Markets have a way of blowing this type of consensus out of the water.

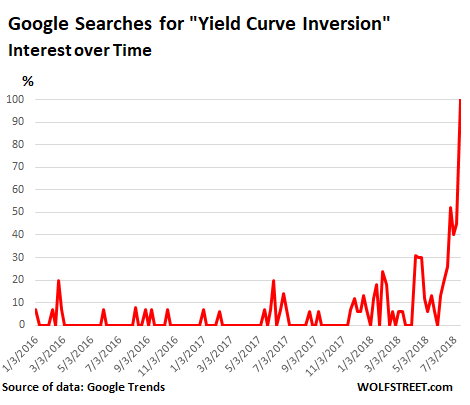

The phrase “yield curve inversion” may not be up there with “Taylor Swift” or “Kim Kardashian,” but it has by now cropped up in the media so often that people are Googling it all of a sudden:

Markets are by now taking this “yield curve inversion” for granted. It’s going to happen, it’s just a matter of time, they say, and whether it’ll be next week or at the next rate hike is not crucial.

This idea that the yield curve must invert is based on the principle that the Fed is raising its target range for the federal funds rate, an overnight rate, and that these higher rates are filtering into short-term Treasury yields, such as the one-month yield, the three-month yield, or the two-year yield. Meanwhile, the 10-year and 30-year yields are doomed to be stuck. And when the two-year yield gets pushed above the 10-year yield, that’s the moment of “inversion.”

An inversion of the yield curve, which happens rarely, has become a popular and accurate recession indicator over the past decades. The last time it inverted was followed by the Financial Crisis.

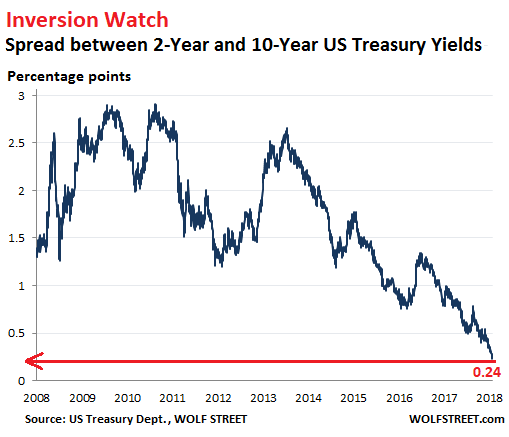

Today, the two-year yield closed at 2.62%, the highest since July 2008. The 10-year yield closed at 2.86%. The difference of 24 basis points is the narrowest spread since before the Financial Crisis.

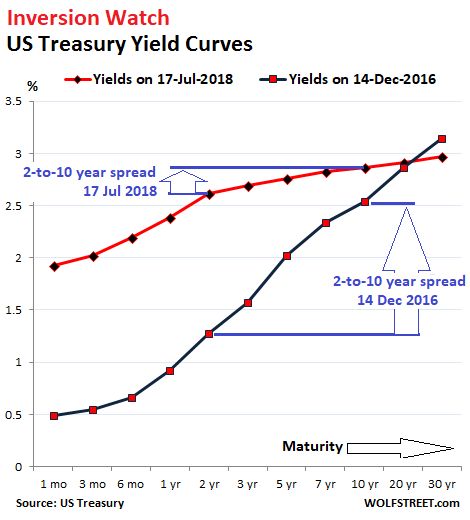

The chart below shows the yield curves on December 14, 2016, when the Fed got serious about raising rates (black line); and today (red line). Note how the red line has “flattened” compared to the black line. The spread between the two-year and the 10-year markers, at just 24 basis points today, is minuscule compared to the 127-basis point spread on December 14, 2016:

If the 10-year yield remains at 2.86%, and if the two-year yield rises 25 basis points to 2.87% (likely by the next rate hike), the two-year yield would be higher than the 10-year yield, and the curve would be inverted.

The chart below shows how the spread between the two-year yield and the 10-year yield appears to be headed to zero – a flat yield curve – or below zero, which would be the inversion moment:

There seems to be an air of inevitability to the coming inverted yield curve. “The Treasury curve is on a one-way trip to inversion,” Bloomberg called it, citing Bank of America Merrill Lynch’s fund manager survey.

According to this survey, only 33% of the fund managers believe that the yield curve will steepen over the next 12 months, the lowest since 2011. Conversely, 67% of the fund managers would expect the yield curve to either stay the same, flatten further, or invert.

The possibility of a snap-back of the 10-year yield, which is infamous for violent snap-backs, is practically removed from this scenario. These fund managers are starting to line up on the same side of the boat.

This is the same crowd whose sentiment peaked at the end of 2016 that the yield curve would further steepen, after it had already steepened sharply for months. But instead, the yield curve changed course at the beginning of 2017 and started flattening—and hasn’t stopped since.

There is no doubt that there will be a recession. There are always recessions. The only question is when. There is a good chance that this might happen starting in 2019 or 2020, whether or not it is preceded by a yield-curve inversion.

By means of QE and ZIRP, or NIRP, central banks have explicitly manipulated bond markets – and other markets – to absurd levels. And in that manipulated scenario, a yield curve has lost its meaning as an indicator of economic realities.

Heck, the Bank of Japan started in September 2016 to explicitly target the yield curve, trying to keep the 10-year yield above but near 0% and shorter-term yields in the negative. “Yield Curve Control,” it called this. And it worked. The yield curve in Japan is precisely where the Bank of Japan wants it to be and is no indication of anything in the economy.

The degree of bond market manipulation is not as pronounced in the US. The Fed is stepping away from its easy-money policies and is turning increasingly hawkish. For many on Wall Street, raising rates and allowing markets to fend for themselves is always a “policy error.” Wall Street lives on cheap money and manipulated markets. And these folks are using the bruhaha about the flattening yield curve as a pressure point to get the Fed to back off its rate hikes.

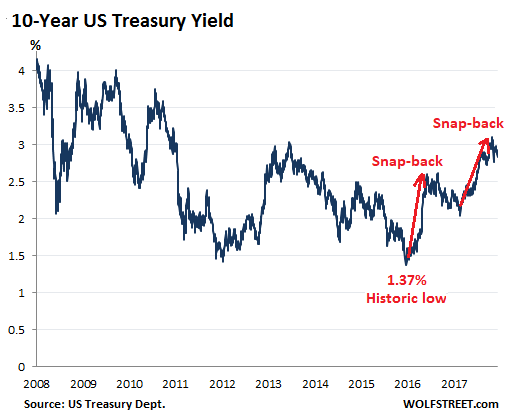

But with so many people lined up on the same side of the boat betting on an inverted yield curve, the contrarian in me thinks that markets have a way of blowing this type of consensus out of the water, and that we’ll see another sharp snap-back of the 10-year yield – of the type we saw:

- Between September 2017 and May 2018, when the 10-year yield jumped by more than a full percentage point, from 2.0% to 3.11%;

- And between July 2016 and March 2017, when the 10-year yield jumped by more than a full percentage point from 1.37% to 2.62%.

The next 10-year yield snap-back would be the third since 2016:

This would steepen the yield curve for a while and get the Fed through several more rate hikes, before the process of flattening would start all over again. Markets, if they’re allowed to do their own thing, just don’t like to follow consensus.

This Fed is getting seriously hawkish: It revealed that instead of thinking about backing off rate hikes because the yield curve is flattening, it’s replacing the yield curve. Read… As the Yield Curve Flattens, Threatens to Invert, the Fed Discards it as Recession Indicator

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, are you going to bet there will be a bit of self fulfilling selling once this happens? Certainly looks that way!

The 10-year is ripe for a sell-off.

So what else pays you guaranteed 3% for 10 years? Or 30 years?

After the sell-off, the 10-year might pay 4% guaranteed for 10 years :-]

Corvettes

I would agree, but to extend my first comment below, there may also be something else going on with regard to demand for long-term U.S. treasuries. Apparently they facilitate a sort of next-level fractional-reserve banking system. As explained by Caitlin Long:

https://mises.org/library/using-blockchain-fix-money-and-capital-markets

There are two ways the consensus can be wrong: either by the curve failing to invert as soon as they expect, or by recession failing to follow inversion as soon as they expect.

Some people write “recession has always followed a yield inversion in the post-Volker era”, but that just means the last couple times. Before that the correlation is sloppy.

Like Japan, the US Fed has also directly targeted the yield curve, through what was called “Operation Twist”. Bernanke wasn’t the first to do the twist in 2011, it had been done by the FOMC in 1961. Those two times were twisting the curve flatter rather than steeper, but anyone old enough to have heard of Chubby Checker knows you twist both ways.

An inverted yield curve makes no sense from the point-of-view of anyone lending their own money. It implies that lending money for ten years is somehow less risky than lending money for two years. Or that the money lent will somehow gain purchasing power in the interim. This is obviously absurd.

The only way an inverted yield curve can be created is for bonds to be bought with someone else’s money, or with money created out of thin air. This is the source of the correlation between inverted yield curves and recessions. Recessions are the result of misallocated capital resources. The timing of the onset of a recession is unpredictable, but an inverted yield curve is evidence that its cause is well underway.

I do NOT understand why people think 3 month is less risky than 10 year. Although it sounds true that longer duration means more “risk”, it is NEVER true for entities that will NEVER default such as a country like USA, especially when US of A is borrowing currency it can print. 3 month or 10 year, there is NO default risk. What you are speculating is what will move for rates and inflation in the next years and longer duration bonds give you more reward if you bet correctly while short term bonds does NOT move if inflation or rate moves.

Your assumption that there is no default risk is in error. The primary victory of a Latina bartender “Democratic socialist” who made economic inequality the centerpiece of her campaign should have the Oligopoly’s Republicrat duopoly water carriers shaking in their boots, as the young people saddled with the staggering unpayable debts bequeathed to them by the Boomers and our feckless politicians will feel no compunction to labor away for a lifetime paying debts their generations did not rack up. Default is ALWAYS an option, especially if populists get elected in place of the Wall Street stooges who currently control the levers of power.

JZ,

You’re correct in that credit risk is the same (practically zero with US Treasuries). But bonds are subject to different types of risks, not just credit risk.

For example, “duration risk” goes up with the length of the maturity. It’s measured by the bond’s sensitivity (reaction of the price to) a one percentage-point change in interest rates. If interest rates rise 1% for that maturity, the bond price goes down. That’s duration risk.

It’s fairly easy to forecast inflation for 3 months, but investors have no idea what happens 6 years down the road or 20 years (with a 30-year bond) down the road. An increase in inflation pushes up interest rates. So new bonds are issued with higher yields than your old bond.

So imagine, you get a coupon payment of 2.8% on your old 10-year T-note, and new 10-year T-notes might come with coupon payments of 5%. If you try to sell your bond, you’ll lose money because potential buyers want a price that is low enough to given them market yield. And holding it, you’ll lose purchasing power to inflation without being compensated for this loss with higher coupon payments. That’s the risk.

Bond investors hate rising inflation. That’s where bonds with long maturities are a gamble.

@Gershon

Replying here since no reply button on your post below. I am also guilty of possibly being stuck in thinking within the context of an outdated paradigm that a select few have moved beyond. If this is true, the few have hit atleast a speed bump.

As far as a US default goes, major countries are all running away from the reaper and the US appears to be atleast lacing up the running shoes so we can continue running a step ahead. Perhaps US writes the rules for a “coordinated default” that is called something positive by the media … after the populist speed bump fades into the distance. Sad but possible.

I agree with Wolf. To emphasis the motive of buyers of long term bonds, I think those “investors/speculators”, in other words, NOT .gov manipulators, buy long duration bonds because they want to speculate/invest based on their rate and inflation forecast. They are NOt coupon clippers who gets puzzled by why would I clip coupons off 10 year while I can clip sale or better coupons on 2 years.

Default risks are usually hedhed by default swaps and rate move is hedged by rate futures product.

To think 2 year rate higher than 10 year rate being “ridiculous” is from the perspective of coupon clippers confusing default risk for normal busineesss with the motive of long term treasury buyers.

Exactly on the timing, etc. Statistics/history show significant variability. The curve can invert, go back to positive (not inverted), for months to a couple of years, and then a recession and/or bear market in equities begins. I haven’t looked at the details in a while, but the lag time between inversion and market/economy problems is variable from near zero time to a few years, if my memory is correct.

Yield curve inversion has been an economic negative since WW2. Most people only look at the data since 1982 since that’s easier to get. The only time since WW2 that there was inversion without an official recession was maybe the late 1960s (depending on your metric), but the stock market took a beating then and didn’t truly recover until like 1982… and young jobseekers were being “employed” destroying Vietnam… so arguing over a “recession” is a bit moot for that case.

There’s a reason yield curve inversion triggers recessions: banks borrow short and lend long. A tight yield curve squeezes bank profitability, forcing a pullback in bank lending together with the Fed’s pullback on monetary supply. In a credit-dependent economy those are put a lot of drag on growth.

I think banks tolerate this because the loans they hold are win-win for them. At some point they’d rather take over the collateral than collect the interest. Others eat the losses and the banks feast on cheap assets afterwards, which they then sell off into the next bubble.

– Nonsense. An inverted yield curve is NOT a “Recession” indicator. It’s a “Risk appetite” indicator.

– Just look at what happened in the previous “recession”. The last recession in the US started in the 1st quarter of 2005 (!!!!!). (source: Steve Keen). The recession in 2005, 2006 and early 2007 was (very) shallow compared to what happened in the rest of 2007 and 2008.

– But the NBER declared that the US recession began in november 2007.

– But when I look at the yield curve then a different picture emerges. The yield curve was inverted from january 2006 up to say june/july 2007.

– The conclusion is that an inverted yield curve is a poor “recession” indicator.

Steve Keen has no standing in calling official recessions in the US. I don’t either. He can have his opinions, and that’s fine. But official recessions are declared by the NBER, whether you or I agree with it is irrelevant. There was an official recession from March 2001 to November 2001. And then the last official recession started in December 2007.

How do we explain the market acting differently than pundits expect? It must be the case that people with money, who do the actual trading, don’t listen to these fools. In fact, they may be using these blowhards as contrary indicators.

The fact that yield curve inversions past recessions has some logical basis. Banks, Reits, and other financial concerns that borrow short term and lend long term get squeezed. They shut down or reduce their activity. Given we live in a debt based financial economy, as opposed to a production economy, that could be a problem. That also explains why inversions preceded the last two recessions.

This media theme about yield curve inversion and the inevitable recession “coming soon” appears like an attempt to create a self-fulfilling prophesy. If enough people batten down the hatches for the recession storm, the recession risk increases. What we have actually been seeing is consumers and businesses finally spending with increased confidence after years in the doldrums … is this making some folks unhappy? The yield curve and recession talk in most media feels politicized.

Beyond that, with inflation increasing, why aren’t longer term bond investors demanding a greater inflation risk premium? The 10 year at less than 3%? So the US market has been manipulated to the greatest extent ever AND other markets still at/near ZIRP/NIRP …does 10 year at <3% seem like a good deal for those outside the US?

Yes, unless the dollar depreciates by more than 3%/year.

I could envision the scenario were the 10 spikes past 4 percent but the dollar within a 30 day time frame crash down to or slightly past a 88 handle.

hmmmm, I recall the lead up to the 2007 recession (when Bush was in office) there was lots of media coverage about how bad the economy was and will be. I was following the economy closely and had an uneasy feeling about the economy, but I still thought there was a certain enthusiasm in the way it was reported and believed there was a political motivation to it.

When Obama became POTUS, after the worst was over, I remember a distinct shift in the tone and theme of reporting on the economy. It was a jobless/crap job recovery but the media tried to paint it in the best light they could manage.

As a disclaimer, I was not a fan of either POTUS and did not vote for either of them. I also thought the office weighed heavy on each of those men, as it should. The buffoon we have in office today weighs heavy on it.

I recall similar themes in 1992. Remember “it’s the economy stupid” that sank Bush Sr. re-election…. the recession that was one of the shortest/shallowest ever as I recall. The poor economy drum beat was incessant and yet few even noticed or recall that recession.

The media cannot tell you what to think (unless you are an idiot). However, media is very well suited to tell you what to spend your time thinking about. Typically they simply release imaginary rabbits they want every to spend time chasing, i.e. ” Recession coming soon …yield curve inversion guarantees it!”

“hmmmm, I recall the lead up to the 2007 recession (when Bush was in office) there was lots of media coverage about how bad the economy was and will be.”

Yeah, although to be fair subprime had already started rolling over by early 2007 (already a few million defaults), the savings rate was negative, and apart from the stock market (which wouldn’t top out until later in 2007), most economic indicators were negative.

“When Obama became POTUS, after the worst was over, I remember a distinct shift in the tone and theme of reporting on the economy. It was a jobless/crap job recovery but the media tried to paint it in the best light they could manage.”

It is still a crap recovery, to this day, but the media continues to paint it in a pretty favorable light. “Goldilocks” job market!

One major difference between early 2007 and today is the spread between 1 month and 30 year Treasury Yield curve rates. Today’s market close has the 1 month at 1.90% and the 30 year at 2.99%; a 1.09% spread.

On 29 January, 2007, the Treasury Yield rates were all nearly the same 5%:

1 month @ 4.95%

6 month @ 5.19%

1 year @ 5.12%

2 year @ 4.99%

3 year @ 4.93%

5 year @ 4.89%

10 year @ 4.90%

20 year @ 5.09%

30 year @ 4.99%

Somehow, the yield-curve inversion seems less consequential than the hundreds of billions in unpayable debts that are piling up in the Eurozone. How much longer can the Keynesian fraudsters at the ECB and Fed keep kicking the can before their financial house of cards implodes under the weight of its own fraud and mark-to-fantasy accounting?

I think the next recession wilo be caused by tariffs stifling trade and promoting investment fear. Yield curve might just be a rear view mirror thing. However, the fact people are discussing it indicates a role in promoting fear and worry.

Along with whatever the IYC means there is:

Most expensive stocks since 1929.

A stock market largely built on Google and Facebook, or on advertising and Amazon, a warehouse and trucking co that does a good job but makes so little money doing it has a PE ratio of 250.

Then there is Tesla with a valuation more than GM. Unlike some other high flyers, this outfit IS Elon Musk who now, with his bizarre hissy fit re: the Thai cave rescue reveals he may actually be crazy.

He is almost certain to be sued for his name- calling, which I do not wish to repeat. Of course he can afford any settlement but he proved he has no self control. We had a foretaste with his moody conference call with financial analysts. Now a different type of analyst is needed.

And leading the flock of Black Swans…..

Bonds represent a promise the Fed and its oligarch handlers have no intention of keeping. The massive, unpayable $21 trillion debt (growing at an exponential rate) will be inflated away by the Keynesian counterfeiters. Only a fool would “invest” in this monetized debt.

Jerome Powell is staying the course on QE-unwind to the tune of $50B/month. That will put price pressure on TYT/10Y notes, and the 10Y yield will rise in concert with the shorter duration yields. Hence no yield inversion, but the stock market, housing market and bind market will ALL drop in value. As planned.

The Fed can save both stocks and bonds by simply halting QT and restarting QE.

The smart money (which is uncannily prescient when it comes to having insider knowledge of what their pals at the Fed are going to do) is betting that that is what the Fed will end up doing.

What “smart money” is that? How do we know what their bets are? Many hedge funds seem to have operated sine 2013 on the assumption that FRB would be a lot tighter with monetary policy than what actually happened. Sell-side analysts are ALWAYS bullish. But what is Wall St doing with it’s “own” money, and how do you know what they are doing?

Wrong. If the Fed was to continue QE, they would blow up the US currency, blow up most fixed income, and generally cause such income inequality as to cause a real civil war. Hungry people don’t buy things. Angry people with guns, shoot. Homeless people tend to invade people with homes. The FED will stay the course. They have little choice. They succeeded in recapitalizing the banking system. Now they have to undo what they have done. Remember, this nations (and the western world BTW) “owners” are going to do what is profitable, not suicidal. If you look at the markets since January, the large institutional money has slowly exited stage left. The smaller funds, home gamers, and smaller investors, traders (and maybe some Chinese escaping capital controls) are the only ones left pushing this market. The 10 year will go up due to supply, and dollars are now being destroyed not created anymore, so they are more expensive to borrow. It will be SLOW, as intended BTW, but the trend is unmistakable. Dollars will gain in value (demand) while things bought with those dollars, stocks, bonds, houses, etc. will go down. Simple supply and demand folks.

Drop in value or in price? Or both?

While I do agree that price paid often is not the same as value received, in this particular case “drop in value” was intended to have the same meaning as “drop in price” ;-)

Sure, I think the 10 year could snap back and temporarily steepen the yield curve. The overall trend going back to 2012 is continued flattening as the economic expansion progressed. The big difference I see now is a Fed that’s suddenly concerned about inflation, with a Fed chair that wants to hike the FFR as many times as the economy can handle it. They also doubt the utility of the yield curve as a predictor of recession despite decades of correctly predicting exactly that. Provided there isn’t a near term inflation spurt that drives up yield on the long bond, we are now bumping up to an area where further hikes run the risk of an inversion. It may not happen this year, but the trend is there.

I think of the power of this signal like this. Imagine it’s 2019, the 2 year yields 3.25% and the 10 year yields 3.00%. Why in the world would someone buy that 10 year bond when they could buy the 2 year? The demand is there because that person thinks when they roll that money over and buy another 2 year bond in 2021, the yield will be far lower than 3%. The bond market is predicting rate cuts in the next two years (recession) and is pricing that in. I don’t have the time, education, intelligence or aptitude to gather and assimilate all available macroeconomic data into a good prediction about where the economy’s going in 6-12 months, but there are major players that can and do — and I can see how their purchases affect the bond market.

@nick kelly

I might be the analyst you are searching for……

The Fed has less control over interest rates than some people think they do. The trillions of QE only reduced the curve by 1% from what it would have been otherwise, according to a study I read.

If they wanted to, Treasury could increase auction supply of 10, 20 and 30 year paper in order to boost long end rates. Maybe this idea is in the works, who knows? Treasury is the elephant in the room of interest rates; the Fed is only a downstream secondary player that has limited control on short term rates.

Todd H. – Exactly. The FED is not large enough to control the entire US treasury market. Not by a long shot. The JCB can control the Japanese market because it is not even close to the size or scope of the US Treasury market. Even the ECB has more control over the Eurobond market than the Fed over treasuries. The Fed follows the market. If they were dumb enough to try to go against the market forces, they would end up committing a real “policy error”

Mad as Hell,

The Fed has no size limitations. Theoretically, it can buy the entire pile of marketable Treasury securities, down to the very last one, all $15 trillion of them, if it chooses to do so. It won’t. But it can.

Gerry at BOOM financial has been extremely helpful to me when discussing the yield curve and linked me to this wonderful dynamic chart:

http://stockcharts.com/freecharts/yieldcurve.php

You can play with it to your heart’s content. Wolf is bang on the money here, the Fed have control and may well steepen the curve as they increase rates. But a recession is due, if only to clear all the malinvestment accumulated to date and open the gates to a new era of prosperity going forward.

But a recession is due, if only to clear all the malinvestment accumulated to date and open the gates to a new era of prosperity going forward.

Oh, Peter, your innocence is touching. The agenda of the Fed and its oligarch owners is not and has never been “a new era of prosperity.” Rather, it is concentrating all wealth and power in the hands of a corrupt and venal .1% in the financial sector, while consigning the 99% to pauperization, debt servitude, and economic serfdom.

Gershon,

Please remove your political discourse and leave the leftist buzzwords at the front door.

To put it in language you’ll find palatable: the Federal Reserve is going to raise rates and eventually trigger a recession because the alternative leads to wage inflation, which is antithetical to the interests of the capitalists who control the Fed. Capitalists will find it more profitable to purchase assets at discounted prices rather then the current inflated prices, and more profitable to make loans with wider spreads. After all, banks borrow short and lend long. The interests of the public are not directly represented in these considerations but it’s axiomatic that a rising tide will eventually lift all boats.

Note: this is essentially the same logic that Gershon presented, just phrased using the banker-approved linguistic framing.

Most Fed conspiracy theorists are right-wingers, FYI.

It’s not just Democrats who are concerned about the growing chasm between the very wealthy and most everyone else. Jerome Powell, a Republican, recently expressed concern that not all workers were reaping the benefits of our booming economy.

Here’s a blurb from an LA Times article cited below:

“We want an economy that works for everyone,” said Powell… “In the last five years or so, labor share of profits has been sideways. This is very much akin to the flattening out of median incomes over the last few decades.”

http://www.latimes.com/business/la-fi-federal-reserve-powell-20180717-story.html

NotBuying,

Please remove your political discourse and leave the leftist buzzwords at the front door.

First, I’m no leftist. Second, both “left” and “right” – misleading labels in my opinion – can unite around one basic precept: the State should resume its rightful role of looking out for the common good, rather than being an adjunct of the corporations and Wall Street sociopaths. Neoliberal economics has enriched the oligarchy at the expense of everyone else, and now finally the screwed-over former sheeple are becoming awake and aware and are starting to fight back. The first step is to reject the lies and propaganda of the corporate media and instead seek out real news and real truth in sites such as Wolf Street. The second is to back independent candidates who will fight for the 99% against the political prostitutes of the oligarch-captured Republicrat duopoly.

The fight is just beginning. You need to pick a side: the banksters or the people.

If prosperity means a renewed/continued credit cycle that buys economic growth then I don’t see why not. Can’t imagine how ‘just’ a recession would reset our gigantic debt bubble though.

I thought the 1% already owned 99%. Surely their can kicking is because they fear social unrest from any real solution.

Whatever happens I can’t see the US ever defaulting on dollar treasuries, it’s not necessary with it being fiat currency under their control and I don’t think any side of the policical spectrum would benefit from a default. Surely the next generation will just use the same playbook as their parents and try and inflate the debt away?

Agreed – But let me pose this thought question to you: What good would having all of the concentration of wealth, if the world is fighting instead of working for you? They know the deal – basically, bulls make money, bears make money – pigs get slaughtered. If they keep QE going, they are the Pigs. Why not just re-adjust back to normal, and short / sell everything effected by the downturn (reset) , then take those spoils and switch position back to buyer when everything returns to normal? The asset buying / money is dead trade is done. Now it is money = valuable / assets are too many, and take too much money to service trade. That has been, and is still the cycle. Manipulated (conspiracy theory of control) or simply nature is completely irrelevant, it just is. The smart / wealthy go with the wave, not fight and ask why.

My best Captain Obvious prediction tells me:

The next recession, as in the past, will be felt at different times, by various regions and sectors.

I would also imagine that those who were slower to recover from the last, will feel a greater impact.

Delta airlines just canceled all of their new hire pilot classes for the rest of the year. Interesting when one sees that they have 358 mandatory pilot retirements this year and increases in mandatory retirements for the next ten years. Does Delta airline management see recession in the near future?

I Googled this and could not find a trace of your statement. So could you please cite a source? Thanks.

What I found instead was that, as of July 17, 2018, Delta is looking to hire over 8,000 pilots over the next few years, and that there is a pilot shortage.

https://www.cnbc.com/2018/07/16/help-wanted-delta-seeks-8000-pilots-flight-attendants-may-apply.html

I’m a Captain with SWA. My new hire First Officers who have recently separated from the military have told me that their buddies from the military have received letters from Delta that say they have been hired, but it will be 6 to 8 months before Delta starts any new hire pilot classes. A First Office (new hire military pilot) I just flew with was explaining to me how the military pilots have to give their respective branch 4 month notice that they plan to separate. He explained how much this has thrown a monkey wrench into his military friends plans, who have planed to leave the military to go fly for the airline, but to do so as not to be unemployed in the interim. I have no other source for you. However, please understand pilots are a very tight fraternity and military pilots even more so.

Thanks. Good enough for me :-]

The QE in the Euro zone and Japan helps maintain resilience in the US equity, long bond and HY markets hence dollar strength, firm financial asset prices and tight spreads. They may find it difficult to end QE without complications, hence this influence will not abate soon. The widening of spreads in Europe has far different implications than in the US. The presence of such a large distortion in market signals contributes to yield curve distortions in the US.

The problems are much larger than a recession on main street, ie since when does main street matter? The first problem has to do with government spending, and that has to do with government credibility, which in turn has a lot to do with the Fed. However congress can pull the rug out from under the Fed policy to provide a base for the (dead) fiscal spending package. Whether credit contracts or rates are too high for business to push through their costs, same result. The Fed could back off, (market thinks so) but the current EM dumping of US denominated bonds has an effect. The Fed has plan A, and government planners are already to plan C. The Cyber Cold War with Russia could replace the war on Terror (we just need an event?) which would suck up available government spending without any concomitant benefit (like Reagan’s Cold War I) for main street Americans. We bankrupted Russia in Cold War I, now they return the favor.

The central bank plan obviously intends to support debt by keeping interest rates low and promoting inflation. The side effects are permanently high asset prices and permanently high wealth gap, permanently low productivity, and an economy with little or no real growth. Debt is transferred to the public ledger through permanent deficit spending. The debt is then effectively retired through a permanent increase in central bank balance sheets and “money printing”.

The inflation that would normally result from money printing is offset by the decreased productivity and concentration of wealth. The permanently high asset prices prevent anybody from investing in productive assets or businesses. Stock buybacks, M&A, and dividends become the norm, and this exacerbates the problem.

This process can continue for a long time but it gradually causes the economy to shrink, wealth to concentrate, asset values to rise, and living standards to decrease for the masses.

The central banks and politicians consider this obvious and foreseeable long-term destruction of the economy more attractive than a short-term recession, which would allow the necessary defaults to occur so debt balances can be reduced.

If the Fed ends it tightening program before asset values decline, this will be a clear indication it intends to shrink and economy and living standards of the masses for the indefinite future. The masses don’t benefit from high asset prices. They benefit from good jobs, wage gains, and real business investment.

Expect the yield curve to be flat until the Fed and other central banks have the courage to tackle the problem, not perpetuate it. The economy and yield curve will return to normal only when the central banks quite suppressing interest rates, supporting malinvestment, and monetizing debt.

“By means of QE and ZIRP, or NIRP, central banks have explicitly manipulated bond markets – and other markets – to absurd levels. And in that manipulated scenario, a yield curve has lost its meaning as an indicator of economic realities.”

I don’t think this is as self-evident as you believe it is. I’m not saying you’re wrong, but I’ve seen some fairly cohesive and convincing arguments that it’s actually the exact opposite.

The fact that we might be inverting as such low levels (if we do, in fact, invert) may be an even stronger sign of an impending poor economy, rather than an irrelevant sign, as you suggest.

That being said, I love a good contrarian trade, and the consensus in fixed income markets is more often wrong than right, but I have a hard time seeing a 4% 10-year. Where it’s going to come from, inflation, growth, both?

Inflation continues to be low– gosh, remember at the start of the year when people were FREAKING OUT about wage inflation and inflation finally booming? How quickly that faded. Apart from those who beat the drums of how inflation is constantly on the horizon, it’s largely become a non issue again.

And now we’re going through the same false notion of “global synchronized growth” which, of course, is being knocked down pillar by pillar for the false narrative that it is. One by one, they fall.. Eurozone inflation lower than expected: check. Japan inflation lower than expected: check.

The Fed in their latest meeting upgraded the economy from “strong” to “very strong” — the fixed income markets and yield curve is telling them they are very wrong.

Personally I think the Fed is freaking out behind closed doors. I suspect they’re feeling very 2007-ish, when they did the same thing… hiked in the face of fixed income markets telling them things were already getting bad.

The Fed has one more tool to manage longer-term rates, although it’s an indirect one.

The Fed has macro-prudential regulatory authority over the banks, particularly the large ones. It can also work with the other bank regulators. If the Fed and other regulators were to begin raising reserve requirements and using other regulatory tools to constrain bank lending, particularly in longer-term loans (corporate bond purchases, construction loans, issuance of fixed-rate mortgages), that would crimp loan supply and put upward pressure on longer-term interest rates.

Given that the long expansion has engendered the usual Minsky-type “stability breeds instability” risks, tightening up bank capital levels and other macro prudential regulations would be a good idea anyway. As a fringe benefit, it would also position the U.S. banks to better survive the inevitable recession compared to overseas competitors.

It doesn’t look like anybody is paying any attention to the Taylor Rule, or its various modifications (the last being a 1999 version), but the Fed Funds rate has been running well below the prescribed rate according to the Taylor Rule since at least 2014. The end result is always asset inflation, tulip fever, followed by a bust. This last happened in the early to mid 2000s, when rates were held too low for too long to deal with the recession of 2000-2003, and we know how that turned out. Strangely enough, the Fed still publishes nice looking graphs and charts that talk about the Taylor Rule and its variations:

https://www.federalreserve.gov/monetarypolicy/2018-02-mpr-part2.htm

https://www.federalreserve.gov/monetarypolicy/2018-02-mpr-accessible-part2.htm#figC4

When I first started investing, around 1985, everything I read said that price earnings ratio and things like the Shiller 10 PE were a good reflection of a stock’s fair market pricing. Fairly valued Shiller PEs were around 10-15 at that time, a go-go “momentum” growth stock could go up to over 20-25.

I look at the numbers today and it’s just mind boggling. The Shiller 10 PE of the entire stock market as of today is 32.6! Most of these are not go-go momentum stocks! Even at the very bottom of the market of the last big crash, on March 1, 2009, the Shiller 10 PE was 13.3.

Growth and increased profits are the true fundamentals that drive stock price, and some of that great inflation of stock price has been a combination of new technology (e.g., the smartphone, which made Apple into a global phenomenon, and the various technologies of Google and Amazon), and some of it has been globalization – the products of successful American companies now sell in huge markets like China and India, which greatly amplify their profitability. Globalization is what has amplified the potential profits of any rapidly growing company with a successful business.

So, if you don’t believe in globalization, and the POTUS is actively, but in a rather destructive scattershot manner trying to rein that back with an unfocused general trade war, and the Taylor Rule(s) tell you that the Fed has been building up a stock bubble …. I don’t know, I smell a rat here, something has got to cut loose.

Another interesting phenomenon is that while corporations have been using their Federal Deficit funded tax cuts to buy back shares of their companies at these hugely inflated prices, the CEOs themselves have been selling the same stocks in record amounts – which is fundamentally dishonest shareholder abuse – they are in essence touting their stocks to the public while selling it quietly out the backdoor.

https://money.cnn.com/2018/07/17/investing/insider-selling-stock-market-buybacks/index.html

The yield inversion? Will it happen or not? Who the heck knows. I continue to maintain that internal and external geopolitical influences can cause economic disruptions as much as anything, and this is something that simply has not been covered in this forum.

The stagflation of the 1970s was fundamentally caused by the rapid rise of oil prices, from about $3 a barrel to over $12 a barrel, and then over $36 a barrel (in 1970s dollars).

http://chartsbin.com/view/oau

This in turn started because the U.S., under Nixon sent massive amounts of military aid to Israel during the 1973 Yom Kippur War, to save Israel, and the Arabs reacted with the Oil Embargo. Later, in 1978, the disruptions in Iranian oil production from the Iranian revolution caused a second oil price surge.

Nobody could have predicted these external events, but the hints of these events had been simmering in the background for a long time.

The world remains an extremely unstable place, and Trump’s erratic behavior and deconstruction of everything that has been built up in the way of alliances and the mostly stable foreign policy of the last 60 years is highly likely to encourage further such misadventures by all sorts of adversaries around the world.

The last such foreign policy tyro of a President that had such a poor grasp of how foreign policy worked and how it affected the economy was Jimmy Carter, and it was his refusal to support the Shah of Iran that set off that second oil shock in the 1970s.

Foreign policy matters, and internal/external geopolitical forces matter hugely, and Nixon and Carter are proof of that.

Here’s the reference for the historical chart of the Shiller 10 PE, which I forgot to include:

https://www.gurufocus.com/shiller-PE.php

(also posted to the other thread about Russia dumping Treasuries by mistake)

iPerhaps US writes the rules for a “coordinated default” that is called something positive by the media … after the populist speed bump fades into the distance.

Setarcos,

News flash: populists aren’t about to “fade into the distance.” Right now only an infinitesimally small percentage of the population is awake and aware, but as the corporatocracy escalates its financial warfare against the 99%, more and more of the sheeple are going to see the light and start fighting back. Trump ran as an economic nationalist and toppled the Goldman Sachs stooges that the Republicrat duopoly offered as “choices.” A populist routed the corrupt Establishment “choices” in Mexico’s recent elections, and is openly talking about standing up for the people against the rapacious neoliberal looting that has had free rein in Mexico for the past thirty years. An Italian populist won in Italy and is standing up for his people against the banksters and globalists and their ECB accomplices. As the central bankers and their oligarch cohorts ramp up their financial warfare against the 99%, more and more populists are going to emerge to lead the fight against these criminals and sociopaths, and their captured Establishment political parties and media propagandists. Bank on it.

So Wolf, how does the curve looks in the Eurozone?

Who cares if the Yield curve becomes inverted, its when the inversion begins to end is the really problem.

Just look at the chart.

https://www.forexfactory.com/attachment.php?attachmentid=2851996&d=1528984611