Highest level since April 2011. It’s not just the Brick & Mortar Meltdown anymore.

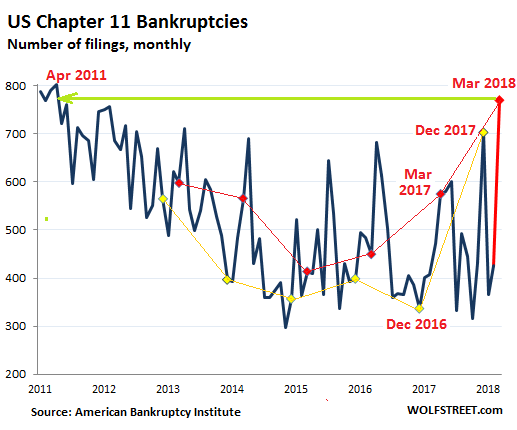

New Chapter 11 bankruptcies in the US spiked 63% year-over-year in March to 770 filings, the highest number of filings for any month since April 2011 (when there had been 789 filings as companies were still trying to emerge from the Great Recession).

This chart shows Chapter 11 filings back to 2011, based on data from the American Bankruptcy Institute. The last six Marches are marked with red dots. The year-over-year jump of 299 filings in March is the second largest year-over-year jump for any month since the Great Recession. It is behind only the jump of 366 filings last December, which had set a post-recession record. The yellow dots represent the last six Decembers (more on that in a moment):

A company files for Chapter 11 bankruptcy protection from creditors in order to try to restructure its debts under the supervision of a judge. This normally involves are large reduction in debt and the transfers of part or all of the ownership of the company from pre-bankruptcy owners (shareholders) to creditors. Most often, shareholders lose everything. Some unsecured creditors too lose everything. Secured creditors are often made whole. And many creditors in between get a haircut, in return for some ownership. The hope is that the company can “emerge” from bankruptcy with less debt and keep operating.

Bankruptcy filings are seasonal and usually peak in April, along with tax season. So the March jump doesn’t augur well for April.

The low points in Chapter 11 filings normally occur late in the year, before or in December, except last December when filings spiked 61% from November, to the highest level for any month since April 2013. In March, it got worse when Chapter 11 filings spiked to the highest level for any month since April 2011.

While the December 2017 spike was truly special, in January and February, filings were close to where they’d been a year ago, and I thought, OK, maybe December was just a blip. But now there’s the March spike, the second highest spike since the end of the Great Recession.

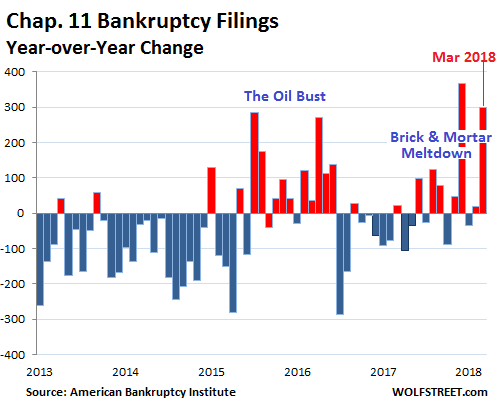

The chart below shows the year-over-year change in Chapter 11 filings. This eliminates the effects of seasonality. Red bars indicate that filings rose from a year ago. Blue bars indicate that filings fell from a year ago. Note the effects of the oil-and-gas bust in 2015 and 2016 and more recently the effects of the brick-and-mortar meltdown; but now it’s not just the brick-and-mortar meltdown anymore:

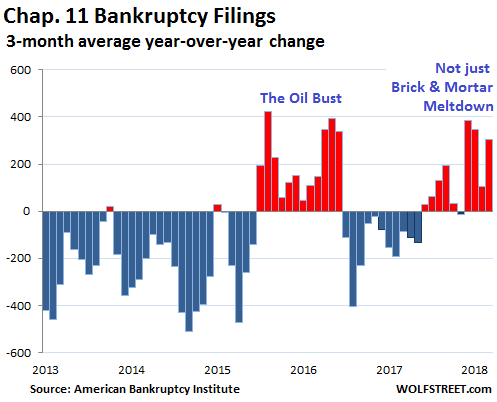

Monthly Chapter 11 filings are volatile. To smoothen out the volatility and eliminate the effects of seasonality we can look at the year-over-year changes as a three-month rolling average. For example, the three-month average year-over-year change for March is based on January, February, and March. And then the image becomes clear: There is a problem, and it’s not a blip:

The by now well-documented Brick-and-Mortar retail meltdown is responsible for part of it. Retailer bankruptcies of all sizes have been piling up in large numbers since 2016. They all started out as Chapter 11 filings, though many of them later turn into messy liquidations, like Toys ‘R’ Us.

Back on January 8, when I discussed the horrendous spike in Chapter 11 filings in December, I figured that there must have been another cause. The economy is doing OK. In Q4, it was stronger than it had been in prior years, when bankruptcies were much lower. And retailer bankruptcies alone wouldn’t cause that kind of spike. I speculated that that the advent of the new tax law had a lot to do with it.

Creditors and shareholders of failing companies knew that they could write off losses in 2017 under the old corporate tax rate of 35%, thus getting the government to pick up 35% of the tab of their losses via lower taxes. In 2018, the new tax law adds uncertainties, but shareholders and creditors knew that losses incurred in 2018 would face the new corporate tax rate of 21%, and so the government would only pick up 21% of the losses.

But in March, this logic no longer applies. So it looks like the December spike was a mix of tax consideration and a sharply deteriorating credit environment for companies.

This is a sign that the economy has arrived at the end of the “credit cycle.” The Fed is trying to push up interest rates and tighten financial conditions. Weak companies are starting to have a harder time refinancing their debts. And those that succeed face higher borrowing costs. Some sectors are getting hit harder than others, such as brick-and-mortar retail, which had a terrible March. But this is now spreading in other sectors, such as specialized subprime auto lenders.

Subprime auto-loan delinquencies have surged to the highest rate since October 1996. Scores of smaller specialized lenders have piled into this field after the Financial Crisis, some of them backed by private equity firms. Three of them have now collapsed into bankruptcy or were shut down. Allegations of fraud and misrepresentations are swirling through the bankruptcy filings. Read… Subprime Carmageddon: Specialized Lenders Begin to Collapse

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

When anyone (well, anyone but everyday people) can borrow tons of money at zero interest or very low interest, a lot of companies can look healthy. It’s only when the bills come due that the dirt hits the fan…

Or, as I believe H.L. Mencken said: “…the rich are different from you and me-they have more money…” (or perhaps these days, given the now-fungible definition of ‘money’, more credit access at better rates…). Thank you, as always Wolf, for your tireless efforts in providing the numbers of the various trucks that continue to plow into us average folks. May we all have a better day.

The Truck is just over the top of the hill! And the hill rises through the clouds.

Thanks for the great info as usual! ahohhhhuuuu

Not Mencken. It was Hemmingway.

“How did you go bankrupt?”

Two ways. Gradually, then suddenly.”

― Ernest Hemingway, The Sun Also Rises

“This is a sign that the economy has arrived at the end of the “credit cycle.” The Fed is trying to push up interest rates and tighten financial conditions. Weak companies are starting to have a harder time refinancing their debts. And those that succeed face higher borrowing costs.”

The Fed is to blame. The plan is to cause an economic collapse now so that Trump can run for reelection in a rising economy that he will be able to take credit for.

If that was their plan they’re too late because there’s no way this is going to be a little blip recession. You’ll get your Democrat in 2020, don’t you worry.

I hope we get another FDR.

I know right? We definitely need more government, more international mayhem like the lend-lease program, more centralization and more Ponzi schemes. /sarc

Seriously, what President or Congress since FDR has been the opposite of FDR? They all look similar to me. Spend, spend, spend, drop bombs, a chicken in every pot, spend, spend, spend, drop bombs, a chicken in every pot….

Won’t the rising economy be based on – just more borrowed monies at a higher rate?

More castles in the sand?

OTOH, retailers typically file BK in Q1 and if this is primarily retail driven, then we should be seeing a spike now. BK’s also lag the economic stress in the business and retailers have been under severe stress for 2+ years now. Not saying there isn’t a wider issue, as increasing rates may be taking their toll on zombie companies, but seems like an industry breakdown would be in order.

But the numbers and charts are comparisons to the same period last year, and to the same period in prior years, precisely to eliminate the effects of seasonality, as I pointed out in the article.

…. and the Fed says:

“Things are so bright, you need sunglasses to even look at the economy

we created.”

Sunglasses do not protect zombies. For the later to survive they need those clothing retail companies, but oops those have gone bankrupt as well.

If only the oldest zombie of them all i.e. Warren Buffet can be exposed. But nah America will bend over backward to help him as much as possible.

Translated: The books are cooked – don’t look.

Raising rates sure seems to start the melt down. Will they back off before it gets bad? Probably not.

Nah

The question is, “Why should ‘they’ have the power to do anything?”

Another Monday, another Dow head- fake. Down 500 + on Friday so there MUST be huge uptick on Monday.

Sure enough there was, for a while. Then it evaporated in the afternoon.

This pattern is becoming so obvious you have to wonder if the same people juicing the early market are the same ones selling before the close.

If so, who is the meat in the sandwich?

My guess: the ‘buy the dip’ guys.

I noticed this for the last month or 2. It is so obvious that I am starting to wonder if it is a computer generated algo the sells to end the week and promptly buys at opening on Monday.

The first guy to sell on Fri (or Thursday because of Good Friday) seems to win and cause the drop for the day. The market then opens for a new week and goes on a 3 hour buy streak until noon Monday depending on how big the drop was the business day before.

Looks like the zombie unicorns are falling from the sky, no more cheap debt to keep flying.

The infamous “0% Interest rates” from years ago have birth to a lot of “Keep going thanks to taking debt” companies like Uber. Also it made leveraged buy outs quite easy, and made companies in trouble willing to take cheap debt to keep going.

All if that has been crashing down for a while, at least since 2017.

Those who got out of enough debt before it started to get too expensive are gonna last for a while more.

Those who didn’t are gonna crash and burn. Don’t you love the smell of burning zombies?

FED: I told you man, I told you I was gonna raise the rates.

Zombie Company: ARRHH! FIRE BAD, FIRE BAD!

Of course that’s the not only reason, some companies just don’t work out, or have failed products, or are outright scams. Remember Juicero?

Banks should be banned from even touching subprime loans.

Leveraged Buyouts should be illegal.

People should be smart enough to not invest in companies that are in so much red it looks like they are at the botton of the red sea.

But then again, we never truly learn, do we?

Many restaurants closing by me. And I live in a big city.

Good Who needs dem stinkin restaurants anyway?

That has been coming since years ago. Big cities like New York have way more restaurants that they need and many are barely scrapping by or operating at a loss.

The fact that as soon as people started to go out to eat less a lot of them were gonna die is well know.

Is almost a cycle.

Every time economy booms going out to eat becomes popular and big cities get filled to the brink with restaurants. But then comes a crash, people eat out a lot less and many restaurants disappear.

Rinse and repeat

Really, because people who eat out a lot don’t cook – at all.

So what are they eating – a Big Mac with fries & coke is just as pricey as a meal in a inexpensive restaurant.

They have scaled down to cheap eats & a soup kitchens once a week.

Restaurants need to be flexible if they want to survive, as the economy slides into the pit of despair, they need to be more creative to keep the customer fed.

Indeed. McD’s is as expensive as Denny’s or IHOP.

The really poor people have scaled down to soup kitchens indeed. When I was in my 20s, McDonald’s was an almost non-existent luxury, the same when I was growing up. I’d go to the market and get a baked chicken leg/thigh section, or a package of lunch meat, really cheap but high nutritional value things. No prepared salads, I’d get a cucumber or some tomatoes. I’d get different grains and things, rolled oats, slivered almonds, etc and make my own “granola” that I could pour milk over and eat for breakfast. Much of the time my breakfast was just a couple of glasses of milk with just enough Nestle Quik in it to make it a little sweet.

The real “McDonald’s” of the poor are the taco trucks. You can get really good tacos for a dollar or so each.

Can you please provide a direct link to the first chart regarding US Chapter 11 bankruptcies in the American Bankruptcy Institute’s website?

The charts are mine based on the raw data I received from ABI. You can get this data by going to the linked ABI site, hover over the tab “Newsroom” and click on “Statistics.” There you can download the data in spreadsheet format.

Thanks a lot Wolf.

I looked at other charts in ABI’s website and then I realized your chart here is for Commercial chapter 11 filings only. The chart for Total Bankruptcies is different, we don’t see an increase like Commercial. So my question would be how to correctly analyze this? What importance do other bankruptcy chapters and consumer bankruptcies have when we want to analyze the whole market?

1. The fundamental problem currently is that our productive capacity (worldwide) has seriously outstripped demand (and is likely to get increasingly worse, thanks to automation), à la the 1930’s. That has combined with an income distribution which (as in the 1920’s) increasingly favors the rich– reducing the overall consumptive capacity. Brace for a depression worse than the 1930’s. What do we do with all that production when only the 0.1% can afford it?

2. This time, the game was kept going beyond all reason by all sources (especially governments) providing ‘unlimited’ amounts of cheap (credit) money to all and sundry. But that has a limit– at some point the non-governmental lenders become more cautious than greedy– and the ball starts rolling downhill. Unfortunately, unlike “real” money, “credit” has a time limit!