Expensive markets face a new reality: lenders get skittish about jumbo loans.

By Wolf Richter for WOLF STREET.

It has been a sea change in no time. Banks and nonbanks – the “shadow banks” – are reducing mortgage lending and tightening up lending standards. Nonbanks, which include the largest mortgage lenders, are asking for a bailout because, as mortgage servicers, they’re facing a liquidity crisis. Home sellers are pulling their properties off the market because there are no buyers. The brokerage industry and the businesses that support it are reeling. In expensive housing markets, jumbo loans dominate, and they’re not backed by government guarantees and bailout programs. And the weekly data on mortgage applications shows where this is going.

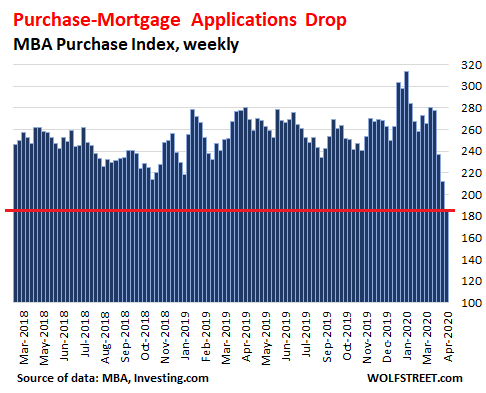

Purchase mortgage applications across the US during the week ended April 3 plunged by 33% from a year ago, the Mortgage Bankers Association reported this morning. A week ago, they’d plunged by 24% year-over-year; and in the prior week by 15% year-over-year. Since the multi-year peak in January, purchase-mortgage applications have plunged by 41%:

The weekly data on mortgage applications to purchase a home is now in the third week of going from bad to worse, under the effects of the lockdowns, the sudden explosion of the unemployment crisis, and the equally sudden tightening of lending standards.

In three states where lockdowns started first, which are also among the most expensive housing markets, the year-over-year plunges in purchase-mortgage applications were the most severe:

- California: -47.5% (from -36.4% the week before)

- New York: -55.4% (from -35.6% the week before)

- Washington: -59.9% (from -32.5% the week before)

This plunge in purchase mortgage applications is occurring even as mortgage rates remain near historic lows, with the average interest rate for 30-year fixed-rate mortgages with conforming loan balances at 3.49%.

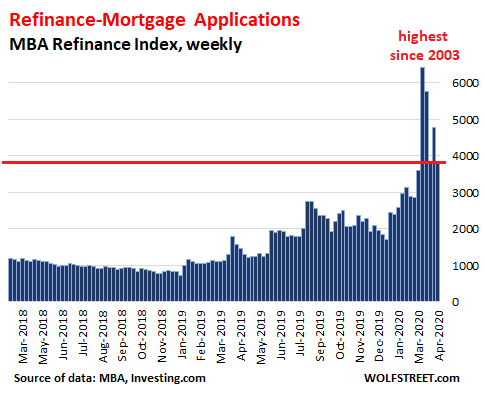

But these low mortgage rates have fired up mortgage applications to refinance existing mortgages. In early March, refi applications spiked to the highest level since 2003. During the week ended April 3, refi applications fell back in direction of earth but remained high compared to the past few years:

The MBA obtains this data via weekly surveys of banks, nonbanks, and thrifts that cover 75% of all US retail residential mortgage applications. Mortgage applications are an early indication of demand by potential home buyers. But they’re not an indication of demand by nonresident foreign investors and larger domestic investors that fund their purchases at the institutional level.

There are now numerous reports from all types of mortgage lenders, banks and nonbanks, how they’re tightening up mortgage lending standards and how they’re stepping away from certain types of riskier mortgages altogether.

Wells Fargo is one example. It and JP Morgan are the top mortgage lenders among banks, though nonbank Quicken Loans is now the largest overall mortgage lender. Well Fargo said in an internal memo obtained by Reuters and confirmed by a spokesperson that it will stay away from many types of mortgage loans including:

- Cash-out refinance loans,

- Most home equity loans above $250,000.

- Non-conforming purchase loans with down-payments of less than 20%

- Most jumbo-loan refis; it will only refinance jumbo loans of customers with at least $250,00 in liquid assets at the bank.

Wells Fargo said that applications for those types of loans were automatically turned down as of Friday.

Homebuyers needing a jumbo loan – which covers many homebuyers in expensive parts of the country such as California, New York, and Washington – are in for additional setbacks. Jumbo loans are those whose balances exceed the conforming loan-balance limits, depending on how expensive particular housing markets are. In most markets, jumbo loans are those with balances over $510,400. The limits for conforming balances are higher in more expensive markets. In the most expensive counties, jumbo loans are loans over $765,600.

These “non-conforming” loans are riskier for banks because they’re not backed by government entities such as the VA or Ginnie Mae, or Government Sponsored Enterprises Fannie Mae and Freddie Mac. The bank ends up with the credit risk.

And the new forbearance agreements that Fannie and Freddie and the government agencies are backing don’t apply to jumbo loans since those entities don’t guarantee those loans. And so the mandated payment holidays are now becoming an issue for banks.

Wells Fargo, in addition to stepping away from jumbo loan refis, also said that it stopped buying jumbo loans from other mortgage originators, including nonbanks. So these mortgage originators too get more careful writing jumbo loans because they may get stuck with them and carry the credit risk.

As lenders are getting more skittish about jumbo loans and less willing to underwrite them, they’re requiring larger down-payments and other criteria to reduce the risks of those loans for the lenders. This will make it even harder for sellers of high-priced homes to sell their homes. In some markets, this would impact only a small number of sellers. But in expensive markets, the majority or even most of the homes fall into this category. And those markets are going to be even tougher.

When the unemployment crisis exploded onto the scene three weeks ago, sales totally collapsed. What’s in store for the industry? Read… How Lockdowns Hit U.S. New & Used Vehicle Sales: Beyond Ugly

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I recently mentioned that driving down my street i saw 5 For Sale signs. We’re down to 2. Somebody’s buying.

Dumping stocks and bonds for real assets.

Houses are definitely better than stocks “currently vastly over priced” or bonds. But, depending on location, houses could fall quite a ways as well. It’s hard to say, where new jobs will be in future “and how much they pay”, as well as, if boomers do start to retire, will they start to sell off houses, plummeting the prices?

Depending on how much money you got, gold/silver is allegedly the only thing, that will actually go up. Just make sure it’s not paper gold/silver. Allegedly silver is better choice of the 2 right now.

Certain housing locations will definitely give huge returns, but predicting where, is the billion dollar question.

There are more millenials than boomers right now. As boomers sell, millenials will buy. And generationally speaking there will be more demand than supply.

Perhaps,

But, every area of the country is it’s own situation. Some will go way up, many might plummet. A lot of it has to do with jobs.

Also, alot more millennials seem okay with apartments, depending on where they are located, if they were new cities on the coasts that were primarily apartments, and resembled European cities. These cities could do very well and people there well off. If enough millennials and zoomers leave their parents cities, the housing market could collapse across the country. A very big IF I know, but, I know quite a few young people who wished such European like cities on the coast existed in America and would move there immediately. There could be commuter cities with houses surrounding them as well.

Exactly correct Gold and silver is the place to be Certainly NOT in overpriced particleboard shacks with ridiculous carrying costs like HOAs , insurance and taxes

I mentioned to a real estate broker friend that homes will come down in price in a big way soon and she agreed with me which is unusual for brokers to admit

Government can simply order you to sell your gold at its preferred price.

When will the mortgage rates drop?

Bead,

Not if they don’t know you got it.

Gold and silver should be ideally purchased in person and stored somewhere securely. There is a max amount you would want to store this way though.

When deflation happens, it affects all assets. It is leveraging in reverse.

Deflation then inflation at some later point “within a couple years” is my and many others guess.

Excuse the intrusion, but I’m unclear what the numbers represent in the vertical scale of the mortgage applications for purchase chart.

It sits at just a tad over 180 for the week. OK. 180 what? Total applications in the U.S.?

If someone can enlighten me, you’ll be giving vision to the blind.

And receiving my gratitude.

Steve M

It’s an “Index” — the “MBA Purchase Index” as it says in big font on the chart, and the number 180 is an index value. It’s like the Case-Shiller House Price Index, the S&P 500 Index, or any of the other millions of indices. An index shows you the change of something compared to prior index values.

As with your articles, thanks for the education.

Sometimes I miss the obvious. Not to fret though. When I do, it eventually smacks me in the face!

Wolf, junk bonds up 8% just today. Is that for real. How much money did they print. Lol

Feels like next leg down?

There’s next to no inventory. The shock won’t come until after this is all over, when the held-back supply comes online, while demand is weakened by job loss, damage to personal finances, etc.

This coming Oct-Feb is going to be the best buying opportunity since early 2015.

Possibly. Maybe a bit quick for the housing market, even with the stupendous collapse of the economy? With mega bailouts coming housing will take awhile to accumulate marked to market comps. However, if no housing bailouts are forthcoming then could be a trap door for sure.

The US does not have a National housing market. Some will sail through it others will still be dropping in March ’22. And than you could have local hotspots with very high death rates where the number of vacant by death is noticeable. Like what could possible happen to those communities in Florida where “everybody” is a pensioner.

Who will be the first to hawk 4th horseman-backed securities .. ??

2008 AIG London derivatives desk didn’t think U.S. had a national housing market either.

They will still be boring as heck and full of bad drivers and poisonous critters lol

It took until like 2011-2012 for the housing market to find a bottom in a lot of markets. You can go find wolf’s charts to check me. Although, I assume prices will fall barring the Fed doing more priveleged bailouts under pressure, but if this turns into a deep heavy recession, it might take awhile longer than until next winter to find a bottom. Housing remains a consumer product meant to be lived in, and unless the jobs come back quickly or the govt decides to do ubi, prices will probably be depressed because people won’t have the ability to buy (until a low enough clearing price is met ;) ).

Housing will scarfed up by the private equity when the rental cash flow numbers are favorable. Just like 2008 and beyond. The idea that millenials will purchase homes en mass is ridiculous. Among my boomer friends, the single women talk of co purchasing a large house to share.

PE will be strip mining NYSE listed companies, once the valuation gets low enough, and the stock floats of these companies are small, because of buybacks. The companies themselves are zombie-like, having lost their connection to real earnings, they have a lot of bloat. Normally the system would cleanse itself in a recession, but the Fed prevents this from happening. What they haven’t figured on is money on the sidelines, funneled through PE, which takes a stake in these companies. Investors want to own good businesses, not over valued stocks. Real Estate moves too slowly, and states mandating affordable housing. RE market may be able to hold prices at near current levels, but the action between buyers and sellers will be missing.

Endeavour, I just saw a WaPo headline detailing this- an economic downturn will create the perfect opportunity for investors to sweep up distressed housing. To which I wonder, what is the “free market/ capitalist” answer to prevent housing-wealth from going to the top? How can we give homeownership back to working-class Americans if every time there are drops in prices the demand from wealthy investors spike? Theoretically, increased supply would address this. But nobody can build “affordable” housing when it isn’t incentivized. SF came out w/a study recently a single affordable unit costs ~600k to build. The LA times posted today they found several “affordable” complexes that cost 900k per unit.

As an older millennial, I want to buy. I do not want “apartment living”. And I dont need a gigantic house. I’d love a starter house, but starter houses are swooped up, flipped, & put back on markets for more than affordable. Or rented out as “cash-cow investment” (real quote from a listing on Zillow).

I don’t have much faith in a free-market answer to housing affordability. I think housing needs to be the next “universal health care” debate.

2015 wasn’t a good buying opportunity in my area It was actually a great selling oppurtunity Real estate will not be a good “ using oppurtunity” by this fall in my opinion anyway I’m thinking 5 years out perhaps but I’m not sure I want anything to do with it at all frankly

A sample space of 5. LOL

Were there Sold signs or just fewer For Sale?

The 6 month sales agreement expired, seller decided not to re-list.

Can you imagine, you are in a lockdown, and your looking for a new house?? Why not look for a new State?? Everybody I know in Cali is looking to get out of dodge.

Even landlords will be reluctant to buy this toxic stuff, how long will tenants be able to ‘rent’ without paying the monthly? It’s all unknown, except one thing the stupidity of your elected asset transferal politicians is a known-known, that they will transfer the good to the bad.

Michael Gorback,

“Somebody’s buying.”

No, but they did what everyone else is doing and what I called out in the first paragraph: they’re pulling their properties off the market. This is happening in massive numbers. And it makes sense in this environment.

BINGO

Would you really want a stranger, possibly infected rummaging through your house?? Mask or Not?

I think most people know that this thing is going to take a long-time to clear,

Do you really want a ‘lockbox’ on your front door during a lockdown??

That’s what happens when everything is LOCKED DOWN! There will be FAR more damage cause by the lock down both short-term and long-term than the Coronavirus will ever do. IMO. Only time will tell.

Fear, suicide, damage to the economy and country,….

A good lock down is cheaper then getting herd immunity. And not only morally because fewer deaths.

Yes. That’s exactly what happening.

Sellers don’t want people in their homes.

Listing agents don’t want to hold open houses.

Inspectors don’t want to inspect.

Appraisers don’t want to appraise.

Notaries don’t want to notarize…..

Transactions after indeed occurring, I know, I have a few, but, it’s significantly less than pre- lock down.

> i saw 5 For Sale signs. We’re down to 2. Somebody’s buying.

Wrong — three people gave up.

And one REALTOAR tried to spin it, and failed. Better luck next time.

In New York City generally, it took 6 – 8 months to evict a tenant = before the coronanova virus. I think most would say 8 months is probably fair estimate. Now court are closed; eviction paperwork will be piling up.

Piling up — 2008 mortgage foreclosure paperwork piled up so high that took 2 years to evict someone.

Landlords may have to be prepared for a 2 year eviction process. Guess who has the most votes in NYC Landlords or Tenants….

Real Estate as an investment is essentially wiped out; no Judge will throw out a family with an out of work provider with coronavirus.

Some people are buying, but don’t confuse the drop in For Sale signs as pent up demand. Active listings have plummeted across the globe, with the worst drops in areas hit by restrictive shelter-in-place orders. There’s a reason Redfin and EXP just furloughed a boatload of agents. The demand destruction is real. The massive unemployment jump is already causing ripple effects. The disruption in the mortgage markets is just adding insult to injury.

Anyone thinking you can shut down the world’s largest economy for 2 months (or more in some areas) without some serious negative consequences is in for a rude awakening.

I’m staring at March pending sales data that points to double-digit declines across the board here in DFW. Closed sales will be positive for the month, likely the last positive year-over-year comparison we get for the rest of the year.

Or the homes are being taken off the market

More likely they took their homes off the market due to the lack of buyers.

They probably took them off the market!! My neighbor had 11 offers the first day on the market!!! That was in November!!! She was soooo lucky. Timing is everything!!!

If a jumbo loan starts above $765.2k and you need to put 20% down, the you will be financing about $605k or more. If I have to leave at least $250k in the bank then it’s like I’m borrowing only $355k. I’ll just pay cash if I want the house. Then wait for a better deal. Interest in Treasuries is close to zero anyway.

I think the piece is about the effect on purchases requiring a mortgage.

Sorry, but I’m not a fan of your numbers as they are wildly inaccurate. Jumbo loans start at $765,601, so you can purchase a home with 20% down starting at $957,002 and up to $2,500,000. You’ll need anywhere from $30k to $140k of reserve assets to qualify. But Agency (Fannie/Freddie) loans will still allow you to qualify with 10% down and a maximum loan of $765,600 ($850,666 purchase price) and no reserves.

Paying cash when mortgage rates are approximately 3.5% is a horrible investment. Alas, treasuries are not the same as Mortgage-backed Securities. Don’t expect rates to move much lower from where they are currently for a variety of reasons. (increased default risk, production capacity to name a few).

Both Schiff and Gammon are saying house should be shelter, not extravagance, but at these rates get longest fixed rate term as possible.

“Paying cash when mortgage rates are approximately 3.5% is a horrible investment.”

No. It’s a guaranteed 3.5% return. You can’t get that anywhere else.

Yeah, but most people don’t have cash, a lot of it, sitting around. I mean cash not borrowed. They just don’t get it.

Do you ever bother to calculate your opportunity cost when you consider tying up most of your wealth in the most illiquid investment available?

@Lisa

I have owned my house (free and clear) for the last 30 years (approx). I have no debt. I don’t invest in houses to rent (or Airbnb).

So yes, I have computed the cost to NOT renting and living in a great community with similarly situated folks. I’ve never had a liquidity problem because I live within my (very simple) means.

I was very lucky in business and even luckier in the inheritance field. When I talk about buying houses, it’s for my kids. I am willing to pay cash up front in the price is right. It’s part of the long range plan.

I don’t count so-called opportunity costs. I just count the cash at the end of the year. If it is more than what I started with, then fine. Very simple formula. Return OF capital is above most others.

Finster has it right. Buying a home with cash, or paying down a mortgage, is buying a guaranteed bond at 3.5%. If need bonds in your portfolio, you are an idiot to buy them if you still have a mortgage to pay off.

@Happy1 – I’ve a bond portfolio paying 5-6% and my mortgage is 4%. Even my cash is bringing in 2.5% for the next few years which brings my mortgage finance cost to 1.5%, which I will pay to be liquid. Just part of the cost of ownership along with the taxes. (I would pay the home off if there were no taxes – just for the rush.) There will be a time to deploy cash – and I will not need to sell a house.

Correct, expect actually they’ll still go down to only 5% down.

Watch out though, those rates are high and so is the PMI

There’s a big difference in being a cash phd.

Not quite. It’s not the value of the house that determines whether a mortgage is jumbo or not it’s the mortgage itself. A $1M house with $300K down is not a jumbo mortgage. a $770K house with $0 down is a jumbo mortgage.

These examples are for the $765K areas.

Correct.

And the 765k doesn’t apply to all counties either.

Jumbo Mortgage starts at $480,000

WF announced that you need the follow

24 months of full mortgage payments in cash in WF.

20% down in cash

This includes refinancing.

You will not even get a refi or home loan at this time because no one wants to make a market prediction right now.

The market prediction is a 50% drop in all prices.

Sellers will have to make up the lost of equity at closing.

Which in most cases the sellers will owe more money at closing then the buyers purchase price.

Chef,

Pretty much everything you wrote is factually incorrect. Please don’t spread that misinformation and burn the originating source.

I don’t want to drop names.

Sometimes ago, key (&peele) appeared in ad for Rocketloans or quickenloans? So, these are the shadow banks? which are exempt from the regular banks. These rules are set in place following great crash of 1929.

If this means, lords of the money (money-changers) invented a by-pass mechanism set in place since the great-depression and GFC.

Anyway, if (and when) my grandkids ask me, where were you granpa, when that COVID-19 crises, I would tell them, I was then totally clueless, let everything happen. I was stupid, that I never got rich out of that…(situation)..”

If it were only that easy, loaning to people who cannot repay means that you have to give 1/2 your take to your muscle, your collection guy’s. Think mafia

Do you really relish not hanging with this crowd?

Once you enter the void of loans with no collateral, and no means of payment, and no intention of payment. Then threatening & physical harm to family members is the only means, worldwide this is how its done.

Why is it do you think the mob goes ‘legit’ as soon as they can?? Second generation? Live in the gutter, die in the gutter.

If you really want to be rich, then find some rich people, study their habits and emulate them.

You could be the richest ‘junk yard dog’ in your slum, but your still a junk yard dog.

Renting to people who can’t pay the rent is insane. Loaning money to people who can’t pay payments is insane, sure you got a contract that say’s an unemployed guy will pay 35% (INT only, no principal-Get $20, pay back $100, sell for $50 ), sure you can sell that paper to another sucker for 1/2 the face value, now that’s how the ‘rich’ get rich by offloading worthless paper to greedy idiots.

One of the best rackets around is ‘medical factoring’, most dentists&docs don’t want to bother with collections, so they charge 10x for treatment, and then sell the bill for 60% of face, then they get the cash up-front, and actual collection, insurance, and getting blood from a rock is not their problem. That’s another way that rich get rich, they buy these medical factor fronts, package them and off load them to the public as ‘assets’.

LOL, nonsense.

Yours is obviously a statement by a non-player watching from the nose bleed section of the bleachers

Are you disagreeing with his last paragraph or the other parts?

I’m no poser, you’re right, you are no poser — you are a tool.

It’s not just rental suckers. It’s also selling on credit suckers. Finally, it’s lousy bond buying suckers. There’s a sucker born everyday.

Your medical factoring discussion is nonsense. It doesn’t work the way you describe at all. No one I know does this as a billing or collections strategy. Insurance is far too big a component. And collections are so far below 60% for the rest no one would pay that amount.

So now risk pricing is “in” again. And this time the Fed can do nothing about it. Unless it also becomes a retail banker (competitor of normal banks). In which case it is “game over” for anything that even smells like a bank. I think I’ve read that maybe the ECB is thinking along those lines as it has completely fooked all the EU banks with ZIRP.

I would think that a 500k mortgage on a condo in Manhattan

is normal.Why would they back out of that market.

Most one bedroom condos cost over a million in manhattan.

Yup ,which is vastly in bubble territory I sold a house to a guy who bought two 1 bedrooms in a nice area in a nice building in 2006 for 450k each and that was at the top of the previous runup( bubble) Prices will correct vastly soon

Because it is a small market which will seaze up during periods when house prizes drop. Living an hour away is possible if you expect you would otherwise loose $100K

The MLS numbers for March are for deals that closed in March, they were entered into in February for the most part.

The Market was doing fine…

Then the RE Market died in Mid March, the numbers for April will come out in early May and look bad…

The May numbers will come out in early June and be horrific.

If you need to sell, and some do, price at 10% below the best comp and hope for enough interest from buyers to get a little boost.

If you are a buyer, unless it’s a one of a kind property there’s no reason not to wait.

Brokerages need transactions, while the price is not immaterial it’s the number of deals that really matters.

During depressions “ One of a kind properties” are a dime a dozen I bought one in 92 and it was prime and sold for pennies on the dollar and that was just a recession It’s NOT a good time to buy right now If you do, you will kick yourself later Buy gold and hunker down Sleep better too

Notwithstanding the constraints on jumbo loans, makes sense, people are afraid to go out and look, Realtors are reluctant to show properties, sellers don’t want strangers in their houses who might have “the virus” and traveling notaries don’t want to meet with loan applicants.

Representing a condo in Manhattan. This week interest picked up. May have an offer in the next day or two. buyer saw the virtual tour.

Online notary is legal till things allow in person closings.

DCR…………….. some people always buy at the top of the market

Way to early to be looking at purchases. Give it at least 6 months.

Not sure impact in the 1% income areas, but there will be much lower entry points for the remaining 99%.

It is stunning how quickly this country turned into sheep seeking a safe space. I was working outdoors with my excavation equipment. Got off to shoot grades….neighbor inquires ( from a very safe distance ) what I am doing. I explain the work I’m doing for my client. Proceeds to ask if this is deemed “necessary”. At this point I have been bingeing on the podcast disgraceland. How would these rock stars have answered that?

But I smile and say yes. Is this the USA or CCP?

My grand kids will never experience the freedoms that I have.

Shame on us.

Tom,

Yeah, working on an excavator by yourself is just so dangerous for the community. (sarcasm alert!!) We’re still logging in logging country, all machine work.

One thing I say every time I see someone like you at work, “God, it’s nice to see someone still working and earning a pay cheque”.

Road bans just lifted, and hill roads are muddy, but the

loggers are still working near me as well!

Not sure on the hardwood loggers, but I would think with the world wide run on toilet paper the pulp cutters would be busy.

Cosmopolis Pulp Mill got itself certified as a “critical business”.

I can confirm that them logs been flowin’ the down hill all week.

what do you expect from people who would stand in line to hoard on toilet papers ?

Tom, you yourself will never experience the freedoms that I did as a much younger person in the US. This US is no longer the country I was raised in. Leviathan will continue to grow until it dies poisoned by it’s own wastes.

Me Too Lisa: sister, 6, and I, 8, could ride our old nags over 2 counties in the early 1950s,,, and/but, anyone who did see us would call mom and let her know where we were, etc.,,, as almost everyone knew almost everyone, etc…

similarly, as teenager, mom would come home from work Monday afternoon, and tell me everywhere I had been, who with, and what we did the previous weekend, almost always totally correctly,,, more freedom, yes,,, but more responsibility too

different world, for sure

The real fun will start when sycophants will arrive in your area. Just give them enough time to understand the world isn’t ending this time around and they will emerge from under their beds to ring the police and demand they go and harass dog walkers and children playing ball in their parents’ yards and to post pictures of passing traffic on social media to “name and shame” imaginary criminals. Politicians love this scum: just read any local newspaper if you still have the stomach for it.

Crises of all kinds bring out the best and worst in people, the chief difference being good people have been up and running since the beginning while the lowlifes start to come out (and sadly getting way too much attention) once the danger was over.

This crisis is no different, and it has exposed for us all some people we knew in a light we hadn’t seen before. Some relationships will be strenghtened, but many many more will be destroyed: nobody wants a sycophant for a friend because who knows when he’ll turn on you like he turned on his neighbors and even complete strangers?

I agree with everything that’s been said above about sycophants, the worst kinds of people now crawling out from under their rocks to try and limit the freedom of others. However, I’d use the word “authoritarians” instead. I think during this lock down I’m going to have to pull out my old copy of Eric Hoffer’s classic.

Stephen,

You might want to pick up some of Edward Bernays’ books as well. It’s a shame he is only taught in the “best” schools.

My father-in-law just passed away 5 days ago and we will be dealing with his house in the medium future. While it is currently empty, (but furnished), just dealing with ‘issues and stuff’ to finalise (including grief) means we most likely won’t get around to listing for several months. I did notice there is very little inventory in his small city (35K) and what is listed still sells pretty quick. It is the kind of town that attracts retirees and flee buyers. So, we’ll see. Regardless, if we list by autumn we’ll have a better idea about the Covid recovery prospects.

I do know this, someone will be getting a very nice home at a current fair price. It’s all relative, anyway. If housing drops it simply means other assets have deflated as well. He bought the place 6 years ago, it has appreciated almost 100% in that short time frame, so what does it matter? It’s the speculators and flippers that bought 3 months ago that are freaking out.

Meanwhile, the neighbours check on the place every day including switching on different lights, a friend waters the plants and gets the mail, and we also have a lawn service to keep the outside up. We’ll stop in every few weeks, or as we need to deal with stuff.

There hasn’t been much inventory in thee area for the last 6 months. It looks pretty quiet on the job sites these days.

Just curious what part of the country.

Honeybucket to the rescue… Housing is a huge portion of the US economy, as I see it, it is the US economy.

Driving for Amazon in Utah has been a huge eye opener for me.

One benefit of being a driver is that you get to see many parts of the State you never new existed.

Places I once considered working class neighborhoods, like Magna, West Valley etc are all teeming with million dollar homes. It’s not just SLC proper but even the most remote areas of Utah( Oakley, Kamas, Hoytsville ) that are now littered with million dollar homes.

Utah county is in a league of its own as homes are being built everywhere and the cornavirus has not slowed anything down.

But wait, I need to pee….

So where are all the local businesses to support these growing communities? They don’t exists, not even convenience stores.

Amazon will not allow you to drive 30 minutes and back to find relief.

New homes mean honeybuckets are sure to be found.

Yep if your the guy brush hogging the ditches along these highways…you

want a tractor with a cab. No fun when the brush hog hits those bottles…or jogs of yellow gold.

I don’t know … You might be correct in your enthusiam, however :

1.) We have, so far, encounted WAR (seemingly everywhere, globally … with the requisite escalations & belligerencies…

2.) Disease is Obviously making a comeback ! Often followed by it’s dark-haired cousin, DEATH !

3.) PESTILENCE = F#ckin Locusts from Hell .. Everywhere you look .. Christ all Mighty! They’ll naw your arm off .. They even devour the Broccoli !! ( ok. I made that one up ..)

What’s left ??

Oh yes !, 4.) Famine – Well .. the Jury’s still out on that score .. what with Covid19 in the fields, and janky supply chains being what they are .. and grocery chains freakin out, with crossed fingers behind corporate backs ..

But the Mormons, for sure, certainly have an edge on things in that categorical regard ..

Of the four, No. 3.) Has the most means to change things in the mopes favor on the home front .. unless War breaks out, Bigly ! .. joining Death in a rictus-grinned enhanced march of creative destruction.

I saw the same thing in Spain, or to be more precise Aragon back in 2013: “ghost” communities of expensive houses with zero services. No schools, no grocery stores, no crèche, not even a restaurant. The closest town with that kind of services is 20km away, meaning a 40km roundtrip to buy groceries and to fill up. Yes, there’s another town in the opposite direction “just” 15km away but it looked like a DMZ in 2013 and still looked like a DMZ in 2019. Who would want to live there? And what about the “good jobs” supposed to pay for those expensive houses?

The only good thing is since the place still looked completely deserted last year, one of the bushes on the outskirts of this ghost town will do just fine.

Is it near a ski resort or something like that. It looks to me like a place that is too cold in winter and too hot in summer but that is the Northern European speaking

Social Nationalist :

1) Friedrich List written 200 year ago is available for $9.99 :

“The National System Of Political Economy”.

2) China built its industries, RE, infrastructure, military…with mountains of debt, mostly with US debt.

3) A new round of investment in China, fresh USD pouring into China, is not capitalism, its a “roach motel trap”.

4) China need USD to swap debt.

5) Us corp profit in China circulate in China, but cannot get out.

6) Their capital is locked in until it will be confiscated.

7) Wall street globalist failed again, as they did in 1930’s Germany, and paid the price.

You better believe that is capitalism. Debt is the point and it is the tool the monarchies used to bail out their kingdoms after 1352. Once markets shut down and capital stops flowing, the system is fooked. US capital flows without foreign areas is a capitalist death rattle.

Michael Engel, your most comprehensible post ever! Are you losing your touch? No offense, I mostly enjoy your financial koans.

Here in Jumbo Loan Country, 2 weeks ago I already received a flyer in the mail (first time in years) offering an all cash purchase for my home.

They are already coming out of the woodwork!

In my ‘burg I’m seeing price reductions in the 1-2% range. The odd 5%. But no more than that. Yet.

You need to wait for atleast 6 months or more to see the difference

Real estate is a slow moving beast

Correct. Same thing happened in 2009 where I live, it took a year for full impact.

All depends when the shutdown ends. If it’s over in the next few weeks, there will be no long term effects. And in 6 months from now, this will all be forgotten. If the shutdown continues through the summer, then in 6 months from now, real estate will be in free fall.

I know guys in finance in the bay-area that plan on giving early retirement to 10’s of 1,000’s and the first move they’ll make is to exit CALIF.

The only problem right now is waiting for the ‘Trump Cash’ to ripple through the companys, this cash will be used to pay cash settlement on early-retirement packages. Company’s want to cull +50% most of the guys near retirement age were promised the moon 40+ years ago, now they have lost all, and they hang on wait for severance, knowing they can’t be fired in the bay-area for being old.

Once this wave of 10’s of 1,000’s “FOR SALE” with 100% cash-out and walk, and no re-investment, you will see things plummet. How long?

I give it Sep 2020.

The Trump Cash should hit in May, and severance checks cut in June, and then people start traveling looking for their new home ( not in calif )

…

Who are these companys? Hint they’re all on the dividend ‘aristocrat’ list. Once the big leagues shit-can all with severance, then the tier-2 companys will say adios with a kick in the rear ( via zoom )

I hindsight ‘lockdown’ will be what it was the social equivalent of a bank-holiday, a time where corp-usa decided who ate & who didn’t

A severance culling of the older guys is exactly what happened in 2008-2009.

The Fed has unleashed so many bazookas out there. Some will only really start next week. How can anyone not expect asset prices to go up? Where will all this liquidity go? I guess you can do unlimited wonders with fiat money.

I’m expecting lots of it to flow into precious metals And then stand back and watch the fireworks With lots of buttered popcorn of course Organic not GMO

“The bank ends up with the credit risk.”

The bank should end up with the credit risk. If you’re in the business of underwriting loans, you should stand behind what you underwrite and be required to keep a certain percentage on your balance sheet.

Why should Fannie and Freddie have to absorb all the risk and let the banks keep the servicing rights for income?

Because the politicians are owned by the bankers, of course.

You don’t understand the secondary market if you believe the GSEs absorb all the risk.

That’s simply not true.

Servicers are indeed scared which is directly causing tightening in loan quality standards.

Again, the simplistic notion that everything is guaranteed and insured and has no risk is a gross generalization and misunderstanding of how the mortgage capital markets work.

> as mortgage servicers, they’re facing a liquidity crisis.

I’ve never understood how a “servicer” can be on the hook when the borrower defaults (i.e. declines to make a payment).

Isn’t assuming exposure to risk of nonpayment, in exchange for compensation, the very definition of “mortgage owner”? Why do these servicers simply not buy the mortgages and hold them. They’re already on the hook if the borrower defaults; why share the profits with somebody else if you’re already eating all the risk?

Doesn’t compute. Unless there’s some kind of cap on the amount of loss the servicer absorbs, but then it’s STILL equivalent to the servicer owning the lowest-rated tranche (i.e. first to take a loss) of the loan bundle.

Debt Wazoo,

“I’ve never understood how a “servicer” can be on the hook when the borrower defaults”

My next article will address that, later today (Thursday).

Correct. Google MSRs and you’ll understand better.

Thanks in advance Wolf. Even though I have been in RE for many years, I too do not understand the ”servicer” part.

Also, please consider including as much as you can regarding the recent infiltration of the SFR market by the hedgies and PE folks. We ran into that, new to us, phenom when we were looking in FL in 15, found our perfect place already snapped up by one of the big boys.

Also might put up one of your great graphs showing certain market movements from, let’s say 09-16 or similar in various areas.

One thing’s for sure re RE, it’s a hugely different market in different locations, with average $/SF $600-1000+ some areas, $200/SF elsewhere for about the same thing.

Wolf, another thing we ran into, a LOT, in 15 was some sort of game being played re foreclosed properties by banks: basically, they wouldn’t sell at a reasonable market price to value.

Most of the houses, all SFR, needed work of one sort or another, roofs, plumbing, electrical, mold,,, basics in other words, not to mention cosmetics; banks would not consider the costs of the work needed and obvious, even to the agent we dealt with, who was competent. Maybe you can explain that part of the RE game also. Thank you.

And BTW, we were cash buyers ready to close ASAP.

Not unless they promised something MORE than just being a pass through of mortgage payments.

I wonder what the contracts reveal. Hopefully, they aren’t MBS heroes who promised a stream of payments.

I have been following rcwhalen on this topic for a long time (since the GFC) and still have the same question.

To qoute:

“Last time, delinquencies rose as economic circumstances progressively deteriorated, almost like rising floodwaters breaking out of their riverbank. Concurrently, prepayments slowed progressively. That gradually put pressure on nonbank mortgage servicers’ need to continue advancing principal and interest to securities owners, because they weren’t able to borrow from prepayments to do so.

Most servicers had commercial bank lines set up to fund their advances and became “net borrowers” in order to meet their obligations. Those advancing obligations can continue for years until defaulted loans are ultimately resolved through a foreclosure sale. During the last crisis, nonbank mortgage servicers were primarily servicing private-label securitizations and so the government-sponsored enterprises — overlay, although present, was much less significant.

As financing needs became more pressing and the wave of delinquent borrowers rose, commercial banks simultaneously began backing away from the servicing advance finance market.”

I still don’t get it.

I’m old. I don’t remember this drama / sleight of hand in the 60s.

Long story short, they’re liable for delivery of the mortgage payments to the bond holders, i.e. investors that have purchased/invested into these large pools.

They are not just simply a pass-through as they do act as an agent however they have their own contractual obligations to the end holders.

They’re scared shitless of massive defaults and forbarance being touted by .gov

As in everything, the devil is in the details.

Long ago the servicers & writers got bonuses on new deals if they were Var-Rate, but if the servicer didn’t get payment or the writer messed up the funding company could rescind the ‘cash bonus’ which typically used to be $5,000 USD avg

Cash incentives is what moves loans on the retail, and flushes them through the servicers, but somebody is going to want his money back, if everything comes unglued

Cash is what moves loans, most people in the racket don’t make any real money, they depend on the cash, the same way wall-st depends on the xmas bonus

If a huge amount of loans are non-performing ( cuz COVID insanity says you don’t have to pay rent or mtg ), then people who fund the loans are going to be pissed,

I don’t see anybody blaming the virus, this is going to be ‘why did you write the loan to a guy who wouldn’t pay?’

To the ‘servicer’ why didn’t you out and threaten to break his leg? On first 5 day late?

So far I see this pollyana left-wing bay-area, its ok not to pay. Sure right, but given there are no courts to hear your case in this lifetime, its cheaper, easier, and more likely to just toss your stuff in the street.

Fonzie Powell and Mnuchin jumped the shark 2 weeks ago with all the corporate bailouts if the over leveraged. Why should even the 800 FICOs pay mortgage now, even if they are still working and have the money?

Part of me is so disillusioned by this system and how fundamental just doesn’t matter anyway, especially with FED pumping as much money as it takes to continue to try to keep asset back to bubble at any cost. What does all this mean? Can’t help but to think maybe real estate market will take a little hit for a short period but then it will just bounce right back to where it was like nothing happened. Take the stock market the last couple of days, triple digits up almost everyday, fundamental and the news are lousy anyway you look at it yet up and up we go again. Maybe nothing goes to heck in a straight line but sure do feels like this new normal of inflated asset is the par for course.

To forecast America’s best future, study Japan;

there, asset price deflation is slow-n-steady,

decade after decade.

Unlikely, I’ve spent time in both countries and they are totally different. There is essentially no immigration in Japan and tremendous bias against foreign influence generally. The US is a nation of immigrants, and current white house occupant aside, will continue to be one of the best places and most welcoming for immigrants on earth. The birth rate is also much higher, and the population less dense. The US may become Japan in the long run but it would be long after anyone on this forum is dead.

“Happy1” replied ( to me ):

> > To forecast America’s future, study Japan;

> > there, asset price deflation is slow-n-steady,

> > decade after decade.

>

> [America’s] birth rate is much higher […]

> The US may become like Japan in the long run

> [ but not in our lifetimes ]

The replacement rate is 2.08 babies per woman

per lifetime; only Utah and South Dakota

have a fertility rate that high,

and it’s rapidly diminishing.

Thanks to runaway asset inflation,

working stiffs can’t afford the cheapest hovel;

— this has to change.

And I think it will, as it has in Japan.

Thanks Wolf,

Yet another reason to be in the stock market in my opinion, certain stocks of course.

Can’t argue with that masterpiece of nebulous ambiguity.

The Fed announce a big new program to help business get loans, and municipal governments too.

The Fed will offer $500 billion to municipal governments so they can deal with their looming revenue shortfalls.

A much more effect approach would be to use a program created by one of America’s great Socialists, Rich Nixon and his revenue sharing program.

Municipal government would be much better helped if Congress were to re-start revenue sharing which would provided direct federal monies to states and local governments. More debt is the problem not the solution. What is needed is fiscal stimulus not more debt.

More debt to small business is also not a solution, but an increase in the problem, which to too much debt.

Instead of forever looking for ways to pile more debt onto more debt, Congress and the Fed should also turn their attention to actual solutions that reduce not increase debt. One idea is debt jubilees, which history shows us are helpful in situations like this.

Bullet proof markets, Fed has unlimited money cannons at the ready to fire. It’s a great big FU to the notion of efficiently functioning free markets (and another FU to the general public, those that won’t be participating in the Dow 30,000-40,000 rally in the near future).

From the Cleveland Fed on Servicers:

The servicer is also responsible for remitting to the trustee the scheduled principal and interest (P&I) advances and paying certain out-of-pocket

costs relating to key servicing functions (servicing advances).

Servicing advances can include paying a local attorney to prosecute a

foreclosure; hiring an appraiser to update the valuation of a property; paying to secure and maintain a vacant property; paying delinquent

property taxes; and procuring substitute insurance when a homeowner allows coverage to lapse.

The servicer is entitled to recoup all outstanding P&I and servicing advances relating to a mortgage from the ultimate proceeds of the

property’s liquidation or the loan’s prepayment.

However, because the advances on a loan might remain outstanding and grow for many months, servicers may incur significant interest expenses

attributable to the credit facilities or other funding sources for the advances. At any given time, servicers may have up to tens or hundreds

of millions of dollars of advances outstanding.

Now it is clearer to me.

Many thanks for the clarification. Always bothered me.

“Well bingo, we just got a huge backstop.”

“Powell’s the man,” Cramer added.

Don’t mind saying I told you so:)

If CGP is “the Man” then we are so screwed…….we need the Bernack!!!!… LOLOL

1) Jim Cramer is exited like a 6Y kid who got a helicopter on remote control.

2) NYC & SF RE ROC for the next 10Y is negative.

3) Dr.Claudia Sahn indicator : 100% recession : a strong vector down.

4) Fed opening a corner stores : vector up.

5) Our Fed is great, they preempted, but the total of the x2 vectors is still negative.

Cramer is more like a 15 year old kid that just found a discarded Playboy magazine in the ditch across the street.

6) SPX up 1.5% // NDX red.

re: car sales

I was told by a dealer rep why there are so few discounts right now. You’d think dealers would be begging people to buy something, anything at any price. Not so. This is one guy’s opinion, and I’m just passing on what he told me. For volume dealers like his store, their goal is maximize units sold volume. Sell X number of units a month, the manufacturer sends a volume bonus. So they’ll give the savvy buyer a great deal knowing it will be made up on the back end. And especially at month or quarter end if they need that extra 1 or 2 sales to hit the target.

But now all those volume bonuses are null and void since no dealer will reach those numbers. and quarters. So the focus has shifted to maximizing profit per deal.

Makes sense.

Hmm…why was the manufacturer paying more attention to volume than profit before C19?

Maybe true, but let me make an alternative hypothesis – one that applies both pre/post C19.

It turns on the post 2000 market for auto debt paper and manufacturer preferences for profit v. volume sales.

Say you are an automaker and you can choose one of two production levels.

1) Try and sell 10 cars at $20k.

2) Try and sell 20 cars at $10k.

Either choice generates $200k in gross revenue.

But #1 does so at presumably higher margins (assuming economies of scale have been achieved – just multiply my sales volume numbers by 100k to address economies of scale issues).

The high profit/lower volume approach also reduces risk (with one vital assumption, see below).

By jacking/keeping jacked prices and therefore lowering volume, the manufacturer only has to produce half the number of cars (or anything) – that is 50% less opportunity for production/operations/marketing f*ckups to derail the business plan.

All because only half the volume has to be produced.

The hitch – you need to find enough $20k suckers to pay that amount.

How do you do that?

By not caring so much if they pay off your financing loan.

How do you care less?

By selling the now crappier paper into the perpetually yield starved ABS mkt (Thanks, DC!).

Now you can sell your overpriced $20k profit-mobile to anybody who can semi fog a mirror, and you (Mr. Maker) don’t really care if the loan ultimately makes good – you have sold off the loan risk.

*And* lowered your production risk by 50%.

Call it the “inverted mass” production model.

The same dynamic explains why true price reductions (relative to true production costs) are so rare – even in a pandemic.

Everybody in the sales chain much prefers to sell one overpriced car to two fairly priced ones.

Fewer sales is just operationally *easier*, so long as you can continue to sell off crappy, high risk loans to yield starved buyers.

The linch-pin is a starved ABS buyer group – both the ABS tool/yield starvation really only hit their full stride circa the late 90’s/early Aughts.

And it has been bad news for car buyers with brain cells ever since.

Competing on Price has been replaced by Conning with Paper from the auto makers perspective.

So they just designed a new economy. I have not seen the pictures.

The new models come up faster and quicker than the iphone.

In 2009, Bernanke initially bought 10 million jingle mailed and other vacant foreclosed houses from the other banks. This is why the well documented foreclosures at the court house steps were in smaller amounts and mainly overpriced junk . The well located houses in need of little repair were secretly and illegally sold to the hedge funds at a discount by Mister Bernanke and rented out. This is one of the main factors that helped create the “shortage” of houses and the rise in prices

I woke up this morning to the Fed buying junk bonds and CLOs. Ok, so we are all done with personal responsibility — I got that memo.

Where does this go? DOW 30,000 and unemployment 25%? Dollar collapse?

National debt, $30T,,Fed “assets”,$10T. I’d hate to be a millenial. And what’s even more pathetic, they’re wanting more socialism.

This is worse. It’s lemon socialism. The public takes all the risk, backing all investment, including junk bonds. Investors get the profits.

How nice, while it lasts, if you’ve invested in something risky.

News this morning on Bloomberg: “Feds to Buy Junk Bonds, CLO’s”.

I guess someone on Wall Street was feeling left out of the shower of cash. Really? Junk bonds?

Isn’t that bailing out people who took very high risk or, I should say, people who were getting paid for risk they apparently didn’t take?

This is a fascinating read. https://www.grantspub.com/primer2020.pdf In just about every case I can guess why the Fed will want to buy their paper. Hospitals? sure. Steak N Shake, restaurants, jobs?? Consumer food groups??? The thing about lousy corporate debt is much of it is attached to vital industries. ENERGY! The Feds cheap credit keeps pumping us into a deflationary funk. You think Russia and Saudis are going to cut back so US can continue to export, and drive Venezuela toward revolution? Sometimes I think the Fed doesn’t understand anything, and sometimes I think I may be right.

Bernanke wants banks to be “cautious” when paying out dividends and doing buybacks…….WTF !!!

https://www.bloomberg.com/news/articles/2020-04-07/bernanke-doesn-t-see-v-shaped-u-s-recovery-after-steep-fall

The narrative is – the Fed is buying everything because YOU WON’T; especially after you lose your job because of the virus. You’ll probably cash in your 401k so the Fed is backing you up there. And the mortgage you didn’t pay, they’ll take care of that, too. You’ll probably need hours just to shop at Trader Joes, Whole Foods, Costco, etc, since they limit shoppers now. Meanwhile, have a nice day.

The fiat money system is based upon growing debt. The loss of the consumer spending reduces the velocity of money creating deflation. If they do not step in system will collapse.

Bad thing?

“If they do not step in system will collapse.”

Like the ability to make such high tech items as paper masks…

The US committed suicide a while back – suicide by lobotomized government on MSM life support.

Anyone “in” assets of any kind is going to get monkey hammered. The Fed and the Government cannot stop what is happening. If the Fed loads up on depreciating assets, it will simply weaken itself to the point where it is impotent for years or decades going forward.

People just don’t seem to get what is happening. Money is being destroyed at a phenomenal rate. Several times faster that any government or central bank can make up for or replace. Do you really think $1200 for an individual or $10K for a business is going to offset the money they are losing? A third of renters are now not paying rent. No vacation homes are being rented. No Hotel rooms are being booked. Delinquencies are skyrocketing, and will soon turn into defaults.

We have reached the point in the debt cycle where we realize the emperor has no clothes. We have spent money we do not have based on inflated pie in the sky valuations. A debt based economy only exists on confidence, and just like any confidence game, as soon as confidence is lost, the game collapses.

Those who think this economic collapse is going to end with the winding down of the virus really do not understand what is happening….

When Jim Cramer helicopter will crash his rich parents will

buy him a new one.

I have heard that they are cutting Jimbo off due to poor judgements. Going forward he is limited to hot air ballooning.