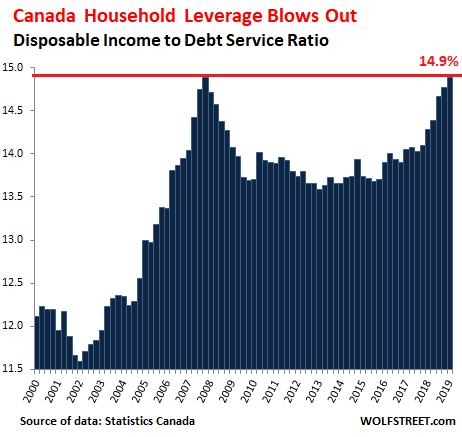

This, despite still ultra-low interest rates and the highest disposable income ever.

Canadian households are known around the world for their uncanny ability to pile on debt. And American debt slaves, who’d gotten trampled during the Great Recession, turn out to be lackadaisical these days in comparison.

The share of disposable income (total incomes from all sources minus taxes) that Canadian households spent on making principal and interest payments on their ballooning mortgage debts and non-mortgage debts reached 14.9% in the first quarter, matching the 2007 record, despite still ultra-low interest rates and despite the highest disposable income ever, according to data released today by Statistics Canada:

The drop in the debt-service ratio in 2008 and 2009 was a function of plunging interest rates. In Canada, most mortgages are variable-rate mortgages or adjustable-rate mortgages, and the lower interest rates turned into lower mortgage payments without having to refinance the mortgage.

These lower interest rates allowed households to spend more on home purchases, and home prices ballooned, creating some of the world’s biggest housing bubbles in certain markets, particularly in the Vancouver and Toronto metros.

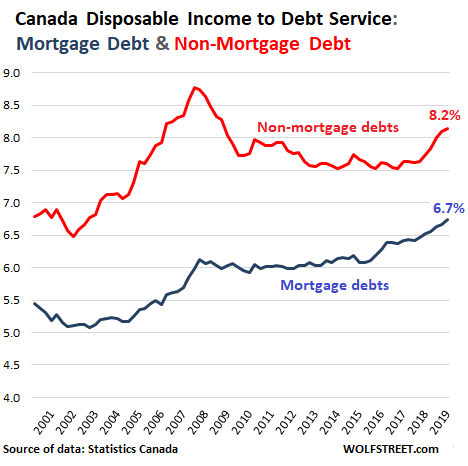

The two main components of household debts are mortgage debts and non-mortgage debts (such as auto loans, credit cards, and personal loans). Mortgages in Canada are mostly variable-rate or adjustable-rate, and as such have far lower interest rates than other consumer loans, with credit-card debt counting among the most expensive debt. But not all households are homeowners, and with mortgage rates being low, debt service across the nation is lower for mortgage debts than for non-mortgage debts.

The percentage of disposable income spent on servicing mortgage debt has ticked up to 6.7% (blue line); and the percentage spent on servicing non-mortgage debts (credit cards, auto loans, etc.) has risen more sharply recently to 8.2% (red line):

Total consumer debts rose 3.7% in the first quarter, compared to Q1 a year ago, to a record of C$2.23 trillion. This includes C$1.45 trillion in mortgage debts (+3.3%), C$662 billion in consumer credit (+4.4%), and C$114 billion in non-mortgage loans (+5.6%).

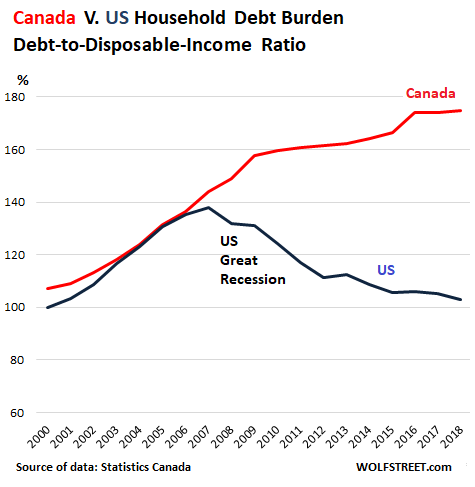

So how do Canadian debt slaves stack up against American debt slaves? Statistics Canada released a report on just this topic at the end of March perhaps because authorities in Canada should get a tad nervous. StatCan:

Levels of household indebtedness in Canada have also garnered much attention in recent years, in part because household spending has been a consistent source of economic growth, compared with less-even contributions to growth from investment spending and exports. The gradual onset of higher borrowing costs since mid-2017 coupled with increased house prices has brought about a renewed focus on the ability of households to manage their existing debt liabilities, particularly in view of slower wage growth.

The annualized data it provided included the household debt-to-disposable income ratios for Canada and for the US through 2018. The ratio shows how large debt is relative to disposable income. For Canada, this ratio was 175% annualized in 2018, one of the highest in the world, and rising. For the US, it was 103%, and declining:

Canada’s household debts have continued to surge since the year 2000 except for a brief dip during the Financial Crisis. But US household debts plunged during years of deleveraging after the Financial Crisis, in part by consumers defaulting on their mortgages and credit cards. Household debts didn’t start growing again until 2013. And it took until 2017 before they surpassed the pre-Financial Crisis peak.

But over the decade since the Financial Crisis, the US population has grown, and the number of working people has grown, and the national disposable income has increased, and so the ratio of household debt to disposable income has continued to drop.

High household indebtedness (leverage) was in part what triggered the mortgage crisis in the US which contributed to the Financial Crisis.

Canada is now in a similar situation as the US was before the Financial Crisis, only household leverage is a lot worse. In addition, the dizzying household leverage in Canada at some point becomes a drag on consumer spending as households have to divert too much of their disposable income to debt service and have less left over to spend on goods and services.

It’s a tough job, but someone’s doing it. Read... The State of the American Debt Slaves, Q1 2019

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Our politicians don’t get it, they add on new and heavier taxes and spending increases across the board.

Oh they certainly “get it”. By whom do you think said politicians are owned? Hint, it ain’t the electorate. MSM has the same owners.

It’s no better south of your border. Our politicians are exactly the same critters. In fact, it’s a worldwide condition.

BINGO

We have a winner,

I’m in ASIA and I can tell you that almost everybody that can get ‘easy money’ up front from the bank for a purchase does, and thus everybody has their debt ‘maxxed out’, the result is they never pay off this debt, and in ASIA they can go after the entire family, not just the debtor.

It’s the same ‘bank ppl’ worldwide that move into areas where pp may had not before preferrred debt, but are sold debt starts with a auto, and then leads to random purchases with a credit-card.

The end result is always the same, the family farm is lost to ‘foreclosure’. Auto/Cycle may only take 1-2 month late payment cycle before they are repo’d, I have known guys who sell the same auto/cycle over&over during the year take the 10% down and maybe sell the same machine 4x+, that’s where the money is, its a known-known that young ppl will default.

Hudsons new book “Forgive them their debts”, goes back to 10,000 year history of who organizes and runs this ongoing scam to get the weakest and dumbest in the world population into bondage.

Debtors make a more docile (and cheap) workforce.

Right on, NJGeezer. Big Business, Big Government, Big Media, one giant mafia stripmining the public.

It’s not “the politicians”. Murray Rothbard long ago commented that with no gold standard, all central banks have to raise and lower rates in unison so that there is no place for savers to hide when they inflate the global supply of credit.

Dale you are correct and with all the central bank collusion citizens cannot see how their purchasing power of their fiat currencies has fallen. Then with all the currency trading, the Wall Street boys and London can manipulate them all based on useless stories.

Low inflation in the US, well I just paid $35 for an automobile air cleaner. Decades ago it was less than $5.

My Dad, several decades ago, gave me an example of what the Government does to currency. He said in the early 1960’s he could have bought his first starter home (in the suburbs of Los Angeles) for about 250 twenty dollars gold coins ($10,000 US at the time). Today those same 250 coins could still buy a nice starter home, at about $330,000 US. Both Gold and Politicians haven’t changed.

I was in So-Calif ( left in 1970’s ), in early 1970 family bought a new track home in Garden-Grove, not farm from beach, for $12k NEW. Sold in 1990’s for $400k.

My grand-mothers estate sold her home in mid 1980’s for $250k, that house today is $4M as its near the Bob Hope mansion. One the few houses left still ‘grand-fathered’ to keep horses in the back-yard ( pickwick trail system )

I moved to the PNW in the late 1970’s, in the 1980’s I could buy houses all day long for $5k, now those same houses went to a $1M in 2007, but now back to about $500k.

IMHO sell-out of all RE in USA, its going down and hard. The only exception would be to buy into an area that never went crazy. I’m sure there are some college towns in the mid-west, where a guy could still buy fixers and populate them with students and pay-off the loans on a 15yr fixed. It’s tax deferred money, and its the only sure way to ‘get rich’ in the USA.

Some folk have been ‘hiding’ very well, gold standard or no. As Egon von Greyerz points out…

“If we look at the whole period 2002-18, Gold in Dollars and Pounds have, in spite of a major correction, gained a very respectable annual 12% on average and also outperformed the Dow Jones and all global stock markets.”

And it’s only just begun…

link to above..

https://goldswitzerland.com/gold-maginot-line-broken-time-to-buy-insurance/

Nothing to do with people being forced to borrow to pay taxes – just plain ol’ usury by the private finance sector (ref: your Bible for further info).

As long as you continue to do what you’ve been trained to do – to have a Pavlovian response to blame everything on government taxes/regulation – nothing will change for the better, unfortunately.

It’s not about taxes it’s about people buying stuff they don’t need on credit

If you can’t afford it then you shouldn’t buy it, if you don’t have the cash for it you should ask yourself do I really need it.

you should learn to live with what you need to get by before you go buy stuff you want.

You are right, it’s not about taxes. At least, taxes are not in the center of the story.

My friend from Vancouver is saying that her income stayed at the same level it was at 20 years ago. (She is an interpreter, whose ex actually forced her into debt consolidation ten years ago and now she wouldn’t even dream of getting into debt.)

In the meantime, everything has been getting more expensive.

It’s hard to lower your standard of living, especially when you are a frog in a pot that is heating up slowly.

Indeed, the same thing happened in the US ten years ago and now it’s time for our Canadian friends to face the music.

Nothing beats shareholder profits and political corruption.

And hope you don’t get into a medical situation which will wipe you out.

@Brant Lee. Maybe you are a US person, but in Canada with our health care system it’s almost impossible to get wiped out by medical emergencies. There is a universal health care system in all of Canada which covers medical expenses for everyone. And it’s mostly “free” ie paid through our taxes. Just like all those other “socialist” countries of pinko commie Europe. Only in the USA are you free to go bankrupt because of your health care expenses.

Better to go bankrupt than die in socialist hospital or not have any treatment for a year.

Contrary to most liberal media lies people rarely go bankrupt in the US because of medical debt. They of course can go bankrupt if they have no insurance (few people) and no money for the deductible, but in that case they would probably go bankrupt anyways.

We travel up to Canada for recreation. We don’t hear much good to report from the Canadians on their “free” medical care. It’s “free” when you don’t need a doctor. But, if you need a new knee or hip…………you’re in horrible pain and are confined to a wheelchair to get around, Canada’s “free” medical care isn’t, as one Canadian put it, worth a pot of piss because Canadian “free” medical care can’t find enough doctors because the docs aren’t compensated for their time and move south of the border to earn a decent living. So, John, you may be young and healthy now and laughing your arse off but wait till you get older and actually need medical help and told you have to wait, and wait and wait because it’s not an emergency your knee get replaced or that hip that keeps giving out. It’s not so funny then.

You will still die when you have to wait a year or better for treatment like us humble folk here in Nova Scotia

In England, the NHS provides a “free at point of need” service. As someone whose family member was recently almost killed by a “bait and switch” NHS activity (investigation supposed to be done by a surgeon, actually having been done by a rushing nurse), I can attest it’s grim, grim and some more grim.

The NHS now comprises of armies of ants at different levels of capability and responsibility, all being centrally managed through a computerised communication system with gaps that one can drive a flock of busses through. If you know what is your disease, and there is a family member available to supervise the hapless peons and force the “consultants” into doing their job properly, on a daily basis, you have a chance of survival. If you have no idea what is happening to you, you’ll be the free of charge experimental cannon fodder.

When Big Don bullies our next spineless Prime Minister into selling the NHS to his favourite Private Equity Fund, we will then be well and truly f***ked. Dead bodies galore, yes give it to me.

Even being a self paying customer of private hospitals will not guarantee survival.

Ah healthcare-

What is the most desirable in healthcare?

1. We want the best healthcare

2. Healthcare should be universal

3. Healthcare should be inexpensive

It’s long been known that you can have owo out of the three, but not all three together

A hospital administer I knew once said that the most cost effective patient possible for him was a Medicare patient that came in through his doors, got registered and diagnosed for the DRG payment, and then promptly died, without the hospital ever spending any more money or resources on that patient

Watchful waiting followed by death used to be the standard of care for a wide range of medical problems. It was very cheap to do, and universally applied to peasants, kings, and presidents

I think… It might be … Called… PERSONAL RESPONSIBILITY !

Missing from much of the discussion these days… Get educated about money and responsibility. Stop expecting everyone to bail you out. Live within your means. I get so sick of listening to all the blame industry shills whining all day bail this, bail that… I wonder – if the indebted masses just declared bankruptcy, re-calibrated their lives and started (Responsibly) all over again… stop rewarding the blood sucking debt industry. What would happen?

It’s interesting how everyone complains about the banks being bailed out in 2009, but no one talks about all those people who cashed in on the real estate bubble.

There are several people I personally know who paid zero down and flipped houses to become millionaires in CA between 2004 and 2007. But yeah, they won’t allude to that at all. Many of those who were left holding the bag wouldn’t have complained if they got to cash in too.

It’s going on right now where I live – people flipping houses like there’s no tomorrow, people buying these overpriced houses hoping to make a buck down the line by overextending themselves. When the manure hits the fan, they will blame the Fed or the bank who lent the money at 5% down.

Need little, want less and love more.

Short Canada?

The first time I heard about how Canadian mortgages worked, I was appalled. But then I realized the US with its 30 year fixed mortgage was the oddball in the world. It was really strange somehow. But then I suppose we are push more and more people toward ARMs given the rise in housing costs in the states, particularly the more progressive ones. So, I suppose in a way we’re catching up with the world. It’ll be just focused on the inevitable refinances as long as interest rate stay at this abnormally low level.

But the Canadian system really does tell us something… mainly that the lazy Americans need to get off their asses and spend more money, go more into debt. How dare the Canadians be more indebted than us. Go out, Americans, stimulate that economy. Buy more junk. Amazon stock prices need to go above $2K a share.

And, when you have filled your “house” with useless junk go rent a space somewhere else and fill that up too! LOL!

“What Fools These Mortals Be!” (Shakespeare, not me)

Canadians come to Bellingham’s Costco gas station (~50m South of Vancouver) with four to ten 5-gallon gasoline canisters in their trunks to load up on gas.

Gas is cheaper this side of the border but if one accounts for the time it takes to drive down (and back), it’s difficult to see the savings. Yet, they keep coming.

Maybe they are not financially smart. Maybe they don’t value time as much as we do. Maybe there’s a gasoline black market in Vancouver.

Whatever it is, if you ever drive on the last stretch of I5 going North, keep a safe distance from any car bearing a Canadian plate. It is likely packed with gasoline!

Heard they also stock up on milk. Due to government imposing high costs on dairy.

Every single thing you can buy is far more expensive in Canada than it is in the United States: food, vehicles, services, entertainment, travel. Most people are using their credit cards just to live, and the rental market is more expensive than the house purchase market, so many people buy homes because it is marginally cheaper than spending all your money just to live somewhere. We have high median incomes in Canada, but we have so much taxation that you don’t keep much of it. There is almost no competition for services here. Communications, entertainment, public transit is all run by monopolies that can charge whatever they want. Of course there is a middle class with actually disposable income, but they are not the majority of the populace.

EXACTLY. That’s the issue in Canada, it costs too much to live because of too much government and regulations, no one has any disposable income left over to enjoy life. No difference between a slave working for room and board and a Canuck working to pay rent or mortgage,food, and the rest to taxes.

Except marijuana and Fresh seafood in the maritimes

The grass is always greener down south, until you actually go and live there. Like everything else, there are good spots and bad ones in any country. And there are always “hidden” expenses — life is not only about packaged foods, cheap entertainment and driving around. Then again, that’s what amounts to “enjoying life” for some people.

Newsflash: It “costs too much to live” EVERYWHERE. Go to Vietnam and you see condos that cost MORE than in the US/Canada. Go to a resto in HK and it often costs more for the same quantity of food.

At the moment it is only $1 per gallon difference but a couple months ago it was over a $2 per gallon difference. For some the costs to get that difference are worth it just to make the point known to the suppliers in Canada, as sales in Canada would suffer and hopefully come down if the sales drop.

Canadians have more debt because we’re much more wealthy than our distant cousins to the south. Median net worth of an adult Canuck is around $105K, vs. US of $61K. Median household net worth is about triple that of the US. Sure debt levels are higher, but we’re simply wealthier. It more than evens out. Now the government is proposing universal socialized pharmacare — could happen, that will improve net worth further, cheap drugs! Otherwise, the economy continues growing, oil is back up — good times.

I hope you recognize the effects of leverage are uneven and often unstable economic growth. What happens to this net worth during a recession?

Also, please explain how government-subsidized programs have costs, pharma or otherwise.

Based on what? Over valued real estate?

Actually, health care probably does make a big difference. The Federal Reserve’s “Report on the Economic Well-Being of Us Housholds in 2018” notes that 1/5 of US adults had major unexpected medical bills in 2018, and 1/4 skipped necessary medical care because of the cost.

I’m appalled by Canadians’ willingness to take on debt, but not having to think about unanticipated medical costs is probably part of the difference.

As long as there’s no China, America trade deal Canadian’s wealth is in free-fall mode. The only thing propping up the Canadian housing market was the Chinaman. Look at the fall in home prices in Markham, Richmond Hill, Unionville, Stouffville and Vancouver. Home prices follow the Chinese money.

Nicko2

Canadian “net worth” is a mirage. It is entirely anchored in house pricing, which in turn, is a function of Foreigners pricing working Canadians out of the housing market.

Booming economy? The second largest Houseboat Company in B.C. which relies on Albertan oil money to get customers, just went bankrupt. Naturally, after taking deposits for this summer.

Cenovus, Seven Gen, Canfor, you name the commodity, and they have all had their shares collapse 70-90%.

As usual, government numbers don’t tell what is really happening.

I live in central Alberta and things are getting worse as time goes on. Many oilfield construction companies have gone bankrupt, as well as many small businesses in the local town.

My brother is a field operator for a company that produces mostly natural gas. They are having a very hard time and have severely cut back on expenditures, including the number of people employed, along with their wages.

The people that are lucky enough to have a full time job are now being worked like mules because companies can’t afford the cost of full time employees. Taxes and over-regulation (socialism) are killing off small and medium sized companies that actually produce things.

The official government employment numbers are a complete fabrication, along with GDP and inflation. We are in full on stagflation and the pain is getting worse. Those who are in debt can no longer pay off those debts.

There is nothing but hot air holding up the Canadian economy. It can’t be very long until banks start going under, unless the Bank of Canada is propping them up with our own secret version of QE.

Alberta isn’t the Canadian economy — it’s a resource-based economy that is highly leveraged to the price of oil first, and farm commodities second. Ontario and Quebec are far larger, more diversified, and in less trouble. Sure, things in Canada could be better, but taking Alberta as an indicator of the whole isn’t valid, particularly because other parts of the Canadian economy benefit from lower oil prices and a weaker Canadian dollar, while Alberta benefits from high oil prices and a stronger Canadian dollar.

Oil is falling and heading down a lot lower. Two former oil companies in Calgary I used to work for are in the process of layoffs. If Iranian Oil wasn’t off the market we would be around $40 a barrel. But don’t worry, over the next year US pipelines in Texas and the Dakotas will start bringing on 1.5 to 2.5 barrels of capacity, that will not only fix the Iranians, but the Great White North. But don’t worry we in Canada will just bring on another magical freebie, like Pharmacare, paper straw plants, Daycare for Puppies, or solar farms in the high Arctic, jobs, jobs, jobs for all, wealth for doin nothin…it’s so easy…why don’t those Yanks get it…..and we will walk in pleasant gardens and sunny ways…

“So collectively Canadian families paid $202 billion in debt payments in the first quarter of 2019… About half was for mortgages, the rest for HELOCs, credit cards, cars and tat financing.

…Worse – for the first time in six years we’re spending more on the interest on debts than we are on paying those debts down.

Chew on that.”

Garth Turner

Now let your home prices deflate by 30% and see what kind of job that decline of a highly leveraged asset does to “median wealth.” That’s what happened in the US during the housing bust. And Canada is due for one.

When your overvalued real estate market collapses (as is well underway) your fake paper net worth will quickly ascend into money heaven.

You are spot on. The median HH net worth in Canada will be higher than in the USA even after de-leveraging caused by lower home prices.

Ireland’s median HH net worth is higher than in the USA and Ireland had a whopper of a housing meltdown from 2007-2012.

The USA is becoming a rough place to live for the majority of it’s citizens. 85-90% of people will not have enough savings to retire comfortably.

I’ve spent most of my life in Canada; have moved to the US twice, once for 2 years, and the second time for good (here 14 years now). In terms of real dollars (ie. cost of living), there’s no doubt that the average American has higher disposable income than the average Canadian. Of course, it varies based on where you land in either country, but I have visibility across the country on both sides of the 49th, and have been observing these realities for 20 years now.

Exactly. It costs way too much to live in Canada and most people believe the government propaganda that they are being taken care of and getting good value. I have lived in both countries and it is much better in the US for someone in the middle class.

Ok, I am curious, is there anyone to mooch off of Canadian’s generous social benefits and not pay any of its ridiculous taxes?

I seem to recall seeing that it is possible to do that somewhere while still owning large houses, but claiming to be poor.

I would like to know, because I’d like to enjoy the wealth of Canada. Preferably without paying the taxes of the Canadians.

The whole world is awash in debt- government, corp, consumer. Record high amounts mean a depression is coming. A tipping point is not far off. Sad really to think how many will be hurt. Do people not see this. Is gold bullion the only answer?

…and a spread betting account so you cab short FIAT against Bitcoin and PMs..!

Gold is a guess, not a clear answer to anything. It may be a traditional holding, but traditions can change, permanently. I hold no more than 5%.

Gold is up 17 of the last 18 years in Canadian dollars, though miners’ shares are lagging — more than they should. Gold and silver mining shares will do very well for Canadians.

Here is an argument for why gold might do well with the US dollar coming under pressure:

“Thus, a key point for us to appreciate here is that a new rate reduction program by the Fed will cause the dollar to drop hard – and it is already under threat from the move to de-dollarize by countries like China and Russia which have been the subject of US bullying and threats for a long time now. The Fed can’t have its cake and eat it too – if it wants to go ahead and drop rates to rescue the stockmarket, fine, then the dollar will tank, and the stockmarket too into the bargain because a lot of overseas investors facing currency losses will pull their funds from the US.”

https://www.clivemaund.com/free.php?id=5069

Interesting overview. Here is a global comparison from BIS until 2017 (page 39ff), which also showns the Canadian side at around 100% of disposable income, while the US are clearly below (and much of Europe much lower as well)

https://www.bis.org/publ/qtrpdf/r_qt1712.pdf

US 30 yr mortgage rates were over 6% during 2006-2007 as the housing bubble started to deflate. Now the rates are less than 4%. People are able to borrow more.

Until rates rise, then these prices will fall. The fact that the market is stalling out at these low rates shows just how screwed this market is.

Canadians on average mostly all take out 5 year fixed rate mortgages. Very few take out variable rate mortgages because they’re too stupid and don’t realize interest rates will take a large drop between now and around May 2020 when they start to increase again. After the 2020 election the bottom will fall right out of interest rates. So rates will fall between now and May 2020, rise between June 2020 and the end of September 2020. Push sideways until the 2020 election and then fall off the table after the 2020 election in the negative category.

With all due respects please provide a link or something proof Tony

The Tony might be real but the prediction is far from real. Just over 10 years ago interest north of the border was over 4%, a number that would make current debt holders crap their pants. It may not reach that level anytime soon, but it is more likely to go up than go negative. This isn’t Japan.

The mortgage difference with the dreaded variable is that you can immediately ‘lock in’ if the rates rise, or if you think they will rise. They don’t float for people to get hosed down the road, even for Hosers.

However, when my kids bought their homes I recommended fixed at 5 year term so they could budget easier. They’ll have their homes paid for by age 45. Both are on vancouver Island in sought after areas to live.

Not everyone is a debt slave. :-) (I’m 63 and have never had a medical bill and don’t anticipate one). Just sayin’

What is this 2020 election business in Canada? Our elections are this year, not next.

The attitude now is if you have the credit then you can spend it. Live for today. At some point there will be a crisis, but it may be the asset owners/creditors/banks/shareholders that get it rather than the debtors…you can’t get blood from a stone….plus we need that consumer buying, don’t we?….or so the Financial MSM keep telling us….I can hear it now….save the economy, save the spenders…

There are at least two fundamental differences in the Canadian vs US economic systems:

1- The US is a global empire that spends over a trillion dollars a year projecting force all over the planet, supporting 800+ overseas bases, fighting endless small wars, and building F35 boondogles.

1A–The Canadian war machine is so small as to be economically irrelevant. Medical costs per capita are half that in the US. No wonder there is so much more available for consumers (debt)! Factor in their much more equal income distribution and the Canadian middle class are more representative of Canada as a whole than the few thousand Oligarchs that really control the purse strings in the US.

2- The purpose of US full spectrum military dominance is to maintain the Dollar as the world’s reserve currency so the US can simply print the money necessary to import or steal what it needs to maintain its life style— (Venezuelan oil, Afghanistan opium). The US has lost the reserve currency battle to the Russian and Chinese vision of a bi-polar world (although the US Masters of the Universe may not yet realize it.

2A–The Canadian economy is a resource based export economy grafted at the hip to the Elephant to the south. The chances of it becoming an independent country in charge of its own destiny are slim at best.

Care to explain how the US has lost the currency battle to the Chinese and Russia?

Last I checked the US dollar accounted for 88% of international transactions.

Russia has an insignificant economy smaller than Italy and Chinese economy looks more on the verge of collapse than about to take over the world.

It’s coming. They’ll be a basket of currencies down the road. I don’t think many Americans, (and this is 1/2 my family), understand how their stature has fallen the past decade, especially the past 3.5 years. It’s palpable where I live, for sure.

It isn’t individuals or ‘the people’ that are disliked…it is the World Domination System masquerading as American Ideals that is hard to take. regards

From the IMF, China is solidly #1 and Russia is 6th, right behind Germany. Italy is 12th. I guess it’s all is the data you select.

https://en.wikipedia.org/wiki/List_of_countries_by_GDP_(PPP)

Lion,

Purchasing Power Parity (PPP) GDP, which is what you cite here, is a form of mental masturbation if you want to use it to compare the size of economies. PPP GDP is dominated by the cost of living. So PPP GDP comparisons give you an answer to questions OTHER than the size of the economy.

California’s economy is a good bit larger than Russia’s economy.

I take the alternative payments system seriously. It already exists as a competitor to SWIFT. The U.S. is alienating everybody.

Moscow started working on its own payment service, which is dubbed the SPFS (System for Transfer of Financial Messages), amid threats that it could be disconnected from the internationally recognized SWIFT (Society for Worldwide Interbank Financial Telecommunication) system back in 2014.

This is still small scale, but one can imagine scenarios in which it could easily ramp up.

https://www.rt.com/business/461958-foreign-banks-russia-swift/

“The purpose of US full spectrum military dominance is to maintain the Dollar as the world’s reserve currency so the US can simply print the money necessary to import or steal what it needs to maintain its life style”

And that’s what many fiat currency naysayers (aka cryptocurrency evangelists) don’t understand. They think such currency is supported by “nothing”. LOL It is supported by MILITARY/geopolitical DOMINANCE, stupid.

The borrowing and spending binge by Canadian households, businesses and governments (all levels) continues unabated. Growing the debt in the economy significantly faster than the economy itself grows seems to have developed into a way of life in Canada.

At the end of March, 2019 the total debt outstanding in Canada (bottom line of the Statistics Canada credit market summary data table) was $8.165 trillion. At the end of March, 2018 the total debt outstanding was $7.785 trillion. In the 1 year period from the end of March, 2018 to the end of March, 2019 it increased by $379.7 billion. This is an increase of 4.8%.

Canadian total (household, business, and all levels of government) debt numbers as of the end of March, 2019

https://owecanada.blogspot.com/2019/06/canadian-total-household-business-and.html

They dont really fit.

Isn’t the third chart down, “Household Debt Burden,” somewhat misleading following the 2008 financial crisis? American consumers didn’t pay-down their debt obligations; wasn’t there massive charge-offs? Heck, even credit card lenders enjoyed some of that government gravy, IIRC.

No, the 3rd chart is not misleading. That’s the reality of how it worked, as explained in the article just below the 3rd chart:

“But US household debts plunged during years of deleveraging after the Financial Crisis, in part by consumers defaulting on their mortgages and credit cards. Household debts didn’t start growing again until 2013. And it took until 2017 before they surpassed the pre-Financial Crisis peak.”

My point is that American consumers are just foolish.

I’ve gotta laugh. People here are too concerned about their FICO scores. They have no idea how debt will kill them.

Another big drag on Canadian spending is the carbon tax. A Canadian guy in BC did a video on his gas bill. The total was C$94 with only C$12 being for the actual gas. The rest was taxes on the C$12. Coming to a liberal/crazy town near you.

“British Columbia saw net emissions fall by 4.7 per cent over eight years after putting in a carbon tax, and for an example outside of Canada, Sweden has seen emissions fall by 26 per cent since implementing a carbon tax in 1991 alongside an existing energy tax. By comparison, Saskatchewan—which does not have a carbon tax—saw heavy increases in greenhouse gas emissions from 1990-2015.”

I will take the liberal/crazy town over Noxious Gasville, USA, thank you.

The jobs all left for China too.

Canada only imports and assembles and ships back out.

Of course emmisions will drop but so too quality jobs.

Big money is made inflating housing and markets.

Not really accurate.

Canada’s economy is resource heavy (including agri as well as mining). Those jobs are cyclical, but do not get exported overseas.

Manufacturing is struggling in Ontario, where I live, but those jobs are moving to the US and Mexico (i.e. lots of vehicle mfg here, and politics is involved).

Services industry is huge and growing though. Software in the Greater Toronto Area has been adding more (high paying) jobs per year than Silicon Valley for a long time.

@ Joe,

gee, I guess I’d better tell my 35 year old son his 200K job is shitty and left for China. Or, that my daughter and son-in-law can’t really afford their home. People that I know here are doing just fine. I don’t know how these stats are so skewed, I guess by Vancouver and Toronto numbers, but they certainly do not reflect the rest of Canada which is mostly rural.

Its easy to reduce CO2 emissions when you export Manufacturing job to China and spend Billions on uneconomical hydro electric project and pay 30 cents a liter more for gas.

BC has the highest median household net worth of around $430K Canuck bucks. That is to say, most people who live in BC are quite well off….they appreciate the wilderness and clean air, thriving high tech 21st century metropolises, and can afford it.

Contrast to Florida, which is a low tax wasteland with crumbling infrastructure.

Bring on socialized pharma-care please.

Oh no! A natural resource with massive externalities has taxes on it, and is still affordable! Whatever shall we do?

FYI — the POINT of a carbon tax is to increase the cost of burning carbon so as to encourage people to use less of it. It should be high enough that they care, but not so high that they can’t afford it.

You cant extort someone into caring

The situation is actually much worse. This number doesn’t include the 100,000+ condos being built across the country. There are not enough high-wealth individuals and/or foreign investors to save all of the local/domestic speculators from the investment properties that need mortgages over the next 4 years.

Biggest worry in planning a retirement is what will healthcare costs be in 20 years. Even if you did everything right and are free of debt, that is an unknown unpredictable expense.

Well if you are (or will be) in Medicare, you only have to worry about Part B premiums, Part D premiums (if you have stay only with Gov’t A & B) and Medigap (hopefully Plan F) Premiums. Yes you can plan for them to increase every year, but that’s inflation like any other thing while you are still alive. I hope you have a Rainy Day Fund in liquid short term Treasuries to pay for the unpredictable.

I pity the old folks who still have a long mortgage and other debt. That was the first thing I did – be debt free.

I just came back to get my meds from CVS. By Medicare Plan D option only allows me a month supply at the drugstore. To get 3 months supply, I need to agree to have my insurance company mail me the drugs. Yet, to make money or to charge me more, CVS offered me a 3 month supply over and above my monthly allocation. Be careful of the offers out there. They are not as friendly as you think.

Healthcare is free in Canada, we pay more income taxes to pay for it but the cost is still less than what Americans pay monthly for their plans, there are no deductibles to worry about and you don’t lose your coverage when you lose your job or retire. At most you may have to pay for prescriptions but that cost will be close to zero ($4 – $25 CAD per medication) if you have good supplementary insurance or qualify for lower cost drugs through provincial and federal plans.

Our biggest worry would be getting old and needing to stay in a nursing home which is not covered by the government or getting hurt while young and not having supplementary insurance to replace your income, provincial disability support programs do not usually pay much in Canada.

Retired people in the US are covered by Medicare. The taxes for Canadian healthcare are the same as any US deductible so it’s a wash. Half the population in the US is covered by government plans, then most of the rest are covered at work, about 5% go without coverage. Not perfect but far from the end of the earth.

Actually, Simply Put….If you are required to go into a care facility you pay 80% of whatever income you have coming in regardless of cost and services needed. If you have all your faculties and choose to enter a facility, the cost seems to be around 6 K/month. For example, if you are rich with dementia you would choose to go private. If you have less than 8K per month, you could enter a Govt facility or subsidised private facility (which are excellent, by the way). Most people try to stay at home with family until the bitter end regardless of income.

Our experience with Medicare Part D is that you can often find better prices by using GoodRX coupons.

Example: (This is true): My wife was prescribed an ointment that – at retail – was @ $1,400 for a 30 gram tube. We started shopping around (because that was idiotic). Through her Part D (Aetna) it was $485. I looked at GoodRX and found it at Walmart Pharmacy for $86 with their coupon.

The upshot is that we now check the GoodRX website first and rarely bother with the Part D. We have to keep it (Part D)… but it’s primarily reserved for “use by force” (hospitals) situations. The only downside is that you have to travel to several pharmacies to get the “best” prices as they vary – sometimes significantly.

I only take one prescription and use CVS mail order because the cost is only $12 for 90 days…. not worth the gas to chase $2.

Aren’t those CA mortgage holders doing pretty well on their equity? I mean more debt usually means more equity. How’s CA’s household wealth numbers stack up?

Canada did not have a financial crisis. Now you know why. The same as Chinese. They just doubled on borrowing.

Canada open pit.

The 20Y @ 1.649% < 6M @ 1.68%.

Everything in between is dug in.

Only 30Y is still slightly higher @ 1.698%.

Don’t know where you got your numbers from.

Current Mortgage rates in Canada : https://www.ratehub.ca/best-mortgage-rates?utm_source=google&utm_medium=cpc&utm_campaign=en-mtg-prospecting-search-terms&utm_term=mortgage%20fixed%20rates&utm_content=&gclid=EAIaIQobChMIyPS15YHq4gIVhEOGCh0ZXQlcEAAYASAAEgKLgfD_BwE

1) ME destructive “event” might benefit Canada.

First, the panic will send the long duration down.

The 10Y will sink < 2Y.

But Canada have oil, coal, gold and U.

ME assets destruction will throw, in a sling shot, the yield curve up.

Global inflation will popup and central banks will not be able to catch up.

2) In the US, rates from 3M to 30Y form two fat bodies, two cluster zones.

The third, is about to be born.

The second zone starting from 2008 until now, is the longest & the fattest.

Its bottom, the support line was hugging the 0% line for eight long years.

Its resistance line is the 30Y, which is tilting down.

Its front of your eyes the second zone disappear, is choked. All rates are all tangled together, mixed together, in a narrow bottleneck.

This twist signal a mess.

The third body is coming next. It might float above water. No zero Powell It will be short and condense.

Those three zones might form an inverse head & shoulders.

Interest rates will jump, and Canada will do well !

The lack of pipelines will benefit Canada. Demand will be higher, but not enough supply !!

Canada self imposed oil embargo !!

If and when that will happen : WCS – WTI will be well > zero.

Canadian debt slaves are really plain vanilla compared to Australian debt slaves. In Oz, over 50% of Interest Only loans can’t transition to Principal + Interest so these people became proper debt slaves as they will be paying interest to the banks for ever.

And to put this in perspective around 50% of the loan book of the 4 major banks in Oz is Interest Only.

Yes, it means the day to pay the bill will come but we keep on kicking the can for now.

And, no there is no limit of how many IO loans our banks can hold so they are not under pressure to move under-performing loans to Principal + Interest. If anything the opposite probably happens.

Yabbut, after adjustment for nonfinancial noncorporate business debt (Chart 5) and health care not covered by public insurance (Chart 26) there is not much difference between the Can-Am household debt to disposable income ratios.

https://www.nbc.ca/content/dam/bnc/en/rates-and-analysis/economic-analysis/special-report-11jan2018.pdf

There is a reflex to the debt crisis pain here in US by some. I will use Dave Ramsey as an example. He teaches you get wealthy by following simple plan. 1) get out of non mortgage debt as fast as possible usually around 2 years for most 2) then put 15% of income in retirement 3) pay off mortgage as fast as possible usually around 10 years. 4) Never borrow another dollar.

We will all be thinking that way by the time the next crisis is over.

I replied elsewhere, and I hadn’t followed Dave Ramsey at all, but used this same basic process. Took me 5 years to complete. Now retired, in retrospect, it was the best move I could have made…period.

Attempt to use cash rather than credit cards.

All this debt talk gives me a headache. All I know is that I’m 66, and owe 3 more house payments. That’s it, and I don’t carry credit card balances.