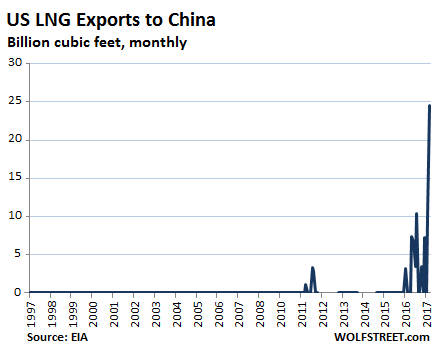

Even China is buying U.S. LNG.

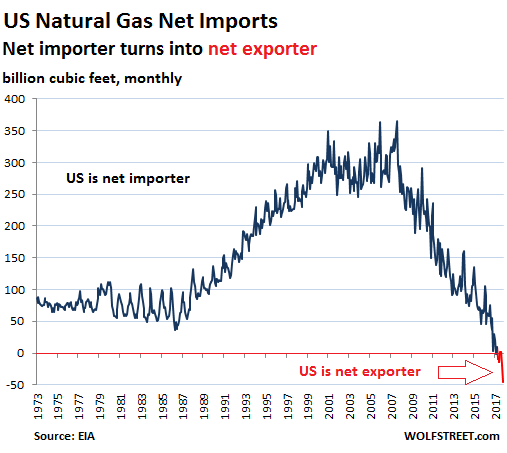

In 2017, the US became a net exporter of natural gas for the first time. It started small in February, when the US exported 1 billion cubic feet more than it imported. By October, the last month for which data from the Energy Department’s EIA is available, net exports surged to 45 billion cubic feet. For the first 10 months of 2017, the US exported 86 billion cubic feet more than it imported. And this is just the beginning.

Exports to Mexico via pipeline have been rising for years as more pipelines have entered service and as Mexican power generators are switching from burning oil that could be sold in the global markets to burning cheap US natural gas. The US imports no natural gas from Mexico.

Imports from and exports to Canada have both declined since 2007, with the US continuing to import more natural gas from Canada than it exports to Canada.

What is new is the surging export of liquefied natural gas (LNG) by sea to other parts of the world.

This chart shows net imports (imports minus exports) of US natural gas. Negative “net imports” (red) mean that the US exports more than it imports:

The first major LNG export terminal in the Lower 48 – Cheniere Energy’s Sabine Pass terminal in Cameron Parish, Louisiana – began commercial deliveries in early 2016 when the liquefaction unit “Train 1” entered service. Trains 2 and 3 followed. The three trains have a capacity of just over 2 billion cubic feet per day (Bcf/d). In October 2017, the company announced that Train 4, with a capacity of 0.7 Bcf/d, was substantially completed and is likely to begin commercial deliveries in March 2018. Train 5 is under construction and is expected to be completed in August 2019. The company is now lining up contracts and financing for Train 6. All six trains combined will have a capacity of 4.2 Bcf/d.

This is just the Sabine Pass export terminal. In addition, there are five other LNG export terminals under construction, according to the Federal Energy Regulatory Commission (FERC), with a combined capacity of 7.5 Bcf/d. This brings total LNG export capacity to over 11 Bcf/d over the next few years and will make the US the third largest LNG exporter globally, behind Australia and Qatar.

In addition, there are several other export terminals that FERC has approved but construction has not yet started. And other projects are in the works but have not yet been approved.

According to the Institute of Energy Research, global LNG demand is currently around 37 Bcf per day. This is expected to grow substantially as China is shifting part of its power generation capacity from coal to natural gas. And US LNG exports to China have surged from nothing two years ago to 25.6 billion cubic feet in October (for the month, not per day):

US natural gas production has been booming since 2009 as fracking in prolific shale plays took off, and the price has collapsed – it currently is below $3 per million British thermal units (mmBtu) at the NYMEX, despite tthe majestic cold wave that is gripping a big part of the country.

Exporting large quantities of LNG is a momentous shift for the US because it connects previously landlocked US production to the rest of the world. Unlike oil, the US natural gas market has largely been isolated from global pricing.

This caused some immense price differences between the US market — where a gas “glut” crushed prices, pushing them from time to time even below $2/mmBtu — and, for example, the Japanese LNG import market, with prices that were in the $16-$17/mmBtu range in 2013 and 2014. Even the average spot price contracted in November 2017, the most recent data made available by the Ministry of Economy, Trade and Industry, was $9/mmBtu. US LNG exporters hope to arbitrage these price differentials.

Meanwhile, US producers are hoping that this overseas demand will mop up the glut in the US and allow them to finally boost prices, including the prices LNG exporters pay. But funding continues pouring into the oil and gas sector to pump up production, and prices have remained low, and drillers continue to bleed.

And there are already global consequences – including in Europe, where large regions, including Germany, increasingly depend on natural gas from Russia as production in Europe is declining. The new competition from the US – though it really hasn’t started in earnest yet since most of US LNG goes to places other than Europe at the moment – is already reverberating through the Europe-Russia natural gas trade. Read… Russia’s grip on European gas markets is tightening

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The cold weather basically just started. It won’t have much impact yet. I read OPEC expects shale to peak around 2025 and others have said as early as 2020. Is it safe to say long-term natural gas prices are going through the roof?

I remember in July 2008 a certain well known investment guru was pitching oil at $150/bbl for Christmas with a “high chance” of $200/bbl by Christmas 2010.

I know at least a couple of persons who fell for it and lost quite a bit of money and heard of others who lost their shirts on this gamble.

Morale: be very very careful when trading and speculating in commodities because, differently from selected stocks and bonds, there’s no central bank safety net underneath.

I am a bit out of touch with the numbers but say 2 years ago 120mtpa of LNG liquefaction capacity had been built but only 50mtpa of regasification.

The market was only expected to go to a suppliers market in 2020-2022 period based on expected new regassification facilities.

Projects like Gorgon in Australia have been $50bn economic disasters. Gorgon needed something like $15/mmbtu to work financially and around $5-6 just to operate cash flow neutral.

At the end of 2017 global liquefaction capacity was 340 Mt while glocal regasification capacity stood at 795 Mt. As it can be well imagined the bulk of liquefaction capacity is located in the Middle East, followed by Asia (Malaysia and Indonesia are major LNG exporters) and Australia.

The US have a huge liquefaction/regasification imbalance however which reflects decades of massive LNG imports from abroad: as US NG production is estimated to go even higher, expect liquefaction capacity to increase fast so as to allow US NG producers to get rid of their increasing surpluses.

Where those surpluses are going to end is a great question. The traditional oil and gas sinks are Japan and Europe, but the problem is US producers aren’t the only one eyeing those two gas sinks to dump their surpluses.

Liquefaction capacity is coming online fast in Qatar, Iran, Egypt, Nigeria etc. Even Russia is jumping on the LNG bandwagon.

To this it must be added that while commodity prices aren’t exactly depressed, prices have come down a long way since 2013 in absolute terms, let alone inflation adjusted ones.

All at a time when investments are going up (see how LNG carriers have started to get bigger and bigger after decades of being stuck around 120,000 m³) and, hopefully, monetary conditions are tightening.

Yes MCO1: Russia signed a 30 year NG contract worth 400 billion US in 2014 /05 with China. ( http://www.laboratoryequipment.com/news204/05 china.)

https://oilprice.com/Energy/Gas-Prices/LNG-Bust-Could-Last-For-Years.html

So the problem is a supply surplus and maybe regas cap in wrong places.

Decades ago NatGas was flared when new “Oil” wells were drilled. It still is, a bit. It must have been of no use. I remember the pictures and videos I saw with the immense fire atop the well, in the USA and in the M.E.

Wow, what farsighted planning and action !

https://www.nature.com/news/flaring-wastes-3-5-of-world-s-natural-gas-1.19141

Now, at some significant overhead cost, we export NatGas instead of saving it for a colder future.

No, we will never run out of NatGas. But it will get more expensive to produce, store and transport.

The day will come when exporting NatGas is understood as being as foolish as flaring it atop new oil wells.

10 years ? 20 years ? Can’t say there are too many factors to consider. Sooner than we want is all I will predict.

Damn, Humanity, especially American humans are terminally stupid.

They flare natural gas where there are no pipelines to it take it away. Pipelines are expensive, and natural gas is cheap, so when you’re drilling for oil, and that’s the primary hydrocarbon coming out of the ground, gas pipelines might not get built.

Flaring should no longer be necessary, if there was widespread adaption of the technology developed at Mango Materials in Albany CA:

http://mangomaterials.com/technology/

Why this company has not gone “full bore” with this ‘breakthrough’ is beyond me. I wrote them, and yes, you could, actually, produce ‘plastic firewood’ and give that to people for cooking, to halt deforestation and carbon-sooty burning. Energy-wise, it works, they say.

Oh, good. So I can expect my electric bill to go up over the next few years?

yes

@Kent,

Yes you can expect much higher prices, as all energy costs will be going up over time.

Right now, US is just starting to be a net exporter of NG. As Shale production declines going forward, this is unlikely to continue.

Energy is a global product and will reflect world prices in all markets unless artificially restrained by legislation or lack of exporting infrastructure. Look at how well countries do who artificially keep energy prices low; Venezuela, Egypt, Saudi Arabia, Mexico… :-)

Long term, all energy costs will be going up for all of us as consumption of petroleum is 10X the rate of new discoveries. Energy is energy, and a shortage of transportation energy will bleed into other forms, plus, a large part of current US petroleum is also NG liquids and bio-fuels. Once again, when the Shale investment frenzy ends the surplus in NG by-products wil decline.

Unless, of course, direct tax dollars are be used for energy production to keep industries fueled. And that isn’t likely, either. :-)

We have a window to increase our use of renewables before the depletion bite hurts and strangles our industrial economies. Not that renewables is the answer for base load, nevertheless, it will help and it could allow for a more sane production of fossil fuels and help with AGW. But, that would be ‘supply management’ and that isn’t likely, either. No let Mr. Market do the managing as we lurch into one crisis after another and ask Central Banks to fix everything.

NG production has only surged due to unrealistic investments in Shale. This has occured due to the low interest rate environment lulling gullible investors chasing yield. NG producers have been going broke for years, and Shale is secretly doing so. Regardless, the copious amount of NG in the North American market is one by-product in the quest for tight oil, unless of course, Trump encourages renewed flaring which had been outlawed by many States this last decade. But, you still have to get the product to market in order to sell it and since Shale wells are 80% depleted within 3 years that isn’t likely, either. As for temporary and small scale power plants that will produce electricity from NG flaring, the lack of powerline infrastructure will also make this uneconomical.

I repeat, once the Shale investment bonanza recedes with higher interest rates, excess NG supplies will start to decline and prices will rise.

I live in a country that is actually a net exporter of energy and our domestic price for oil is considerably higher than the US price simply due to taxation. I pay $4.88 CDN per US gallon of reg. gas which is about $3.90 US. It is also expensive to heat homes with NG and Electricity even though my Province is a net exporter of both of those as well.

I spent several thousand dollars over the last 10 years super-insulating our home and upgrading all windows. I think the current cold snap is a good reminder for people that this is probably the wisest energy plan for households going forward.

regards

Google has funded a company Dandelion Energy that is attempting to bring widespread use of heat pumps and thermal energy from the earth, as a substitute for burning fossil fuels. As with wind energy, you start, and ten years later, you actually have a viable competitive product.

But, must start with a deep pocket funder.

“NG production has only surged due to unrealistic investments in Shale. This has occured due to the low interest rate environment lulling gullible investors chasing yield. NG producers have been going broke for years, and Shale is secretly doing so.”

Secretly? Right.

And water and food to cost more as fracking destroys our aquifers.

Can you post to studies which show such destruction??

Yes Todd, we will just bend to your whims rather than all the science out there for anyone to see, just because your trolling is so effective.

The graphs made me wonder about the resulting impact on coal production, transportation and consumption and how that would play out in terms of pollutants. There is some reasonable notion that natural gas is slightly less harmful to the air, although water and soil impacts, especially depending on the mode of production, might have layers of concern over long horizons.

Do readers know if there is some type of consolidated net carbon or similar footprint or impact comparison or graph available? I’m looking for whatever good news there may be, even prior to looking at geo-political ripples through lower reliance on OPEC.

“Carbon Footprint” is propaganda. There isn’t one.

There IS a carbon DIOXIDE footprint; it’s plant food

That is the worst type of simplified misdirection, the old “plant food” idea. Statistics do not bear this out: otherwise, every power plant would be surrounded by green houses, and bumper crops of “plant food” products would abound.

So nuts, that people sit on the sidelines, and toss out already-investigated stuff, such as “plant food”.

Chemical reactions run faster when the concentration of reagents is higher, so the small increase in CO2 lead to photosynthesis running slightly faster, up to some concentration limit. In geological times, the concentration of CO2 was higher and decreasing (as evidenced by air samples from e.g. Antarctic ice), due to it being tied by plant matter in fossil fuels. It took the emergence of “intelligent” species to reverse the trend.

It’s interesting to note that ice and CO2 existed simultaneously at higher concentrations, thanks. So the oceans obviously were more acidic at the time as a result.

Although, I have concerns regarding the receding of glaciers, seems humans may have to obtain water elsewhere, not to mention wildlife. Of note: I’ve heard recently of some forecasting a wetter climate in parts of Africa, going forward.

It sure wouldn’t be a surprise if special interest groups were to attempt benefiting from creating hype and panic leading to legislated advantages.

Oh, dear-poor RD. Fell asleep during junior High school science, did you?

I don’t know what the truth is.

https://journal-neo.org/2017/12/24/a-golden-era-in-eurasia-what-can-americans-learn-from-the-yamal-lng-project/

Yeah, Russia is adding to the coming global LNG export glut, along with everyone else. It has a lot of natural gas and it wants to diversify its customer base away from Europe, where it faces competition from LNG, Norway and other sources. Hence the recent deals with China, hence LNG. Just basic business.

CNG modification is a far more practical solution than the electric car, and CNG has no CAFE standards. It’s already in government and public service vehicles, why it hasn’t been accepted for the general public is a matter of politics. I consider a huge boost to countries like Japan which pay 5X the rates, and Europe which lives under the shadow of Gazprom. Should we ever get back into the Climate change accord exporting LNG to China would be prove to be beneficial. Currently the cost per BTU is about half of that for gasoline. And once LNG gets full marketability the cost should rise more.

For some reason, CNG and propane vehicles have not sold well in the US though they have been available for decades. A lot of times, they were aftermarket installations. Some manufacturers periodically offered factory models, such as the 2016 Ford 150 CNG/Propane. But maybe it flopped. I don’t think Ford built a 2017 F150 CNG/propane version, though there are aftermarkets versions. And I don’t think it has a 2018 CNG model in its lineup.

The failure of CNG autos in the US comes down to one simple factor . An abysmal lack of infrastructure creating a level of inconvenience that utterly overwhelms any benefits that may be had .

Which in fact …. are many .

But on the overall subject of CNG ;

Aint it just a bit odd and ironic in light of the overall tone of this article that CPR ( Colorado Public Radio ) and the Denver Post are both reporting massive scale backs when it comes to new CNG wells and well as many existing wells being placed on hold here in CO ?

I agree, social media’s inability to flush out technical detail highlights it’s value.

I will give you an anecdotal story, first-person, that illustrates the problem with CNG for automobiles. First I should mention that twenty-plus years ago, I spoke with a program director, up in Sacramento for a government meeting, about the Southern Cal Gas Co program with CNG cars. Big funds, big program. Could not get people to take the cars, love or money. Here are the problems, which I experienced first-hand:

(1) range constriction. You cannot find a place to fill up. Very difficult, often on government property, which is closed on weekends. You have to fill every 150 miles or so.

(2) intimidating filling process. The amount of signs and warnings, and pictures of explosions, around the “fuel pump” even intimidated my brother, a long-time welder used to hooking up high pressure oxygen, acetylene, etc. He could not hook up the hose. Too much resistance to clamping in the nozzle. I had to take over, and just shove the damnn connector into place, hard. Meanwhile, it’s December, 6:30 PM Sunday at the San Bernadino County yard, no one around, no help, and not enough fuel in the tank (?? maybe? maybe not?) to get back to Ontario Intl Airport, where I rented this CNG car at a discount. Impossible impossible tension. I missed my flight by ten minutes.

Great comment. The hassles are just too great with CNG. As for CNG potentially replacing diesel, the horsepower needed to move 40 ton OTR trucks is just not there with CNG. Liquified maybe, but not CNG, and LNG creates a whole other set of problems.

“once LNG gets full marketability the cost should rise more.”

Thanks for making that perfectly clear, I feel like I just contracted a brain disease.

Agree totally. Instead of exporting LNG why not convert US cars to run on CNG and LPG? And that`s only for starters. You can add trucks, diesel locomotives and all kinds of “stationary vehicles” (e.g forklifts). Your oil import dependency would vanish like vapour in the sun.

My LPG car (converted) is clean, reliable and saves me about 40% on fuels costs compared to petrol which is about the norm in Europe with about 30k filling stations. Even here in Norway with few filling stations I never worry about “range anxiety” because if need be I can run on petrol or gas as you say.

Natural gas is, in fact, worse for anthropogenic climate destabilisation thanks to the fugitive emissions of methane. Fracked wells will, in many cases, leak methane for decades. Game over, but at least we made a few bucks, and that’s all that counts, isn’t it.

here in citrus county florida duke energy decommissioned their nuke plant to be replace by natgas . https://citrustimesonline.com/duke-energy-breaks-ground-for-natural-gas-plant/2016/03/02/.html

Wolf,

Good article, but a lot more comments need to be made, to complete the connections with other articles and comments on your website about the U.S. oil/gas industry

1. Turning the US into a net exporter of natural gas was entirely the result of the fracking industry (which got considerable criticism and skepticism in one of your other articles)

2. Some projections prior to 2014 had the U.S. also reaching a state of oil independence by 2017 because of fracking. And then the Saudi oil price drop was done specifically at that moment to drive U.S. frackers out of business, as the early costs for extracting oil by fracking required $100/barrel. As I have mentioned in other posts, the Saudi price drop instead forced the U.S. fracking industry to figure out how to lower the costs of production, to as low as $23-25/barrel.

3. The Saudi oil price drop did have some of their intended effect of slowing down the fracking industry in the U.S. quite a bit. In 2014 Shell and Exxon got out of their fracking projects, selling their projects to smaller independents, and shutting down others. Numerous small independent frackers went out of business. This is what prevented the projections of oil independence in the U.S. by 2017 from happening. As the price of oil rose again, after the Saudis decided that their plan was not exactly working, Shell and Exxon have since bought back into the U.S. fracking industry.

4. Natural gas comes out of almost all oil/gas wells. If the oil well produces lots of oil compared to natural gas and whoever owns the oil well has no interest in capturing the natural gas, the gas gets flared off, on site. This happen at oil fields globally, but due to the plethora of drilled wells required for fracking, apparently the U.S. leads the world in the total numbers of gas flares, based on satellite images. Terrible waste of an energy product, while contributing unnecessarily to global warming. (This is also why in countries where natural gas is cheaper and more readily available than coke, like Iran, direct reduction iron production with natural gas has become the #1 method of raw iron production rather than traditional iron smelting with coke).

5. The Obama administration decided in 2015 that what made the most sense was to end the ban on oil exports from the U.S. in return for instituting an Interior Dept. rule to ban natural gas flaring from oil wells by 2019. So that is indeed what happened.

6. Now, in numerous comments on this website, people have sharply criticized exporting oil from the U.S., but it is really important to understand that oil products, e.g., gasoline and lubricants, had NEVER been banned from U.S.export, and as a result, the refineries were profiting handsomely from sales of U.S. refined gasoline, etc. (some of that was done with imported oil!!). The oil industry is no longer vertically integrated, and this is especially true for the refining industry. The major oil production companies like Shell and Exxon and Chevron for various reasons divested almost all of their refining capacity to other companies. Among the two biggest – Valero, and Motiva.

7. It is important to understand that Motiva is a Saudi Arabian company. So really, cool it with this criticism of exporting oil and natural gas from the U.S.! A Saudi Arabian company owns numerous U.S. refineries, and was profiting handsomely from exporting gasoline and lubricants to other countries at a time that the rising oil production in the U.S. by U.S. fracking companies was banned from export!

8. As I have mentioned, the Jones Act, which forces all U.S. shipping BETWEEN U.S. ports to be carried on U.S. flagged and crewed ships, increases costs, and so discourages the shipment by oil tanker of fracked crude oil from U.S. ports, located largely in Texas and Louisiana, to the East and West Coast refineries, which are not connected by crude oil pipelines to this crude oil source. This is why those coastal refineries continued to import foreign oil.

9. The rising stocks of fracked oil in Texas caused the price of this oil to drop, and it really made no sense to force this oil to continue to be sold only to the refineries in Texas and Louisiana that had easy access to this oil. Remember, a number of these refineries were owned by this Saudi Arabian company, which could then sell the refined gasoline and lubricant products at a handsome profit. Mexico, as I mentioned gets 60% of its gasoline from the U.S. now. Getting rid of the Jones Act would have made more terrific economic sense but was politically impossible.

10. Now, back to the 2019 Obama ban of flaring off natural gas at the oil wells. The Trump administration and the Republican Congress have been busy trying to overturn this. Democrats in the Senate introduced a bill in 2017 to formally turn this administrative rule into a law. This is an ongoing topic that has received little attention in the news media. Most recently, in early December 2017, the Trump administration essentially undid this Interior Dept. rule. Banning the flareoff of natural gas from oil wells will capture mass quantities more of natural gas. You can guess what the economic effects will be if natural gas is not allowed to be exported.

11. Natural gas is way cheaper today than using coal for power plants. That has been the #1 reason for the decline of total coal production in the U.S. The Obama administration also tightened air pollution rules on power plants, which increased costs at the coal fired power plants, which further encouraged the power plant industry to shift from coal fired plants to natural gas. The Trump administration has since overturned these air pollution rules, overturned pollution control rules on coal mining, all efforts to reduce the costs of mining and using coal in the U.S. However, this will only serve to increase the profitability of coal mine owners and power plants that still use coal. This will NOT bring those coal mining jobs back, as increased mechanization has been the #1 reason for the decline in the total numbers of coal mining jobs in this country, a decline which started during the Reagan era in the 1980s and continued even during brief boom times in coal production in the early 2000s, when China’s raging economy resulted in the U.S. exporting mass quantities of coal to China. FYI, for all the, unemployed coal country people who voted for Trump.

That was a very informative post.

Personally, I’m against exporting raw oil or NG from the US but I’m not against exporting finished products. At least that way, we maximize the jobs and economic activity that we can extract from these Natural resources within our own country.

Why export crude oil so some other country can create a thousand good paying jobs to refine it?

Similarly, cheap natgas may suck for drillers, but if that leads to cheaper energy for the rest of the country’s industry then on balance, it’s better to keep it here. How Much additional GDP does the US get from having cheap electricity due to cheap natgas vs another country that’s energy starved?

The bottomline is that we’re not like Saudia Arabia who literally has no use for the oil under their ground. We have refining technology, and a massive national economy that can make productive use of that energy. Exporting natgas and thereby raising energy costs for the rest of US industry is being penny wise and pound foolish.

If you ‘maximise economic output’, you destroy the planet’s habitability for our species. But what is that besides lots of lovely money, ever more concentrated in fewer and fewer paws?

The question is: what will happen once cheap-money stops flowing into the fracking industry? Are these exports possible just because shale gas is being subsidized by investors?

Do not fool yourself. US shale gas will never be able to compete with Russian gas, or even that of Qatar or Iran.

“Are these exports possible just because shale gas is being subsidized by investors?”

I thought back in 2010 investors would stop throwing good money after bad. They finally did for a brief period in late 2015 and early 2016, and in no time, some gas drillers went bankrupt, and others (like Chesapeake) threatened a debt restructuring. But then the money gushed back in, and it started all over again. This industry is full of hype and investors continue to believe it.

That said, if the money finally dries up, US natgas prices will rocket higher, thus making it a more profitable business for drillers. Then the question arises if LNG exporters can still make money if they have to pay a lot more for natgas and export as LNG (liquefaction is an expensive process).

Wolf, you are not reading my posts. The frackers went out of business and the majors like Exxon and Shell pulled out of fracking because the Saudis drove down the price of oil by refusing to lower their oil production, starting in late 2014 and continuing through 2015 and 2016. In late 2016, the Saudis got OPEC to agree to production targets which have stabilized oil prices – oil has stayed above $42, and is currently around $60/barrel.

Fracking has picked up again because during the period of severe price drop, when oil went down to below $30/barrel, the inefficient frackers went out of business, and the stronger ones learned how to frack oil at lower cost, $25/barrel and lower.

The fracking boom and bust cycles have nothing to do with a cheap money supply or the stock market asset bubble or any other conspiracy theory. It’s all about the price of oil, versus the cost of production, and always has been. Market forces, in other words

Let me start with where you’re right. You’re right that drillers cut their costs by renegotiating contracts with service companies and suppliers. And some have picked up some assets for cents on the dollar during the bust.

But the overall cost of fracking for natgas still hasn’t come down nearly enough to actually be cash-flow positive at $3/mmBtu. Natgas drillers continue to be cash-flow negative. They continue to bleed. But investors keep feeding them with new money – equity and debt both. Just look at the huge amounts they raised in the second half of 2016 and in 2017. This flow of new money is what makes this work.

And drillers that went bankrupt ended up restructuring. Ownership changed, etc. but they never stopped producing. Your theory that the weak ones died doesn’t apply. The weakest ones are still around. They just buried their old investors and are now funded by new investors.

There is almost no oil in the Marcellus. And natgas production has surged over the past 12 months. This has nothing to do with oil, or the price of oil. This is the most prolific natgas play in the US.

Then there are plays that are mostly liquids, and the associated natgas is the byproduct. If there is natgas takeaway capacity (a pipeline), drillers can sell the gas rather than having to flare it, and this part of natgas production does depend on oil production. If there’s no gas pipeline, they have to flare it.

If you don’t see the connection between production and a constant flow of new investor money, you’re missing the core of the business. This is the Tesla of oil & gas.

Also, if, as the Obama administration regulation to ban flaring of gas at U.S. oilwells by 2019 had been left intact, this would have likely increased costs of oil production/fracking slightly, but would have massively increased the amounts of recovered natural gas, natural gas which is currently being burned off into our atmosphere and adding to global warming. So banning gas flaring at the wellheads would have gone well together with allowing exports of oil and gas. Trump and the Republican Congress are not having any of that, however

Don’t suggest it may be part of a national energy policy to make America self sufficient and to protect our allies from energy blackmail, or to help Japan get off of nuclear energy. Government never does anything right.

i used to go from Bangkok to Cambodia by van and they would stop to refuel the natural gas powered vans at 7/11 ,no big deal , took maybe 10 minutes, enough time to grab a snack and use toilet and it was very popular .Not sure why this never caught on in the U.S. but is so popular elsewhere?

Are you sure these were natural gas and not propane(LPG)?

And yet the US continues to import fuel.

Americans must be crazy!

I guess unprofitable activities can sometimes persist for a long time even in the supposedly bottom line driven private sector. When fracking went through it’s first big expansion I can see that the Ponzi-like aspect would be hidden by rapid growth of the enterprise, but investors should have started to figure this out by now.

Even though money is being lost by investors, overall the fracking boom has been economically positive for the USA. I wonder if somehow government is helping to make this happen?

Sorry Wolf, I did conflate the oil and gas parts of the fracking industry together. The Saudis and OPEC have a lot to do with oil pricing, much less so with gas prices. Both are valuable but not the same markets, kind of like the gold and silver markets. Gas prices are more driven by local country markets. Here’s my understanding of what happened with the gas market:

The rise in gas imports came just as the fracking industry was getting started in the late 1990s. So of course, the early fracked gas wells, and their investors, did quite well with royalty fees, etc. as gas prices were at good levels for profit. Nobody in the early stages of a boom ever goes into a new unproven technology intending to lose money. Well, the usual happened, as people saw how much money was being made, more money entered the gas fracking industry, and as this area tends to be dominated by small independents, which historically have been more prone to hucksters and con men (remember the story of Tony Dorsett), yeah, lots of those are going to be investors left holding the bag. Where the cheap money of today really pumped this possibility for fraud up was because investors started seeking better returns than they could on their tiny bond returns. Venezuela bonds for instance, were also popular for a time because of their 20% interest rates, and lured similar gullible investors. Promised returns from fracked gas wells were often in the 10% or higher range. This produced a massive rise in the production of gas in this country and caused the usual collapse in prices which are now making most gas fracking companies/partnerships/whatever unprofitable although the gas wells themselves are still making money – the discrepancy is likely because everybody with the good clauses in their contracts is sucking out their piece of the pie from the sale of the gas and leaving the shell companies and the gullible investors with the bad clauses in their contracts with nothing but a negative balance sheet.

But, market forces are taking hold. Investment in fracked gas wells has plateaued, i.e., the total amount of gas produced from fracked wells is no longer rising. The market will stabilize. Lots of gullible investors will get fleeced, again.

Gandalf, sounds like you’re a wise wizard on the O&G sector.

Its always interesting to hear from insiders or at least folks with some experience in the field, to get an idea whats going on….at least on a simplistic level.

Not that it really matters since I’m not an oil trader, and I’m betting most folks have no idea how the oil sector functions. Even oil trader “experts” mostly got it wrong…like in the previous oil price crash of 2014. lol.

My question is this:

Why is the US exporting nat gas and then importing it at the same time??

I believe US is now a NET exporter but my take is why the heck do such a roundabout process?

Shouldn’t the US just pump the cheap gas they have for their own domestic use first, and then export whatever excess to other countries, so there is no need for any gas imports in the first place?

Or they could also just store the current excess production like they way they do for their national (emergency) oil reserves. Nat gas have no expiry dates when stored and last practically forever until they are burned during use. So, there is no need for any inventory refresh cycle and very little cost in storage except perhaps insurance for the hazards of any large gas storage facilities.

My understanding too is that nat gas does not require any complicated refining process compared to oil or tar sands. Meaning imported nat gas is pretty much close to the same “stuff” as nat gas extracted from domestic sources, correct? If so, then it makes very little economic and common sense for US to sell their “cheap” gas overseas and then import relatively more expensive gas at the same time.

I can understand Oil is a different story since (for example) Iranians are blessed by God with oil that is mostly better quality “sweet” oil compared to some other countries, and hence it could potentially be cheaper to import or refine etc., so it might make sense to import or even re-export after additional processing.

But Nat gas has nothing to “process”, so there is little basis for comparative advantage and hence trade between nat gas producing countries other than differentials in maybe wages or transportation costs. In fact, it should definitely be cheaper to just extract nat gas from your own domestic country for use after factoring in the cost of shipping from overseas.

Care to enlighten me (and other O&G amateurs) here?

i’m going to bring a series of my Naked Capitalism comments over here, Wolf, since i dont know if you ever see them over there…

first, in re: “the US exported 1 billion cubic feet more than it imported. By October, the last month for which data from the Energy Department’s EIA is available, net exports surged to 45 billion cubic feet. For the first 10 months of 2017, the US exported 86 billion cubic feet more than it imported.”

US gas imports are seasonal. we will likely import more from Canada this January than we export to meet our own needs, and December and February are likely to be close, given colder weather this year (population weighted heating degree days last winter were 17% below normal)

we burned the most natural gas ever on Monday, breaking a record set in 2014.

from my notes on natural gas for the week ending December 23rd:

premiums for LNG in Asia and Europe saw a record spread over the benchmark price for US natural gas as set at the Henry Hub in Louisiana this week…with the price of LNG delivered to Japan, Korea and Malaysia averaging $10.85 per mmBTU early this week, LNG delivered to northeast Asia was $8.11 per mmBTU higher than the US price, while the UK’s natural gas price climbed to as high as $8.83 per mmBTU over the US price…with US natural gas for January delivery hitting a cycle low of $2.598 per mmBTU on Thursday before closing the week at $2.667 per mmBTU, US natural gas suppliers would be in a position to triple what they get from domestic natural gas customers, even after paying for liquefaction and transportation costs, if they could export that gas today…with the weekly Natural Gas Storage Report from the EIA indicating that US natural gas supplies are 5% below their level of the same week of a year ago, our domestic needs are not yet really threatened, but that will certainly be something to watch as the wave of new US LNG export capacity additions starts to come online in the 2nd half of next year..

the point is, our natural gas exporters are contracting to sell natural gas at less than the marginal cost of expanding our own domestic production…the number of drilling rigs targeting natural gas formations fell by 2 rigs to 182 rigs for the week ending December 29th, which was still only 50 more gas rigs than the 132 natural gas rigs that were drilling a year earlier, and way down from the recent high of 1,606 natural gas rigs that were deployed on August 29th, 2008…

if natural gas was profitable to produce at current US prices, drilling for it would be expanding, not sitting close to its all time low..

in line with that, here are the historical US natgas production figures monthly up to October: https://www.eia.gov/dnav/ng/hist/n9070us2m.htm

though they set a record in 2015, the growth pace had slowed…then output was down in 2016 and will be down a bit again in 2017, although the recent months are rising YoY…production will be up in 2018, but not because of natgas drillling…rising oil production from the Permian in west Texas is producing a surplus of natgas as a by-product

Baker Hughes’ count of drilling rigs labeled primarily for natural gas has more than doubled since the natgas bust in mid-2016, from about 84 to 182. And there is a large amount of associated natgas coming from wells that are primarily producing liquids.

Both drilling and production are soaring. Natgas production hit another all-time record in October (last month for which data is available):

https://www.eia.gov/dnav/ng/hist/n9070us2m.htm

Take another look at the chart in the article. Sure there are seasonal fluctuations, but the chart shows the long-term trend of net imports in most dramatic fashion.

The past has shown that fracking for natgas can ramp up so quickly it makes your nose bleed. If the US runs a little short on gas this winter, and prices jump to $4/mmBtu or $6/mmBtu or higher, drillers will hedge at whatever price they can get and then drill like maniacs. Then watch production soar even as the price re-collapses.

And the LNG exporters (along with the pipeline exporters to Mexico) have long-term supply contracts to cover part of their needs and lock in prices. So seasonality will not impact exports. Exports will continue to rise based on the capacity to export. But seasonality will impact consumption, storage levels, prices, and imports from Canada.

The thing that might draw a line through this export trend is the price of natgas in the US over the long term. If investors demand that natgas drillers are cash-flow positive — or else no more money — then all kinds of things are starting to happen that will turn the fracking industry upside down. But that hasn’t happened yet.

i’m not doubting that US exports will continue to increase, probably at a rate in excess of 10% p.a.

nor that our gas production will increase, albeit at a lower rate…

but since domestic consumption will increase at a greater rate due to the coal to gas utility conversions and an eventual return to normal weather compared to the last two years, our demand will outrun our supply, and domestic prices will spike…

at that point we’ll be stuck selling natural gas to china and europe at the low prices we contracted to sell it for today, and paying much higher prices for the new gas for our own use that will be supplied with the ramp up in drilling in response to those higher prices…

today’s Natural Gas Storage Report… http://ir.eia.gov/ngs/ngs.html

Summary:

Working gas in storage was 2,767 Bcf as of Friday, January 5, 2018, according to EIA estimates. This represents a net decrease of 359 Bcf from the previous week.

8 more weeks like that, and the USA is totally out of natural gas…

Eight more weeks of that kind of weather, and the US is going to have a much bigger problem.