can imagine it.. if that did happen housing prices would drop to compensate.. housing prices reflect the ability of the buyer to service the debt to some extent.

Housing prices rose as the interest rates fell. However, housing prices are “sticky”, so if interest rates jump back up, people will do everything they can to avoid catastrophic losses.

I bought a 1-bedroom condo during that time, and took a loss when I sold it 8 years later.

2B and Implicit:

People of your generation still believe in the 3X income conventional wisdom. Which may have made sense in an era of 18% (!!!) mortgages. In an era of 3-4% mortgages, that 3X income is obsolete.

Simple example: $100K mortgage at 18% = $1500/mo

That same $1500 payment at 3% will pay for a $350,000 mortgage.

And what do you know, in 1983 median price of homes was $75K. Today it’s…..drum roll please…..$320K. Which is 450% higher than 1983. So yes homes are somewhat more expensive today vs 37 years ago, but not really that much, when accounting for interest rate. And also, the typical home is much larger today vs 1983, so on a per sq ft basis it’s basically the same.

Income has stayed the same for most people or dropped during that time while most things went up in price in addition to housing

Property taxes, HOA fees, insurance and utility costs have all skyrocketed, as a percentage of income, since the bad old days too.

And all that goes into how much house you can afford.

And fyi, buying a house then and now the “golden rule” was no more than 28% take home pay for all housing expenses.

Random

Excellent interest rate inflation / deflation comparison. ;-)

Random,

Going to disagree. If people stuck with the 3X figure, houses would be more modest and less expensive.

It’s not what you can afford when you are working full time, it’s what you can afford when you’re not working. I have lived by that and it is the main reason why I retired young.

They’re expensive because of mark up and everyone has the idea that they always sell for more.

Flat panel TVs used to cost $8000 for a 42″ on the low end. But global production brought the price down. Look at the price on the Cheap china made home fixtures and stuff. There is no way there is tons of markup. And houses today are stapled together, wrapped in saran wrap followed by vinyl siding.

Just need to change the idea that the prices always go up somehow.

True taxes have increased. But outside of extremes like CA or NJ, taxes as a % of total housing cost is quite low.

“And fyi, buying a house then and now the “golden rule” was no more than 28% take home pay for all housing expenses.”

Agreed. And that is my point exactly. Housing expenses is what matters, not the price of the house. It’s all about the interest rate, not the purchase price. Yet 99% of talk about real estate whether by bulls or bears focuses on purchase price. Have prices gone up or down matters a lot less than have interest rates gone up or down.

High interest rate is better for first time buyer.

A. Principal price will be much lower (the world operates on how much a month.)

B. Future opportunities to refi to lower interest rate versus being locked in at the bottom.

C. Opportunities to pay down principal much easier

D. More returns on other savings.

E. Mortgage interest deduction is higher

Give me much lower principal and higher interest rate any day

When home prices fall 20 % in 3 years it won’t make any difference what your interest rate is.

Real estate taxes as a % of selling prices are about the same in TX and NJ

There is a big correlation with high interest rates and inflation.

If everybody pays 18% interest on a mortgage that the likelihood that next year your wages will increase by 10% is very high. With 3% that is not so likely so 3x income is not obsolete because interest rates are low.

“When home prices fall 20 % in 3 years it won’t make any difference what your interest rate is.”

I’ve been hearing this for 7-8 years.

Woe to those who trade on logic. These markets operate on a lie that transcends all matter.

Maybe it is time for barter to make a comeback? In Shiloh1’s recommendation – flea markets, garage / estate sales – this method of commerce would work well. In addition, it would be more efficient as it keeps any income from going to the state via sales tax/ income tax…

Barter doesn’t work because the odds of two people simultaneously having what the other wants (and in the right quantities) are vanishingly small. Unless one of the two has a few standard “barter items” that aren’t taxable upon trade… and the other is willing to use those as money. Durable, fungible, store of value… Used to be cigs and booze would do the job. Nowadays?

You rock! Explains my life, and why I have money in the bank (none in the stock market).

Waiting for the BAIL-IN for the banks, earning< 0.1%. Good planning!

Ths wil get a lot worse before it gets better, these are early days yet and it will take time to play out.

I have a friend whose family owns a few motels. He’s not involved personally. Not a fun business from what he tells me. But profitable. He said they’re doing OK so far, treading water, but he is worried what will happen if the lockdowns return in full again.

They are going to run out of acronyms for SPVs

LOL but not likely. There are 33,696 possible 3-letter acronyms where the first is a letter and the 2nd and 3rd can be letters or digits. There are 1,213,056 possible 4-letter acronyms.

(Used to have software that would search online for all the existing ticker codes for NYSE and NASDAQ, by trying each possible code and looking at the server response…. exactly the same math there for the potential combinations. Someone at the exchanges eventually got smart and published the official listings.)

I suggest Spinster Avenue or Old Maid Circle. LLCs of course.

“So long and thanks for all the financial services.”

“The SPV at the End of the Universe”

What’s the most important thing you put in a bank and when was the last time you actually did it?

I’ll play….

“Trust?”

[Commercial mortgages have a balloon payment at the end of the term, and when the loan matures, the balloon needs to be paid off or be refinanced. But when this becomes impossible, “maturity defaults could still be an issue,” Trepp said. “If that is the case, the expectation would be that the increases in the delinquency rate going forward should be smaller than what we saw in May and June.”]

Shouldn’t this instead read “If that is the case, the expectation would be that the increases in the delinquency rate going forward should be greater than what we saw in May and June.” ??

Ian B.

The sentence is correct. It discusses the “increases” in the delinquency rate. The delinquency rates “increased” in May by a month-to-month record of 481 basis points (from 2.3% in April to 7.1% in May, and in June by 317 basis points, from 7.1% in May to 10.3% in June.

So Trepp expects the “increases in the delinquency rate” to be smaller than both 481 basis points and smaller than 317 basis points, so maybe an increase of 280 basis points in July, which would push the delinquency rate in July to 13.1%. So it expects the delinquency rate to increase, but at a slower pace.

With bad news like this and earnings season approaching, we need to think outside the box. How about a BLS style “survey” to determine reported earnings? That way like the BLS employment rate, Wall Street can drop all pretense of using things like math, facts, critical thinking skills to post their “profits” so they can partner with the Fed in making the stocks go up. Sounds perfect to me.

?

Creative accounting has already started with:

– suspension of Mkt to mkt accounting standard replaced by ‘fantasy’ value accounting

-GAAP and Non-GAAP reporting

-Reducing the ‘reserve’ loss ratio to increase the value of assets

– A ‘good will’ business ‘credit/debit’

-Forward PE is always ROSY to the trailing one

“creative” accounting has been a sham from day-2.

On day-1, it was used to keep track of the “real-time” [present-time] status of all incpme and obligations , as the rising volume of transactions overwhelmed the owners capacity to keep it all in mind.

On day-2, it became creative in order to be able to show interested-outsiders what was happening, i.e. tax collectors and all kinds of other noses.

“Mark to market” is itself a kind of fantasy accounting — it can give considerable latitude depending on interpretations of “market value,” and how much market value fluctuates depending on boom/bust trends.

One of Enron’s biggest victories was getting approved for mark-to-market valuation. The next step, they joked, was valuing assets based on “hypothetical future earnings.”

Difference between TSLA and Enron

Enron lied when it stated that it would have future FCF while TSLA does not lie when it when it estimates that it will never have FCF in the future

Wolf,

Just this morning I was contiplating how much the governments have intruded into our life by what regulations you needed to build a home.

Back in the 1950s, you and your neighbors helped to build your home as there were no regulations on how to build it.

Today, you need at least 7 certificated different trades all have to have updated safety programs with updated safety equipment as they expire.

A minimum 12 different building inspections and safety inspections. Heavy fines for any infractions to get an occupancy certification.

Any work becomes outdated to new technologies have your old stuff obsolete.

From experiences renovating 1950s, or earlier, houses…

There are some damn good reasons for those codes and inspections.

Yea, they protect the banks…..

It depends on where you live Joe. I am a builder and know this.

The only mandated trades with inspection regimes are electrical and plumbing. In rural, it is just electrical, but sewage must be cleared through a health authority.

Permits are mandated/controlled by local Govt and must be signed off either by local inspectors, or increasingly by an engineer.

A local builder with a good rep often/usually receives a cursory drive by or phone call at different phases of the project….even in the most rigorous areas.

Regardless, even in areas with no building inspection (where I now live) it is a fool who does not build to code. I take photos at every stage of completion while walls etc are yet to be buttoned up. My son pulled the electrical permit on my last job, (my own rental) and the inspector didn’t even come by for a look. I’m not sure he even looked at the images I sent in by email.

New Home Warranty programs require contractors to be certified members of the program. A new build cannot be covered under this program, otherwise. When that happens someone must live in the house for 1 year and then it can be sold as a used home.

However, I very much agree with your assertion that new construction standards are insane and often self defeating. I use tarp paper instead of building wraps. Air tight wrapped houses are prone to condo disease and rot. Tar paper underlay allows water vapour movement through the structure.

regards

So your opinion is that tarpaper or asphalt felt paper is better than, say, Tyvek?

Joe:

Don’t know where you lived in the “1950’s” but have to disagree that there were no regulations when buying a house.

My first house purchased in the outskirts of SF CA had “regulations” and house inspections.

I would rather have those “rules of the game” to protect me (and cost some “vigorish” on the side to the politicians) than not.

Inspections and other rules and regulations as well as actual building codes vary widely from place to place s7.

Last new house I built, circa 2000, ( not in CA,) required two inspections: Septic permit was $50 and included that inspector, an employee of the county health dept, being present and watching every action of the contractor, after he had done the ”perc” test himself and approved the location. The other was $75 including ”temp pole”, rough in, and final electrical inspection by a state employee.

Last new house I built in CA, circa 1990, included plans signed and sealed by PE Structural Engineer, Licensed Architect, and GC, and cost $22,000.00 for only the building permit — not PB or EL or HVAC — that took six months, not to mention the other fees from PG&E, etc.

My understanding from a friend currently trying to build nearby is those fees have approximately tripled in CA.

Let me get this straight. The world is drowning in debt and facing mass insolvency due to too much liquidity, so the answer is to inject more liquidity and induce more debt? Is that right? So what they are saying is we can cure debt based insolvency with more debt?

What could possibly go wrong?

LOVE THAT!! Yes what possibly??

Well, they can nuke all these malls and build shiny (made of glass and PVCs) new condo buildings with all that money that don’t know where to go.

intosh,

Yes, that’s already happening (sans the nuke). The two entry points:

In a place where property prices are very high, such as San Francisco: A mall landlord with enough resources doesn’t default on the mortgage but tears down part or all of the buildings and builds high-end housing. This only works where the land itself has a lot of value and where housing can be sold/rented for a lot of money.

In places were housing and land prices are not that expensive, it’s better for the landlord to walk away from the mortgage and let the lender have the property and take the loss. The lender then sells the mall for a song, so that the buyer (property developer) has a low entry cost in the property and can then tear down the mall and build housing or mixed use and come out ahead. This is the more common option.

These deals can be complex and will require re-zoning. In places like San Francisco, they can drag out for years because the surrounding community has a right to get involved, and it can delay or block the plan (NIMBY). Their worries may be congestion, inadequate infrastructure, dust and pollution from the construction, and the like.

” landlord to walk away from the mortgage” = gets to keep all past profits, [including other, substantial benefits].

“lender have the property and take the loss” = whoever is the final backstop, i.e. the banking trade and its master, the FED, which ultimately translates to obligations passing thru to society-at-large, namely u and me.

Someday, perhaps, we will get to understand how brain-syphilitic Woodrow Wilson was chosen by Warburg et al to become their owned-President and sign their Fed Res into law.

In the last couple of days I’ve seen news that SF residential real estate is in total turmoil. It’s unclear whether it’s the rise of WFH culture, shuttered tech startups, people wanting to move to less crowded areas, or a combination of the three. Regardless, it doesn’t look like a good place to be a landlord of any type of right now.

Yes, I think “turmoil” is a good word.

i see lots of moving vans around town and it seems like they’re moving out, not in. but i also work very closely with prop managers and so far i hear that although there is a spike in move-outs, for now at least, they’re being filled back up fairly steadily.

in fact, the residential rental market is the one sector that’s been paying my bills. commercial and hospitality on the other hand: total bloodbath, tears all over.

Turmoil at median price of $1.35m

Lower the prices by 50% and the market will become hot again

Re SF RE…when you spend years tap dancing on the razor’s edge…eventually you are going to get cut in half.

If over 20% of the nation is unemployed, just how does anyone make a profit selling more empty high end condos or apartments? I do not believe that the economy is going to do anything but contract for sometime. What happens when the owners of a mall tries to sell or redevelop a dead mall?

Dan Bell is standing by with his video production crew.

But the glory days, especially for business travel – the most lucrative segment for hotels – may well be gone

Yes, they are gone. I had booked a flight, prior to the outbreak, on Norwegian Air Lines (NAL) re: Los Angeles to Paris, France for March.

I received an email in early March from NAL letting me know my flight had been canceled. I rescheduled for Sept and I’ve just been told it was too just canceled. The NAL agent helping me with my refund (if I ever get it) indicated the company was close to filing bankruptcy and canceled the flight due to financial concerns. It’s all coming down together.

Kasadour: Norwegian Air Shuttle (NAS) has been flirting with bankruptcy for years now. They have just completed a debt for equity swap which has left the company in the hands of the main creditors, meaning leasing companies such as BOC Aviation.

Last week the new owners cancelled their maxi maintenance contract they had with Boeing, meaning they’ll have to sign new ones if they want to resume flying. I strongly suspect they’ll end up selling all their Dreamliners (the aircraft you were supposed to fly from Los Angeles to Paris), or the new owners will simply take them back and lease to somebody else.

NAS is not behaving nicely: among other sad things they presently owe about $400 million to customers like you who have seen their flights cancelled. This has led to a class action lawsuit in New York: you might want check into it if you don’t get your money back.

Finally a word of advice: while Air France, Lufthansa and other companies have already announced a schedule for resuming long-range flights from here to October it’s likely regular direct passenger flights between the Schengen Area and the US will be the last to restart. Besides the healthcare concerns there’s a nasty tit-for-tat spat going on that we hope will be solved shortly. But as the saying goes hope for the best and prepare for the worst.

We received a €69 refund payment from NAS overnight. What a joke.

Meanwhile, some friends of ours drove to Venice from Saarbrücken last week for business and said Venice is a ghost town. Nothing is open, not a single tourist in sight- not even any ever-reliable Asian tourists with their selfie sticks. None of the big water taxis were operating on Grand Canal- just the smaller charter boats which were barely operating themselves.

Bankrupt airlines, flight concerns from US to Schengen areas, I don’t see how Europe will survive. I suppose, as Mr. Richter puts it, these truly were the “good times”.

Summer of 2019 was in many ways our ‘summer of 1914’: rising tensions, but still glorious and even Golden compared to what we now face….

Like 1914, we are seeing the inauguration of decades of decline – and that’s being optimistic.

Japanese and Korean tourists may start to come back in the late Summer/early Fall but the Americans and the Chinese won’t be back for a very long time, if ever.

This will affect all those destinations like Venice which depend on extra-European tourism: Barcelona, Florence, Paris, Rome… it will be interesting to see how the AirBnB catastrophe will trickle through these real estate markets and what idiotic measures will be taken to prevent the bubble from blowing up and perhaps inflate it a bit further.

Ordinary European destinations have started to see tourists trickle back, but compared to the past glory decade this is just that: a trickle. Numbers will slowly pick up throughout July and August, but everybody is looking nervously over his shoulder at what our politicians will do. While they fancy themselves Winston Churchill during the London Blitz, they would have waved the white flag the instant the first bomb fell from the sky. Things have indeed changed forever: as a commenter here wisely wrote a while back “politicians are nowhere near as harmless as they appear”.

One thing to add to all this, as far as putting people in restaurants, pubs, planes, is the actually amazing extra costs of doing this. I’m talking about PPE , hand gel, masks, distancing. A good example is the British health service which has spent an extra 4.5 Billion Pounds on PPE since all this started, an incredible amount. Even if they all open up, it’s doubtful if profits will be made and if you don’t make a profit, you usually make a loss.

Next bomb to explode!?

239 Experts With 1 Big Claim: The Coronavirus Is Airborne

The W.H.O. has resisted mounting evidence that viral particles floating indoors are infectious, some scientists say. The agency maintains the research is still inconclusive.

But in an open letter to the W.H.O., 239 scientists in 32 countries have outlined the evidence showing that smaller particles can infect people, and are calling for the agency to revise its recommendations. The researchers plan to publish their letter in a scientific journal next week{..}

cnbc/nyt

“239 experts ” That is the problem.

No, in this case, WHO is the problem.

There are far, far more than 239 experts disagreeing with WHO on the airborne-vectors issue.

I thought 322 experts already said it was airborne. *shrug*

Crazy days and nights for sure.

I am honestly and genuinely surprised we are still forced to listen to the OMS/WHO after what they have done over the past few months. This is akin to taking a fire safety course from a convicted arsonist: beyond ridiculous.

That organization must be cut off from all funding until they have told us exactly what happened between them and the Chinese government. If their “advisors” and “researchers” need private jets and diplomatic passports to skirt travel bans and quarantines around the world they should ask China for help.

Oh yeah, and to be honest I am starting to be a bit tired of all these “experts” who may be authorities on viral infections but wouldn’t pass a Physics I or Biochemistry exam.

I’ve heard so much silliness originating from these folks I want to ring Ellon Musk and tell him to start funding research on Covid-19, not to develop a cure or a vaccine but to obtain the secret to bypass Newtonian and Einstenian physics. That way we can have a stealth flying car able to time travel without even needing a power source.

I’ll be honest here: I shouldn’t have paid so much attention at the Uni. I wouldn’t be so tempted to smash my head against this stupid table each time some “expert” opens his mouth.

MC01,

One expert you might appreciate is Vernon Coleman, a medical doctor who has written many books. His youtube channel is quite informative. As a physicist I agree with your conclusions on so called “experts.”

Nothing to worry about: my country, Italy, will be glad to sell you our surplus facemasks and all the hand sanitizer you may need.

We have so much of the stuff the local emporium (ironically run by a Chinese family from Hubei) will give you two free surgical facemasks for every €20 spent and is selling hand sanitizer at 50% off. All good stuff, not made in China junk, low price low price until stocks last. ;-)

If you need more sophisticated medical equipment such as CT scanner spare parts or chemotherapy mixing and dosing machinery, we may be able to help you. We have bought so many of them our hospitals have literally run out of storage room and since they need to reopen the wards where all this hi-tech goodness has been stockpiled we will cut you smoking hot deals.

Help us avoid the embarassment of a scandal five years down the road when this life-saving equipment will be found rotting and unserviceable in a crumbling warehouse by buying right now: our loss is your gain!

Countries like Senegal and Sri Lanka have already taken up this amazing offer and many others are lining up: stocks won’t last forever!

Here’s an additional data point for June delinquencies in the restaurant industry (NYC region):

“80 Percent of NYC Restaurants Did Not Pay Full Rent in June, Survey Says”

https://ny.eater.com/2020/7/2/21310016/nyc-restaurants-rent-payments-june

A non-CMBS anecdote. My friend who works for a midsize regional bank says 90% of their portfolio hotel loans on the SC coast are non-performing.

Many tourist area related hotels depend on summer income profits to make it through the rest of the year. I imagine by this time next year, there will be more bankrupt hotels than anyone imagines…..

In my part of the woods we have places like Spain and Portugal, who depend almost totally on summer tourists. Spain also has the double whammy, that it’s only other industry is construction, selling villas and appartments, to wait….tourists…. from both Britain and Germany who buy there to avoid rain. lol

Ouch!!

Short $KRE.

One can also look at this little factoid for a more realistic view of Delinquency rates as of Q1 2020.

PLease note that the rate for all Commercial loans was 1.61% as of Q1 2020 compared to 10.21% in Q1 2010.

https://www.federalreserve.gov/releases/chargeoff/delallsa.htm

I know, I know it’s going to get worse. Is that not the case always and forever ?

akiddy111,

WHY are you trying so hard to be such a moron? (I know you’re a smart guy)

1. The most recent entry of your linked table is for the FIRST QUARTER, WHICH ENDED ON MARCH 31, (in case you missed it). The last entry in my chart is for JUNE. The entry for March in my chart is 2.07%. The entry for June is 10.3%.

The table you linked will be updated mid-September to reflect Q2. I gave you Q2 today.

2. The table you linked is a COMPLETELY DIFFERENT category of debt: “commercial loans and leases” held by BANKS. What banks hold on their books and what gets packaged into CMBS are not the same things.

Wolf,

it would be interesting to correlate how many of these folks who are delinquent also have CLO that they have to pay off. I’m sure that’s a real deep dive into the financial statements in that case, but you have to figure some of these public companies have CLOs as well with various banks or institutions, or other investors. So we could be looking at multiple whammies when this heap finally all collapses.

There may be dual CLO/CMBS debtors but one limiting factor is that the same collateral can’t really serve two masters (I hope no lenders were this stupid…).

CMBS is defined by RE collateral…making it very unlikely to also serve as CLO collateral (“loans” being defined by the presence of collateral…versus bonds which are usually unsecured and packaged into CDOs).

I don’t *think* there are too many lenders so stupid as to accept another primary lender on the same collateral…and prices have probably not soared enough for second lien loans to have made sense.

But ZIRP inspires a lot of lender insanity.

This is random anecdotal but we drove outside the Bay Area for the first time in months this weekend, and for the first time in living memory the traffic was heavier outside of the Bay Area than inside it.

The rural, physical economy, agriculture and industrial production, seem to be doing fine. The urban human/social economy is what’s stuck.

Passenger #s on BART were down % 95 at its nadir in April. Two weeks ago numbers were still down %89.

I had a recent dental appt in Berkeley. The procedure took longer than usual. I thought oh no , a 2 hour commute back to Solano County via 24 and during rush hour. My phone stated 35 minutes. It ended up taking 35 minutes with stop and go traffic nonexistent

A Tsunami is rarely noticed from a distance. I wonder if all the people in winter sports are buying binoculars right now. Or is the white cane industry booming?

Social distancing on the ski slopes isn’t too hard, sort of different at all those evening post-slope watering holes.

Social distancing on the ski slopes was a lot easier in the old days when they still had single chair lifts. Now with quads and gondolas you rub shoulders with strangers all the way up the hill. One of the earliest and most extreme Covid-19 outbreaks was in Sun Valley back in March. It was so bad it sidelined the entire ER staff at the only hospital in the county. All cases after that had to make a multi-hour trip to another hospital. Think twice before buying those seasons ski passes folks.

Was thinking more of the financial wake. These things are another house of cards…one bad business season and they go under. Basically worth the value of the daily income of the core runs with everything else dependant upon that main revenue stream for the solid 90 days in the season. That gone, the rest mothballed, it all begins to deflate. Then the forced buyout at real cheap values. Of course, the stinking bankers will prevent investors from grabbing it. Right to their buddies in the club.

Once again this is more pressure on the meter toward deflation . On the other hand these properties that are in default might be acquired by the Fed via Black Rock and an SPV . Bundled up as stock and thrown into the insane NASDAQ. Stoke up the Robin Hood wacko’s and Bada Bing Bada Boom , pump and dump at 3x the value. Next throw a bond offering and dump it into the Calpers pension black hole. Asset is now duly inflated. With un-regulated financial engineering and the Fed gravity does not exist.

I dislike Trump and detest the democrats. What will happen to Trumps real estate empire as 1/3 of hotels in NYC go bust , prices on high end condos tube and corporations cut back on golf memberships

I have to admit my ignorance when it comes to Trump hotels. Doesn’t he simply lend his name i.e. he is in the licensing business as opposed to him owning the hotels outright?

Don’t really know. Unfortunately, lots of businesses and activities have been adversely affected by the coronavirus. For some, wonder if it might not depend somewhat on the SPV structures?

What does it matter? The Fed will just keep bailing out everyone.

And Wolf will regaile his short winnings. They are all amoral and sick.

Maybe. My guess is they will save too many, but will have to let the worse offenders fail to stop the excess speculation. It’s getting to rediculous as Amazon is 5 times sales and Tesla 8.5 times sales. Not sure any large company can sustain a value more than 3 times sales.

All aspects of our life and economy are under attack and stress including state and local governments. The Orange County Florida tax assessor’s office just lost a major RE Property Tax assessment case against Disney. This case goes back 5 years and will have repercussions throughout the whole state. Possibly the country.

https://insidethemagic.net/2020/06/disney-world-wins-legal-battle-tm1/

My very favorite scene in the movie Gone with the Wind is where Scarlet reunites with her now blind father after all the carnage and he is consoling her. She tells him all is lost. He says, “No, we still have the bonds.” Scarlet looks relieved and puts her head back on father’s chest but then a concerned look comes onto her face. She asks, “Daddy, what kind of bonds?” He replies, “Why Confederate bonds, of course.”

If you like finance and history the financing the war effort on both sides is interesting. If I remember correctly the North issued currency and promised to repay in gold and then tried to weasel out of it after war was won. Eventually paid if I remember correctly. South had currency that paid interest and more traditional interest bearing bonds.

As a kid I used to see some Confederate money and couldn’t understand how it was worthless.