The price of rising interest rates.

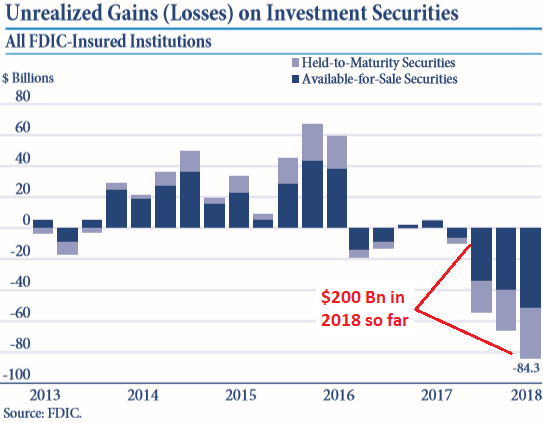

The FDIC just released the aggregated third-quarter performance metrics of the 5,477 banks and thrifts it insures. The amount of their combined assets ticked up to $17.7 trillion. These assets – mostly loans but also investments of all kinds – include $3.6 trillion in securities (not including the securities in their trading accounts). And banks got hit by the biggest quarterly losses on those securities since the first quarter of 2009.

Banks designate these securities either as “held-to-maturity” securities (valued at “amortized cost” or book value) and “available-for-sale” securities (valued at “fair value,” such as market value). For Q3, these were their unrealized losses – meaning, banks have not yet sold the securities:

- Available-for-sale securities: $51.5 billion in unrealized losses, or 2% of their amortized cost, as the FDIC said, “the highest loss level since first quarter 2009.”

- Held-to-maturity securities: $32.8 billion in unrealized losses.

- Both combined: $84.3 billion in unrealized losses.

Note the damage done in 2018, after years of big gains: $83.4 billion in Q3; $66.4 billion in Q2; and about $55 billion in Q1; for a total so far this year about $200 billion in unrealized losses.

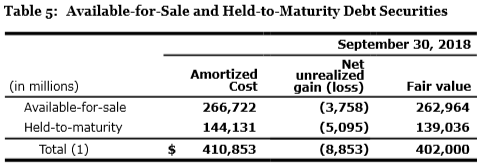

Not that this is a huge surprise. For example, Wells Fargo disclosed in its 10-Q filing for the third quarter that on its over $411 billion in available-for-sale and held-to-maturity security holdings, it suffered total unrealized losses of $8.85 billion so far this year. This includes net unrealized losses of $3.76 billion in available-for-sale securities and net unrealized losses of $5.1 billion in held-to-maturity securities (image from Wells Fargo 10-Q):

Wells Fargo explained that it was its $411 billion of available-for-sale and held-to-maturity debt securities, such Treasury securities, municipal bonds ($54 billion), mortgage-backed securities, corporate bonds, etc. that decreased by “$8.6 billion in balance sheet carrying value” since the beginning of the year. The reason: “primarily due to higher long-term interest rates.”

This $8.6 billion decrease in “balance sheet carrying value” largely bypassed the income statement.

Bond prices fall when yields rise; and in 2018, yields have ticked up across the yield curve. The weighted-average maturity of Wells Fargo’s available-for-sale debt securities was 6.2 years. So, with the 10-year yield rising from 2.4% to 3.05% over the nine months – a move of just 65 basis points – it nevertheless sent Wells Fargo’s unrealized losses soaring.

And as the FDIC data shows, with banks having incurred $200 billion of unrealized losses so far this year – of which $8.6 billion stem from Wells Fargo – it is not bank specific. All banks have this issue.

If banks don’t sell these securities but hold them to maturity, they will be paid face value at maturity. In other words, those unrealized losses dwindle and then disappear as the maturity date approaches, even under rising interest rates.

This assumes that there is no default or other impairment. But if those securities default, banks will take a loss, classified as an “other-than-temporary impairment” (OTTI).

Currently, defaults are still rare, as credit is still easy, rates are still relatively low, and investors are still chasing yield. So most companies, even risky ones, are not yet having trouble refinancing their maturing debts or borrowing more to make interest payments. And losses for bondholders are low at this point.

But credit has started to tighten a little. Parker Drilling is an example of what happens when the market loses interest in refinancing a company’s maturing debt. Parker Drilling has unsecured bonds that mature in August next year, but the credit markets lost interest. Unable to service and roll over this debt, Parker Drilling filed for bankruptcy. Holders of those unsecured bonds will get cents on the dollar. If a bank holds any of those bonds, it would have to take a loss on them. But this is still a rare case.

Wells Fargo confirms this. So far in 2018, it wrote down its debt securities by only $23 million due to “other-than-temporary impairment.” These OTTI losses at banks rise along with rising defaults among corporate and municipal debt, but this hasn’t happened yet.

Treasury securities that Wells Fargo holds will not see a default as the US government always has a buyer-of-last-resort in the market (the Fed). The only possible reason for a default of Treasury securities would be Congress’s refusal to lift the debt ceiling at the last moment. But not even Congress is that stupid.

So, losses on Treasury securities that are held to maturity are only temporary and will reverse as the maturity dates approach — during times of smooth sailing. However, if the bank is forced to sell those Treasury securities and other high-quality securities at fire-sale prices, as it might be during a liquidity crisis, which is what happened to some banks in 2007 through 2009, it may incur sharp and permanent losses on the securities it has to sell. These losses, in stressed times, can then combine with losses from other corners of the bank’s operations and balance sheet into a very toxic mix.

Something’s not right: Banks are heavily exposed to record business debt as credit quality deteriorates. Read… US Bank Stocks Spiral Down

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, we need to have a frank conversation here about your psychic/fortunetelling banner ad service.

It is yet again providing promotional commentary on your articles, as well as mercantile advising to the aforementioned banks. The banner-ad slogan conveying this eerily-prescient warning reads thusly, warning the banks:

“beware the impending apocalypse, **IT’S LIKE A POWER WASH FOR YOUR BOWELS**”

Don’t believe me? https://imgur.com/MvlsfJu.jpg

I get some stupid “pop-in” thing at the bottom of the page from “Ninja Casino”, That, frankly, idiotic-looking scuzzbag (Ken Fisher?) from “Fisher Investment Norden”, Something about Something bankrupting America and the “Number 1 Czech Dating Site” with young women just gagging for meeting older men – or so it says. There is also an add for an iPhone card-reader, which actually is a legit product (seen those), don’t know about the service though.

So, “The Machine” knows I am older since there are 2 ads about getting my pensions “leaned up” by experts and secret reports. There are those Czech women with a little too much plastic applied. I also do gamble. But only on stocks, horses and derivatives. I think that “hit” is random since the Casino / Betting crap is everywhere.

So much for Big Data!

—-

The “Power Wash for Your Bowels” reminds me of that time I consumed a 750 gram container of prunes in one setting.

Maybe that’s the feeling of writing a ton of naked puts on the reasoning that: “The FED/PPT has the markets” and then there is a 10% down day :)

The Power Wash is standard prep for a colonscopy. It comes with a packet of lemon flavoring, which real men do not use.

> “The Machine” knows I am older since there are 2 ads about getting my pensions “leaned up” by experts and secret reports.

Not necessarily. I’m decades away from social security bennies yet I still get spammed with ads peddling advice about it.

I often reply to those emails from Russian babes with gorgeous photos of them. I tell them that they are far too fat and I am into anorexic women and really into scatophilia.

I usually get a reply a couple of days later with more photos thanking me for the sweet things I said to them and how age doesn’t matter.

I ask myself are these Russian girls really up for anything or is it an automated email???????????

Hahahaha, this stuff just cracks me up. If you look at ads with a sense of humor, in the context of my site, as you did, this is some of the funniest stuff out there.

As-bo-lute-ly! The sad thing is that there are enough out there as dim as the big-data algos to make the whole process pay for someone. (Of course, I’m fine with them providing their unwittingly lighthearted sponsorship of this always-excellent site!). A better day to us all.

I find the ads funny, too. Except for the Ashley Madison ones. That company is a pet peeve of mine for reasons I won’t go into. Other than that, love the site and your insights.

my ad says ” The Deep States plot to BANKRUPT America – Click here” These ads are always amusing.

I have this one too. I think it’s site-related, not user-related.

Of course, deep state superfluous in the current serious effort to bankrupt America. :)

Didn’t realize this site had ADs! I use an AD blocker.

Bad Boy! You’re eating my lunch (WOLF STREET is free, and ads are how I get paid). At least don’t brag about it :-]

Alternatively, if you block the ads and still want to support WOLF STREET, you could locate the “How to Donate” tab in the navigation bar. Yes, you can use your credit card. Much appreciated :-)

Sorry bro! Made a small donation to offset my adblocker use.

Thanks!!

You are missing some of the craziest and funniest ads on the Internet.

The dating sites from Eastern Europe are almost as hilarious as the “power washer for your bowels”… I really hope nobody takes that advice literally.

The other day, Bloomberg had an article about the Fed losses on 4 trillion of securities if it was marked to market. It would make the Fed insolvent.

Think about all the primary dealers and the banks. They probably are insolvent, too.

Looks like moving forward, holding short term Treasuries at less than 3% is the best we’ve got.

The Fed cannot be insolvent. It is the creator of money. For the same reason, I doubt the primary dealers would ever be allowed to become insolvent. If they were forced to sell depreciating assets, I’d expect the Fed to just step in, print some money, and buy those assets at par. Just like with QE. Which is why US treasuries are always the safest asset to hold.

I think this is the article:

https://www.bloomberg.com/news/articles/2018-12-12/fed-piles-up-66-billion-in-paper-losses-as-it-faces-trump-wrath?srnd=economics-vp

It is true the Treasury and the Fed can print all they want and INFLATE the heck off the value of the US Dollar. I wonder how safe that is.

I worry about this since my investments now are almost all Treasuries.

The Fed holds these bonds to maturity. When they’re redeemed, it gets paid face value. Unlike banks in a liquidity crisis, the Fed can never be “forced” to sell those securities at fire-sale prices. The mechanics of the QE unwind were designed on purpose to not trigger actual losses. So in this respect, the Fed is off my worry-list.

The FED can inflate the price of basic necessities such as housing out of reach of first time buyers, but it won’t effect the exchange rate of the dollar much. The whole world is a bigger trashcan than the US is, thanks to successfully exporting the model to the world. Now, I have to take my anti-depression pills.

https://www.alhambrapartners.com/2018/12/11/us-banks-havent-behaved-like-this-since-2009/

The banks have been stockpiling liquid assets while their business has been in decline but Snider also points out the great bond bear never materialized because banks were saying one thing and doing another. As Wolf points out the paper held to maturity has face value, but if the meager rise in rates has destroyed the M-M basis in their paper (rendering it illiquid) imagine what happens when rates really rise? Okay we won’t go there.

This is when a “trader” becomes an “end user.” When you cannot afford to sell and instead have to hold till maturity.

They sometimes call that “orphaning” a bond.

Were not all of these theorerical, paper (unrealized) losses inevitable once interest rates began to rise? A decade of virtually zero interest rates in effect slowly poisoned the whole system. It seemed great at the time, but you did not have to be clairvoyant to see the outcome.

Wow, you had me at Parker Drilling. Hard to imagine an 80 year old drilling company, in the glorious age of fracking, having to file bankruptcy. Here’s a headline from 2011:

“Parker Drilling Gets The Knack Of Fracking, Stock Eyes New Highs”.

So what does this tell us about the future of the much ballyhooed U.S. oil and gas fracking industry, when Parker Drilling’s bonds get a massive no confidence vote?

Shale oil is a scam that’s why is going bankrupt. Shale oil is only profitable when oil is about 100 bucks a barrel. The fact they convinced so many idiots to keep fracking when oil went under 80 bucks shows you how much Cool Aid they drank. No wonder they are starting to drop dead.

Isn’t Telsla the same thing? Without FED created environment for mal-investment, none of these will able to survive. But you have to look at it another way. The Chinese are building empty buildings for the same reason as to keep the economy going even when there is NO profit to be made. At least Telsla and Fracking advance techinologies which is much more productive than empty buildings. These wasted malinvestment may turn into something useful in the future. Empty buildings may be utilized in the future as well but if you ask me to pick where to waste money, Inwould rather pick technologies.

Many years ago while receiving training and instruction in Tang Soo Do, an important lesson was learned: “Never underestimate your opponent.”

With this echoing in my mind, I read one of the best sentences I can remember, “But not even Congress is that stupid.”

Damn, now a scene from Forrest Gump is flashing back …

Wolf that graphic shows that things started to suck since last year, not this year. This year just increased the loses to tsunami levels of suck.

Yes :-]

“The world is ending, the world is ending”, shouted Chicken Little from the farm. But no one could hear him because he was just a small voice in a So. Dakota farm in Montgomery County Rural Route 113. Eventually his message will be heard in Times Square and will be heralded by both the Mayor and Governor of New York. Oh, it IS happening, the fissures are becoming fault lines and soon, very soon CL’s voice will be heard, but will it be heard too late ? History confirms an affirmative on this one…..

I would think that shadow banks look similarly dismal?!

When the bank on the corner closes where do you go? The loan shark.

Same guy. Bank and loan shark.

Good to see that you are no longer chanting the “banks are safer” mantra, Wolf.

Still waiting to see you put up that long post I wrote here about the far too low capital-leverage ratios in the biggest banks, especially Goldman Sachs, why the Fed’s safety tests of the big banks are absurdly too easy, abd how Dodd Franks has been gutted this past year.

I’ve concluded that focusing on this issue of “will the Fed keep raising rates and unwinding QE” is missing the Big Picture, which is that once again, it’s our banking/financing system that’s going to set off the next big crash

Your perception is wrong. Nothing I’m saying here indicates any change. What I have been saying, and what I still say, and what all the data shows in minute detail, is that banks are much better CAPITALIZED than they were before the financial crisis. This means they can take bigger losses without collapsing.

I never once said banks were “safer”. Big capital cushions make them safer, BUT other things make them less safe. “Safer” is the totality of what banks do. For example, their mortgage lending practices are more conservative than they were before the financial crisis. But their derivative books may be riskier — we don’t know that, but we know for some banks, they’re bigger.

So talking about banks being “safer” includes the totality of their actions, and I have no opinion on whether that totality is better than it was before. I know some parts of it are better (capital buffer, mortgage lending, credit cards at big banks); and some parts are worse. And I know that banks can take much bigger losses than before.