Turkish state-owned banks and subsidiaries of European banks on the hot seat.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

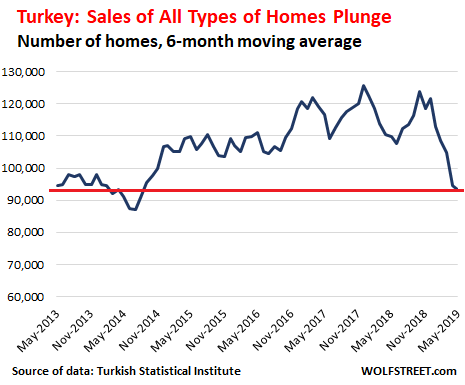

Sales of homes of all types in Turkey plunged 31% year-on-year in May to just 82,252 units, after having already plunged 18% year-over-year in April, according to the Turkish Statistical Institute. It was the sharpest year-over-year drop in the data going back to 2013, as Turkey’s economic crisis continues to bite. For the first five months of 2019, home sales dropped 19% compared to the same period last year, to 423,088 units.

The six-month moving average, which reduces the large seasonal and month-to-month swings of home sales in Turkey, dropped to the lowest levels since 2013-2014:

In terms of new homes, sales crashed 39% in May compared to the same month last year, to 33,765 units, after dropping almost 30% in April.

Turkey’s housing market is in a deep downturn after a debt and currency crisis last year sent interest rates on mortgages soaring and decimated consumer spending power. The government has lowered taxes on home purchases and offered cheap lending via state-run banks to help boost activity in the industry and stem the rising number of new homes lying empty.

But it’s not working. Last year, the total number of homes sold fell by 2.5%, the first decline in this data going back to 2013. The number of mortgages signed, however, plunged by 42% to 276,826 from a record high of 473,099 in 2017. That was a foretaste of things to come. For the first five months this year, the number of mortgages signed collapsed by a 65%, from 154,000 to 54,000.

Indeed, demand for mortgages is falling so fast that Turkey’s two biggest public owned banks, Vakifbank and Ziraat Bank, this week started offering mortgages to home buyers at below market rates in an attempt to reverse the trend. Both banks have cozy ties with Turkey’s President Recep Tayyip Erdoğan.

Vakıfbank’s new chairman, appointed last month, is Turkey’s former interior minister and Erdoğan ally, Abdülkadir Aksu, while Ziraat Bank is managed under the auspices of Turkey’s sovereign wealth fund, which is chaired by Erdoğan himself. The lender has been instrumental in spearheading the government’s efforts to revive the economy in recent months, by giving cash-strapped, debt laden consumers and businesses the chance to reschedule the debt they owe to many of Turkey’s private banks at low state-subsidized rates of interest.

This surge in loan growth helped the economy expand by 1.3% quarter-on-quarter in the first three months of this year, just in time for municipal elections, following three consecutive quarters of negative growth. But it could come at a heavy price: the more these state-owned lenders are called upon to support the economy by flooding it with more fresh debt, the more credit risk they themselves take on board.

Just this week, as political tensions between the U.S. and Turkey intensified, Moody’s downgraded the two state-owned lenders by two notches, compared with one notch for the other 16 Turkish banks it covers.

“The larger downgrade reflects the unseasoned risk that the banks have built via recent higher-than-average loan growth,” the ratings agency said. Moody’s also warned of a significant increase in external vulnerability for the country and a higher risk of more extreme government policy measures, including restricted access for depositors to foreign currency.

Erdogan has so far shown scant interest in implementing the sort of measures international investors, banks and ratings agencies have been calling for, such as requesting an emergency bailout from the IMF, much as Argentina did last year, admittedly to little avail, or dialing back his growing interference in monetary and economic policy decisions.

Erdogan wielded that influence to deliver over a decade of uninterrupted economic growth through unrestrained borrowing. But that all came to an end last year when a currency crisis sent shock-waves through Turkey’s economy, lifting the country’s debt levels and current account deficit to dangerous levels. Late last month, the IMF called on Turkey to ensure economic and financial stability, saying the government should introduce a comprehensive package of reforms.

The dilemma for Erdogan is that much of what is left of his waning popularity derives from the early success of his debt-fueled economic miracle, which is now fast turning into a nightmare, not to mention his vocal opposition to the IMF, to whom Turkey finished repaying $23.5 billion of debt in 2013. And there’s still little sign that Erdogan is willing to reverse course and deal with the very same financial institution he has spent the last 16 years denouncing.

“They want to see a Turkey like before, a Turkey that went cap-in-hand to the IMF,” Erdoğan recently said.

In the meantime, the deleveraging continues, which is bad news not only for Turkey’s state-owned banks, which are having to pick up much of the slack in the credit markets, but also the five major European lenders that have carved out a sizable, and for many years highly profitable, presence in Turkey — — BBVA, Unicredit, BNP-Paribas, HSBC and ING — and are now struggling with rising default rates in their Turkish entities.

Unicredit had to splash out roughly €1.5 billion last year to support its part-owned Turkish subsidiary Yapi Kredi, of which it owns a 40% stake. Spain’s BBVA, which owns just under half of Turkey’s largest listed lender, Garanti Bank, has warned that conditions are likely to further deteriorate in 2019 on the back of stalling credit creation and rising defaults.

This week, the Bank of Spain, worried about the exposure of Spanish banks, echoed the concerns raised by the ECB, which had warned last year about the risks of Turkey’s unraveling economy for European banks. The Bank of Spain now warned for the second time this month of the contagion risks posed not just by BBVA’s outsized exposure to Turkey but also to Argentina, whose economy continues to sink despite the $56 billion bailout it received from the IMF last year. By Don Quijones.

Non-performing loans remain dangerously to catastrophically high in Italy, Greece, Portugal, and Cyprus. Read… Bad Loans Still Too High at Eurozone Banks, ECB Warns

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Well, as Turkey implements its decision to snuggle up to Russia (a world famous financial screw-up, seller of generally-not-very-good military junk, and general-all-around puddle of corruption), that should really help the economy.

In June 2018, Erdogan won the general elections amid allegations of intimidation and ballot stuffing.

Shortly afterwards, he promoted his son-in-law Berat Albayrak from energy minister to finance minister. During the campaign, Albayrak blamed the sharp drop in the lira on foreign powers that wanted to sink Turkey. Apparently it never occurred to him that said foreign powers weren’t thrilled about Erdogan’s relatives accumulating so much power.

“…Last year, the total number of homes sold fell by 2.5%…”

Erdogan, on the account of being a great leader, is showing the way out of the crisis. If Turks build themselves a residence like the one he built for himself, the housing crisis will be solved in a matter of weeks (data from the Daily Mail):

Erdogan has one of the world’s most lavish residences, the Ak Saray, otherwise known as the White Palace, which has 1,100 rooms, 250 of which are for the sole use of the Erdogan family.

Thought to be 30 times the size of the White House and believed to be the largest palace built anywhere in the world for more than 100 years, a reported £7 million was spent on carpets and another £5 million on 400 10ft high double doors.

The silk wallpaper is thought to have cost £2,000 a roll and one drinking glass in the household is worth £250.

Due to the numerous spas, swimming pools, bathrooms and steam rooms, the heating bill is thought to run up to £500,000 every winter. The entire home is thought to have cost £500 million to construct.

Is the palace even bigger than the one Ceaușescu built in Romania ?

I have read(no real knowledge) that the russian S-400 is a remarkable weapon?

Thanks Don. Excellent article.

Every weapon the old USSR and now Russia has ever built has been described as “remarkable”, including the poison-tip umbrella.

Russian GDP is $1.6T (roughly twice the Pentagon’s $700B budget). When they do develop something “remarkable”, they can’t afford to make very many of them.

Until the S-400 actually shoots some important stuff down, who knows how “remarkable” it is (one thing it does have is very high speed)? It sure makes a great bogeyman for increasing US air defense budgets…

@chip I wasn’t sure if you were talking about the US there for a second.

Since Islamic banking is talked about as having world wide growth, I would have expected Turkey to have a large share of their banks be Islamic banks. Since Islamic banks don’t deal in interest products or speculation, what’s the story with them in Turkey during this downturn.

I don’t think Turykey’s banks follow Islamic banking rules. Most of them are standard banks, many of them foreign owned, with all the problems that standard banks have.

Islamic banking is growing leaps and bounds, quite profitable…. Just perhaps not in Turkey.

I won’t write about the gory details of Islamic banking and finance because it would quickly turn into an interminable essay.

Suffice to say the reality is much different from what the brochures say, especially if you picked up said brochures in Saudi Arabia.

The market share of Islamic banking in Turkey is about 5% and if I remember correctly the largest such bank is foreign-owned (DIB of Dubai). This is considerably higher than Indonesia (2.5%) and Pakistan (1%) but much lower than Malaysia (15%).

Generally speaking Islamic banks struggle to keep up with more modern and streamlined forms of credit: for example while successful in the 60’s in providing much-needed credit to the rural areas, these days Islamic banks struggle to compete with microcredit in those same areas, and microcredit itself has lost a lot of luster recently.

I bet I could buy a very nice house in Turkey for a lot less in Massachusetts. And Turkish men are very good looking as far as I can tell. Plus my dollar would go for so much more.

I was thinking the same, not about the good looking men (or women in my case) part though. There seem to be plenty of new apartment buildings in west outstrikes of Istanbul priced well blow what one would have to pay for a 100 years old ugly house/condo around Boston. Only problem is that not many speak English there and I’m not seen myself learning Turkish any time soon.

Meanwhile back in America….

I went to an open house today (that’s the hot new trend now, Friday evening open houses instead of weekend ones). I asked the realtor some questions and she basically brushed me off saying they’ve already got 2 offers and unless I come in well over asking, don’t even bother. So I said OK, thanks for the cookies (they were delicious) and left. Oh did I mention this house was listed for sale yesterday? That’s also the new hotness, open house the day after listing, in order to get all those offers in one shot.

So it’s great that Turkey is having a crash. It’s also pegged right at 0.0 on worry about stuff meter.

I might still make an offer. House would be a great vacation rental.

Big mistake to listen to the professional liar, I mean, REALTOR(TM). House will probably languish and have a price cut in 30 days. Don’t make a bid to be the knife catcher.

Excellent article! Spanish banks have high exposure to Brazil as well, which is joining the default party… Not looking good for Europe at all

Also your articles on Pemex, their bonds are getting smoked! Moody is preparing to junk them, dual ratings will officially have them in it, already yielding junk but losses on forced selling will really hurt their credibility, wtv is left of it anyways…

What happens when Turkish developers who borrowed billions of euros from Eurozone banks end up defaulting on those loans?

Looks like the Euro banks are going to go Kaboom pretty quickly as they are already leveraged with massive derivatives. The problem for Americans is that there are no real fire walls here. Banking is truly global, so contagion is not containable to any great degree. The 2020’s will be an ‘interesting’ decade. I am hoping my instincts are wrong and that the decade is not a global disaster.