But rents surge in 22 other markets by the double-digits.

Southern California – sampled here by Los Angeles, San Diego, Santa Ana, and Long Beach – has decidedly entered the list of big and expense rental markets where apartment rents are on the decline. Other decliners from their prior peak rent, in some cases years ago, include San Francisco, San Jose, Seattle, New York City, Chicago, Honolulu, and Miami. In terms of two-bedroom asking rents, seven of these cities booked double-digit declines from their prior peak, including -26% in Honolulu and -33% in Chicago.

In Southern California, the median asking rent – half of the advertised asking rents are higher, and half are lower – fell broadly. In Los Angeles, 1-BR rents fell 5.3% from their peak in October 2018 to $2,300; and 2-BR rents ticked down 1.5% from their peak in June 2018. In San Diego, the median 1-BR asking rent ($1,830) fell 6.2% from its peak in December 2018; and the median 2-BR rent ($2,380) fell 5.6% from the peak in October last year.

In Santa Ana (Orange County), the median 1-BR rent ($1,920) plunged 15.6% from the peak in September 2018, and 2-BR rents dropped nearly 10%. In Long Beach 1-BR rents fell 3.7% from the peak in June 2018 and 2-BR rents dropped 9.1%.

San Francisco, in terms of major cities, is the most expensive rental market in the US though there are three zip codes in Manhattan and two in Los Angeles that are more expensive than the most expensive zip code in San Francisco (Rents in the USA: from the Priciest ZIP Codes to the Cheapest).

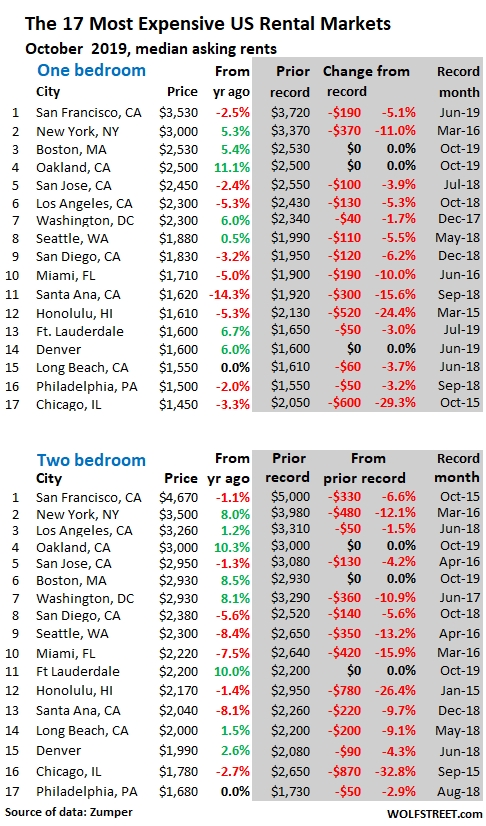

San Francisco rents had peaked in October 2015 and then fell almost 10% before the “Trump bump” infused new energy into housing in the Bay Area. This caused rents to rise again, with 1-BR rents beating by a hair the Oct. 2018 high, and 2-BR rents getting close, but no cigar. In June this year, this energy petered out.

In October, the median asking rent for 1-BR apartments, at $3,530, fell 2.5% from a year ago and 5.1% from the new record in June 2019 ($3,720), which itself had been just $50 above the old record of October 2015 ($3,670). In other words, in October 2019, the median 1-BR asking rent was 3.8% below where it had been in October 2015.

The median 2-BR asking rent, at $4,670 fell 1.1% from a year ago and was down 6.6% from the record in October 2015.

In San Francisco, as in many cities in the US, there is a lot of supply of newly or recently built rental units – rental apartments and condos for rent – but it’s nearly all high-end. And as landlord are trying to fill these units, they’re pressuring rents from the top down.

Seattle, after years of ballooning rents, is feeling the pressures from the building boom that has thrown a lot of high-end supply on the market. The median asking rent for a 1-BR, at $1,880 is about flat with a year ago and is down 5.5% from the peak in May 2018. The median 2-BR rent fell 8.4% from a year ago to $2,300, which is down 13.2% from the peak in April 2016.

In Chicago, where the housing market is facing the structural challenges of a slowly declining population and plenty of new construction, the median asking rent for 1-BR apartments, at $1,450, has plunged 29.3% from its peak in October 2015; and for 2-BR apartments, at $1,780, it has collapsed by 32.8% from the peak in September 2015.

In Miami, rents have come under pressure from a high-end building boom of condos that are now appearing on the rental market. This high-end condo market in Miami is slithering into serious trouble. The median asking rent for 1-BR apartments, at $1,710 was down 10% from the peak in June 2016; and the 2-BR rent, at $2,220, was down 15.9% from the peak in March 2016.

In Honolulu, rents are still trying to find a bottom, after spiraling lower for over four years. The median asking rent for a 1-BR fell 5.3% from a year ago to $1,610, and 24.4% from the peak in March 2015; the median 2-BR rent fell 1.4% from a year ago to $2,170, and is down 26.4% from the peak in January 2015.

In New York City, asking rents had peaked in March 2016, fell sharply, and then bounced but remain down from their peaks. The median asking rent for 1-BR apartments rose 5% from a year ago, but was still down 11% from March 2016. The 2-BR rent rose 8% year-over-year but was still down 12% from March 2016.

In the table below of the 17 most expensive major rental markets in the US by median asking rents, the shaded areas indicate peak rents and the changes since then. Note that three cities – Boston, Oakland, and Fort Lauderdale – set new highs in October:

The data is collected by Zumper from over 1 million active listings, including third-party listings at Multiple Listings Service (MLS), of apartments-for-rent in apartment buildings, including new construction, but not single-family houses or condos for rent, in the 100 largest markets. Rents do not include incentives, such as “one month free” or “free parking for three months.”

“Asking rent” is the amount the landlord advertises in the listing. It’s a measure of the current market for people who are looking to rent. It is not a measure of the rents that long-time tenants actually pay. “Median” means half the advertised rents are higher, and half are lower. Rooms, efficiency apartments, and apartments with three or more bedrooms are excluded.

The Cities with the biggest percentage rent increases:

Of the most expensive cities in the table above, Oakland had the biggest year-over-year rent increases: 11.1% for 1-BR apartments and 10.3% for 2-BR apartments. In dollar terms, those were the largest increases in the US, amounting to $250 a month for 1-BR rents and $280 a month for 2-BR rents.

Boston also had sharp rent increases and set new records. Other cities in the table above –including Fort Lauderdale, Washington DC, and New York – had sharp increases but the latter two remain down from their peaks years ago.

Below is a table of the 25 rental markets of the 100 major rental markets that in October had the biggest year-over-year percentage increases in median asking rents for 1-BR apartments. Of these 25 markets, 22 experienced double-digit rent increases (if your smartphone clips the sixth column, hold your device in landscape position):

| The 25 Cities with Biggest % Increases in 1-BR Rents | |||||

| City | 1-BR Rent | Y/Y % | 2-BR Rent | Y/Y % | |

| 1 | Indianapolis, IN | $800 | 15.9% | $910 | 9.6% |

| 2 | Chattanooga, TN | $900 | 15.4% | $1,030 | 15.7% |

| 3 | Cincinnati, OH | $900 | 15.4% | $1,290 | 15.2% |

| 4 | Norfolk, VA | $900 | 15.4% | $940 | 1.1% |

| 5 | Gilbert, AZ | $1,250 | 14.7% | $1,480 | 8.0% |

| 6 | Rochester, NY | $940 | 14.6% | $1,090 | 11.2% |

| 6 | Glendale, AZ | $870 | 14.5% | $1,060 | 12.8% |

| 8 | Newark, NJ | $1,280 | 14.3% | $1,580 | 15.3% |

| 9 | Detroit, MI | $660 | 13.8% | $780 | 14.7% |

| 10 | Cleveland, OH | $930 | 13.4% | $1,000 | 14.9% |

| 11 | Memphis, TN | $850 | 13.3% | $890 | 11.3% |

| 12 | Milwaukee, WI | $1,120 | 13.1% | $1,170 | 9.3% |

| 13 | Lincoln, NE | $780 | 13.0% | $950 | -2.1% |

| 14 | Akron, OH | $620 | 12.7% | $700 | 0.0% |

| 14 | Arlington, TX | $900 | 12.5% | $1,110 | 3.7% |

| 16 | Reno, NV | $1,000 | 12.4% | $1,300 | 3.2% |

| 17 | Columbus, OH | $820 | 12.3% | $1,080 | 0.9% |

| 18 | Tallahassee, FL | $820 | 12.3% | $900 | 3.4% |

| 19 | Wichita, KS | $670 | 11.7% | $760 | 0.0% |

| 20 | Oakland, CA | $2,500 | 11.1% | $3,000 | 10.3% |

| 21 | Chesapeake, VA | $1,140 | 10.7% | $1,240 | 3.3% |

| 22 | St Louis, MO | $840 | 10.5% | $1,110 | 4.7% |

| 23 | Chandler, AZ | $1,230 | 9.8% | $1,390 | 5.3% |

| 24 | Portland, OR | $1,470 | 8.9% | $1,750 | 6.7% |

| 25 | Virginia Beach, VA | $1,110 | 8.8% | $1,230 | 2.5% |

The Cities with the biggest percent rent decreases.

As we have seen in the most expensive rental markets, rents go up and they go down. The table below shows the 26 rental markets among the 100 major rental markets that in October had year-over-year decreases in median asking rents for 1-BR apartments. Four of them had double-digit drops, including Houston (if your smartphone clips the sixth column, hold your device in landscape position):

| The Cities with the Largest % Decreases in 1-BR Rents | |||||

| City | 1-BR Rent | Y/Y % | 2-BR Rent | Y/Y % | |

| 1 | Baltimore, MD | $1,110 | -15.9% | $1,400 | -10.8% |

| 2 | Santa Ana, CA | $1,620 | -14.3% | $2,040 | -8.1% |

| 3 | Jacksonville, FL | $900 | -10.9% | $1,060 | -3.6% |

| 4 | Houston, TX | $1,080 | -10.0% | $1,300 | -12.8% |

| 5 | Laredo, TX | $790 | -9.2% | $950 | -3.1% |

| 6 | Minneapolis, MN | $1,310 | -6.4% | $1,790 | -8.2% |

| 6 | Los Angeles, CA | $2,300 | -5.3% | $3,260 | 1.2% |

| 8 | Honolulu, HI | $1,610 | -5.3% | $2,170 | -1.4% |

| 9 | Lexington, KY | $710 | -5.3% | $950 | 0.0% |

| 10 | Miami, FL | $1,710 | -5.0% | $2,220 | -7.5% |

| 11 | Des Moines, IA | $780 | -4.9% | $900 | -3.2% |

| 12 | Dallas, TX | $1,200 | -4.8% | $1,620 | -4.1% |

| 13 | Aurora, CO | $1,100 | -4.3% | $1,400 | 0.0% |

| 14 | Baton Rouge, LA | $800 | -3.6% | $890 | -4.3% |

| 14 | Durham, NC | $1,100 | -3.5% | $1,230 | 0.0% |

| 16 | Atlanta, GA | $1,430 | -3.4% | $1,810 | 0.0% |

| 17 | Chicago, IL | $1,450 | -3.3% | $1,780 | -3.8% |

| 18 | San Diego, CA | $1,830 | -3.2% | $2,380 | -5.6% |

| 19 | Orlando, FL | $1,240 | -3.1% | $1,390 | -6.1% |

| 20 | San Francisco, CA | $3,530 | -2.5% | $4,670 | -1.1% |

| 21 | San Jose, CA | $2,450 | -2.4% | $2,950 | -1.3% |

| 22 | Philadelphia, PA | $1,500 | -2.0% | $1,680 | 0.0% |

| 23 | Anaheim, CA | $1,660 | -1.8% | $2,060 | -3.7% |

| 24 | Madison, WI | $1,260 | -1.6% | $1,330 | -11.3% |

| 25 | Fresno, CA | $950 | -1.0% | $1,150 | 3.6% |

| 26 | Tampa, FL | $1,140 | -0.9% | $1,340 | -0.7% |

Yup, of the 100 largest rental markets, 26 had declining rents. But 74 had rising rents or stable rents, and so overall, on average, rents in the US have increased year-over-year. According to Zumper’s National Rent Report, the median asking rent for 1-BR apartments across the US in October rose 2.5% to $1,237 and for for 2-BR apartments, it rose 2.6% to $1,480.

Below is Zumper’s list of the top 100 most expensive major rental markets, in order of 1-BR asking rents in October, with year-over-year percent changes. As you can see at the bottom of the list, median rents in the $700 range exist in the US, in some nice cities too. You can use your browser’s search function to find a city (if your smartphone clips the sixth column, hold your device in landscape position):

| City | 1-BR Rent | Y/Y % | 2-BR Rent | Y/Y % | |

| 1 | San Francisco, CA | $3,530 | -2.5% | $4,670 | -1.1% |

| 2 | New York, NY | $3,000 | 5.3% | $3,500 | 8.0% |

| 3 | Boston, MA | $2,530 | 5.4% | $2,930 | 8.5% |

| 4 | Oakland, CA | $2,500 | 11.1% | $3,000 | 10.3% |

| 5 | San Jose, CA | $2,450 | -2.4% | $2,950 | -1.3% |

| 6 | Los Angeles, CA | $2,300 | -5.3% | $3,260 | 1.2% |

| 6 | Washington, DC | $2,300 | 6.0% | $2,930 | 8.1% |

| 8 | Seattle, WA | $1,880 | 0.5% | $2,300 | -8.4% |

| 9 | San Diego, CA | $1,830 | -3.2% | $2,380 | -5.6% |

| 10 | Miami, FL | $1,710 | -5.0% | $2,220 | -7.5% |

| 11 | Anaheim, CA | $1,660 | -1.8% | $2,060 | -3.7% |

| 12 | Santa Ana, CA | $1,620 | -14.3% | $2,040 | -8.1% |

| 13 | Honolulu, HI | $1,610 | -5.3% | $2,170 | -1.4% |

| 14 | Denver, CO | $1,600 | 6.0% | $1,990 | 2.6% |

| 14 | Fort Lauderdale, FL | $1,600 | 6.7% | $2,200 | 10.0% |

| 16 | Long Beach, CA | $1,550 | 0.0% | $2,000 | 1.5% |

| 17 | Philadelphia, PA | $1,500 | -2.0% | $1,680 | 0.0% |

| 18 | Providence, RI | $1,480 | 0.0% | $1,700 | 3.7% |

| 19 | Portland, OR | $1,470 | 8.9% | $1,750 | 6.7% |

| 20 | Chicago, IL | $1,450 | -3.3% | $1,780 | -3.8% |

| 21 | Atlanta, GA | $1,430 | -3.4% | $1,810 | 0.0% |

| 22 | Scottsdale, AZ | $1,410 | 7.6% | $1,980 | 1.0% |

| 23 | New Orleans, LA | $1,400 | 6.9% | $1,550 | 6.9% |

| 24 | Nashville, TN | $1,350 | 1.5% | $1,400 | 0.0% |

| 25 | Minneapolis, MN | $1,310 | -6.4% | $1,790 | -8.2% |

| 26 | Sacramento, CA | $1,300 | 0.0% | $1,500 | 3.4% |

| 27 | Newark, NJ | $1,280 | 14.3% | $1,580 | 15.3% |

| 28 | Austin, TX | $1,260 | 4.1% | $1,570 | 3.3% |

| 28 | Madison, WI | $1,260 | -1.6% | $1,330 | -11.3% |

| 30 | Gilbert, AZ | $1,250 | 14.7% | $1,480 | 8.0% |

| 31 | Orlando, FL | $1,240 | -3.1% | $1,390 | -6.1% |

| 32 | Chandler, AZ | $1,230 | 9.8% | $1,390 | 5.3% |

| 33 | Charlotte, NC | $1,220 | 5.2% | $1,300 | 0.0% |

| 34 | Pittsburgh, PA | $1,210 | 3.4% | $1,330 | -2.9% |

| 35 | Dallas, TX | $1,200 | -4.8% | $1,620 | -4.1% |

| 36 | Plano, TX | $1,190 | 3.5% | $1,600 | 4.6% |

| 37 | Buffalo, NY | $1,140 | 8.6% | $1,370 | 7.0% |

| 37 | Chesapeake, VA | $1,140 | 10.7% | $1,240 | 3.3% |

| 37 | Tampa, FL | $1,140 | -0.9% | $1,340 | -0.7% |

| 40 | Henderson, NV | $1,130 | 6.6% | $1,330 | 5.6% |

| 41 | Irving, TX | $1,120 | 0.9% | $1,430 | 2.9% |

| 41 | Milwaukee, WI | $1,120 | 13.1% | $1,170 | 9.3% |

| 43 | Baltimore, MD | $1,110 | -15.9% | $1,400 | -10.8% |

| 43 | Virginia Beach, VA | $1,110 | 8.8% | $1,230 | 2.5% |

| 45 | Aurora, CO | $1,100 | -4.3% | $1,400 | 0.0% |

| 45 | Durham, NC | $1,100 | -3.5% | $1,230 | 0.0% |

| 45 | Fort Worth, TX | $1,100 | 5.8% | $1,290 | 1.6% |

| 45 | St Petersburg, FL | $1,100 | 5.8% | $1,450 | -1.4% |

| 49 | Salt Lake City, UT | $1,090 | 5.8% | $1,340 | -7.6% |

| 50 | Houston, TX | $1,080 | -10.0% | $1,300 | -12.8% |

| 51 | Richmond, VA | $1,070 | 0.0% | $1,310 | 4.8% |

| 52 | Raleigh, NC | $1,020 | 2.0% | $1,190 | 1.7% |

| 53 | Phoenix, AZ | $1,010 | 6.3% | $1,250 | 4.2% |

| 54 | Reno, NV | $1,000 | 12.4% | $1,300 | 3.2% |

| 55 | Colorado Springs, CO | $990 | 8.8% | $1,210 | 11.0% |

| 56 | Boise, ID | $980 | 2.1% | $1,200 | 15.4% |

| 57 | Fresno, CA | $950 | -1.0% | $1,150 | 3.6% |

| 57 | Kansas City, MO | $950 | 2.2% | $1,070 | 0.0% |

| 59 | Rochester, NY | $940 | 14.6% | $1,090 | 11.2% |

| 60 | Cleveland, OH | $930 | 13.4% | $1,000 | 14.9% |

| 60 | Las Vegas, NV | $930 | 1.1% | $1,190 | 6.3% |

| 62 | Mesa, AZ | $910 | 5.8% | $1,180 | 14.6% |

| 63 | Anchorage, AK | $900 | 0.0% | $1,150 | 0.0% |

| 63 | Arlington, TX | $900 | 12.5% | $1,110 | 3.7% |

| 63 | Chattanooga, TN | $900 | 15.4% | $1,030 | 15.7% |

| 63 | Cincinnati, OH | $900 | 15.4% | $1,290 | 15.2% |

| 63 | Corpus Christi, TX | $900 | 0.0% | $1,100 | 1.9% |

| 63 | Jacksonville, FL | $900 | -10.9% | $1,060 | -3.6% |

| 63 | Louisville, KY | $900 | 2.3% | $970 | -4.9% |

| 63 | Norfolk, VA | $900 | 15.4% | $940 | 1.1% |

| 71 | San Antonio, TX | $890 | 2.3% | $1,110 | 0.9% |

| 71 | Syracuse, NY | $890 | 7.2% | $1,000 | 4.2% |

| 73 | Glendale, AZ | $870 | 14.5% | $1,060 | 12.8% |

| 74 | Memphis, TN | $850 | 13.3% | $890 | 11.3% |

| 75 | St Louis, MO | $840 | 10.5% | $1,110 | 4.7% |

| 76 | Knoxville, TN | $830 | 6.4% | $950 | 4.4% |

| 76 | Winston Salem, NC | $830 | 7.8% | $870 | 3.6% |

| 78 | Columbus, OH | $820 | 12.3% | $1,080 | 0.9% |

| 78 | Tallahassee, FL | $820 | 12.3% | $900 | 3.4% |

| 80 | Baton Rouge, LA | $800 | -3.6% | $890 | -4.3% |

| 80 | Indianapolis, IN | $800 | 15.9% | $910 | 9.6% |

| 80 | Omaha, NE | $800 | 0.0% | $1,000 | -3.8% |

| 80 | Spokane, WA | $800 | 6.7% | $1,000 | 6.4% |

| 84 | Laredo, TX | $790 | -9.2% | $950 | -3.1% |

| 85 | Des Moines, IA | $780 | -4.9% | $900 | -3.2% |

| 85 | Lincoln, NE | $780 | 13.0% | $950 | -2.1% |

| 87 | Augusta, GA | $770 | 8.5% | $850 | 4.9% |

| 87 | Bakersfield, CA | $770 | 8.5% | $900 | 0.0% |

| 89 | Oklahoma City, OK | $750 | 5.6% | $910 | 5.8% |

| 90 | Greensboro, NC | $730 | 2.8% | $850 | 3.7% |

| 91 | Lexington, KY | $710 | -5.3% | $950 | 0.0% |

| 92 | Albuquerque, NM | $700 | 6.1% | $830 | 0.0% |

| 93 | Tulsa, OK | $680 | 7.9% | $830 | 6.4% |

| 94 | Tucson, AZ | $670 | 4.7% | $880 | 7.3% |

| 94 | Wichita, KS | $670 | 11.7% | $760 | 0.0% |

| 96 | Detroit, MI | $660 | 13.8% | $780 | 14.7% |

| 97 | El Paso, TX | $650 | 1.6% | $780 | 1.3% |

| 98 | Shreveport, LA | $640 | 1.6% | $700 | 0.0% |

| 99 | Lubbock, TX | $630 | 0.0% | $750 | -2.6% |

| 100 | Akron, OH | $620 | 12.7% | $700 | 0.0% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m not surprised to see Rochester, NY on the list of 25 Cities with Biggest % Increases or 59th on the Top 100 Most Expensive Major Rental Markets. The rent increases can be easily tied to the criminals at Morgan Communities buying up of massive amounts of multi-unit housing in Rochester and surrounding areas. For the last three years they’ve been buying properties at an alarming rate, even those not for sale. Then, with no value added to the properties, they jack up rents by $300 or more each month. As well as nickel-and-dime tenants by charging for what used to be included like sewer, water, trash, cable, etc in addition to charging a fee for the utilities bill service even though it’s their company doing the billing. Morgan Communities transferred ownership to Morgan Properties in PA thanks to all the indictments, but the management company is still the same so nothing has changed.

GenXer: I was under the impression from friends who live in Rochester that housing prices have not gone up much in recent years compared to many other places. Your comment on rents surprises me but not the corruption in NY! I see another billionaire just left NYC!

WES, it’s all relative. Prices are definitely up, though not as crazy as the West coast. Houses that should be priced at $160-170K at most are priced, and sold, at $210K or even higher. That might not seem like a lot compared to other areas but here, where the median income is $30K, that’s huge. Rents have jumped anywhere from $300-400 more per month everywhere, but most especially the properties Morgan bought up, with no value added to them.

GenXer, these rapacious oligarchs forget that The People’s vote still counts: the one that’s done with the feet.

I rent 1 bedrooms for $475 in Tucson

2 bedroom nicely done – $800

but hey thanks for pricing power

it’s been while since we’ve been able to raise rents

now I do it annually – just because

“Another” left for WHERE, Wes? What else do you “see” lately?

Credit Suisse Wealth Management shows over half the people in the world worth over $50M (about 75,000) live in the US. And that’s just reported wealth.

This ultra rich people leaving if they are taxed more in any way is BS propaganda. Sure, lower level wealthy might play state jumping games, but they stay in the US.

It much easier just to hide wealth, remain, and enjoy the taxpayer funded safety, security, family, friends and familiar culture/laws right here, (not to mention the ability to “help” write our laws) and the vast majority DO.

I thought he was talking about Trump changing residency to FL. The “billionaire” description threw me a bit too. Maybe he meant to add huge Austin Power’s Dr Evil air quotation marks….”billionaire”. (It’s possible I’m projecting since he referenced corruption and leaving NY.)

Either way, I agree wholeheartedly with your analysis. We sure have spent a lot of years handling the uber-wealthy with kid gloves. Not sure what we have to show for that.

WES, I just spoke with someone yesterday who bought their house a few years ago for $120K in one of the nice surrounding suburbs. They were looking at possibly selling, until they decided they couldn’t afford to buy a house at the prices they are. Comps for their house are listing for $180-190K right now, selling for $200K or more. Prices jumping 60% in a few years is not normal or sustainable in Rochester. Wages can’t support it.

For instance, UR is the largest employer here for the last couple decades. Over a decade ago, they employed 20K Rochesterians which is probably now closer to 30K with all the expanding and acquisitions in surrounding areas. The average wage is about $35-40K. However, raises are, at most, 2% per year. Even promotions are capped at 15% which results in internal candidates making a great deal less than their colleagues hired as external candidates. Insurance premiums also go up by 5-7% each year, and this year are going up by 25%, which eats into the measly 2% annual raises. Not to mention everything else here has gotten more expensive, like utilities and food.

Rochester wages can’t support these house prices. People in SoCal and more expensive areas don’t seem to understand.

Financial bubbles do not usually occur as the result of normal market forces, but by the pursuit of monopolistic practices by predators who grab a market, hold it upside down, and flog it to shake the money out.

I ran into that latter game 2006-8. It was a bill separate from rent, monthly, and went to a P/O box (forget the strange name). Anyway, it was “for” water, garbage, gas and elect “hookup” and some other similar and strange charges. At first it varied between $40-60/mo, and then got up close to $100, so it was not nickel and dime. They later demanded everyone had renter insurance which they would add to rent for$25/mo, (to you save shopping time).

I had heard their were class action lawsuits against this practice but they were defeated. Fairly large complex in Santa Rosa, CA.

NBay, it’s much more than nickel and dime, you’re right. The utilities bill does run about $40-60 per month right now. It’ll suck if/when it gets up to $100. And yes, they also require renters insurance which is about $200 per year, but we had that anyway. It’s like that at all properties owned by Morgan. Because Morgan bought up so many properties in and around Rochester, it’s difficult to find one that isn’t owned by them. Since we’re still so far grandfathered in under market rent, we’ll still stay where we are. Unless/until they charge us the rent new tenants are paying. Then we’ll look into buying a house. For now, renting is way cheaper than anything we’d spend on a house with the prices they are here.

My daughter was presented with a lease renewal that included a 7% rent increase. Downtown Denver studio 1.5 year old property. I suggested she counteroffer a 2% increase. It was accepted. Lots of new development coming online there that is mostly luxury.

USA: Home of the fleeced, Land of the debt slave.

Welcome to the Corporate Shakedown economy. It may also be helpful to think of it as a great olive press, for squeezing money out of humans.

or Urban Dictionary: wytai

A hipster term for something that is not really complex but is made to sound complicated for the sake of making it seem very intricate regardless of how mundane and dull it actually is.

The Fed put 60B in the Repo market so that banks would lend to each other. They don’t call it a gift using taxpayers money. Totally wytai…

I’d call that absurd and grotesque, AB. State-sanctioned larceny also fits. TBTFs aren’t getting ‘help’. They’re helping themselves, and taxpayers are on the hook for it.

Ambrose-

I’m a big fan of Bucky Fuller, and he wrote that a Rockefeller friend of his once told him, “Why make business simple when you can make it complicated?”.

He also wrote a short essay on the history of corporations following a challenge from the same guy. I HIGHLY recommend it. It begins with sailing ships and exploration, and the shareholders and organizers wanted to be immune from upset families when their loved ones were lost (or trashed on the job) at sea, for any reason, while trying to make a few richer.

A business where no involved “businessmen” were responsible for ANY consequences of their decisions or actions slowly developed.

The greatest wealth extracting system in the world was born.

Ft. Lauderdale has been supplanting Miami as the coolest place in south FL for the last few years. All the overpriced empty condos have finally caught up with Miami. People actually live in Ft. Lauderdale and the young cool/artsy factor is definitely up.

Petunia,

It seems your comments are sent to my moderation queue by my AI-driven anti-spam system as of today. I have no idea why. The system also looks at how your comments are routed — for example, if they go though a server along the way that is known to be a spam server. This happens to a lot of people here. Someday it will likely go back to normal. So please be patient.

Maybe it’s a fat loudmouth housewife tracking device, your tax dollars at work. Or my social score is worse than I thought.

LOL

Throw in a pro China line from time to time to keep your score above water.

for what it’s worth, it happens to me a lot, too. and i just thought i was being provocative ;-)

OUCH!

“We have always viewed Softbank as an investor driven Ponzi scheme, but we suspect our readers already knew that. ”

https://www.zerohedge.com/markets/repo-madness-rest-story

Rent’s coming back to earth? No jobs, Unicorns dying?

Biggest fear of ‘elite’ is populism, next elections could/should flip to socialism ( huge tax increases ), funny thing is the election’s will be driven by fed-up, huge debt millenials, who are the very ‘pushers’ of the Unicorn.

Corporate USA is already dead, so why not put property-taxes on holding stock, the entire market plummets, easy-corporate money evaporates, more layoffs. All these over-price apartments become shooting gallerys and whorehouses.

Go figure how they’ll justify taxing the hell out of geriatrics that hold ‘AAA’ rock-solid company stocks.

Rents always go up. Every year.

Mortgage payments stay the same for 10, 15, 20 or 30 years.

Just Some Random Guy,

“Rents always go up. Every year.” Do yourself a favor and check the data in the article. AT LEAST read the title. Then look at the Chicago rents which are down 30% from the peak in 2015, and Honolulu rents (down similarly), and at some of the other markets, such as Houston where rents are down by the double digits from a year ago. There is a whole list of cities in the article with declining rents.

Fine rents go up at least once every 2 years. How’s that? The point is long term rents go up. Medium term, up. Shorter term in the vast majority of cases, also up. I’d love to see an example of an actual apartment in Chicago that is 30% cheaper now than in 2015.

The last apartment I rented was $1600/mo in 2003. An apartment in that building right now goes for $2900. This was on the east coast. Nice building, nice location, but by no means anything luxury. In between 2003 and now, I’m sure there were years with negative increases. Big deal. It’s long term that matters, not year to year noise.

And now compare someone in 2003 (like say me) deciding whether to rent or to buy. Would renter me or buyer me have come out better 16 years later?

I personally experienced declining rents that lasted decades. It was slow but continued. I moved from Texas back to Tulsa, OK, in about 1986. I rented a new 1-BR with river view, something like $650. By the time I moved out into the condo I’d bought from a bank (developer had gone bankrupt), my rent had dropped to around $450. Then it dropped further. In 2001, when I moved from Tulsa to the East Coast, the 1-BR in that complex were being advertised in the upper 300s. Somewhere along the line since then rents started rising again. Today, the median 1-BR asking rent in Tulsa, on the list above, is $680. So about where I started in 1986.

House prices in Tulsa went through similar dynamics. There are many cities like that (see the bottom 20 or so cities on the list above). In real estate, it’s all about location, location, location (but you knew that).

BTW, Tulsa is not some hell-hole. It’s a nice hilly city with lots of trees on the Arkansas River near big lakes and within driving distance of skiing in Colorado — you start driving after work and go skiing the next afternoon… we used to do it in our younger years :-]

JSRG, yeah, the mortgage stays the same, but, maybe the neighborHOOD doesn’t… if you know what I mean.

A bit rough but the pluses and minuses could serve to show where the Fed’s reflation efforts are succeeding/failing.

Lots of new supply in central LA. I would expect rents to continue to decrease in the near future just from the supply increase alone.

HOA fees are rising. They took out a loan for over a million dollars to redo the golf course as the irrigation system was antiquated and there were too many weeds. The country club restaurant is also losing money. Residents ate at home.

One gated condo association does background checks before property sales can be approved.

In the apartments they will be doing evictions. They put the tenants’ belongings on the curb and changed the locks while a police officer watched. Landlords asked to see paycheck stubs and did credit checks before approving leases.

Some apartments are over occupied.

The homeless shelters are full.

So rent just went up in many places but money market rates just went down making it more difficult for savers to pay these rents.

Consider the Fed’s buying $60b of T bills a month and their subsequent rollover. After the 2016 SEC money market reform, mostly all money market funds are in government securities (in short term up to one year or less).

The Fed’s purchases have been mostly 52 week bills and 26 week bills. Recently they bought even shorter 8 and 13 week bills.

If the Fed buys this much, then what bills will the money market hold. The yield is lowered and will continue to drop. Poor people. Rents are increasing but income from savings are getting wiped out. Thanks to the Fed.

A community must be inhabitable to charge people rent. I’m noticing the LA area is becoming uninhabitable for a variety of reasons. Item: Highway 101 closed for 10 hours due to a man threatening to jump from an overpass. Item. ‘Easy’ fire in Ventura sourced to Edison electric equipment. That the Kincade fire in Sonoma is also being blamed on PG&E suggests the utilities will have to expand the power cuts during wind events.

Evacuations, power shut offs, closed highways, unsafe air to breathe, constant wildfire outbreaks, homeless population spreading disease. This is very negative to the quality of life and property values

Unit 472 –

But the 405 Freeway was reopened that day…though many of the off-ramps were closed. You can get on the freeway, you just cannot leave! Yes, the weather is awesome but the trend is clear. Intermittent power availability, pot holes that break your car, laughably high fees and fines, etc., and a trip to the DMV is like purgatory. The biggest issue will be water availability and that just assumes taxes will continue upward while quality of services downward. I needed a tax rate & direct assessments for a property in LA County… I was on hold for 30 minutes and the first person couldn’t figure out how to help me and she dumped me back on hold… 20 mins later I was helped. Good thing, it was 4:50pm; they close at 5pm and are closed on Fridays. One hour of my life I will never get back I have a number of friends who have bugged-out.. Montana, WA, Colorado, WY and NV… My guess is the Prop 13 Repeal will be based on many issues, but mostly water storage and availability. Rents in Reno are 44% less than LA and no State taxes… do the math

Spent most of my childhood thru early 30’s in LA (SF valley and Miracle Mile) and it’s getting worse on just about every fronts except for much better air quality compared to the 70’s. Many of the once decent hoods became 3rd world Latin America and traffic is getting worse in a city designed for driving with even the surface streets getting clogged in the west side. SF Bay area is much better place to be and can’t wait to move to no tax NV or back to WA when my youngest graduates.

I95 into Miami is a nightmare commute too. Every week there would be horrific accidents, cop chases and shoot outs where the traffic was stopped for hours. Don’t miss that, it’s easier to fly into Miami than drive into Miami.

re: “… homeless population spreading disease'”

Affluent anti-vaxxers are doing their part.

The rent decline trend should continue. There is a sea of new high density construction from San Jose to Fremont.

Yep, same with Dublin/Pleasanton area, just acres and acres of new townhouses coming online.

Oakland (and even Alameda) has lots of the condo/townhouses under construction.

Wish there was more along ECR in San Mateo/Burlingame/Millbrae, hopefully someday.

It’s slowly making a difference.

We are moving into apartment next month and had looking for awhile now. The “deals” have started, lots of “$500 off first month” and reduced deposits. We watched a 4bd 2bath house in Alamada sit “for rent” at $4k/month all summer, then was finally reduced to $3,800 in Sept and again to $3,600/month and was just taken off the listing two days ago. The property manager told us it was an investment property and the owners were holding out for $4k when went to the open house. So it sat empty for at least 5 months this year.

Seeing lots of reductions and it’s great that Trulia and Zillow keep track of rental listing. We can see how long it’s been empty and see the price reductions.

The cracks in the dam are starting to leak.

We were lowkey looking to buy this summer (decided to sign another 2yr lease) so I have a bunch of bookmarked houses/condos on my zillow. I am noticing a ton of them are now being put up to rent. Either they weren’t sold and so placed to rent. Or they were sold and then quickly put to rent. I think so many people in CA assume RE = quick buck and want a piece of easy money.

I’m also seeing tons of reductions for rentals and I know the condo across the street from us has sat on the rental market since June. The owner told us he is offering reduced rent for a longer lease, so his “list” price doesn’t even reflect this.

Supply is probably catching up with the demand in the SF Bay area.

There has been a lot of buildings of new apartments thru out the SF Bay area and suspect more are on the way given how long it takes to get various approvals to developing new flat projects.

No, the supply is almost exclusively super expensive.

As in $6000 to $8000 for a 2 BD/2 BA.

I live in Scottsdale AZ which is basically a resort town. Rents are insane and continue to rise because of lack of supply. Investors continue to build huge new luxury apartments as the older buildings empty out and offer better deals to the less qualified renter as well as the riff raff which seems to be changing the face of Scottsdale. Another problem is all the vacation rental properties which used to be available for a resident, but now has become an air b n b rental. Investors are actually securing 3 year leases on properties here and furnishing them as vacation rentals to be used as air b n b. Seems like the vacation rental business is the new industry here. Im certainly not against business or investing, but this is really going to end badly.

I think there is a lot of noise with the numbers in some of the smaller cities which are dominated by universities and the educational industrial complex scam.

A mega landlord REIT was just saying they are buying in the senior and student housing markets, especially from Florida through Texas.

Nice to see rent is falling, can’t wait for the glut of “luxury” homes to come to the market to put more pressure on rent in the near future.

People making duplexes and triplexes out of these places would make an interesting reality show….quite challenging.

Most new low rise apartments in Portland have empty new retail on ground level.

The recession put on old yet again.

August’s 168,000 number was revised up to 219,000. September number up from 136,000 to 180,000.”

No biggie right. Just an extra 95K jobs created the past 2 months that BLS – oopsie – forgot to mention.

It’s interesting how every jobs report for the last 6 months or so has been revised upwards. And of course 99% of the public doesn’t read about the revision, only the headline number. It’s almost as if the MSM/Deep State is actively trying to bring on a recession for 2020. But that’s crazy talk, I know.

At some point people will start asking where the hell is this recession that the news has been warning me about for the past year? You can fool most of the people sometime, you can fool some of the people most of the time. But you can’t fool all the people all the time.

Yes, exactly, as I pointed out a million times, this is “not a rate-cut economy.”

https://wolfstreet.com/tag/not-a-rate-cut-economy/

It’s a rate cut Fed. Is the explanation for that the heat the President subjected the Fed to, or did Powell lose control of the Fed or some other inside drama? Maybe hanging out with The Gang that benefits from low rates as I guess the Fedsters do just instilled group think.

Jobs numbers are great on the surface if you count only “job numbers” on a short term basis. I know, I had a triple leveraged long on the Rut today that went up 7.36% from yesterday’s low. I gambled the jobs numbers would be “great” today, as the media and algorithms only look at the headline numbers, and momentum does the rest.

Under the surface long term, remember that the 47,500 food service jobs created in today’s report pay 1/3 the amount of a manufacturing job ($389 food services, $1,198 manufacuring, per https://www.bloomberg.com/opinion/articles/2019-11-01/america-s-love-for-restaurants-keeps-creating-food-service-jobs )

Thus for every 10,000 jobs lost in manufacturing, it takes 30,000 in food services to equal the same amount of “personal income” flowing into the economy. Job “numbers” are great, but how much one gets paid matters greatly over time. Data can be massaged, yet people like Wolf do a great job at fishing the truth out of the numbers, as you can massage the data somewhat, yet it can’t be easily forged, at least not easily long term (unless you have a central controlled govt, like China).

Wolf,

My grand-daughter is an Attache’ to the UN for 3 years. The Government (taxpayer) is shelling out US$9999 a MONTH for a nice 2 plus study within walking distance to the UN building. Nice view of the Empire State she says.

That’s probably the UN price. Regular price might be about $5,000? Or maybe $6,000?

So how much does rent control legislation bothers these numbers?

Portland City Counsel has decided we should have “rent control” just like the big kids at the top of the Most Expensive list. And surprise, look which direction we’re heading, one year into it. Perhaps that has something to do with my friend’s wife buying a new apartment building here last week, and not in San Francisco where they live.

They have rent control in SF too? Now Ca will have it statewide. This certainly puts the bite on other than corporate landlords. (I suppose the gov is right, the public is on board, just like the gas tax, the rt wing will challenge it, spend a ton of (taxpayer) money and come up empty, again?) There are also proposed changes to prop 13 in Ca, but any significant drop in home values will offset those changes. I suspect if they did away with 13 altogether that values might fall in half and the assessors office would collect the same amount in taxes minus the panic in the mortgage market and the reverse mortgage HELOC lenders. Stability in housing prices is probably more important to the economy than volatility in stocks.

Read the Law (AB 1482) that has passed but not yet signed last time I checked. This is rent control watered down. 5% to 10% annual increases allowed, you can boot tenants with 1 month of rent as relocation compensation if upgrading requires permits, etc. Down the road, it will get more onerous but for now its not horrible except for properties with rents that are badly lagging market levels. Now think about it, if you get a building with really low actual rents, you can empty it out and upgrade which will actually reduce the supply of more relatively affordable units. I am NOT a proponent of rent control , but for the most part, the initial bite is not as bad as one would think IMO. If values decline 50% owners can appeal their property assessment.

The Prop. 13 challenge isn’t to abolish it, but rather to split roll.

Or in other words, no longer allow billion dollar companies and $10M houses by super-rich to be governed by the same policies as everyone else.

A really smart setup, but one which doesn’t solve the ultimate problem of too many properties with property taxes based on 1980s valuations.

I am presently living in a nearly new apartment complex near all the Intel campuses in Oregon. The complex is owned by a big national operation with similar complexes all over. The are geared to keeping the place full and constantly adjust the rent as well as offering 2 months free if needed. They also have a full time sign spinning guy down at the main intersection. But the vacancy rate is slowly but surely going up every month.

Was driving this morning when the local radio station news was bragging that Lakewood Ranch ( on the border between Manatee and Sarasota counties) had more single family housing starts for the second consecutive quarter than anywhere else in the US.

Yeah, summers are sweltering, but $300,000 will buy you a decent house and twice that would get you a mansion ( unless you want to live on the beach). Still average January high temperature is 72 degrees and fires are rare as are ( surprisingly ) hurricanes.

Wolf, what do you make about the quality of this data?

Zumper isn’t really a real estate powerhouse. They seem to specialize in large multi-family rentals. This could argue towards early signal and not noise. Corporate owned rentals aren’t going to sit vacant as their owners care about quarterly numbers. The mom & pop landlords may be slower to come off their asking rents.

Conversely, the big story in San Diego are the companies signing master leases on entire apartment buildings and leasing the units out as short term vacation rentals. This would skew at the higher end leaving the lower quality apartments for long term renters. This could very easily be distorting the rental data.

https://www.10news.com/news/local-news/san-diego-news/more-apartments-becoming-vacation-rentals

This data is not just based on Zumper’s listings, as I said in the article:

The data is collected by Zumper from over 1 million active listings, including third-party listings at Multiple Listings Service (MLS), of apartments-for-rent in apartment buildings, including new construction, but not single-family houses or condos for rent, in the 100 largest markets. Rents do not include incentives, such as “one month free” or “free parking for three months.”