Rising first-payment defaults and 60-day delinquencies, which are “leading indicators,” caused the retailer to become “prudent.” Shares plunged 33%.

By Wolf Richter for WOLF STREET.

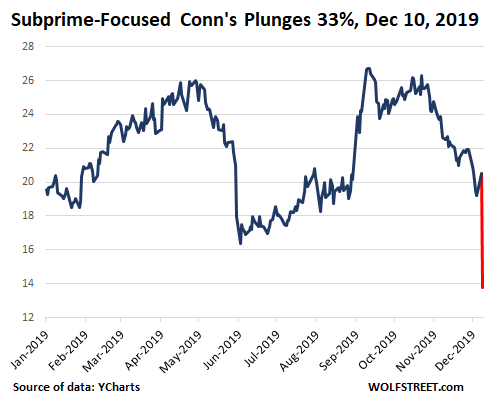

Conn’s – a retailer with 137 stores in 14 states that sells household goods and electronics to subprime customers preferably financed at blistering interest rates or on a lease-to-own basis – had a five-year anniversary of a crash on December 10.

Its shares plunged 33% on Tuesday after it reported earnings, on issues that included credit deterioration among its subprime customers. Suddenly rising 60-plus-day delinquencies and first-payment defaults, where not even the first payment is made, caused the company to become “prudent” and “tighten credit,” which caused same-store sales to drop 8.5%. And shares plunged (stock data via YCharts):

The company cited several reasons, including the dropping prices of TVs, with the average selling price for all TVs down 8% during the quarter, and for large-screen TVs down “nearly 22%,” according to chief operating officer Lee Wright during the conference call (transcript via Seeking Alpha). But what spooked investors was the warning about the deterioration in its subprime credit portfolio and the actions Conn’s undertook to get a grip on it.

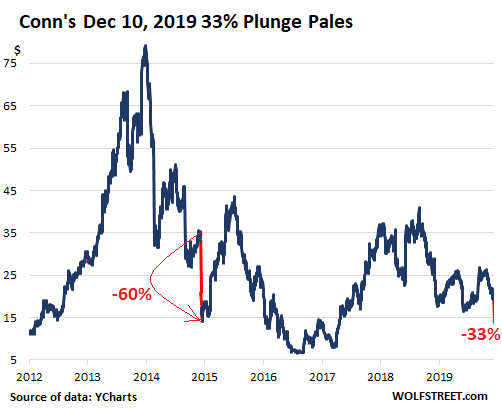

Five years ago, between December 9 and December 16, 2014, Conn’s shares plunged 60% on subprime credit issues. And even that was only part of the 83% plunge from the peak of $79.24 in December 2013 to $13.80 now (stock data via YCharts)::

“During the third quarter, we began to see deteriorating performance of certain segments of the portfolio,” said CEO Norm Miller during the earnings call.

New customers and customers who applied for credit online earlier this fiscal year, that’s where first-payment defaults and 60-plus-day delinquencies were suddenly increasing, he said. So the company made “prudent underwriting adjustments” – tightening credit – which cut into same-store sales.

“I mean, when we tighten, we tighten by increasing down payment, we tighten from a lever standpoint, we tighten by just declining outright,” Miller said. “All three of those are actions that we take to impact the credit availability that we provide. And ultimately, that will reduce sales.”

And COO Wright warned: “Our near-term provision and allowance will be higher as we account for charge-offs associated with accounts originated prior to the third quarter.”

The company increased its store count by 13% year-over-year, adding 16 stores over the past 12 months to a total of 137 stores.

And despite the big increase in stores, product sales (not finance charges) fell 1.3% year-over-year to $280 million.

What increased were the credit revenues (finance charges from loans and lease-to-own). The company financed 92% of its retail sales, via three financing options: the majority are financed in-house; Synchrony Financial financed 18.5% of retail sales, and Progressive’s lease-to-own accounted 7% of retail sales. These credit revenues rose 8.5% to $96.6 million.

In its 10-Q filed with the SEC on December 10, the company explained where this increase in credit revenue came from:

- Sky-high rates: “From the origination of our higher-yielding direct loan product, which resulted in an increase in the portfolio yield rate to 22.1% from 21.7%.

- And rising balances: “From a 3.2% increase in the average outstanding balance of the customer accounts receivable portfolio.”

“New customers have historically – and we’ve communicated that many times, and this isn’t a Conn’s phenomenon, this is a subprime phenomenon – they’ve defaulted twice the rate of existing customers,” said CEO Miller.

While the company “had the best credit performance in six years,” that is a “lagging indicator,” said CEO Miller.

The “leading indicators” are first-payment defaults and 60-day delinquencies, he said. “And we see that typically in 60 to 120 days from an underwriting standpoint.”

It’s the new customers, particularly those the company picked up via its website – “We’re getting an abundance of customers there,” he said – where the problems now are, not the established credit accounts.

“We start to see those vintages come in, we take action. And we do it regularly, but we saw more of a softening on the new side of the house, new web, especially,” he said. And “we have to be very prudent.”

He didn’t “think” it was a “macro” issue, because in a recession with unemployment rising, delinquencies among existing accounts would begin to rise. But it has been “fairly stable there,” he said. The issue is in new accounts.

But that’s where the growth is. Or rather, was. Since the company tightened credit due to the first-payment defaults and delinquency issues by new accounts – the leading indicators – retail sales have taken a hit, despite the steamy expansion of stores.

So the previous sales growth came from taking on the riskiest customers that stretched the most to get there, and once underwriting becomes more prudent, sales decline? This is a broader phenomenon in the current economy, including in subprime auto sales.

In the 10-Q, Conn’s explains how this business works – and this is not for the faint of heart:

We provide in-house financing to individual consumers on a short- and medium-term basis (contractual terms generally range from 12 to 36 months) for the purchase of durable products for the home. A significant portion of our customer credit portfolio is due from customers that are considered higher-risk, subprime borrowers.

Our financing is executed using contracts that require fixed monthly payments over fixed terms. We maintain a secured interest in the product financed. If a payment is delayed, missed or paid only in part, the account becomes delinquent. Our collection personnel attempt to contact a customer once their account becomes delinquent.

Our loan contracts generally reflect an interest rate of between 18% and 36% … [depending on the state].

We offer qualified customers a 12-month no-interest option finance program. If the customer is delinquent in making a scheduled monthly payment or does not repay the principal in full by the end of the no-interest option program period (grace periods are provided), the account does not qualify for the no-interest provision and none of the interest earned is waived [so all of the waived interest suddenly becomes due].

We regularly extend or “re-age” a portion of our delinquent customer accounts as a part of our normal collection procedures to protect our investment. Generally, extensions are granted to customers who have experienced a financial difficulty (such as the temporary loss of employment), which is subsequently resolved, and when the customer indicates a willingness and ability to resume making monthly payments. These re-ages involve modifying the payment terms to defer a portion of the cash payments currently required of the debtor to help the debtor improve his or her financial condition and eventually be able to pay the account balance… [re-aged loans are then no longer considered delinquent].

Re-ages are not granted to debtors who demonstrate a lack of intent or ability to service the obligation or have reached our limits for account re-aging.

To a much lesser extent, we may provide the customer the ability to re-age their obligation by refinancing the account, which typically does not change the interest rate or the total principal amount due from the customer but does reduce the monthly contractual payments and extends the term.

These are the good times, but why are subprime credit cards, auto loans, and short-term installment loans blowing out? Read… What’s Behind the Subprime Consumer Loan Implosion?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

They should just adjust their business model like the banks have done, to offer their customers loans with negative real interest rates. Then if a customer can’t pay their existing loan, they can just sell them a new loan and use the interest the customer earns from that to pay off the previous loan. The unlimited revenue potential from this business model will push their stock value towards infinity.

Isn’t that the way it all works now?

Great idea This should end well ( sarc off) Debt saturation has obviously been reached

@Jon W: I am copying pasting your comment for posterity, it is such a GEM. Love it. This is exactly how QE led to the everythign bubble, and in that light, negative rates are insane! (BTW, Willem Buiter’s (Financial Times) opinion of US likely NOT doing negative rates: “So only a zero policy rate would be constitutional — Islamic banking US style”).

These elites sure have cheek!

The ’12 month no-interest option’ sounds an awful lot like those ‘Trigger Bonds’ that blew up on Orange County back in the day.

One wonder if they are holding onto this crap or repackaging it and selling it off to future road-kill investors ‘looking for yield’. Or they were intending to ‘financialising it’, but the market for dodgy bonds is getting tighter and now they are sitting on more and more of it.

“… repackaging it and selling it off to future road-kill investors ‘looking for yield’.”

Yes, they’re repacking some of these loans into subprime-backed structured securities (ABS) and sell them to investors. Demand is insatiable for this stuff.

The TBTF Club in not that big.

And you ain’t in it.

“Its shares plunged 33% after it reported earnings, on issues that included credit deterioration among its subprime customers. Suddenly rising 60-plus-day delinquencies and first-payment defaults, where not even the first payment is made, caused the company to become “prudent” and “tighten credit,” which caused same-store sales to drop 8.5%.”

The solution is obvious:

The Fed should expand it’s Repo operations to include Conn’s credit applicants.

It could be called the Repo TV QE4 Operation.

Why should only the rich benefit from the Fed’s repo’s?

Let’s make it The People’s Fed.

OLED – Operation Liquidity at Extreme Discount

How about ..

FOILED – ‘Fed Oligarchic Incompetence whilst Ludicrously Enabling Destruction’

Touche!

Next time you exercise your “freedom”, be sure and choose wisely the Private Bankers that you vote for to govern you at the Fed.

Not participating in our democracy , by not voting, is not a wise choice.

And it ain’t even Christmas yet. Imagine what happens after Xmas. More will probably join the club.

I didn’t know you didn’t know, you’ve

got Overlords, sheeple.

Everything is fine today; that is our illusion. Neistche

People don’t want the truth, because they don’t want their illusions destroyed. Voltaire

The most helplessly enslaved; are the ones that think they are free. Wolfgang Von Goethe

Nietsche but hey were sheeple so we can’t be expected to spell very well can we Overlords yeah whatever I just live my simple little life and try to enjoy as much as possible along the way The rest doesn’t really matter all that much now does it Got GOLD ?

Reverend Johnson:

Order, order. Goddamnit I said “order”.

Howard Johnson:

Y’know, Nietzsche says: “Out of chaos comes order.”

Olson Johnson:

Oh, blow it out your ass, Howard.

” ‘Scuse me while I whip this out. ”

That’s why I love it here: highbrow and lowbrow can coexist.

An old schooler, Descates -famous for his deductive reasoning quote- “I think therfore I am” sits at the bar having a few drinks. The bartender asks “Would you like another one Rene”, Descates replied

“I think not” and vanquished into thin air.

An infinite number of mathematicians walk into a bar.

The first orders one beer.

The second orders half a beer.

The third orders 1/4 a beer.

The next orders 1/8 a beer.

And so forth.

The bartender looks up and says “You fellas should know your limits.”

And places two beers on the bar.

Oh well, I found your two jokes to be laughers.

I don’t understand why cable and other media companies don’t just give TV sets to their customers. A TV is useless now without some media service so they should be like the telephone used to be. You ordered telephone service and AT&T brought you a phone

There’s still old fashioned Over The Air (OTA) TV with an antenna. Quite useful if you live in a city with lots of local stations. And, if you’re out in the boonies, but have internet there and access to a location in a city with lots of TV channels, you can hook the antenna to an AirTV box that will stream those local stations to your TV out in the boonies via Amazon Firestick.

This is a one time purchase of a TV antenna ($30-80), AirTV box (roughly $100), and a Firestick (about $40) plus cables and other accessories (a laptop cooling fan really helps – the AirTV boxes tend to overheat and freeze up)

My understanding is that some of the TVs that are sold centered around a platform (Roku, etc) are partially subsidized by the app vendors. The app vendors pay to be on the TV, lowering the purchase cost for the end user.

No one needs to finance a tv.

Walmart will sell you a new 32″ flat screen TV for $79. This is a TV with a picture quality people in the 1990’s dreamed of some day being able to afford.

I Call it – New Business “WE WATCH” free tv, internet and device for watching endless ads, with a bit of crap – o enter-train-ment thrown in…

First round A finance – I want 4 Billion…

Watching TV gets on my nerves after a while. Too many commercials. Too many juvenile programs. I threw mine out. Radio is much better in my opinion. Still too many commercials except on public radio, but at least they are not visual.

Hah! I killed my tv 27 years ago when I had to choose between diaper service and cable :-)

I went TV free in ’93. Though the internet can be every bit a time waster as Television…

Reminds me of this story. (My niece and nephews know that Uncle Brian is kind of weird) So a few years ago my sister and brother in law came out to visit. I’d moved into a brand new house, and there was a huge empty space above the gas fire place insert for a flat screen TV. When my two nephews walked into the house and saw the big empty space on the wall they both stopped and their jaws dropped… “Uncle Brian you don’t have a TV!” Silence… “what do you do?”

Uh all kinds of stuff. Ride my bike, play ham radio, make bike bags, go outside. Cook food. Work programming computers. Do stuff with friends. Build/fly kites.

The astonished looks were priceless.

You make a good point about television becoming obsolete. Most kids now are using a smart phone while still in their strollers. And the fake news is not worth watching either. Conn’s market is shrinking.

Conn gotta Love the name Speaks volumnes doesn’t it?

I have been in one of their stores and it was not in the high rent district. The people that shop with them probably have no other options for buying home goods.

Managed by Dewey, Cheatham, and Howe?

You beat me to it… yes, that name, and that it’s a sub-prime/rent-to-own racket…

Who says the Gods, cruel though they are, don’t also have a sense of humor?

Your right Petunia .. however, All those youngins will be sufferin from teensy screen induced blindness by the time they reach our age …

Go long canes !

‘;]

You should join the rest of the world and watch commercial free mindless entertainment on Netflix.

We have sub prime in household goods and autos? We have collateralized leveraged loans so businesses can eat each other up or sell products at a loss? Where else do we have dumb loans to support losing ideas? Oh and loans on bubblishous stock prices for housing down payments and more stock buying.

And the point of sub prime is?

Just to see how deep we can dig the hole before it all caves in on us? All sounds like magical thinking to me. Or a belief that there really is life at the center of the earth.

not much deeper. The point of subprime is to keep the economy rolling along in a deflationary mode without having to raise real wages. Despite (allegedly) approaching full employment, wages remain more or less stagnant or even declining for 80% of people and the debt swells, so the only way people can keep consuming (and the economy can keep growing) relies upon granting credit to broke consumers. This kind of thing is why left-wing and right-wing populism is on the rise, the system is clearly broken but the powers that be insist that things are great and that there is no excess inflation – my own frustrated aims for home ownership are evidence enough of that. Eventually you won’t be able to service the consumer debt and the whole over-leveraged system will come crashing down.

Q: how do you steal from people who have nothing?

A: lend them some money

Gets on my nerves after about five minutes Sure wish they would produce good sitcoms like Seinfeld and Taxi like in the early 80s While were at it could we bring back the great music from the 60s to 80s thanks

There has been enough media content already produced to last any baby born today until the day they die. We don’t really need any more. I personally wouldn’t care if they never made another movie, TV show, or even song. There is a lifetime of stuff I have never even listened to yet.

Not saying that’s what should or will be done, if other people are hungry for new content, then great. Just saying that whatever happens to disrupt the entertainment industry doesn’t matter to me one iota.

Content is a real issue. Remember the dance craze during the 60s? The dances were different, and had different names. Then one day it was over. People still go to nightclubs and dance, but the content aspect has disappeared. Disco was probably the final nail. Netflix originals seems to be an over the top effort in an industry with changing tastes, and a rising (smart phone) small device market. I said to my writer friend, you have to learn to write novels that people will read in Kindle, or similar devices. To that end audio books which you can listen to on the bus, and block outside noise. These changes make content a challenging market.

it’s so much more effective than government brainwashing in schools, due to the huge amount of time people spend behind the screen (whether TV, smartphone or whatever). I’m sure a lot of parties are hungry for new and even more effective brainwashing content ;(

who cares about Conn’s this is not a bellwhether of anything. just a crappy retailer having trouble. anyone who shorts the market based on this, just write me a check, it will go to better use.

Stock market: To Infinity And Beyond!

Me: right

It’s a clip joint . If you ain’t got the basics of living nailed down first, you don’t need a 400 in tv at 1000% interest(slightly overstated for dramatic effect) . I built all my beds and repaired old furniture and small appliances for 10years while in and after college in order to get a “grub steak” in life . I Did all my auto maintanance also. I have un-informed idiots tell me that that was the “good old days ” when cars were “simple to fix”. I am here to tell you that if I would have been armed with a Wall-Mart OBD coupled with the internet during those 10 years my situation would have been greatly improved. If you were too lazy then to learn about such things as coils,points,plugs,condenser ,rotary button and mechanical timing advance then , you are still too lazy to learn the equivalent of function and control today using micro controllers.Electronic Fuel injection systems with OBD vs a Holly 4bbl or a dog Rochester, gimme the EFI baby. If these clip joints all go out of business ,good riddance.

Amen to that sentiment Dr Faber

Changed the spark plugs on my 2010 Honda Accord a year ago. No more coils, condensers, mechanical timing thru a distributor, or high voltage spark plug wires. Each cylinder had its own solid state high voltage generator thingy, fed by low voltage wires. The instructions for how to change the plugs were posted on the Internet

It was all impressively better and easier than the Olde Days

Well sure .. until a, uh, ‘vital’ computer chip (or several ..) goes all janky on you as you find yourself stuck in the boonies !

I wish to god they would open source the software on my stock Clarion head unit in my Subaru. I could write much better software for it than the crap they made. It would be fun actually. Too bad it will never happen.

Anybody want a dwell meter and timing light…free?

Haha, I remember those timing lights. What a pain

I remember when the 1985 Ferrari Quattrovalvo came out …. and a fellow resident bought one (I guess he had rich parents).

Oooooh FOUR VALVES per cylinder! I remember the guy explaining how you get more horsepower that way in that Ferrari. Something I later read was common to all high performance warbird aircraft engines during WWII, but not the norm for ordinary cars then

4-valve DOHC is the norm these days.

Recently saw an article about how a modern Honda Accord V6 (which Honda has sadly discontinued) could out accelerate a long list of 1980-1990 super cars – Ferraris, Lamborghinis, Porsches, including that Quattrovalvo

And of course a Tesla Model S can out accelerate them all

Points, coils, condensers, and carburetors are a pain! Anyone who has had to work with them loves electronic fuel injection and electronic ignition!

I do all the plumbing, electrical work, and carpentry at my house and I do most of the work on my cars..

Another recession tripwire. The profile of the “newly” subprime raises the issue, being primarily online customers. The poor you always have with you are not the problem, its the “nouveau” poore who are defaulting. Can Jerome keep main streets problems away from Wall St., where they have franchised out the old pawn shop, leveraged and sliced and diced and buried that paper in pension fund portfolios next to those 100yr Argentina bonds? In 2007 subprime was nominally much higher, (though if you add up student, mortgage, etc) this time around we are more highly leveraged. Cutting off new credit is the first sign of trouble.

Ambrose, couldn’t disagree with you more. Conn’s has screwed up their sleazy business model before (2014, 2015). No recession ensued.

This time they changed their business model to go after subprime customers online, and it should be no surprise that they got a lot of new customers who wouldn’t pay their outrageous scam rates.

Seems to me that without face-to-face contact, Conn’s doesn’t know who they can profitably rip off.

LOL …. a Subprime retailer named “Conn’s”. Yeah, we already knew it was a giant con.

So many questions.

Who are these subprime borrowers that cannot save some money and pay cash for a TV? Are things that bad our there?

Why is allowable to charge unsophisticated people a 36% predatory interest rate in some states?

Are outfits like this getting repo cash from the Fed?

Interestingly, I was at Goodwill the other day to check things out. I noticed they had lots of working 32 inch and larger screen working LCD televisions for $20, and many had HDMI capability. Isn’t that type of package preferable to a new $500 LED TV with 36% interest rate? Perhaps many of these subprime borrowers have high-end tastes. I shiver to think they may be buying iPhones and $80 jeans as well.

My wife bought a Samsung phone here in Turkey for around 275 dollars Apple would have been over a grand just common sense No showing off for us Been there done that Poor people often have poor common sense right? It’s a human failing If you have nothing you want something to show off that you’re not a total failure I suppose And the poverty continues

But unlike Apple, the new Samsung phone doesn’t have punctuation keys.

I kid, I kid.

…that’s why it is easier to be born without a leg or arm than to lose one; you don’t miss what you never had.

With that logic, it follows that things would be best if you were never born.

I just bought 2 used HF radios for $200/per. Excellent condition vrs a new radio list price of $1300. In other words, $2600 worth of radios for $400. Another $100 bought two antenna tuners and a pile of coax cable, also new. I saved $2500 buying used. The cable was free because the guy was so happy we bought his gear. Then, he threw in an antenna just to make us smile.

Oh yeah, cash private sale so no Provincial or Fed taxes, saving an additional 13%. My buddy is a retired Marconi technician with about 40 years work experience. He did the tests and provided a thumbs up. I’ll build him some furniture some time as a return favour. These days everything is instant gratification, well seasoned with confusion over needs vrs wants. Buying used is a wonderful experience as far as I am concerned. Financed electronics? Really?

Bye for the day; heading out to my pub/shop where the radios are. Last week I talked with a guy from the Bay Area. Maybe he’ll be around? Or maybe they’ll be someone on the northern trapper/bush net? So much to do, so much to learn, no time to buy….or was that no buy on time? hmm.

73

To quote a blogger I read – craigslist is a place where people store stuff for you until you need it. :)

Used HF gear: The prices you are seeing are way better than what I am seeing in the PDX metro area. I wanted an SDR radio to replace my ~35year old IC-730, so upgraded to an new IC -7300 last year. Can’t complain!

Great quote about Craigslist!

Used to if you didn’t pay your bills you couldn’t get ANY credit. Now they make a business model out of selling to customers with a 500 credit score. I’m surprised it’s not legal yet to send ‘The Boys’ around to collect or get some body parts broken. The 12 months-no interest is probably the best scam going along with payday loans.

It is legal The police or the Sheriff do the breaking from what I’ve heard in many cases

For-profit debtor’s prisons, anyone?

Sounds like Innovation to me!

Smart TV’s may bring income by collecting data about user preferences. This lowered. sales prices.

ANYTHING that’s labeled ‘Smart’ should avoid at all costs.

Seriously .. the Internet of Sh!t can’t be flushed fast enough !

One possibility in the nineties middle easterners would open up liquor stores fill them up with inventory and then disappear a week later. Could be a similar scam.

Yep, was thinking about all the meth heads that stay awake stealing identities and selling them to people that must use places like Conn to “abscrammay: with all the rentals and sell them for cash at 10% of their value.

LoL, just another Rent a Center finding da Poor’s is a bad inwestment, lol… All they need is some good old fashioned financial engineering to disguise the non-payment fraud, and extend past the put back, just like it used to be in 2005 when we sold homes to the homeless.

Same old same old

What a miracle of generalization. Well done.

Seems the snowflake here doesn’t like the truth much!

Not a bad business model for crooks hiding in the executive suites. Make bad loans to increase revenue fast and juice the stock. Sell stock at the top, then write off the bad loans. Repeat the play until the market crashes.

Interesting variation to the surge in shoplifting suggested by Home Depot today as factor in lower profits. For the “consumer” it comes down to much of the same though, or do they try to repo unpaid flatscreen TV’s in the US? I guess with the shoplifting the financial mob doesn’t profit so that sounds slightly better (but maybe they still do through insurance gimmicks etc?).

> [ surge in Home Depot shoplifting lowered profits ].

I’ve noticed that too, here in Seattle, big time.

I’m seeing crowds steal with impunity,

trespass with impunity, assault with impunity.

It’s a wonder anyone pays their mortgage anymore.

So long as oil is cheap,

anyone can do whatever, with impunity.

> do they try to repo unpaid flatscreen TV’s in the US?

Yes, but it doesn’t work;

they can’t get inside the house.

I’ve seen it with my own eyes;

it felt like a twilight zone episode.

Comedy Central’s “South Side” depicts it.

Same story in Europe, shoplifting is basically free now especially for certain “stigmatized” groups. Which means the other (paying) customers are charged for it by raising prices.

There also is a strong increase in debt forgiveness over here pushed by the left, for people with debts older than 3-4 years. Is was already very easy to get out of mortgage debt, but now it’s basically for almost everything (e.g. debts due to social security fraud, tax cheating, CC bills). Said otherwise: you are stupid to be honest and pay your bills…

I guess the repo problem is similar over here. I heard some interesting details about problems with lease contracts for gas boilers that often run for very long times. Officially the device is property of the energy company and they could grab the unit from your a home if the lease is no longer paid (e.g. when the owner sells the home without paying the penalty for early termination of the boiler lease). Here too the problem is that they are not allowed to go into the house and dismantle the boiler (plus that could introduce some serious liability). Probably one reason that these lease contracts are so expensive relative to outright ownership.

I wonder if having like 5 bankruptcies and being able to go for a 6th is affecting the market. Thestar is doing a series, with titles like these I wonder why we have a bank and credit rating agencies anymore.

He filed for his fifth bankruptcy with $20K in credit card debt. He still got a new credit card

One family, eight bankruptcies, millions owed

He was a titan of Bay Street and a senator. But J. Trevor Eyton died owing millions in taxes and on the verge of bankruptcy

Does anybody know if Conns sends out folks to repossess the TV’s and appliances when the buyer doesn’t pay?

What would they do with a used TV?

Sell it at a discounted 16-34% interest of course

Credit used to be premised upon the ability to repay what was borrowed.

It seems to me that the entire concept of credit has become completely debased in the past two decades.

Before a person had to have a track record of creditworthiness. A record of savings for example was needed before applying for a mortgage

It seems that none of this applies anywhere today.

That was before the FED printed money for nothing. Loans used to represent savings, and if the loan defaulted the savings disappeared.

Today loans are just a keystroke, and when defaults get too bad, the Fed simply creates more money with a keystroke to replenish the coffers of the lenders. Isn’t virtuality a wonderful thing?

Paul, maybe it’s just the logical (okay, my logic) result of massively expanding consumer credit availability having the effect of popping thick smoke over the massive stagnation of real wages in the U.S. since 1980?

May we all find a better day.

I Call it – New Business “WE WATCH” free tv, internet and device for watching endless ads, with a bit of crap – o enter-train-ment thrown in…

First round A finance – I want 4 Billion…

Sub Prime is the canary in the coal mine. When sub prime begins to default, it is the beginning of the next recession, or possibly depression in this instance….