And other juicy banking nuggets.

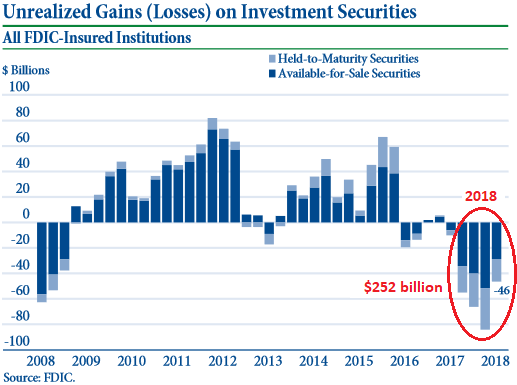

Net income in Q4 2018 among all 5,406 FDIC-insured banks and thrifts more than doubled year-over-year to $59 billion, due to “higher net operating revenue” and “lower income tax expenses”; and full-year net income rose 44% to $237 billion, the FDIC reported today in its Quarterly Banking Profile. But over the same period, “unrealized losses” on investment securities – losses that are not included in the “net income” figures above – ballooned to $251 billion, the largest unrealized losses since 2008.

“Unrealized losses” are losses on securities that dropped in value but that the banks have not yet sold. In other words, they’re “paper losses.” Every quarter in 2018 brought steep unrealized losses: Q1: $55 billion; Q2: $66 billion; Q3: $84 billion; and Q4: $46 billion (chart via FDIC, red marks added):

Banks designate these securities either as “held-to-maturity” securities, valued at “amortized cost” or book value (light blue in the chart above) and “available-for-sale” securities valued at “fair value,” such as market value (dark blue).

These securities holdings are concentrated in bonds. When yields rise, as they did during much of 2018, bond prices fall. This is where a large part of these losses come from.

When banks hold bonds to maturity, the bonds are redeemed at face value, and banks are paid face value for those bonds. If banks didn’t pay a premium when they bought those bonds, they will not lose money on them, and the “unrealized losses” go away. Also, if bond prices rise, as they have been in the current quarter, some of the unrealized losses will be reversed.

But if banks are forced to sell those bonds during a liquidity crunch, as happened during the Financial Crisis, the “unrealized losses” become real losses.

Other juicy banking nuggets from the FDIC:

Banks gobbled up US Treasuries: In Q4, banks added $93 billion to their securities holdings, bringing their securities holdings to $3.72 trillion. That $93 billion included $55 billion in Treasury securities, the largest dollar increase since Q4 2014. Their total Treasury holdings now amount to nearly $500 billion!

Total assets rose by $270 billion among those banks and thrifts, to $17.94 trillion, the most ever.

Declared dividends in Q4 rose to $52.7 billion, the most ever.

Average cost of funding – total interest expense paid on deposits, bonds, and other borrowed money as a percentage of average earning assets – rose to 0.91%. This is still so low because a lot of deposits earn zero or close to zero in interest. However, it’s up from 0.54% a year ago.

Net interest margin in Q4 rose to 3.48% the highest since 2012. In other words, banks have raised the interest rates they charge on loans more quickly than their cost of funding has ticked up.

Banks set aside $14 billion in loan-loss provisions in Q4. These are losses that banks anticipate they’d experience on their loans. It was the largest amount since Q4 2012. About 40% of all banks reported increases in their loan-loss provisions.

Net Charge offs were $13 billion from loans banks deemed uncollectable. From Q3 to Q4, charge-offs for credit cards increased by $348 million and for commercial and industrial (C&I) loans by $523 million. For other categories, including mortgages, charge-offs fell. And overall, charge offs ticked down a little from Q3.

Loan-loss reserves rose by $1 billion to $125 billion in Q4 from Q3. This increase is the result of banks charging off $13 billion and setting aside $14 billion in new loan-loss provisions. 58% of the banks increased their loan-loss provisions.

Loans 90 days or more past due declined by $1 billion in Q4 from Q3. This quarter-over-quarter decline was mostly a result of two opposing factors: declines of past-due balances on residential mortgages (-$2 billion) and C&I loans (-$554 million); and increases of past-due balances on credit cards ($1.6 billion). These rising credit card delinquencies are starting to crop up everywhere.

So, it’s still a good time to be a bank – especially since $251 billion “paper losses” don’t need to be included in net income. But loan-loss provisions are starting to indicate that the credit cycle has turned, and that banks are preparing little by little for the next phase in the cycle.

Unless there is a sudden catastrophic event, hiring trends don’t go from awesome to shitty in just one month. Read.… Why I’m Not in Panic Yet About the Lousy “20,000 Jobs Created”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Financial Accounting Standards Board (FASB) voted yesterday to let banks ignore market prices for assets if they judge the market is illiquid and that the most recent sales are being done at firesale prices by distressed sellers. There will also be changes to allow banks to book smaller losses on impaired assets that are available for sale, which could take extra pressure off many of the biggest banks in the US.

April 2009

https://www.independent.co.uk/news/business/news/us-suspends-mark-to-market-rules-on-bank-assets-1661117.html

How about the more than 2 trillion on ZIRP bound Treasuries bought from 2009 to 2016. They are liquid. Yet they have lost a lot of value.

Trying to find what securities are used for HTM vs AFS, and if they can simply change the label on those they hold. The closest I found was

https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/46750353

plus Wolf’s numbers that suggest government securiries and highly rated bonds are used as HTM . What comment in that article suggests is that banks can get zombified with HTM maybe. The way policy and CB involvement is open to influence bank behaviour e.g. bananas’ example suggests that they are mostly covered whatever they do.

This is a good overview of EU NIRP, its effects on bank balance sheets and lending practice, in Spanish but the research papers in English would be searchable

https://www.eleconomista.es/empresas-finanzas/noticias/9755644/03/19/El-balon-de-oxigeno-del-BCE-que-permitiria-respirar-a-la-banca-pero-sin-lograr-el-alta-medica.html

The theme is on how EU banks might have their earnings improved by raising interest on excess reserves (1.2t), and how the “credit trap” of increased commissions and higher lending standards being used to offset low carry profits might be overcome – the theory to that is that banks are actually avoiding being productive lenders because they are ending up with reserves that are punished, which is some kind of counterintuitive direction that might not be as true as suggested – northern banks… err DB?… are said to be more in this circumstance, ergo they want paying for their reserve? They like this stealth approach in EU where you are watching the wrong hand the whole time, so the above analysis has some merit – subtle background adjustment that greatly changes the financial environment. Basically they are talking a tiered negative rate on excess reserves. Something to mull over anyway as it is going to take quite a bit of reading to actually get a clearer picture of how it is all laid out in those terms.

My understanding is banks get to shield changes to “hold to maturity” from the income statement and reserve calculations. I kinda understand this, but I’m real uncomfortable with the way this is implemented (it can probably be manipulated).

Apparently, non-financial companies (example: Berkshire Hathaway) do not have this “hold to maturity” safe harbor, and their income statements are whip-sawed by valuation changes. Undoubtedly, both industrial & financial firms need to disclose changes to so-called “hold to maturity” investments (example: real estate book at original cost), but the current system is a mess.

I think I’m coming around to advocating a 4th financial statement (addition to balance sheet, income statement and cash flow) focused on investment portfolios of whatever stripe. Potentially, this could apply to all financial companies and industrial companies of a certain size with material investment portfolios.

This hypothetical 4th statement might also be used to catch off-balance sheet items as unexpired leases (retail stores trip over this) and various real estate booked at original cost (old-line supermarkets trip over this). Investors deserve to know what’s there, so the more transparency, the better.

Wolf,

Many thanks. Great stuff.

Cycle indeed has turned but the non-banks seem not to notice. Sub-prime auto loans still going strong. Credit Acceptance Corp in fact reduced its loan loss reserves by more than 50% from 2017.

Cost of funding still sub 1%? Fed needs to get to work and keep hiking.

If you follow rcwhalen, he shows the big banks cost of (wholesale) funding at around 1.5%

The risk is real in junk… here are some plots you may find interesting.

distribution of underlying trading above/below par from august 2018 semi-annual of HYG: https://ibb.co/QCJp5Tt

log normal returns and log normal bid ask spread of HYG from sept18 to present on the ~30 sec time frame (notice the regime change in spikes after sept): https://ibb.co/VCycFzW

I may be horribly unfair to “non-banks”, but my stereotypical view is an industry run by ex-used-car salesman and real estate appraisers, only focused on next-week’s commission check.

These not-quite-Harvard-MBAs will take whatever funding they get and push the limits until the whole $300B industry goes over the cliff, fancy mag wheels and all.

Even then, some will stand around looking at the rubble pile asking “How in the world could we have let this happen?”. It’s one thing for crazy rich people to play these games as individuals; it’s quite another thing for Joe-six-pac’s pension fund manager to be investing other people’s money here. Unregulated non-banks should be off the table.

Wolf

I posted on the wrong topic – ok with me if you delete erroneous post

Wall Street’s FIC income has been going down.

Meanwhile, regulations have been emphasizing more and more government securities for HQLA. Just look at the money market and the repo market. They are mostly in Treasuries.

Where did the “debt cushion” go?

More companies with low credit ratings are limiting loans to those that will be paid first in a bankruptcy. Junior bonds and loans absorb losses first. This is a debt cushion for investors in first-lien loans.

Roughly 27% of first-lien loans are backed by companies that don’t have junior debt outstanding. This is the largest share going back to 2007 when it stood at 18% and we all know what happened in 2008!

Banks’ exposure to Derivatives may be the biggest risk. And that risk is difficult to quantify. Since everything is linked globally these days, it’s not hard to see how contagion could spread very fast to all parts of the world.

Decade After Crisis, a $600 Trillion Market Remains Murky to Regulators

https://www.nytimes.com/2018/07/22/business/derivatives-banks-regulation-dodd-frank.html

(I hope I posted this link correctly)

CDOs. Good guess though.

Don’t tell anybody. It’s supposed to be a surprise.

CLOs. Sorry. CDOs were last time.

How much longer can we go? :-)

There was supposed to be an image there

https://i.imgur.com/UucuEJw.png

Excuse my ignorance but this seems to be a Catch 22, banks own bonds as their principal assets which decline in value as interest rates rise, while their primary source of income is interest received. Thus the value of the assets decline as their income should be rising to offset the losses. Seems like a heck of a small needle to thread, one small jolt and…well let’s hope they can unload bonds with the most downside before any jolts occur.

FASB 157 became effective in 2007 and the timing was remarkable to say the least. If you would like more information just google FASB 157. Here’s a good link to start with:

https://financetrainingcourse.com/education/2010/07/fas-157-fair-value-accounting-and-level-3-assets/

Pay close attention to level 3 assets “mark to management”.

My M.B.A. at Wolfstreet .com continues.

Everything looks good.Banks great,jobs great,

heloc’s being paid down etc.The only thing I can see

going wrong is if we choose to stop buying because

we have all we need.

Those bonds can lose value without rates going higher, during the past fifty years of debt expansion the supply of bonds rose along with price, it will work the same way when it unwinds.