Today’s rate hike by the central bank of Sweden ends an absurdity. ECB and other central banks with negative rates are getting ready to follow.

By Wolf Richter for WOLF STREET.

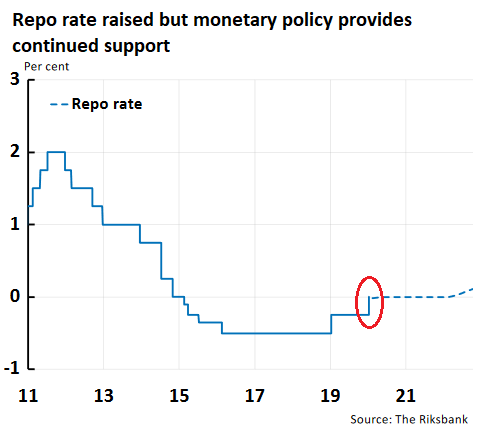

The central bank of Sweden, the Riksbank, has thrown in the towel on negative interest rates, and has become the first central bank in history to do so. At its meeting on October 24, it said that it would “probably” do so, after already suggesting at its September meeting that it would do so. And today, it did so. It announced that it raised its “repo” rate to 0%.

It wasn’t exactly a heroic move, but it was the first time in history that a central bank that had gone full NIRP, and had done so before most others in early 2015, has exited it. The new repo rate will be effective January 8. Chart via the Riksbank’s presentation materials. I circled today’s decision:

All options are on the table: “Improved prospects would justify a higher interest rate. But if the economy were instead to develop more weakly than forecast, the Executive Board could both cut the repo rate and take other measures to make monetary policy more expansionary.”

But it’s not getting out of NIRP because the economy is running red-hot. On the contrary. The statement:

Similar to economies abroad, the Swedish economy has entered a phase with lower growth. However, the slowdown is occurring after several years of high growth and strong developments on the labor market, and overall it means that the Swedish economy is going from a stronger-than-normal cycle to a more normal situation.

Inflation has been close to 2 per cent since the beginning of 2017. After an expected decline over the summer, it has once again risen to just under 2 per cent.

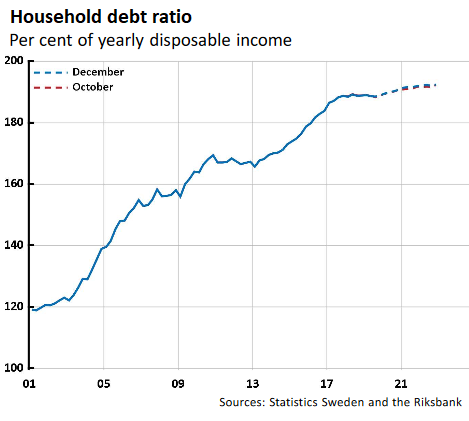

One of the motives for raising its repo rate out of the negative is visible in its warning about household indebtedness which is among the highest in the world – with household debt exceeding 190% of disposable income — in part due to the low and negative interest rate environment that caused Swedes, as would be expected, to borrow with reckless abandon. The chart (via the Riksbank) includes the Riksbank’s forecast that household indebtedness will continue to rise, though it has started to dip just a tiny little bit:

The Riksbank suggested the government should take measures to tamp down on this reckless abandon and its impact on the inflated housing market:

Swedish households are heavily indebted and thereby sensitive to changes in economic conditions. In order to reduce the risks linked to household indebtedness and address the structural problems on the Swedish housing market, measures within housing and tax policy and appropriate macroprudential policy are required.

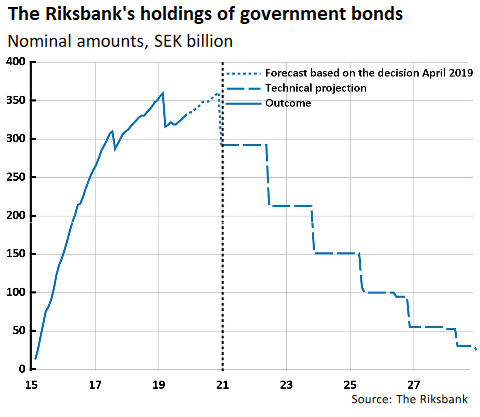

QE continues but at a fraction of its former rate. The Riksbank forecasts that it would end QE entirely in 2020 and start unwinding its positions and reduce its balance sheet in 2021 until all its QE government bond holdings have disappeared from it by around 2030. The chart below shows the “forecast” through 2000, and at the beginning of 2021, at the dotted vertical line, its forecast turns into a “technical projection”:

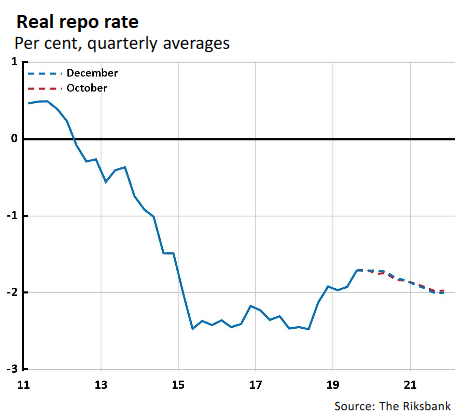

And it also pointed out the “real repo rate” – the repo rate minus the inflation rate as measured by CPI – was still steeply negative at near -2.0% and would remain so, brutal financial repression still being the rule:

The Riksbank isn’t exactly the largest central bank with negative interest rates; those are the ECB and the Bank of Japan. The ECB is now undertaking a “policy review,” to determine how it wants to move forward. It is facing a wall of resistance against negative interest rates among the finance ministers of Eurozone member states because of the damage negative interest rates do to the banking system and pension funds, and because of the housing bubbles they’re now creating. Among ECB governors, the wave of resistance against negative interest rates has already boiled over the top when Draghi was still running the show. And the ECB’s policy review will likely produce a NIRP-exit strategy. But little Sweden has led the way.

Canada’s “high household debt load is the most important risk facing the financial system,” said the governor of the Bank of Canada. But it’s complicated. Read… The State of the Canadian Debt Slaves, How They Compare to American Debt Slaves, and the Bank of Canada’s Response

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Rising inflation will insure negative rates for some time to come. Ask any saver.

So higher inflation will lead to negative rates? Ask any saver? Did you get your economics lessons at Trump University? ECB has missed inflation targets since forever that is why we have negative rates.

I think Endeavor meant to say “negative real rates” — the rate minus CPI. That’s how I read it.

Thanks Wolf. We have had negative real interest rates for quite a while if ones looks at shadowstats.com and/or the Chapwood Index I think it’s called.

I have been reading everything I can find on stock SKT. It illustrates how the current low interest rate regime works.

In the US there are excess deposits people have in the bank drawing less than 1%. Banks loan the money to SKT for 3.5%. SKT runs their retail rental rental operation with leverage and pays out much of free cash in dividend which is 9.5%. Of course bricks and mortar is under stress so you have to make a judgement on that. So as an investor there are 3 of the infinite choices. Leave your money in the bank and get 1%. Buy you some corporate bonds and get about 3.5% or go out on the risk curve and get 9.5% knowing you might get crushed if things go wrong.

I love the chart about the projections how they plan to shed the government bonds through 2030.

Reminds me about our Fed’s tightening, it didn’t last long did it before they reversed it to take the balance sheet even higher. Dow 30k here we come!

And so it goes…as we mortgage the future of our grandchildren who are NOT even born yet !!!

Yup. Wishful thinking. Japanification or kurota style laughter awaits the western world. Someone will try to form a global debt reset talk to extend the Ponzi. But first a major distraction is needed.

We all know the end result, when a CB tries to do a 90 to 180 degree turn on massive government bond accumulation! This ‘plan’ from a NIRP country?

once I painted myself in a corner….

Not a good position to be in, ever…

Beware condo owners…

Latest scam for any quick big returns is buying up condo’s and forcing owners to pay up for the new hefty fees in which your locked into the contracts.

What is this magic occurring in Sweden? If growth is slowing there, even from “red hot” to “normal”, how does raising rates, even from NIRP just to zero, in the face of a massive household debt level, not trigger huge problems? If it’s really that easy to exit the deep hole of NIRP, then why does a measley 25bp rise in the historically low interest rates cause chaos in American markets and panic in the housing industry during a boom economy? And how can Riksbank unwind all of its assets, when the Fed nearly crashed the global financial system by bleeding off a relatively few billion? Like Sweden, we also currently have less than a 2% inflation rate (officially), so that can’t make the difference. I say we’re either doing things grossly wrong, or we should import an ocean’s worth of whatever Kool-Aid the Swedes are drinking.

You ask an excellent question. How? Answer: they can’t.

If a commander of a spacecraft decides to investigate what’s inside a black hole but later, after going beyond the event horizon, realizes only death awaits and so commands the craft be turned around, well… it won’t happen.

Central bankers have gone beyond the event horizon of their own black hole. They can say whatever they like but the gravity of hyperinflation has grabbed hold and there is no escape. Their best course is to continue to announce that getting crushed by an inflation black hole is a good thing – like a bad 1980’s Disney film a utopia paradise must surely await on the other side.

Very good analogy! … will they ever discover who the “evil mind control aliens” are that tricked them into the black hole in the first place?

You know the answer, don’t ya? Those evil savers! /s

Wishful, magical thinking is the curse of our day….even the Christian websites have shed the verbs of the Gospels and gone headlong into the crazy house.

It’s everywhere….like bad Disney films.

But there IS a solution and the only Black Hole is our own refusal to acknowledge that solution: interest rate increases can be completely and totally offset and then some by vigrious, aggressive, government social spending that benefits working people.

Waiting for a western world pension system to go bust, then let’s see what happens. Wonder how they fix that.

Iamafan Simple they will inflate the money away by printing Same as ever No magic to it The Romans did it by clipping the coins right?

Sweden November CPI inflation was 1.8%.

Negative interest rates will not put bread on the table.

There are European stocks with higher dividend yields.

Yes, see chart #4 above (near the end of the article), about the “real repo rate,” adjusted for inflation, with projection into the future.

still better than some Eurozone countries like Netherlands, with -0.5% to zero rates on savings accounts and CPI 2.7% (for those who believe in fairy tales) plus a 1.2-1.7% wealth tax: real rates for savers are 4-5% negative even if you believe the Ministry of Truth :(

Lo and Behold, as Global Trade was brought to near standstill on a dime, countries RAISED rates…..just as E-CONjob 101 predicted, NOT!

We (the fiat dollar world) have traveled too far down the road to now use interest rates to correct the problems of all types of debt. Governments will not collapse themselves, they never do. A peaceful,thoughtful controlled exit is impossible. Cry havoc! And un-leash the dogs of war.

Proof that central bankers are idiots: some guy who lives in his van has a better idea what their own future policy will be. They believe (or at a minimum say they believe) they are going to raise rates above zero, stop printing money and reverse all of their past money printing. How is it possible that they don’t seem to know what even I know: they are going to lower rates deep into the negative (to tax bank accounts) and they are going to print insane amounts of money to fund government spending – same as all other central banks.

Central bankers have no credibility, why does anyone pay attention to anything they say. The ONLY time central bankers are telling the truth is when they say they will be printing more money.

Apparently the bar is pretty low to achieve a PHD in economics.

“Apparently the bar is pretty low to achieve a PHD in economics.”

I think it’s gone negative.

Ha ha! I saw what you did there!

In my experience of a few New Zealand and UK central bankers, they are typically not much more than useful idiots. This is a logical outcome. When central banks were made independent, the idea was that they would deliver the hard medicine when politicians got out of hand with deficit spending. But what govt wants a central banker who will try to thwart their plans. So they choose bankers who aren’t completely useless, but are still easy to manipulate and not smart enough to know when they’re being played.

It’s the same reason property developers are all like trump. Not completely stupid, but so full of themselves that they don’t stop and question why those friendly bankers are throwing money at them during bubbles times.

The exception to this of course is Carney. But politicians don’t need to be able to control him, because he has their interests at heart – keep the bubbles going.

Apparently the bar is pretty low to achieve a PHD in economics.

Mainstream economics became the propaganda division of the Financial Industrial Complex in the 1980s, depending on who you ask. When you sign up to become a Ph.D. economist you’re signing on to become a shill.

It’s too bad. I was thinking of getting one.

The bar is low for academic rigour, (lots of hoops to jump through), but the cost of obtaining a PhD is beyond expensive. I really like doing research. I then priced out a PhD program and did a recovery cost-benefit-analysis factoring in my age. The answer was work just a few years more and then retire. Now, I research radio gear and build furniture for winter projects. :-) Waaay more satisfying.

Me too. I’m very partial to tube amplifiers and quartersawn red oak, only available from the New World, but for a long time I’ve mostly made tools and string instruments and only the occasional tube, although I did restore an Orange amp recently. People who want bells we send to Innsbruck to see Grassmayr. He takes cash.

My favorite economist is Richard Wolff, mostly because he’s a Marxist and is always right. Entrepreneurs are typically Marxists because they own their own means of production, avoiding a lot of grief by pretending to be capitalists.

Have to admit, making the economics program have a poor cost-benefit ratio is a great way to filter out people who understand economics.

I also like doing research and got a PhD “light” long ago when college was still cheap; but my work in bio solar energy was axed by the government in favor of fossil fuel and nuclear subsidies. End of research career … After several decades I started doing research on my own outside official academics, and even got an official publication out of it. I can do research that no one else does because it is too risky or expensive (in time required) for official academics ;)

Academic ethics have gone down the drain over the years; if it isn’t for boosting ones career opportunities (in big government or big business?) I don’t see much value in academic education nowadays.

Modern economics is constructed on the wrong foundation. It’s really something akin to political economics or deceptive economics.

It’s built on mathematics and central planning and assuming a 2% inflation rate and elastic currency. Fiscal policy and monetary policy has so many politiburo carrots and sticks in it that overall it’s just a dead on the economy. Just like in article above central banks are giving people incentive to borrow and then complains about it when they make a housing bubble.

Hard sciences and social sciences are totally different. PhD in chemistry, physics and biology has more objectivity and reproducibility than the economics which is really a social science. Lot of these people in big places are PhD economics from ivy league schools. When premise, objective and hypothesis is bad, the following methods, advanced computers and rigorous statistics will give very crappy results. Crap in = crap out. So, like you said, in social sciences your guess is good as a PhDs

Which is why there is NO Nobel prize for economics. Check it out, the Nobel family is stilled pissed about the faux prize given out.

Central bankers are not selected based on their history of boat rocking, I suspect. The function of these institutions is to suppress any signals of alarm, and to fit everything into an image of normality and control.

One tools in their toolshed is to employ simplistic models dressed up in complexity, feed in some unsubstantiated, yet somehow established, false assumptions, and hey presto, we’ve got rainbows and unicorns projected into the future. Otherwise known as crap in and crap out, with some crap thrown in between for good measure.

I imagine that a number of the protagonists, however, are privately asking themselves questions, and furiously crossing their fingers and hoping that someone comes up with an economically viable fusion reactor or something, so they can go on pretending that it mostly their monetary policy, and not thermodynamics, that determines our prosperity…

Solution Pull your savings from your bank and buy Gold and / or Silver The banksters kryptonite

So the NIRP crisis is over then? Woo hoo.

Premature jubilation, so to speak. But it’s a start.

OK I laughed out loud, literally. Well played Mr. Wolf, well played, sir.

It’s the start of yet another lie. Sounds like status quo to me.

Lies are a part of the process down the path of a currency crisis, just a way to avoid politically unpopular, but desperately needed, austerity.

There is now no check on government spending, Powell has signaled the Fed will monetize any and all deficits, this is a very dangerous turn for the currency. Wasteful government spending can never be cut and becomes structural/permanent (until the collapse of the currency enforces austerity).

This same script has played out so often in history that it’s hard to believe people are still willing to buy into this free lunch fairytale.

VDBR:

Central bankers have gone beyond the event horizon of their own black hole.

We (the fiat dollar world) have traveled too far down the road to now use interest rates to correct the problems of all types of debt.

Both are apparently true.

NIRPZIRP was the wrong thing to do, as were bank bailouts, bank deregulations, and causing debt to launch skyward, but it was all necessary to preserve the wealth of the richest, and that’s pretty much their job.

What was needed, and still needed, is radical reform of the global banking system and enforcement of the laws, but they’re not about to do that, and will not even when the markets tank again. Soon enough they’re going to wish they had, but by then it will be too late. It’s probably been too late for years.

Sorry, Dr. Doom, but I neglected to include your credit in my reply:

We (the fiat dollar world) have traveled too far down the road to now use interest rates to correct the problems of all types of debt.

This comment, and thinking back on the article’s exposure of personal debt levels, leads me to state that much of the problem is personal responsibility. I think of Canadian debt levels. So, when this BS passes, and it will one day, is the meme going to be it was the CB fault and somebody else has to fix it?

My Dad used to say, “No one owes you a living”. I expect if he was still alive he might say, “No one should be expected to cover your debts or fix your stupidity”.

Correct. Between 2004-2007 U.S. banks had terrible underwriting standards, but no one forced people to take out huge mortgages they would not be able to repay.

Ditto with retail investors shoveling money into wildly overpriced stock index funds today.

no one forced people to take out huge mortgages they would not be able to repay

Predatory lenders don’t need to force anybody. Deception and externalisation of financial consequences work just fine.

People were weaseled into taking out extravagant loans on promises that house prices only go up, so buyers could always sell if things didn’t work out. The process was enabled by, among other things, non-enforcement of underwriting standards.

Similar processes will eventually take down the equity markets, but you probably already knew that.

Disagree, vehemently!

Lenders and NOT the borrowers invented sub-prime loans like:

stated income only, interest only, No verification loans and NINJA loans etc!

Besides lenders specifically failed to follow the cardinal rules of lending anywhere in the world!

Fiduciary duty and DUE diligence before doling out the (depositors’ money) loans to ONLY ‘qualified’ There was no exception under the CIA (Community investment Act)

They did the same (malfeasance) thing across the Atlantic!

I am sick of reading about pointing fingers to borrowers only when in fact Lenders went unaccounted, unchallenged and unpunished! In stead they got bailed out! Wow!

2Sunny129:

Both borrowers and lenders (and the people who enabled them, central banks and politics) are to blame. For sure no one put a gun to borrowers heads forcing them to buy. And in general BOTH have been bailed out while those who did NOT participate in the madness (savers, small business, taxpayers in general) got the bill.

In Netherlands almost no one who took on too much housing debt got in trouble after the Financial Crisis and this has created huge moral hazard. If people are 3 months behind in paying the rent they are evicted; if people haven’t paid the mortgage for nearly one year they aren’t even registered as delinquent over here. After the financial crisis many focal borrowers who got in trouble were forgiven (most) of the loans and many of them could stay in the home that they really cannot afford, no bad consequences. Basically the ECB bailed out the whole EU housing market (especially in Spain, Netherlands and a few other countries with extreme RE speculation) and despite this story about Sweden I see ZERO sign that the ECB is going to change direction, on the contrary – it looks more like they are doubling down on their stupid, reckless policy of taking from savers and giving to speculators (both the big ones in the financial sector and all the little ones in the housing market).

Netherlands had a small housing bubble in 1975-1980 caused by a relatively small number of private housing speculators. Prices increased by about 100% and then crashed by -50-60% ion 1981 when the bottom fell out of the market. Many of the small speculators got burned and they deserved it. After that the housing market went nowhere for 10 years, people learned their lessons. But such lessons are quickly forgotten with the help of central banks, politics and the financial sector and as a result we now have a bubble that is WAY bigger and will take the whole country with it when it finally pops. Some other RE speculation countries like Spain probably same story. While Sweden seems a bit worried about a housing bubble, we can only wonder what they are thinking, with nice Swedish homes selling for less than the price of a simple car garage in Netherlands ;(

Only a very harsh lesson (not just for the big players, also for all the small housing speculators) will bring the EU economy back on sound footing.

I’m so sick of economic experts with no solutions. I saw a wonderful author today talk about the gig economy and the horrible working conditions. When asked about a solution for the little guy who cares, he said, “Leave your Uber driver a nice tip and good rating.”

I love that….be the one with a little candle.

As a young boy my Mother would drag me to Doctors because of some health issues. By my teenage years I became skeptical of “experts” of all sorts (almost always adults). One of the smartest lessons I ever learned and I learned it early.

The nominal rate is nothing. This trifling move by Sweden is meaningless.

The [ rate of growth of currency supply ] – [ nominal rate ] IS your real rate

For example USD supply is growing about 7% annualized and us 10 yields about 1.9% right now so your real rate is -5.1%

So real rates are negative just about everywhere right now. This is global theft.

This is global theft.

You’ve discovered the subtext to nearly every article on this site. Congratulations.

..and who gave you the secret decoder ring?

But we owe it to “ourselves”. Are we global thieves?

The gig economy can be great. Millions of people (yours truly included) work as independent contractors. I do NOT want a full time job. Been there done that, never again.

As for Uber drivers, it was never intended to be a full time job. It’s mean to be a part time gig for people with some time on their hands. If you’re driving full time for Uber, you’re doing something wrong in life.

CA has effectively banned gig workers. Which is idiotic and also won’t change anything. All you need to do is incorporate, hire yourself, bill yourself out to the client and presto….you’re a “full time employee” and not subject to the law.

I love that….be the one with a little candle.

It is better to light a single candle than to curse the darkness, but when you’re caught out in a typhoon you’re better off with a generator.

Wow, what a terrible piece of advice: ride Uber but tip better.

That’s right up there with: The American health care system is working great, which is why there are so many GoFundMe campaigns.

Once you have spent too much (LBJ Viet Nam plus Great Society), you have to pay the piper. We paid with a recession and inflation then.

Debt expansion means good years, when it pops means bad years. We were stupid enough to do it again (middle East and welfare state). Only question is who and how the payment is to be made. That will be determined by politics. Printing money doesn’t fix anything, but does make for winners and losers.

Who got the money during the last 35 year debt expansion? You can make the list. Who didn’t get it is the average Joe without political connections.

Way off topic, but I appreciate the Sexiest Bikinis of 2019 ad and also the Trendy Swimwear for Large Busts ad as well. Great content and great ads – a winning combo!

I feel cheated. Nothing of the sort for me.

Correction, i do receive the great content thanks to Wolf and all of you.

Merry Christmas All.

Crush the Peasants!

Is this what you saw? I just now saw it again. People who’re blocking ads have NO idea what they’re missing. Click to enlarge (the image) :-]

And NJGeezer, just for you, so you don’t feel cheated.

God I love this website

the sentiment in the comments is that no one believes the central banks. but the bankers did give themselves an out (of course):

“But if the economy were instead to develop more weakly than forecast, the Executive Board could both cut the repo rate and take other measures to make monetary policy more expansionary.”

black hole 2020!

let’s see if they can flip-flop even faster than Mr. Powell ;(

And if they don’t (little chance IMHO) it will be interesting to see what happens when Christine Lagarde manages to jack up official CPI in the eurozone to at least 4% as desired. Sweden isn’t an island …

After the past twenty years of characters like Greenspan the Bernank and Mario Dragski why in gods name would anybody trust central bankers

One swallow does not make a summer! Let us see what these schmucks do when the markets take a tumble like it did in Dec 2018.

As long as we provide the keys of the country to the schmucks, whom we call central bankers, we cannot be sure of when the rates will turn negative again.

The only question is will these schmucks be recognized for the arsonists that they are when things go downhill or decorated as the firefighters that they portray themselves as!

The problem right now is not financial markets: those go only up because… nobody is exactly sure but in the doubt overpay for certified money losers like Netflix and Delivery Hero because the price will go up even further tomorrow.

The problem right now is industrial production, or to be more precise the ceiling industrial production worldwide hit after the boom in 2016-8.

This is especially palpable in the capital good sector, stuff like five-axis CNC and injection molding machines. This is stuff whose demand can only be artificially stimulated so much, and that particular card has already been overplayed.

Put it this way: people have grown accustomed at seeing order books grow by 30% per year and now are throwing a tantrum because orders are stagnating or growing by single digit. Apparently they stopped attending Sunday Bible school before the seven fat cows and seven lean cows part in the Book of Genesis.

For politicians and their pals in the media such issues always stem from the demand side, meaning the solution is always more tax cuts, more deficit spending, lower rates… more stimulus for short. But demand is maxed out. In fact the fat orders book have been trimmed all year long as folks realize they don’t need a dozen arc-welding robots, just four or five, and that’s in the present good times. People shouldn’t sign contracts immediately after a demonstration. ;-)

While I am pretty much sure the ECB and the BOJ will slash rates and increase asset purchases even further in 2020 to stimulate demand, effects will remain very limited for the simple reason industrial production already sits on an extremely elevated plateau.

Even assuming no real-world recession in a major market (we’ll avoid that, but exclusively thanks to unreported inflation and population growth) industrial production is bound to come down as capital goods are delivered and order books whittle down. No amount of stimulus can prevent that, but it won’t stop the folks at the helm from doing it.

“While I am pretty much sure the ECB and the BOJ will slash rates”

I am not so sure of ECB slashing rates given the now fairly vociferous noise about NIRP from the decision makers and powers that be.

Regarding the demand, I have always thought if you bring forward the demand today, are you not creating a vacuum some time in the future? It is a vacuous idea at best, but taken it to extreme (as these guys have done over 30 years) demand will definitely fall like a stone one say. May be that is what is playing out. One does not know. This game can last another 30 years for all you know. The problem is as long as it appears that the fire has been put out no one questions the strategy. More galling is the fact when it all comes apart (as it has to!) these guys at the Fed will not only get away but will be treated as great firefighters.

Euribor 12 stood at -0.175% when this “rebellion” started. At last check it stood at -0.270%, hardly an indicator of change. I’ll believe these folks when Euribor 12 goes positive and stays positive for at least six months.

Regarding demand… I could go on a long-winded tirade about the dynamics of capital goods nobody really wants to read, but suffice to say they aren’t the same as those of the car market.

There are a tons of headwinds right now, and none of them has to do with an ordinary recession, and that’s the reason of the disconnect between industrial production and everything else.

Layoffs haven’t started yet because order books are still thick from 2016-2018, but expect them to start in a few months as old orders are fulfilled and new orders can’t replace them. One factory here, one factory there, maybe not massive layoff but cut a couple of shifts… not enough to cause a recession but enough to send politicians and central bank officials into a frenzy, and just at a time when they are slashing rates like there’s no tomorrow to prop up real estate and other unproductive assets.

Let’s see where Euribor 12 is in a year and the loser has to buy ice cream. ;-)

My brother works for a Swedish corporation and from what he told me the high level of household debt there is a pretty hot political topic, especially given said debt is closely tied to the high cost to of living (due to wages not keeping up with real life inflation) and especially crazy real estate prices.

Problem is nobody really wants to tackle the issue of the high cost of living and even more critical nobody wants to prick that magnificent real estate bubble. Nominal GDP growth figures are at stake and we all know they are all that really matter.

But at the same time those increasingly angry voters need answers, otherwise Sweden may join Germany in the list of countries whose once stable political system is cracking.

So what a better solution than pretend to do something about that out of control household debt and high cost of living by hiking (nominal) repo rates all of a massive 25bps? That will cause jaws to drop!

Move over Volcker defeating Nixonomics in one fell stroke: when the going gets tough, the tough hide under the table.

Sweden, the country that is still in complete denial about their serious migrant / crime crisis. The “solution” will be even more government manipulation and MSM propaganda.

How dare they!

@unamused

What? With Russian tubes?

Woodworking was a hobby of mine. Quartersawn wood, rare and too expensive. Only special yards have cherry, walnut, etc.

My father in-law made violins and the larger voila. I remember buying my kids violins from Romania. My mother distributed her silverware to her kids years before she died. I am not sure how I’ll ever use them on Popeye’s chicken sandwich. I’ll be missing the old world. I’m not a big fan of the new one but I’m lucky to be alive.

With Russian tubes?

Hardly. Start with a torch and a jig and glass-working tools.

Popeye’s chicken sandwich

That’s a symptom of a larger problem.

I’ll be missing the old world.

I won’t. We do preservation.

It’s bigger than Sweden.

https://data.oecd.org/hha/household-debt.htm

Click on Table, then click to sort on “latest”.

US is “only” 108%. Sweden is 188.9%. Denmark is 281.33%.

Isn’t that the place where Mortgages are negative?

It’s peak fiat money and peak debt. The bubble is in sovereigns and its oozing out in all the seams.

Denmark has slightly negative rates at one or two banks, but that’s not the real cost for a mortgage. I think the actual cost of a mortgage is lower in Netherlands, e.g. 1.0% for 10-year fixed rate, with a significant chunk of that one percent paid by the tax payers (income deductible).

Denmark had household debt close to 300% some years ago; they realized that trouble was brewing in the housing market and debt has been declining a bit despite negative mortgage rates (also negative rates for some small business loans, if you have a real stupid idea for burning money, Danish bankers love to hear from you …).

Number 2 the Netherlands on the other hand still has the pedal to the metal when it comes to household debt, politics is using every incentive they can think of to entice splurging on even more debt (primarily for housing speculation, other debt relatively insignificant). I’m pretty sure the Dutch will be number 1 (again) for household debt in 2019 or 2020.

One day my furnace will burn that instead of oil.

Until the rates actually become positive I wouldn’t hold my breath.

LIBOR is starting to show some action. EEFR and SOFR are complete frauds, Powell manipulated government interest rates.

Watching Repo in the last few days has been uneventfully boring.

The Fed has taken out all the excitement.

The December 2019 compared to December 2018 bank reserves number is similar (around more than $1.6T). Cash bank assets are around 1.8 -1.9n T. Same same. What’s there to blow up? The Fed is watching diligently. Balance Sheet reflects similar size of Treasuries (about 2.68T) and MBS (about 1.88T). So there is still enough balance sheet. December 31,2018 overnight GCF repo spiked to 5.149%. But now the Fed is watching with hawk-like eyes.

I think Mr. Zoltan Pozar will be very unhappy, maybe.

So long as private debt is so high I can’t see adjusting base rates up or down will make much difference to the real economy. Surely central banks know this. So what’s their game?

Really negative interest rates are only one recession away. And then they are here to stay.

“It is the Federal Reserve’s actions, as a central bank, to achieve three goals specified by Congress: maximum employment, stable prices, and moderate long-term interest rates in the United States””

I repeat, “moderate long term rates”, not extreme, neither too high nor too low. Objective: to maintain a fair balance between lender and borrower. To keep a positive yield curve.

Why has everyone forgotten this, forgotten to mention this with the other two mandates?