But some flat spots are showing up!

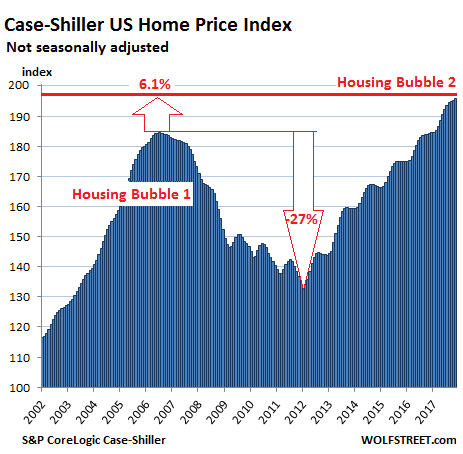

Just after I reported on the minuscule 1.4% year-over-year growth of per-capita “real” disposable income and the lowest saving rate in 12 years — for the lucky ones — there’s another asset-bubble doozie: The S&P CoreLogic Case-Shiller National Home Price Index for November, released this morning, rose 6.2% year-over-year (not-seasonally-adjusted). The index has now surpassed by 6.1% what was afterwards called the crazy peak of Housing Bubble 1 in July 2006 and is up 46% from the bottom of Housing Bust 1:

Real estate prices are a result of local dynamics but are also impacted by national and global factors, including monetary policies and foreign non-resident investors trying to get their money out of harm’s way. This causes local housing bubbles, operating on their own schedules. When enough of them occur simultaneously, it becomes a national housing bubble. See chart above.

The Case-Shiller Index is based on a rolling three-month average; today’s release was for September, October, and November data. Instead of median prices, the index uses “home price sales pairs,” for example for a house that sold in 2010 and then again in 2017. The index provider incorporates other factors and uses algorithms to adjust the price movement into an index data point. The index was set at 100 for January 2000. An index value of 200 means prices as figured by the algorithm have doubled since then.

Here are the most magnificent leaders among the housing bubbles in major metro areas:

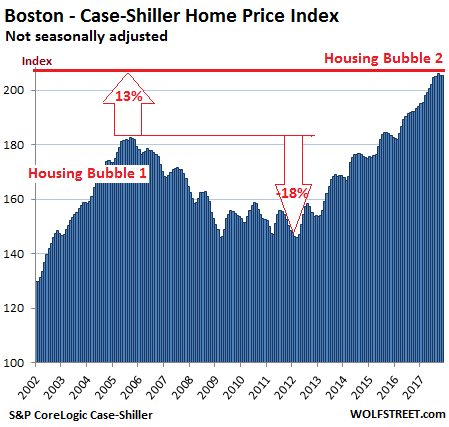

Boston:

The index for the Boston metro area edged down again on a monthly basis, the second decline in a row after 22 months in a row of increases. It has essentially been flat for four months but is still up 6.3% year-over-year. The slight monthly decline could be within the normal seasonal variations but there were no seasonal variations during the relentless surge in 2016 and 2015. During Housing Bubble 1, from January 2000 to October 2005, the index for Boston soared 82% before plunging. The index now exceeds the peak of Housing Bubble 1 by 12.5%:

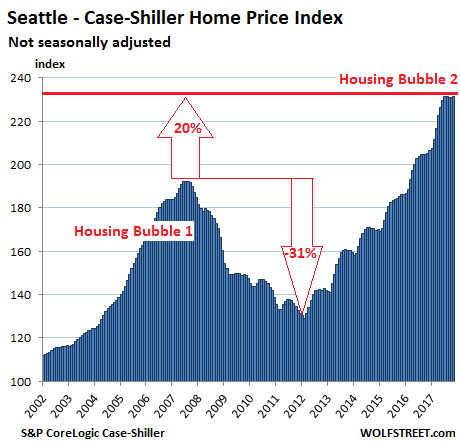

Seattle:

The Case-Shiller home price index for the Seattle metro ticked up a smidgen on a month-to-month basis, after the first two back-to-back declines since the end of 2014! It has now been flat for the past five months. However, flat spots or slight declines in the index this time of the year were not unusual before 2015. The index is up 12.7% year-over-year, 20% from the peak of Housing Bubble 1 (July 2007), and 79% from the bottom of Housing Bust 1 in February 2011:

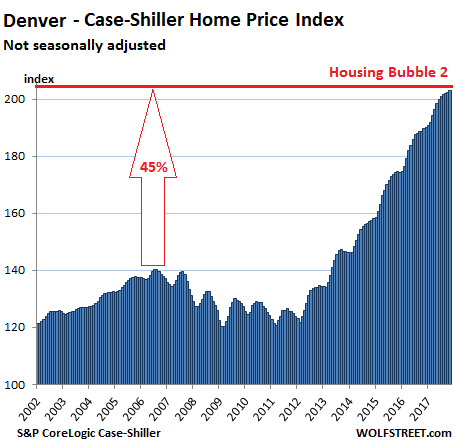

Denver:

The index for the Denver metro ticked up again on a monthly basis, the 25th increase in a row. It is up 7.0% year-over-year and has surged 45% above the prior peak in July 2006. Instead of the craziness of Housing Bubble 1, Denver experienced more “normal” home-price increases, and was therefore also spared the ravages of Housing Bust 1. But in 2012, Housing Bubble 2 erupted in full force:

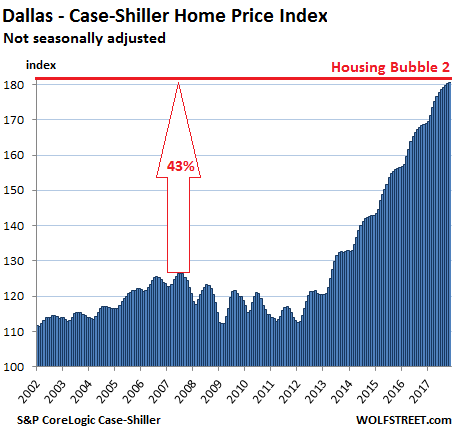

Dallas-Fort Worth:

The index for the Dallas-Fort Worth metro ticked up again on a monthly basis — the 46th month in a row of increases. It is up 7.0% year-over-year and 43% from the prior peak in June 2007. Like Denver, Dallas experienced saner times during Housing Bubble 1. But prices began to surge relentlessly in 2012:

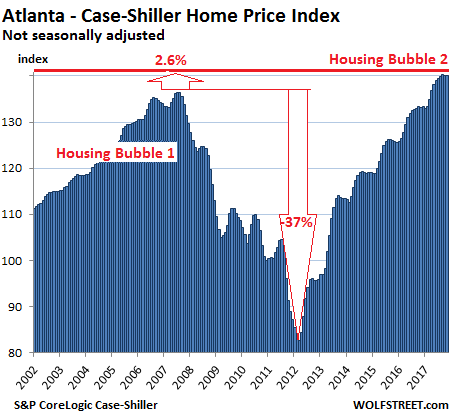

Atlanta:

The home price index for the Atlanta metro has now been flat (actually down a tiny bit) for three months in a row, in line with prior seasonal declines, but is still up 5.2% year-over-year and 2.6% above the peak of Housing Bubble 1 in July 2007. From that peak, the index plunged 37%. It’s now up 70% since February 2012:

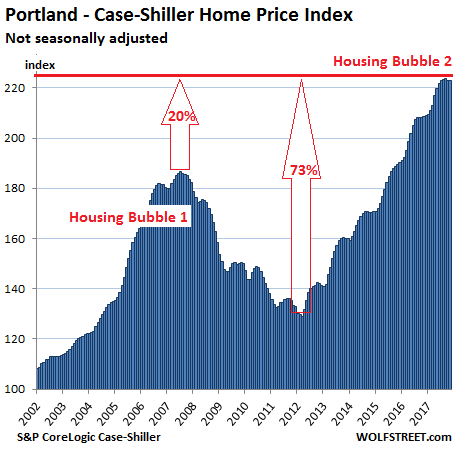

Portland:

The Case-Shiller index for Portland was flat in November, and has now been flat or slightly down for five months in a row, and for now still in the range of normal seasonal patterns. The index is up 6.9% year-over-year and has skyrocketed 73% in five years. It’s 20% above the crazy peak of Housing Bubble 1 and has ballooned 123% since 2000:

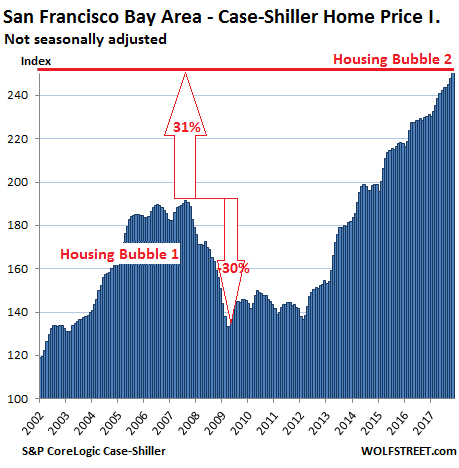

San Francisco Bay Area:

The index for “San Francisco” covers the county of San Francisco plus four other Bay Area counties — Alameda, Contra Costa, Marin, and San Mateo (the northern part of Silicon Valley). It jumped 1.4% for the month, after jumping 1.2% in the prior month. It’s up 9.1% year-over-year, up 31.3% from the insane peak of Housing Bubble 1, and up 85% from the end of Housing Bust 1. The index has surged 151% since 2000:

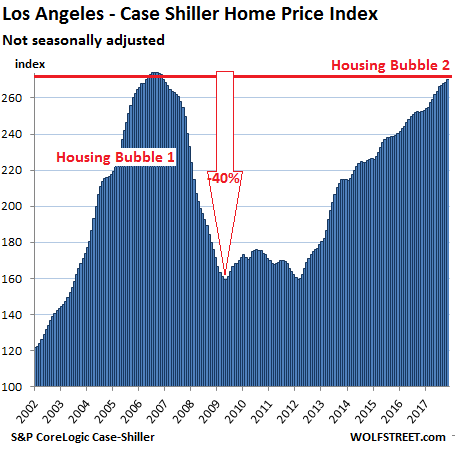

Los Angeles:

Home prices in the Los Angeles metro, as tracked by the index, rose 0.7% for the month, and 7.0% year-over-year. LA’s Housing Bubble 1 was in a category of its own in its steepness on both sides, with home prices skyrocketing 174% from January 2000 to July 2006, before collapsing and surrendering much of the gains. The index has skyrocketed since Housing Bust 1 and is now within a smidgen of the prior insane peak:

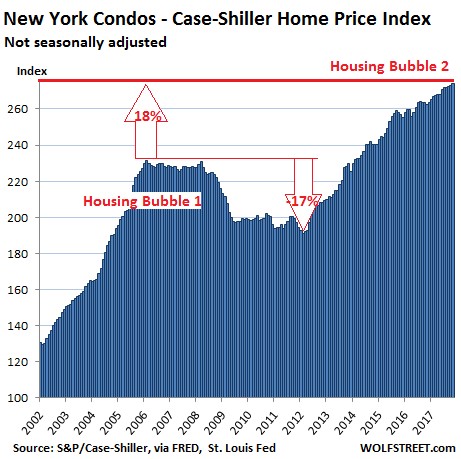

New York City Condos:

Case-Shiller has a special index for New York City’s condo because this is such a vast market. And this index rose another notch in November and is up 4.4% year-over-year. The index soared 131% from 2000 to February 2006 during Housing Bubble 1, barely deflated during the bust before QE unleashed money from around the world which then re-floated Wall Street more than anything else. The index is 18% above the peak of Condo Bubble 1 and has nearly tripled over the past 17 years:

This is asset-price inflation at work — now that “homes” have become a global asset class. These homes didn’t get 50% bigger or 50% nicer over the past few years. Instead the purchasing power of the dollar with regards to these assets has been purposefully demolished by the Fed’s monetary policies that resulted in practically no wage inflation, moderate consumer price inflation, but massive asset-price inflation. Asset-price inflation without corresponding wage inflation means that the value of labor (wages earned) with regards to homes and other assets has been crushed — a phenomenon now hypocritically called the “affordability crisis” in many big urban areas in the US.

What are the averages hiding? Read… What Does it Mean, Saving Rate drops to 12-Year Low when 50% of Americans Don’t Have Savings?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Moving out of Boston this month because of the housing bubble. No way any of us in a younger generation could ever own a house here so no sense in making life harder for yourself trying. Maybe I’ll come back after it crashes

that’s how I feel about Denver. For most of my life, a decent house there was 150-300k. 300k gets you a crapshack at the moment….riding it out in Pueblo, CO till then.

We bought in Denver in 2011. Now, similar places in our neighborhood are selling for more than double. We think about selling all the time. But, where do we go?

What if I told you that you could sell, take your equity, invest that equity and rent? I wish I had your problem.

Why buy it when you can rent it for half the monthly cost? Buy later after prices crater for 75% less.

Wow. The “home” as a global asset class. That says it all. Thanks, Greenspan Benanke Yellen for the big spoonful of financial repression.

This is actually quite old actually.

Investing in land or in “bricks” aka houses to sell them later is a very old business. At least it became common about two centuries ago.

What’s new is the bubbles.

Before you had to wait like ten years to be able to sell what you bought at a good price. Let’s say you bought land because you knew the town or city was gonna expand or because the railway was eventually pass over there and so on.

GLOBAL asset class

Raxidian. Good points. Seems to me that a lot of the bubble mentality in housing started when boomer’s parents began down-sizing and selling their homes for multiples of original prices. Younger folks were dazzled by the gains in value of these homes. The catch was that people had lived 30 years or more in these houses, raised families in them and let’s not forget replacing roofing, HVAC, painting and other routine maintenance. But folks wanted the same monetary gains in 5 years. Bubble time.

I had neighbors in Costa Mesa who had lived a while and seen a lot. The Mr. served in the Navy in D-Day and the Mrs. told me about growing up in the 1930s; her father repaired train cars and they were 7th Day Adventists and fed people even poorer then themselves. The Mr’s father was a literal Beverly Hills cop.

Anyway, they’d seen RE boom and crash a lot, but said “your house is a place to live, not an investment”. To them, this idea of making money in real estate, assuming it’d go up and up, was new, strange, and wrong.

Of course you could always “make money in real estate”, you’d buy up houses and rent them out, for instance. But it wasn’t as good as US Savings Bonds (War Bonds) etc.

…. ahhh … but what is not mentioned is the fact that the loverly ‘ so called ‘ tax reform is now making things even more interesting when it comes to the real estate Bubble Bubble Toil & Trouble and its potential bursting in air .

Hmmmm ………..

Wolf, excellent article but why make a distinction between housing (asset) inflation and consumer inflation? People who are paying rent don’t view their living quarters as an asset but probably their largest expense. Your unwavering belief in government statistics is admirable, but there are many people who are paying for health insurance, college tuition, utilities, quality food, longer commutes and countless other items who would have a different view about “moderate consumer price inflation.”

It may be unfair to blame all this on the Federal Reserve, but at a minimum, they’ve transferred a fantastic amount of wealth to the top while unleashing vicious housing inflation on renters, first-time homebuyers, kids trying to get out of the parents’ basement and a significant number of low-income folks who are getting battered by higher property taxes (and even forced out of their homes in some cases). It’s unfortunate that the Fed is not being held accountable for this and are even getting away with the absurd idea that the problem with the economy is that there is not enough inflation.

Let property go to zero, I could put the property tax relief to much better use.

The REIT boys are lining up another harvest of foreclosures. Another consolidation of wealth by the 5% who can borrow billions at near zero rates.

Banks create new money out of thin air when they create a loan. And they prefer to lend that money against real assets, because they will always have value if they need to repossess it. Whenever you deregulate banks, you’re going to end up with this kind of bubble. The solution is to get rid of the concept of “free markets” when it comes to banks. Banks must be brought to heal or they will make debt slaves of everyone.

The free market works across the board as long as the losers (and especially the criminals) don’t get bailed out.

So that I don’t get a reputation as a grammar nazi – I like your pun – “brought to heal” :)

Anyway, good point about lending against an asset whose value can be confidently assessed. Unfortunately, it means banks are most willing to lend in an industry where innovation and thus gains to be had are the least. So they get the privileged position of creating money, but do not finance the sectors that will benefit humanity – science, technology, medicine, etc.

The asset value of a home can be confidently (accurately) assessed on an individual basis, but when 1,000 to 3,000 mortgages are packaged up and sold, that accuracy is not the same.

How many trillions of dollars in residential MBS are out there?

Mortgage pools used to be very carefully constructed. They pooled mortgages from the same zip code, same asset value or mortgage amount, etc. They only bought mortgages that fit the criteria they were looking for. Now heaven only knows what they do.

Or maybe said another way, why abandon the concept of free markets when the currency should not be the monopoly of a private banking cartel?

“Give me control of a nation’s money and I care not who makes it’s laws” — maxim widely attributed to the House of Rothschild (but more likely hard money advocate T. Cushing Daniel)

Banks “create value out of thin air” just to control people, make sure they do something (have jobs) that keeps them motivated to live … the American dream, some kind of artificial symbol of achievement …. It’s all about controlling the majority of otherwise stupid people or herds of sheep with a human face and a brain of a cat :) It’s been like this for centuries, will always be like this. Form might be different, but substance will stay the same … Good luck, PEOPLE!

Banks “create value out of thin air” just to control people, make sure they do something (have jobs) that keeps them motivated to live … the American dream, some kind of artificial symbol of achievement …. It’s all about controlling the majority of otherwise stupid people or herds of sheep with a human face and a brain of a cat :)

Yeah Kent it’s just terrible that these banks actually lend money to people. Something needs to be done about that.

Every time I go into a bank I see people lined up with guns to their heads being forced to take out property loans . Then when I go to car dealerships I see all these people with guns to their heads again being forced to take out tens of thousands in auto loans. Then when I go shopping at the mall there are all these people with guns at their heads again being forced to buy stuff with their credit cards. It’s just so terrible.

It’s also just so shocking that banks secure their RE loans with the actual real estate Kent because if your were lending thousands of dollars of your own money you would much prefer to loan it totally unsecured would you not?. Further, if you had $100000 in the bank Kent you would much prefer that the bank not secure the loans it is making with the deposits you are lending them. I bet you run a really profitable business for a living.

Yep bubbles have nothing to do with demand and speculation do they? The last economic crisis and RE bubble was not caused in large part by massive numbers of idiots who took out loans they could never afford to pay back was it? Not to mention all the gullible speculators. Now we have a brand new set of idiots who have taken out loans that they will not be able to service when the much loved by all, insanely low, artificially suppressed interest rates we have now inevitably go up. Lets not get into the subject of auto loans on what are heavily depreciating consumer items. Buying something for tens of thousands that loses at least half it’s new retail value in 3 years and taking on a loan to do it is financial madness but try telling that to the idiot masses who always want to buy what they cannot afford. But hey, it’s all the fault of “someone else” because the world has all these banker people with AK47s leveled at the consumers’ heads forcing them to take out loans to buy stuff.

Strong demand always causes prices to rise on items in limited supply. Quality RE is in limited supply in the areas where most people want to live and no one is making more land. When you increase the population by natural growth and by immigration you increase demand. All these new people have to live somewhere, they all want to live where services are the best and where the jobs are more plentiful and if they don’t buy they have to rent or live in a tent. You also increase demand when non residents are buying your local RE and they are going to buy in the areas where most people want to live – not in crap areas.

All businesses clamour for a substantial ever increasing population regardless of the downsides which they could care less about. The more people, every year to infinity, the better. More people = more consumers = more sales = more profit opportunity.

US Population

1980 226.5 million

1990 248.7 million

2016 324 million est.

If you want to stem excessive inflation in RE prices then don’t blame the banks. Do something about your levels of immigration (which is a controllable factor) so that you limit total market demand increases. But in truth that is just not going to happen for a whole range of reasons, especially political drivers. Try ever having a rational discussion about immigration numbers in any western country.

So look forward to more price inflation in housing stock over the longer term and increases in rents. Housing in those areas where most people want to live and work will become less and less affordable as time goes on because the perpetual increasing demand will see to that.

But you can all stick your heads in the sand and blame the banks or perhaps just blame Donald Trump because surely he is responsible for every major problem the USA has ever experienced in the past two decades because he has been President for a year.

Learn how money is created, and then talk. It is lent into existence. That’s why a bank can lend more than has been deposited at that bank.

Fools think banks only lend out depositors’ deposits.

Fools think inflation is due to illegal immigration.

Fools think rising prices are due only to increasing demand rather than ongoing currency devaluation.

ZeroBrain, you’re correct, though no one could blame people from not understanding your point. If you look at a chart of US prices going back to the 1700’s or 1800’s, you will find that every great inflation in American history occurred around the time of a war, when the government suspended convertibility to gold, and printed with abandon. Nothing looks like the price level on the chart since the U.S. “temporarily“ abandoned the gold standard under Nixon in 1971.

Even under a gold standard, though, there have been price bubbles. Where there is irrational demand, people will find the way to speculate, and drive prices ever higher, until people realize that they have paid too much.

Supply and demand obviously play their part, but things could not get so out of control with a gold standard.

Your entire comment would hold some validity if they were lending their own money. We wouldn’t have this problem if we were on a gold standard and they only lent out their own gold. And not the gold of their depositors. But alas…

and even more validity if they ate the losses. and its not just rates its LTVs and DSCRs and perhaps most overlooked – recourse provisions.

And this is the biggest failure of the Obama administration (and why we have Trump now). When he was elected the first order of business was for him to have an FDR moment and fire the CEO’s of the financial institutions which caused the great recession, implement strict controls on Wall St, bring back some form of Glass-Steagal. Then focus the work of the government on helping the everyday man regain the ability to earn an honest living.

Instead we got more bail outs for Wall St, record bonuses for Wall St, no meaningful regulation of Wall St, the codification of too big to fail, easy money policies which caused massive inflation on everyday needs of regular people, the hollowing out of middle america so Wall St could thrive, the transference of wealth to the 1% and the complete crapification of the job market.

Obama seems like a nice guy (to critique him sacrilegious) especially compared to Trump. In the end he proved himself to be just another politician who was bought by Wall St long before he was sworn in. The people sensed this and were pissed off, hence Trumps false populism won the day.

But yes, the banks and Wall St must be brought to heel…….. just don’t hold your breath waiting for it.

well stated Kent

C’mon Housing Bubble 2.0…Pop! Pop! Pop!

Got my savings ready…

These charts indicate that there was plenty of time to see the last downturn coming – prices had fallen quite a lot in the expensive markets before the equity markets really began to crash. Even with the 3 month (?) delay in Case Schiller data, there was enough notice. Hopefully history repeats in that respect.

Yes, but when everyone sees the same signs, many folks are trying to sell even while buyers, who also see the signs, evaporate. The housing market is only liquid on the way up. On the way down, it becomes dreadfully illiquid.

Certainly. I wasn’t clear – I meant equities: shorting, buying puts, or getting out at the very least.

An anecdote on the market drying up – my mother’s siblings inherited a house in Oakland, which they sold, chasing the market for several months on the way down. They were initially upset about having to lower the price, but eventually relieved as prices continued tanking long after they sold.

It’s worse than the article states. Federal Reserve data shows that homeownership rates have done nothing but decline, as has median take home income. What’s driving it? ZIRP? Nah…

“The housing market is only liquid on the way up. On the way down, it becomes dreadfully illiquid.”

Excellent point and THAT will be the biggest tell when Bubble 2.0 is getting ready to blow.

Sonoma County is a special case due to the loss of housing stock in the fires.

Sophisticated investors are betting on a roughly 20% increase in prices between September 2017 and August/September 2018 when they can reasonably expect to have completed homes to sell based on the prices they are Tpaying for cleared lots and smoke damaged homes in good neighborhoods ( Not Founaingrove).

I base ha statement on two of my own transactions, conversations with other Realtors and conversations with buyers.

Where the money will come from to buy these homes is another matter.

Most likely correct. Look at the lower Florida Keys after the hurricane. Up at least 20%.

And to think the NPR program Marketplace said that ‘Janet Yellen was right’ for essentially unleashing massive amounts of QE or money printing. Despicable, disgraceful and bias journalism.

Case-shiller is a lagging indicator. We will reach the price inflection point well before the index reports the change in direction. November may have been the pivot point. In my home town of Fremont we have seen two months of decline in median asking prices since November. One more and I will call it a trend in the right direction.

The true value of a house is the price of the land added to the cost od building it. Fine-tuning is necessary based on the expected amount of property tax vs. job opportunities in the area.

Much of the rest is speculation, based onoptimistic and quite broke borrowers believing in variable interest rates in mortgages.

Our friends recently sold their house in Burlington, near Toronto that they paid 640,000 for 3 years ago, for 990,000. The buyers now are trying to get out of the deal 2 months later. The sale had a long closing. The agents have their commission, and the lawyers are salivating. Our friends are not happy.

I find your comment perplexing. I am neither a lawyer nor Canadian, but if the sale has closed (i.e., everyone has signed deeds and such), then how can the buyers back out? The deed (no pun intended) is done.

Conversely, if the sale has not closed, by what means (logical or legal) can the sellers force the buyers to go through with it? In the U.S., anyway, that’s not how any of that works.

As far as I know, a buyer can back out if something bad shows up in an inspection, usually without penalty. If they just change their minds after they’ve signed an agreement to buy, they may lose their deposit or downpayment, but there’s nothing a seller can do AFAIK to force an unwilling buyer to buy.

Likewise, why are the lawyers “salivating”? Assuming the sale hasn’t closed, your friends keep the buyers’ deposit. The buyers walk away. There’s nothing to litigate. This all should have been spelled out in the agreement to buy. If there’s anything to take more than an hour of paperwork on a lawyer’s part, somebody messed up writing the agreement.

All from my non-Canadian, non-lawyer perspective, of course.