The soothingly low mortgage delinquency rate is a deceptive indicator: the New York Fed weighs in.

Mortgage delinquencies at all commercial banks in the US inched down to 3.14% in the second quarter, the lowest since Q2 2007, according to the Federal Reserve. But after those soothingly low delinquency rates in 2007, something happened. By Q3 2008, the delinquency rate hit 5.2%, and in Q4 2009, it went over 10%, and stayed in the double-digits until Q1 2013. This was the mortgage crisis. And we’re a million miles away from it, thank God. Or are we?

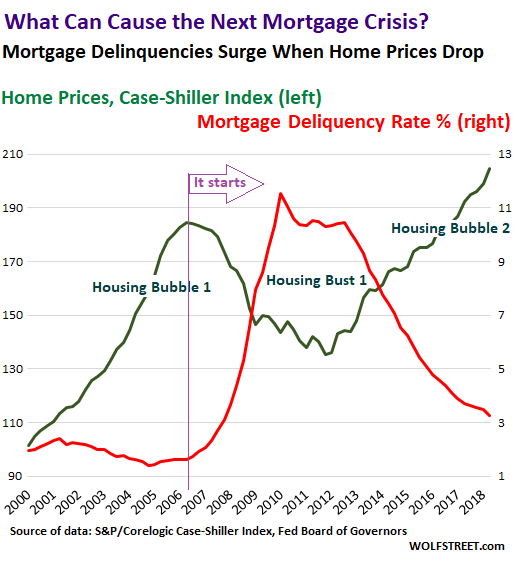

This chart compares home prices in the US (green, left scale) to delinquency rates (red, right scale). Delinquency rates started surging after home prices started falling. The inflection point is marked by the vertical purple line, labeled “it starts”:

Home prices began falling in 2006. By 2008, some homeowners were seriously “underwater” – they owed more on their house than the house was worth. When they ran into financial trouble because they were in over their heads, or because one of the breadwinners in the household lost their jobs, or because they’d lied on their mortgage application and never had enough income to begin with, or because they were investors who couldn’t make the math work out anymore, or whatever, they were stuck.

In a rising housing market, they would just sell the home and pay off the mortgage. But they couldn’t sell their home because it was worth less than the mortgage, and default was the only option.

The chart above shows the relationship between home prices and delinquencies. In a rising housing market, delinquencies will always be low but are not an indicator of future default risks. But home prices are an indicator of default risk.

“Borrowers’ ability to withstand economic shocks depends importantly on housing equity,” the New York Fed explained in its new Economic Policy Review. “This dynamic played a key role in the 2007-09 recession, when surging mortgage debt followed by falling home prices put many homeowners ‘underwater’ on their mortgages.”

When home equity turns “negative,” that’s when serious trouble begins. The New York Fed:

Over the first half of the 2000s, U.S. household debt, particularly mortgage debt, rose rapidly along with house prices, leaving consumers very vulnerable to house price declines. Indeed, as house prices fell nationwide from 2007 to 2010 and unemployment rates soared, mortgage defaults and foreclosures skyrocketed because many households were “underwater”…

But the national averages don’t do a good job. About a third of homeowners own their homes free and clear, and there is no risk associated with them. Another third of homeowners owe relatively small amounts or very manageable amounts on their homes, after years of having made payments without cash-out refinancing. And they’re not a risk factor either. They can always sell their home and pay off their mortgage, even if home prices drop 40%.

The risk lies at the remaining third of the homeowners, the most vulnerable, the most leveraged, those that bought recently at the highest prices, those that refinanced to cash out their home equity….

Then there’s the issue of home prices dropping a lot more in some regions – and this is averaged out in the national statistics. The New York Fed (emphasis added):

At a more disaggregated level, the time series of our leverage metrics clearly reflect the dramatic regional home price dynamics that others have observed, with the widest swings in prices found in the “sand states”: Arizona, California, Florida, and Nevada. Studying these states illustrates one of the key lessons from our analysis: Looking at measures of leverage based on contemporaneous housing values will often lead one to misestimate the vulnerability of a housing market to shocks.

Homeowners in the sand states were much less levered in 2005 than those in other regions, yet as home prices reverted to their mean, the leverage of these homeowners rapidly increased and extremely high mortgage defaults followed.

The paper warns: “Most importantly, higher leverage, and in particular a household being underwater on its mortgage(s), is a strong predictor of mortgage default and foreclosure.”

In fact, according to research cited by the paper, negative equity is a “necessary condition” for mortgage default:

Negative-equity loans represent a pool of default risks: If the borrowers are hit with liquidity shocks resulting from, say, a lost job, then default may be the only viable option. Positive-equity borrowers faced with liquidity shocks, on the other hand, are generally able to sell the property and avoid default.

Thus, “household leverage” blowing out is not a function of the mortgage, which doesn’t change much, but a function of the home price, which can decline sharply. This increases household leverage due to market forces, without even any input from the household. It happens on a case-by-case basis, and the national averages fail to predict this condition.

Even if they don’t default, households that have become overleveraged due to declining home prices impact the broader economy, the New York Fed points out:

- They may cut back consumption in response to a negative shock, in part because they lack “debt capacity” that could help them smooth consumption.

- They’re often unable to refinance to take advantage of lower mortgage rates.

- They may reduce spending on property maintenance or investments.

- The may not be able to move when opportunities arise for them elsewhere.

- High leverage in conjunction with down-payment requirements further reduces transaction volume and prices, “thereby generating self-reinforcing dynamics.”

And the differences, as real estate in general, are local, according to the report: “In cities where more homeowners are highly leveraged, house prices are more sensitive to shocks (such as city-specific income shocks).”

It all boils down to this: There can be no mortgage crisis unless home prices decline enough in some markets. And given how inflated home prices are in many markets, and that mortgage rates are now climbing, any reversion toward the mean of home prices in those markets would cause the delinquency rate to do a beautiful “déjà-vu all over again,” so to speak. That low national delinquency rate these days, often touted as a sign of low risk in the housing market, has zero meaning as an indicator of risk for the most vulnerable households when the prices of their homes begin to drop.

Refinancing activity plunges to the lowest level since 2000. Read… What Will These Mortgage Rates Do to Homeowners Trying to Refinance, Homebuyers, and Mortgage Lenders?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“What Can Cause the Next Mortgage Crisis in the US?”

That’s easy, no one can afford a fucking house at 10X incomes……..well at least in my world.

So you’re saying the natural mean of home prices is a factor of the mean demand for housing and the mean ability to pay, which ratio is at or beyond sustainable limits? Only you said it better. ;)

You sure got that right!

The Bernanke housing bubble completely priced out first time buyers. The middle class has splintered into two groups 1) those who owned a house prior to Bernanke’s great dollar devaluation and 2) those who did not own a house before the Bernanke insanity, are now priced out and getting hit by out of control rent.

I sense building resentment in the second group. I’m in the second group and, having no more incentive to work given the dollar has zero purchasing power, I’m dropping out and making plans to get the hell out of this country, you can have it – let me know who wins the ongoing culture war (hurray for our side whichever it happens to be).

One less engineer, the country will never miss me. A country of professional, rabid consumers has no need of engineers anyway, your job and purpose as an American is to borrow and consume. It’s time for those who are more inclined to work and save to move on, you are not welcome in these here parts.

I just hope I manage to escape before Trump builds his walls to prevent people escaping. Wondering why it is empires always start building walls just prior to the collapse.

Will we perhaps hear a future leader of the free world demand: Mr Trump tear down this wall (and let your people free)

I think the bursting of the Fed’s Everything Bubble, and subsequent financial wipeout of millions of people who are going to lose their homes, pension funds, and nest eggs, will be the last straw for the screwed-over middle and working classes. Trump’s election signaled a decisive repudiation of the corrupt, crony-capitalist status quo, and remember, he ran as an economic nationalist on a promise to “drain the swamp.” He’s since shown himself to be an amoral sociopath and a flim-flam man, but the seething anger against our political and financial elites has only grown since 2016. When the Fed causes yet another financial crisis, I suspect there is going to be a critical mass of people who finally say “enough!”

Sounds like you’re a bit of a gold bug too.

I don’t think we need a collapse to make gold a compelling investment, though it’s certainly a nice hedge for that.

Completely agree with you. I am in the same boat as you, although I am not looking to move out of the country just yet. This is the beautiful by product of corrupted capitalism…some generation will need to hold the bags..I think we now know which class and generation will be the bag holders.

Phoenix I did and don’t regret it a bit Just had emergency Hernia surgery by a great skilled surgeon at a modern hospital for 350 USD including all testing and two nights private room Try doing that in the states If my wife’s family wasn’t here in Turkey I would probably chose Eastern Europe somewhere

A little dramatic don’t you think Van? However I do agree with points 1) and 2). I’m in category 2). I make 74k a year, have 180k cash, 820 credit score, not a dime of debt, with the same company for 10+ years, live in San Diego. I rent. Can’t afford a house. And Wolf, I read your article when it first came out, got depressed, and didn’t comment. So what if we have another housing crash; it just gives private equity funds more ops to buy up homes and rent them. This world, this country, it’s passing me by. Greed. Can you see why I didn’t post? I get upset

Nobody is buying a million dollar home making only 100k. Even with 20% down they won’t qualify.

Little bit of a dramatic statement.

In Toronto, starter bungalows are going for over $1M. You don’t really have a choice if you want to live in the city.

So you get a loan from family, tell the bank it’s yours, and just barely qualify for the other $800K. Any small shock to the market, and… Boom!

I cannot comment on Canadian lending, however, in US see below comments from me on qualifying.

No they dont , they buy $850k bigger house with additional 30 of commute.

850k is still tight. Doable assuming 0 other debt, good credit and with 20% down.

Other debt: credit cards, car payments, personal loans, student debt, etc……

Then who is?

Entities that does NOT need to work. They pool money from “market” at low rates, compete out those W2 buyers and collect rent from the W2 to pay for interest on the money they pooled. The difference between them and W2 buyer is that W2 buyers have to work. Fed prints, they borrow and rent squeeze W2 buyers.

that’s why nobody wants to work any more. Let’s all figure out how to be friends with the FED and rent squeeze the suckers who are doing jobs.

Wolf wrote an article about the 2nd wave of wall street buying armed with money pooled or guaranteed from Fanny and Freddy and other sources. They squeeze the rent and then securitize the rent and sell them back into the market. This is who. Not your W2 earners who have to work.

Broker Dan,

are the US mortgages written after the crash non-recourse? I thought lending standards improved significantly since 2008 in terms of down payment, credit history etc.

Yes lending standards have improved dramatically since 2008 it is like night and day from pre-crisis Lending. there is no question loan quality now is vastly superior to that during the crisis in all aspects: income verification credit asset requirements etc…..

Whether a loan is recourse or non-recourse depends upon the state laws.

+10!

2008 was a artificial bust saved by treasury and the Fed which will not be repeated? Wells Fargo will NOT be the repeat nor D.B? Marginal companies also loaded up on cheap credit and may be the new liar loans? A blow up in high yield blamed on tariffs and high oil prices? Demand will cap any meaningful bust in housing anyhow!

Someone ought to tell Calculated Risk that a low mortgage delinquency rate is not a guarantee of anything. CR has completely lost his ability to spot a bubble. Great article.

McBride has consistently reported improving housing conditions since 2012 with a bias towards California where i think he lives. Was he wrong ?

Although his format is to provide reports more so than his opinion, it’s worthwhile to pay attention to his comments at the end of his reports to get a sense of a turn in his viewpoint. Mind you, at that point the cycle may have already broken.

CR (McBride) being right in 2005 or 2012 does not mean he is right in 2018.

Yes, CR is reporting CURRENT housing conditions. But he has lost his ability to look forward and see that this bubble will burst, too, There are some small signs that he is changing his tune, but it is too late already for that.

It is likely that home prices are not falling in a vacuum. The bad news usually comes from many angles, such as falling stock prices, layoffs, falling revenues, etc. Unfortunately, I know there are lots of people on the West Coast that bought homes at 4x to 8x their pre-tax income. There’s is no question many of these people will default when the parade of horrors begins.

This time around, people know the system is thoroughly rigged. So don’t expect any integrity or understanding from the debtors. In this dog-eat-dog world the government has sponsored through wreckless bailouts and reverse wealth shifts, people will walk from their loan obligations en masse.

At the same time, the public will be adamantly opposed to any sort of second bank bailout.

“people will walk from their loan obligations en masse.”

Actually that is an interesting thought – “en masse” being the key. Would it be easy to go after them for the banks (in recourse cases) if it is en masse?

As an aside, why is it the borrower is only responsible for the loan but not the lender. If lender is also made responsible then he will be more prudent while lending. Looked that way non-recourse loans make a lot of sense.

But then since laws are made for the lenders (since the law maker and the lender are in bed together) it is but expected that the pliant citizens will be okay with being screwed as always. But then it does strike me that everything has a limit and the day the people have had enough and get together (which is the key), the times will prove interesting indeed. But given that politicians are adept at diverting the issue, they are likely to conjure up enemies and go to war with a battle cry when they are threatened.

We the citizens are sitting ducks or sheepies, playing to the pied piper’s (politicians and central bankers) tunes.

“As an aside, why is it the borrower is only responsible for the loan but not the lender. If lender is also made responsible then he will be more prudent while lending.”

That one is easy,,,, In the U.S., government sets lending standards. If you try to be prudent and deny a loan to someone who meets Uncles standards what do you think is going to happen. If you said end up in trouble with Uncle you understand the problem.

I assume implicit is the understanding (while setting the loan standards) that should the loan become sour, then Uncle will take care of it via mark-to-fantasy accounting, tax-payers bailout and skinning the savers, prudent people and retirees for all they are worth. The agencies would also have the courage to act. If that would not be enough, bankers can dump the assets on central bankers (or other government agencies) for 100 cents on the dollar. This is really good governance.

Lenders ill be whining the same phrase produced by foreign policy blowback….”Why do they hate us?”

The moral of Mr Wolf’s story (as I see it) is the Fed will take whatever steps deemed necessary to keep the Great Bernanke House Price Bubble inflated and growing. The quotations in the article make it pretty clear the Fed believes bad things will happen if they do not continue to allow assets to inflate. The Fed does not want these bad things to happen so you can kiss the purchasing power of the dollar good-bye as the Fed continues the destruction of the dollar to keep assets inflated and to prevent an ever expanding and profligate government from defaulting. How is any other outcome imagined?

Can anyone provide a rationale for the policy that asset inflation is good, while wage inflation is bad?

Yes. If you’re Corporate America…

Consumer price inflation is good because it means that, without having to sell an extra thing, you get to charge higher prices and boost your sales, margins, and profits, and it lowers the burden of your debt.

Wage inflation is very, very, very bad because it makes your labor costs go up and thus reduces your margins and profits.

On whose side is the Fed? (That was a rhetorical question)

Falling mortgage values as the last bonds cant get “pushed out” of the shadow bank and O.J gets the blame and not Jerome?

The fruit rots from the outside in.

Meaning the next financial crisis, will arrive via the periphery to the core.

Currently the $8 trillion of emerging market debt, both corporate and sovereign, is causing heightened risk concern as $250 billion is now scheduled to be paid or refinanced. As the Fed tightens and raises rates, this US denominated debt becomes even harder to service.

Corporate US dollar issued debt outside the US, sits at about $1.75 trillion and has also risen in risk. This is not counting the $250 trillion of unfunded liabilities (pensions etc:) that will be defaulted on.

The negative result being? A Great Devaluation.

Watch just not real estate, but most every so-called “asset” suffer a re-valuation, including stocks which means a drastic lowering of market indexes. The question being; Can TPTB pull this devaluation off without causing a catastrophic financial mishap?

I am looking at a great set of clubs to go along with my block of apartments bought out of my own inventory ! (#MAGA) its great to be the king! White wingtips are not cheap.

Let’s be realistic, the previous crisis occurred in a somewhat sane financial word. Time-honored rules still lived – occasionally. Today, there will be a barrage of a response, not least the drop of interest rates, and fiscal at the first sign of sneezing. The movers and shakers are scared to move the needle by even half the percentage.

Are They scared? Seems like They usually come out on top regardless of (or because of?) whatever happens to the rest of society. No? And I really don’t think They see the populous as a threat. I certainly don’t. The American public are fat old toothless lap dogs. It’s only fitting that we’ve almost eradicated the wolves in this country.

Not all of us are so fat and useless James I’m 64 and the same weight as in high school but I realize I’m the exception and not the rule You be underestimating how nasty those porkers will get if you take away their bottles

I have to at least partially disagree with you on this one. With respect to the housing crisis, pre-2008 were the crazy days, much more than today. This is clearly evident from this chart:

https://goo.gl/images/FuDATC

Note the size of the orange, red and blue lines compared to post-2007. Note also that this chart is not adjusted for inflation so in reality it was even much worse than what the chart implies, especially the further back you go.

That’s not to say that housing isn’t overvalued (or even in a bubble in certain places) nowadays. It certainly is and the gist of Wolf’s article is absolutely correct. Defaults will rise substantially as folks go upside down in their mortgages and the current apperant calm level of defaults is very misleading. However, I wouldn’t expect the same degree of crisis as the previous one due to various factors such as the fact that the credit profile of borrowers is much better than the last time and that people have more skin in the game this time, stricter underwriting standards and finally the fact that in real terms housing is still hasn’t reached the the 2006 valuations, neither will it given that in most markets prices have already started coming down.

In other words, this is not the same hidden “big short” opportunity that 2007 presented. There are probably better credit short opportunities out there this time like covenant light loans which have absolutely exploded since the last credit crisis.

Non-bank lenders (quicken/rocket mortgage, etc) are replacing the risks of banks the previous go-round. Poor quality loans are still being given out and on the rise. The questions now are: are banks lending money to non-bank lenders to issue loans and if so, how much? Also, are these non-bank lenders successfully selling off these mortgages to government entities so they socialize the risks and keep the profits?

https://www.wsj.com/articles/big-banks-find-a-back-door-to-finance-subprime-loans-1523352601

https://www.cnbc.com/2018/04/10/big-banks-have-found-a-new-way-to-stay-in-the-subprime-lending-business.html

https://www.brookings.edu/blog/brookings-now/2018/03/08/the-mortgage-market-risk-no-ones-talking-about-plus-a-proposal-to-redesign-the-system/

https://www.washingtonpost.com/realestate/the-mortgage-market-is-now-dominated-by-nonbank-lenders/2017/02/22/9c6bf5fc-d1f5-11e6-a783-cd3fa950f2fd_story.html

As an aside, Rankin County Mississippi (the market I pay attention to since I work there):

Median household income is around $68k, median home prices now around $235-250k (a good bit over historical trend of 2.5-3x income)

Zillow pre-foreclosure listings for the area in the last few months (since May or so) has gone from ~108 to ~125 a couple weeks ago and now has popped to ~168. That’s a huge increase in a *very* short time.

Interesting times ahead?

The fact that banks now make up a negligible portion of subprime mortgages and that non bank lenders now the ones who service the non-prime population still doesn’t change the fact that that the overall credit profile of mortgage borrowers has vastly improved since 2008 as can be seen in the chart I attached.

The anecdotal pre-forclousre stats you noted go hand in hand with non-foreclosure housing data I have seen also that show the housing market having peaked in around the May timeframe of this year. I would expect the Case-Shiller index to reflect that at some point, especially now that we are entering the slower housing seasons of the year. There are a lot of houses out there which have been sitting unsold throughout the summer with more price cuts to come.

“are banks lending money to non-bank lenders to issue loans and if so, how much?‘

The answer to that is in one of the articles you attached actually: $345 billion in 2010 through 2017. Frankly, that is a drop in the bucket compared to the close to $150 billion (in 2018 dollars) in subprime loans per *quarter* the banks were issuing during the 2000s housing bubble.

Yeah I saw the articles answered my own question, doh! Also a good read if you haven’t seen it is https://www.bloomberg.com/news/features/2018-05-24/small-time-bankers-make-millions-peddling-mortgages-to-the-poor

Your “small town bankers” article issuing subprime mortgages reminds me of Wolf’s articles discussing default rates for credit cards at the smaller banks compared to the default rates at the big boys.

At the end of the day what will probably happen is that Fannie and Freddie will be bruised after the next crisis but they’ll survive. Ginnie Mae on the other hand will probably become insolvent given the type of loans it’s guaranteeing in pursuit of the US government’s goal of “increasing homeownership” (basically among people likely to default on their loans at the drop of a hat).

Note also this tidbit from the article: “only 3.5 percent of new loans are to people with credit scores below 620, compared with 15 percent in 2007” which is essentially what I was alluding to in my earlier comments. The one issue of course is that unlike the previous crisis, this entire segment of borrowing is guaranteed by the taxpayers since fully private mortgage lending has all but disappeared since the 2000s housing crisis.

Everybody needs to realize that just because a lender sells off a loan in the secondary Market which ends up Fannie Mae or Freddie Mac or just a large investor does not mean the original lender does not incur risk. I know I broker to many wholesale or non Bank lenders that fund on their credit line and then sell this loan on the secondary Market or securitize it and hold for Servicing.

Here is the rub, if there is any defect in the loan file of which there are typically a million moving parts or there’s an early payment default or any hint of fraud that loan is instantly pushed back on to the originating lender as a buyback.

BuyBacks are what brought down the industry before and triggered the liquidity crisis. Just a few BuyBacks can put a lender under immediately.

furthermore FHA tracks what is known as compare ratios and what this does is Compares a certain lenders default versus performing loan origination ratio versus other lenders and if one has a high compare ratio FHA will cut them off from being able to lend.

so to say that originating lenders that are non banks have no risk because Fannie Mae will buy the loan is not entirely accurate.

The Fed will see those who bought houses (and other assets) at these insanely inflated levels as having had “the courage to act” and the Fed will aggressively reward these people and make sure they suffer no financial harm.

No financial gamble can any longer be considered risky or foolish. No, these seemingly risky bets are “courageous acts” and the government and Fed will reward these people for their courage (and continue to punish the cowards who sit on the sidelines).

Sorry, that’s just the way it is.

That’s not what happened in the last crash. Ordinary people who bought near the top were mostly screwed, while the banks and big investors got bailed out. I’ve known plenty of people who lost their homes and much more. Programs like HAMP helped a few lucky people, but did nothing for the vast majority.

The only way to recoup the loss to some extent last time was to stop paying the mortgage and live rent free until the bank could finally evict you, though most people felt morally compelled not to do that. I bet more people do that the next time around. Even if you successfully game that though, you’re lost down payment is worth several year’s rent so you lose pretty big on the deal.

Another thing of interest is the default rate of subprime vs “good” borrowers during that period. https://qz.com/1064061/house-flippers-triggered-the-us-housing-market-crash-not-poor-subprime-borrowers-a-new-study-shows/

Yeah, that’s what I was trying to explain ro Petunia below.

I really don’t know, nobody thought the Fed would be tightening and rates rising, right?

We heard NIRP and ZIRP (painters itself into a corner) for the past decade and then lo and behold the Fed started QT.

Wolf has already the roll off to maturity.

So, it seems it’s not so easy to predict what the Fed will do or can do as they are doing the very thing most did not think they would.

Money growth is still coming from the tree!

I don’t find the correlation between home prices and defaults helpful. I think a better measure would be unemployment/incomes and defaults. Historically, way before 1990, the default rate was in the 1-2% range, 3% is extremely high on a historical basis. Even during the savings and loan crisis of the 1980’s, I don’t think default rates hit 3%. This is because job markets were more stable then than they are now.

The mortgage default rate is tied to income and jobs. The more unstable the job markets are, the more defaults you will see. Increasing home prices are now a function of distortions in local markets. Palm Beach home prices are soaring because the second White House is there. CA and NJ are dropping because people are fleeing, etc.

There are also structural reasons why home prices may decline and affect the default rate. The baby boomers are retiring at the rate of 10K a month. They will not be able to service long term, high interest, large mortgage loans. They are joined by those paying off student loans. Working class incomes are also not rising, nor keeping up with inflation.

The pool of mortgage loan customers is shrinking.

Well, one thing to consider is that “way before 1990” downpayment requirements were generally tougher, which meant that people had more equity in their home at the outset which in turn meant that people were better able to withstand a downtrend in housing values, notwithstanding the overall employment situation.

The defaulters didn’t have enough equity is a myth of the financial crisis. What they didn’t have is enough income to keep their homes. That was my story. We had 40% equity until we didn’t. We lost or income and equity at the same time. The next crisis will be the same, low income and crashing equity.

You should take a look a Scranton, PA right now. All of the cash producing assets of the city were privatized and the resulting deficits was passed on to homeowners in the form of higher property taxes. Many of those homeowners have owned their homes free and clear for generations. Now their equity has been impaired. They can’t get out because real estate taxes are too high for local incomes. There are no jobs there, retirees can’t afford the cost of living, and most of those living in their free and clear homes will lose them. You can say they didn’t have enough equity, and you are partially right, but it doesn’t tell the real story.

Many of the defaulters in the last cycle we’re speculators who banked on price appreciation in a relatively short period of time so they can turn around and cash out their position. Once the housing market went the other way they got stuck with underwater properties. This is regardless of their employment situation.

The tie between employment and default is not quite as strong as you think becuase as long as they have equity in the property greater than the market price, folks can just sell the property and downgrade their housing or move to a place with a lower cost of living. But if the housing market changes direction like is happening right now (combined with low downpayment requirements) then for a lot of folks who bought at the top the option of selling doesn’t really exist and they have to default.

Max,

I know that there was speculation, but that was not the average case because most foreclosures displaced families. Just three years ago, I could still see the doubled and tripled up families on my Florida street.

Just to bolster my case, if you look at the single family rental companies, which paid cash for houses, they are hitting a rental income ceiling. Those rents are dependent on the incomes in the areas they operate. Their decreasing revenue flows will eventually deflate the prices of their homes, without a mortgage being anywhere in sight. It will all be about income and jobs.

Petunia, jobs is a trigger but equity is the determinant of default.

In other words, a turndown in employment may force people to reevaluate their housing situation. If they have sufficient equity they’ll most likely sell the house and rent in a cheaper place or move somewhere less expensive. The result is job loss but no default. If they are underwater though, they have no choice but to default on the mortgage.

That is the point of the article… Not what causes people to stop being able to afford the house but rather their ability to get out from under it if they need to.

taxing property too much means no one can buy it, and no one can sell it to buyers because it costs too much to own.

imagine the 30 at 6.5. ouch.

strikes me that ownership at more than 1.5 rental value is getting warmer, so to speak.

i may seem obscure, but the arithmetic makes sense.

A comment I made under “mortgage rates do to homeowners” got stuck in mod for some reason, but one article link was opinion thar 83% of gdp expansion was due to realty. As “in moderation” comments show after commenting, I’ll post this and go see if I can fish out the link which I don’t have saved. The short of it is is it suggests less money supply from housing brings down jobs and wages.

Nah… looks like it got wiped :-( . Anyway, the idea is that stated, you will just have to spend a few hours searching up all the charts, links and data I assembled.

In my neck of the wood, British Columbia, that number certainly sounds modest, no link necessary.

Banks will get into other kinds of trouble and that will spillover into the mortgage business.

It will be interesting to see how the elites respond to the next banking crisis or recession. They’ve tapped just about everything possible to preserve high asset prices and economic growth for themselves.

Assuming there is no real political revolution, I think the elites have one major play left, and that’s a huge public infrastructure investment that gets tacked onto the government debt. That could keep economic growth and asset prices propped for several more years, until the day they finally have to hand out something more than scraps to the middle class to preserve growth.

Another facet is net worth of households e.g.

https://www.thebalance.com/american-net-worth-by-state-metropolitan-4135839

…which is a bit outdated but still close. Property prices drop enough they will sink a lot of people I think, given a large part of wealth is stored in property. Under 45s look most vunerable…no one is going to be very positive when they find overnight they are net debtors, not savers.

Crysangle,

Unrelated and FYI: You’re a prolific commenter, and sometimes you go overboard with the number of comments under one article. To keep this place balanced, I have a 5% guideline. If about 5% of the comments under one article are yours, it’s time to stop until enough new comments have been posted to allow for another comment within the 5% guideline.

If you haven’t had the chance to look at the commenting guidelines, here they are:

https://wolfstreet.com/2017/10/07/finally-my-guidelines-for-commenting/

Thanks!

:-)

– The chart suggests that 1) delinquencies are still very low but 2) they are above the levels of the early 2000s when delinquencies were much lower. So, the term “low” is relative.

– What will cause the next crisis ? Quite simple. A simple thing called “affordability”. Just look at what happened in the 2000s. Like: 1) rising oil prices, 2) increased productivity 3) wages remaining flat 3) weakening USD 4) changes in federal taxation, etc. etc.

– And all lead to a decrease in the growthrate of debt.

– Whether or not there will be a new mortgage crisis also depends on how well lenders have followed the existing regulations. Keep in mind, there was a MASSIVE fraud in the early 2000s. One source said that even in 2008 80% of mortgages were fraudulent.

Almost all mortgages written today are based upon income guidelines.

the vast majority are standard income verification via W-2 tax returns and pay stubs, there are some bank statement for income programs for self-employed individuals that use deposits for income however those require good down payments and decent credit.

Since demand for housing in 2005 was driven by poor underwriting and easy availability of loans, what is driving the demand this time around if we have good underwriting and high quality loan appraisal?

Ummm… how about simply “people need a place to live” :-)

Speculation. “Money for nothin’, chicks for free.”

Ted,

Regarding speculation, investors needs 20-25% down on investment properties. They have skin in the game unlike the pre-crisis mortgage programs which had little to no risk.

Dan,

OK, I will take your word for it. But how many “investors” are borrowing that 20-25% from their stock brokers on a portfolio loan account or taking out a 2nd mortgage on their primary residence? That scenario is even more dangerous than 100% financing on a speculation property.

Ted,

The latter is feasible as long as the borrower meets the debt to income ratio and there is enough equity. Most levers will not go above 80% loan to value on a line of credit.

The only way the former works is if you borrow against, stuff it into a bank and let the funds season for at least 2 months. borrowing against an unsecured asset is not allowed with conventional financing so the only way to make that work is to put the money in your checking or savings account and let it sit there for a few months that way the bank statements will not reflect the large deposit and therefore the money does not need to be sourced. You cannot just borrow against it and go buy a property the next day does not work that way.

Lastly, gifts are not allowed on investment properties, so you cannot get money from someone else to use.

a reliable source said to me 40%. in response to my observation of 20%.

so let’s go with 30%. 30% tends to scatter the troops.

– And how much is lent out by the socalled “Shadow banking system” ?

Increased wages are out as long as Free Trade forces American labor to compete with cheaper foreign labor. Lowering interest

rates just continues the speculation. I think the FED will eventually

be forced to hold interest rates steady in hopes that population growth increases demand to the point that it can resume raising rates. Until then, housing should slowly stall.

The last mortgage crisis removed the stigma of walking away from one’s loan obligations. If we were to have another, I can see where many could walk away given the stigma has been removed and precedents set.

You are correct in your conclusion, however, I think that it was Obama’s 1-2 of bailouts and zero prosecution that really did the work of erasing any last feeling of “honouring ones obligations” towards bankers!

Can you trust a realtor in your area to tell you if the local prices are high or low?

I’m given comps on my home by agents and they use the sales from the last 6-12 months. Each realtor shows different homes as comps yet they all manage to come up with the same exact value for my home to the penny. It can’t be a coincidence, and some of these people are from different areas and unlikely to be colluding.

Do all real estate agents today use a common computer program to assess home values??? It seems a home is worth whatever the real estate agent’s valuation program says it is worth!

In which case there’s no limit to how high valuations can go, and no reason they should ever fall.

I don’t know exactly if they use the same piece of software, but they surely use the same parameters: realtors operate in networks and those networks tend to adopt a unified pricing structure using the same parameters and elaborated in exactly the same way. It would be interesting to see exactly the formula used but apparently they are only available to the Initiated. :-)

It makes things easier for the realtors themselves but it also makes for pretty heavy distortions, the most noticeable being that pricing in a given area (at least this is what I am noticing right now) does not seem tied to unsold stock and especially how long that stock has been on the market at exactly that same price.

I don’t know how realtors are paid these days (when I lived in the US I always rented), but I bet their fees are somehow tied to the value of the house they sell, so they have every interest in keeping values from falling too much.

On top of this rising prices are the key to “sell” potential customers the idea an area is “gentryfying” (a term that has on me the same effect as a steel nail on a chalkboard) and that average wage in the area is increasing faster or even far faster than in reality. In short the realtor is not merely selling a house, but a ticket to the next step in the social ladder.

Valuations will never fall? I can ask whatever price I want for the pencil I have near my keyboard right now. There’s no law against aspirational pricing, no matter how delusional. But it’s another matter completely if I’ll find somebody willing to give me whatever I ask for my pencil.

That’s the same with real estate.

Virtually all listed and sold properties are stored in the MLS so they all choose from the same pool of properties which they can search and find using various criteria and parameters. You can pretty much do the same yourself on Zillow if you wanted to double check their work, although I would caution you to check the actual listing price history under the price history tab rather than rely too much on Zillow’s price estimates.

Don’t worry guys, X is gonna crash first!

The problem is figuring who X is

Argentina, Spain, Italy?

My guess is war where China and Russia amalgamate to attempt to destroy America. This will certainly affect housing and insurance companies. This is the next crises that few see.

This article is reaching and Wolf is letting his own bias as a renter cloud his objectivity.

Housing may very well be overvalued but the widespread impact like in the last crisis is not possible. The last crisis was drivel largely be abs derivatives such as synthetic CDOS. These products mushroomed during the 2000s and we’re the cause of the crisis.

It’s a totally different situation today. Even if house prices decline (a lot) there won’t be another crisis like 10 years ago. Read up andoing educate yourselves.

Did you read more than just the headline? Because your comment is just commenting on the headline.

Is the NY Fed also “showing its bias.”

FYI, this was an article about the cause-and-effect relationship between home prices and default rates.

The next crisis will likely show up in BBB rated corporates failing and pension funds being unable to absorb the losses due to demographics. Some time in the next 10 to 15 years so. A cascading series of failures will likely show up in public and private pensions. This may very well be connected to EM debt as well. In times of stress everything is correlated…

I have a friend lives in Lake Placid, FL with a home fully paid for due to inheritance. Property taxes with a disability & Homestead Exemption, 3 years ago was $538.. 2 years ago, $837. Last year, $1126. 2019 property tax bill estimate – $1,346. He lives on only $1,100 Social Security monthly. Kicker is – He is not carrying ANY form of homeowners insurance because he can not afford it & lives without air conditioning. Still in my Class C RV enjoying an easy life.

With both high levels of personal debt and little cash liquidity, a rise in unemployment has amplifying secondary effects for the financial system at large. Low personal debt levels and more cash liquidity would act as a firewall, but that isn’t the case for most Americans today. That may be one factor that lately we have had long booms followed by terrifying panics (2000-1, 2008-9, 2019?) and asset price crashes. Business debt is easy to shed in default and bankruptcy; personal debt defaults are more pernicious and take longer to flush from the system.

What you say isn’t exactly bourne by facts… While household debt as a percentage of GDP has been on an upwards trend over past 40 or so years (mainly as an inverse function of falling interest rates since the early 80s), it’s actually down by a lot since the last financial crisis.

The type of debt that is now equaling or surpassing the levels set in the financial crisis are government and corporate debt, not personal debt.

Max Power,

I have some questions here…

If household debt could trigger a contagion in 2007, is it not possible that corporate debt also can lead to a similar crisis. Also talking of government debt what happens if interest rates spike for Italy? Would it not lead to ECB launching a fresh QE?

Yes, too much corporate debt can lead to a crisis, especially if the economy starts to wobble a bit.

Not only is corporate debt as a percentage of GDP back to its 2007 highs but what is worse this time is that the percentage of the debt that is light covenant or junk rated is much higher than last time.

The other issue I see is that the ability to increase leverage at debt rollover points in the past 35 years due to the overall reduction in interest rates is now gone given that we have reached the zero bound in interest rates. In my opinion, this “no cost” increase in leverage has been the main driver of economic growth since the 1980s. However, the inability to increase leverage due to rates rising or even just staying at or above the previous cycle’s interest rates will likely cause a structural shift in the economy that few are expecting.

As for Italy… yep, it will be very interesting to see what sort of yields transpire as the ECB backstop is removed.

What you said doesn’t refute anything I said.

I expect price inflation to be over 10% by the middle of next year. In five years all these overpriced loans will be paid off and median income in the US will be something like $300K. Multi-trillionaire will be the new billionaire. Mortgage interest rates will probably be under-priced at around 9.75%. QE was tried and was found lacking. Inflation is distasteful but proven.

What the housing bubble does in many instances is to create a sort of “mania” around housing as a “good investment”. People stretch and buy the most house they can. People that have been in a house for awhile easily rationalize a new kitchen, bathroom, whatever. Most everybody gets caught up in the perceived big gains, even though when you do the math if you sell, the gains aren’t quite what they seem (6% commission, money to fix all the things ID’d by your friendly agent and inspector, etc.)

So then the recession hits. Housing prices falters. People lose jobs around the margins. More houses go up for sale or go into default.

It really depends on the magnitude of the recession. If it’s severe, I’d say housing will be in trouble again in some areas of the country. I’m from Charlotte and I can tell you the “mania” has been going strong for several years now. It can’t last and when it ends, there will be people that get hurt.

Six percent to sell a house is theft pure and simple You need to negotiate it down as I’ve always done or sell on your own Brokers are parasitical and need to be avoided at all costs like bankers IMO

Unlikely a recession hits while Trump is in office. All the US dollars in existence can only be spent in the US by law. Everywhere else spending dollars depends on Global trade. US Government is spending dollars like it hasn’t spent since WW2. And the US Government isn’t selling War Bonds. US Treasuries are being monetized not sterilized. Slowing illegal immigration will upscale housing. Fewer Automation jobs but they pay much better. Section Eight housing and Penthouse Apartments will become less of the market and 200K to 500K range will become more affordable for the reduced masses. People who voted for Trump get rewarded. By the time inflation has to be brought under control Trump will be out of office. Automation bubble.