“Don’t rely on Social Security”: Inflation adjustments are punitively low, and benefits become more inadequate as you age.

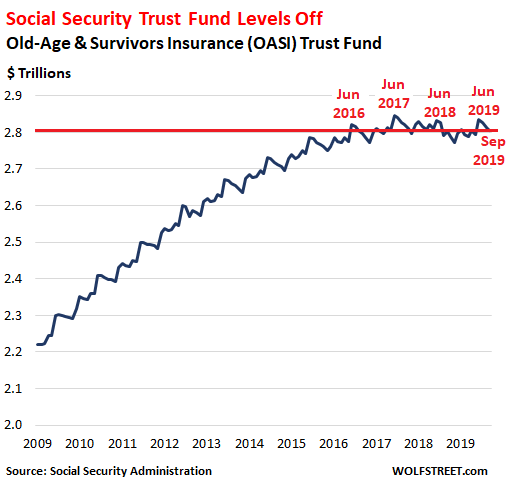

The Old-Age and Survivors Insurance (OASI) Trust Fund – which does not include the Disability Insurance (DI) Trust Fund – closed the fiscal year 2019 at the end of September with a balance of $2.80 trillion, according to figures released by the Social Security Administration. This balance was up by $3 billion from September last year, but was down $16 billion from September 2017.

The balance tends to hit annual peaks in June. The all-time peak was in June 2017, at $2.846 trillion. In June 2018, the balance was down by $13 billion. In June 2019, the balance, at $2.834 trillion, was up $1 billion from a year earlier, but was still down $12 billion from the peak in June 2017. You get the drift: 2017 was a record year, 2018 was an alarming down-year, and 2019 has reversed the down-trend, but not by much:

The Social Security Trust Fund is benefiting from the increase of workers – particularly millennials, the largest generation ever – and from rising wages that trigger higher Social Security deductions. And the date when the trust fund is depleted keeps getting moved out further, currently estimated to occur in 2034.

Depletion of the Trust Fund doesn’t mean that Social Security will collapse or whatever. It means either that workers will have to pay in a little more, or benefits will get cut, or a little of both. Social Security has been fixed before. Raising the maximum amount of earnings subject to Social Security tax would be one way of doing it.

Over 63 million retirees are drawing Social Security benefits (in addition, 8 million people are drawing SSI disability benefits).

Back when I was a senior in high school, the dad of my sweetheart told me that Social Security was a “scam” and that it wouldn’t be around for him to use when he’d retire. He was a CPA and had his own business, an accounting and tax firm. He ended up retiring and collecting Social Security, which was still around. And a few years ago, he passed away, and his wife began collecting survivor benefits. Social security, which has been around for 84 years, has outlived him, and it’s going to outlive me too.

But he gave me a piece of wise and correct advice – for the wrong reason: “Don’t rely on Social Security.” It’s tough to live off Social Security benefits, and it gets much tougher as you get older, as we’ll see in a moment.

Of the SS Trust Fund’s assets, almost all, $2.79 trillion, were invested in long-term US Treasury bonds at the end of September, with a weighted average maturity of 7.8 years. The remaining $12 billion (less than half of 1% of the total) were invested in short-term “certificates of indebtedness,” similar to Treasury bills.

US Treasury securities are considered among the most conservative assets. The fund’s investment in Treasuries is very similar to a bond fund’s or a regular pension fund’s investment in Treasuries. The funds receive interest payments and are paid face value by the Treasury Department when the security matures.

But there is one difference: Bond funds, pension funds, and other investors buy “marketable” Treasury securities that can be traded in the bond market. The SS Trust Fund buys nonmarketable Treasuries that cannot be traded, which has an advantage: Since they cannot be traded, their value doesn’t change on a daily basis. The Trust Fund accounts for them at face value, and face value is what the Trust Fund gets paid when the securities mature.

Fed’s interest rate repression crushed interest income.

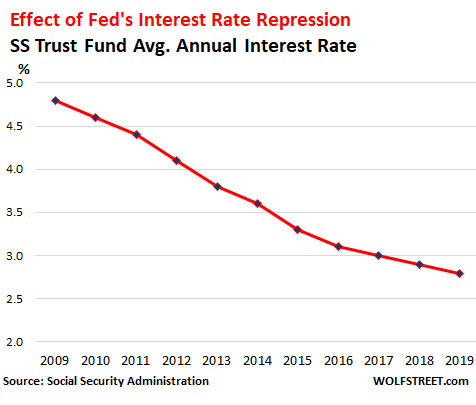

In September, the weighted average interest rate of the securities in the Trust Fund fell to 2.73%, the lowest in my lifetime. The average annual interest rate for each year has been declining relentlessly since 2009, dropping from 4.8% in 2009 to 2.8% in the fiscal year 2019:

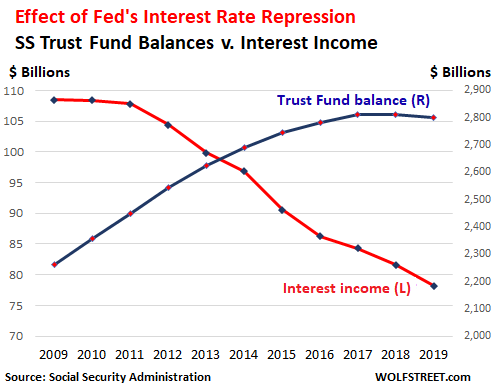

This means that despite rising balances in the SS Trust Fund, interest income has plunged. Trust Fund balances rose 24% from 2009 through 2019. But interest income fell 28% over the same period, from about $108 billion in 2009 to $78 billion in 2019. The chart below shows average weighted annual interest income (declining red line, left scale) versus Trust Fund balances (right column):

This decline of interest income speeds up the deterioration of the Trust Fund. At current Trust Fund levels, each decline of 1 percentage point of the average annual interest rate slashes the Fund’s interest income by $28 billion a year.

And interest income will fall further as securities that were acquired years ago at higher interest rates are replaced with securities bearing much lower interest rates.

Punitively low Cost of Living (COLA) adjustments.

Benefits in 2020 will increase by just 1.6% for the year, starting in January 2020, the Social Security Administration announced on Thursday.

Social Security benefits are adjusted for inflation based on the Bureau of Labor Statistics’ inflation measure for “urban wage earners and clerical workers” (CPI-W). The fundamental problem is that CPI does not measure changes in the costs of living — and “Cost of Living Adjustment” is really a misnomer. CPI only measures changes in prices of the same thing or service at the same quality over time. And when quality of goods (such as electronics or car) or services (such as housing) improves, the BLS removes the cost of these improvements form the index.

In other words, CPI only measures the loss of purchasing power of the dollar, and purposefully does not measure the costs of quality improvements.

This produces a situation where over the past 20 years, the CPI for new vehicles has been flat, even as actual retail prices have soared, as the cars have gotten a lot better, such as going from two air bags to 10 air bags, and from a 4-speed automatic transmission to an 8-speed automatic transmission, etc. Here is my detailed discussion on these “hedonic quality adjustments” for new vehicles and how they relate to CPI.

But it is impossible today to buy these products or services without the quality improvements, and therefore retirees have to pay more even if they don’t want those quality improvements.

The 1.6% increase in benefits doesn’t include the increases in prices due to quality improvements. It just compensates for the loss of purchasing power of the dollar (price changes of the same thing at the same quality). That’s one massive issue with the COLA adjustments.

Another massive issue with the COLA adjustments is that the basket of goods and services used by an elderly person is different from the goods and services used by the average urban worker. For example, the average elderly person has much greater healthcare needs than the average worker. And healthcare expenses have far outrun the Consumer Price Index.

The inadequate COLAs are transpiring every year, year-after-year, and they’re additive, and for retirees who’re dependent on Social Security, which is already tough to live on at the beginning, face a gradual and pernicious reduction of the standard of living they’re able to pay for.

This is why my high school sweetheart’s dad was right, but for the wrong reason, and yes, dear millennials, that’s for you: Don’t rely on Social Security, not because it won’t be there for you (it will be), but because the COLAs are purposefully insufficient once you draw benefits, and the benefits will become more and more inadequate as you age.

This scheme worked wonders for a while but has now run into trouble, and a lot is at stake. Read… How the SoftBank Scheme Rips Open the Startup Bubble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Depletion of the Trust Fund doesn’t mean that Social Security will collapse or whatever. It means either that workers will have to pay in a little more, or benefits will get cut, or a little of both…or the most obvious solution government will simply have to deficit spend like it does for all programs.

A lot of public pension plans in other countries work that way. There isn’t even a trust fund of any kind. It’s just “pay as you go.”

A lot of military budgets and illegal wars of aggression work that way too and yet we never hear a peep about the deficits they cause from the Deficit Fetishistas.

That’s right, move the defense dollars to SS or just print more money.

To hell with the dollar or anything else. That’s what I’ve learned from the financial industry, republicans, corporations, etc…

Pulling out Syria – about time

BRING 100% of our TROOPS back to U.S.

Line them up at SOUTHERN BORDER to protect merica 1st

endless $TRILLION warmongering only benefits MILITARY INDUSTRIAL COMPLEX

and OUR TROOPS PAY DEARLY – 1,000’s DEAD, 100,000’s INJURED FOR LIFE

MILITARY INDUSTRIAL COMPLEX = rich beyond dreams

In a large country, there is no other choice. Nearly all the goods and services produced each year are consumed each year. So if you throw out the money, and just look at the flow of goods and services, the workers are producing every year, and both the workers and the non-workers are consuming what they produce. The more non-workers there are, the less is available for the workers to consume. You can dress this up with numbers in accounts, but this is the reality of what is happening.

Thank you very much for your article, Wolf. It is a shame that the looming problems with social security are not considered. They can be fixed for a long time, e.g., with a property tax on the wealthiest 5% of Americans, who are holders of most of the wealth in the US. See https://www.brookings.edu/blog/up-front/2019/06/25/six-facts-about-wealth-in-the-united-states/

The readers should also note that pension funds are in the same position: their earnings have been minimal due to the “Federal” Reserve banking cartel benefiting its banks with ultra low interest rates, even when they have been insolvent, since 2008. I.e., US pensions will mostly not be able to meet their commitments or the expectations of their pensioners.

Thus, even relying on your pension may not be realistic. Talk about failing upwards: the control groups of the banks drove them into the ground and the “Federal” Reserve then indirectly transferred most Americans’ retirement savings to them.

CORRECTION of above comment: I meant to say “not considered by most publishers or news sources, except for Forbes and yourself, in this article.” Sorry and thank you very much for your excellent article.

Disagree on the property tax. Just eliminate the ceiling on the social security tax or increase it substantially. I think the max taxable income is $132,000 in 2019. The max tax, in my opinion for what’s its worth, is so rich people will not feel like they are having to subsidize the sullied masses who rely on SS because they perceive them as losers.

Unfortunately the GOP is bent on defunding SS.

As to comment about raising social security tax (which would fall most harmfully on the poorest Americans) or eliminating the income limit on that tax (which would increase the harm the working middle and upper class but NOT multi-millionaires or billionaires), I respectfully disagree. I can teach any multi-millionaires or billionaires how not to pay ANY such taxes, ever.

Just invest in stock of or buy companies that do not pay dividends and live on loans, for example. Thus, your proposed social security change would benefit those who have avoided paying taxes (other than property taxes) for many decades and collapse the consumption of the majority of Americans. It might cause a depression if those taxes were raised enough to cover total US federal and local liabilities of $124 to $210 trillion. A property tax would also serve unmask our shadow olygarchs, (less than 20,000) who rule the world by their vast wealth and many also by being organized crime’s true leaders.

What’s the old expression…”we are from the government and we are here to help you”.

I think that “old expression” was, “We are here from Corporate America and here to extract everything you have from you”.

Or, like Lincoln said, “Corporations have been enthroned, and all the wealth will be in the hands of a few”.

well LINCOLN should KNOW – he’s one who OBLITERATED STATES RIGHTS

now FINANCIAL CYCLES are getting so HUGE that when it hiccups whole world will explode

NOT QE is now here to tune of $60,000,000,000 a month

thank you federal reserve for screwing the pooch(ie 99%)

Really, your lamenting the fact that Lincoln eliminated the ability to own slaves?

Joe- Corporations crush most States like bugs. The Federal government costs them a lot more money to buy.

Lincoln did not create the “Federal” reserve banking cartel. Most Americans would have a substantial net worth were it not for their “help.”

Most loss of purchasing power and economic harm can be traced to such cartels but the Fed is the worst by orders of magnitude of harm. Their agents and members should be converted into a federal agency owned by taxpayers and indicted after wiretaps. Of course, if the AMA were outlawed too, we could easily bring in foreign doctors and nurses and only pay a pittance for healthcare compared to today’s prices. Those two cartels are like huge, parasitic tapeworms harming 99% of America’s population.

I wonder how many “already retirees ” and those nearing retirement are considering moving to a foreign country?

When I was in Ecuador about three years ago, I met a number of American retirees there and I’ve met many here in the Asian country I’ve moved to.

I’m one who is Building three houses with a pool on the SW Turkish Med coast with my Turkish bride Life is good without a mortgage , insurance or property taxes Just expensive gasoline is all Eating out and groceries I are much much cheaper here but I lived in Sag Harbor( Hamptons) before so just about anywhere would be cheaper Poland is great and inexpensive if you enjoy cold weather

Don’t laugh yet. I am a retiree on Medicare. I need it specifically after my stroke. Once I feel confident I can make it longer, I will find a place where we can go. I am no stranger to foreign countries and culture. I don’t depend on SSA income since I elected to postpone it. Not sure if I’m thinking straight.

Anyone with any smarts is looking at ways to get out. Countries with a national health service, and educated work force, and a coherent culture are the norm, not the exception that the US is.

Easy to fix, stop voting Republican. Americans never learn.

Easy to fix, stop voting Republican.

It’s more insidious than that. One must also stop voting for Republicans posing as Democrats.

Americans never learn.

Certainly they do. They have learned to love their chains.

Deficit spending is independent of a political party. All politicians find it very easy to spend other people’s money to buy votes to get re-elected. Show me a party who says it is time to do less with less spending.

Spot on, Wolf.

As a young 30 something financial services trainee in the early 80’s, we were taught the same “incorrect projection” about SS not being there when boomers would retire. It was leverage to sell annuities. Well, I have been collecting SS for over 5 years, and do not see a problem collecting during my lifetime.

I agree with you, congress will just tweak the system for the next few generations.

And it will be similar for other programs.

“Pay us now and we will take care of your basic healthcare for nominal cost”. Definition of “basic” and “nominal cost” will get tweaked as time goes by.

In the 1970s, my best friend’s father (who had a PhD in Econ from the U of Chicago) used to tell anyone who cared to listen that SS was primarily a political issue, not a financial/economic one. So as long as the politics required such a program to continue, it would continue.

However, over the last 40 years, I’ve seen a concerted effort to make the “will of the voters” matter less and less in politics.

The compensation for most Senators and Representatives is $174,000 per year. And though they contribute to SS like all workers, they are covered by the Federal Employees Retirement System. Their retirement will take good care of them so don’t expect yours to be improved any time soon. On the contrary, expect cuts and tax hikes on the benefits.

FERS has only been around for 30 years.

Those covered by Civil Service Retirement Plan do not contribute to SS.

The US Debt Clock.org shows Fed pensions cost $286 billion. Over a quarter the amount of Social Security. Wish we all could collect what we think we’re worth.

It is easy to boost the fiscal security of S.S. Just raise the income cap, which is currently around $120,000. This means that somone making $500,000 now pays S.S. tax on only $120,000 of that income. If the cap was raised to $250,000, S.S. would be financially stable for as far as the horizon can see. But this is a touchy subject in Congress, since the politicians don’t want to anger the 1% rich donor class. And the corporate media avoids talking about this obvious solution either – they only talk about benefit cuts and extending the retirement age even further out – it is currently at 67 years old. Only a tidal wave of public opinion can move the politicians to do the right thing: raise the cap.

The cap is 132,900, and it will be 137,700 in 2020. To me the cap should be eliminated, the government just spends the money anyways and though it is invested in treasuries it does not count for the deficit. For the wealthy individuals, they make most of their money through capital gains or loopholes that use capital gains taxation (carried interest loophole) and pay no SS at all. To me there should be one line on income tax, your income from all sources, and stop giving preference to income that does not come from labor.

It would not raise as much tax revenue as you think, since a large chunk of equities are held in IRA/401k accounts, which will already taxed at income tax rates. The total retirement assets nearly equals the stock US stock market capitalization, though a lot of retirement assets are in bonds.

Nope

https://www.nytimes.com/2018/02/08/business/economy/stocks-economy.html

“A whopping 84 percent of all stocks owned by Americans belong to the wealthiest 10 percent of households. And that includes everyone’s stakes in pension plans, 401(k)’s and individual retirement accounts, as well as trust funds, mutual funds and college savings programs like 529 plans.”

Yep, the rich get paid significantly through capital gains, and pay a lower percentage in taxes on it. A lot of middle class tax payers surely pay a larger percent of their income than many of the rich due to these tax policies including the ss cap. This is purely the doing of Republican politicians who reward the rich, and saddle everyone else with deficits. Somehow Republican voters never call out their party on this. When working class Republicans get yoked with the bill instead of the rich (cuz they are untouchable sacred cows in conservative land) they will still blame Democrats.

Lance Manly – I remember a saying about the stock market, to not play in it unless you can take $50,000 cash and put it in a little pile in your driveway and burn it.

So it would make sense that most of the stocks are held by people who have the money socked away and can afford to either burn it or ignore it.

My numbers come from the Federal Reserve. If you combine the Federal reserve estimate that all retirement account assets roughly equals the US market cap, with the NYT article that says 85% of equity is not in retirement accounts, that would mean almost all of retirement accounts are invested in bonds and international assets, which I don’t believe. Actually, I probably believe only 15% of what NYT says, so maybe it makes sense.

r>g……as the Frenchman said.

It’s primarily a corporate thingy.

Why should there be any social security tax at all. Just run larger and larger deficits and bond buyers will

buy more and more

The cap makes sense because the benefits are capped.

If you remove the cap then you you have to remove the benefits cap too (although granted the disbursement formula for dollars at those earnings rates is relatively low).

If you don’t remove the benefits cap but remove the earnings cap then SS becomes just like any other tax and you might as well just raise the regular income tax since at that point there really isn’t that much difference between the two taxes.

“Saving” social security isn’t really that hard. A moderate rise in the rate in combination a moderate rise in the cap and possibly a modest increase in the retirement age can extend the trust fund for decades to come.

The real problem is Medicare due to the ever-rising cost of medical care in the USA.

“The real problem is Medicare due to the ever-rising cost of medical care in the USA.”

Thats not a problem with medicare, its a problem with healthcare.

The real problem is Medicare due to the ever-rising cost of medical care in the USA.

It’s one part of the problem.

Half the problem is wage suppression, because worker compensation funds SS. Suppress worker compensation, suppress SS.

The other half is cost increases imposed on workers, medical costs being only one of them, but also other costs: housing, education, transportation, and so forth. These costs are not reflected in CPI, which is why your masters want people to focus on CPI, to persuade them that their costs are not increasing, and therefore no need for increased compensation.

It’s analogous to the pincer military strategy, conducted in the context of effective control of labor, consisting of a frontal attack – wage suppression – with a flank attack – cost increases. Capital wins both ways by decreasing their costs while increasing their gains. Labor is crushed in the pincers.

Victory is imminent. The plan is working.

The plan is working.

Benefits are not linear with taxes paid, particularly on the low end.

It is already a wealth transfer program, so eliminating the taxable income cap and not the benefits cap doesn’t change anything.

Why have a cap at all?

According to my calculations, removing the cap entirely would only increase the amount of money raised by 3%, because very few people have a salary higher than $132K.

1 in 10 taxpayers have income that exceeds the SS cap. Removing the cap would result in 88% of the gap being closed. You can play SS reformer in a game produced by American Academy of Actuaries http://socialsecuritygame.actuary.org/

Removing the cap is basically a tax increase on the middle class, which includes many people making $200k in the Northeast and California. The these people are already struggling and can’t afford another tax increase, (after the Trump tax increase).

@Lance – According to the official statistics from the SSA, only 5% of wages earned made more than $132K in 2017, the latest year for which statistics are available. The 99th percentile starts at about $260K, and the 99.9th percentile starts at starts at around $480K. Only .044% of workers had a salary higher than $1 million.

That’s why eliminated the cap wouldn’t raise much money.

I took early pension at 60 years.

Our politicians are so flakey that I have no idea new and improved polices that they will apply to the pension system or raise the age or crash the pensions…

Take what I can now so not regret it later.

30% penalty but at least I have something out of it.

When reductions in benefits are discussed. Would that include benefits currently being paid or only new enrollees?

It is automatic that if you want to apply for early pension in Canada, then it is at a 30% reduction for life. Small yearly increases for inflation are in it too. At 65, I can also receive the income supplement which is much more.

That’s exactly the same reduction in Social Security if you took it early vs. waiting for full retirement age. What is left out of the article is ever increasing tax on SS benefits by adding them to non SS income. It is increasing because the threshold for adding SS benefits in is not indexed to inflation at all, so what started as a tax on SS benefits that affected 1% now affects 40% of recipients, and that will keep increasing.

Joe : OAS is about 2/3 of the combined CPP & OAS these days with annual inflation adjustment.

Just don’t plan on becoming a Canadian Non- resident in order to live as an ex-pat……… OAS evaporates if you become a non-resident.

I thought about moving offshore to my old stomping grounds in Argentina when the peso took its nose dive ( not the first or last time I’ll bet.) Getting paid in CDN$ , converting to Arg peso I would have got one heck of a pay raise. The kicker there is the 50% annual inflation rate……. getting a 2% COLA on my CPP would have reduced my lifestyle to almost poverty level in a few short years. :(

It is quite easy to fix Social Security treat it as what it is: a Ponzi scheme

1) If you received benefits in the past 5 years those are retroactively taxed at 50%

2) All funds currently in the trust fund are divided based on a formula to private accounts with 3-4 investment choices eg stocks, bonds, gics . The apportionment should grant lower income individuals more than their contributions.

3) Put a 20-30% tax on contributions from incomes above $80k/year that is redistributed to the accounts of lower income earners.

Chris,

If Social Security is a “Ponzi scheme,” as you claim, ALL forms of insurance are a Ponzi scheme squared, including auto insurance and homeowner’s insurance, because policy holders pay into these systems, and their contributions are used to pay for the actual losses of others, and some policy holders may NEVER receive any benefits if they don’t have a claim. For example, some drivers with auto insurance or some insured homeowners may never see a dime in benefits if they’re lucky enough to not have a claim though they paid into the system for decades. That’s how insurance works.

Calling it insurance doesn’t make it insurance. Let me list some important differences.

Buying into SS is not optional. With insurance if premium is too high for the perceived benefit, there is the option of not buying it – earthquake insurance for example.

There is no competitor who sells SS. That’s a tell tale sign of a program that’s not sustainable. It can only continue to exist by government mandate and/or government subsidy.

Insurance covers risk events – accidents, loss of property, disability etc. Retirement is not a risk event. It is almost guaranteed to occur.

[P.S. nice article; thanks for bringing attention to this important matter]

Thank you GP. Id have opted out the SECOND I started working if that were an option.

I’m glad I moved to the Philippines where my social security helps me live a comfortable life with no need to work

Insurance companies usually invest ~5-30% of their premiums. As such they could make money (and do during some bull investment markets), even if they pay out a bit more in claims than they take in for premiums. Social Security cash/capital has earned about 3% in recent years- not too great.

The Social Security (and Medicare) actuarial basis has been a joke for a long time (since inception)- this is the unethical behavior that voters want- promise voters something they don’t have to pay for- future generations will pay for it (either by taxes, reduced benefits, whatever).

Social Security “will be there”, but might not be worth much.

wkevinw,

Social Security works a heck of a lot better than a lot of other insurance programs, including health insurance, and of course long-term care insurance, with carriers going out of business, leaving people high and dry. Private-sector insurance is a nasty business. A lot of times, you HAVE TO SUE to get your claim paid. Private-sector insurance works on the basis of collecting the most possible premiums and delaying payouts, or not paying at all, unless you sue. Ask the fire and flood victims!

I completely disagree. Medicare is actually a relatively well-run program. It’s a travesty that Americans under 65 cannot sign up for it. If it was available to me, I would sign up for it in a heartbeat.

American health insurance adds a middleman to healthcare making it more expensive, often substantially so. I spent the last year collating California hospital data. Medicare reimbursement rates are the lowest rates you can pay in California. Some hospitals accept the Medicare rates if you pay cash.

Insured patients in California usually pay more, much more. The average insurer discount is only 30% off, while Medicare reimbursement rates are 80-95% off hospital list prices. The data I collected is at http://www.ClinicPriceCheck.com.

Wolf- I now live in a flood area. I know all about the flood victims being able to (or not) to collect. As you may know, the flood insurance industry is heavily subsidized and manipulated by the government- where you and I pay for people to build in flood plains- they get flooded and we pay part of their claims.

Of course, the private long term care insurance was a disaster. However, in a way it shows the power of the free market- it drove a bunch of companies to bankruptcy. Private actuaries also make mistakes- difference? they can often pay for it.

Nothing you said addressed the fact that the Social Security long term future will have to be one of reduced benefits and/or increased costs- it already has been.

People want the government to give them something for nothing. There are lots of studies showing that the early Social Security beneficiaries made out great and the later ones will not do as well.

I stand by what I said- Social Security may not be worth as much as people hope.

Wolf, what you and the commenters failed to realize is that SS is not just a retirement system. It also pays out substantial sums to survivors and to senior spouses who may have contributed little or nothing based on their own earnings. A commercial insurance company would charge higher premiums to an individual who also wanted these extra benefits, which would be of no value to a single individual. It would also charge higher Medicare premiums to insurance applicants in poor health.

SS and its related programs create winners and losers.

Most defined benefits pension plans – if not all — have survivor benefits. This is standard for corporate or government plans. Or else, if hubby moves on to the happy hunting grounds, the window, who may never have had a job outside the house, would just end up with nothing and starve? Survivor benefits are one of the main functions of a pension plan.

One sees the financial stories almost daily advising how much one must save per year to have $1 million at retirement if you start saving at age 20, 30 etc. Of course the cap rate is X so even saving at the required rate may or may not get you there and does not take into account extraordinary or unforeseen events ( losing a major war, a depression, political upheaval etc.). One of which is likely to occur over a human lifetime.

The other assumption ( increasingly unlikely) is that you will have job each and every year and that it will pay close to the current median annual income in order to save the requisite amount. By definition half the working population will not make the median income and even if half will make more few will make more over the entirety of the working lives . Thus for most saving that $1 million ( which is sort of the minimum amount for a comfortable retirement) is just not going to be possible.

@unit472 Agree with your assessment. In addition to being a rat race worker who can never get ahead due to SS financial policymaker machinations, the overachieving saver/investor is also subject to the same machinations by the Fed and others affecting his/her stored wealth (currency manips etc). I have friends who just say to heck with it, will rely on eventual SS and Medicare with presumption the gubment will penalize some asset class or industry or the wealthy or whatever, to assure Joe Bag-o-Donuts can still have a house, a car, drugs and take a vacation every year.

Thinking of the 30% penalty…

The inflation on money then is a big incentive to pull it early too.

The inflation is far more than what the media publishes.

One sees the financial stories almost daily advising how much one must save per year to have $1 million at retirement if you start saving at age 20, 30 etc.

Which begs the question: how is one to save for retirement when you can’t even afford to move out of the basement because your overpriced college degrees only got you a crappy job that doesn’t even cover the monthly payments?

I’ve heard this from STEM postgraduates and fresh MBAs for so long it’s turned into background noise.

I can’t agree enough with this comment–the problem with a lot of what passes for personal finance advice is that it operates the assumption that you’re making 6 figures and not living in an ultra-high cost of living city (e.g. San Francisco).

While there are certainly people who make bad financial decisions, a lot of people are unable to save for retirement because of lack of income: i.e. the math is simply impossible.

Try living on $20,00-30,000 grand per year in any reasonable sized city and see how much you can save for retirement once costs of living and healthcare are part of the financial equation.

Ideas to improve the fiscal viability of social security administration and fund:

—————————————————————————————————

1) Allow a new lump sum option as a choice, which can be taken as a one time lump sum any time after a person retires. The lump sum amount could be calculated by social security administration based on proper models, and on when the retiree takes the lump sum. Many people may like it and opt for it . They may consider the choice especially helpful if they want to relocate to another country and settle there after retirement because it gives them freedom of choice. They could take the lump sum and decide to use and/or invest it as per their individual/family needs and circumstances.

2) STOP social security payments for anyone, above a certain level of verifable ASSETS/WEALTH (This level could be again determined by the administration to be 10 million or 20 million or 50 million dollars in total wealth). wealthy people don’t need social security by its very definition.

How on earth would you verify assets and wealth?

Would we have to hire the guys from Antiques Roadshow?

I always maxed out on SS wages after grad school till I retired. That’s decades friend. Are you suggesting I don’t get anything back considering I paid the max for almost all my commercial life? I thought SS witholding on wages were supposed to be a SAVINGS plan and not a tax which has no cap and is extra. Give me my money back.

&imafan

I’m confused

The maxing out

Is a boast Or financial competence

The believing in a trust is An acknowledgment of almost utter political ignorance

So

How should we all read u?

Your SS contribution is based on your income up to a certain point. That point is the maximum rate. I paid that for decades because I was highly paid employee. Later when I opened a company I paid myself a high salary for which SS contributions were also paid. I always paid a lot of taxes because that’s the right thing to do. I paid and earned my SS benefits.

https://www.ssa.gov/oact/cola/cbb.html

The maximum taxable amount for 2020 is $137,700.

I worked in New York City. That amount does not make you rich.

I remember it was in the 50’s in the eighties. So it’s easy to get to the max if you’re in a high priced area.

The greatest problem with all pay-as-you-go social retirement/aid programs is you eventually run out of Other People’s Money.

US Social Security will always be there. Unfortunately, in time, your entire check may only buy you one Big Mac and a large shake and fries.

Voting always produces increasing largess from the Treasury.

No amount of money can buy happiness. Enough money can rent it.

You don’t run out of other people’s money if they keep making more money. You may find it odd, but lot’s of people keep making money every year! Taking a small portion of that and giving it to the elderly and sick only makes people want to make more money, so they work even harder. The real world is a funny thing.

To imply most people will work harder so they can “give” more of their money to others is ridiculous. Can you cite any studies that indicate this phenomena? Whats your definition of “small portion”?

The more you tax something the less you get…

How can it be any other way? If I want to spend $75,000/year and the government taxes me so that I can only spend $70k, where’s the other $5k going to come from? I have to find a way to earn more. Obvious.

“The more you tax something the less you get…”

Absurd. The fastest growth in modern America’s history was in the ’50’s and ’60’s when it had the highest tax rates. And it’s obvious why: if you wanted to make more you had to invest more. Taxes are at some of their lowest rates in history and so is business investment.

Do people stop buying more expensive houses even though the taxes on the houses will be higher? Experience says no.

I hear one political party constantly talking about guaranteed incomes and income inequality, but not one of them talks about increasing social security payouts. They also don’t talk about eliminating the income taxes on social security benefits. We already paid income taxes on the money we put into the system.

My opinion is that the income level for paying into the system should be raised by a lot, may all income should be taxable. The rate should be lowered so low wage workers don’t carry a disproportionate burden. If you pay more, you should get more, but the floor should be higher to protect the working poor.

Actually, you didn’t pay taxes on the money your employer contributed on your behalf and the employer got a deduction for his contribution. So you should be paying taxes on the employer portion (i.e. 50%), but not on 85%.

1) 1M stocks account, paying 2.5%, will give u 25k annual dividends,

before taxes.

2) The average SS will click 25k to your bank account, every 2nd Wed,

even if its zero, instead of a million.

3) China most important export in the last 30Y is deflation.

4) The rising US dollar send WMT food prices down.

5) Energy glut reduce the cost of heating.

6) Recession empower those on SS.

==> 7) But one day, when we will be older, energy blowup will extract NR,

reduce the value of OASI Trust Fund and make SS payments worthless.

8) Younger generation will demand and get higher income, depend on their skills, but those on fix SS income will become poor.

Those who today _depend_ on SS income are already poor today.

If they stay in the US yes Go abroad and live without the stress life in the states involves That’s what I did and boy am I glad I did I also have some rental income and get 4% on some dollars and 15% on some Lira so all told I’m living pretty darn well In NY I was housepoor from the ridiculous property taxes and homeowners insurance

Expat life is hard to beat; converting USD to many other currencies means a cost of living 2-3 times cheaper when compared to the US…which means you can live like a king.

That’s the secret to a comfortable retirement. Go outside the US. It’s a big world. I know it’s scary to xenophobes who have never left their Zipcode, but there are many wonderful places to live in the world. You start by traveling before you retire. Don’t do the tourist bit, looking at all the spots on travel brochures. Stay at a small local hotel, explore around, meet the people, do what they do on a daily basis.

It’s easy to find a place where the US dollar buys 3X as much in lifestyle. Or more.

You don’t need a country where Social Security makes direct deposit. Find a bank that has branches in both the US and your retirement destination. Your SS and pensions go into the US branch, and you take it out of the ATM in your new home country. There are a number of apps like TransferWise that make moving money between countries cheap and easy. Explore that option.

Medicare does not cover you outside the US. In many countries you can get excellent health care at low cost, by paying cash. The cost out of your pocket is often the same as the deductibles with Medicare. I’m in China, but only one mile from a large hospital associated with a medical college. I don’t worry about health care.

A lot of places take a LOT of money to move to, but a lot of places will give you citizenship if you have roots like Italian, Irish, etc., or you may have connections of some type in some place where you can get out of the US. Maybe your wife is Filipino and there’s the family back there. Or you were in India with the Peace Corps and have connections there. And so on.

The US is an outlier in so many ways, the decreasing life expectancy, high costs of medical care and education, etc.

All the SS admin needs to do is to issue bonds. Then the FED can buy some of the bonds. Others will clamor to buy the bonds on the idea that the interest rate can only go down as the FED buys more of them, causing the value to go up, at which point they will dump them to some greater fool.

If you think this whole scheme for funding shakey lending and for manipulating value of actually worthless assets is too idiotic to have even bothered typing, you are right, I just made it up.

A couple of thoughts I have on social security:

1. Because of the way social security benefits are calculated and taxed I determined that by 50 I had probably already had obtained about 85% of my social security payout after tax and I wasn’t going to work another 16.5 years to get the remaining 15%.

2. Most calculations for when to take social security do not include mortality risk before starting to collect. If you consider this risk then the breakeven date is pushed out from claiming early is pushed out from roughly 80 to 90.

After giving it some thought I took social security at 62 to spend socialized money first and my savings as late as possible. I think I would feel vulnerable to spend through my assets by 70 and then depend on social security to send me a check.

With information age I anticipate that at sometime government will in addition to taxing income will tax wealth. I don’t think it would have been technically possible 20 years ago, but now no problem. Like E. Warren’s wealth tax on the rich, we all will have to list our assets maybe not to tax, but to determine we have enough and don’t need social security.

Final thought is on financial maneuvering by central planners. The central banks most likely did not improve the economy over the lady 10 years, but they did inflate assets so that if your time horizon is 20 years your expected future return will likely be near zero in real terms. Plan accordingly.

With information age I anticipate that at sometime government will in addition to taxing income will tax wealth. I don’t think it would have been technically possible 20 years ago

It’s been done in Western countries since the 19th century.

Confiscation of inordinate wealth has long been pursued, not only to provide employment for the poor but to prevent the rich from undermining the government. It’s why the Roman empire lasted so long. In the Athenian Empire the wealthy were subject to ‘liturgies’. You don’t suppose all those grand marble temples were paid for by taxes on the poor, do you?

The concept formed much of the basis of tax reform in the US in the 1930s and in Europe after WWII, and enabled the broad prosperity of Western nations after 1950 and the emergence of the modern middle class. Trolls who claim that “the more you tax something the less you get” are talking their greedy book and arguing against the experience of the history of economics: the US economy never had it so good as when the wealthy were taxed at 90% – and neither did the wealthy, for that matter, as that tax regime enabled the increase of their wealth by more than they were taxed.

Now that the practice has been ended and the rich can get rid of the middle class, crush the poor, and run governments to their profit, the end is in sight. Inordinate wealth is always – always – fatally destabilising.

You can watch it happen in real time.

Europe tried wealth taxes, and they failed. Piketty, as usual, said that there wasn’t enough of the taxing and said only a global wealth tax would work. Good luck with that.

https://www.npr.org/sections/money/2019/02/26/698057356/if-a-wealth-tax-is-such-a-good-idea-why-did-europe-kill-theirs

Europe tried wealth taxes, and they failed.

Europe succeeded with wealth taxes until your overlords succeeded in getting rid of them.

Success is never permanent. Failure usually is. Thermodynamics alone guarantees everything will eventually fail permanently.

This too will end It always does and with a lot of bloodshed unfortunately New Zealand won’t save them

Employment for employment’s sake doesn’t mean much. If it did I could cut your grass, wash your car and my wife could keep your kids and you could reciprocate and all four of us would be employeed. True wealth creation perhaps can be visualized be two employees driving a mile long train of goods that in the past would have taken 10,000 people to do. Its the 100 years of capital investment in the railroad that made this possible.

The reason the US economy prospered from 1950 to 1970 is because all of Europe and Asia was a smoking ruin. There was literally no economic competition for US heavy industry until well into the 60s.

The reason the economies of Europe and Asia did so well during this time frame is because they were growing up from smoking ruins under US military protection, of course they grew rapidly. Economic growth from the “very poor” stage is easy, it’s happened all over Asia as soon as private enterprise has been allowed, case in point on the largest scale being China.

If high taxes are so great why is the economy of the EU completely stagnant? Why are IL and NJ and CT and upstate NY stagnant and TX and FL booming?

“CPI only measures changes in prices of the same thing or service at the same quality over time”. Actually it does not. There is a very large bias in the CPI as it does not account for substitution which became part of the CPI measurement in the 1900s in order to understate inflation deliberately.

Correction. Substitution (in the CPI) was introduced in the 1990s not the 1900s.

Correction number 2: The 1990s were in the 1900s.

Morning… Yesterday I was out canvassing and delivered voter information re a highly debated city bond proposal that is a clear money grab(real estate tax) on the older population which make up a large percentage of the small city. People are on a tight enough budget and cannot absorb any more of this BS from the government. I could see it in their faces.

As thing fall apart, and unfunded public liabilities grow ever more unsustainable, lemons will be squeezed until the pips squeak.

Most of us will qualify as lemons.

Those who have had enough ain’t seen nothing yet…….

I had enough in 2015 got out and never looked back There’s a great big world outside the US borders if you look alittle I met a retired school teacher from Chicago living very well in Warsaw He even bought me a beer

Just move to New Jersey, where the average real estate tax is %2.37 of assessed value

In Texas it’s 1.86% (higher in many well to do areas) and catching up to NJ!

Only plebs pay that much.

The wealthy of course, get agriculture and recreational exemptions.

Connecticut real estate is a disaster Bigger and bigger deficits and shrinking income levels and tax base Its only a matter of time now

For most of this year bond buyers have been in a buying panic , sending prices higher and yields lower. So it is obvious that any projections of future deficits are irrelevant to them .

Given the fact that interest rates are going lower and lower despite deteriorating deficits, what is to stop the Federal government from assuming local and state pension obligations?

The answer is the really nothing but the party in control.

Just watch what Illinois is trying to do with pension obligations.

Can your projected SS benefit go down? Yes it can and did in my case. I will explain how so you can ponder this. If you don’t have 35 years of FICA taxed income, the calculation uses less than 35 years down to 31 years. In other words, zero income years are not hurting you until you have less than 31 years. If those years between 31 and 34 were good income years, and you retire and take on a smaller earning or part time job, what was not counted as a zero income year now gets counted, and can be low. This lowers your monthly benefit, because no income with less than 35 years is better than adding in a worse year than the other years. Think about this if you want to retire early and work a little on the side.

Some more ideas to improve social security

—————————————————————-

1) Allow 5 to 10 percent of trust funds to be invested equally between US stocks and international stocks

2) allow 5 to 10 percent of social security to be invested in us and international bonds

3) convert social security into a sovereign wealth fund like Norway and get a good HONEST management to manage it

4) index SS increases to inflation

5) overhaul CPI

6) change CPI to include quality improvements (Value added improvements) so that CPI accurately reflects cost of living (include drug, taxes, insurance and education costs in calculating CPI)

There’s a simpler solution. Just tell the Fed and the Treasury to pay real fair interest rates.

Put my SS money into Tesla and Uber? I will take what they give under the current system. Risking my 401 in the stock and bond market is enough.

Scare tactics…..in 2034 fully 1/3 of the us population will be on social security. So what politician will allow benefits to decline?

Low Cola means less demand on the trust fund.

Just raising the retirement age two years to adjust for life expectancy and raising the threshold for payroll taxes to $150,000 or so just about balances the program. So what is the big deal. Folks need to work later anyway since they have not saved a nickel and the country needs labor.

Its the raid on medicare by the (never thought I’d say this) demorats that is disturbing. They stole billions to fund Obamacare and now want to place the entire population into a system that was funded by working folks for those that paid. Raise the tax by one half of one percent over 20 years and you have all the medicare dollars you need.

There are a lot of synergies in the system, states should take the liability for a lot of it, including disabilities, and certain health care provisions. MMT could provide money for the system, and if politicians want to monetize consumers there is no better method than “recalculating” CPI. I feel like SSN will do just fine, but I also thought the Post Office had certain advantages over the package carriers, but they have become a miserable anachronism. Much of it is the lack of political will. At least SSN is not a tarnished brand.

Good comments Ambrose……I suspect that the 30% of the population receiving benefits most of whom will be older and voting wlll be quite a motivation. 45% of registered voters or more will be receiving benefits

Speaking of MMT, don’t you think if printing money created wealth it would have been figured out a long time ago instead of real capital.

the point cynically is they have been printing IT for years for the benefit of the bankers, how bout a little for the rest of us?

The “package carriers” hand off a lot of their stuff to the US Postal Service and having dealt with them heavily (Ebay seller) since 1997 I can say they’re excellent.

Social security is nothing more than generational theft. Right now 40% of it is being paid by foreign investment of US debt. No, it will not be around much longer.

1) The house beg. The media criticize the betrayal.

When out of the crossfire, a new campaign will start and the 10Y

will plunge.

2) The 3M/ 10Y spread popup above zero, but when US attack,

the spread will invert and the CPI will plunge.

What you are predicting?….stagflation?…

would you please write in complete sentences.

I find him fun to read if you pretend hes nostradamus.

(No offense Michael Engel. Keep em coming)

I think it’s a bot.

Sounds like you’re expecting a deflationary bust?

What about a large part of the trust fund assets being IOU’s issued by the Treasury in order to offset the government deficit by borrowing from the that trust?

What???

My momma told be the gummint always and only put its social TRUST money into solid gold bars with each and every american contributor’s name etched right on its side. Now show me that ain’t the truth!

Don’t call my mama no liar!

No one gonna believe no government that can Print they own money gonna actually put that money in gold and silver unless the write folks names on that shit.

And then NOT let folks touch and feel and count that shit.

Who be the fool to think otherwise?

ALL Treasury securities by definition are IOUs issued by the Treasury Department, no matter who holds those Treasury securities, whether it’s me in my brokerage account, or the SS Trust Fund. And all of the money in the SS Trust Fund is invested in Treasury securities (long-term Treasury bonds and short-term certificates of indebtedness which are like Treasury bills).

The more money government takes, the more dependent all of us become on government largesse requiring more lobbying for more constituency groups in order to get that money paid to their particular group. Bernie Madoff only wishes he could have kept up a scheme like social security for as long as social security has existed. It only works because there is a mandated captive group of people always following behind who are forced to pay into it. I feel safe in writing that if people were told who is optional and they could save the money themselves, you would quickly find people opting out of Social Security.

“if people were told who is optional and they could save the money themselves, you would quickly find people opting out of Social Security.”

Down the road, there would be a lot of elderly starving to death. This used to the case. And so SS was formed to keep the elderly from starving to death. Young people don’t understand what it’s like to get old and have no job and no income and lot’s of health problems and no money…. It’s brutal, dude.

Bull crap. That is not what this is about. Most people collecting SS would do just fine without it.

CaptHank,

Yes “most people.” Something like 60% or maybe pushing it 70% would be just fine to OK-ish without it, or at least they’d somehow survive. And so let the other 40% or 30% starve to death? Even if just 10% of the elderly starve to death, that would be catastrophic. In one of the richest countries in the world?

Your comment makes me despair in humanity.

My gosh, Americans really are just temporarily embarrassed millionaires aren’t they? Even though a majority couldn’t come up with $500 in an emergency if their life depended on it, and most are one paycheck away from destitution….. (Just to be clear, these may be truths, but it’s also a horrible tragedy).

Err, no. That $1200 a month or so that’s the minimum is keeping millions of people off of the streets.

I need a link or some stats to verify that statement…

Well I for one wouldn’t do so fine without it

“And so SS was formed to keep the elderly from starving to death.” well said Wolf, its fun bashing the nanny state but consider the clients

WR:

Thank you Mr. Richter!

Too many Americans have no clue as to the origins of SS. Not only to forestall any future major economic disasters to lead to revolution, it was also recognized that “things had to change” or the country would slowly be burying most of the elderly before their time.

Growing old is inevitable. “It’s brutal, dude” (WR). is true. Too many believe in a perfect society where everyone is able to “invest” their hard earnings in “secure” investments. We all know how untrue that is.

SS was NOT intended to be a FULL retirement program. It was supposed to “augment” a self inflicted program of prudent living and savings…..for the future.

A country is considered “progressive” on the basis of how it treats it’s young and elderly. How would the US be rated?

Some commenters point to SS as a, “Ponzi” scheme! LOL! We endure and tolerate “Ponzi” schemes in US economics throughout our lives!!

SS is not a “handout”; the monies are a mandatory savings plan to forestall destitution in old age.

Some “things” in society must not be thrown on the maniacal highway of “free markets”. SS is one.

Caveat: I’ve been retired since 1994 on a very modest organized labor pension/health plan/SS and small savings. I live outside of a major urban area in CA and am thankful for SS as an augmentation to my other income.

Too many do not understand why SS was implemented; having been born in 1930 (SF, CA) and having vivid memories of what kind of lives my parents and their relatives lived at that time (all Italian immigrants) I don’t believe many Americans have those memories anymore. It was brutal.

The maintenance of SS will define what kind of society we want to be….one of compassion or one, “Kill them all and let God sort them out”.

Which will it be?

SS would be much better if it were a program geared toward paying a survival level pension for the very poor unlinked from a person’s own contribution. No reason people earning above median income in retirement should be collecting SS

Looking at how many people couldn’t come up with a few hundred dollars for an emergency or the average IRA account balance, the notion that allowing people to opt-out is a good idea is wishful thinking.

Yes some would do just fine but many who opted out would be in for a rude awakening: i.e. they reach retirement and it turns out they don’t have enough saved for retirement. What do we do then?

Our choices would basically come down to either letting people starve in retirement or bailing them out, neither of which of is a particularly desirable option, so we’re better off leaving the current mandatory system in place.

Isn’t that the elderly equivalent of “won’t somebody please think of the children?”

Emotions and intent behind SS were noble, economic soundness not so much. When the program started, it asked for nominal contribution (both percentage and tax max). It became apparent unless higher and higher portion of income is captured, program will go bust.

Historical rates and tax max for reference:

https://www.ssa.gov/OACT/ProgData/taxRates.html

https://www.ssa.gov/OACT/COLA/cbb.html#Series

Also, when these schemes started, a large % of potential claimants conveniently died in the 55-65 age range, due to untreatable conditions, mostly blood pressure and heart- related – death at that age was not remarkable, and often expected.

Death soon after retirement was very common, above all for men leaving lots of merry widows who would live much longer relieved of the burden of a husband…..

My parents died in their early 60s; when you’re poor even if you were middle-class when you were younger, you’re supposed to die relatively young.

Corporatists naturally prefer people to die once they become unprofitable, so as not to compete with them for money to keep them alive which would otherwise accrue to their bottom lines.

They’ve gone through a lot of trouble to get people to acquire unhealthy and profligate habits to get them to die younger and poorer, which is why life expectancy is declining and the middle class is disappearing in the US. The plan is working, and bigger and better plans are in the works.

SS would be in better shape if people who never contributed a cent were not allowed to draw from it. SSI is used to pay out to all kinds of low income people who never paid into SS.

Petunia,

I think you’re confusing the Social Security retirement program (officially Old-Age and Survivors Insurance or OASI) with some other programs.

The PDF linked below shows how SS benefits are figured, and no, you won’t get any benefits — not even a dime — if you’ve never paid into it. There are minimum requirements, including the number of years you must have contributed before you can draw ANY benefits. Benefits are based on a formula that includes how much you paid into it, how many years you paid into it, and at what age you start drawing benefits:

https://www.ssa.gov/pubs/EN-05-10070.pdf

Wolf & Petunia,

I don’t think SSDI is based upon how much you paid in or for how long. I think Petunia is correct on this.

QQQBall,

SSDI = SS Disability Insurance. Not retirement. That’s a different program, and that topic was specifically excluded from the article because it’s a different topic with a different trust fund and different rules. But even then, you don’t get a dime of SSDI if you have never contributed (you need enough “work credits”).

BUT… I’m now re-reading Petunia’s last line, and what I had missed was that she was talking about SSI (Supplemental Security Income), not SS. SSI is another program for the disabled and Petunia was correct, it does not have work requirements.

Yeah, lots of different programs with different rules.

Also note that if you have not paid in at least 40 quarters of employment you will have to pay more for Medicare. Sometimes much more – when it is least affordable.

Petunia,

I’m just re-reading your last line — your distinction between SS and SSI, which I had missed on first reading. Sorry. See my reply to QQQBall above.

When the global economy collapses, and it will collapse, social security will be the least of anybody’s worries.

The ‘global’ economy will slow, but not collapse. Globalization has ensured we’re all linked now.

My household is scheduled to receive about $70k per year of social security. To earn that guaranteed income stream at today’s 2% interest rate, you’d need $3.5M in the bank.

It’s hard to reconcile past promises with today’s low growth reality.

I’m 40 and it’s something I pay into but will not rely on when I get older. Personally as a self employed individual I hate paying into it. But realize most would be penniless if it weren’t around.

Yes, you should rely on SS. All other companies are killing its pension plan. GE announced its end last week. what is going to happen is that the SSN will pay 76 % of the promised benefits by 2034. Please note that the benefits in 2034 will be higher then than now.

SS will pay 100% in 2034. I’ll be collecting by than along with tens of millions of boomers. Any politician who let’s SS payments start sliding will be voted out of office. This won’t be an issue.

Milliennials are a far bigger generation than boomers. Once they start voting en masse, they can easily outvote boomers, no problem.

They won’t vote to cut their parents income. Do they really want Dad moving in with them?

Wolf – another great article and I am glad to see you pick this up. Critically important. And yes, we need to remove the cap. Saying that benefits are also capped has nothing to do with this. And yes, we need to fix CPI and COLA. What a rigged system that is. And yes, fiscal spending will have to fill the gap. The boomer generation is a huge voter block and SS really is a political question much more so than a financial one.

The rich have always wanted to get rid of the US Social Security system ever since its inception, and have propagandised against it and otherwise undermined it at every opportunity for over 80 years.

They figure all that money should come to them more directly, and not pass first through the hands of the masses first. SS provides a measure of security to the general population, whereas the rich prefer people to be desperate wage slaves. For the same reason, the rich also want to get rid of any social program: pensions, Medicare, minimum wage, rent controls, usury, and a litany of others, all of which cost them money, reduce their control of profitable labor, and compromise the pursuit of their wealth and power.

Avarice is blind and has the morals of a famished barracuda.

They will succeed in getting rid of Social Security. All those trillions are just too rich a target. They will say anything and do anything to undermine public support for it. The comments on this page are full of it.

The history is interesting. As folks moved off the farms into industrial settings in the early 1900’s, people’s ability to take care of their parents on farms started going away in a big way. Americans working in industry suddenly had no way of supporting themselves as they aged, nor did their children, who often could barely support themselves.

By the 1920’s, this started becoming a crisis, and their was a big fight between the scions of industry who wanted to create a corporate pension system, and “socialists” who demanded that the government create a retirement system patterned off the one created by Bismarck in Germany.

Initially, the corporate plan was the winner. In terms of national myths, it was important for the population to always believe that income only could come from the “sweat of your brow” and a corporate pension was just reward for a life of hard-work and dedication to your corporate leaders.

The Great Depression destroyed all that, as the pensions died along with the corporations. And, the elderly really were starving in the streets, with their savings destroyed and no ability to earn an income. So the population demanded the socialist response and it has worked well for generations. But it is disastrous from a mythological point of view. It does show that the people can depend on the government to provide for them when in need. It starts down a road where people do not necessarily have to feel and be subservient to the upper classes. Which is why “Medicare for all” has to be beaten.

For a European observer, the US is one of the most myth-ridden and irrational places on the planet.

So many mistake corporate enslavement for ‘freedom’ and ‘choice’.

I’m no lover of European socialists and Marxists by the way.

The hard fact is that , as our civilization crumbles and viable net energy per capita declines, pensions, SS, etc, are simply history.

Just a moment in time which will not be repeatable as the surpluses will not be available.

Also note that the US is one of, if not the most hypocritical places on the planet. A vast difference between what is said and done.

Which is why “Medicare for all” has to be beaten.

The US health care system is a gigantic corporate cash cow, and getting bigger. It’s essentially state-sanctioned extortion: “Your money or your life.” The rapacious want more of it.

Socialism works, as the vultures know all too well despite their panicked shreiking. There are far too many unarguable examples. But it does not enrich the wealthy as much as they would prefer, and their preference is for maximisation at any cost. That’s why they hate it.

It’s always ‘My wealth is just; your pittance is entitlement’.

I had dinner with some very rich, European, bankers, and their line was:

‘Why shouldn’t people still work at 75?!’

Boy, are they afraid of redistribution!

It’s going to be fun seeing what happens………

I had dinner with some very rich, European, bankers . . .

When I have dinner with wealthy European bankers they congratulate themselves on finally getting millions of western Asian refugees flooding in to provide bargain-basement labour and to undermine worker legal protections. A real bonanza on every geopolitical level if you take a good look at it.

There is zero chance of SS being shut down. The wealthy don’t even pay for SS as it’s capped on regular income and doesn’t apply to interest and dividend and capital gains, why would they care if it exists? SS does fleece the people who pay for it, who could otherwise invest their own money at a higher rate of return than they will receive on their SS payments, but that’s another discussion entirely.

Canada might increase old age security for those aged 75 and older thanks to Trump’s proposed zero or negative interest rates. Trudeau looks like a sure winner in the upcoming October 21st election in Canada. Thanks to zero interest rates seniors may starve to death thus the increase for those living to 75 and older.

The election in Canada is neck and neck, Trudeau is no “sure winner”

https://www.politico.com/interactives/2019/canada-election-polls-2019-latest-polling-updates-by-region/

There is an amendment for an income tax to our Constitution because income tax is really unconstitutional. Ergo Social Security, Medicare, Medicaid should not exist. They are unconstitutional as well. Keep all your money and make your own decisions. Problem solved. Anything less is communist and not American. Don’t like it, go elsewhere.

All of the social programs come out of the great depression caused by average people going into debt to make money on wall street. We need the social programs because people are financially illiterate, then and now. The new “retirement” programs that are self directed are destined to be retirement programs for the financiers and taxable treasure chests for the govt.

Only a small percentage of the population was involved in the stock market back in the late 1920’s. But you are right. Much of the population is financially illiterate, in spite of all of the free financial information available on the Internet.

“There is an amendment for an income tax to our Constitution because income tax is really unconstitutional.”

The amendment explicitly makes it constitutional.

Is this math right here Wolf? BTW I’m a long time reader and first time poster.

78 billion income

71 million people drawing from it

78b / 71m = $1100 per person per year.

And isn’t the average payout like $1100 per person per month?

Seems in the red by 90% to me.

This $78 billion is the interest income in 2019. This is money the Trust Fund earned in interest on its $2.8 trillion investment in Treasuries. In addition, the Fund receives contributions from workers and employers, and pays out benefits to retirees.

Where in the US Constitution is the Federal Government authorized to operate benefits programs for individuals?

Nowhere I can find.

So I believe the entire federal welfare apparatus is illegal under the highest law of the land and I reject any supreme court opinions used to justify these unlawful programs.

freewary:

“……provide for the general welfare….”