Repo-blowout solved, the Fed is stepping back as lender-of-first-resort.

By Wolf Richter for WOLF STREET.

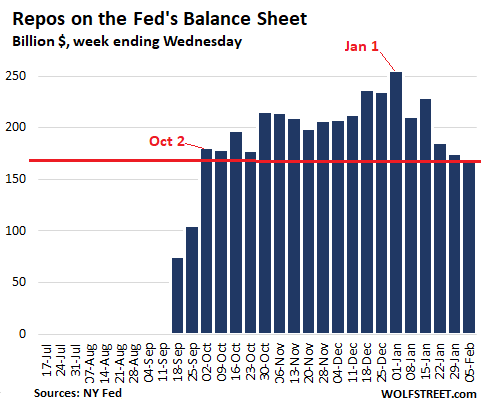

Total repos on the Fed’s balance sheet of February 5, released Thursday afternoon, have plunged by $85 billion from the peak on January 1, to $170 billion, below where they’d first been on October 2:

Under these “repurchase agreements,” the Fed buys Treasury securities and mortgage-backed securities (MBS), guaranteed by Fannie Mae and Freddie Mac, or Ginnie Mae, whereby the counterparties commit to buy back these securities at a fixed price on a specific date, such as the next day (overnight repo) or a longer period, such as 14 days (term repo). Repos are by definition in-and-out transactions. When a repo matures and unwinds, the Fed gets its money back, and the repo on the Fed’s balance sheet goes to zero.

By buying these securities, the Fed adds liquidity to the market for the duration of the repo. When the repo matures and unwinds, the liquidity gets drained from the market. When a new repo transaction occurs, the process starts over again, but with a different amount and with a different maturity date.

The Fed is stepping back as lender-of-first-resort in the repo market.

The Fed raised the interest rate at which it offered the repos – for borrowers, the money is getting a little less cheap. Through January 29, the Fed’s average offering rate for overnight repos was 1.55%. On January 30, this increased to 1.60%. And the rate for 14-day repos increased from 1.58% effective through January 29, to about 1.61%.

The Fed had been the lender-of-first-resort in the repo market, by offering to lend at these low rates. By increasing the rate, the Fed is gradually making the cash it is handing out less cheap and less attractive compared to what banks might offer, and more of the demand is switching over to banks.

Overnight repos have been undersubscribed all year, so there is less and less demand for them at this rate. But the 14-day term repos are often oversubscribed, meaning there is more demand for this two-week cash at 1.61% than the amount the Fed is offering. As the Fed continues to raise the rate on two-week cash, at some point, it will become less attractive than the rate banks are offering, and demand will further decline.

The Fed cut the 14-day repos by $5 billion to $30 billion, effective February 4. The Fed offers two 14-day repos per week. These repos unwind in 14 business days. So at anyone time, there are about four of these 14-day repos outstanding. Reducing the maximum amount by $5 billion means that the maximum amount outstanding, assuming that these repos have been fully subscribed, is getting cut by $20 billion.

In summary, the Fed has done three things to begin weaning the market off the Fed’s repo cash:

- On January 17, the Fed let a 32-day $50-billion repo from December 16 unwind without replacement.

- On January 29, the Fed raised the rates on repos for the first time.

- On February 4, the Fed reduced by $5 billion the maximum amount offered of its 14-day repos

T-Bill balances balloon.

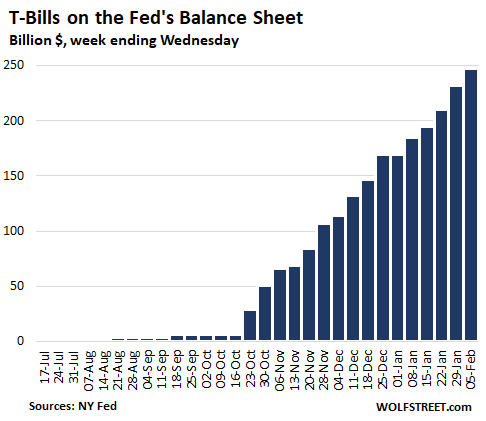

The Fed continued to increase its ballooning stash of T-bills (Treasuries with maturities of one year or less) at a rate of about $60 billion per month. To increase its stash, the Fed has to buy the amount of the maturing T-bills, and it has to buy the amounts needed to obtain the targeted increase of about $60 billion a month.

Over the five weekly balance sheets since January 1, the Fed has added $78 billion in T-bills, and the total amount of T-bills on the Fed’s balance sheet has now ballooned to $248 billion:

These T-bills are a major part of the Fed’s strategy to bail out the repo-market. The purpose is to increase Excess Reserves that banks have on deposit at the Fed. The Fed blames low Excess Reserves last September for the banks’ refusal to lend to the repo market, which then caused the repo market to blow out. So bringing up Excess Reserves to an “ample” level is the goal of these T-bill purchases. Once that “ample” level is reached, the Fed said it will back off this program.

T-Bills Boost Treasury securities.

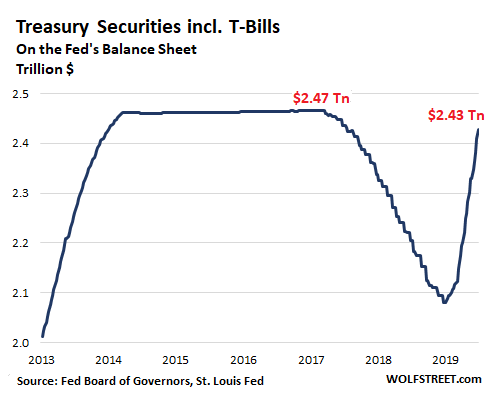

Since January 1, the Fed has fattened its stash of Treasury securities by $99 billion, of which $78 billion are T-bills, and $20 billion are longer-dated Treasury securities. This brings the balance of total Treasury Securities to $2.43 trillion, the highest since February 2018, and well on the way to reversing the QE-unwind of the Fed’s Treasury portfolio:

MBS continue to decline.

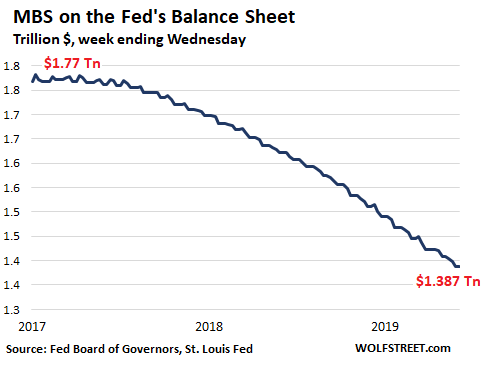

The Fed doesn’t actually sell its MBS. Holders of MBS receive pass-through principal payments as the underlying mortgages are paid down or are paid off. About 95% of the MBS on the Fed’s balance sheet mature in 10 years or more, and the current reduction in MBS is mostly due to these pass-through principal payments.

The lower mortgage rates over the past year produced a surge of refis as homeowners took advantage of the lower rates. As the old mortgage gets paid off, the principal balance is passed through to MBS holders. There has been such a flood of pass-through principal payments that far more than $20 billion roll off the balance sheet every month. So the Fed is buying enough MBS to maintain the $20 billion limit.

Over the past four weekly balance sheets, the Fed reduced its MBS holdings by $21 billion, to $1.39 billion, the lowest since October 2013:

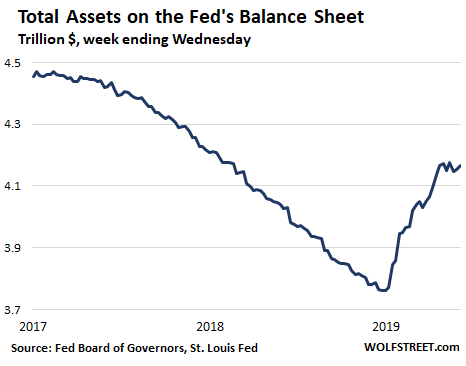

Total Assets: Looks like the end of QE 4.

Sharply declining repos, ballooning T-bills, slowly rising “coupon” Treasury securities, and falling MBS, along with other activities reflected on the Fed’s balance sheet, all combined, have the net effect that total assets, at $4.167 trillion, are back where they’d been on December 25, 2019, and are down $9 billion from January 15 and $7 billion from January 1, but up a tad from last week. This is the image of a balance sheet that has stopped expanding over the past six weeks and is in a mild decline:

Between mid-September, 2019, and January 1, 2020, the Fed added nearly $410 billion to its balance sheet – a huge amount in just three-and-a-half months. The Fed was panicking about the repo market turmoil that threatened to blow up some of its darling hedge funds and mortgage REITs that borrow in the repo market – that have to borrow in the repo market because they’ve been borrowing in the repo market for years and cannot suddenly find alternate sources of cash. And if they run out of cash, they blow up. And rather than let capitalism do its thing with those risk-takers, the Fed stepped in and bailed out its cronies with over $400 billion. But now this task has been accomplished. And QE-4 appears to have ended.

Is this the black-swan event people have been predicting for years? Read… What Will the Coronavirus Do to the US & Chinese Economy?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“So bringing up Excess Reserves to an “ample” level is the goal of these T-bill purchases. Once that “ample” level is reached, the Fed said it will back off this program.”

Is the Fed buying bills from banks that can put the cash on deposit with the Fed as excess reserves? Or is the Fed buying from intermediaries that banks won’t lend to – banks that have excess reserves on deposit, and would rather leave it there, than lend it a higher rates to intermediaries?

The Fed is dealing directly with the Treasury Department and with its “primary dealers” which are the largest broker-dealers and banks in the US.

To get the list of primary dealers, click on the heading “List of primary dealers”

https://www.newyorkfed.org/markets/primarydealers

Thanks Wolf.

So repo market should be fully funded while there remains any excess reserves on deposit at the Fed.

If the repo market needed more funding, that implies the excess reserves had fallen to zero. (otherwise dealer banks would have drawn down the ER and lent it).

if there is no limits on size of repo market, the Fed will need to continue to fund the expansion indefinately via the dealers. (and so there is no upside limit on the Fed balance sheet.

If there are limits on the repo market, what are they in dollar terms, thus we can establish the limit of Fed contingent obligation.

Is the Fed buying bills from banks that can put the cash on deposit with the Fed as excess reserves? YES.

Or is the Fed buying from intermediaries that banks won’t lend to? NO.

Fed only AS OF NOW deal with primary dealers only. It is up to the primary dealers (and their bank holding companies) to relend the money, if they want to.

But there is a new desire for the Fed to do repo with non-primary dealer banks or to lend at the GCF repo to hedge funds. Bad idea.

Wolf, how does this ending of QE4 relate or reconcile with the Fed’s liquidity/stress index…which as far as I can read the small line appears to show liquidity in the system at a recorded all time high? Are there other ways the Fed/Treasury/Working Group-PPT can still pour in easy money?

Keynes66,

Yield spreads are near or at record lows. Yields are super low. Even junk-bond yields are super low. Yield-chasing is in full swing. The financial stress indices — there are several of them — all indicate record-low or near record-low financial stress in the system. For example, the St. Louis Fed’s Financial Stress Index was at minus -1.6 at the end of January, an all-time record low. It has since ticked up to -1.46, which is near all-time lows. 0 (zero) is considered neutral. During the Financial Crisis, the index spiked to over +5.

In other words, easy money still rules. What the Fed’s balance sheet is showing is that the Fed seems to have ended throwing more cash at the market.

The Fed has barely slowed down the massive & ongoing pump of repo into the market.

These dealers know that level of repos can be expected to be renewed as they have the last 3 1/2 months. That is the theme the fed wants & what sustains and drives the market higher while preventing price discovery on dodgy debt securities.

To somehow conclude this is a change of direction by the Fed is really just not born out by the facts as you’ve presented.

Wolf, I love you but I’ve got a part company with your title But I am grateful for your articles and your contributions.

I’ve read a lot about overnight repos here for a while now, and whilst I understand what they are, why a bank seeks to borrow for such a short time period escapes me – anyone care to enlighten me?

When you are buying long dated trash on leverage, you need to post collateral (with portfolio margin, the trash in your portfolio are used as collateral to some varying degree depending on how bad the trash smells).

The value of the trash or collateral fluctuates everyday. If the value of the trash/collateral goes down below a certain threshold, you need to post more collateral or sell your trash and reduce exposure to acceptable limits.

If you dont have enough collateral, you may try to borrow against a portion of your trash to cover the shortfall to avoid forced unwinding of the trash while conviently for GAAP purposes, you still have that portion of the trash used in repo as still an asset on your balance sheet.

If you cant tell the difference between whats trash and whats collateral, well join the club.

Which is why Fed moved closer to cash, shorter duration paper. A liquidity trap occurs when rates are low and investors hold cash against an expected turn up in rates, at which time longer term paper is “trash”. IMO the spread between savings (overnight sweeps) and MMs is what caused the REPO blowup. When someone says “cash is trash” they have taken the Feds Koolaid, (rates are permanently low). When Fed puts enough cash in the system it will be recycled in bond fund ETFs. When there is not enough money investors must make decisions, (reallocate). Monetary Velocity is making new lows. If the Fed is moving REPO rates higher perhaps the savers spread is again asserting itself. Ingloriously they have nowhere left to go in their buying but further out the curve, which brings up OP Twist, and the yield curve.

right, so essentially the only people who pay high rates are little people

Anyone know if there is a risk to short sellers of stock if the repo market seizes up?

SwissBrit,

It is not banks, as in commercial banks, that are doing repos but investment banks, investment companies, brokerage firms, etc…that are doing repos.

Here is the list of primary dealers that does business with the Fed.

https://www.newyorkfed.org/markets/primarydealers

I believe repos are mainly done for money market funds. For example mutual fund companies like Vanguard, Fidelity, etc… have money market funds who’s holdings include highly liquid instruments with a short-term maturity. This includes repos.

Here is the holdings of the Fidelity money market fund.

https://fundresearch.fidelity.com/mutual-funds/composition/31617H201

You are better off taking the SIFMA numbers here,

https://www.sifma.org/resources/research/us-gcf-repo-index-triparty-repo-and-primary-dealer-financing-reporeverse-repo/

Open the spreadsheet at go to Tri-Party Repo Worksheet.

Then look for Non Fedwire-eligible, Money Market, if you are interested at the money market.

I have yet to fully understand the role of Fidelity (I am a customer) in the Repo Market.

U.S. Treasury Repurchase Agreements 12.37%

U.S. Government Agency Repurchase Agreements 9.41%

Other Repurchase Agreements 11.27%

These are dwarfed by…

Certificates of Deposit 34.47% and

Financial Company Commercial Paper 29.60%

I understand you mentioned the SPRXX mutual fund.

My sweep account is in the SPAXX fund which is the Government Money Market Fund.

I hope you understand the 2016 SEC Money Market reform especially those that differentiate a CONSUMER vs an INSTITUTION investor money market account.

The SPAXX is almost in 100% gov’t securities. 7 Day Yield = 1.21%

The SPRXX has a 7 day yield of 1.44%.

So for a spread on 23 basis points, you sacrifice liquidity and counterparty risk.

I would rather buy 4 week T bills that yield > 1.5% in Treasury Direct, and keep currency bills for shorter term cash needs.

Thanks and I do understand the money market reform.

However the repurchase agreements of that Fidelity money market fund (SPRXX) are not really dwarfed by that funds holdings in Certificates of Deposit (34.47%) and in Financial Company Commercial Paper (29.60%) since the repos add up to 33.05% of the fund’s holdings.

34.47 + 29.60 = 64.07%.

Just the facts.

If that how you come to the conclusion that the repos are dwarfed then the same can be said of the Certificates of Deposit. And also the Financial Company Commercial Paper is dwarfed.

SwissBrit,

Banks can borrow in the repo market if they want to, but they have other options, including borrowing from each other without collateral (in the federal funds market). But banks are big lenders to the repo market.

Other institutional investors borrow in the repo market, including hedge funds and mortgage REITs. They borrow overnight because it’s absolutely the cheapest form of borrowing that they have access to. They borrow overnight every day to fund long-term investments, such as MBS (mortgage REITs do that). To borrow short-term to fund long-term investments is super risky and can blow up the borrower in no time. And contagion can spread from there. Hence the repo blowout and the Fed’s reaction to it.

Wolf,

Slightly off topic but I don’t think I have seen a response from you on an item I came a across and mentioned a couple weeks ago – namely that Sept may have been at least partly a lenders’ strike aimed at intentionally starting to goose up the repo rate…which is scheduled to replace discredited LIBOR on a few trillion in syndicated bank loans to corporations.

Have you heard this theory? What do you think?

If true, I would imagine that banks may absent themselves from the repo mkt more frequently going forward.

Not entirely, but enough to push repo/LIBOR 2.0 rates up.

Yes, that’s one of the theories of why the banks suddenly refused to lend to the repo market. After listening to Jamie Dimon some time ago, I thought it was a pretty good theory. For now it’s just a theory, though, like so many others. Years down the road, when no one cares anymore, the Fed will reveal what happened.

I suggest you read up on Zoltan Posar and Prof. Paul Mehrling. They are two of the best. You can also listen to them at the Odd Lots podcast of Bloomberg.

Thanks for this article. At least one theory for the unending bubble in the stock market goes down the drain. very odd to see such major geopolitical issues, reversal of liquidity, reduction in earnings, and yet newer and newer highs in the stock market.

But isn’t it the buying of t-bills that is pumping cash into the market? They fed is taking t-bills out of the system and putting cash in. And that appears to be continuing to the tune of 60 billion per month.

Wolf suggests that the fed is doing that to ‘bail out the repo market’, but where is the guarantee that they money goes into the repo market instead of the stock market?

Or am I misunderstanding?

Z,

You are right – pumped in money is fungible…Repo borrowers can free up funds to put anywhere else they want (constrained by the fact they have to find the money to repay the repo – from somewhere – in fairly short order).

Bottom line: you need cash to fulfill your commitments right now (tonight) or your creditworthiness evaporates. And, since you’re a smart banker, you “know” you can borrow more money tomorrow to pay off the loan you take today (because you are creditworthy). Until you can’t. As long as the music plays no one has to sit down.

I guess it rubs off on the population. On tv there are countless commercials of younger folk checking their credit scores with phone apps, apparently, on an hourly basis. The delight on their faces when they see a larger borrowing envelop? Priceless.

As someone who has avoided debt beyond a mortgage, to buy a home in my twenties, I will never understand this situation. My buddy and an ex employer of mine used to own a small airline. He had a sell-by-before-date and did so, basically retiring at 55. Now, he just leases out his aircraft and develops property without carrying debt. Another ex employer was Mr Debt, and thought himself smarter than everyone else as he expanded. He is now in his seventies and working 6 days per week…down to 4 employees and two aircraft. The difference? Debt. Carrying debt in a shrinking market is no joke.

This so-called expanding economy means absolutely nothing if debt expands faster than growth. And if that expansion is actually fueled by debt all the way up the entire food chain, it’s just a racing hamster wheel with no way to measure what is real and what isn’t.

Lisa said, “Bottom line: you need cash to fulfill your commitments right now (tonight) or your creditworthiness evaporates.”

Debt hiding debt. Doesn’t matter if it’s a bank or a person. It’s all borrowed numbers. Wasn’t their once some quaint concept about a ratio of debts to assets? And when the tide goes out, we’ll see who is standing on their feet?

Like or not but you are living with credit economy like the rest if us. The world the way we know with all the good and bad wouldnt exist otherwise. It is nice that living debt free lifestyle but US economy could not exist or develop rapidly without credit economy. The issue is not debt, the issue is that rich folks aren’t expected to eat losses on bad debts due to central banks, IMF, etc. When they make bad choices we pay, when a poor loser makes bad choices we moralize his consumption and seek to punish him. I guess everyone complicitly agreed that legal entities and the rich just beyond moralizing. Just boys being boys!

As far as credit is concerned it is also worth mentioning “open account” financing (similar to credit cards) used extensively in commerce, especially manufacturing. (1 1/2% discount if paid in 10 days, net 30, which hopefully speeds up payment.) When a buyer can’t meet the terms the need for cash ripples through the supply chain up to the banks. No one accurately tracks this indebtedness. Yet another weak link.

Credit has all the qualifications of a drug.

“We’ll see who is standing on their feet”

As opposed to the long-drowned corpse of ZIRP’d savers – 20 yrs worth.

Cas127:. Yes, Central banker’s killing off those who live within their means to support those who can not live within their means.

Ensuring nobody will be able to support anybody when this hits the wall!

Lisa,

“until you can’t”

Agreed – that is how borrowers go Bk – slowly at first, then all at once (when the lenders keeping you alive finally decide that “you are a bad little pony, and I don’t think I’m going to bet on you any more”).

This market is stuffed to the gills with “bad little ponies”.

It’s not QE4:

“I want to emphasize that growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis,” he said. “Neither the recent technical issues nor the purchases of Treasury bills we are contemplating to resolve them should materially affect the stance of monetary policy.”

“In no sense, is this QE,” Powell said.

This QE is just shorter term than the prior QE’s. I think it is all about keeping the prices for “trash” high.

Right…it shouldn’t be confused with “the large-scale asset purchase programs that we deployed after the financial crisis,..”

Because, there is no financial crisis (apparently), but a record stock market. That’s the only difference.

QE definition: the introduction of new money into the money supply by a central bank.

Looks like a QE4 in my opinion. Because the increase was from a lower base, not from a higher past point when QE2 or QE3 was announced years ago, is that the FEDs argument why it shouldn’t be labelled?

Oops , just seeing your reply now Wolf. Thanks!

It certainly wasn’t designed as QE-4. It was designed as repo-market bailout (because hedge funds and mortgage REITs and other entities were threatening to blow up). Whatever the purpose, the effects are also whatever they are, as we have seen.

Whatever it’s designed as, whatever it’s called, not called or denied ………….

It Is creating new money to manipulate markets, manipulate asset prices, it picks winners and losers, it is socialism for gamblers and the select, and oppression for savers and the prudent. Is it not theft?

Why do intelligent people continue to buy in to the bastardization of language. Quanitative easing is MONEY CREATION and that’s all it should be called. To use the terms of the FED is to be part of their propaganda machine.

Do the world a favor. Refuse to use FED-speak. Call them out for the ruinous scum they are, and pay them the disrespect and disdain they deserve.

“The Fed had been the lender-of-first-resort in the repo market, by offering to lend at these low rates”

Those who are getting this repo money are borrowing below the rate at which the Treasury borrows short term. How is that?

There MUST be a penalty or fee for repeated use of this Fed facility unless, of course, the Fed enjoys the endless feeding of the monster.

Just two things.

First, the “Total Assets” graph in 2019 looks suspiciously similar to the performances of the mega-cap stocks that have been driving the crazy valuations we are seeing right now. I suspect I am not the only one who thinks this relationship is anything but a coincidence.

Second, I have been hearing these central bankers and assorted bureaucrats we cannot send packing moan about “banks refusing to lend to grow the economy” for so long I am wondering if somebody still believes them. If you own a business and/or have good credit rating your mailboxes are probably receiving a non-stop barrage of loan offers from all the banks you work with.

Again, I am really curious to see where this stuff will go after November. ;-)

Re: I am really curious to see where this stuff will go after November.

You might not have to wait that long. The Fed said they will back off repo about April and stop T bill purchases in the end of June.

Ok so they will just buy the 20Y Treasury bond starting June.

Of course they’ll cut back…….now. The equity mkt has been on a tear. This doesn’t prove in any way that the fed is done with this shit. As soon as the mkt goes down five percent again…..you know the drill.

There seem to be two kinds of people on this whole issue. The first kind is the majority and they think fundamentals matter and the market is irrationally exhuberant and will fall to earth when it wakes up.

The second, of which i am a part, thinks the fed is …now…the… mkt. They have usurped that power and the mkt is in no way irrational. The mkt realizes that the fed controls the price of equities and it will do ‘whatever it takes’ to maintain control of the price level of equities. And they obviously have the ammunition to do so when they can buy as much as they want of anything.

Just two more things.

When has a gov’t institution EVER given back control of something that they have acquired control of? How about NEVER! They will no sooner give up control of the pricing of equities than they would give up their control over interest rates, now that they have all these powers.

Also, we all know that they have destroyed pension plans with their zero rates and now pensions are completely dependent on a rising stock mkt. Conclusion: they will do ‘whatever it takes’.

For all the people that think they can’t stop a stock mkt from going down, would you please take a look at the Venezuelan stock mkt and get back to me?

I guess you don’t know much about the history of Venezuela. The revolt of 89 has a long window into time.

Forget about the Fed. When debt servicing reaches the nadir, the cycle is done. My guess this time it’s the 5000 co commercial subprime banks. Much like when New Century of Countrywide mortgage collapsed…….it won’t be good. The consumer underwriter will be gone, the economy will correct no matter what they do.

clyde, you were doing well until part 2.

For example, I’m old enough to remember when Reagan gave US Steel a ginormous bailout in the early 1980s. They proceeded to blow the government assisted bailout on executive bonuses, hookers and blow. And yes, they vaporized the pension way BEFORE the stupid Fed got involved with interest rate suppression full time. There are myriad examples that go back decades of CORPORATE ineptitude leading to pension fund collapse.

Further, while the Fed has ‘elected’ Board members, any guesses where those members come from? My recollection is that JP Morgan, Goldman, et al… have a certain degree of ‘ownership interests’ if I may put it gently.

Finally, I also recall GM, Ford & Chrysler getting a couple of bucks from us taxpayers, ie., the government and lo and behold, we, the taxpayers have zero input now. So, after having a controlling interest in at least 3 of the biggest corporations in the US, it turns out that we HAVE given back control.

Do keep posting, but this ain’t Zero Hedge. Facts matter.

I have no idea why you seem to think the points you make have anything to do with the subject at hand. If you’re a bitter union worker who lost their pension, it doesn’t have a thing to do with the fed attempting to levitate the mkt. And why you might think fed board members from jpm etc are a counter, is frankly delusional.

Do keep retorting, even if you have this problem of staying on subject.

@Clyde – Weinerdog just completely refuted one of your later claims: “When has a gov’t institution EVER given back control of something that they have acquired control of? How about NEVER!”

The US government had control of a number of major corporations in 2009 and gave them back.

One could add the entire wind-down from WW2 as another example. The US also had military control of Iraq and a few other places at various times since, but chose to give that back. And there would be more examples if one chooses to look.

I’d agree with you on a more general point that it’s difficult to persuade powerful bureaucracies to return that power – but overstating your case makes you look bad.

OK, back in your hole, troll. Keep digging.

clyde the snide,

“For all the people that think they can’t stop a stock mkt from going down, would you please take a look at the Venezuelan stock mkt and get back to me?”

OK, I’ll get back to you… The Venezuelan stock market is priced in bolivares, and this currency has totally collapsed. So what you’re seeing in the Venezuelan stock index is a chart of the total collapse of a currency. It really doesn’t tell you anything else.

wut?

Central bankers can make the mkt go up even if the economy collapses. Why are you arguing against that fact?

clyde the snide,

I’m not arguing against that. So please reread what I said.

You used one of the few examples that you should NOT have used, the Venezuelan stock market. The index soared because the currency in which it is denominated experienced hyperinflation and became worthless. Argentina’s stock index is another example NOT to use to support your theory. The peso experiences 50% inflation a year right now, so just to stay flat, stocks would have to rise 50% in a year. You see what I’m saying?

This had nothing to do with the economy but with the currency that a stock index is denominated it. When the currency collapses, the index soars. That’s how it is.

To support your statement, you should have used the S&P 500 or the Nasdaq as examples. That’s what most people do, and it works.

Also, the counter-example is the Japanese stock market. It peaked in 1989 and is still down close to 40%, despite decades of QE and ZIRP and NIRP. There are many examples among European stock markets (despite QE & NIRP) that are today LOWER than they were in 1999 or 2007.

Clyde,

You’ve made your pt pretty clearly – but at the end of the day the Fed can only print money…and really can’t control where that money ends up.

It might start out pumping the SP500 to a 25+ PE…and end up doubling median rents/mortgages…the latter of which ruin tens of millions in the real economy – and must ultimately create blowback politically…stopping the money pump.

Hey Wolf, did you get those rose colored glasses on Amazon? I sure would like to get a pair.

It’s just data. Just the numbers from the Fed’s balance sheet. Go back to basics and look at the numbers. No rose-colored glasses needed. Just reading glasses.

I am ordering rose coloured reading glasses, just like the ones the Donald uses.

When your wearing rose colored glasses, red flags just look like flags.

Donald DOES know the truth. He’s just doing what every President has done before him. Take Obama: “Ah shucks. Look, folks, we had to bail out the banks.” No, Obama, you didn’t HAVE to.

Donald knows what the Fed is doing, just like Obama knew before him.

The Treasury Department is issuing a 20-year bond for the first time in 34 years to help pay for the ballooning $1 trillion dollar budget deficit.

Shhhh: Repo Operation in Process

For you additional edification:

https://www.treasury.gov/_layouts/SPDynamicResources/DownloadS3File.aspx?s3filename=current_production/current_TBACRecommendedFinancingTableQ22020.pdf&x=1581089518122

TBAC already scheduling $10B for June 1 and $8B for June 30. I believe the 20Y bond will be issued just like to 10Y and 30Y =Feb, May, Aug, Nov and the other months as re-openings.

Just the Facts, sir/maam.

Interesting word edification:

the moral or intellectual instruction or improvement of someone.

Government Deficits 100% Funded By Fed Monetary Creation Since September 2019

By Daniel R. Amerman, CFA

http://danielamerman.com/va/ccc/F3debt100Fund.html

That bottom in 2019 and sharp reversal, that was it. We crossed the Rubicon and we are never, ever going back. This is fiat money printing and debt monetization. This is the reality going forward. It’s “not right.” It’s uncomfortable. We may as well start discussing how to deal with it from an investment perspective.

Not buying it. If the market as a whole thought the Fed was going to print money to eternity to keep assets propped, inflation would be running a lot higher. It’s definitional that money printing leads to higher inflation at some point.

I think your view is the minority view. What we are seeing is simple asset price speculation based on nothing more than momentum. Interestingly, Fed proxies are now saying there is no link between QE and stock prices, as though they are warning people that QE won’t continue forever.

I don’t believe there is any new paradigm here. It’s just a momentum-based buying frenzy. Unfortunately for the momentum people, we appear to be seeing a blow-of top in the market leaders. Look at MSFT chart. The good times could be ending, in a big way, pretty soon.

Momentum-based buying doesn’t explain Tesla. Something else is going on here.

Same happened to VW in 2008. Then epic crash.

Real inflation IS RUNNING HIGHER. The three biggies – Healthcare, Education, New Home Building, have been inflating at 5-10% a year for decades now. They have inflated SO MUCH that they now make up over 30% of the US economy!

But they don’t make up 30% of the basket of goods that the BLS uses to calculate CPI!

So in other words that 5-10% INFLATION in Healthcare, Education, and Homebuilding gets counted as GROWTH in calculations of the FAKE GDP, but are barely counted in the FAKE CPI put out by the guvmint.

Yes, it’s a racket, and so far the American people, the slowly boiling frogs in the pot, haven’t realized that the temperature is rising

The other aspect of inflation and interest rates has to do with the question of why we, Europe, China, and Japan, all countries doing QE, ZIRP, or NIRP aren’t experiencing massive hyperinflation, like Argentina, or Zimbabwe, or the Weimar Republic.

And, I’ve finally concluded that this is because of the globalization and coordination of central bank policy with all the world’s major economies inflating their money supplies post GFC together.

It’s not like the 1970s or 1980s, where Europe and Japan had recovered from WWII and the Deutsche Mark, Swiss franc, and Yen were all threatening the dollar as a world reserve currency.

Ask yourself, if ZIRP and QE and inflating the money supply are such great ideas, why couldn’t we have use those tools in the 70s and 80s?

The answer: other foreign currencies were growing stronger – the countries were more frugal than the US – and just waiting for the dollar to slip up. The dollar could have weakened further and the inflation rate would have skyrocketed. The US had to raise interest rates on Treasuries just to get investors to buy them and get serious about reducing its budget deficit as the high Treasury interest costs were at one time consuming up to one third of the Federal budget

So hyperinf

So hyperinflation isn’t happening because the world’s major economies and currencies are all inflating together. Weaker and out of favor countries like Argentina, Venezuela, and Zimbabwe, lacking this special protection, easily get their currencies destroyed on the international market, adding to the costs of imports, thus accelerating any problematic internal inflation into the realm of hyperinflation.

The difference between the way Weimar Republic and post war Germany were treated is notable.

Weimar Germany, groaning with the burden of war reparations to its former enemies, tried money printing to solve its problems. Its former enemies, mainly Britain and France, weren’t going to let it off the hook and crushed the value of the Deutsche Mark in response, and this drove the internal inflation in Germany to hyperinflation levels.

Postwar, the US, realizing that West Germany was burdened by a massive amount of debt accumulated by the Nazis (this was how the Nazis accomplished their economic success pre-WWII, by going off the gold standard and borrowing and deficit spending massively), organized a conference of all the debt holders and got them to take a 50% haircut.

This was done to ensure that West Germany could recover economically and stay out of Communist hands

Don’t forget that before the Great Recession it was unthinkable for the Fed to buy treasuries and expand the balance sheet the way it has done the last decade.

It’s a completely different environment and the Fed has tremendous powers without any oversight from congress.

The game rules have changed.

Agree that inflation is purposely understated by the Fed

The real question is, when does Qe5 start and how big will that be? I’m guessing this year and bigger. Alot bigger. What happens if Qe5 isn’t enough, and they have to simultaneously do something else.

But, the corona virus could cause unforeseen things to happen. Also cannot forget it’s an election year.

it’s good news but way too early for victory laps.

I like the bearish spin on the title : end of QE4.

Then lower in the article is a chart of the Fed’s balance sheet. It is higher than ever and keeps increasing. Dow is going to hit 30k pretty soon.

Fed is out of control.

Memento mori,

“I like the bearish spin on the title : end of QE4. Then lower in the article is a chart of the Fed’s balance sheet. It is higher than ever and keeps increasing.”

Total BS. Put your glasses on!!!! The Fed’s total assets chart is at the very bottom. I know you’re not going to read this article — why bog down your brain with numbers. But at least read the headlines of the charts so you know what you’re looking at.

And if you don’t want to go through this trouble of reading chart headings (and I get that), then at least please refrain from posting BS.

Hey Wolf, I’ve been confused by that too, and I work with data for a living. And I know this isn’t the first time readers have been confused. Unless you know that the Fed owns more than “Treasury Securities, T-Bills”, that chart is easy to confuse with the Total Assets chart.

I wonder if it might help to try leading with the “overall” chart and then disaggregating it, instead of putting out the more detailed charts first and then the aggregate at the end? Or maybe plot the “Treasuries and T-Bills” curve, the “MBS” curve, and the “Total Assets” curve as 3 traces on a single chart?

Might be able to save everyone some heartburn with a slight change in presentation…

In my monthly Fed balance sheet reports, I started out with the overall balance sheet many times. This depends on priority.

Right now, the priorities are repos and T-bills, because they’re new and they’re big, so they come first.

Also note that the title has the items in the same order as the charts.

Once this issue of repos and T-bills settles down, and there is not a lot of movement anymore, the total balance sheet might come first again.

While Fed submits MBS in 14 day REPO it goes largely under subscribed. The last two daily REPOs MBS submitted is more than treasuries, which doesn’t jive with the charts? Is the Fed already thinking of going longer duration?

It jives with the charts. The repo numbers on the Fed’s balance sheet, and those in the chart here, include repos of all types and maturities, including Treasury, MBS, and Agency. So if the mix changes, with more MBS and fewer Treasuries, it doesn’t change the totals. And the totals are reflected here.

This trend of more MBS and fewer Treasury repos has been going on for a while — and it does pose some interesting questions as to why.

The repo bonanza since last September is all about providing funds to fascilitate the t-bill and other treasury purchases.

The Fed is buying 70% of new t-bills. Repo-palooza is all about doing the monetizetion two step. It’s a little dance where the use of intermediaries allows the Fed to sidestep laws about directly buying government debt.

Otis,

So you are saying it is illegal for the Fed to print to buy new issue gvt debt, but not to print to lend to entities…that buy new issue gvt debt?

Sounds plausible.

Cas127 – Exactly. It is explicitly illegal for the FRB to buy newly issued notes/bills/bonds directly from the US Treasury. It is not illegal to buy them from Primary Dealers, even if the Primary Dealers buy from the Treasury and immediately sell to the FRB. This is known as money laundering, for which the launderers charge a percentage.

But the Fed can replace (“roll over”) maturing Treasury securities with new Treasury securities directly via the Treasury department, and has been doing it for years, which cuts out the primary dealers on the roll overs.

The whole point is to roll over repo liquidity via intermediaries, buy t-bills, and flip them to the fed.

Repo money is rolled over long enough to transfer ownership of t-bills from the US Treasury to the Fed.

Look at it like a pass through transaction.

That may not be the best example by definition. What I’m trying to say is repo liquidity is enabling the transfer of debt assets from the Treasury to the fed using favored sons.

How to Read the Fed Repo B.S. at the H.4.1

The h.4.1 is a SNAPSHOT. It only reports what is in the Balance Sheet as of a certain date. That date is usually the THURSDAY of each week, taking into consideration that Thursday can be holiday. The h.4.1 is released each Thursday, generally at 4:30 p.m. Publication may be shifted to the next business day when the regular publication date falls on a federal holiday.

You need to adjust your mind to this calendar because Repos come in 2 flavors:

(a) Overnight Repos. 1 day Repos started on Monday, Tuesday, Thursday, and Friday do NOT hit the h.4.1 balances since they have EXPIRED. They were lent and paid back before they can be even measured by the h.4.1. They affect only the balances within the week but not Thursday’s numbers.

Only overnight repos started on Wednesday hit the books since they are still alive as of publishing time.

(b) Term Repos, MOST term repos are for 14 days; and they are offered two per week (Thus and Tues). Because they live longer, 2 of them will be added to the numbers THIS week, and three of them will be added to the numbers NEXT week. It is the Term Repo that really affects the numbers reported at h.4.1

For example, the past week ending Jan 6, the Fed went through 329.93B or repo but only 170.25B of that gets reported in the Balance Sheet because that is the UNEXPIRED and still active repo balance.

Both overnight and term repos ADD to the available RESERVE BANK BALANCES. Therefore they INCREASE liquidity in the system.

But there is another way to increase liquidity in the system – the Fed buys Treasury securities (like T bills or Notes and Bonds). Because the Fed decided to buy T bills (short term securities maturing 1 year or less) they said it was NOT-QE.

What they did not tell you loudly was their intention to rollover those T bills at maturity. Therefore, they intended to permanently keep the Balance Sheet high regardless of what term of Treasuries they buy. The key is they actually told us again and again they want to keep an ample and high balance of (liquid) bank reserves to help them achieve their monetary policy. This is not open to debate guys and girls.

The only thing you need to understand is HOW (what is the transfer mechanism) these bank reserves actually improve liquidity in the market TO DRIVE DOWN INTEREST RATES. This is the real goal. Ample money supply is the way to drive down interest rates. The way the Fed thinks is that by flooding the primary dealers (big banks) with money (reserves), they will lend this out at lower rates because they have too much of it.

Well that is not exactly happening as there are OTHER risks to lending out money. One of them is called COUNTER-PARTY risk. The ability or solvency of the borrower to pay you the lender.

Most of repo is settled TRI-PARTY, meaning there is a Central Counter Party (CCP) who goes in the middle of each deal and becomes the counter party to each side. They the CCP takes on a lot of risk and have to finance the trades INTER-DAILY. This is one of the biggest issues of a central counter party – Within the Same Day Financing. This is why you are hearing cry babies asking the Fed to directly finance the CCPs today. Without the Fed guaranteeing the money itself, repo is dead. So this is not just an issue of having ample bank reserves. It is a willingness to actually lend.

Since we are dealing with trading TREASURIES here (debt of the US Gov’t), the Fed has no choice but to support it. Hence the Fed is trapped.

Hedge Funds use Treasuries or Agency MBS at Repo to get CASH and use that Cash to leverage highly risky endeavors such as derivatives. If something breaks, they may have a fire sale of Treasuries. Not good.

I hope this explains the predicament.

Sorry the past week ENDED FEB 6. I said the wrong month, Jan.

right, so as many of us understood back when they began QE, the GFC never ended and never will until the system implodes. We’ve been in the eye of the Hurricane for almost a decade now.

Dear FED:

We don’t have the cash right now this minute. Would you please roll over our repo for another two weeks.

Thanks, the Fund

Iamafan,

“What they did not tell you loudly was their intention to rollover those T bills at maturity. Therefore, they intended to permanently keep the Balance Sheet high regardless of what term of Treasuries they buy.”

EVERYONE, including me, rolls over T-bills at maturity. That’s normal. In my account, it’s done automatically. That’s what you do. This is not a secret but normal practice.

When you need the cash, you don’t roll them over, and you take the cash that you get when the T-bills are redeemed. This too isn’t a secret but normal practice.

The Fed had more T-bills on its balance sheet before the Financial Crisis than now. And it constantly rolled them over. At the time, about a quarter of its total assets were T-bills.

Just to maintain its T-bill balance, the Fed HAS to replace (roll over) all maturing T-bills.

If the Fed wants to increase the balance of T-bills, it has to do two things: roll over maturing T-bills and add new T-bills so that the total amount increases. I explained this in the article. This is not a secret either. I do this too when I want to increase my stash of T-bills.

Before the repo mess started, the Fed was already planning to replace some longer maturities with T-bills because T-bills give the Fed flexibility and reduce the average maturity of its portfolio to bring it in line with the average maturity in the market.

Most of the T bills they purchased MATURE after May 2020, so you have not seen the MASSIVE Rollovers yet. I track these purchases by CUSIP in a spreadsheet so I see them. You ain’t seen nuthing yet since they have NOT matured yet.

Some (a small part) of the 60b/mo purchases were 8 and 13 week and you can see LARGE 4 and 8 week Fed SOMA Addon Rollovers on 12/12,19,26/2019 and 1/19,16,23/2020

So action wise, you don’t see it YET, But word wise, you heard them say:

Consistent with this directive, the Desk will roll over at auction all principal payments from the Federal Reserve’s holdings of Treasury securities. As Treasury bill holdings mature, the principal payments will be rolled into new Treasury bill securities.

In addition, I expect them to get tired and simply do an operation twist again. Why bother rollover bills to bills <1 year when that rate is HIGHER than longer term notes because of the inverted yc.

You want to do LESS work.

The T-bill rollover it totally routine. Everyone who holds T-bills rolls them over. To maintain your balance, that’s what you have to do, whether it’s the Fed or a bank or me. The roll-over has no impact on the market because the Treasury Dept also refinances its maturing T-bills constantly (at the T-bill auctions), which is their end of the rollover.

The market impact of what the Fed is doing comes from ADDING to its balances (not the roll-overs). That’s the $60 billion a month it is adding.

The NY Fed actually per-announces their Treasury Purchases. This is not routine. The Fed can always stop T bill purchases.

This is a matter of policy and implementation. It just LOOKS routine but it ain’t routine like my automatic rollovers in Treasury Direct (note Treasury ain’t the Fed). The Fed actually opens this to bidding by primary dealers.

In this case, we are only interested in T Bill purchases. They generally come in 2 flavors or OPERATION TYPES:

(a) Reserve Management Purchase, Treasury Bills 0* to 1. Approximate Amount per event $7.525 billion. Note this is NOT a SOMA add-on. This is solely a purchase from primary-dealers.

(b) Reinvestment Purchase, Treasury Bills 0* to 1. Approximate Amount per event $3.025 billion. Note that this can and may be a SOMA add-on during the weekly public Treasury auctions. The Fed can simply buy these from the Treasury. No need for dealers.

The $60b per month NOT-QE is Reserve Management. This is done monthly till June, 2020 (as their announced policy).

The $20b MBS to T Bill reivenstment is reinvestment. This is NOT done monthly. (There is no given end date to this policy.)

The OPERATION Results are published the day it’s done. You can download an xls spreadsheet also.

You can identify them as Operation Type = Outright Bill Purchases and they are detailed up to the CUSIP and maturity level.

As far as I know, the T bill purchases for RESERVE MGT only started on October 16, 2019.

But the REINVESTMENT purchases started way earlier when the Fed decided to exchange maturing MBS for T bills.

For the readers, you really need to understand what the Fed intends to do with the T bills (about $60b a month) it purchased.

This is not a small amount of money (like the amount coming from maturing MBS purchases). Reserve MGT purchases (Not-QE) is already upwards of $225B today.

If this goes on till June about 4 more months, then another $240 billion will be purchased.

Since the Fed stated they will NOT shred them upon maturity, then effects can be deemed PERMANENT.

Good luck to us who live on interest income.

Curious what you consider ‘their’ assessment of the risks. Publicly ‘they’ were concerned that REPO markets might blowout in Sept. That was four months ago. Then there is the notion that the Fed buying T-bills is somehow monetizing spending? What happens when the Tbills run out? Do the bills come due?

Are they propping up hedge funds, and foreign entities who have to borrow against dollar denominated debt? If the price of (currency) derivatives rises that blows up the hedge and funds unload shares or the dollar blows out, Are we approaching the AIG moment? Is mortgage paper the least significant risk factor, circa 2008? A massive transfer (not a run) on bank reserves, through margin calls, would freeze the mortgage market? Margin calls hardly deserve a mention. When I opened a PLOC several years ago they assured me they would never mark my balance to market. How do you make that kind of promise?

No. The market simply want the Fed to FINANCE the FICC GCF repo.

This move (hand writing on the wall) is obvious. First you get SPONSORED repo (of the hedge funds), then next you want the Fed to fund their (hedge funds’) repo. My goodness.

Source: New York Fed.

On September 11, 2019 the Fed only held $3B in T Bills. That really is nothing, too small to bother to track. Therefore, any rollover of T bills BEFORE September is too INCONSEQUENTIAL.

On February 5, 2020 the Fed held $247.536 Billion of T Bills.

Whoa! In 5 months, they bought more than $245 billion in T bills. That’s what the $60b/mo purchases for Reserve Management purposes “mostly” did. (Some were the MBS maturity to T Bill “swapping”.) The largest chunks of these bills have NOT matured yet. Wait a few months.

Even the TBAC was concerned the other day. Quote:

Next, Debt Manager Katzenbach provided the Committee with an overview of the current state of the Treasury bill market. Katzenbach began by summarizing the recent purchases of bills by the Federal Reserve Bank of New York, noting that purchases have skewed toward longer-dated bills with maturities of more than 3-months. Since reserve management purchases were announced, the spread between bills and matched-maturity overnight indexed swaps has narrowed, representing a richening of bills, though the spread remains within the one-year range. In addition, trading volumes from the Trade Reporting and Compliance Engine (provided to Treasury by the Financial Industry Regulatory Authority) suggest that liquidity in bills has remained robust. Average daily trading volumes of $86 billion since mid-October 2019 are comparable to the prior 1-year average. Furthermore, Katzenbach noted that most primary dealers agree there has been no material change to market liquidity since the introduction of reserve management purchases.

Looking ahead, the pace of Federal Reserve bill purchases expected by dealers through June 2020 could result in the supply of privately-held bills declining to the mid-$1.8 trillion range, which would be the lowest absolute level since October 2017. Katzenbach noted that this level is within the range of estimates for the minimum privately-held supply that would be necessary to maintain benchmark liquidity as implied from primary dealer feedback, but below some dealers’ estimates. The Committee briefly discussed the bills market and agreed that Treasury should continue to monitor the implications of reserve management purchases on liquidity conditions and the level of privately-held bills outstanding.

Watch you set folks.

To clarify he is concerned about a “lack” of liquidity in private markets? So are Nelson and Bunker Hunt running the Fed? Cornering the market in anything implies the price will go to zero, (when the buyers step aside). If rates do float higher, I would assume that would start at the short end, combined with lack of supply. hmmm?

Fed SOMA AddOns (Noncompetitive) is already about 10% of total 2019 Note and Bond Auctions. To the Treasury, this does not matter much because almost all of the interest payments that go to the Fed are actually returned to the Treasury minus Fed expenses. It does not matter what term structure the Fed buys since SOMA Rollover makes the debt permanent anyway.

But where it matters is Yield Curve Control (they don’t want to call it that). They also don’t want to call the massive Fed buying as targeting Interest Rates. They are also concerned that if the Fed buys too many T bills, there would not be enough in PRIVATE hands including the level needed to support the Money Market (short term). They means the Treasury and not the Fed.

Either the TBTF banks are in such bad shape that they still need billions in help or the Fed is playing a shell game to enrich the banks at public expense by promoting the pretence of prosperity with interest rates.

Probably both.

One has to wonder why the banks still need so much bailing out, more than ten years after the last meltdown and during the Greatest Economy Ever.

Wolf, after QE 4 accomplished it’s goal do you anticipate further reductions in total balance sheet? Any thoughts if and when QE 5 will see the daylight?

I expect the balance sheet to fluctuate up and down going forward, sort of what we have seen over the past six weeks, or maybe the moves are little bigger. And I expect the composition to change, in favor of T-bills and shorter-term notes, with MBS gradually disappearing. And over the long term — so years — I expect the Fed to let the balance sheet rise at the historical rate that prevailed before the Financial Crisis (a function of liabilities, the two biggest of which are currency in circulation and reserves)

At the current Fed and with the current President, there seems to be no appetite for bringing the balance sheet down again, as it did over the past two years.

Non-finance-literate guy here. I read 80% of the posts and head is spinning.

Why does the Fed need $4T in anything on their balance sheet? Why do they need a balance sheet? I get the various rants: Cheap $$ for hedge funds (aka primary dealers), preparing to bail out anything from Unicorns like Tesla or WeWork to blue chip banks, keeping equities high across the board…..yadda yadda yadda.

I kinda just want to understand why a small group of banks need to have $4T in anything? Wasn’t 2009+ QE(s) supposed to be “…OK, we will do this once….after this, if you screw up, you die…?”

If, as Wolf says, there really is an unwinding occurring:

1) Why is it not done yet ?

AND

2) What number represents “unwound?”

Sorry….my finance education is sub-101, but I am hopeful a neophyte question might spawn a lightbulb moment for someone.

Why does the Fed need $4T in anything on their balance sheet?

Good question. The answer is because they did it to get out of the last Financial Crisis and subsequent recession. We have not seen anything close to this before; so you are not the only baffled.

I kinda just want to understand why a small group of banks need to have $4T in anything?

They don’t. But this is the way the Fed wants their new monetary policy to work.

There isn’t a social force powerful enough right now to change this.

So here we are.

When will the Fed Unwind repo?

I don’t think they have announced When and How they will unwind the repo.

I could be wrong but I have not seen any official plan.

There is nothing wrong with you. It’s the Fed policy that’s creating a greater divide in our country. I don’t think citizens have to understand the Fed gobbledygook.

Iamafan – I appreciate the explanation. Fed “policy” is baffling. I read almost every Wolf Street article, but the labyrinth of Fed machinations and shenanigans is incomprehensible to me. I don’t understand why they have created all these post-Hank Paulson safety nets and borrowing opps for the big boys which has, as you (and others) have aptly stated, has created a financial and social divide in our culture. I want to cry, but instead I keep chasing yield like everyone else. It is a hopeless feeling.

Beardawg,

Lots of great questions. I’ll just take a crack at this one: “Why does the Fed need $4T in anything on their balance sheet?”

The Fed doesn’t need it. But it decided that asset prices needed to be inflated, including home prices, and that banks, which held foreclosed homes and MBS, needed to be bailed out by re-inflating home prices, and it decided that the largest asset holders need to get immensely rich, and so it embarked on this effort to create the “wealth effect,” whereby the asset holders get wealthier with the hope that they would spend some of this money. These emergency measures were supposed to be temporary and brief, and they’re now permanent, because any effort to back out and reduce the balance sheet crashes the markets, as we have seen.

Way back in 1896 in his “Cross of Gold” speech William Jennings Bryan told the Democratic National Convention:

“There are two ideas of government. There are those who believe that if you just legislate to make the well-to-do prosperous, that their prosperity will leak through on those below. The Democratic idea has been that if you legislate to make the masses prosperous their prosperity will find its way up and through every class that rests upon it.”

Almost all reputable economists are in agreement that prosperity does not “leak through” but instead “finds it way up”. Consumers, not the immensely wealthy, drive the American economy. It was to restore the prosperity of the masses that the Fed focused on mortgage interest rates after the Panic of ’08. Just as in all panics the good assets lost value with the bad. For American families, this meant that household owners’ equity in real estate fell by 43% from a peak of $14.4 trillion in Q4 ’05 to $8.2 trillion in Q1 ’12. The Fed focused on mortgage lending by directly investing $1.8 trillion in recently issued retail mortgage-backed securities (RMBS) that had financed or refinanced one to four family owner-occupied homes, almost all of them middle class homes because of caps on the size of mortgage loans. The Fed also purchased longer term Treasuries to put downward pressure on longer term rates in general. This worked, restoring wealth to the middle-class — by Q3 ’16 household owners’ equity in real estate had risen to $14.8 trillion and in Q3 ’19 was $18.7 trillion. The focus on mortgages also helped employment recovery directly since among the hardest hit sectors in the Great Recession were the residential building trades.

Dink Singer,

Good lordy.

No one is more responsible for the homeless crisis in America than the Fed — the very entity that pays you to post here on every article about the Fed. No entity is more responsible than the Fed for the “housing crisis” in many cities in America where the middle class can no longer afford to rent or buy due to rampant asset price inflation – the very thing engineered by your handlers.

What you just posted is vomit-inducing Fed propaganda. Tell your handlers that. Warren Buffett was the single largest beneficiary of the Fed’s action when his finance and insurance empire got bailed out. You’re talking tens of billions of dollars for just one guy. Explain that to the homeless here who got pushed out of their apartments because they could no longer afford the rent increases due to rampant asset price inflation.

The Fed engineered the biggest wealth transfer in the history of mankind, from labor to capital, and in the process destroyed the fruits of labor.

What the Fed has done is a NATIONAL TRAGEDY. And now it’s sending out its trolls to post its effing propaganda BS on my site. If the Fed wants to post its propaganda on my site, it can buy a banner ad, and I will make it a special deal, denominated in billions of $.

Powell can contact me via the “Contact us” tab. Tell your handlers that. No more FREE effing Fed propaganda on this site. Next time, it’s going to cost a few billions, which is no biggie for the Fed since it can just create the money.

And I’ll spread some of this money as QE & bailouts for Wolf Street readers, instead of feeding it to Warren Buffett.

While the Fed has stepped back on its repo action, the more interesting question is it has been able to. Meaning to say, it sees no crisis on the repo front. What does this mean? That the bailed out entities are now able to get funding without need for the Fed and all is well. Can and how can a crisis come about again? Is it going to be a case Fire-Extinguish-Rinse Repeat!

Wow, Wolf. You are channeling economist Michael Hudson!!

“The Fed raised the interest rate at which it offered the repos – for borrowers, the money is getting a little less cheap. Through January 29, the Fed’s average offering rate for overnight repos was 1.55%. On January 30, this increased to 1.60%. And the rate for 14-day repos increased from 1.58% effective through January 29, to about 1.61%.”

The overnight repo offering rate (the minimum rate for bids) has been kept at the rate set for interest on reserves by the Federal Open Market Committee. From September 24 through October 30 it was 1.80%, from October 31 through January 30 — 1.55% and starting January 31 — 1.60%. While the FOMC kept the federal funds target range unchanged at its last meeting it increased interest on reserves from 1.55% to 1.60%.

I think of The Fed’s repo window activities as ‘Operation PawnShop’ – it seems to work the same way. An entity swaps an asset for cash now, and returns at a later date to repay the cash and regain the asset.

How does The Fed charge it circa 1.5% pa interest fee?

Does it accept $100 million in assets in exchange for $99.9x million in cash?

Is there any legal compulsion for the entity to return to the window and reclaim it’s asset, or could the entity walk away, leave the asset at The Fed and keep the cash? ie The Fed becomes the bagholder when/if the asset turns sour.

Is someone divesting themselves of an asset-class they don’t want to hold and nobody wants to buy?

The FED has been monetizing the Treasury debt since September. This is a temporary pause. Have to keep the masses controlled with BTFD. Print Onward to infinity.