US bank stock index down 17% from January. EU bank stocks crushed, crushed, crushed since Financial Crisis.

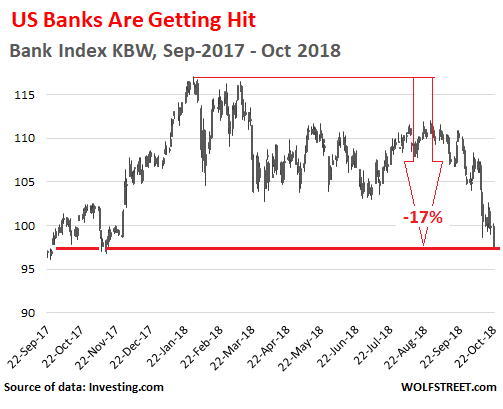

Monday early afternoon, the US KBW Bank index, which tracks large US banks and serves as a benchmark for the banking sector, is down 2.5% at the moment. It has dropped 17% from its post-Financial Crisis high on January 29. If the index closes at this level, it would be the lowest close since September 18, 2017:

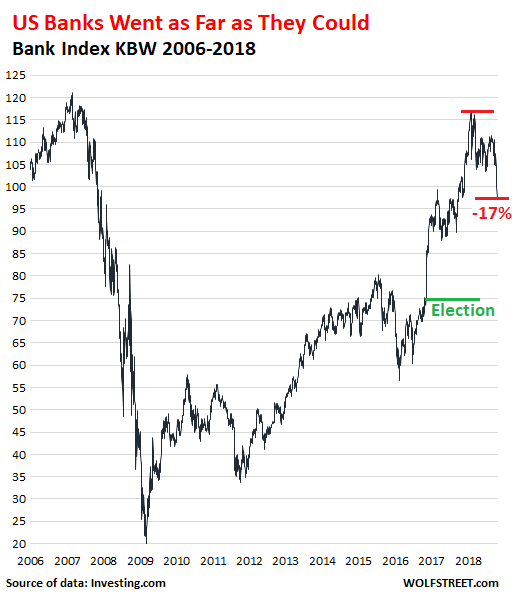

While that may be a nerve-wracking decline for those who have not experienced bank-stock declines, it comes after a huge surge that followed the collapse during the Financial Crisis:

The second chart is on a different scale than the first chart above. So this year’s decline is small fry compared to the movements since 2006, including the dizzying plunge toward zero in early 2009, and the subsequent boom when it became clear that the Fed would pull out all stops to save the banks with all kinds of mechanisms, including ruthless financial repression – forcing interest rates to 0% – that it waged on depositors and savers for a decade. Profits derived from these mechanisms effectively recapitalized the banks.

The 55% jump in bank stocks after the 2016 election through the peak in January 2018 was a reaction to promises for banking deregulation and tax cuts from the new Trump administration along with signs of lots of goodwill toward Wall Street, as top positions in the new administration were quickly being filled with Wall Street insiders. However, the “Trump bump” for banks is now being gradually unwound.

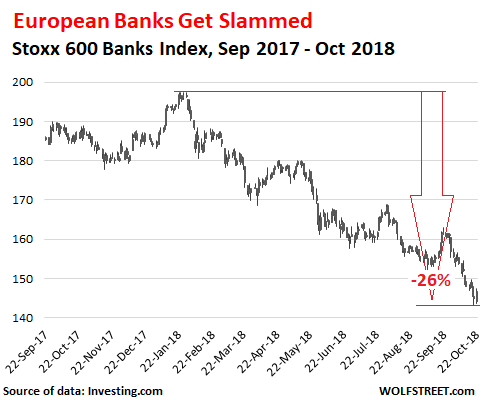

But unlike their American brethren, the European banks have remained stuck in the miserable Financial Crisis mire – a financial crisis that in Europe was followed by the Euro Debt Crisis. The Stoxx 600 bank index, which covers major European banks, including our hero Deutsche Bank, has plunged 27% since February 29, 2018, and is down 23% from a year ago:

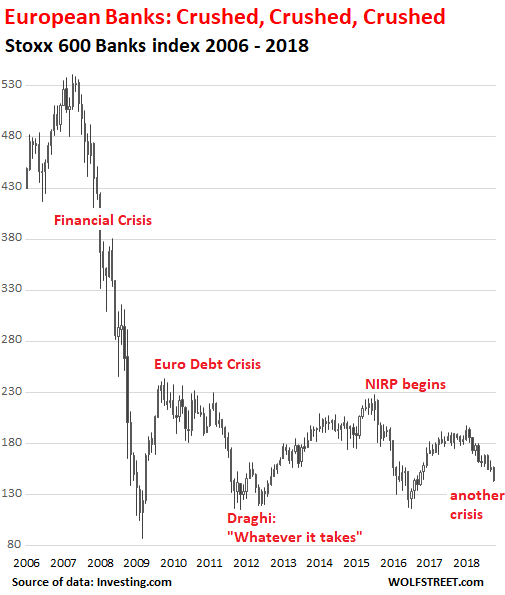

But note how minuscule this year’s 26% drop is in the overall collapse-scenario in the chart below going back to 2006: The Stoxx 600 Banks index never got anywhere near recovering after the Financial Crisis, as after each hopeful partial recovery, it kept falling off the wagon, and is once again falling off the wagon:

It’s not exactly a propitious sign that the banks in the US, after nearly recovering to their pre-Financial Crisis highs – “Close, but no cigar!” – are once again turning around and heading south as the Fed is “gradually” removing accommodation, which results in higher funding costs for banks and greater credit risks on outstanding loans.

And the European banks remain a mess and have an excellent chance of getting still get messier.

Why does this sell-off smell different? Read (or rather listen to)… THE WOLF STREET REPORT

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I thought Net Interest Margin for US banks was increasing, has this changed? New loans are going out at higher rates; most depositors are still getting near-zilch.

http://www.bankregdata.com/allIEmet.asp?met=NIM

Net margin is made up two factors: Cost of funding for the banks and interest rates charged by the banks. Check your credit card interest and see how high it is. Then subtract your bank’s cost of funding, and you’ll have the bank’s net margin on your credit card.

Yes, and the link I provided shows the actual reported NIM from the regulatory call reports for each bank.

NIM has recently been rising, not falling, as banks are charging more for new loans while avoiding raising rates paid out to depositors – except for the savvy tribe of certificate-of-deposit shoppers here!

Earlier articles pointed out that banks will run into issues when the yield curve inverts, because the cost of new deposits (short-term borrowing by the bank) starts to exceed the income from new loans (longer term lending by the bank). And rising rates pressure the shorter-term side of the bank balance sheet first. Independent of the yield curve, banks also run into issues when loan quality deteriorates because enough overextended borrowers get in trouble and can’t pay. And so on.

Since today’s article shows stock prices rolling over (or, in Europe, flat-out “playing dead”), is it fair to infer that investors have doubts about future NIM, or about credit deterioration? The call reports available from the regulators are typically stale data, so I was wondering if anyone had fresher data from the recent wave of bank earnings reports? Are delinquencies up?

Otherwise, another scenario for the US banks is that it’s the European banks that are in deep trouble, while the US banks are still fairly healthy, and the US selloff is due to spillover risks from Europe e.g. Yankee / Eurodollar bonds etc.??

Paribas owns The Bank of the West, also owns a lot of Turkish debt denominated in (rising) USD, when the daisy chain breaks FDIC bails out who exactly?

You really have to dig into a particular banks balance sheet quite a bit to get a read on NIM expectations. Frankly, I am surprised how slow the deposit repricing is, but they manage deposit cost much more closely that customers manage deposit income. How else can they be getting by with these deposit betas < .50? A fool and his money … They also hedge rate risk.

As of August Consumer lending delinquencies and losses are down slightly Yr/yr if mortgage lending is included. Auto is down slightly yr/yr. Card is up yr/yr, but remains healthy and below historical norms. Mortgage delinquency and losses are down rather sharply yr/yr and lower than any point since 2006-2007.

LOL. I couldn’t care less what my credit card interest rate is. I pay the card off immediately after the charge hits the card; all they get is the transaction fee between the vendor and the cc company, and no interest at all from me; in my world, I’m known to the banks as a DEAD BEAT. LOL.

They probably break about even on those of us who never pay a fee outside of the money they make on transactions and annual fees.

Then we probably double as good advertisement for their cards to hopefully the next person who may pay some fees.

Don’t be so sure about that. Used to do a few direct to retail sales in a manufacturing business I owned. After the first year of great sales the card merchants jacked our fee from 2.5 to 4%. When we asked what was going on they said too many of our customers were using platinum cards and they needed to cover the rewards on these! Basically said take a hike if we didn’t accept it as they couldn’t otherwise make money.

Bottom line is that you are basically letting them cream 2-4% of all your spending if you use them.

It is a genius system. Those ultimately paying for the scam put pressure on the retailers to have to use the scam merchants because they want a free electric kettle every couple years.

The problem is that these are no longer the banks from an old black-n-white Jimmie Stewart movie that make money by collecting deposits and then making loans on that money.

Another blogger recently wrote a piece on the current media hype about how bank stocks go up when interest rates rise, and she included the statement “When it comes to five of the mega Wall Street banks – JPMorgan Chase, Bank of America, Citigroup, Goldman Sachs and Morgan Stanley – you can throw that advice out the window. That’s because these are not so much banks as they are black holes of interconnected and concentrated interest-rate risk with trillions of dollars of derivatives sitting on their balance sheets.”

Why do I keep hearing that I should buy bank stocks in a rising interest rate environment?

Won’t they be lending out money at higher rates?

You hear this because someone wants to sell you their bank stock.

Banks are stupid, too slow to change and they tend to accumulate failed cookie-cutter investment schemes they cooked up themselves in the latter stage of a boom: Thus they end up eating their own dog food and choking on it.

I am looking for Deutsche Bank to go through 9 EUR a share. Then it could go all the way down to maybe 3 EUR.

Why not buy it then? It won’t go bust, it is “systemically important”, nanny state will come and change it’s diaper. Then it will have another run.

I’ve heard that phrase coming from shareholders of the following companies: Alitalia, Areva, Sabena, Bipop and many others.

“Don’t worry, the government will step in”. And it did step in. Time and time again.

What were the results for shareholders? Unless you engaged in short-term speculation, you would have been wiped out once dip and panic buyers started cashing in their cheques.

Deutsche Bank will eventually meet the same end as any of these companies: it will either become a moribund ward of the State or will be “reorganized”, meaning it will be broken up, the best bits auctioned off and the rest dumped upon taxpayers. A takeover is unlikely, as Commerzbank has so far resisted successfully all attempts by politicians to force them into such a suicidal move.

You can look at Alitalia for what will happen: sure, the government won’t allow it to meet its fate, but shareholders have been systematically ground into dust. The only reason to buy those shares is when they are cheap enough and there’s a periodic bailout/reorganization/forced merger on the horizon. Watch the panic buyers do their magic and dump your shares upon them before they go back to where they belong.

Sure, but, banks are different critters: “Eventually” will (IMO) be happening on such a long timescale that it does not really matter to anyone.

There is just too much risk held by DB to unwind. “They” will surely avail themselves of the opportunity to flush some of it under the convenient cover of a hard Brexit, then their book will be golden for another 3-5-6 years.

I won’t mention another “systemically important” bank, which is in a mess of its own making, by name since last that got my post deleted.

That one is an un-flushable turd, swirling the drain, yet never going down and alway popping right back up again to menace the bowl. I think we call that kind of stock for “cyclical”.

So far this particular smelly dog has yielded four solid runs of between 100-400% on 3 stealth-bailouts and 1 official since the 1980’s. Another one is certainly coming once they figure the fix (assuming the DOJ does not pull their USD clearing, of course, in which case they finally go down and join the rats).

Good imagery, fajensen. Thanks. Brings this lofty thinking right down to earth.

Don’t the rate hikes now using IOER (Interest On Excess Reserves) that were created using Fed’s QE? About 2% interest on $2 trillion excess reserves means approximately $40bn that the banks are earning for free thanks to the Fed. Shouldn’t more rate hikes result in more profits for the banks? What am I missing?

Sreeni, I believe the rate the Fed pays for IOER is not in any way linked to the rate-hiking it’s doing with e.g. overnight rates – IOER was simply fixed at some low-but-non-negligible rate a few years back, and that rate won’t change unless the Fed mandarins decide it should.

Not true. IOER data is available and tracking the Fed Funds rate upwards. Currently 2.2%.

The size of “Excess Reserves” is dropping, however, as the Fed sells off its excess Treasuries via QT – which Wolf reports on thoroughly. So in a couple of years these money-for-nothing handouts to the banks (which ought to be totally illegal) will finally stop. Unless there’s another crisis.

https://fred.stlouisfed.org/graph/fredgraph.png?g=lHBd

Excess Reserves have plunged by close to $1 trillion since their peak in 2014. They’re now down to about $1.74 trillion.

Any time market cap and book value differ significantly, the loan quality numbers are prime suspects. Nobody truly believes the loan quality numbers.

Regulatory fudges have been made as to how & when loans need to be classed as non-performing & written off. Credits can be shuffled into obscure portfolios (with regulatory agreement).

US banks appear generally better capitalized and regulated than the dangerous floating crap game called “EU banking”, but investors simply don’t believe the numbers.

A good first step would be to rigorously classify & disclose loans so investors could evaluate the new level of risk against the current capitalization. Even so, US banks would almost assuredly come out looking better than EU banks.

Given bank behavior over the last 20+ years, banks simply don’t have much credibility.

Is this true while p/b is greater than unity (as many have been for some time and still are)?

Accounting rules are always in a state of flux or should I say tide that washes women and children out to sea….

Have to point out that this chart is not the case for Canadian banks. More like the reverse. RBC was C$ 65 in April 2013, now is down from a high of 110 to 98.

Nor has there been any need for a bail out. (Unknown to most Canadians, US FED money was made available to Can Banks but was not needed)

OK, no doubt a hit is coming with real estate and Helocs, but this overlooks the big factor: the Canadian sector is a very profitable cartel.

The vast majority of Canadian banking goes through 6 institutions.

The US economy is about ten times larger, but there aren’t 60 US banks there are about 4500.

Outside perhaps of gun sales, there is no other US retail business with 7 times the exposure relative to GDP.

Does this mean there is a lack of competition? For a small business loan,

probably. For a mortgage, they sure seem competitive: they make house calls etc.

But in general, there is probably a cultural preference for banks that are very conservative, even at the expense of some lost opportunity.

No one lost a dime in a Canadian bank during the Depression, when almost ten thousand US banks went under.

Part of the reason they went under: there were more than ten thousand. However, the point is not a critique of the US banks. It is that the barrier to entry is very high in Canada and their earnings increase year after year. If you want to buy on the dip you could do worse.

But maybe not on the first dip.

Because of the leverage employed, all banks risk insolvency but are viable because of government guarantees to depositors and shareholders, as 2008 demonstrated. And Canadian banks are no different, despite their oligopoly.

However, remove the sovereign put and they’re toast when the next “2008” occurs. Why? Because sovereign credit has, more than likely, been fully employed. “Da boyz” might fire up the printing presses to hyper drive to bail themselves and the banks out again, but that will only result in destroying the currency. So yes, you can buy the dip in the next crisis but the ensuing gains might buy you a dozen eggs.

Sorry,forgot a main point: the dividends. All the big 6 pay good,VERY regular dividends. From 2004 to 2014 the total return on RBC was over 14 % per year.

Good comments Nick!! Even Cdn Credit Unions are quite conservative. I remember when I went for my first mortgage at the credit union in Powell River. I couldn’t get one as they had already used their allotted funds for mortgages for that year. It meant RBC for about a decade until I switched back to credit unions around 1990.

regards

A little story slightly off topic (with apologies).

Last week I went to Bank of America’s branch office to open a checking account. The branch manager is a funny woman and the only reason I’ve been banking there for decades. I joked about the days banks would give stuff like toasters as incentive to open savings accounts. She sighed “yes, those were the days”.

We talked about the salaries of employees not keeping up with inflation. I told her that Brian Moynihan (BoA’s CEO) made $20.2M in 2016. She said, “If you came here to make my blood boil I’m going to switch your checking account to a $15,000 daily minimum”.

The English language doesn’t have profanities that match the obscenity of the plundering of corporations by their executives.

Old Dog,

Here’s a little more data for why BofA employees are more than a little peeved. And why anyone who has an account at BofA that’s not paying interest should be as well.

Over the last 10 years BofA has done 20 Billion in buybacks to keep the stock price inching up.

BofA has paid approximately $53,000,000,000+ (yes that is trillions,) in penalties since 2008. (This includes Merrill Lynch and Country Wide.)

If you want some really interesting data go to goodjobsfirst.org and look at the Violations tracker. Select “Financial Services” from the Industries Drop down.

A total of 226 trillion in penalties since 2000. With 10 well known financial services companies accounting for about 75% of the penalties.

Petunia,

Bofa will never sell Merrill unless forced by changing federal regulations. Broker Dealers are a cash cow for banks. Merrill is still in the protocol for broker recruiting, but will probably drop out in the next 12-18 months as more high producers jump ship for the independent model.

2GeekRnot2Geek

BofA has “only” paid about $73 Billion (B) since 2008.

Still a stunning number

Since 2008, all banks under US regulation have paid a total in fines & penalties of about $250 Billion (B),

A billion is a thousand million.

1 million is 1,000,000 (or one thousand thousands)

So a billion is 1,000, (one thousand) 000,000 (million)

Or 1,000, 000,000

53, 000, 000, 000 is 53 thousand million or 53 billion, not trillion.

A trillion is a thousand billion, so a 53 billion dollar fine (if that is what is was) would be .053 or about 5 % of a trillion.

A LOT of fines though.

BTW: much of the press, like the Vancouver Sun, use million and billion interchangeably.

nick kelly,

“BTW: much of the press, like the Vancouver Sun, use million and billion interchangeably.”

Ha, I can do that too, as our commenters have pointed out.

Millions, billions, trillions … with the huge sums we’re throwing around so casually these days, it’s easy to do.

“There are 100,000,000,000 stars in the galaxy. That used to be a huge number. But it’s only a hundred billion. It’s less than the national deficit! We used to call them astronomical numbers. Now we should call them economical numbers.”

In that spirit, perhaps the economical numbers should now be written in scientific notation?

National Debt = $2×10^13

BofA fines since 2008 = 5.3×10^10

Paper wealth about to be vaporized globally in the next market crash ~ $10^14?

You’ll know it’s really bad when BofA sells off Merrill Lynch.

Banks have customers who are liabilities. Safest banks have the fewest customers. The quality of reserves, not the notional amount is at issue. Customers leverage their deposits. Does FDIC cover HELOC? Banks charging their liabilities interest (for income) doesn’t offset the quality of their uncollateralized assets. The global system is wrapped a whole lot tighter and shaky EMs pushing debt in USD, that’s much more of a problem than tariffs.

HELOC (Home Equity Line of Credit) is a loan. FDIC (Federal Deposit Insurance Corporation) covers deposits So, no, FDIC does not “cover” HELOC.

Both the notional amount (quantity) and quality of reserves (capital) is an issue. If you have the highest quality reserve (capital) possible, but you only have $1 of it, that’s not much capital.

I think you are mixing the accounting and colloquial usage of “liability”. Simple overview: Customer deposits are balance sheet liabilities. Banks may charge fees for deposit accounts, and may also pay a small amount of interest (eg savings accounts, CDs). Beside fee income from some deposit accounts (liabilities), banks charge interest on loans (balance sheet assets). Most loan accounts (liabilities) also have fees (eg credit cards, late mortgage payments). The sum of all interest & fees is the banks income.

my bad:

All loan accounts are balance sheet assets; sorry for mis-type

If you have a HELOC and RE falls 50% your deposits take a hit, but in a non-crisis fashion its on you. If however enough depositors lose enough money the banks take the hit and its on the FDIC? Customers in the aggregate become a liability, which is why Chase was (chasing) them (customers) away a few years ago?

Wolf,

Your thoughts on the amount of US Treasuries on US banks balance sheet? I assume they hold no reserves against them and I can imagine they are pledge as collateral to create financial leverage (ie buying stocks, corporate bonds, etc. for their own accounts). Thus the fed unwinding their US Treasuries is creating a lot of problems for the US banks.

If you buy US Treasuries when they’re issued and hold them to maturity, you’ll be paid face value when they mature, and you’ll collect the interest payments along the way. Unless you trade them, there is a near-0% chance of losing money on them. That’s the most secure asset banks can have on their books.

Nominally sure. Argentina paper will be paid back as well. What will it buy?

Wolf was asked about US, not Argentina Treasuries.

Reread my answer Javert. It holds.

Argentina’s annual inflation rate is now approaching 40%! So that’s in one year. It took the US 18 years to do the same thing. Which is why it sounds funny when you guys keep comparing Argentina’s peso debt to US Treasuries.

But yes, there is a risk that inflation will speed up in the US. There are many other risks too. If you invest at all, you’re going to take risks. You’re being paid to take those risks. That’s why you invest. It’s just a question if you’re being paid enough to take those risks. And you also know that when you invest, you will (hopefully) win some, and you will lose some.

And by the way, as far as bank balance sheets are concerned, mild inflation is a non-issue because it lowers the purchasing power of their assets and of their liabilities at the same pace.

In terms of their income statements, mild inflation creates an environment where banks can charge higher interest rates (revenues go up), and they hope that they don’t have to compensate depositors fully for it.

But no one likes it when inflation gets out of hand, not even the banks. Inflation can be a devastating experience to an economy, and it destroys wealth. That’s why you can bet on it that the Fed will crack down on inflation before it goes haywire.

Not to be forgotten: deflation is far more destructive than inflation. Consider the effects of a 20% rise in inflation vs. deflation. Lenders get walloped if their collateral deflates or disappears entirely – although the interest earned improves (currency strengthens with deflation – cash is king). And as deflation gets a grip, people withhold buying things, expecting prices to fall, the opposite of inflationary expectations – cash is trash.

That 0% chance is the difference between a bond and a note or a bill. The 30yr TIP note is called a bond. The distinction between a UST money market and a conventional MM was once thought to be parsing terms, as we enter a time when these distinctions really do matter and the WS buzz is about CDs. 45 promised to default on bonds if the situation arose, if I recall.

The banking system used to be a partner in business, government , etc ,now it is the master how (why ) did we let this happen?

They bridge the gap of the global wage arbitrage that Congress subsidized with taxpayer wealth.

Because they acquired enough money that they bought the key players in the rest of the system so they could have whatever they wanted, and then they decided it would be more fun and profitable to convert themselves from symbiotic partners in the economy to parasites.

But what if the US Treasuries on the banks books are used as collateral for other trades. Wouldn’t they have to post additional collateral as their value decreased?? Ie margin call, or sell other assets.

My somewhat educated guess estimates the banks have probably levered their US Treasuries portfolio 8 to 10x for other proprietary trades.

We will find out if the fed continues down this path.

Sorta surprising how low deposit betas still are, but then again most depositors apparently don’t seem to mind enough to really move their no/low rate deposits around with any fervor. Until that happens, deposit rates will rise very slowly.

Still not really understanding why average CD rates are slightly lagging T-Bill yields at the same maturity. If people were more comfortable buying US Treasuries guess that would change.

DOW futures down by 446 so far this morning. How many trillions in fake wealth and valuations created by the Fed’s fake-money “stimulus” are going to get vaporized as true price discovery re-asserts itself after ten years of Keynesian monetary malpractice?

This should be interesting. Propping up the big banks in 2008, saved Wall Street with the added bonus of the Feds allowing regional banks to go under. In other words, not only was Wall Street saved under Fed cover, it was able to kill the competition and pilfer Main Street one more time. Nothing like turning a loss into a win, as Steve Mnuchin knows. I expect Wall Street will try the same thing next time, and follow Europe’s lead in absorbing smaller banks into bigger ones. Claiming they are saving the world, they will stick everyone and anyone the can find with losses and bad debts of the smaller banks, and hide any of their own. Then our hero’s will lay off everyone possible, foreclose on the rest and fill their pockets, cleansing the system of every honest buck ever made. Hopefully this time Americans won’t be suckered, but Wall Street will sure try.

->Hopefully this time Americans won’t be suckered, but Wall Street will sure try.

A bit late there mate. They aren’t just swimming in debt, they’re already treading water and tiring fast. And the tide will rise further once Fair Isaac completes its loosening of consumer credit ratings.

It’s nothing to look forward to, but never underestimate their gullibility.

Tell them all things ill turn good;

Thew and sinew will be stronger

Thriving on the deadly food

They’re proffered for their hunger.

Tell them all things false are true,

Bitter sweet, that fools are wise;

They will not doubt nor question you;

They are in the mood for lies.

Savings rates in Tampa Bay are rising: Third Federal Savings and Loan has a 3.5% on a 59 month CD, a 2.25% 15 month CD, or a 2.15% 3 month CD all with a $500 minimum and 2% on a money market with balance over $25,000; Synchrony Bank is offering a 2.75% 15 month CD with $2000 minimum (rated 5 stars by Bankrate); Wells is offering 2.3% 11 month CD with $25,000 minimum but it must come from outside Wells. Also says available in Conn. and NY plus rest of Florida.

Circa S&L crisis, the interest rate manna to lift the banks doesn’t work if they have to pay depositors more and no one is borrowing. The questionable nature of the bank reserves, not deposits but Fed induced phantom collateral only suggests that the banks are prebailed. The shadow banking industry has similar assets, and is just as well (poorly) collateralized and has fewer regulations, and is taking away their business. There was once a shadow auto manufacturing industry, they called it Japan.

Eurozone spent trillions of printed Euros on supporting corrupt governments and social spending. The U.S. spent trillions of dollars recapitalizing the banks. Who is better off today???

There was one thing that was different last time (2008) with the banks that cause something to be different next time. In 2008, the healthy banks were asked to absorb the unhealthy ones, which has happened over and over again in previous crises. What was different is that the healthy banks were in turn fined, not for their behavior, but for the behavior of the unhealthy banks they absorbed. (The government couldn’t really fine the unhealthy banks since they were going under anyway.) Given that first time ever political stunt of punishing banks that behaved, do you think the healthy banks will absorb the unhealthy ones in the next crisis? When asked, Jamie Dimon said “we’ll see”. Can you imagine the government trying to run Bear Sterns, Countrywide, Merrill Lynch, etc. all at the same time if the healthy banks didn’t absorb them. Next time could be different.