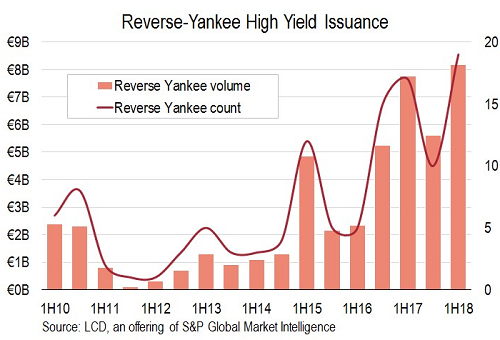

“Reverse-Yankee” Junk Bond Issuance Hits Record.

It’s paradise for US companies looking for cheap money. They range from sparkly investment-grade companies, such as Apple with its pristine balance sheet, to “junk” rated companies, such as Netflix with its cash-burn machine. They have all been doing it: Selling euro-denominated bonds in Europe.

The momentum for these “reverse Yankees” took off when the ECB’s Negative Interest Rate Policy and QE – which includes the purchase of euro bonds issued by European entities of US companies – pushed yields of many government bonds and some corporate bonds into the negative.

By now, yields in the land of NIRP have bounced off the ludicrous lows late last year, as the ECB has been tapering its bond purchases and has started waffling about rate hikes. Investors that bought the bonds at those low yields last year are now sitting on nice losses.

But that hasn’t stopped the momentum of reverse Yankees, especially those with a “junk” credit rating.

Bonds issued in euros in Europe by junk-rated US companies hit an all-time record in the first half of 2018, “taking advantage of decidedly cheaper financing costs in that market,” according to LCD of S&P Global Market Intelligence.

In the first half, US companies sold €8.2 billion of these junk-rated reverse-Yankee bonds, a new record (chart via LCD):

These bonds are hot for European investors who are wheezing under the iron fist of NIRP that dishes out guaranteed losses even before inflation on less risky bonds. Anything looks better than bonds with negative yields.

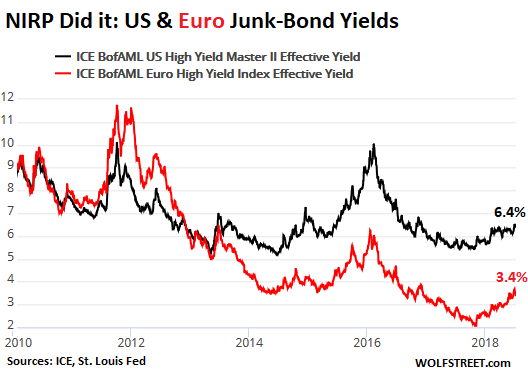

And here is why it makes sense for US companies to chase this money: It’s still ultra-cheap particularly for lower-rated companies. The chart below shows just how much sense it makes for the companies – though investors are going to have their day of reckoning.

The euro high-yield ICE Band of America Merrill Lynch index currently shows an average effective yield of 3.4% (red line). These are junk-rated companies!

The equivalent index for the US shows an effective average yield of 6.4% (black line). This is a spread between the two of 3 percentage points – thanks to a different central-bank regime.

Also note how during the euro debt crisis in 2011 and 2012, junk-bond yields spiked in both markets, but a lot more in the Eurozone where the average effective yield of euro-denominated junk bonds shot into the double-digits:

As the chart shows, the average euro junk-bond yield, while still ludicrously low at 3.4%, has surged from even more ludicrously low levels last year, when it fell below the 10-year US Treasury yield, a hilarious distortion that I pooh-poohed a few times not without some relish. In October 2017, the average euro junk-bond yield fell as low as 2.08%.

At the time, investors took sizeable credit risks on those bonds and are getting paid less than the rate of inflation to take those risks. Those investors are now getting punished. When yields rise, bond prices fall by definition. Investors can either sell those bonds at a loss or hold them to maturity at a yield of just over 2%, if a default doesn’t x out that option.

In terms of reverse Yankees, they’re ultra-cheap money for US companies. For investors, they’re engaging in similar credit risks with those euro-bonds as they do with dollar-bonds issued by the same US companies, but they’re getting paid only about half as much to take those risks!

I’m just in awe of how central-bank policies have blinded investors to risks and have altered rational thinking.

And yet, the US high-yield market – both for bonds and leveraged loans – is still richly valued as well, and yields are still very low. Credit is flowing easily and in large quantities despite the Fed’s ongoing efforts to tighten financial conditions – or “remove accommodation,” as it likes to say. And this ebullient junk-bond market in the US will see higher yields and lower prices. So the chart above is comparing one ebullient market (black line) with a vastly more ebullient market (red line) – though both markets have already taken a licking and are facing bigger lickings.

Rising interest rates have a peculiar effect. Read… Leveraged-Loan Risks Are Piling Up

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“…I’m just in awe of how central-bank policies have blinded investors to risks and have altered rational thinking.”

One could say that having a child is a 30-year investment in one’s genes. The uncertainty before one starts seeing returns on this investment is colossal. Yet, people have been taking the long odds for millions of years.

Since a rational person would never take these odds it’s safe to conclude that we all carry a fair amount of insanity in our genes:)

I know you are just joking, but at least from the perspective of the gene, that bet is the most rational investment, as the flipside involves risk of extinction.

“extinction” for who? Science proves that *you* will become “extinct” regardless of what you do. Your body *will* die permanently. The “investment” in offspring has always been to supply extra workers in the farm (or factory or mine) and to look after the parents as they prepare for their extinction. Throughout the history of humans children have always been quickly put to work in one way or another. So your analogy does not hold up as children began “producing” well before 30, and thus the cost was justified. In this current overpopulated & polluted society, I see no reason at all to waste resources in such a cost center. Save the costs to be able to pay for someone else to care for you while you wait for your extinction. I have no idea why anyone should care one dot about “the species” at all: let it “extinct” away as its future will have nothing to do with [dead] you. This is the pure Logical Scientific Newtonian Darwinism on which the current holy financial system is based.

As I said, from the gene’s perspective (not the individual)

Why should we care about the future. What has the future ever done for us?

Modern medicine has thrown a wrench in natural selection for the human specie.

That is just irrational exuberance, not worth paying attention to by the obviously superior minds at the ECB.

That’s b/c nature saw fit to imbue MORE pleasure plexus nerve endings in the LOWER part of the spinal cord than the UPPER!

Ironic that 3.4% is considered “high” yield!

1) 3.4% as high yield??? I’m currently earning 2% on a MM fund. No capital loss risk like a passbook savings account of old (only less yield, they paid 5% for decades – people sneered – 8% on an IRA CD was considered not personally embarrassing). Yes, 2% is low but last year it was less than 1% and not worth the effort.

2) Now looking into some floating rate high yield funds. These are bank loan funds with short duration and flexible rates to the borrowers. Low capital loss risk, especially now that rates are maybe a couple of percent from the normalized rate. Share price variation is surprisingly minimal.

3) The big enchilada … the US yield curve. Short end rates are influenced by the Fed and they are going up and up and up. Long end rates are influenced by central banks who don’t want to see their world end. (Who could possibly be keeping the yield curve flat???) Venezuela proves that the market always wins, although the start of the catastrophe always proceeds at an infinitesimal rate, but also like a juggernaut, with exponential growth to the bad for those who want to keep the fantasy alive. (Hello Euro)

4) The big unknown: After the US yield curve goes negative in six months (2s10s) due to unlimited funds keeping the 10 rate year low, what’s next????? Will the curtain be pulled back and will people suddenly get smart as a result? Or will a really good excuse buy some more time for those holding the artificially low rate bag?

Or, if the 10 year jumps in relation to short term rates, and does it quickly like a spring being uncoiled at once, what will that do to the debt market for a while??? Personally, I expect a panic, some market liquidity issues, but the US will adjust nicely to normalized debt, thanks to a strong and strengthening economy.

Europe … not so good. Kick the can and ECB continental financing only works for so long, even if it looks very respectable and officials act huffy towards others. My guess is ECB kablooooweee in one way or another, or the EU starts looking more like China to compensate (see below).

Japan is a mostly closed system in another universe. China is strongly managed. Both will be OK for a while no matter what.

Also, about why investors bought into NIRP: If you’re thirsty and need to drink or die and no water is on the horizon, you will dip your cup into anything liquid and hope that what happens is better than the certainty from not drinking water. Central banks know this. This is why NIRP only works if everyone does it.

The Fed doesn’t do it and won’t for at least two more years. Hopefully never ever. This is also why the rest of the world is screwed and in an extremely slow motion but sickeningly massive train wreck from a financial perspective.

Personally, I think this event will rank above the Tulips, the South Seas, and everything else considered a major scam in History. The big difference is that is was the govt screwing the people world wide to help favored few. 1000 years from now, people will wonder ‘Why???’

“Who could possibly be keeping the yield curve flat???”

Corporate America?

After retiring I took a job as a part time teller in a small savings bank. I have been there a year and a half and we have had more rate increases in the past 5 months than they had had the previous 2 years. We currently offer a 3.00% yield on a 3 year CD. I expect it may go up as we are expanding our mortgage business and need additional funds.

The central banks have achieved their objective of making assets very, very expensive. They have explained that expensive assets are a net positive for the economy and they have been put in charge because they know what’s best for the economy, right?

So, even though you have been told, on many occasions, nearly free money for companies and investors is a benefit to us all, you people still complain as if it’s a bad thing.

Just sit back and enjoy the bountiful economy they have created for one and all and set your mind at ease, after all grown-ups are running the show and they must know what they are doing, right? They all have PHD’s, do you have a PHD?

Let them continue their courageous work, they would not destroy the world’s currencies without good reason.

BTW, central banks announced to the world, in advance, they were going to destroy their currencies so don’t pretend you didn’t have time to plan.

Phd stands for “Piled higher and deeper”, right?

In a world searching for yield everyone but you is looking to make money anywhere except in stocks. The U.S. stock market is the biggest bubble of all times past, present and future.

“These bonds are hot for European investors who are wheezing under the iron fist of NIRP that dishes out guaranteed losses even before inflation on less risky bonds. Anything looks better than bonds with negative yields.”……………………………………………..It’s almost like the next financial crisis is being offshored to Europe or any other nation that does NIRP, and I’m not sure if that’s bad.

I think it is important here to see the larger picture, and not lose that out of sight. Both the Rothschild US Federal Reserve policies and Rothschild EU ECB policies are policies of one and the same master that is playing out a theatrical scenario here for the world to behold, so that no one sees the manipulation behind it. No one is going to benefit, except the few that control this global NWO ponzi scheme.

MAGA! Bring those financial crises back home!

Concommitant with this missive an article today @ Bloomberg about junk related debt.

https://www.bloomberg.com/graphics/2018-corporate-debt/

“…I’m just in awe of how central-bank policies have blinded investors to risks and have altered rational thinking.”

Okay, let’s talk about ‘risk’.

History clearly shows that any troubled major corporation can be bailed out at taxpayer expense (thank you for your contribution) if it can just avoid imploding overnight from the sheer weight of its own inequities, practically eliminating risk and making the capital asset pricing model obsolete at the same time.

Perhaps investors see things more clearly than you are prepared to give them credit for. Portfolio valuations over the last couple of years clearly show that rational thinking doesn’t feed the bottom line nearly so well as adoption of the post-fact paradigm.

There has never been a Nobel laureate in the Forbes 400. Diogenes disagreed, but the Greek proverb says it is better to be rich than to be a philosopher, for we see philosophers haunt the doors of the rich, but the rich do not frequent those of philosophers.

But 50 bps increase is too much and unnecessary right?

Most financial institutions don’t pay their bond portfolio managers enough to attract the best in the business. So if they are lucky, they get average returns, which probably include some bond defaults.

You have to consider that people are exchanging Euros for this junk debt. Maybe they are thinking the Euros aren’t worth much because of the endless QE. Can you blame them?

But they are getting paid back in Euros, so not even USD exposure.

It’s a lose-lose-lose investment

The Fed tightening is a fraud by definition, tightening on main street, not Wall St. The Corporate High Yield market (HYG) hasn’t suffered at all. The cassandras calling for a high yield event have it backwards, the frog getting boiled is those highly rated bonds whose return goes negative more quickly than junk. Here’s a question if all the debt globally gets downgraded one notch, would anyone notice? Or is it like the fX charade on competitive devaluation, a winner for every loser? Either way the debt bubble continues, and the worst is first.

It’s a sad “market” that central banks have created. You have to take crazy risks in the stock market at all time highs, or sit on your cash and lose value as they print new money for the wealthy bankers. There is nothing in between. It’s like the Deer Hunter. You have to play Russian Roulette or rot in the rat hole.

Well that’s the whole point of the system – turn everyone into a financial speculator/gambler by forcing them to become so in order to provide for their future, in order to drive markets.

No more paying into your pension fund and getting a safe, steady compounded 6% PA – that facility has been taken away from us Deliberately.

And under the ‘rules’ of the same system, if you don’t game it and are left short then that’s just your own silly fault, not the fact you’re slaving away trying to make ends meet and don’t have the time to research or the money to risk.

It’s another symptom of the smashing of the social contract and the glorification of greed.

MD…..Great synopsis. Our leaders have betrayed us. They destroyed the value of our hard earned money to benefit themselves and corporations. I don’t just blame them though. Americans got greedy too.

Real Estate is in between. Cash out refi and flip apartments for $$$

Central banks have flooded the planet with easy money and it is running out of crevices to flow into.

If you are a pension fund and you need to stuff a billion dollars some place you don’t even have the option to put it in cash. Any bank or money market you park your money in could be insolvent overnight so you have to put the money in bonds no matter how much the ECB makes them pay.

So you can see why institutional money is running into the stock market even though the S&P yields a record low dividend of just 1.6%. The stock market often has sudden drops but it never goes insolvent overnight and because of that it is one of the safest places to park money – regardless of trading at insane levels.

Money continues to trickle up from wage earners to wealthy investors and the investors are left scrambling to find anything and anyplace to park the bounty of booty shoveled into the their coffers. And that is why ASSETS WILL CONTINUE THE INEXORABLE RISE. Cash is trash, only gamble what you are willing to lose in cash. Cash is just too risky to hold.

“And that is why ASSETS WILL CONTINUE THE INEXORABLE RISE.”

Yeah, you say that to any investor in gold and silver. Or are they not assets? Can you pick what asset will be inflated next or deflated? Will money come out of real estate then go into gold one day or hog futures, who knows?

Yet on a global basis the US QE rolloff is a drop in the bucket and according to Naomi Prins, the other central banks have taken up the slack where the US is drawing down.

I doubt on a global basis there will be an ‘global QE’ for many years to come. This year stocks are protected by buybacks, but next year I wouldn’t count on it.

When I refer to “assets” I’m talking about productive assets, not great hunks of metal that lay around collecting dust and consuming wealth to pay for safe storage.

A better asset would be the vault used to store the gold, at least you can collect rent on that asset.

The belief in gold is more a religion or cult then an investment strategy.

And yet if there’s no “valuable” things like gold that require storage, you can’t collect rent on the asset. Whether something is valuable or not is also belief.

Belief in the omnipotence of the central banks, and that the rise in bubblicious assets is ‘inexorable’ is the cult-like groupthink, my friend.

But keep speculating away in your massaged, illusory markets – I’m sure nothing can go wrong.

The people who put all their life savings into tulip bulbs had a better chance than the people today in U.S. stocks. The DOW might hit 100,000 but will end up at 1,000 very shortly afterwards.

As they say there is one born each minute.

The sad thing is that when this bubble pops it affects pension funds.

Ah whatever, you work until you die anyway, right?

Gold is used by Central Banks as collateral for them and to lease out for collateral to others. Gold was about $100 an ounce in 1973 and today it is about $1240. Losing value over decades!

I wouldn’t say investors are blind to the risks, so much as willfully kept in the dark by the banksters and their captured Establishment politicians and media. The schemes and scams of the central bankers are creating huge systemic risks that could literally bring down the global financial system, yet the corporate media assures the sheeple that Everything is Awesome – buy moar stawks!

Meanwhile, by deferring the inevitable financial reckoning day with their endless can-kicking, our Keynesian central bankers and central planners are ensuring that when it does show up, it’s going to be cataclysmic. And the corporate media will intone, as usual, that “Nobody saw it coming.”

https://www.livemint.com/Opinion/2DjIse0nDA6j818tVtfTUN/Europes-remarkable-ability-to-remain-in-denial.html

what is “the media”? It’s all the hollywood studios that provide “news”: Universal (NBC colossus), Paramount (CBS), Disney (George Stephanoapulus), Warner Bros (Erin Burnett), oh,…..and Fox! They might as well yell “Cut” at the end of the news segments. And people are so well informed

The stock market is based on a believe system. You have to believe/assume that there will be some investor/sucker who will pay more for the imaginary shares you just purchased on line from some broker you have never met. There are imaginary rules to the game. If earnings beat some conjured up expectation, then the stock will hopefully go up because speculators/investors/greater fools will see it as more valuable and you will get a profit.

This all works unless the company admits that things might not be as good in the future or someone called an analyst says the same thing in concepts that no one understands–like discounted cash flow.

There is one thing that always occurs. Just like death and taxes, bull markets always end in bear markets. The only question is trying to guess he date that the bear market will occur. Since the ability to discern that date is unlikely, the only smart thing an investor can do is leave the party before the music stops.

You can always get back if you leave too early. It much harder from a psychological stand point, to take those losses once the plunge begins.

The smartest thing an investor can do is jump from the stock market ponzi into a new unfolding ponzi. The only chance you have in ponzi’s is getting in at the start. 95 percent always lose everything in ponzi’s and it won’t be any different with the U.S. stock market ponzi.

As to bull markets always end in bear markets – The number and severity of these Bear markets alluded to seem to decrease, as Bear markets are shown as blips, decrease, as time goes by. (Way by) Long term equity investers have fared well through every Bear market. Maybe?

If the difference between high yield debt of the same credit quality is 300 bps (6.4% minus 3.4%) then what is the arbitrage and why hasn’t that difference been arbitraged away?