How will Canadians service $1.56 trillion in mortgage debt plus other debts such as credit cards? What about tenants who can’t pay their rent?

By Steve Saretsky, Vancouver Residential Realtor, Stevesaretsky.com:

We live in interesting times. I have been fielding a lot of questions regarding the market turmoil and what it may mean for the Canadian Real Estate market, particularly Vancouver. Yes it’s true, the S&P/TSX Composite Index fell 12% on Thursday, the biggest one day drop since May 1940 per Bloomberg. Surely this will all have serious implications, but what does it mean for our beloved housing?

The short answer is, I don’t know. Nobody does. What I can tell you is there are a few things I’m watching very closely and a few possible outcomes worth considering.

First, this is absolutely an economic shock, one that the Bank of Canada is probably ill-prepared for, just like the rest of us. Canadian households are the most indebted in the G7. We chose not to take the medicine in 2008, and thus, household balance sheets remain bloated today. The household debt servicing ratio sits at a record high, despite low interest rates.

Further, household savings rates are near 60 year lows. In other words, there’s not a whole lot of cash put aside for a rainy day, households are not well positioned for an economic shock.

This shock will unfortunately result in a hit to incomes, and will bring rise to job layoffs. Thus, servicing debts becomes increasingly difficult. Further, this is not something that can be fixed by lowering interest rates. We have a global pandemic where policy makers are encouraging people to disengage from economic activity. In other words, avoid restaurants, organized events, and travel — the very thing that makes society function and drives consumer spending, which accounts for over 65% of GDP. Remember, one man’s spending is another man’s income.

And so, this leaves us with a host of questions to ponder. How will Canadians service $1.56 trillion in mortgage debt, not to mention other debts such as credit lines and credit cards? What about tenants who can’t pay their rent?

Perhaps we should look at how other countries are coping. In Hong Kong, the Government will cut a check for HK$10,000 to every resident. In Italy, the Government is working with the banks to get a moratorium on mortgage payments. In the city of San Jose, they have adopted a moratorium on evictions for residents who can’t pay rent because of lost income resulting from the coronavirus outbreak.

These all seem entirely plausible in Canada. You can debate the moral hazard around it, and whether it’s the right or wrong thing to do, however we might not have a choice.

In terms of the overall real estate market, I suspect we will see a halt in activity. Not just a slowdown in sales, but in new listings as well. You won’t see this reflected in the data for several months, mostly because of the lag time for data processing. Further, while it seems logical prices could drop, if they do, that also won’t be reflected in official price metrics for many months. Due to the emotional nature of real estate, nobody cuts their price overnight. Unlike stocks, there is no mark to market on a daily basis.

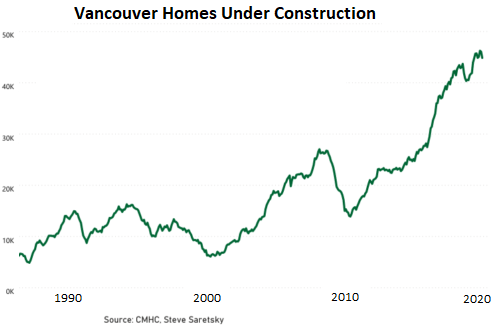

I’m also thinking a lot about new construction projects, which are capital-intensive and often funded using significant amounts of leverage. Every month sales are delayed, carrying costs add up, putting profit margins under pressure. Further, closing risks are no doubt something to consider, should pre-sale buyers have a change in their employment status upon completion.

This comes as we are expected to see a record number of new completions this year with the number of units under construction at all time highs. Units under construction across Metro Vancouver.

Lastly, I am thinking a lot about the private credit market. We know private mortgage lending has been growing at a rapid pace these past few years. It’s estimated to be about 10% of new mortgage loans issued. This increases renewal risks for buyers who, again, might have a change in employment as the loan comes due. Most of these mortgage are one year terms.

Further, I would not be surprised to see Mortgage Investment Corporations halt redemptions on their investors, in order to stem liquidity issues from investors wanting to pull their money from the fund. Many of these mortgage investment corporations borrow on a line of credit from a bigger bank. Will these loans be recalled? In a best case scenario, we should at least expect an increase in private mortgage rates in order to account for the increased market risks.

As I have said, nobody knows how this will play out. I have heard from others in the industry that they expect real estate to act as a “flight to safety” and thus it won’t be impacted. I personally don’t share that same view. But perhaps they are proven correct and my concerns fail to materialize. To be honest, I hope they are right. Nothing is more destructive than a sharp decline in home prices. However, I am well aware there are others desperately hoping for this type of event.

Regardless, I will keep you all updated on how the situation develops. We all know how important Real Estate is to the Canadian economy, irrespective of your views of the current housing market. Now more than ever, we will need to navigate these waters carefully. Stay tuned, and stay safe. By Steve Saretsky.

The Fed is going nuts trying to contain this. Read… As Everything Bubble Implodes, Frazzled Fed Rolls Out Fastest Mega-Money Printer Ever, up to $4.5 Trillion in Four Weeks

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If a significant number of the elderly die as a result (e.g. 8% of 70+) of the virus, then a couple of years worth of housing will be dumped on the market, both rental and owned. The vendors will be motivated.

This is a likely outcome if the ICU spaces are overwhelmed and we lose a lot of people who only needed oxygen or a ventilator.

They will need a lot of family court judges and lawyers for estates.

My old mother was one of those ventilator users at the hospital. She needed a nurse 24×7 since those tubes need cleaning and replacement.

Doctor needed to reposition feeding tube also.

When she died she owned dozens of properties. We have not even settled her estate after 3 years. It takes time to dump properties.

of course it does

we finally settled our grandmothers estate after 2 years(farm no less)

it’s a clusterF when siblings are involved

no one agrees to anything but SUPER HIGH PRICES

takes time to wear them down to reality

Once the fuse is lit on the debt bomb. And I refer to all dead bombs as well as other asset bubbles floating around. the effects of the virus no longer mean anything

I am a probate attorney in the states.

Disagreements between family is the hardest part of my job. Much of the time it isn’t an issue if the offers for real estate or assets match the appraisal than I instruct the fiduciary to sell. It isn’t fair for heirs in a large estate if the fiduciary is trying to wait to sell assets for the possibility of getting a better price later.

I have seen tight knit families split apart due to money or the frustration with the probate process in general.

Heirs generally have no input if there is a power of sale in the will. If there is no will and there is fighting for whatever reason, i instruct the transfer of the property to the heirs to close the estate and let them deal with selling it outside of probate.

An estate shouldn’t be open for 2 years unless its for a specific purpose like a lawsuit or some other extraneous circumstance.

Jared Mayer:

One of my favorite cartoons goes as follows.

First frame: Smiling family members gathering around lawyer’s desk for the reading of the will.

Second frame:. Lawyer reading the will.

” Being sound of mind, we spent it all”!

Shocked look on family member’s faces!

I am sorry to say I have no sympathy for anyone that gets in over their heads when it comes to debt and borrowing binge that they have done to themselves and their families.

The responsible and prudent, well prepared are once again by the Bank of Canada and governments. If it weren’t for local credit unions here, major banks are gauging depositors with 1.5% GIC rates. Loan rates 3.5% to 5% I see for many Canadian banks, 19%-25% credit card rates, 4.5%+ line of credit rates, reverse mortgage rates 5.25%+ rates etc. etc.

Inflation at 2.0%+ which is really low than real inflation, cost of living expenses from much higher rents, property taxes, hydro rates, auto, home insurance rates, food prices from shrinking product sizes 9%+ to higher prices as well etc. etc.

The big banks 6% to 7% dividend yields and 30% to 35%+ declines in their share, stock values just shows how not blue chip, safe they are in my opinion as in a few weeks this happens. Think long term. The toronto stock market TSX 300 was 15,000 back in 2007 now it is 13,300 still down 22%-25% when modest investment fees are included. Maybe breakeven if dividends are included or modest 5% loss over 13 years.

Coal trains at a near halt. Alberta oil and gas in depression. China flat on it’s back. Export Lumber dead.

Canadian dollar at 72.5 centsUSD. Chicago 2x4SPF down $150 in 3 weeks.

Who knows what the future holds, but if the insane price of housing in Vancouver hasn’t broken it’s back this time, then it is to the moon and back.

“Nothing is more destructive than a sharp decline in home prices.” ????

Or the corollary, nothing is more destructive than letting foreigners price local Canadian citizens out of their homes.”

Makes one wonder what the government thinks it’s function is if it can’t be bother to protect the common citizen from the laundering of foreign money.

Couldn’t have said it better my self, thinking about our futer generations that now have NO future

Oh please. Do your homework. Foreign buyers are less than 5% of the market here in Van.

It’s been measured again and again.

We (the residents) did it to ourselves.

It’s bigotry that keeps this myth alive.

Foreign ownership in Vancouver is at 10% if it is measured correctly, that is MORE than enough to skew any market. NO foreigner should be allowed to own Canadian real estate.

The Condo market is designed to be passed on no matter what to the inherited and are locked in should prices go down.

The Alberta market had their taste of relatives having the costs passed onto them.

Good luck Canada…your screwed.

This will playout with personal bankruptcies. As I understand it, Canadian mortgages are recourse loans – backed with the totality of your personal assets.

When you sign a recourse loan you better know what you are doing. In the US on a non-recourse loan you just send the keys back, but not Canada, I have met Canadian people who foolishly co-signed recourse loans for relatives. They did not seem to know what they were doing.

In the good old days, you just took over a mortgage. I don’t know if they were recourse or non-recourse but even during the many house price crashes over the last few decades I never heard of the lender coming back to the original mortgagor of a sold property.

Anyway, any default on a mortgage is usually handled with power of sale, which can take place in only a few months or less as opposed to foreclosure which can take a lot longer in the courts. And power of sale means that any surplus (if there is a surplus) over the outstanding balance plus expenses goes to the mortgagor.

In the US the ability to take over a mortgage was eliminated a while back in most mortgage contracts. I don’t know about Canada. And actual practice may be different from technical rules.

All I know for sure is I have no debt (unless i get a doctor/hospital bill from years ago that was denied by insurance – these things happen).

Wolf, you mention an increase in mortgage rates at the end of the article. Any idea why the same is happening in the US right now?

Been checking a few sites daily, beginning of the week I could get 3.375 on a 30 year with no points. Today the best offer is 4.125% with no points.

@sc7, I’d guess that some of that is mortgage rates tracking US10year T-bonds, where yields have backed up by almost 0.5% from panic-lows earlier this week. There could be some added spreads being put on by the banks, due to tightness and uncertainty in the markets.

The US 10-year yield is still below the 1% level and is still lower than at any time except the last 2 weeks…

Right, but rates have been sub 4 for a while now, ever since the 10 year yield was even as high as 1.5%. Perhaps MBS buyers are expecting them to further increase in the weeks ahead.

This jump in rates along with the corona panic isn’t gonna be good for the spring market. Will be interesting to see if it just pushes back to a busy summer.

I agree. I don’t get all the mass increase in refi’s. Been checking several sites for the last few weeks and it doesn’t seem like rates are spectacularly down requiring me to do something now. Still can’t find a rate better than the one I got in Aug 2016.

sc7,

Just to clarify, the author of this article is Steve.

What you saw reflected in the mortgage rates was this: The 10-year US Treasury yield nearly tripled this week from 0.38% Monday morning to 0.98% now. This is a huge move. And mortgage rates follow the 10-year yield.

Steve was talking about private-sector mortgages in Canada – not those funded by the government. His theory is that those private-sector mortgage lenders will have trouble borrowing at these low rates to lend at low rates because some of the risk factors they’re now facing.

I experienced the real estate bust in Florida in 2008. Expect that any programs passed by the government to give relief to home owners will not be honored by the banks. The govts pass laws now, but they don’t enforce them, especially when it benefits the working class.

Thank you for this article.

For me the key phrase was:

‘might have a change in employment as the loan comes due’

For exactly how long would a similar measure, as the Hong Kong administration have suggested, actually practicably work if it were employed in Canada, Australia, France, Anywhere?

The confidence of either financially burnt or just ‘worried’ employers in sectors that are currently or likely to be affected sectors, won’t bounce back like a rubber ball, so neither will their hiring approaches I would think.

So, if I were a real estate agent (we call them ‘Estate Agents’ in the UK) or mortgage lender, I think I might be a little concerned right now.

By the way, in terms of real estate Wolf, have you looked at the age-old tradition of lease-hold scams that continue to plague the UK housing market?

With Best Wishes.

Nice article. I am curious if all these same predictions would apply to the US Real Estate market, especially the low to mid price ban mortgages and rental real estate.

To draw upon the wisdom of the famous cartoonist Bill Watterson, we are now playing “Calvinball” – the rules will be changed as needed by those in charge.

With specific regard to real estate, I expect detached housing to hold up far better than condos in terms of demand. High-density housing with mass transit has many advantages, but disease risk isn’t one of them. And the prospect of a coronavirus mutation triggering more outbreaks will be a long-term issue.

Agree or not…BoC +CMHC are fully responsible for all mess (with some contribution from careless politicians)

The karma is haunting them back. I wish they let irresponsible people go bankrupt rather i suspect they will let CAD$ let go in drain.

Insanity…yeah. Canada authorities need a lesson of lifetime for their reckless spending and irregular environment, and irresponsible speculators also need to get same lesson.

I am sorry for poor regular citizen who bought on top of market.

Toronto house price averages just hit over $1MM in the last couple of weeks, a new record.

We’ll see how long that lasts because the first of the roller coaster declines usually starts in June. Any sooner would be a bad leading indicator.

The seasonal swing is usually 10% or more – in the last couple of months the rise has been over 20% – from $845K to $1021K – bubblicious?

“Toronto house price averages just hit over $1MM in the last couple of weeks”

Apparently the knowledge of how to build additional housing supply has been lost to the mind of Man…

Judging by the architectural tastes of the house-flippers in my area, yes.

They’ve been building full-speed for years, every square inch, even the odd lots, seems to be taken up with new condos and townhouses. The skyline has been cluttered with cranes; always a leading indicator of a bubble emerging. All the old factories and huge manufacturing facilities have either been converted to condos, or leveled to build new condo towers, some of them of staggering size.

My only lingering question is if we don’t make anything any more (and we don’t), where is all the money and job creation coming from to pay for this?

Does this mean I wil be able to buy a condo with particle board exterior walls and laminate wood flooring from China for less than a million CAD?

And unfinished concrete ceilings and partially unfinished concrete walls with unfinished 3-foot wide concrete pillars running through them? A lot of these places feel like you’re living in a parking garage.

Anyway, a thousand bucks a foot.

Canadian here…64 years old. All my friends paid off their homes years ago, decades past, and these are modest working folks. They will be just fine. The people in trouble will be the hype stampeders, those who bought million dollar tear downs in cities….in every city in the World, actually. People bought $500K condos like it was normal. Folks like me said it was stupid 10 years ago and now we are proven right.

It is a hard lesson to learn.

I mentioned this story years ago on WS, and it is about Art the barge loader. Barge loaders run the big cable cranes that load log barges on the west coast of BC. They are extremely well paid and always have work. Anyway, my job was to fly the barge loaders to wherever they had to go, and wait 8-9 hours to take them home. (I always went fishing and ate steaks while I waited….pretty cool job). One day, we were having lunch on a large ocean going tug and a deckhand remarked he just bought a house in Gibsons, (by Vancouver). This was in the late ’80s. His mortgage payment was going to $1200/month, which was astronomical at that time. In fact, it was 3X my mortgage payment. Anyway, he was bragging it up to Art and replied to Art’s head shaking with, “I make good money, I can afford the payment”

Art’s reply, “It isn’t what you can afford when you’re working, it’s what you can afford when you’re not working”.

As with Art, this has always been my philosophy and the main reason why I retired in my 50s; could retire. My kids have never known hard times and it has often pained me when I see them waste money. They will both be okay and will not lose their jobs, homes, or anything else because they don’t do debt either, (having watched Dad suck it up during downturns), however, they are finally getting a big big wake up call that the past 15 years was insanely unrealistic.

Canadians used to think like Art. It was the norm. They were a frugal bunch with ties to the prarries, logging camps, mining towns, strikes, lockouts, and long winters. They knew poverty and knew how to work hard. Loggers knew if they had a good year, they might miss 6 months work the next. The survivors saved for the downturns. I have no clue what happened other than old lessons will now be relearned, and hopefully not forgotten if this ever turns around. The illusion of wealth and being able to buy any damn thing you think you ‘just have to have’ was nuts. Is nuts. Buying rentals on margin and needing it always rented or lose it is not smart. It is a gamble, and always was. Gambling means losing.

Watch any modern RE show. Listen to the new home buyers talk about granite counter tops, or quartz, polished concrete. Front doors with sidelights. En-suite bathrooms. I’ll bet they don’t even know what arborite is, or can imagine a home with just one bathroom? It won’t hurt Canada to see some hard times and get back to reality. I am sorry some innocents will be hurt, (I’ve been there and worked away for years during past recessions when I was the sole breadwinner). You get through it. Canadians will just have to buckle down and relearn forgotten lessons. This time is never different.

regards

I suspect many people in the Western world will be finding out what it is to live much more simply within the next year or so. Certainly, it can become a comfortable way of life. I, too, grew up in a frugal home. We also had one bathroom for a family of five (toilet separate) and never felt deprived. It would be harder for me now that I have become spoiled.

Times are different. In much of the west coast of the USA, we have morphed to a rentier society. Workers are forced to rent; they either rent property, or rent money to buy property. Either way it extracts a large % of the median family income in most areas where there are jobs. Workers must stay on that hampster wheel.

Plenty of young people who worked the last recession in 2008 learnt those lessons. Those of us unable to access generous family benefits, who had to work to pay bills, know what it’s like to do without.

There are plenty though that have had very good times that will find the reality of the workplace brutal if they find themselves having to return. Plenty of high paid finance and IT people will likely be hit with the reality that their jobs can easily be cut.

I’m in my 30s and grew up in a modest house with one bathroom. Plenty of us did. It’s just that there is a mentality with many that the government will provide an easy life. If government benefits at the higher end were cut it would make for interesting experience for many.

It’s obscene in Australia that people with two houses can get any government benefit. There are caps on assets but it’s still overly generous for home owners in my opinion.

I guess we’ll see how our government copes. So far they are throwing money at the wall hoping it sticks. Raising interest rates will be inevitable eventually and then things get bad fast due to record household debt.

If you are single without children in Australia, under 40, you are used to watching the dollars. That group has higher incidence of living with parents than during the great depression and 1940s. The GFC hit that group the hardest – particularly women who had twice the unemployment as men. Everyone else has had it much better.

Hi Paulo, thank you, Wolf and others here for your reply to my question on this subject.

I checked around and found Steve Eisman (The Big Short) shorted the big Canadian banks starting last summer. His interview at that time can be found on youtube. Coronovirus nor oil price crash were not even in the mix then. He was mainly talking about low bank reserves and the housing bubble.

*my question last week on another thread

Canada is one of the very few countries in the world where the bank reserve ratio regulation is … Zero. The States is 10%, China is 17%, etc.

But Eisman’s biggest concern and the reason for the Canadian bank short was that loan-loss reserves were inadequate for even a normal contraction in the economy.

I have a gut feeling, those past experiences are coming back as these bubbles finally deflate. Unfortunately, it took a dumb virus to pop the everything bubble.

Canada has been relying on imported goods from China to make up for the environmental laws imposed on its own citizens.

Too many choices have made any type of recycling impossible.

Even though they have recycling programs, the plastics are not being recycled as too many stickers and different quality of plastic is impossible to sort at a reasonable cost.

Vancouver house prices soared with the inflation boom in the 1970s.

Then that boom failed and homes up in the “British Properties” were owned by expense-account executives (not old money).

In the bust these fell to 1/3 of their highs.

Over in more modest but very nice Kerrisdale the typical home price fell in half.

In Toronto in the same period there was a home in a high-end region that the owner who was a promoter went broke on.

The mortgage company seized it. And it took about three years to dispose of it.

At 1/3 of the price at the high.

Oh don’t go there

When I was little I remember my grandad (grandfather) telling me about when he grew up in the 30’s he said, and I quote :

‘we suddenly had nothing’

He subsequently had an almost pathological fear of debt.

We had that conversation around 1990 – 1991, when mortgage rates were punitive in the UK, around 10-13%.

I put it it to him later, much later, that if one wanted to buy a house or whatever, one had to work within the constraints of what was accepted as the realities of the time.

He was unmoved.

The Canadian population grew over half a million in 2019. They need new homes.

20% of the Vancouver population are ethnic Chinese. With the communist party crack down in China, some Chinese bought property and businesses in Canada to get dual citizenship.

China doesn’t allow dual citizenship

Actually they do, in the sense that they won’t revoke Chinese citizenship because the person acquired an additional passport.

They simply ignore the person’s second citizenship and pretend it doesn’t exist.

That’s good enough for most people.

I retract this. I was wrong. They actually do claim to terminate the citizenship of mainland Chinese, simply for having another country’s passport.

WTF, that is some medieval policy right there.

You know you’re living in a prison when…

I saw a comment on another site that contradicted this. He said a lot of the “wealthy” Chinese do have dual passports, saying the Chinese authorities just look the other way when the wealthy are doing it.

If they changed their name on their Canadian passport, who is going to be the wiser? In other words, how would the Chinese government find out even if they were looking, which I’m sure they’re not. There are so many privacy laws that protect personal information.

Also, many Chinese were using Canadian proxies in order to buy properties, or using shell corporations to hide their identity. Even if the Chinese authorities did care, how would they know or find out?

Like their money laundering, the paper trail is covered.

Like Paulo in Vancouver, BC, I am 66 and live in Toronto. Retired when I was 47. Having married at 40, my 2 kids are 19 & 23, so are not yet as independent as Paulo’s kids are. Having RP, my health isn’t as good. Otherwise we are in similar boats.

I have been very puzzled by Canada’s on going housing boom and what is under pinning it. Certainly the central bank of Canada and politicans and their liberal policies, are the two biggest culperts.

What has bothered me, is all through out this never ending housing boom, these same politicians have implemented policies to discourage true wealth creation in Canada.

They have stopped cold, well over many hundreds of billions in new wealth building projects in Canada.

When this Canadian housing boom turns to bust, and it will, Canadians may fined out the hard way that there are simply not enough true wealth being created in Canada to support their current dreams.

To be honest, I thought a housing bust would have happened years ago, but have consistantly under estimated how long central bankers could continue to print money, certainly longer than I will be able to stay solvent!

Now that the Canadian oil industry is on its death bed, the only remaining “industry” is housing: bring in the immigrants by the millions, sell them debt against houses (and everything to fill them in with), hope that they’ll find a way to thread water financially to keep up with the debt interest obligations ’til they drop.

They can not afford to let the housing bubble deflate. Can not.

And to think that Canada used to have real industries! Even Leica, that paragon of old school German quality, deemed it appropriate to have a Canadian assembly for some of their optics.

These days, the main business is immigration.

>>They can not afford to let the housing bubble deflate. Can not.<<

In Canada, it is the big banks that hold most all of the mortgages versus in the USA where they are packaged and sold (off loaded) on investors. I believe Canada would rather hyperinflate its currency (too keep house prices high) rather than cause their big banks to tank under the load of bad mortgage loans.

@S

I concur, but hyperinflating is their Plan B. Plan A – selling nation’s housing to *anybody in the world* who can come up with the dough – is much more preferable, as with that they get an infinite income stream in the form of property taxes (in the amounts conveniently determined by themselves).

A reader it’s the same immigration housing growth model in New Zealand.

@Kiwi

At least NZ still has some industries – dairy, wine, tourism, movies. Canada’s been stripped bare.

Also, to my surprise the current govt actually delivered on their election promise (imagine that!) to prevent non-citizens’ from buying nation’s housing. There’s hope yet for Kiwiland!

It would seem to be impossible to thwart Canada with the massive natural resources of so many types, the beauty for tourists and the fisheries, coastal and internal. But hey, government can undermine everything.

I forgot to add to government screwing it up is perhaps the larger problem of parasitic finance.

Erle : Not sure if you are familiar with this saying : ” If you want to screw up a good idea give it to a committee but if you REALLY want to FUBAR it make sure it’s a government committee . ”

Personally, I think economists and Central Bankers should be declared an ” invasive species ” and hunted into extinction. IMHO

No One Knows How the Coronavirus Will Impact Canadian Real Estate

It’s not cov-19 you should be worried about. There are relatively few cases in CA, comprehensive containment measures are underway, and the country has a modern, national healthcare system.

The problem is financial contagion from the US, which was unprepared for cov-19, has a late and still inadequate response, a weak health care system with lots of gaposis, and lockdowns across the board. The recession in the Real Economy hasn’t hit the banks yet.

The US is Canada’s largest trading partner by far, accounting for nearly half the total, and the US recession is sure to affect Canada. RE can expect some headwinds, but those it can weather.

“the country has a modern, national healthcare system.”

Bureaucrats, not doctors, decide which procedures and treatments are covered under the CHA — based on data and statistics rather than on the needs of patients.

There is a scarcity problem due to its single-payer system. The health-care system, government central planners ration care and cap the number of procedures offered in a given year, leading to queues, longer wait times, and a deterioration in the quality of care.

Wealthy/rich Canadians seek healthcare elsewhere.

There is a scarcity problem due to its single-payer system.

Scarcity in some locations, particularly rural, and overabundance in others, the rich cities. The problem is not due to the single-payer system. It’s the mismatches in the allocation of resources.

Not even a good try.

You can’t possibly be arguing that canada has any surplus health resources whatsoever to deal with this virus. We don’t. Italy has the second best healthcare system in the world as per the WHO rankings Iland they’ve been overwhelmed. Canada ranks #30, just 8 notches above the US. When hospitals become overcrowded in Ontario, do you know what we call it? Saturday. We are not in any way prepared for this. Unlike countries with top rated healthcare systems like France and Italy, there is no parallel private system in Canada to pick up any slack.

I am a hospital based physician in Canada. The normal rationing is only for elective procedures like total joint replacements, etc. In the USA rationing is done by keeping the people too poor from being able to access it. Still rationing but by another name.

Our hospital will simply cease to do elective procedures and free up a lot of resources for the Covid-19 crises as it occurs. We have already been given notice that that is the plan. Totally rational. Sure my income is going to get cratered but we are debt free and have savings so we are okay.

My 23 year old son in Vancouver, and who is fiscally conservative like his dad, already has seen his work in the film industry dry up. He hasn’t been working a long time so his savings are not high, but he is debt free and I will help him out gladly.

Nonsense the really poor in the US gets the same access to care as anyone in Canada. The US insurance industry is crap but there is a high level of government care for the poor.

I’m a Canadian living in the USA, and the quality of care is vastly superior here.

The wait times are much shorter, the technology is far more advanced and facilities are clean and modern. None of this is true in Montreal.

The Canadian health system is on the brink of collapse.

Pre-COVID, 8+ hour ER waits were common. The system will utterly implode with even a small uptick in demand for emergency services if severe coronavirus cases need intensive care.

The hospitals are all old, crumbling and poorly sanitized; personnel are overworked and underpaid.

Economics follows the laws of physics like everything else. The bigger the debt bubble, the bigger the crash that follows it.

What is going to follow this crisis, is going to be a return to reality. Not only financially, but people are going to discover during this crisis that we have truly devolved into a feudal existence once again as is being proven by the governments tyranny over property owners in San Jose. I guess that leaves no doubt about who actually owns your property. One thing is sure, when it is all over, the wealthy will be wealthier, and the poor will be poorer. That is how the system is designed….

Economics follows the laws of physics like everything else.

Technically, they’re not exactly the same, but there are sufficient similarities between them so that an economy can be treated as a kind of thermodynamic system. I argued with a professor of finance about that, many years ago. I was very polite. He lost. Then he lost his ass when the dot-com bubble burst. I didn’t rub it in.

Social Sciences, including Economics, do not follow the laws of physics.

All assets lost value, so will real estate, this is a full-blow deflationary shock, RE is just less liquid and move slower.

The effect will take a while to trickle down in an economic cause-effect domino.

I think oilpatch regions (NFLD, Sask, Alberta) will feel the pain first then province who depends 100% on government ( Nova Scotia, PEI ) and have no industry will bite the dust when the unavoidable government budget cuts hit the deck. The manufacturing in Ontario-Quebec will need to pick up the slack.

Skeptic:. That is the problem! There is very little manufacturing left in Quebec/Ontario! These are dying out because they are not green! Trudeau won re-election on eliminating polluting industries!

Wes – like our politicians care about going green! “Going green” just provided them with a convenient excuse and explanation for why the jobs have been offshored to Asia. The only “green” they care about is the green money lining their pockets and those of their corporate friends. They went there for the cheap labor and no environmental controls.

If our politicians actually cared about the average person, they’d have slapped environmental and wage parity tariffs on the offshoring corporations from the get-go. If that had been done, they never would have gone, and we’d have good-paying manufacturing jobs instead of service jobs.

I agree with you, this greenwashing as been the Trojan horse for the war on Middle class while the real environmental problems are not being tackled. I dont want to expand too much on this, I think we’re on the same page.

Manufacturing in North America died out because of automation and a lack of willingness by consumers to pay a premium for North American sourced products.

Just 8 years ago, you could buy smartphones made by Blackberry, Motorola or Nokia in Canada and the USA.

Fast forward to today and Blackberry is gone, and Motorola and Lenovo are brands slapped on Chinese phones.

Consumers were not willing to pay an extra $150 for a phone made in Ontario or Texas.

Most of my friends in the bay-area ( SF-CALIF ) want to sell. They’re telling me things have gone nutz, especially at work.

I have always felt it was going to end this way, $1M homes; Everybody at once try’s to sell, the stuff falls to $30k ( 1982 prices ), happens quick in the real world. It’s going to be interesting watching the banks deal with the collateral evaporating.

Not a good time to be in home debt, IMHO its going to revert to pre proposition 13 prices say think late 1970’s. Averaging $50k for a home or less, my folks bought a brand new home in So-Cal for $15k in about 1970. The home sold in 1990’s for $300k-ish, I’m sure its $1M today.

I sold all my real-estate in the past decade. Done. Cashed out, the future of the home being a piggy-bank is over.

The Gov switches gears, instead of the 500LB gorilla being the banks, it becomes the medical-industrial-complex. Free fiat is about to end, if the USA ends up being the knee-capped by the virus it will once and for all end USD hegemony.

Some medical stocks are going to do very well. There is never an end to the world. The obvious thing is the end of globalism, no way it can pull through this, too much manufactured hate now say, USA hates Chinese, and vice verse; Same everywhere.

Huge packages coming at all the USA oil company’s, early retirement; All want to sell their homes & run, the packages give an incentive to sell the home take a loss.

Where will they go? Lot’s I know say Vegas ( if you like hell )

Anybody have a clue, where all these city slickers are going to move? They want out of the rat-race, but where in the USA can they go, and especially not bring it with them like they have done to Bend, Oregon.

It’s not like it was anymore, say Kalispell, MT; where you could come into town and buy a home in the 1980’s for $5k, heck you could be the richest guy in town if you just had a job. But back then there were no strip malls, and modern crap in these Montana towns, just like in Idaho, all the small towns have been yuppified in the past 30+ years.

Where are people going to go?

My only feeling is they’ll return to the dust-bowl era family farms of the 1930’s, those places are super cheap, super remote, and have family ancestry, which makes it real easy for an outsider to slide in, the problem with most remote USA places is they’re hostile to outsiders. If you have a family line, or a good known name then your good. Tons of people came into the coastal mountains of 1960’s from Oklahoma, they could easily return given that urban life in the near future USA will be a death sentence.

Biggest complaint I’m hearing is my friends are tired of fighting over toilet paper. Heck 90% of the world doesn’t use trees to wipe their posterior, maybe USA can go natural too and use water.

As a Canadian who sold July 2019 and following Wolf and ZH articles I went short Jan 2020.

After being called quite a few names and being told “You will NEVER get back in the housing market again”.

Guess who is smiling like chesire cat now enjoying this week and just slobbering at the thought of low balling in the near future.

Enjoy the fireworks next week!

Hahaha where is socaljim now? Thought the fed would keep him afloat indefinitely.

Danno,

ZH has been saying go short for more than five years! lol

Currently, there is a lot of uncertainty for many asset classes. World wide. Hundreds of trillions in debts, and much more in hundreds and hundreds of trillions of unsupported liabilities (derivatives, pensions, off book, mis-accounting, etc), vs ~$60T in declining GDP. What could go wrong? So it is a good question to explore an asset pricing outlook.

Stocks are easier as ultimately they are often valued on report earnings. Other asset classes, are harder to assess, as they are based on real buyer-seller trends; value is in the eye of the buyer-seller transaction.

But, as a long term area Vancouverite, l would suggest, there is a whole lot more going on, in Vancouver RE, than the typical price-trend graphing, and local-wages-to-price graphing.

I admire Steve Saretsky’s reporting! But keep in mind he is a professional real estate agent and commentor too, good stuff, but he is likely professionally constrained in a publicly stated reply on RE pricing outlooks.

But, my point is, sure: a) there are deep concerns about fairness of Vancouver RE affordability, especially for long term locals on local wages. Not to mention the consequences to long term locals on their unfairly applied and escalating property taxes. And b) there are deep taxpayer concerns about any de-regulated industry practices, or systemic too, that crash the financial system, and cost taxpayers buckets of money; (ie 2000, 2008; & 202????). But, c) there are, many many other factors that apply to Vancouver RE prices, than what is typically reported in the traditional media.

I would also add, too, as you know, RE is sold to the highest bidder, not to the lowest bidder, not to the ‘what they can afford’ bidder. Just like that Renior at the Christie auction house; it is one winner and one seller, $128 million in cash later, (or???), and a whole pile of ‘thanks for showing up’. Harsh. But true.

So l am saying look at the transaction (reported and behind the curtain); not the opinions of those that showed up – ie local wages. Very simplistically for Vancouver RE: not all buyers are local, and not all buyers need financing, and not all sellers need to sell. And Vancouver is not susceptible like a local resource economy is, nor is it a former factory town economy either. As for its amenities, you have heard it before; apparent or otherwise if you look, and they are true. Hopes, or exasperation, or trend graphing, or concerns, don’t count. Sorry. BC stands for bring cash. That is its economy. And there are reasons why that happens.

Okay, and then there is that worry about ‘over extended’. Well, so far and even today, world wide, governments and central central banks, despite the reported and unreported debt loads, crushing savagery to workers and savers, unfair access to financing, (ie main stream gets 22% credit cards and gig jobs, while repo recipients are charged ~1% for their $4% to 6% earning RE rental companies), or reporting of local wages to local RE prices, they have said, “what ever it takes”. It is “party on”. And the recipients of this largess, show up in many many asset classes.

So l suggest caution on what is the narrow and even mis-characterization of this Vancouver RE price issue; often reported as ‘local wages to local RE prices’. Sure, affordability is a fairness issue for locals on local wages. But these RE prices would not be happening, for some 30 years l have been here, if local wages was the only determining factor. So, evidently there is way more going on. And there is.

Finally. End game? IMO, this is not a Vancouver RE only issue. It is a world wide issue. But maybe, if it becomes a cash only game, say in the Vancouver RE?, or?, then as there is a lot of cash out there, and even now being printed this week, then maybe some/alot of Vancouver RE is excused from the detention room. Just saying. Maybe future asset pricing is not determined by historical and typically determinants. Maybe it is about who has cash, or who has access to special newly printed cash, and that asset class’ features and amenities, as it appeals to those who have cash or printed cash.

In summary, l suggest caution about applying, gross national averages to the local Vancouver RE market, or applying local reported wages to Vancouver RE prices, when it is anything but locally influenced, or even easily or typically transparent. It is best understood by exploring local stats and local factors, international and domestic (economic, demographic) trends, and capital flows; both reported and especially insider anecdotal.

Impressive pretzel twisting logic to say your property value can’t POSSIBLY go down.

Sorry, you’re screwed.

interesting analysis

Canada is not a normal country.

A top destination for high-net-worth individuals, immigrant friendly (350k this year at minimum) – almost four times greater than the US on a proportional basis, there will be no housing bust, not this year, or ever. Will there be a recession? Perhaps. The government will protect the banks, the banks will keep the money flowing. Oil will bounce back.

Canada remains a safe-haven.

We have a shortage of low paid workers as immigrants are educated to the labor laws and the rest of Canadians are not lowering their standards of barely surviving to pay all these massive taxes and bills it takes to survive monthly.

Not worth getting sick or injured for life on dangerous jobs.

It’s different here.

There, I shortened it for you.

Everybody is wrong wrong wrong.

1) The supply side shock from the partial reverse globalization will be highly highly inflationary. Watch the prices at WalMart, HomeDepot, and AMZN jump. The prices on raw inputs of production will spike and that will flow to finished goods. Remember supply and demand? If demand falls, but supply falls even more, prices spike. That was the lession of the 1970s. Stagflation. This will be supercharged stagflation.

2) Get ready for MMT … big time. Add that to the supply side shock, and you are now in the range of hyperinflation.

3) Real estate is the new gold. Forget the BITCOIN. That will evaporate.

4) The whole sharing economy is dead. No more UBER. No more public transportation. AirBnB? Forget it. High density urban condos? Dump those fast. Spread out single family and private cars, the staple of Southern California, is in. So much for global warming. The sharing Bay Area economy is out.

5) All virus outbrreaks are always tamed by sunshine and warm climates. This one will be no different. Watch the worlds wealthy storm to live in Southern California’s spread out single family homes where the warm temps and sunshine keep virus outbreaks in check. This virus will return yearly just like the flu. Did you notice SoCal has very little community spread? Most virus cases here are travel, cruise, or close contact related. This virus will return every year and warm weather single family is in. The rich will flock to warm weather SoCal beach homes.

6) The stock market will be fine. After the weather warms in full force, the virus will go into hiding, and Trump will strut in campaign events and the country will give him another term. The stock market will surge to new highs. The only great depression will be in the head of Democrats, especially those that don’t live in warm climates.

See that? First comment in so many months goes to moderation. That is why I rarely come here anymore. Waste of time.

This comment is precisely why your comments go into moderation. With this comment, you just proved the point.

I agree Socaljim. Reading your comment was a waste of time. There was someone here doing a parody of you a few months ago. Try as he might, he could not exaggerate enough to make it obvious that he was a parody. We kept falling for it.

I am a retired wall streeter in my 40s … how? Because I never fell in line with group think. Group think never works out.

SoCalJim,

As you have noted just now, someone just did some name-calling on you, which is inappropriate here. And I deleted that comment, which also automatically took down your reply to that comment.

I welcome most of your comments, and I encourage you to comment here. You’re like a permanent opposition voice or something. There is nothing wrong with that.

But please follow the commenting guidelines. That will make it a lot easier for me.

Not all viruses are tamed by sunshine/warm weather. And I don’t think this one will be.

Here is an opinion … I can’t share the link.

“Top infectious disease specialists at UCLA and across the country say the coronavirus’ ability to spread through sneezing and coughing could be hampered by Southern California’s typically sunny climate.”

Another clip from the same article

“Klausner’s observation about the benefit of Southern California’s weather on the outbreak is backed by the Global Virus Network, a team of internationally known virologists. According to novel coronavirus research just published by GVN, “it appears that the virus has a harder time spreading between people in warmer, tropical climates.””

A Bloomberg article notes the same pattern where Bankok seems to be getting off easy relative to colder climates.

The corona virus pales in comparison to the “housing virus” that has infected the populace.

It has been like a plague that has swept over the land.

“Nothing is more destructive than a sharp decline in home prices.”

No, nothing has been more destructive than a four-fold increase in the price of housing and the fact that the country has been sold out to the highest foreign bidder.

The people left out of the housing market have seen their rents increase astronomically, if they could even find a place to live. Where were the calls for them to be bailed out while this virus swept over the land? When they complained, they were simply told: “It is what it is.”

Why should the corona virus be treated any differently? Is it because this virus involves the “winners”, the ones who have benefited the most? Bail out the winners again?

The government fights one virus while propping up and encouraging the other.

This is slightly out of date but close enough to understand that the Canadian Housing bubble is still bubbling up.

“The average Canadian household was using a record 14.9 per cent of its disposable income to meet debt obligations, Statistics Canada said on Wednesday”

https://globalnews.ca/news/5055092/canada-household-debt-service-ratio/

The debt to income is crazy high still around 179%…

A large portion of the housing stock is paid off maybe 30-40%

And it is estimated about >50% of condos are owned by investors who are cash flow negative.

The low interest rates are blowing the gas bag near bursting..

What is likely to happen is that the alternate lenders who charge very high mortgage rates 3-5% above bank rates I think will have funding problems. They will soon have their own debt problems and might cause some panic in the lending market as happened I think it was with Genworth when suspected income became suspicious on the mortgage applications.

There is one company that makes loans to people in debt and they claim they can make money with a 6% default rate and their payments can be >9% interest, it is called goeasy was growing at 20-30% a year and its stock tanked.

backwards… yes agreed, NZ is the similar (as mentioned). Homelessness was unheard of until relatively recently. I heard a guy on the radio who runs a homeless shelter/soup kitchen in a poor(ish) region saying 20yrs ago they had to search out the homeless and would struggle to find a handful. Now it is a problem trying to house/feed ‘them’.

The days that people followed the Rich Man Poor man advice are over. Borrowing money to make money worked well for decades. This has now come to an end. Cash will be king for the foreseeable future and those that are highly leveraged (at the wrong time) will pay dearly. Deflation will be with us for a long time and will be so painful that the cry of the populace will be so loud that the Government printing press will be turned on full steam ahead. That will be a ways away though.

Lucky for everyone I showed up. Steve knows a bit but only a bit at best. All the trends that are already in place in Canadian real estate will continue. Alberta will keep on falling forever in price. The greater Toronto area will see prices move hyperbolic and rents will skyrocket by 50 percent in the next 3 years. Manitoba and Saskatchewan will see a reversal as prices will start to rise. New Brunswick, PEI and Newfoundland will see prices move sideways as zero interest rates diminish retirees yearly income. Vancouver will see price appreciation at the low end of the market. The GTA will be the next California no one will be able to buy or rent and people will move out of the Golden Horseshoe.

So after reading the article and subsequent comments, it seems the only thing going for the Canadian economy these days is real estate and government spending. Fueled by low interests rates, vast amounts of money printing and debt. How is any of this sustainable?

Supposedly the private lending market doesn’t like all of the rate cuts from the Bank of Canada.

Not a good time for private lenders to be turning people away when many Canadian speculators need to close on their investment properties that are being completed this year.

https://twitter.com/ronmortgageguy/status/1239533558131232771

You do know, and everyone knows what this is and how it’s going to play out; it’s a once in a century bloodbath. It’s fine to say nobody knows, but in reality, we all know the certainty of the main themes, just not all the precise details. This is the slope of hope now, that secular bear market that keeps clawing you, drawing you into his cave to destroy you. You’ll be able to buy most assets including stocks, bonds, housing and land, for pennies on the dollar. Canada’s getting hammered from a long housing bubble collapsing, the oil crash will settle around $5/US/bbl, plus manufacturing has gone to Mexico, plus rates will go up as bond prices crash. It’s a massive flip, in everything, a tectonic shift. Most will get wiped out, flushed out of the game as the weak hands they were. Canadian housing should drop 30%, 50%, maybe more in certain areas and depending on the time frame and it will stay down for 12-18 years.