Seattle house prices fall year-over-year. New York condos drop to Aug 2017 level. San Francisco Bay Area near-flat. Los Angeles, Denver, Boston reach new highs. Las Vegas, Phoenix dream of crazy Housing Bubble 1. Miami stalls

“Prices are cooling, and Western states are starting to see the dip,” said CoreLogic in a statement when it released its S&P CoreLogic Case-Shiller Home Price Index this morning. But prices are not cooling everywhere. So let’s see.

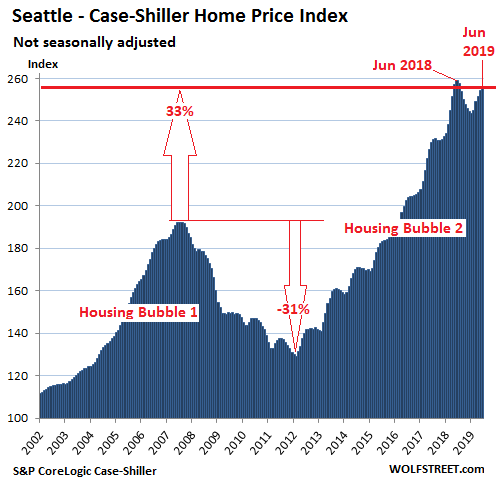

Seattle House Prices:

Prices of single-family houses in the Seattle metro ticked up 0.6% in June from May, according to the Case-Shiller Index. This was a much smaller increase than the seasonal increases in prior years. So, compared to June 2018, house prices fell 1.3%, the second year-over-year decline in a row, after May’s 1.2% year-over-year decline – and the first such event since Housing Bust 1:

The Case-Shiller Index is a rolling three-month average. Today’s release represents closings that were entered into public records in April, May, and June. So the data roughly coincides with the peak of spring and early summer home buying season.

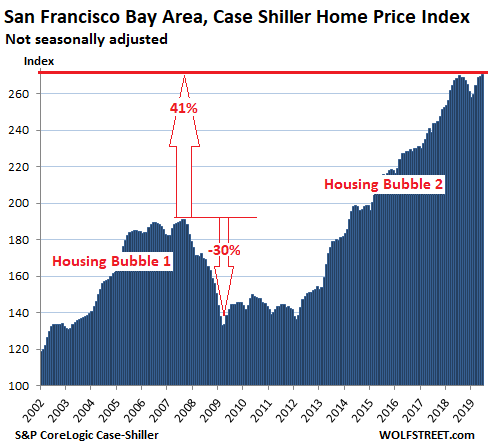

San Francisco Bay Area Single-Family House Prices

Single-family house prices in the five-county San Francisco Bay Area – the counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay) – inched up 0.3% in June from May, about half of last year’s seasonal increase in June. And it eroded the year-over-year price gains to just 0.8%:

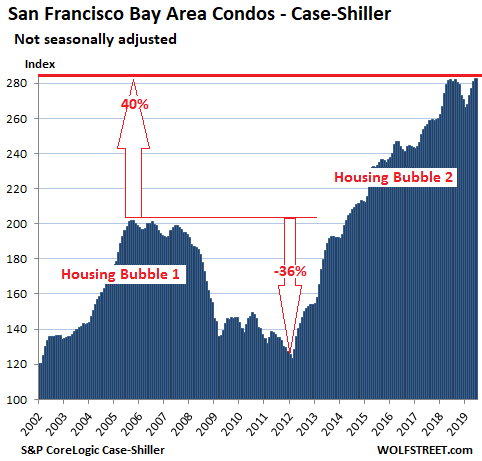

San Francisco Bay Area Condo Prices

In most of the 20 markets in the Case-Shiller series, the index covers only single-family houses. But in a handful of big markets where condos play are large role, it also covers condos. Condo prices in the five-county San Francisco Bay Area ticked up 0.6% in June from May and were flat compared to June 2018:

The Case-Shiller index was set at 100 for January 2000; an index value of 200 indicates prices have doubled since January 2000. Every housing market among these most splendid housing bubbles in America has or had an index value of over 200, either during Housing Bubble 2 or during Housing Bubble 1, which is the minimum requirement to make this list.

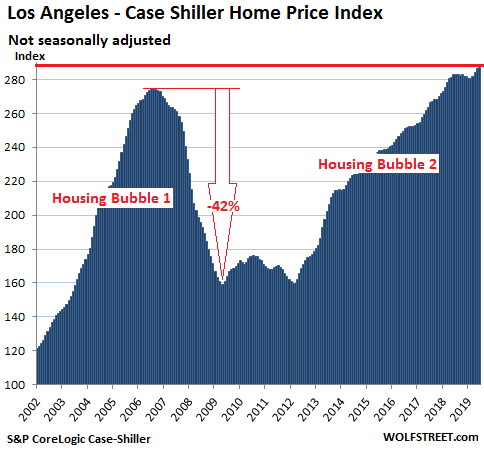

Los Angeles House Prices:

House prices in the Los Angeles metro edged up 0.2% in June from May, to a new record. This seasonal increase was comparatively small, and it whittled down the year-over-year increase to 1.6%:

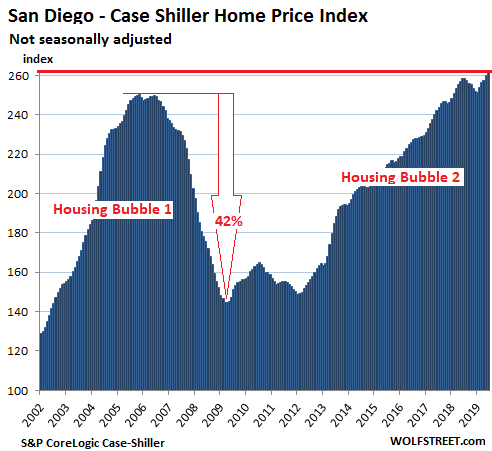

San Diego House Prices:

The Case-Shiller index for the San Diego metro rose 0.7% in June from May to a new record, which was only 1.3% higher than the prior record set in July 2018, and it was also up by 1.3% from June 2018:

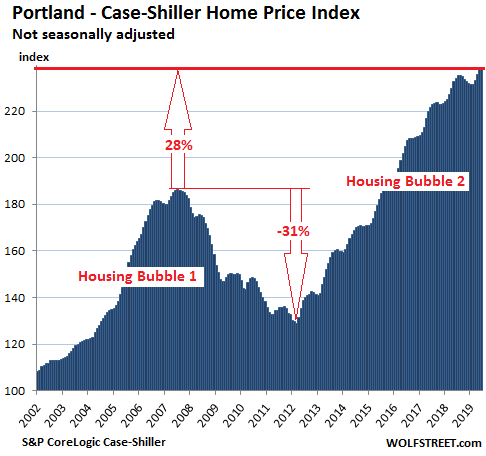

Portland House Prices:

In the Portland metro, house prices remained flat in June compared to May, and were up 1.7% from June 2018, the smallest year-over-year increase since May 2012:

The index as a measure of house price inflation:

The Case-Shiller Index (methodology) is based on “sales pairs,” comparing the sales price of a house in the current month to the last transaction of the same house, which may have been years ago. In other words, it tracks how many more dollars it takes to buy the same house over time. In this manner, the index tracks the purchasing power of the dollar with regards to houses in various markets. This makes it a measure of a specific type of inflation: “House-price inflation.”

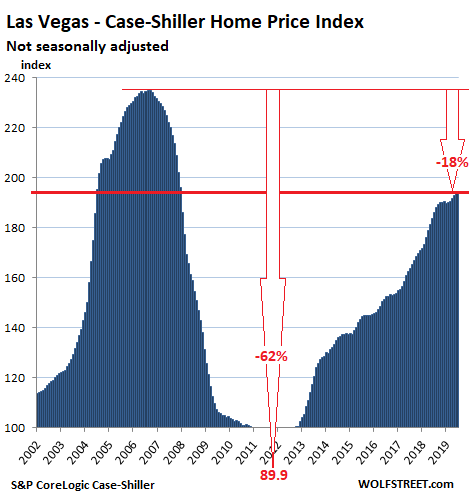

Las Vegas House Prices:

In the Las Vegas metro, house prices rose 0.5% in June from May, whittling down the year-over-year gain to 5.5%, from 6.4% in May. While the 5.5% gain is still out of whack, it was the smallest such gain since August 2016. There are not many markets in the US that embody crazy gambling in the housing market quite as well as Las Vegas (though below we’ll get to a couple of charts that are nearly as crazy):

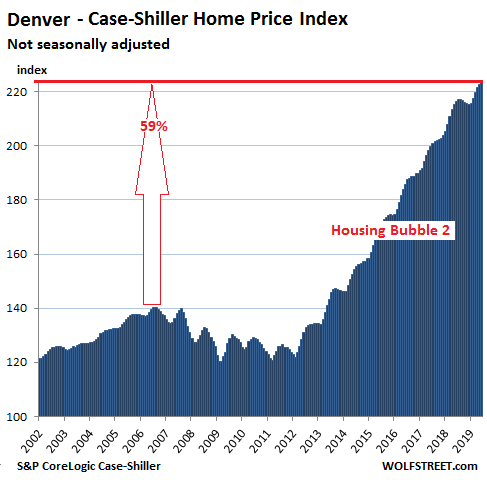

Denver House Prices:

In the Denver metro, house prices rose 0.4% in June from May, which whittled the year-over-year gain down further to 3.4%. While still a big-fat gain, it was the smallest year-over-year gain since April 2012:

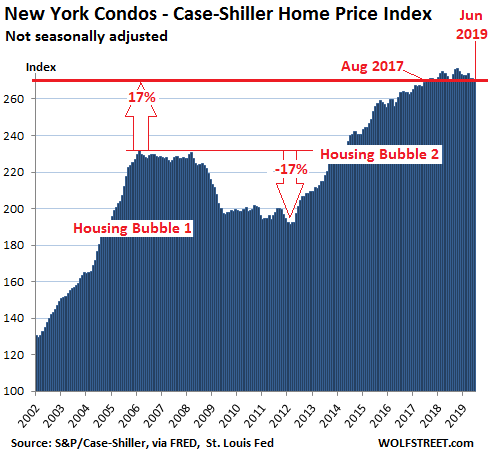

New York Condo Prices:

The Case-Shiller index for condos in the New York City metro, instead of rising seasonally, fell in June compared to May. While the index is still up 0.4% from June 2018 (which had been a dip, as you can see in the chart), it is now down 2.2% from its peak in October 2018 and is back where it had first been in August 2017:

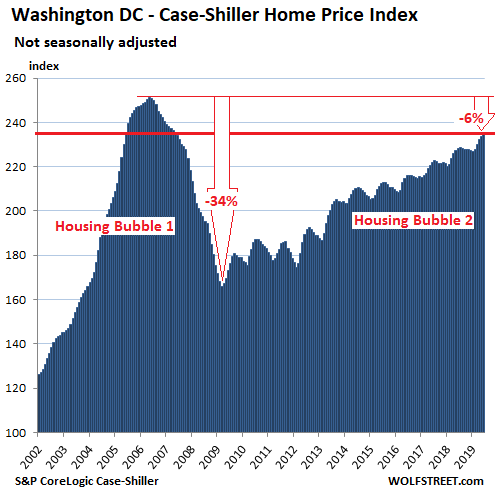

Washington DC:

In the Washington D.C. metro, house prices rose 0.5% in June from May, and were up 2.9% from June last year:

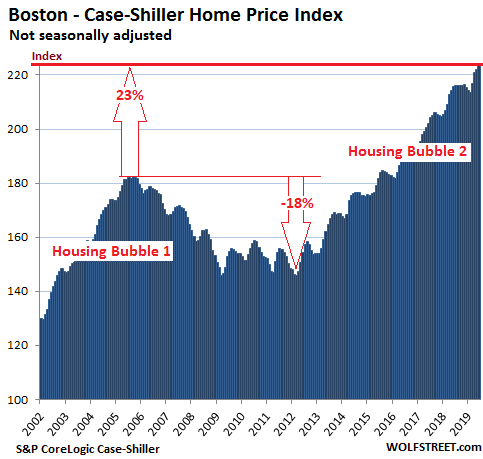

Boston House Prices:

House prices in the Boston metro rose 1.1% in June from May to a new record, and were up 3.9% year-over-year:

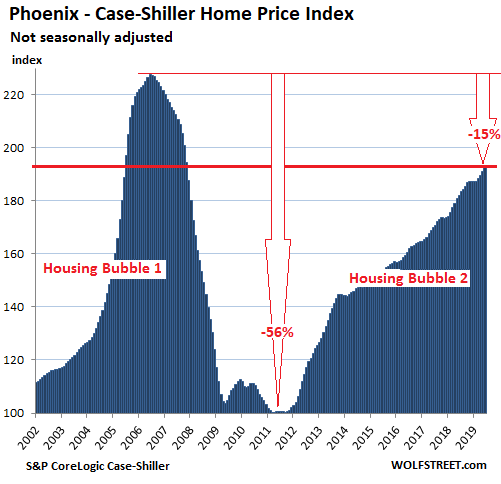

Phoenix House Prices:

House prices in the Phoenix metro rose 0.9% in June from May and were up 5.8% from June 2018. In terms of nuttiness, the Phoenix housing market – along with Miami and Tampa below – ranks near the top but can’t quite match the nuttiness of the Las Vegas market:

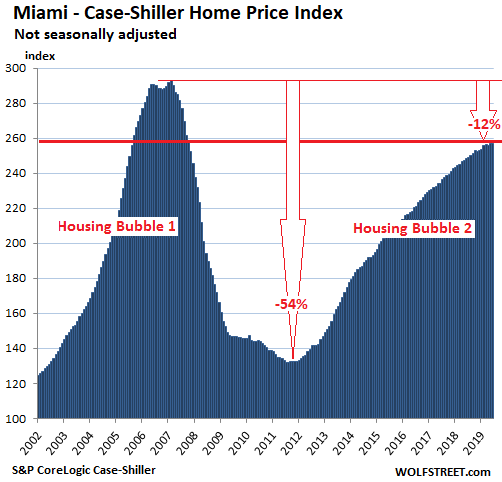

Miami House Prices:

In the Miami metro, house prices were flat in June compared to May, stalling efforts to catch up with the crazy peak of Housing Bubble 1. The stall reduced the year-over-year gain to 3.3%, the slowest such gain since May 2012:

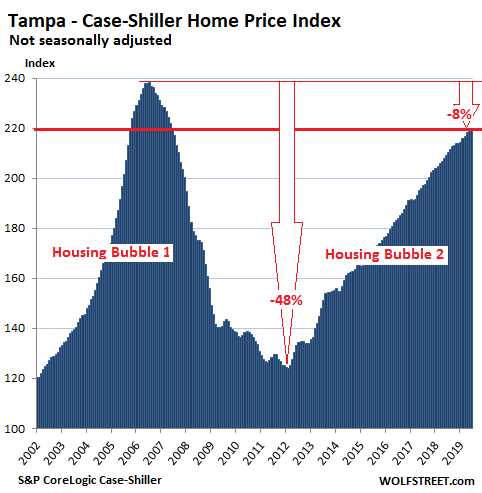

Tampa House Prices:

House prices in the Tampa metro inched up 0.2% in June from May, which whittled the year-over-year gain down to 4.7%. As big as this gain is, it’s the slowest such gain since August 2012:

Last time this happened was during the Financial Crisis. Now it’s happening in a kinder and gentler way, but there is no crisis. Read… Near-Record Low Mortgage Rates No Relief for Dropping New House Prices

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

These anemic YoY rises when rates are 120bp lower YoY, combined with a near elimination of bidding wars, buyer concessions, and lower sales volumes, shows just how far at the end of the cycle we are. If unemployment goes up, good night sweet prince.

The ingredients aren’t here for a crash, but they absolutely are for a correction. 2016 prices could be the lower bound. Don’t hold your breath for 2012.

June closings entered escrow at April and early May rates which were much higher than today’s rates. There is more upside here.

Rates have been at 4 or below since February. There’s not nearly as much upside as you’re implying. Sub 4 is the all important psychological barrier. Then again, you can cherry pick the bullishness out of anything RE related.

When you’re relying on .25% changes in mortgage rates, you’re clinging to straws. Such small fluctuations shouldn’t have this much of an impact if this was stable growth.

sc7 – Just got approved for 3.25% on conventional and 3.4% on jumbo. We are going to experience rapid price appreciation in real estate, gold, and crypto. Maybe too late for gold and crypto but real estate in high quality location is a solid bet.

The blueprint has been laid in the Euro zone where mortgage rates have actually gone negative in some countries. This implies bank deposits are earning negative yield and people are better off keeping cash in their mattresses, real estate, crypto, or gold.

SocalJim is a fool, but he is correct that we are going to experience another leg up due to the 175bp mortgage rate drop in a little less than a year. Luxury houses are much more appealing when you are getting between 3.25%-3.5% then they were at 5%-5.25%.

@Ed

Enjoy catching a falling knife. The rates have been lower for a good six months, it’s not showing any rapid increase. There are multitudes of reasons why you won’t see negative mortgage rates in the US.

And it’s not showing up in sales volume as mortgage applications have once again dropped:

https://www.zerohedge.com/news/2019-08-28/mortgage-applications-plunge-purchases-hit-6-month-lows

Rapidly lowering rates have diminishing returns.

Ed

I think it is rude to call someone a fool in the comments section. He has his position and has done very well for himself as he focuses in on very specific investment opportunities. I may disagree with him but all he is doing is expressing his view of things. When this thing goes down real estate may not be the thing you think it is. When the tax base drops so that states can no longer afford to operate you may find your property taxes going through the roof. Even in California.

In the “nicer” areas of OC:

Newport Beach, Laguna Beach, Costa Mesa home sales drop 12% as O.C. suffer worst 1st half in 8 years.

https://www.ocregister.com/2019/08/19/newport-beach-laguna-beach-costa-mesa-home-sales-drop-12-as-o-c-suffer-worst-1st-half-in-8-years/

GirlInOC, sales are down, but prices are up. Not sure how that is “suffer worst 1st half in 8 years” … prices are at a record high, and they are higher than those 8 years. I don’t get the OCRegister. Owners only care about prices … sales volume is not that important. Realtors care about volume, but they don’t care about prices. OCRegister must be speaking from a realtors viewpoint.

@socaljim

It’s not a good omen, it’s a sign the prices are too high, esp when combined with climbing inventory.

IIRC, volume dropped before prices last time.

SoCalJim, the article says that prices were flat in OC. Regardless, owners will certainly care about falling sales volume if it means it’s more difficult to find a buyer when the owners want to sell their homes!

GirlInOC, the latest SoCal home sales report was released today … last month, both sales and prices rose in SoCal.

From the peak in November 2018 to last week, average rates on the 30-year fixed-rate mortgage have dropped about 1.5%. That’s an 18% drop in the monthly principal and interest payment.

Most of the drop in rates happened recently. So, the full impact of the rate drop will not appear in CaseShiller till the August report witch will be published in 8 weeks, although we will see some of the impact in July report due in 1 month. The Boston price spike and the LA price increase is the beginning of the pattern.

Socaljim is very predicatable.

Does that mean his cat can predict what he’ll say?

JZ – Sure, and a broken clock is right twice per day. This time he is absolutely correct.

Predicate: “state, affirm, or assert (something) about the subject of a sentence or an argument of a proposition.”

So — I think — what JZ is telling us is that Socaljim can be the subject of a sentence or an argument of a proposition. I sort of assume that of all of us.

Well between SocalJim and Ed, I am now convinced that I must seek safe haven in real estate. My personal observations in unsuccessfully attempting to sell my properties and watching the market “soften” as my last realtor called it, mean absolutely nothing because of the comments stated here. Everyone needs to max out as much debt as they can and get into real estate ASAP. They aren’t making anymore land, rates are low which makes a lot of sense considering how great our economy is, everyone works for a unicorn company and walks around with millions in spending dollars, homeless / drug epidemic is fully under control, student debt will all be forgiven so that crowd will be entering the market to over bid properties, global recession is a hoax, all is good!

Lol, nailed it. The resident speculative RE bulls here have a LOT of time on their hands.

Leverage up now before rates go to -100%!!! Ignore all the other signs in the market with falling rates and record low unemployment not helping because of this suspicion that mortgage rates will go to zero. Never mind that asset prices have completely gotten out of touch with reality and incomes.

In the Boston area, my neighbor 2 homes down from me just closed on her sale. Asking price $347,500, selling price $357,500.

I calculate that to be $10,000 over asking.

CS seems to be reflecting that generally in it’s Boson area data.

Three years ago these homes were going for 300-315k.

Boston area has a lot of Medical, Education, Military Complex, Financial Services, Computer & Tech related businesses. Many are not affected by recession as much as other businesses.

@timbers

How far are you from the city? Is is technically still part of Boston metro? I haven’t seen prices that low near me for anything but 2br, 1ba condos since 2014. Those condos near me were going for 230k in 2014, now, $350k+.

I agree that Boston is strong economically, however, it’s not immune. There’s a theory that those that burn the hardest and hottest in good times are more subject to “cool offs”, though Boston will never spontaneously plunge because of what’s here. See the history where Boston felt both the 90 and 08 downturns, though of course recovered:

https://fred.stlouisfed.org/series/BOXRSA

As I have said before, regardless of what the fed does, they don’t have enough ammo. I continue to anticipate a modest correction of 10-15 percent in the next recession, followed by a good 5 years of stagnation (many of the hot areas near the city are going flat). I don’t see a crash. This is the best outcome for future buyers and us current owners alike.

Also, FWIW, $10k over asking is nothing compared to years prior in Boston metro. Last year, I was seeing $50k+ over asking, now I am seeing more under than over. Then again, it seems like the hotter, closer suburbs are cooling while the affordable inventory further out is getting fought over. Not a good choice for those people when the market does correct.

On an unrelated note, I’m even curious why you have so many neighbors selling their homes? Near me, if one in the neighborhood goes up per year, that’s a lot.

Boston hasn’t really burned the brightest or hottest. It’s just not falling it’s going up – as I’ve been saying for some time now. I live in the Southeastern Massachusetts less than 15 miles from Boston. I’d say prices here may be performing a tad better than Boston because they are more affordable vs northern suburbs. My guess is Boston’s healthy appreciation is partly due that Asian money is less a factor as it might be on the West Coast where you are seeing declines.

I’m curious why you think I have so many neighbors selling their homes? This is the first neighbor I’ve mentioned although 2 other neighbors bought within months of me 3 years ago (in fact 1 placed a bid on my house after I put it under agreement…they bought the house next to me which went on the market about when I closed). The others where co workers, and nearby comparable homes I’ve seen sold or drive by and noticed selling online as I usually check what’s listed from time to time.

sc7 – Tread very carefully here. The Fed has plenty of ammo. What do you think will happen if banks start charging -1.0% on bank deposits and mortgage rates hit -.25%? In a negative yield environment, everyone will flee cash and bonds and dump cash into hard assets and crypto. Especially leveraged hard assets that have negative interest rates.

I’d rather pay $1M for a house at -.25% then $500K for the same house at 3.25%.

@Ed — I don’t know. The payment on the house at $1M at -0.25% would be 23% higher on a 30-year fixed rate loan. 55% higher on a 15-year fixed rate loan.

But 48% lower on a 100-year fixed rate loan, so maybe that’s where we are going next… what could go wrong?

@Ed, agreed. In your example you would pay 100% more for the house but the payment only goes up 23%.

Conversely, if the CBs lose control and rates normalize to 4% above inflation then houses will be unaffordable.

@Ed

You are massively speculating on what the banks can/will do. As someone else noted, $500k at 3.25% is a much better deal than -.25% (which I really doubt you’ll ever see) on $1mm.

Prices are up by a smaller margin almost everywhere YoY than they had been for years, and that’s after the largest yearly rate drop. All this house of cards needs is to take the pressure of record unemployment off and demand will not sustain prices.

If I were you, I would tread lightly with any speculative buying.

How about Toronto GTA area outlook now?

An on the ground observation from another West Coast Housing Market. My wife and I spent the weekend in Vancouver B.C. Saw some stopped but half finished condo projects, and a few blocks of single family houses that had been purchased and boarded up in preparation for being cleared for a condo complex but seemed stalled out and covered in dust. One of them had a big sign, ” Luxury Condo’s ready for Sale in August 2019.” In the hotel was one of those glossy magazines with a full page add for a finished Condo Development. The sales pitch read as follows,” We know the market has slowed and prices are down but our quality development will withstand the test of time and deliver you value in the future.”

I had a hunch 10% year to year housing gains were not sustainable, as long as inflation was close to 2%.

Parts of Florida near me offered vacant land for sale. I saw mainly single family zoning areas in a world where multifamily construction might conserve land and lower housing costs by sharing roofs and walls. Where they do not allow additions with separate entrances, some people rent out rooms in their homes to strangers.

Vacation homes were being let out through Airbnb when owners were not using them. Airbnb is growing faster than Marriot or Hilton.

This was just posted a few days ago:

“Southern California hotel owners find it tough to fill more rooms this year.

Occupancy in the first half rose in just 12 of 31 local submarkets.”

https://www.ocregister.com/2019/08/22/southern-california-hotel-owners-find-it-tough-to-fill-more-rooms-this-year/

And anecdotally, all my friends this summer used various vacation rental apps for homes/cabins when they traveled. I was the only one that booked at a hotel. Old habits die hard.

None of my friends under 30 stay at a hotel unless it’s paid by someone else. It’s AirBnB all day, every day.

Rowen – I work in DC a few days a week and hotels occupancy seems to be very low. I’m getting solid hotel rooms for $60 per night on hotel tonight app (owned by Airbnb). I think it’s actually cheaper to live in a hotel then rent out a luxury apartment in SF, NYC, and DC at this point. We are approaching a world where younger workers may live in a different short term rental/hotel every day of the week instead of long term rentals.

Hotels on ‘hotel tonight’ are now significantly cheaper then Airbnb.

You need to read the entire article not just the headline. It’s more difficult to rent than last year, but not by much, and in some markets only. Overall, hotel performance has been phenomenal since 2015. The year over year increases in Revpar have been jaw dropping. Though it is tapering off. Not bad, considering that thousands of rooms have been added during the same period.

My corporate travel service now makes AirBnB options prominent. And we’ve been recommended to take Ubers instead of rental cars, depending on the situation (in some cases when the Uber costs more, on the theory that employees burn up thinking cycles when driving).

BTW, I’ve had much better luck with VRBO than AirBnB, but YMMV.

Have they considered their liabilities when one of those AirBnB rents they recommend for business trips suddenly burn up with their employees trapped inside?

AirBnB and Uber for that matter are unregulated “services”, there is no commercial insurance, no fire regulations, all is for private use and insured accordingly.

At my place, We are explicitly forbidden to use private accommodation and private transportation (and Ryanair) for business travel.

While housing prices may be peaking or rolling over the peak in some markets, my take is housing will not be the reason for the next recession. As Wolf points out, all markets are a bit different in this cycle. In the previous cycle, all markets went higher.

It won’t be the cause for sure, but it will be a factor in it, and will likely feel the negative effects of it.

I wouldn’t encourage anyone happy with their home to sell, but I wouldn’t encourage anyone to buy right now, either.

Housing excess got prime billing in 2008. It, like the stock market, will have to settle for supporting actor nominations this time around. The real star this time will be an epic bond market collapse that will show the previous crashes to be just dress rehearsals for true calamity.

Calm Horizons – Except the bond market has outperformed everything over the past 18 months. If you bought 10 year bonds last summer you’d be sitting pretty right now.

Pardon my naive question. What will happen if there is a bond market collapse. Does that mean bond prices go down and yields up?

Sargento,

Yes, that’s exactly what it means. Mortgages and other debts follow. If it is a “collapse,” as you call it, rather than just a mild bond-market downturn (which is bad enough), it turns into a financial crisis where credit freezes up and companies cannot borrow anymore to make payroll and pay vendors, and paychecks begin to bounce. It’s a very painful experience.

If Las Vegas is crazy, it’s caused by all the Calis bringing money over as they clear out of the real craziness. Nevada, Arizona, Texas and Washington are all benefiting.

What do Phoenix Las Vegas, Tampa and Miami have in common? (bubble two lower than bubble one). The possibility of ecological disaster. For AZ and NV the loss of a water source in the Col. River. Florida has the threat of rising sea levels. I think Wolf should add Hawaii. It’s all about location location.

https://blog.nationalgeographic.org/2013/04/05/landmark-cooperation-brings-the-colorado-river-home/

There is a treaty that we share Col River water with Mexico, though tearing up treaties is de rigueur for this admin one might suspect clawback is coming.

@AB

Haha

How dare you mention risk of ecological disaster and not throw California into the mix!

Or are they not included because they are already a confirmed eco disaster zone?

In the last 60 years, Arizona’s population is up 450%, but total (not per capita) water usage is down. The CAP (Colorado River) is not the primary water source for the Phoenix metro area– that primary source is the SRP, which derives its water from Arizona watersheds.

In other words, you *might* be waiting a while for Phoenix to dry up and blow away. But you never know.

Dale – Agreed. The West isn’t going to run out of water. Worst case is you build a river or pipeline from the PNW or Northeast. If they can do it for oil, they can do for a far more valuable resource.

The risk to habitability in these markets gets priced in (lower) and more people come into the market (lower prices) and the risk factor multiplies. The same thing could happen in fire prone areas of California which are uninsurable. Somebody will write policies (on the back of napkins although the state board will regulate that in other places they won’t) and the implied risk factor goes up. The reverse flood, what happens when the tap goes off? One seismic event from here. Millions of homeless people on the move, and RE prices in CA skyrocket.

Tearing up treaties de rigueur for this administration??? How about EVERY administration in American history…Manifest Destiny, American Exceptionalism, call the disease of Empire whatever you want. But it’s victims are legion.

Thoughts on Denver.

The limiting factor for supply is water availability so infrastructure needs to be built before development. There is ground water but the aquifer doesn’t replenish so once it’s gone it is gone. Therefore surface water is preferred and that means acquiring rights and building dams. Hence housing supply tends to come in big chunks as water supplies become available. My guess is prices are reaching the point where a lot of that is happening and new supply will start to come in strong. Unfortunately the “tap” fees can be quite high to hook up new homes to the system which makes affordable housing even more difficult.

Since there is really no indigenous industry other than tourism and pot is becoming legal in other states I wouldn’t want to be highly leveraged on a recent property purchase in Colorado when the inevitable economic downturn comes.

Your comments about Denver are way off base. Water is a long term limiting factor but has nothing to do with the rate that homes are built here. Legal pot is a draw for some but is not the driver of growth for Colorado. To say there is no “indigenous industry” is also very odd, is there anywhere in the west that has any “indigenous industry” other than mining or ag? The state has good weather and physical beauty and is a sizable tech 2nd tier location for knowledge workers of all kinds, with a highly educated population relative to most states. Tourism is a very small part of the economy, tech and engineering are large, and the area is growing as people are priced out of the west coast for tech jobs. The property market here is certainly out of whack and probably in a bubble, and I wouldn’t be over leveraging here either on the short run, but on a 10 year or longer time scale, there are few places in the US with a better economic outlook, and the state has grown very consistently for multiple decades.

I have seen several headlines like this come across my feeds in the last few days:

“Orange County homebuying slows to 8-year low as prices flatten.”

Could be ground zero for the next RE collapse.

The hot money is migrating to the Midwest. Someone I know was going to buy a house for X and at last minute an out of stater offered X+30%, deal! Heard other stories similar.

I’m looking at the Midwest/Nova Scotia for my future. This summer on the SE Coast was simply too hot. Between the heat, humidity, sea levels, and hurricanes, I can’t wait to leave.

The one thing that scares me about the Midwest is that the depopulated areas tend to be full of crazies. All the normal people left as soon as they could.

I have a big concern. Where could we Americans get good elderly care???

Great weather is kind of limited. At least one half of the USA gets snow. The other half gets heat/humidity and hurricanes maybe forest fires. But the real bid deal is where can you get quality care for older people?

It is the everyday little things that count.

Iamafan:

Ah, yes…the elderly!

“Where could we Americans get good elderly care???”

It’s available but expensive. Sometimes, very.

As an 89 year old in reasonable health but declining stamina I have looked for that kind of care in Central California. I live in the Sierra Foothills.

Most all “good” care money starts out at $3000 plus month for “non-assisted” care. For every escalation in trending into “assisted” care the price goes up…and up. For care in the “greater SF Bay Area, push the beginning price by minimum $1,000.

Additional facilities are being built in the Modesto area that will keep the prices a bit in flux but we do have lots of people getting older.

If you are “blessed” with good genes and decent health it isn’t too hard to make it; otherwise good luck!

This is America. Everything is for sale. You are a commodity whether young or old and bound for exploitation.

Try to plan accordingly if u can.

Assisted living complexes are being built in Mexico catering to expats from America. I saw one online that cost less than $2K a month includes everything.

Yep, just us crazies left here in flyover country.

STAY AWAY!! Only the 0.1% own a 7 figure mansion out here.

Garden is wrapping up, fall is coming. Fall is harvest time. Chainsaw is oiled and ready to go. Bow hunting soon for deer. Gun for small game & deer. Spend some time fishing to add diversity to the freezer.

Spare roosters to butcher ( great soup ).

All organic & free range just like the city folks preach.

Yep, just us crazies out here.

Speaking of the West Coast and disaster areas. Unlike most of California which has mandated reinforcement of old masonry buildings for years, Portland is full of old unreinforced brick residential apartment buildings that have not been upgraded. Now that the high probability of a Subduction Zone Earthquake is well known the local government is twisted in knots with what to do about these dangerous structures that will certainly collapse in even a moderate earthquake. ” Many of these have been turned in to Condo’s and are on the market. I am astonished at the foolish folks who buy these things at high prices ( they are all in cool parts of town) and never consider that it is almost certain in the near future that retrofits will become required. Such retrofits are very disruptive and and cost $50-$100 per square foot or more and would certainly be assessed to every condo owner. I guess there is always a greater fool.

I remember my college geology teacher chuckling gleefully at the inevitable fate of the multi-million dollar houses on the cliffs of California. Money can’t buy time nor stop erosion!

Horses for courses seems to be the issue. The United States built 2,400,000 homes circa 1972. Mostly single family units on their own lots. We’ve not matched that level since. US population then, about 220 million. Today we’ve crammed another 100 million people into the country and there is no where to put them in our major metro centers except in highrise complexes that cost a lot more per square foot to build.

In 2005-6 i saw another housing boom in 2nd tier cities in the mid atlantic, florida and, I gather exo suburbs in California) took off but it never reached the levels achieved during the Nixon era.

Today I see new construction in even the second tier cities consist of high rise units from the $1 millions and sub $250,000 starter homes are ageing crap shacks. We’ve maxed out our ability to house any more people.

Something that is often overlooked is that US population growth is very low compared to any time in the past– less than 1%.

In fact, the number of housing units per capita is very near its all-time high. And, in fact, there are about 1M more units than are required to match the housing units per capita available in 2015.

So, nationally, housing is not really an issue. The problem is that lots of people like to congregate like sheep in the same place.

The secret sauce to American success has always been generous immigration, hopefully the next administration will rectify that before it’s too late.

People move where they can get jobs. All the money and jobs are in the big cities, so we’re all forced there. When small business was the big hiring engine, jobs could be more dispersed. Also, globalization has pretty much eliminated US jobs that can be done remotely as well as the manufacturing jobs that were often located in more rural areas.

John Taylor:

Thank you!

Geez, Loooweeeezzzz!

It’s Jobs, Jobs, Jobs!

Where they are located you will find the highest concentration of people!

In the Boston area there is major “drive until you can afford it” going on….all the way to NH & RI in many cases..:we shall see…should be interesting!!!

I agree. Route 9 through Brookline, Newton, Wellesley, and all the way out is backed up. Back in 2012, you could get a decent small fixer in one of those three towns for just above 400K so you did not need to drive far for a home. Now, in those 3 towns, 1M seems to be the minimum if the street is quiet and the house is not a teardown. So, those Route 9 commuters are headed out to the 495 area to get something around 500K. As you said, drive until you can afford it.

Even apartments aren’t cheap in the Boston area. I was lucky to find a fairly basic and rather small 1 Bedroom condo for $1500 in Andover. People tell me that’s a great deal, but it’s $400 more than than I was paying for the 3 bedroom ranch I sold 2 years ago in Northern Vermont. Thankfully Boston wages make doable.

Well, keep an eye on good old Albuquerque NM as more media and Hollywood production companies and tech moves in. Netflix and Disney are two and housing is cheap compared to LA.

Where is San Jose the 3rd largest city on west coast, the urban center of Silicon Valley and the most expensive market in the USA?

The Case-Shiller index only covers five counties of the SF Bay Area, as listed. It does not cover all nine counties. But those five counties are a pretty good sample of the Bay Area.

These beautiful bubbles are only going to inflate even more. Wait for another round of ZIRP and QQE… I bet that in a very short period of time US (financial terrorist) Banks will be offering negative yield mortgages to “costumers”!

I guess the words Banks+Financial+Terrorist are still too much for an old folk to accept!

I realize I’m commenting late and most folks won’t see this, but I’m beginning to wonder if the plan was to raise the cost/value of major assets in order to increase tax collection.

California has it’s Prop 13, but many of those affected are aging and looking to finally sell. Most other States have no restrictions on the increases in property taxes, and as valuations rise so do the taxes collected.

Raising the cost of housing drastically impacts the amount of taxes due/collected, and that’s easier to change due to interest rate manipulation (a gov’t function) than through voted increases.