But one-third of voting slots are vacant: What will the “New Fed” do?

There was a sense of relief today the Fed didn’t state clearly that there would be four rates hikes in 2018. And this was interpreted as a sign that the Fed is sticking to three rate hikes.

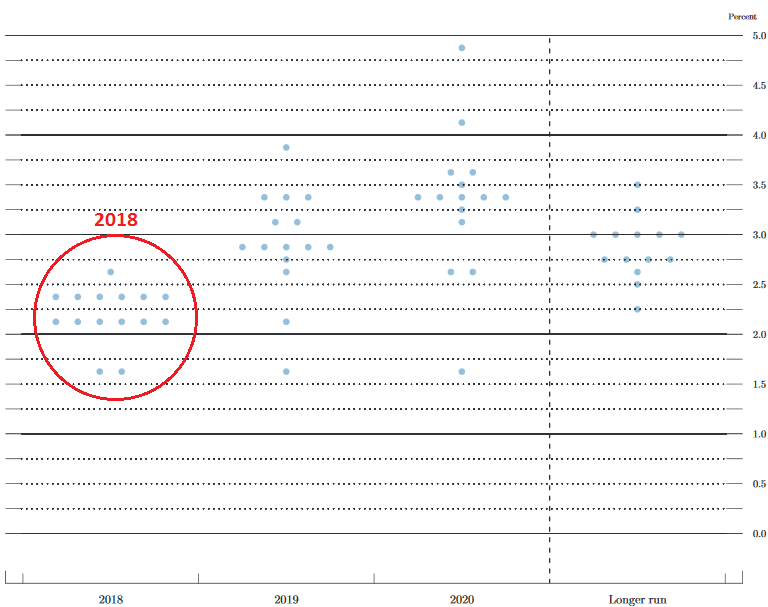

Not that the Fed ever states anything clearly on rate-hike days. But it does supply a lot of tea leafs to tea-leaf readers. And one pile of tea leaves is the “dot plot” that it releases four times a year, including today.

Today’s rate hike is included in the dot plot. After the 25-basis-point increase, the Fed’s target range for the federal funds rate is 1.5% to 1.75%. Rate hike number one in 2018. The “dot plot” picks up from there.

The “dot plot” is where the FOMC members indicate their projection of where the midpoint for the Fed’s target range for the federal funds rate should be by year-end. It indicates how many rate hikes each member of the FOMC envisions for 2018.

According to this dot plot, the median projection by all 15 FOMC members today is 2.1% for the federal funds rate at the end of 2018, 2.9% at the end of 2019, and 3.4% at the end of 2020. Below is the dot plot (click to enlarge, red marks added). These dot plots change a lot over the years. So the projections for next year and out are not critical. But the projections for 2018 are, and we’ll get to them in a moment:

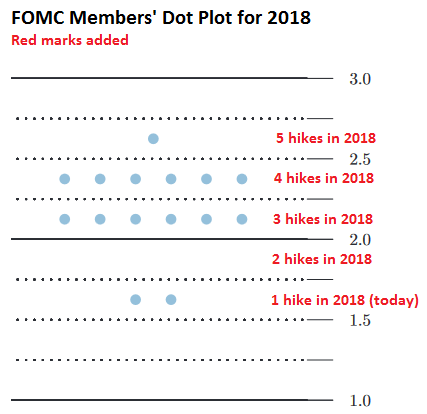

For clarity, I have enlarged and isolated the dot plot for 2018 and annotated it in red (below). Note how tight it is compared to those for future years: 12 of the 15 members are spread evenly over the three-hike and the four-hike camps. It shows that the range of disagreement is fairly narrow:

So the dot plot says that as of today:

- Two members see just 1 hike for 2018 (today’s)

- Six members see 3 hikes in 2018 (including today’s)

- Six members see 4 hikes in 2018 (including today’s)

- One member sees 5 hikes in 2018 (including today’s).

In short: If just one member of the six in the 3-hike camp switches to the 4-hike camp, the entire dot plots switches to a median projection of four rate hikes this year. All it takes is one member upgrading the projection by one hike. This is how close the projections are to four rate hikes.

But monetary policy is decided by vote, not by dot plot. And there are some historic uncertainties this year, including four vacant slots at the seven-member Board of Governors, which forms the core of the FOMC. These four future members will be voting as soon as they’re sworn in. But we still don’t know who the are.

The Board of Governors is an entity of the federal government, unlike the regional Federal Reserve Banks, which are owned by their member banks. The policy setting FOMC consists of the seven (now three) members of the Board of Governors who have a vote at every meeting; the President of the New York Fed, who also has a vote at every meeting; and the governors of the remaining 11 Federal Reserve Banks, who rotate annually into and out of four voting slots.

With four unfilled slots at the Board, the FOMC had only eight voting members today. When the four slots of the Board are filled – each candidate has to be nominated by the President, confirmed by the Senate, and sworn in – it will have 12 voting members. In other words, one-third of the future voting members are unknowns.

In addition, William Dudley as New York Fed president fills a slot that always votes. But he will retire over the next few months as soon as the New York Fed has decided on a replacement. This is the fifth voting slot, out of 12, that is still an unknown for later this year.

It is likely, in the current political landscape, that the new members will have a slightly more hawkish disposition on average on monetary policy than those who occupied those slots before them. The fourth rate hike this year is within a hair in today’s dot plot. And the New Fed still has to take shape.

These dang trillions are flying by so fast, they’re hard to see. Read… US Gross National Debt Spikes $1.2 Trillion in 6 Months, Hits $21 Trillion

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I assume all those dots are provided in braille for the learned folk at the Fed

And what if the guys who wants five votes for four because is close enough?

Way I see it, is gonna be four because of the hole left due to the tax breaks.

Of course, the chairs are vacant. Nobody wants to be known by name in the case of a collapse.

And that collapse is gonna be a doozey

It’s too late – Greenspan, Bernanke,Yellen,Powell, and their merry band of flying monkeys.

As consumers, we don’t generally like price fixing schemes. No economist would say price fixing is effcient ….or without adverse ramifications. Yet we have this mother of all price fixing schemes sitting atop all industry and economic activity.

Perhaps the FED is independent, interested in the economic well being of the US, and apolitical. Keeping rates at zero for so long appeared to demonstrate the exact opposite. If the new guy isn’t also a political hack, he doesn’t deserve what he has walked into.

A famous line comes to mind: “Bull markets do not die of old age- they end when the Fed raises rates.” When asked about rising rates causing a recession yesterday, Powell blew it off. But I think he is whistling past the graveyard. Look out below- there goes the stock market!

The Fed’s role is to pull away the punch bowl at the moment the average American wage slave is poised to get a raise.

Kent- you are so right! When asked why the Fed was raising rates even though wages are flat and inflation is very low, he bumbled that they still expected inflation to go up. When asset prices are in a bubble, it does not concern the Fed. But when the (highly inaccurate) employment numbers improve and it might mean that workers get a raise, then the Fed is on high alert, poised to clamp down on the economy!

Wolf, you planning on doing a writeup on how the LIBOR has doubled over the past year? Seems ominous to me…

The dollar LIBOR is dependent on the dollar rates, in the US, such as the federal funds rate, the 1-month Treasury yield, and the 3-month Treasury yield. They all skyrocketed!!! You’ve seen my charts. Put the dollar LIBOR chart and the 3-month Treasury on top of each other, and it all makes sense. I have no idea why the financial media is making such a big fuss out of it. What did they expect? That the dollar LIBOR is tied to euro rates?

I think when it is in between lines it means 2 or 3 rate hikes. If you look at long term, the dots are on the lines.

Don’t think so, dots are between the lines because it is the midpoint as the Fed essentially targets a range [1.5-1.75] and not a specific point rate (1.75%).

Looked at another way, even using your logic, if you count from the bottom up, since one rate increase is in the pocket already, it is a 1-2 hikes and not a 0-1 hike expected?

They need to have a number from which to decrease rates , when that moment arrives. Being “data driven” seems to mean waiting until there’s an avalanche of data available.

They’re just building up ammo for the next crash which will probably be on Trump’s watch and, of course, blamed entirely on him.

For good reason it will be. Bankruptcy expertise will not help him here. Trump is an army of 1 and owns all this mess. No loss. Happy to see him fail. He has done nothing to succeed nor help anyone but himself. Story of his life. Just ask all the Bunnies he knows…. :)

The NY Fed will choose someone who will go with the program set by the next incarnation of the globalists. Any goofy theory they promote to print money and lower, possibly to negative, rates to finance asset bubbles and debt monetization will be supported by the new NY Fed candidate. Main Street will suffer from a lack of interest income but this person won’t care. Not his constituency.

Hopefully, the balance of the positions will be filled by normal people who understand income from interest comes from rate normalization and the result is spending and a growing economy on Main Street and wealth spread around more widely.

I think you could gleen more from the dots on a cabi’s bum. The Fed has created and popped two huge bubbles in the past couple decades. They’ll pop this one too, and the graph is meaningless. I wonder what their silly graph looked like in 1999 or 2007.

Maybe I just haven’t look at the last to crashes enough. But it would seem the inflated asset prices of today are clearly a direct result of the Feds QE. Which puts them in a new position compared to the last 2 bubbles which were not direct products of fed policy.

From a casual perspective, it seems market lows are never retraced, except in the case of the 2007/2000 lows which gives you pause.

Well, looks like there’s one precedent (in the S&P) of 1970/74

And we all know what happened then. Let’s call it a regime change.

Bernanke in ’05 – “we have never had a decline in house prices on a nationwide basis”.

The Fed’s “price of money” was a significant contributor to the housing bubble. Without significant excess credit in the system, that bubble could not have formed.

So many other factors as well, which have largely gone unexamined in mainstream media. Thanks for sites like this one where there is an emphasis on real information. Pretty sure those factors have been covered here in the past, but one in particular I would point to was how the Community Reinvestment Act was used as a stick with the banks in the 90s.

Red herring. This was perhaps an 800 billion dollar housing problem turned into a 20 trillion dollar asset problem via securitization and credit default swaps. The fact that the slice and dice guys deliberately and hopelessly mixed up the good mortgages with the bad, then securitized them, then banks used those securities to run up their leverage by declaring them “assets” and creating loans based on the fictive value of those assets, then for good measure all became each other’s counterparties in credit default swaps based on those securities–that’s what threatened the global economy. If the originators had held the loans, it would have been another S&L scandal and been put behind us years ago. It was the way financial capitalism has morphed since then that turned it into a global crisis.

@James

Was involved in lending admin in early 90s. Regulators used a big stick. To meet the new “targets”, the FI could a.) make high risk loans to certain groups, b.) decline good risk loans to certain groups. Only real option was “a”. Now, what to do with the high risk loans? …hence emphasis on secondary markets, CDOS, etc.

So the Fed had a role in the asset bubble from a monetary and regulatory perspective. The things you cited certainly did happen as well, but later.

“Which puts them in a new position compared to the last 2 bubbles which were not direct products of fed policy.”

Last 2 bubbles were also due to the Fed policy on interest rates (not QE). Looks like they could stem the tide with interest rates. Also in hindsight they thought they could do it in 2008 too but it did not work so they introduced all the acronym money and added QE to it. The point is interest rates were not enough. I also feel 2008 has scared them to such an extent that they went all in. Not only the Fed but ECB and BoJ. Now they are in a box and I am watching and waiting to see how they extricate themselves.

IMO, they CANNOT as all assets have been blown sky high and it will blow them up. Imagine the size of QE they are going to need.

The rubber is definitely hitting the road in 2018. I rub my hands in anticipation.

https://www.federalreserve.gov/monetarypolicy/reqresbalances.htm

There is something more interesting than rates, its inflation, and the 2020 projection shows inflation will barely budge, which you might assume is the result of these rate hikes and rates have nothing to do with economic growth and inflation does

Powell could fumble and get promoted to Treasury Secretary. That’s what happened to Miller back in 1979 when he got outvoted by other governors. The Blue Wave should leave our President in a foul mood. Thus far those moods seem to result in some functionary being relieved.

It’s the worlds biggest three card monte game.

Most people can’t think of future ramifications

of Fed policy so they wind up paying the price.

Hard to make long term decisions when you

have immediate issues to deal with.

I don’t know, but, the way I see it is, around 10000 baby boomers are retiring every day. This would mean roughly 300000 are leaving the employment scene every month. How many new jobs are we actually creating. Does the employment data take into account this?

Also does the demographics of all these Baby Boomers pulling money from 401 K’s support the Lofty Stock Market ???

The real question is, who is going to be presenting the options from which Trump will pick, because this is not a man who is going to engage in due diligence and seriously research and vet the candidates. Most presidents are dependent on their staffs on most issues. Trump has no coherent staff, and is even more prone to listen only to people he trusts (rich idiots like Adelson et al.) than most of his lamentable recent predecessors. Perhaps the scariest thing is, the results might be the same, and it really won’t matter, because everyone at the top is pretty much on the same page and they are driving off a cliff while whistling happy tunes about robust employment and growth.

I just don’t see 4 interest rate hikes this year. As we speak the trade war has started with China. In for a turbulent time in the short term.

Storm Brewing Rate Hikes , Fed Unwind, and Government overspending . I wonder if there will be enough buyers for all those Treasuries ???

There will be for Treasuries, but not at today’s yields. Yields will have to be more attractive to pull in more buyers.

I’b be more worried about junk bonds, stocks, commercial real estate, and the like. When liquidity dries up in the junk bond market, no one is buying anything until prices are destructively low and yields sky-high.

They are floating volumes of Tbills and the bid to cover has been abysmal. To get back to LIBOR I have read the denials that this reflects a credit problem, but of course it does, credit costs more, and as Doug Noland says, this is reflected in the cost of derivatives, risk insurance, which leads to risk aversion. This is esp poignant for foreign investors in US markets trying to hedge our dodgy dollar. For now the corporate high yield market is big enough that nothing moves it quickly. LIBOR puts a bid under the FED rate hike program and it’s a very shaky floor, and we saw yesterday the market is fighting the Fed. Never seen anything like this, really.

If the FED is serious it dumped a truckload of bonds into this buying frenzy.