The request is “essential to Tesla’s continued operation.”

Tesla burned $1.1 billion in cash in Q1 and likely more in Q2 – we’ll find out on August 1. It cut its workforce by 9% in June and promised to cut other spending. CEO Musk told the entire world in a bizarre earnings call that he didn’t “want to” raise new capital in 2018, though Tesla had only $2.7 billion in cash at the end of last quarter. No one can figure out how the math is supposed to work out…. Well things are getting pretty tight, it seems, and the year is only half-over.

In a memo that a global supply manager at Tesla (TSLA) sent to some suppliers last week, the company has asked the suppliers to refund what it called a meaningful amount of money of what it had already paid these suppliers since 2016; the purpose of these retroactive discounts is to help Tesla become profitable, it said. The memo was reviewed by The Wall Street Journal and reported Sunday evening.

According to the memo, the request for cash back is, as the WSJ put it, “essential to Tesla’s continued operation.”

The memo said this cash back would be like an investment in Tesla “to continue the long-term growth between both players,” in the words of the WSJ.

The memo said that all suppliers were being asked to fork over this cash back so that Tesla could become profitable. But it remains unclear, the WSJ said, how many suppliers were asked for a discount on contracted spending amounts retroactively.

Some of the suppliers that the WSJ contacted about the retroactive cash-back request told the WSJ they were unaware of it.

The WSJ reached out to Tesla:

Tesla declined to comment on the specific memo. But it confirmed it is seeking price reductions from suppliers for projects, some of which date back to 2016, and some of which haven’t been completed. The company called such requests a standard part of procurement negotiations to improve its competitive advantage, especially as it ramps up Model 3 production.

The WSJ added:

Supply-chain consultants say sometimes auto makers will demand a reduction in price for a current contract going forward or use leverage of awarding a new deal to get upfront savings on a contract,” the WSJ pointed out. “But they say it is unusual for an auto maker to ask for a refund for past work.

“It’s simply ludicrous and it just shows that Tesla is desperate right now,” Dennis Virag, a manufacturing consultant who has worked in the auto industry for 40 years, told the WSJ. He said this kind of solicitation could put suppliers in financial peril and jeopardize Tesla’s future supply of car parts. “They’re worried about their profitability but they don’t care about their suppliers’ profitability.”

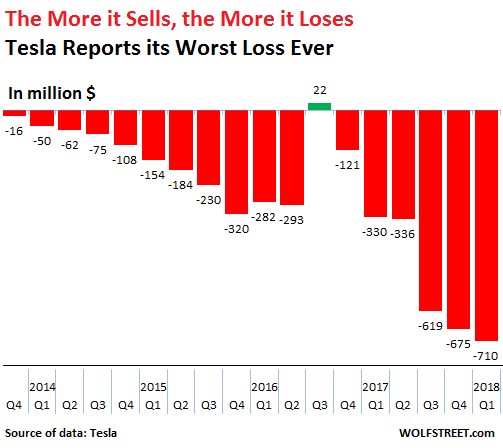

Tesla really needs all the help it can get. In Q1, it lost $710 million, its largest net loss ever. While total revenues – automotive and energy combined – rose 26% in Q1, it’s net losses jumped 114%, on the time-honored business model: the more it sells, the more it loses.

In addition to burning through cash at a breath-taking pace, Tesla has some obligations coming up. The WSJ:

Tesla will need to pay down a $230 million convertible bond this November if its stock doesn’t reach a conversion price of $560.64, and a $920 million convertible note next March if the stock doesn’t reach $359.87.

So the true believers need to go to work because Tesla’s shares, at $313.58, are just a little shy of those conversion prices. And if shares don’t hit those conversion prices, Tesla will have to raise even more money in 2018 that Musk said it wouldn’t need to raise.

At this point, given Tesla’s current share price, its investors really don’t care about anything other than doing whatever they can to keep the share price high. So it’s in their own best interest to support the shares, they think. A market capitalization of over $50 billion guarantees that Tesla can always raise more billions and burn through them in no time. That share price is Tesla’s lifeblood. Few other companies are so utterly dependent on an astronomically inflated share price for their survival. Once Tesla loses its ability to raise fresh cash to burn through, it’s over.

At least one of them is very wrong: Atlanta Fed GDPNow v. New York Fed Nowcast. Read… Is the US Economy Really Going to Pop 4.5% in Q2?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“If you owe your bank a hundred pounds, you have a problem. But if you owe your bank a million pounds, it has a problem.” – attributed to John Maynard Keynes

My advice to any of Tesla’s suppliers is to get out while the getting is good. I would only accept cash and would extend no credit. If a check bounced that would be cut off time. If a supplier is joined at the hip to Tesla they are in too deep and they have a problem.

The main concern with Tesla is not that it is too big too fail but that it is too loved to fail without psychological fallout disproportionate to its size.

Apart from employees and shareholders who loved Enron or Global Crossing?

It’s been a while since we had a cult that is also a manufacturer, Apple being the only one I can think of since the Dot.com crash when the market was full of gurus.

I think there is an lesson for Musk in the story of Bombardiers C-Series jet airliner. The company almost went bust building it, getting it certified etc. In fact it would have gone bust without big investments from Quebec and Canada, a thing duly noted by Boeing that applied for a huge tariff (over 200%).

The tariff was struck down by the US internally, with the regulator noting that Boeing offered no plane of comparable size but more time had passed. Who wanted to buy a plane from an outfit that might go broke?

So Airbus took it over. Bombardier still owns a third.

Already big orders are coming in.

Bombardier can get back to its main thing, land transit.

There would be no shame in letting Hyundai take over the Model 3.

Then Tesla auto could get back to the high- end niche it should have never left.

Their CEO has been doing quite a good job at bring hated in recent years. So let Tesla fall, people will celebrate.

It is surprising how a cult- like figure, even in politics can be hated by many and still loved by the cult.

As a Tesla Auto skeptic commenting here, I’ve felt their wrath.

However I’ve never before heard the word ‘hate’ used about Musk.

There are only so many words in English. There is scale of ‘bad’ reflected in court sentences.

If you use up ‘hate’ on Musk what do you use for guys who kill people for fun ?

Musk is just a highly immature, highly driven, and super smart guy with a ruthless streak – all the characteristics you need to be an entrepreneur.

As I mentioned in another post, he also owns 54% of SpaceX, which right now is privately held and the only other alternative to United Launch Alliance in the U.S., the only one other than ULA’s rockets certified by the military to carry their satellites.

Musk’s idea to make the rockets re-usable, copying what had been done for the Space Shuttle rockets, basically gives SpaceX a huge leg up over all his competitors by making his rocket launches the lowest cost in the industry, even compared to Russia and China rockets.

And guess what? As of 2018, SpaceX currently has an estimated whopping 65% of the commercial satellite launch market, taking most of the market once dominated by the French-Euro Ariane (which had 50% at one time) and just about wiping out the Russian commercial satellite business (the Ukraine related sanctions helped).

Jeff Bezos’s Blue Origins are also working on this, but they have been moseying along and don’t seem to be in a hurry. Blue Origins was started in 2000, SpaceX in 2002, and look how far the two have progressed.

So SpaceX, if it ever does an IPO, is likely to be worth far, far more than Tesla – Musk only owns 22% of Tesla stock.

As for Tesla, you have to remember that when it was started 2003, GM had just closed its EV1 electric vehicle program, recalled all the cars (which were only leased, not sold) and promptly crushed and ground them up. Electric vehicles seemed to be dead in the water.

If you look at the scenery today, every car manufacturer in the world has an electric vehicle program going, most at the highest priorities.

China has plans to go all out with electric vehicles, and considering how they basically took over the solar panel market worldwide, they are going to succeed. Leading the way is Volvo, now owned by Chinese car maker Geely, which has plans to go all electric in the near future.

VW has plans to recover from its diesel engine fiasco/scandal by going massively into electrics, especially in its specialty – small cars.

At the high ends, BMW and Mercedes all have fancy electric cars here or coming soon.

So, its not clear if Tesla will survive, but Musk has so many projects going on that he is going to come out of this just fine.

What people have not noticed in the midst of the current Tesla storm is just how rapidly SpaceX went from having its rockets blowing up and/or crashing on YouTube videos to having 65% of the rocket launch market.

Musk is a high risk high reward kind of guy.

In 2017, there were a total of 30 US orbital launch attempts (one of them was launched in New Zealand). Globally, there were 90 (Russia 21, China 18, Europe 9…). SpaceX launched 19.

So this isn’t exactly a high-volume business.

SpaceX says: $62 million for a Falcon 9 launch and $90 million for a Falcon Heavy (SpaceX: “Modest discounts are available, for contractually committed, multi-launch purchases.”)

SpaceX launched 19 Falcon 9 in 2017 = $1.18 billion in revenues for the year. This is a 50-year-old mature industry.

Wolf,

They plan to colonize Mars; they’ve already sent a Tesla there. Expect them to open for public pre-order of a tent on Mars soon. So the number of launches will increase exponentially. At least, that’s their thinking.

So Musk only owns 22% of Tesla but 54% of Space X. He thinks the chance of EV saving Earth is slim. ;-)

why can’t hyundai just copy it?

because. it’s. not. worth. it.

the arithmetic don’t work. but the ideals keep things floating. sometimes i have soft spot for them,

but. not. the. stock.

imagine ford chrysler gm with ideals. ha ha ha. said slowly.

You happen to be correct, Joan, but the problem is that if you are a supplier and leave Tesla before you have a replacement contract, it is like you lighting the fire and burning yourself at the stake. If I remember my history, you have some knowledge as to how that will turn out.

Large supplies that could possibly bear the retroactive discounts tend to be much larger and economically sound companies than Tesla ever was. For their own safety, they can swallow the decrease in sales in order not to suffer much greater losses after the of bankruptcy.

The fire didn’t do my expensive hairdo any good. That was what I was mainly worried about…that, and overheating. I knew that I would be free from the stake once that it had burned through.

Musk will still have SpaceX, a company that he actually founded, and probably the most successful of his recent ventures, mostly because he was competing only against United Launch Alliance, a bloated operation that had gotten fat and lazy from feeding at the USGA trough.

Privately held SpaceX is likely already worth more than Tesla, as it already has a steady stream of customers for its rockets, including the US military and NASA, and Musk was discovered from a filing in 2016 to own 54% of its stock, compared to 22% of Tesla:

https://electrek.co/2016/11/16/elon-musk-stake-spacex-tesla-shares/

Of note, Musk did NOT actually start Tesla – the company was founded in 2003 by Martin Eberhard and Marc Tarpenning. Musk gained control of the company in 2004 by providing its first round of major funding and becoming Chairman of the Board. He then forced out Eberhard in 2007 as CEO, and took that position as well.

What’s SpaceX’s profit margin per launch? Or is it launching at a loss to capture to grow market share, à la Tesla business model?

And yet just as the three-card monty act is called out, his Muskness announces a giant new manufacturing plant in China? Okay, flamethrowers, impossible tunnels, and missions to Mars aside, I’m willing to suggest that there’s something happening indeed..consider merely the inexplicable constant investment..

“And yet just as the three-card monty act is called out, his Muskness announces a giant new manufacturing plant in China?”

How many times has Tesla announced a factory in China, now? I think this is the third time I’ve heard such an announcement over the last 2 two years.

“Privately held SpaceX is likely already worth more than Tesla”

By what metric? Tesla’s market cap is $50B+. The last round of private funding valued SpaceX at $27B. If SpaceX can keep launching a Falcon 9 rocket every two weeks at $64 million a launch, that’s about $1.6B in yearly revenue. Tesla’s 2017 revenue was over $11B. Of course, neither companies are profitable.

Yet as busy as he is he still finds time to attack a perfect stranger half way around the world who helped save some boys in a cave in Thailand. The attack came with no documentation whatsoever concerning the mans social or sexual status. The attack was completely uncalled for and the attacker’s character and mental stability should be called into question the next time he goes begging for more funding.

Well, I kinda agree*, except that “Social Media” is engineered and tuned by machine learning tools** to bring out the very worst in all people, because: There is nothing quite as effective as rage, bigotry, cruelty and crazy rantings to drive those click-ratings and page-views which move that needle on ad-revenue!

Condemning people over SoMe behaviour is a bit like* blaming an alcoholic for being an idiot after putting 5 liters of bum-wine within easy reach. The incidents are entirely predictable from the outset.

The SoMe business wants our outrage and condemnations over some idiotic message – if we always give it to them, we become their batteries.

*) Still an idiot in the specific instance, but maybe not in general and in all aspects of life, is what I mean. He got “help” from his “digital friend”, as it were.

**) Google, Twitter, Facebook, Apple, and so on – they are all in the “Brain Business” now. They want to be “sticky” as they call it; they don’t like to use the word addictive (“addictive apps” were all Edgy Talk in the naughties, now they got the theory to work and its all gone dark because it’s proprietary and it will at some point attract regulation).

Musk is toast It’s just a matter of time now His instability is becoming obvious to investors

If he were truly devious, he would act unstable to get the shorts to pile on and then completely obliterate them with great financials. Not that I think that is going on.

The only way he could pull that off would be to go into the fetal position for 30 days under blaring headlines. It would be an economic winner causing shorts to short 90% of the stock’s open interest. The short covering could then take the stock to at least $600.00 per share when the hospital announces that he has recovered. Unfortunately, his ego is too big to let it happen.

According to one of our Australian Newspapers, Musk is the Teflon man. He will get away with any problem that surfaces.

Quote : THERE ARE VOTES IN TESLA. – Tesla is so prominent that politicians will want to save it. – Tesla is now “too big to fail”. – he will have no difficulty convincing politicians to give up other people’s money : Unquote.

I’m not so sure. If Musk has a serious breakdown, it’s all over for Tesla. Tesla is Musk – Musk is Tesla.

The car company will be pared off to existing manufacturers and then eventually stripped apart and allowed to die.

An excellent observation, Les Francis, and I agree that the future for Tesla is indeed in this ball park. It has happened before, many times, and the inevitable outcome is always the same.

I have personal experience of being too personally involved with the company I founded in 1986. I was forced out in 1995, quite rightly, as being too entrepreneurial to manage the company going forward. My fellow directors were bang on, and the company prospered in my absence and is now a stable and profitable cash cow which my son now manages.

The founders should always bail out after the company turns from a rising star to a cash cow; the skills required to manage successfully are entirely different.

An alternative: Build and stay personally involved in a sole proprietorship. Your future doesn’t depend on the judgement of others.

At the risk of sounding like a Elon Musk cultist, it appears to me that Elon Musk is a great salesman and true visionary….but a god-awful manager. When Tesla introduced their roadster and the Model S, they could do no wrong, and they had buyers lining up the wazoo willing to wait months for a new vehicle. But now that they’re trying and struggling mightily to come up with a mass market vehicle, their shortcomings are becoming visible to everyone. I would hate to see Tesla go away, but maybe the only way to save the company is to sell it to an experienced auto manufacturer who can smooth out all of the rough edges in production, and for Musk to step down and focus on SpaceX.

Napoleon had a lot of followers, also.

So did Jim Jones.

“Tesla is so prominent that politicians will want to save it. – Tesla is now “too big to fail”. – he will have no difficulty convincing politicians to give up other people’s money”

If it’s about saving jobs, Tesla’s employee count isn’t that high. If it’s about the importance of a BEV future, other more competent manufacturers have been building affordable BEVs for years. And if the GM bankruptcy would be the model to be followed, shareholders will be left with nothing and bond holders will be shafted by the government. T

GM had demonstrated it could build cars profitably. Since it’s inception Tesla has shown that the more cars it builds the more money it loses. What would be point of pouring tax payer money into that black hole?

Telsa is toast….it was highly dependent on a Clinton administration pushing both solar and electric cars subsidies. Trump isn’t likely to support such a route…and the rest of Congress can’t afford to push it due to budget issues.

Californa…which IS likely to support some further subsidies… SERIOUSLY can’t afford to replace the federal subsidies…but they will likely TRY due to the political pull Musk has built up in Sacremento.

They just have to wait a while and buy all the equipment and components for weight. The real losers will be the suppliers.

It’s bad enough being a supplier to any automaker – or any major corporation for that matter – nervous breakdowns to satisfy impossible delivery ‘schedules’, razor-thin margins, and skids of returns deducted from invoices that haven’t been paid for 120 days come to mind, – but retroactive multi-year price rebates is the stuff of ruin.

“According to one of our Australian Newspapers, Musk is the Teflon man. ”

It has been scientifically proven that Teflon is a carcinogen that causes cancer and reproductive problems, to name a just two health related risks. And yet we were sold on cooking bacon, eggs, and hamburger in the Teflon coated pans over the television for decades. Hopefully, Tesla isn’t using Teflon.

Not only that – It is getting difficult to buy cooking utensils without them being covered with that crap. The machines are planning to kill us all (or at least all those people who cannot afford a 100 EUR frying pan)!

See the Toyota System of modern auto manufacture/ assembly.

There is nothing in a defunct Tesla plant of any use to another manufacturer. The possible exception would be land. land leases, with or without buildings.

The only use of Tesla parts would be if some outfit decides to service the abandoned owners.

Trying to screw suppliers is pretty standard tactics for pre-IPO cash-starved silicon valley start-ups. But Tesla is way past that stage. Even by silly-con valley standards it’s long past time for them to be paying their suppliers. In cash, not stock, and certainly not in hand-wavey platitudes about future double-happiness.

Asking for kickbacks on a contract where the goods have already been delivered and paid for? Seriously? YGTBKM.

It’s really too bad the Tesla fans can remain in their irrational long position a lot longer than I can hang in there on a short position.

“It’s really too bad the Tesla fans can remain in their irrational long position a lot longer than I can hang in there on a short position.”

Hmmmm. It is not my cup of tea, but have you thought to look at Tesla’s suppliers for shorting opportunities? The first domino may be a supplier who does not enjoy “cult” status. And Tesla is not treating their suppliers as generously as Tesla fans are treating Tesla.

“standard tactics for pre-IPO cash-starved silicon valley start-ups”

SOP for the auto industry too, like WSJ says. A colleague who had worked for a parts supplier told us that a buyer from a very big company came around once and said that starting next month, their parts were going to cost 30% less. No back talk. Supplier just had to squeeze those savings out. Not retroactively, though.

Iffy. You don’t want to go bankrupting your vendors, at least not until you’ve lined up some cheap Asian knockoffs. Of course, a sole supplier is going to call your bluff, so you need to be holding something better than a busted flush.

Elon might want to consider demoting himself in exchange for a fat bonus.

A Tesla in orbit redefines space junk!!

Correction: a pile of Tesla bonds in space redefine space junk. ;-)

“Once Tesla loses its ability to raise fresh cash”

modern economics in a nutshell, raise cash, profits are sooooooooooooooooooooo old school

Yup , just like working hard and personal responsibility are Sad world we have created for future generations There is hope though when it all crash’s and burns The reset will be very painful however especially for anyone foolish enough to not be prepared

Macroeconomically, a sad world. Microeconomically, not so much. For those of us who have prepared by living outside the world of money as much as we can, and raised our children to do the same, life might go on relatively serenely.

There was a wonderful cartoon in a UK newspaper during the Dot Com boom days.

A bank manager is pictured handing a loan applicants business plan back with the comment “I am sorry, but there is no demand today for companies that actually make a profit”

In those days all a company Chairman had to do was mention “Internet” and “web site” in any presentation and the company stock was good for a 10-20% uplift as soon as he/she stopped speaking.

The question is, are Tesla bonds less risky than 100-year Argentine, or Mexican bonds? The invisible hand of financial repression works in Tesla’s favor.

This is all gossip. What is the reality? Every passing week Tesla produces more cars, every car produced has a dozen willing buyers… when the cash is needed, it will be found. Musk isn’t running a regular car manufacturer… he’s following the Amazon model.

It used to be said that the primary aim of any business is to bank the customers cheque (and make sure it clears!)

TSLA gets paid when it sells a car, and most will not want to pay until the car is ready for delivery. That leaves TSLA and its suppliers funding most or all of the production costs. TSLA cannot afford to stockpile cars which they cannot deliver for whatever reason because each week another 5-6k vehicles are coming off the line.

I assume the $1000 deposits for the 300+k Model 3 are in an escrow account. It is said that the time taken to refund those deposits is lengthening which does not sound good for escrow money.

“ready for delivery”

Does that include a fire suit ?

Hahaha Good try Nick What about the story on Zerohedge with pictures of the thousands of Tesla’s being stored in a lot in Southern California The Porsche Toucan will outsell Tesla for sure

Correction “Porsche Taycan”

Ummm… no.

Amazon makes money. Yes, it’s a measly amount of money (escpecially compared to its revenues) but it’s positive.

Tesla loses money, and the more product it sells the more it loses. This is not a sustainable business model.

Sorry, but this latest Tesla maneuver against its suppliers smells of extreme desperation.

Woops! Amazon’s model was built on product diverification.

Musk’s is built on two automobiles and a few high-cost futuristic ventures.

Calling all you smart accountants. If a supplier complied with a request for retrospective “refunds” would they have to restate their previously published accounts?

Restating accounts would be a red flag to investors, and any admission that a supplier was agreeing to retrospective “bungs” would impact the market perception of both supplier and customer.

No, you would recognize the adjustment in the period it is made. As long as the original contract was made in good faith.

My guess is the main difference between Tesla and other cash burning enterprises is that Tesla is manufacturing a real world product. It’s much easier to burn thru billions for an extended period while delivering not much more than hype & empty claims. It’s a different story when there’s a physical product to get out the door.

The key to understanding Tesla’s is understanding their debt. They have a $230 million convertible bond due this November at a price of $560.64. It is highly unlike their share price will reach that level by Nov, so they will have to come up with the cash.

But the real problem is the $920 million convertible note due March 2019 at a price of $359.87. If Tesla’s share price is below that level in March, it is highly questionable whether they will be able to make the payment.

So Tesla is betting everything on getting the share price above that level by March. The gigatent, layoffs, production pushes, and shakedown of vendors is an attempt to generate cash flow to prop up the stock price. At the same time, Tesla is refusing to issue equity to raise capital since it would jeopardize their ability to achieve the critical March share price target… potentially creating a liquidity event.

And that is the conundrum Tesla faces. If they don’t raise capital, they are risking a liquidity crisis. But if they try to do so prior to March 2019, they are risking a liquidity crisis.

This is why Musk forecast a profitable Q3 and Q4. That forecast is not a statement of what WILL happen…it is a statement of what NEEDS to happen.

BONUS: For those who enjoy game theory, image you are an institutional investor with a large position in Tesla. What should you do? If all the big investors refuse to sell, Tesla might make their March conversion price and everyone wins. If you start selling, you could trigger a drop in Tesla’s share price that brings down Tesla. But if you move first, the losses will fall primarily on the other large investors. However, if you try to hold the line and another big investor sells first, you could be the one left holding the bag. So what is your play?

Hint: This is known as the prisoner’s dilemma.

But the prisoners will die of starvation well beforehand. As wolf said, the math doesnt work; where will the operating cashflow come from to make it to March?

->So what is your play?

Of course, if I’m hedged to the hilt and have bought up the right politicians to bail me out then I really don’t have to do anything. But let’s assume I was so overconfident and focused on avarice that I didn’t plan ahead, and further assume that the best consultants in Panama are already booked.

Can I hire a body double for public appearances while I consider my options? I’m leaning towards making sure my golden parachute is locked in before I quietly acquire some promising properties (in a country with no extradition treaty) and announce my retirement at the earliest possible opportunity.

You can be sure that I’m not the only one who has put a lot of thought into this. Maybe I should consider a less traditional approach.

Buy some deep out of the money puts maybe?

Yeah. By all means. The casino needs the churn.

Resolute sole proprietorships recognized that they are “victims” of prisoners dilemma. They could go “bigger time” by cooperated with others, but they don’t care.

Among their benefits are: Relative absence of greed and envy and absence of pressure to live up to somebody else’s standard of performance.

And no single proprietor has enough capital to run a major car co.

A proprietor can’t raise money through share sales.

To say Musk should be a single proprietor is to say he shouldn’t be a car manufacturer. That business model is typical of small service ops. plumber etc.

Trey,

This is not much of a dilemma and an easy game to game. The investors need to start buying up large positions in the suppliers and then Musk will get his wish of reducing costs and paying off the new investors with more Tesla paper, all the while capturing his supply chain.

Tray,

Good summary. I would add the production push to 5K Model 3s a week is an attempt to avoid another Moody’s downgrade. Which I think is going to come and would only have a negative effect on share price.

The model S and the supercharger concept is really good. It seems as if Musk shut out the hydrogen fuel cell concept. Unfortunately, the nuts and bolts of manufacturing are hard to master. These are skills that the US no longer has in abundance and the US supply chain is limited as it has been downsized. It would be interesting if a Chinese company acquired Tesla and started shipping an improved model S to the US in large quantities at a relatively low price. If Tesla loses financing in the next year and they have a plant in China up and running that is an easy transition. The Chinese can buy it cheap, keep Elon on as front man and make a ton of money on it.

There is nothing wrong with US manufacturing skills and the 20 million plus car built there last year enjoyed access to an excellent supply chain based largely on the North American NAFTA integration and with overseas parts as needed. It hasn’t been screwed up by politicians YET.

There is no NATIVE Chinese company in the same league (yet) The only cars made in China of exportable quality are branch plants.

We agree on some things. Tesla production of the 3 should go overseas but Hyundai is a better bet than Chery.

The 100 grand S can probably survive here because at that price you can hand build the body, and do on the spot QC and reworks.

It’s the 3 that is killing the patient.

The most profitable car co is Porsche. It does not want to be the car for everyone.

first one out the door wins! Old wall street rule.

I hear a loud boom coming.

You must be standing behind Elon’s unicorn.

raining hot lithium skittels no doubt ..

Are there any Wolf Street readers out there who own and drive a Model 3? If so, what do you think of it?

Car and Driver rates it as 0 to 60 mph in 5.1 seconds with a top speed of 141 mph. That’s very respectable performance, but it does cost $50,000 or more as of April, 2018 when the review was written. “Our Model 3 ends up at $56,000, hardly the “affordable” model by any measure.”

https://www.caranddriver.com/tesla/model-3

Two days after posting this comment, and still no Wolf Street reader has replied back as to what they think of owning/driving a Model 3. Supposedly over 28,000 Model 3 cars have been produced.

I am curious to know how they drive.

I have seen several driving around and parked in SF. Out of hundreds of thousands of cars. So we know they’re out there. But 28,000 vehicles spread over the whole US is really very thin. There are about 270 million automobiles registered in the US. So the Model 3 makes up 0.01%, or about 1 in 10,000. So there would be about two dozen Model 3 owners in the WS readership over the past 30 days, but not many people read every article, and fewer read the comments, or all comments… so the percentages really go down each step along the way.

Also there may be a selection bias – a Model 3 owner might not read an article like this :-]

Why couldn’t you just naked short Tesla below this mark?

Well, it increasingly looks like the next financial crisis will start with Tesla bankruptcy. The business model does no look viable at all. And they have not yet made any meaningful investment in service.

This is the Enron business model.

*****

So it’s in their own best interest to support the shares, they think. A market capitalization of over $50 billion guarantees that Tesla can always raise more billions and burn through them in no time. That share price is Tesla’s lifeblood. Few other companies are so utterly dependent on an astronomically inflated share price for their survival. Once Tesla loses its ability to raise fresh cash to burn through, it’s over

Buying a Tesla reminds me of the Elio offer. Pay money up front and then wait for a product that will be arriving soon, honest. Just pay a deposit to hold your place in line.

Regardless, we finally have a Tesla in our somewhat remote Valley. My son was asked to wire in a new service so that it could be charged. The owner? A US tourist who pulls it behind his $300,000 motorhome. I would think the only purchasers are the super rich.

If a car company wants to be successful going forward, they better come up with some no frills options for the increasing sector of society. the growing numbers of poor. Maybe more Tatas? https://www.tatamotors.com/products/cars-utility-vehicles/

Catering to the top ten percent is more than enough to run a successful business. Besides, Tesla’s China factory will cater to Asia, faster growing and wealthier clientele….and politicians who understand the need to transition toward EV.

Musk has indicated that the Model 3 will be the electric car for the masses.

Tesla already has other, very expensive models that are targeted at the wealthy.

Top 10%? If only. . .

Musk has captured 0.26% of the market even if he caters to only ONE percent.

He doesn’t even have a market, he has a handful of niche or fringe buyers.

The middle class is not going to buy the Model 3 for ~50K because the middle class cannot afford it.

Germany removed Tesla Model 3 from its list of eligible EV subsidized, and there goes the EU. He’s going to pivot to China? Unlikely, but we’ll see.

The tourist is likely from California and received public funding of $7,500 from the Fed/IRS and another $2,500 gift from Sacramento to help ease the burden of towing it.

Elon needs to vertically integrate Spacex with Tesla and stick some solar panels on the rockets and car

I have seen this kind of tactic before, but not in a retroactive sense. I saw an oil company bully service providers, the big enough companies to survive without the work didn’t take the offer. The smaller companies tried until they collapsed.

If any of Tesla’s suppliers are limited to just serving Tesla, they will have to bend and Tesla will drag on a little longer. If all of his suppliers are stable without Tesla, Tesla will be tits up when that March deadline hits.

We’ll soon find out if Tesla is too politically-influential/connected/powerful to fail.

What happens to all those Tesla owners if Tesla goes under?

It’s not as if you could just buy off the shelf parts, and where would they go to really get the car maintained?

Now, in theory, those people shouldn’t care since if you’re rich enough to afford a Tesla, then you probably are rich enough to ignore having to junk it. But still I bet it would just add to the pile of lawsuits that would happen if Tesla went under.

Tesla sells to the aspirational but superficial customer who seeks to show off a certain lifestyle and fill a certain void. The world is full of them. The customers will always be there, but I believe Tesla has over-promised and under-delivered. The demand will likely be pacified by another company, or a recession.

Tesla has lots of cars.People are buying Suv’s and pup’s.

Yikes

The auto industry has evolved into a public utility. Is this guy the Ken Lay of companies who use financial engineering to generate an existing product which is also highly regulated?

It would take all the money in the world to keep Tesla running at this point. Holy moly, they burn $500K a minute, 24/7, seven days a week.

There is no market for the Model 3, or any other Tesla model, in the United States. It’s a fringe of a fringe market, at .026 or 0.26% market share, at best.

The magic of reverse compounding at work!

I was going to short this PoS, but beware of the following: https://www.scmp.com/news/china/diplomacy-defence/article/2155171/chinas-firefighter-wang-qishan-powers-us-business

I think the Chinese will end up owning Tesla.

Maybe, but not anywhere near today’s price. There are already 487 EV makers in China. Tesla is would be #488. Tesla is nothing in China.

Unlikely. Firstly, it’s 50B with a huge goodwill even the Chinese are unwilling to pay. Secondly, owned by China would diminish the Tesla cult status.

If you read the scmp article, the Chinese government is inviting and courting (pitting?) US CEOs to lobby against tariffs. Now, imagine if it was vice versa.

Tesla burned $1.1billion in cash in Q1. This amount of cash pays for the NHS service for about 5% of its annual costs. How does a car company, that doesn’t actually supply cars “burn” a billion. That’s 1,000,000,000 dollars. What do they spend this amount of cash on? Camshafts? If I tried to spend a billion (it’s the ‘welcome back from the holidays year 2 primary school’, what would you spend a billon on) I would be hard pushed – a house, a yacht, a small war in some unknown part of the post- colonial world, free water for sub-Saharan Africa…

Emperor’s new clothes?

Go long the shovel makers!!

All I tell you is it isn’t being spent on camshafts.

Ya, I just left that one alone. I was tempted to say something.

So essentially Musk wants all his suppliers to be UNPROFITABLE, so he can call his own company “profitable” for a couple months. Tesla is way past insolvency, so no supplier should send this crook even a penny.

All those Tesla’s that keep piling up in grounds around California, are in ‘hock’ obviously, as Musk used them as collateral to get more loans, to keep his factories burning more cash to hit his fake ‘goal’ of 5000 cars per week, which is a meaningless number, bc they had to virtually burn the company and its employees to the ground to do it.

Any depositors and recent ‘payees’ (aka suckers) will soon need to get in line behind creditors to ever see a dime of their money back let alone one of these cars. Imagine the defects from this latest run, and abysmal quality. They abandoned QC to meet a lame Elon ‘PR stunt, he called a ‘goal’ ‘. Sick. Just sick. The obama regime aided and abetted this criminal CEO, and taxpayers have lost a LOT of money in the process.

And 20 high placed executives bolting out the door in Q2 alone, following dozens of others in prior quarters, clearly points to the fact that these people want to not have anything to do anymore with this Ponzi scheme.

One has to demarcate between TSLA the business and TSLA the stock.

The business has never been profitable and probably never will be . It once had a significant time advantage over other manufactures, but that time advantage will be completely gone in 2 years as every major auto manufacturer will produce EVs

It once was subsidized by a number of different governments, but that will disappear by 2020.

Its stock is another story , trading at a market cap of over 50b or almost equal to BMW. Investors have pumped up the stock to irrationally silly levels.Its stock price is the underlying basis for its financing.If the stock did not exist , it only means of financing would be VC at considerably lower valuations.

Once the silliness of the tech stocks is corrected, TSLA will have to depend on its business and not its stock to finance future needs. And that future is marginal at best

Tesla makes two main products.

(a) Unprofitable automobiles

(b) so far profitable casino chips – to be played in the market

E.M. can be a bit amoral, so if TSLA has a $10 billion short on it from some cayman hedge fund that is owned by Musk, he could literally go and drop a ton fo bad news, and then get enough money from the puts to go ahead and keep on making cars.

Even if you didn’t believe that there is a cult of Tesla followers, after reading all the empty, meaningless comments about Tesla, and how Iron Man, I mean Musk is going to save the day like superman, should convince you that not only the cult exists, but also how radical, and irrational Tesla fans can be. I’ll be disappointed if Elon Musk doesn’t fly into the sun and comes out from the other side this week to prove to all of us that he is really Superman.

How would suppliers recognize such payments to TSLA? As a loan or rebate?

If they are public companies, would disclosure be required? Is TSLA

required to recognize these payments as revenue?

Definitely sounds desperate, given the public accounting issues.

The ponzi scheme is starting to crack…

Tesla is TOAST.

Shorted it yet?

https://www.zerohedge.com/news/2018-07-24/vertical-group-tsla-may-have-admitted-actionably-false-statements-prior-filings

Is it possible that the usual Musk watchers have missed another income stream that Mr Musk will soon add to his group of cash cows. Namely, transportation to and from burgeoning Chicago airport.

https://www.newcivilengineer.com/world-view/elon-musk-beats-motts-to-chicago-tunnelling-job/10032164.article

Tally Ho